Accounting Applications: Principles vs. Rules Based Approach

VerifiedAdded on 2022/11/09

|11

|1592

|202

AI Summary

This document discusses the principles vs. rules based approach to accounting, evaluating their advantages and disadvantages, and determining which is the most reliable and accurate method. It also includes aged accounts receivable, aged accounts payable, profit and loss statement, and balance sheet.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING APPLICATIONS

Accounting Application

Name of the Student:

Name of the University:

Authors Note:

Accounting Application

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING APPLICATIONS

1

Table of Contents

Part A:........................................................................................................................................2

Aged Accounts Receivable:.......................................................................................................2

Aged Accounts Payable:............................................................................................................2

Profit and Loss Statement (30 June 2019):................................................................................3

Balance Sheet (30 June 2019):...................................................................................................4

Part B:.........................................................................................................................................5

Evaluating the advantages and disadvantages of the Principles vs. Rules based approach to

accounting:.................................................................................................................................5

Discussing and critically analysing the Principles vs. Rules based approach to accounting,

while determining which is the most reliable and accurate method:.........................................7

References:.................................................................................................................................9

1

Table of Contents

Part A:........................................................................................................................................2

Aged Accounts Receivable:.......................................................................................................2

Aged Accounts Payable:............................................................................................................2

Profit and Loss Statement (30 June 2019):................................................................................3

Balance Sheet (30 June 2019):...................................................................................................4

Part B:.........................................................................................................................................5

Evaluating the advantages and disadvantages of the Principles vs. Rules based approach to

accounting:.................................................................................................................................5

Discussing and critically analysing the Principles vs. Rules based approach to accounting,

while determining which is the most reliable and accurate method:.........................................7

References:.................................................................................................................................9

ACCOUNTING APPLICATIONS

2

Part A:

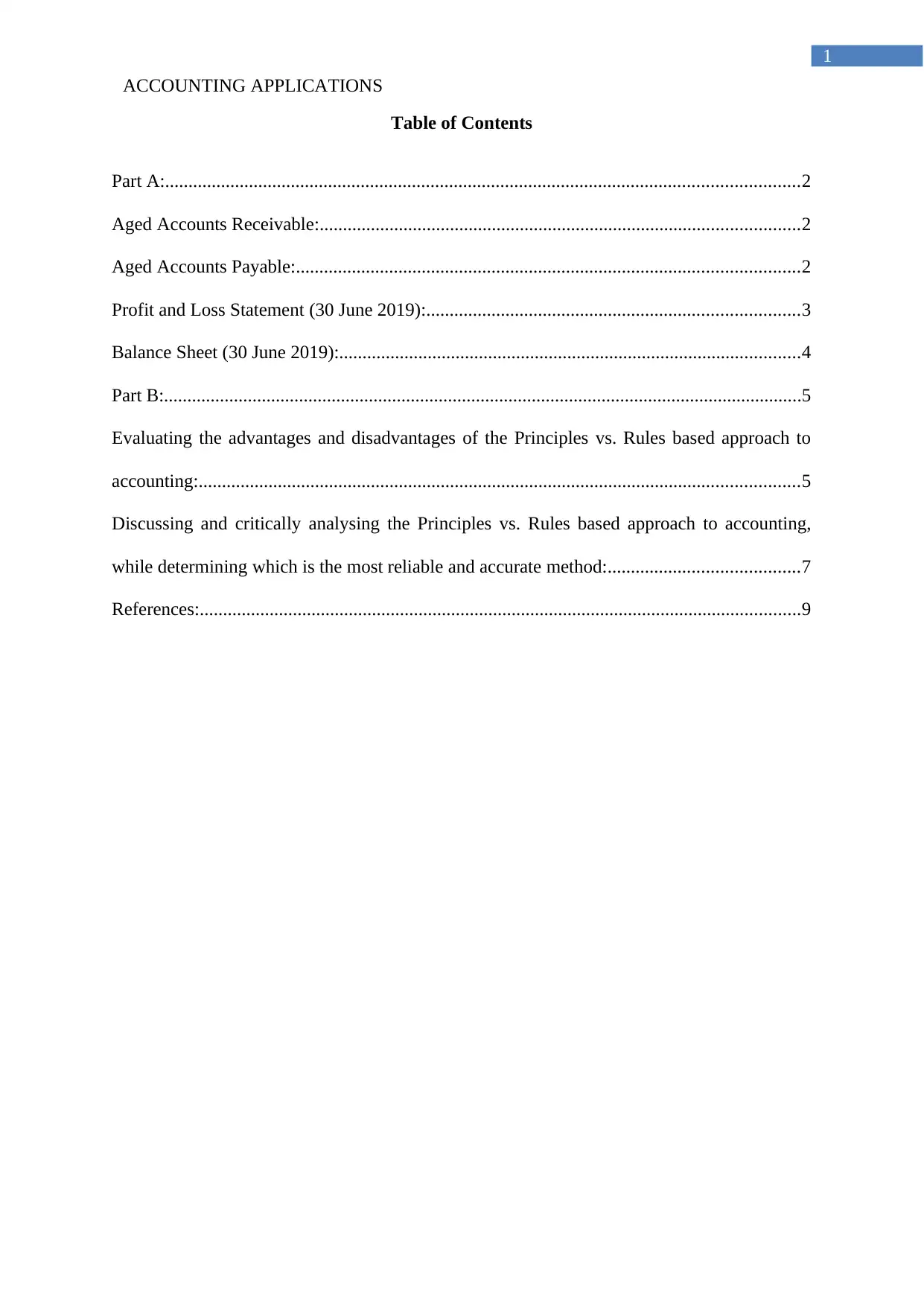

Aged Accounts Receivable:

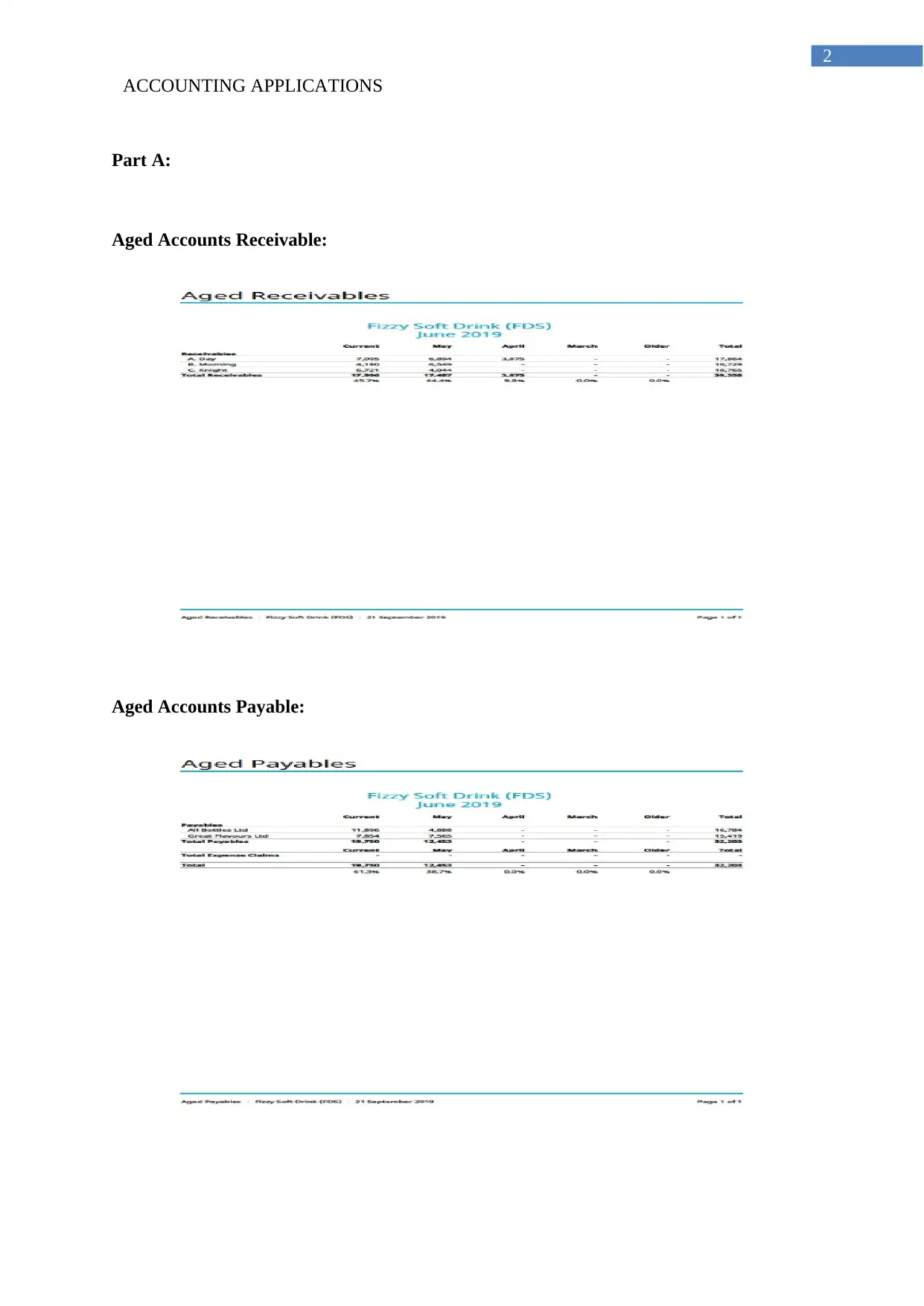

Aged Accounts Payable:

2

Part A:

Aged Accounts Receivable:

Aged Accounts Payable:

ACCOUNTING APPLICATIONS

3

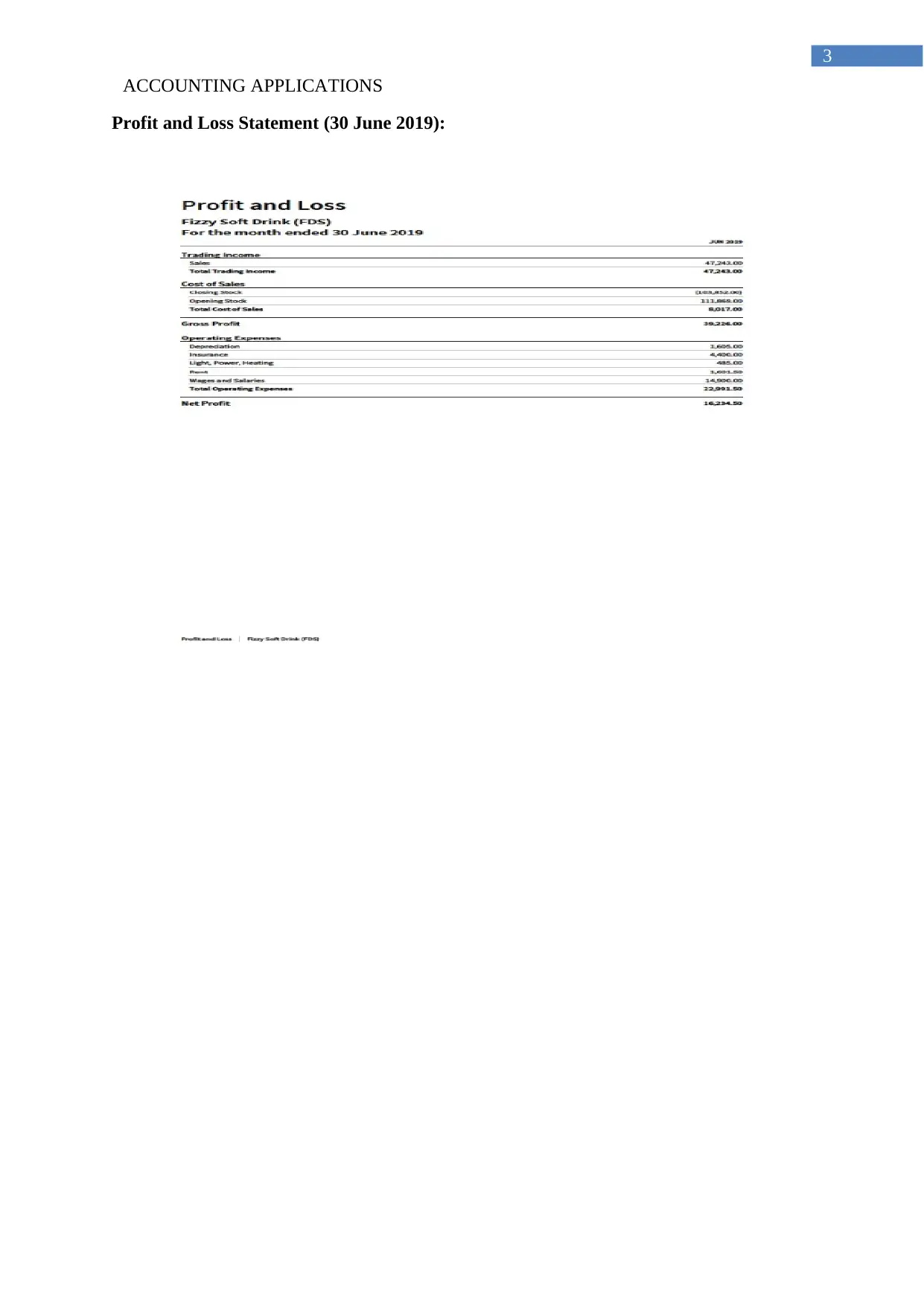

Profit and Loss Statement (30 June 2019):

3

Profit and Loss Statement (30 June 2019):

