Financial Analysis of Britvic Plc and Nichols Plc Comparison

VerifiedAdded on 2023/01/18

|26

|5258

|35

Report

AI Summary

This report presents a detailed financial analysis of Britvic Plc, a UK-based soft drink company, and compares its performance to its competitor, Nichols Plc. The analysis includes an executive summary, an introduction to Britvic Plc's operations and financial performance, and a comprehensive ratio analysis covering liquidity, activity, debt, and profitability ratios for both companies. The report evaluates Britvic Plc's working capital management and assesses a proposed project, considering various scenarios and funding options. It identifies project risks, critically discusses the methodologies employed, and concludes with a final recommendation. The financial data and ratios are used to evaluate the company's performance over a period of time. The report also explores the financial health of the company by evaluating ratios for both the companies and the market share of the companies.

Running head: ACCOUNTING AND MANAGERIAL FINANCE

Accounting and managerial finance

Name of the project

Name of the university

Student ID

Author note

Accounting and managerial finance

Name of the project

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND MANAGERIAL FINANCE

Table of Contents

1. Executive summary..................................................................................................................2

2. Rational of the project..............................................................................................................3

Question 1........................................................................................................................................3

Requirement (a)...........................................................................................................................3

3. Ratio analysis...........................................................................................................................4

Requirement (b)...........................................................................................................................4

Requirement (c).........................................................................................................................10

Requirement (d).........................................................................................................................11

4. Project financials....................................................................................................................14

Question 2......................................................................................................................................14

Requirement (a).........................................................................................................................14

Requirement (b).........................................................................................................................17

Requirement (c).........................................................................................................................19

5. Project risks............................................................................................................................21

6. Critical discussion of the methods..........................................................................................21

Requirement (d).........................................................................................................................21

7. Final recommendation............................................................................................................22

Reference.......................................................................................................................................23

Table of Contents

1. Executive summary..................................................................................................................2

2. Rational of the project..............................................................................................................3

Question 1........................................................................................................................................3

Requirement (a)...........................................................................................................................3

3. Ratio analysis...........................................................................................................................4

Requirement (b)...........................................................................................................................4

Requirement (c).........................................................................................................................10

Requirement (d).........................................................................................................................11

4. Project financials....................................................................................................................14

Question 2......................................................................................................................................14

Requirement (a).........................................................................................................................14

Requirement (b).........................................................................................................................17

Requirement (c).........................................................................................................................19

5. Project risks............................................................................................................................21

6. Critical discussion of the methods..........................................................................................21

Requirement (d).........................................................................................................................21

7. Final recommendation............................................................................................................22

Reference.......................................................................................................................................23

2ACCOUNTING AND MANAGERIAL FINANCE

1. Executive summary

Question one of the tasks is to carry out detailed financial analysis of Britvic Plc using the

financial key ratios and analysing the financial statements of the entity. The report will further,

compare the performance of the company against its main competitor Nichols Plc which is the

supplier of soft drinks to the catering, wholesale, retail, licensed and leisure industries in UK.

The report will focus on critical evaluation of Britvic Plc and will analyse its working capital

management. Question 2 will analyse the project that is intended to be carry out by the company

and taking into consideration various scenarios presentation will be prepared to the investment

board regarding the acceptability of the project. Recommendation will be provided taking into

consideration different funding choice and other information provided in the question.

1. Executive summary

Question one of the tasks is to carry out detailed financial analysis of Britvic Plc using the

financial key ratios and analysing the financial statements of the entity. The report will further,

compare the performance of the company against its main competitor Nichols Plc which is the

supplier of soft drinks to the catering, wholesale, retail, licensed and leisure industries in UK.

The report will focus on critical evaluation of Britvic Plc and will analyse its working capital

management. Question 2 will analyse the project that is intended to be carry out by the company

and taking into consideration various scenarios presentation will be prepared to the investment

board regarding the acceptability of the project. Recommendation will be provided taking into

consideration different funding choice and other information provided in the question.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND MANAGERIAL FINANCE

2. Rational of the project

Question 1

Requirement (a)

Introduction

Britvic Plc which is the soft drink company is UK based entity. It operates in soft drink

manufacturing and distribution industry and operates through 6 segments including GB carbs,

GB stills, France, Brazil, Ireland and International. Across the 4 markets the entity has developed

the strong portfolio of own iconic brands including Tango, Robinsons, J2O, MiWadi, Teisseire,

Maguary, Fruite and DaFruta. Apart from that, In Ireland and GB it sells and produces various

soft drinks for famous soft drink company PepsiCo including 7UP, Pepsi, Mountain Dew and

SoBe under the exclusive agreement with PepsiCo. It is the largest supplier for branded soft

drinks and number 2 suppliers for branded carbonated soft drinks in GB and is the industry

leader in France and Ireland (Britvic.com 2019).