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING APPLICATIONS

4

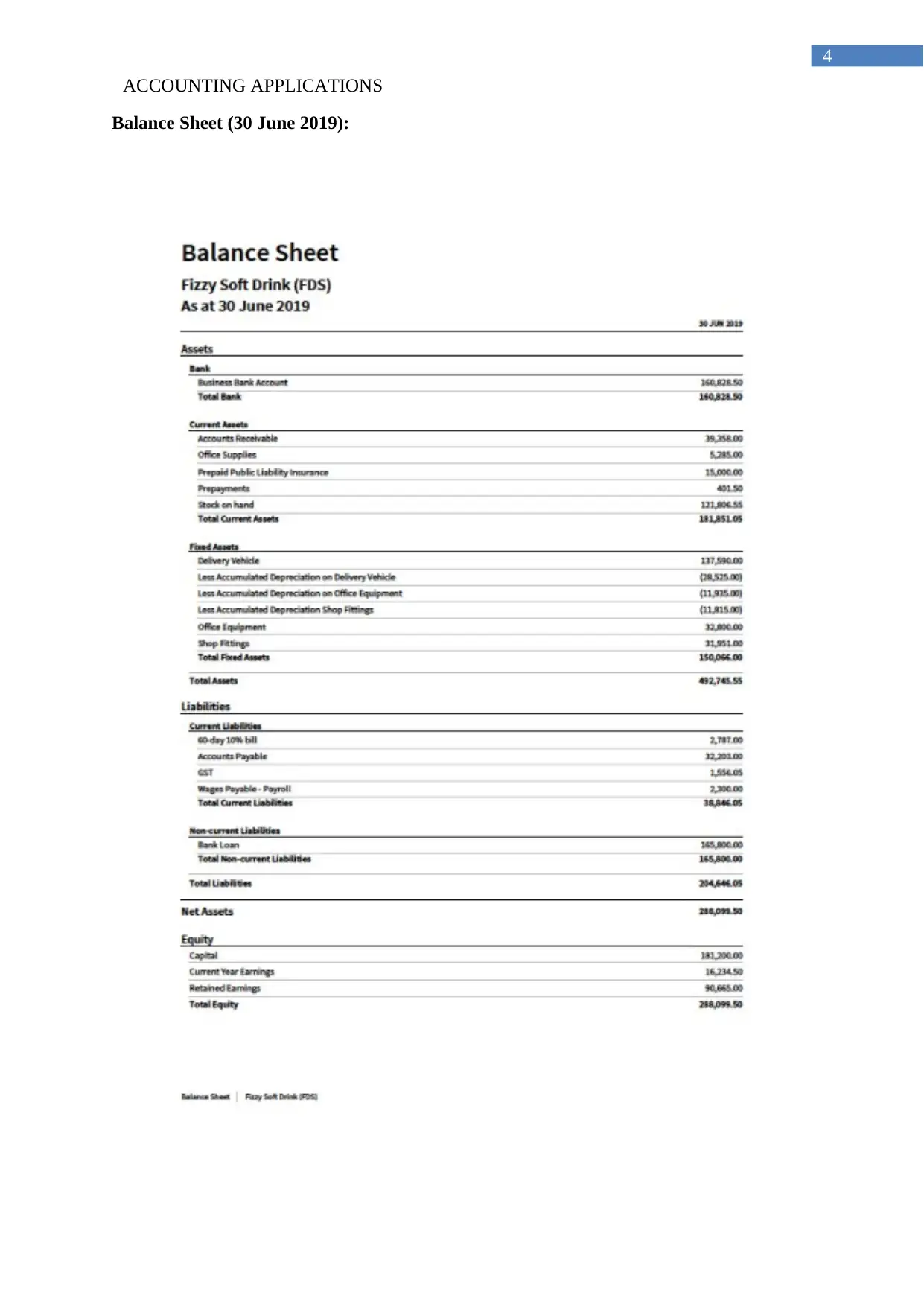

Balance Sheet (30 June 2019):

4

Balance Sheet (30 June 2019):

ACCOUNTING APPLICATIONS

5

Part B:

Evaluating the advantages and disadvantages of the Principles vs. Rules based

approach to accounting:

The analysis has mainly stated that companies can use two different type of

accounting approach based on their financial requirements. In addition, the performance of

the organisation is based on the accounting approach that is being used by companies for

preparing their financial report (Fisher, Garnsey and Hughes 2016). Therefore, both the

approach to accounting has relevant significance and limitations that is faced by the

organisations over the period of time. The Principles and Rules based approach to accounting

has relevant difference, which can be depicted as follows.

Advantages of Principle based approach to accounting:

The principle-based accounting has relevant advantages, which is used by the

organisation while presenting their annual report. The organisation is provided with a broad

guideline, which can be used for preparing the annual report and handing numerus situations

that is encountered by the company. In addition, the method helps in mitigating the

occurrence of unethical activities and manipulations, as it reduces the occurrence of pitfalls,

while providing the organisation with the relevant actions that can be taken on precise

requirements. Moreover, the method relevantly allows the accountants to rely on professional

judgements, while assessing different accounts, while analysing the entries of the annual

report (Jefrey 2018). Furthermore, the approach allows the organisation to utilise a simplistic

tactic, which is easier to accommodate all the relevant transactions and increase transparency

with the outsiders. Nevertheless, the approach provides the leniency to the organisation for

accurately depicting their financial performance in the annual report, as the occurrence of

manipulations is substantially reduced. Lastly, the use of principle-based accounting method

5

Part B:

Evaluating the advantages and disadvantages of the Principles vs. Rules based

approach to accounting:

The analysis has mainly stated that companies can use two different type of

accounting approach based on their financial requirements. In addition, the performance of

the organisation is based on the accounting approach that is being used by companies for

preparing their financial report (Fisher, Garnsey and Hughes 2016). Therefore, both the

approach to accounting has relevant significance and limitations that is faced by the

organisations over the period of time. The Principles and Rules based approach to accounting

has relevant difference, which can be depicted as follows.