Looking into the financial performance of the entity for the last 5 years it can be

identified that the revenues as well as the net profit margin of the entity are in increasing trend.

Further, the entity is regular paying dividend the payment of dividend for the last 5 years is in

increasing trend. However, it has been observed that apart from the cost of sales, selling and

distribution expenses is one of the major expenses for the entity and the entity is spending

considerable amount in this head (Britvic.com 2019). Looking into the balance sheet of the entity

it can be identified that current ratio of the company has been reduced after the year 2015 as the

liabilities started increasing as compared to the current assets. However, the leverage position of

2. Rational of the project

Question 1

Requirement (a)

Introduction

Britvic Plc which is the soft drink company is UK based entity. It operates in soft drink

manufacturing and distribution industry and operates through 6 segments including GB carbs,

GB stills, France, Brazil, Ireland and International. Across the 4 markets the entity has developed

the strong portfolio of own iconic brands including Tango, Robinsons, J2O, MiWadi, Teisseire,

Maguary, Fruite and DaFruta. Apart from that, In Ireland and GB it sells and produces various

soft drinks for famous soft drink company PepsiCo including 7UP, Pepsi, Mountain Dew and

SoBe under the exclusive agreement with PepsiCo. It is the largest supplier for branded soft

drinks and number 2 suppliers for branded carbonated soft drinks in GB and is the industry

leader in France and Ireland (Britvic.com 2019).

Looking into the financial performance of the entity for the last 5 years it can be

identified that the revenues as well as the net profit margin of the entity are in increasing trend.

Further, the entity is regular paying dividend the payment of dividend for the last 5 years is in

increasing trend. However, it has been observed that apart from the cost of sales, selling and

distribution expenses is one of the major expenses for the entity and the entity is spending

considerable amount in this head (Britvic.com 2019). Looking into the balance sheet of the entity

it can be identified that current ratio of the company has been reduced after the year 2015 as the

liabilities started increasing as compared to the current assets. However, the leverage position of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND MANAGERIAL FINANCE

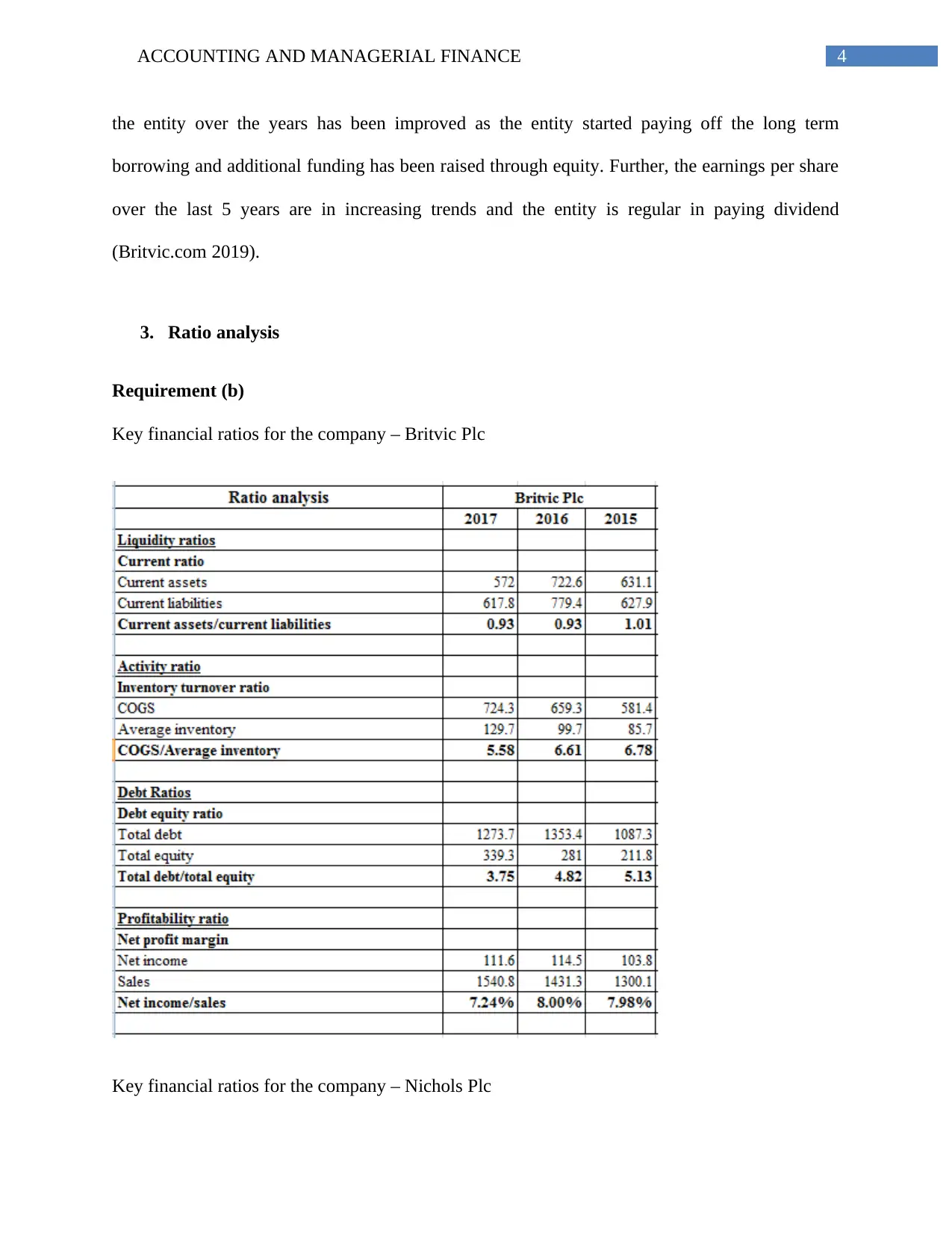

the entity over the years has been improved as the entity started paying off the long term

borrowing and additional funding has been raised through equity. Further, the earnings per share

over the last 5 years are in increasing trends and the entity is regular in paying dividend

(Britvic.com 2019).

3. Ratio analysis

Requirement (b)

Key financial ratios for the company – Britvic Plc

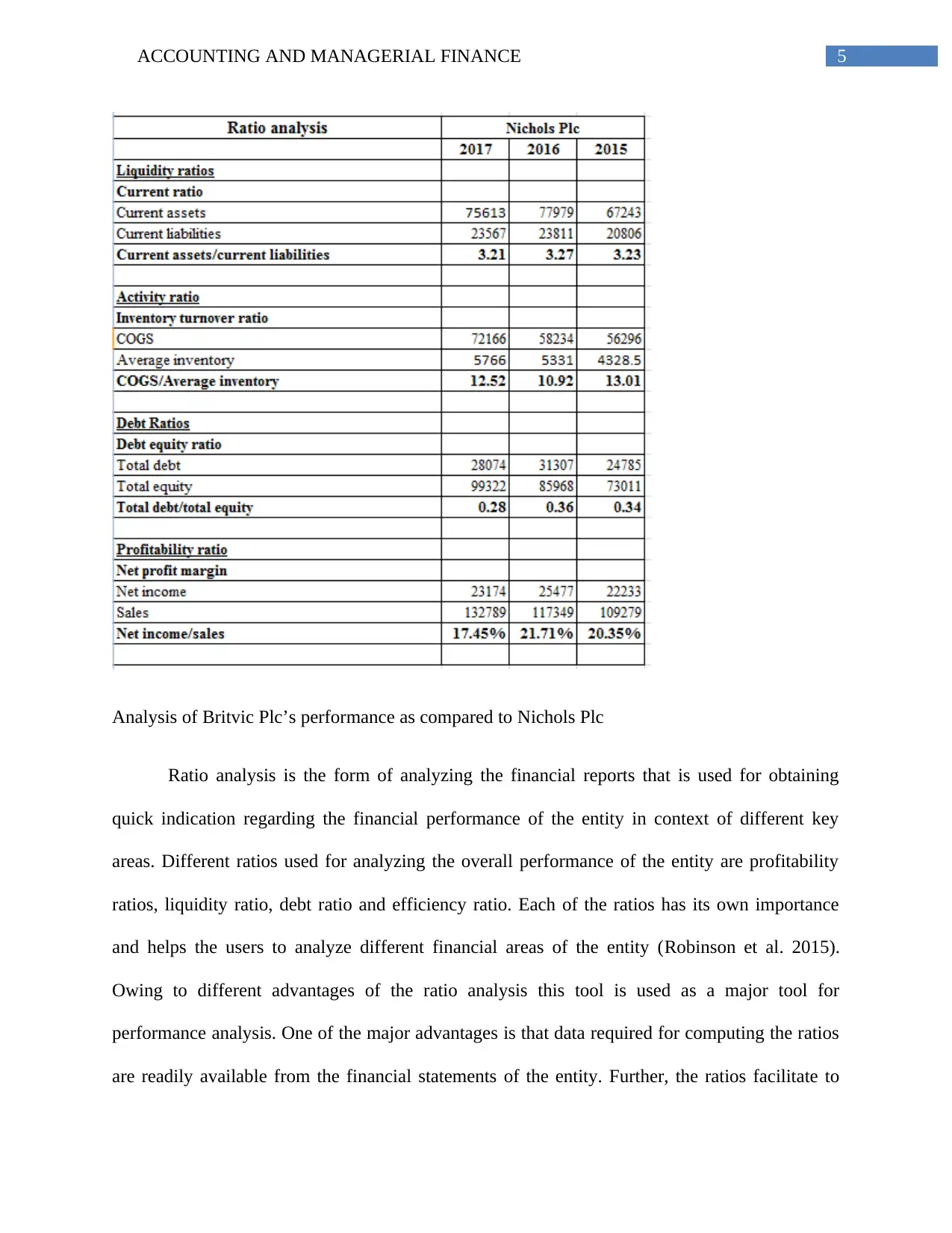

Key financial ratios for the company – Nichols Plc

the entity over the years has been improved as the entity started paying off the long term

borrowing and additional funding has been raised through equity. Further, the earnings per share

over the last 5 years are in increasing trends and the entity is regular in paying dividend

(Britvic.com 2019).