Advantages of Principle based approach to accounting:

The principle-based accounting has relevant advantages, which is used by the

organisation while presenting their annual report. The organisation is provided with a broad

guideline, which can be used for preparing the annual report and handing numerus situations

that is encountered by the company. In addition, the method helps in mitigating the

occurrence of unethical activities and manipulations, as it reduces the occurrence of pitfalls,

while providing the organisation with the relevant actions that can be taken on precise

requirements. Moreover, the method relevantly allows the accountants to rely on professional

judgements, while assessing different accounts, while analysing the entries of the annual

report (Jefrey 2018). Furthermore, the approach allows the organisation to utilise a simplistic

tactic, which is easier to accommodate all the relevant transactions and increase transparency

with the outsiders. Nevertheless, the approach provides the leniency to the organisation for

accurately depicting their financial performance in the annual report, as the occurrence of

manipulations is substantially reduced. Lastly, the use of principle-based accounting method

ACCOUNTING APPLICATIONS

6

directly promotes the use of comparative ability, which can be conducted by investors with

competitors and understand the performance of the company.

Disadvantages of Principle based approach to accounting:

The major disadvantage of the principle-based approach is excess leniency that is

provided to the organisation while preparing the annual report. The approach does not

provide exercise guidelines, which increases the problems for the organisation to present

approach actions in their annual report, which in turn creates inconsistency with the

organisation. Hence, the excess leniency would lead to absence of appropriate standards

across different standards, which is mainly used by companies in formulating the annual

report. the principle-based accounting is somewhat vague, where the accountants use the rule

based accoutring method, as it helps in minimising the occurrence of conflict, as it has an

existing pattern of judgement for each transaction (Braun et al. 2015). Furthermore, the

principle-based accounting approach provides the organisation with adequate clemency,

which reduces the change of any economic realities that can be compared with the

organisation’s performance. the company financial report under the method is not comparable

with other organisations, which reduces the chance of detecting irrelevant financial

performance of the organisation.

Advantages of Rule based approach to accounting:

The major advantages of the rule-based accounting method are utilisation of

accounting standards, which could be used for increasing the accuracy of company financial

reporting capability. In addition, the method also helps in verifying the actions of the auditors

and regulations, as it allows the auditors to utilise the standard, while depicting the

information of the company in their disclosures. Furthermore, the presence of the approach

mainly helps in reducing the occurrence of any earnings management that could be conducted

6

directly promotes the use of comparative ability, which can be conducted by investors with

competitors and understand the performance of the company.

Disadvantages of Principle based approach to accounting:

The major disadvantage of the principle-based approach is excess leniency that is

provided to the organisation while preparing the annual report. The approach does not

provide exercise guidelines, which increases the problems for the organisation to present

approach actions in their annual report, which in turn creates inconsistency with the

organisation. Hence, the excess leniency would lead to absence of appropriate standards

across different standards, which is mainly used by companies in formulating the annual

report. the principle-based accounting is somewhat vague, where the accountants use the rule

based accoutring method, as it helps in minimising the occurrence of conflict, as it has an

existing pattern of judgement for each transaction (Braun et al. 2015). Furthermore, the

principle-based accounting approach provides the organisation with adequate clemency,

which reduces the change of any economic realities that can be compared with the

organisation’s performance. the company financial report under the method is not comparable

with other organisations, which reduces the chance of detecting irrelevant financial

performance of the organisation.

Advantages of Rule based approach to accounting:

The major advantages of the rule-based accounting method are utilisation of

accounting standards, which could be used for increasing the accuracy of company financial

reporting capability. In addition, the method also helps in verifying the actions of the auditors

and regulations, as it allows the auditors to utilise the standard, while depicting the

information of the company in their disclosures. Furthermore, the presence of the approach

mainly helps in reducing the occurrence of any earnings management that could be conducted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING APPLICATIONS

7

by the directors of the organisation for increasing the occurrence of aggressing reporting

choices (Niklis, Doumpos and Zopounidis 2014). The method mainly helps in depicting all

the relevant standards that needs to be used by the companies and no assumptions could be

made by the company in presenting their transactions, which minimises the occurrence of

manipulations, which could be conducted to inflate the financial report.