3. Ratio analysis

Requirement (b)

Key financial ratios for the company – Britvic Plc

Key financial ratios for the company – Nichols Plc

5ACCOUNTING AND MANAGERIAL FINANCE

Analysis of Britvic Plc’s performance as compared to Nichols Plc

Ratio analysis is the form of analyzing the financial reports that is used for obtaining

quick indication regarding the financial performance of the entity in context of different key

areas. Different ratios used for analyzing the overall performance of the entity are profitability

ratios, liquidity ratio, debt ratio and efficiency ratio. Each of the ratios has its own importance

and helps the users to analyze different financial areas of the entity (Robinson et al. 2015).

Owing to different advantages of the ratio analysis this tool is used as a major tool for

performance analysis. One of the major advantages is that data required for computing the ratios

are readily available from the financial statements of the entity. Further, the ratios facilitate to

Analysis of Britvic Plc’s performance as compared to Nichols Plc

Ratio analysis is the form of analyzing the financial reports that is used for obtaining

quick indication regarding the financial performance of the entity in context of different key

areas. Different ratios used for analyzing the overall performance of the entity are profitability

ratios, liquidity ratio, debt ratio and efficiency ratio. Each of the ratios has its own importance

and helps the users to analyze different financial areas of the entity (Robinson et al. 2015).

Owing to different advantages of the ratio analysis this tool is used as a major tool for

performance analysis. One of the major advantages is that data required for computing the ratios

are readily available from the financial statements of the entity. Further, the ratios facilitate to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND MANAGERIAL FINANCE

make comparison with other entity’s performance. Apart from that, it can be used to perform

trend analysis and identifying the areas where the performances have been deteriorated or

improved (Wahlen, Baginski and Bradshaw 2014)

Liquidity ratio –

In accounting, liquidity is depicted as the entity’s ability in terms of meeting the financial

obligation as it becomes due. Hence, the liquidity ratio is used for measuring the ability of the

organization to meet the short term debts. Liquidity ratio represents the number of times the

current assets of the entity can cover up the short term payables. If the result is more than 1 it

signifies that the current assets are sufficient to pay off the current obligations. On the contrary,

the liquid ratio of less than 1 signifies that the company’s current assets are not sufficient to pay

off the current obligations (Easton and Sommers 2018)

One of the most used liquid ratios is current ratio that measures the current liabilities of

the entity against its current assets. It is used to measure the entity’s liquidity position quickly. It

is computed through dividing the current assets by the current liabilities. Here, all the current

assets and all the current liabilities of the company are taken into consideration. Looking into the

current ratio of the company it can be identified that current ratio of Britvic Plc is in reducing

trend and over the last 3 years it has been reduced from 1.01 to 0.93. Major reason behind the

reduction of current asset was decrease in cash and cash equivalent that was significantly

reduced to $ 82.5 million in 2017 from $ 205.9 million (DeFusco et al. 2015). It is indicating that

the company’s current assets are not sufficient to meet the current debt obligations. On the other

hand, if the current ratio of its competitor Nichols Plc is considered it can be identified that

through the company’s current ratio over the last 3 years has been reduced from 3.23 to 3.21, for

make comparison with other entity’s performance. Apart from that, it can be used to perform

trend analysis and identifying the areas where the performances have been deteriorated or

improved (Wahlen, Baginski and Bradshaw 2014)

Liquidity ratio –

In accounting, liquidity is depicted as the entity’s ability in terms of meeting the financial

obligation as it becomes due. Hence, the liquidity ratio is used for measuring the ability of the

organization to meet the short term debts. Liquidity ratio represents the number of times the

current assets of the entity can cover up the short term payables. If the result is more than 1 it

signifies that the current assets are sufficient to pay off the current obligations. On the contrary,

the liquid ratio of less than 1 signifies that the company’s current assets are not sufficient to pay

off the current obligations (Easton and Sommers 2018)

One of the most used liquid ratios is current ratio that measures the current liabilities of

the entity against its current assets. It is used to measure the entity’s liquidity position quickly. It

is computed through dividing the current assets by the current liabilities. Here, all the current

assets and all the current liabilities of the company are taken into consideration. Looking into the

current ratio of the company it can be identified that current ratio of Britvic Plc is in reducing

trend and over the last 3 years it has been reduced from 1.01 to 0.93. Major reason behind the

reduction of current asset was decrease in cash and cash equivalent that was significantly

reduced to $ 82.5 million in 2017 from $ 205.9 million (DeFusco et al. 2015). It is indicating that

the company’s current assets are not sufficient to meet the current debt obligations. On the other

hand, if the current ratio of its competitor Nichols Plc is considered it can be identified that

through the company’s current ratio over the last 3 years has been reduced from 3.23 to 3.21, for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND MANAGERIAL FINANCE

all the 3 years its current ratio is quite high as compared to Britvic Plc and are sufficient to meet

the short term debt obligation (Nicholsplc.co.uk 2019).

Activity ratio –

Activity ratios are used to measure the company’s ability in context of converting the

balance sheet accounts into the revenues. It is used for assessing the efficiency of the entity with

regard to generation of revenues in cash form and the sales on the basis of its liability, assets, and

capital accounts. It determines the relationship among the sales and the given assets, say,

inventories. It indicates the ratio among how much investment is made for the particular assets

and the time taken to convert the same into cash (Coates 2014)

One of the most used activity ratios is inventory turnover ratio that measures the time

taken by the entity to replace or to sale the entire stock of inventories. It focuses on relationship

among the COGS and the average stock maintained by the entity (Entwistle 2015). Hence, it is

also known as the stock velocity ratio. It is computed through dividing the COGS by the average

inventories. Looking into the inventory turnover ratio of the company it can be identified that

inventory turnover ratio of Britvic Plc is in reducing trend and over the last 3 years it has been

reduced from 6.78 to 5.58. It is indicating that the company’s efficiency in replacing or selling its

assets is reduced over the years. Major reason of the reduction is the cost of sales of the entity

has been increased at higher pace as compared to the increase in inventories (Britvic.com 2019).

On the other hand, if the inventory turnover ratio of its competitor Nichols Plc is considered it

can be identified that though the company’s inventory turnover ratio over the last 3 years has

been reduced from 13.01 to 10.92, for all the 3 years its inventory turnover ratio is quite high as

all the 3 years its current ratio is quite high as compared to Britvic Plc and are sufficient to meet

the short term debt obligation (Nicholsplc.co.uk 2019).

Activity ratio –

Activity ratios are used to measure the company’s ability in context of converting the

balance sheet accounts into the revenues. It is used for assessing the efficiency of the entity with

regard to generation of revenues in cash form and the sales on the basis of its liability, assets, and

capital accounts. It determines the relationship among the sales and the given assets, say,

inventories. It indicates the ratio among how much investment is made for the particular assets

and the time taken to convert the same into cash (Coates 2014)

One of the most used activity ratios is inventory turnover ratio that measures the time

taken by the entity to replace or to sale the entire stock of inventories. It focuses on relationship

among the COGS and the average stock maintained by the entity (Entwistle 2015). Hence, it is

also known as the stock velocity ratio. It is computed through dividing the COGS by the average

inventories. Looking into the inventory turnover ratio of the company it can be identified that

inventory turnover ratio of Britvic Plc is in reducing trend and over the last 3 years it has been

reduced from 6.78 to 5.58. It is indicating that the company’s efficiency in replacing or selling its

assets is reduced over the years. Major reason of the reduction is the cost of sales of the entity

has been increased at higher pace as compared to the increase in inventories (Britvic.com 2019).

On the other hand, if the inventory turnover ratio of its competitor Nichols Plc is considered it

can be identified that though the company’s inventory turnover ratio over the last 3 years has

been reduced from 13.01 to 10.92, for all the 3 years its inventory turnover ratio is quite high as

8ACCOUNTING AND MANAGERIAL FINANCE

compared to Britvic Plc and are efficient in replacing or selling its inventories (Nicholsplc.co.uk

2019).

Debt ratio –

Debt ratio is used to signify the debt proportion of the entity as compared to the assets. It

indicates how much the entity is dependent on debt for financing its assets. It provides the users

with quick measure of debt amount the company reported in its balance sheet as compared to the

equity for financing the assets. Higher ratio indicates that the company’s operation is exposed to

higher level of risk. Conversely, lower ratio indicates that the entity has conservative financing

that provides the opportunity to borrow in future with lower risk (Nobes 2014)

One of the most used debt ratios is debt to equity ratio that measures the comparative

contribution of the shareholders and the creditors in capital employed by the business. To be

more specific, the ratio of total liabilities against total equity capital is termed as the debt equity

ratio (Brigham et al. 2016). Looking into the debt equity ratio of the company it can be identified

that though the debt equity ratio of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 5.13 to 3.75, debt, for all the 3 years under concern the entity is highly

leveraged as the debt equity ratio is significantly high. Reason behind the high leverage ratio is

that the company has financed through higher amount of long term as well as short term

borrowings as compared to the equity finance. For instance, the entity has $ 582.7 million long

term borrowing whereas the amount of issued share capital with share premium accounts for $

186.7 million (Britvic.com 2019). On the other hand, if the debt equity ratio of its competitor

Nichols Plc is considered it can be identified that the company’s debt equity ratio over the last 3

years has been reduced from 0.34 to 0.28 and for all the 3 years its debt equity ratio is

compared to Britvic Plc and are efficient in replacing or selling its inventories (Nicholsplc.co.uk

2019).

Debt ratio –

Debt ratio is used to signify the debt proportion of the entity as compared to the assets. It

indicates how much the entity is dependent on debt for financing its assets. It provides the users

with quick measure of debt amount the company reported in its balance sheet as compared to the

equity for financing the assets. Higher ratio indicates that the company’s operation is exposed to

higher level of risk. Conversely, lower ratio indicates that the entity has conservative financing

that provides the opportunity to borrow in future with lower risk (Nobes 2014)

One of the most used debt ratios is debt to equity ratio that measures the comparative

contribution of the shareholders and the creditors in capital employed by the business. To be

more specific, the ratio of total liabilities against total equity capital is termed as the debt equity

ratio (Brigham et al. 2016). Looking into the debt equity ratio of the company it can be identified

that though the debt equity ratio of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 5.13 to 3.75, debt, for all the 3 years under concern the entity is highly

leveraged as the debt equity ratio is significantly high. Reason behind the high leverage ratio is

that the company has financed through higher amount of long term as well as short term

borrowings as compared to the equity finance. For instance, the entity has $ 582.7 million long

term borrowing whereas the amount of issued share capital with share premium accounts for $

186.7 million (Britvic.com 2019). On the other hand, if the debt equity ratio of its competitor

Nichols Plc is considered it can be identified that the company’s debt equity ratio over the last 3

years has been reduced from 0.34 to 0.28 and for all the 3 years its debt equity ratio is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND MANAGERIAL FINANCE

significantly low as compared to Britvic Plc and are hence, it will be considered as lower

leverages and less exposed to financial risk (Nicholsplc.co.uk 2019).

Profitability ratio –

Profitability ratio compares the income statements items and categorise the same to

measure the ability of the entity to generate the profits from operation. It is used by the creditors

and investors to analyse the return provided by the entity on shareholder’s investment. To be

more specific, the profitability ratio can be used for judging whether the entity is generating

sufficient operation al profit from the assets (Loughran and McDonald 2014)

One of the most widely profitability ratios is net profit margin that measures the net

earnings earned by the entity from selling the goods or providing the services or simply, the

amount of profit generated by the entity at particular sales level. It shows the revenues or

earnings left for the equity as well as preference shareholders after paying all operating expenses,

financial expenses and tax expenses. Looking into the net profit margin of the company it can be

identified that net profit margin of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 7.98% to 7.24%. The reason behind the reduction is the increase is revenue

was at lower rate as compared to increase in cost of sales (Britvic.com 2019). It is indicating that

the company’s efficiency in generating profit from sales after paying the expenses are reduced

over the years. On the other hand, if the net profit margin of its competitor Nichols Plc is

considered it can be identified that through the company’s net profit margin has been reduced

over the last 3 years from 20.35% to 17.45%, for all the 3 years its net profit margin is quite high

as compared to Britvic Plc and it is efficient in generating higher percentage profit from sales

after paying the expenses (Nicholsplc.co.uk 2019).

significantly low as compared to Britvic Plc and are hence, it will be considered as lower

leverages and less exposed to financial risk (Nicholsplc.co.uk 2019).

Profitability ratio –

Profitability ratio compares the income statements items and categorise the same to

measure the ability of the entity to generate the profits from operation. It is used by the creditors

and investors to analyse the return provided by the entity on shareholder’s investment. To be

more specific, the profitability ratio can be used for judging whether the entity is generating

sufficient operation al profit from the assets (Loughran and McDonald 2014)

One of the most widely profitability ratios is net profit margin that measures the net

earnings earned by the entity from selling the goods or providing the services or simply, the

amount of profit generated by the entity at particular sales level. It shows the revenues or

earnings left for the equity as well as preference shareholders after paying all operating expenses,

financial expenses and tax expenses. Looking into the net profit margin of the company it can be

identified that net profit margin of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 7.98% to 7.24%. The reason behind the reduction is the increase is revenue

was at lower rate as compared to increase in cost of sales (Britvic.com 2019). It is indicating that

the company’s efficiency in generating profit from sales after paying the expenses are reduced

over the years. On the other hand, if the net profit margin of its competitor Nichols Plc is

considered it can be identified that through the company’s net profit margin has been reduced

over the last 3 years from 20.35% to 17.45%, for all the 3 years its net profit margin is quite high

as compared to Britvic Plc and it is efficient in generating higher percentage profit from sales

after paying the expenses (Nicholsplc.co.uk 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND MANAGERIAL FINANCE

Hence, if the overall financial performance of Britvic Plc is compared with its competitor

Nichols Plc it can be stated that the Nichols Plc’s performance is better as compared to Britvic

Plc in all aspects including liquidity, solvency, efficiency and profitability.

Requirement (c)

Interpreting the performance of Britvic Plc for 2017 as compared to previous years

Current ratio – Looking into the current ratio of the company it can be identified that current

ratio of Britvic Plc is in reducing trend and over the last 3 years it has been reduced from 1.01 to

0.93. Generally, the current ratio of more than one signifies that the current assets of the entity

are sufficient to meet the short term debt obligation. However, the current ratio trend of the

company is indicating that the company’s current assets are not sufficient to meet the current

debt obligations. Further, the current ratio for 2017 is lowers as compared to previous 2 years

(Britvic.com 2019).

Inventory turnover ratio – Looking into the inventory turnover ratio of the company it can be

identified that inventory turnover ratio of Britvic Plc is in reducing trend and over the last 3 years

it has been reduced from 6.78 to 5.58. It is indicating that the company’s efficiency in replacing

or selling its assets is reduced over the years. Further, the efficiency of the company in 2017 has

been reduced as compared to previous 2 years (Britvic.com 2019).

Debt equity ratio – Looking into the debt equity ratio of the company it can be identified that

though the debt equity ratio of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 5.13 to 3.75, debt for all the 3 years under concern of the entity is highly

leveraged as the debt equity ratio is significantly high. However, if the leverage position of 2017

Hence, if the overall financial performance of Britvic Plc is compared with its competitor

Nichols Plc it can be stated that the Nichols Plc’s performance is better as compared to Britvic

Plc in all aspects including liquidity, solvency, efficiency and profitability.

Requirement (c)

Interpreting the performance of Britvic Plc for 2017 as compared to previous years

Current ratio – Looking into the current ratio of the company it can be identified that current

ratio of Britvic Plc is in reducing trend and over the last 3 years it has been reduced from 1.01 to

0.93. Generally, the current ratio of more than one signifies that the current assets of the entity

are sufficient to meet the short term debt obligation. However, the current ratio trend of the

company is indicating that the company’s current assets are not sufficient to meet the current

debt obligations. Further, the current ratio for 2017 is lowers as compared to previous 2 years

(Britvic.com 2019).

Inventory turnover ratio – Looking into the inventory turnover ratio of the company it can be

identified that inventory turnover ratio of Britvic Plc is in reducing trend and over the last 3 years

it has been reduced from 6.78 to 5.58. It is indicating that the company’s efficiency in replacing

or selling its assets is reduced over the years. Further, the efficiency of the company in 2017 has

been reduced as compared to previous 2 years (Britvic.com 2019).

Debt equity ratio – Looking into the debt equity ratio of the company it can be identified that

though the debt equity ratio of Britvic Plc is in reducing trend and over the last 3 years it has

been reduced from 5.13 to 3.75, debt for all the 3 years under concern of the entity is highly

leveraged as the debt equity ratio is significantly high. However, if the leverage position of 2017

11ACCOUNTING AND MANAGERIAL FINANCE

is compared with previous 2 years it can be identified that the leverage position has been

improved in 2017 (Britvic.com 2019).

Net profit margin – Looking into the net profit margin of the company it can be identified that

net profit margin of Britvic Plc is in reducing trend and over the last 3 years it has been reduced

from 7.98% to 7.24%. Hence, the profitability position of the entity for the year 2017 has been

deteriorated as compared to previous 2 years. It is indicating that the company’s efficiency in

generating profit from sales after paying the expenses are reduced over the years (Britvic.com

2019).

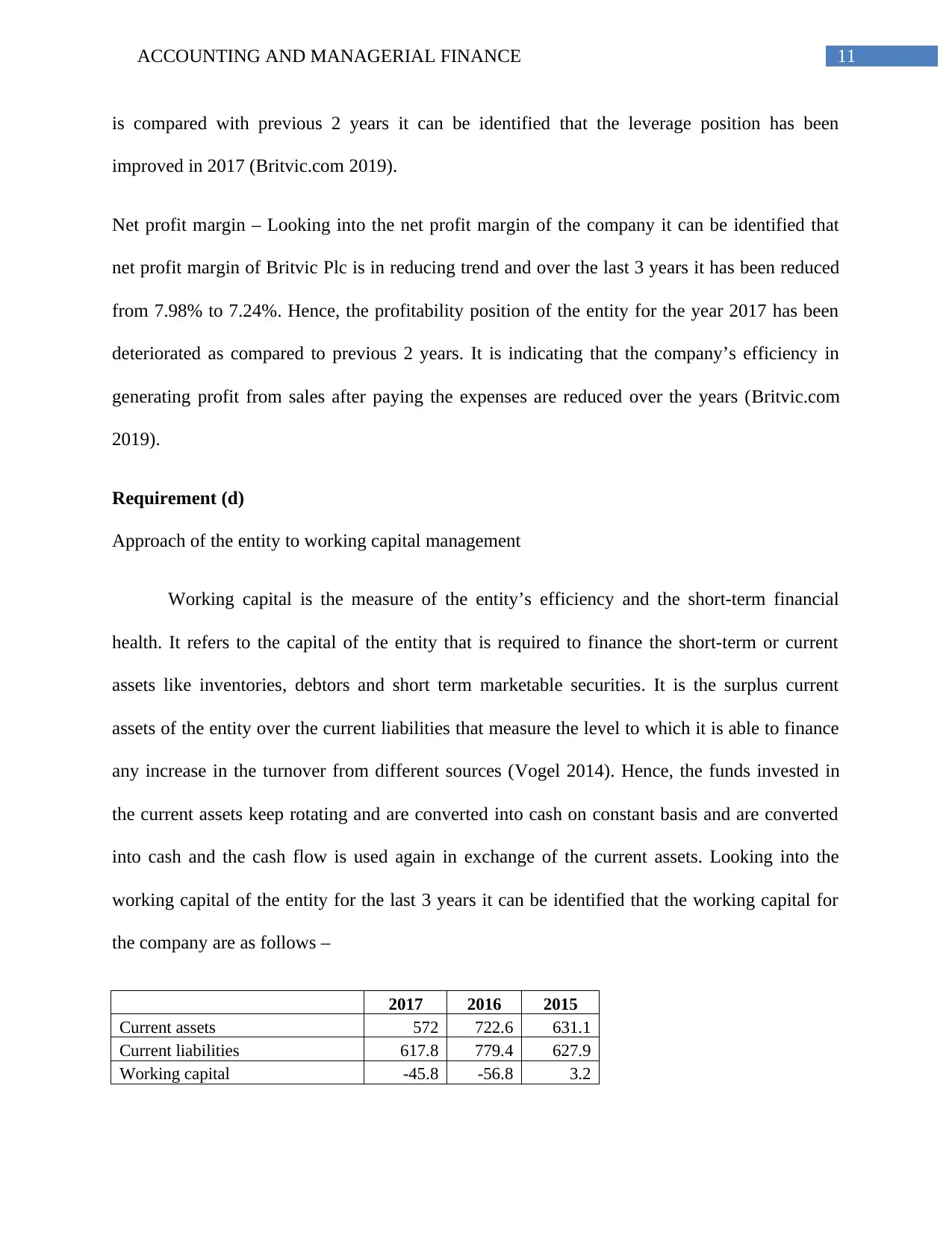

Requirement (d)

Approach of the entity to working capital management

Working capital is the measure of the entity’s efficiency and the short-term financial

health. It refers to the capital of the entity that is required to finance the short-term or current

assets like inventories, debtors and short term marketable securities. It is the surplus current

assets of the entity over the current liabilities that measure the level to which it is able to finance

any increase in the turnover from different sources (Vogel 2014). Hence, the funds invested in

the current assets keep rotating and are converted into cash on constant basis and are converted

into cash and the cash flow is used again in exchange of the current assets. Looking into the

working capital of the entity for the last 3 years it can be identified that the working capital for

the company are as follows –

2017 2016 2015

Current assets 572 722.6 631.1

Current liabilities 617.8 779.4 627.9

Working capital -45.8 -56.8 3.2

is compared with previous 2 years it can be identified that the leverage position has been

improved in 2017 (Britvic.com 2019).

Net profit margin – Looking into the net profit margin of the company it can be identified that

net profit margin of Britvic Plc is in reducing trend and over the last 3 years it has been reduced

from 7.98% to 7.24%. Hence, the profitability position of the entity for the year 2017 has been

deteriorated as compared to previous 2 years. It is indicating that the company’s efficiency in

generating profit from sales after paying the expenses are reduced over the years (Britvic.com

2019).

Requirement (d)

Approach of the entity to working capital management

Working capital is the measure of the entity’s efficiency and the short-term financial

health. It refers to the capital of the entity that is required to finance the short-term or current

assets like inventories, debtors and short term marketable securities. It is the surplus current

assets of the entity over the current liabilities that measure the level to which it is able to finance

any increase in the turnover from different sources (Vogel 2014). Hence, the funds invested in

the current assets keep rotating and are converted into cash on constant basis and are converted

into cash and the cash flow is used again in exchange of the current assets. Looking into the

working capital of the entity for the last 3 years it can be identified that the working capital for

the company are as follows –

2017 2016 2015

Current assets 572 722.6 631.1

Current liabilities 617.8 779.4 627.9

Working capital -45.8 -56.8 3.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.