Disadvantages of Rule based approach to accounting:

There is certain limitation of the rule-based accounting approach, which mainly

increases the reliance of the accountants with the overall regulations that needs to be used

while analysing reach transactions. This increases the doubt among the accounts, as they are

not able to decipher all the relevant transactions based on the depicted standards of the rule-

based approach (Hayes 2017). Moreover, the rule-based method directly forces the

accountants to use the legalistic approach for detecting all the relevant transactions of the

company in their financial report. in addition, the approach does not provide the accountancy

with the adequate steps, which used in principle based method, which directly increases the

chance of irrelevant information occurrence in the financial report.

Discussing and critically analysing the Principles vs. Rules based approach to

accounting, while determining which is the most reliable and accurate method:

Principles and Rules based approach to accounting mainly indicates about the

accounting methods that can be used by the organisations while formulating their financial

report. In addition, the International Financial Reporting Standards System (IFRS) mainly

uses the principle based approach accounting method, while Generally Accepted Accounting

Principles (GAAP) uses rule based accounting method. There is a significant difference

between the financial viability and transparency between the financial reports presented in

IFRS and GAAP formats (Jefrey 2018). From the analysis, it has been detected that the

7

by the directors of the organisation for increasing the occurrence of aggressing reporting

choices (Niklis, Doumpos and Zopounidis 2014). The method mainly helps in depicting all

the relevant standards that needs to be used by the companies and no assumptions could be

made by the company in presenting their transactions, which minimises the occurrence of

manipulations, which could be conducted to inflate the financial report.

Disadvantages of Rule based approach to accounting:

There is certain limitation of the rule-based accounting approach, which mainly

increases the reliance of the accountants with the overall regulations that needs to be used

while analysing reach transactions. This increases the doubt among the accounts, as they are

not able to decipher all the relevant transactions based on the depicted standards of the rule-

based approach (Hayes 2017). Moreover, the rule-based method directly forces the

accountants to use the legalistic approach for detecting all the relevant transactions of the

company in their financial report. in addition, the approach does not provide the accountancy

with the adequate steps, which used in principle based method, which directly increases the

chance of irrelevant information occurrence in the financial report.

Discussing and critically analysing the Principles vs. Rules based approach to

accounting, while determining which is the most reliable and accurate method:

Principles and Rules based approach to accounting mainly indicates about the

accounting methods that can be used by the organisations while formulating their financial

report. In addition, the International Financial Reporting Standards System (IFRS) mainly

uses the principle based approach accounting method, while Generally Accepted Accounting

Principles (GAAP) uses rule based accounting method. There is a significant difference

between the financial viability and transparency between the financial reports presented in

IFRS and GAAP formats (Jefrey 2018). From the analysis, it has been detected that the

ACCOUNTING APPLICATIONS

8

GAAP annual report is more complex and has low transparency, which does not allow each

financial report user to understanding the relevant transactions. On the other hand, the

financial report presented in the format of IFRS directly provides all the relevant information

in truthful manner, as the transparency level of in financial report is high, which can help

investors understand the actual financial performance of the company (Liu, Liang and Wang

2015).

Thus, it could be understood that the best possible accounting method that could be

used by organisations is relevantly not possible. However, the accountants all around the

world are indicating to use the principle-based accounting method, as it helps in minimising

the occurrence of manipulations and increases the possibility of modifications that improves

the effectiveness of the annual port. The information in the accounting report needs to be

reliable, comparable and relevant across the reporting periods, which directly indicates that

principle-based accounting method is more appropriate than the rule-based accounting

method (Monroy, Nasiri and Pelaez 2014).

8

GAAP annual report is more complex and has low transparency, which does not allow each

financial report user to understanding the relevant transactions. On the other hand, the

financial report presented in the format of IFRS directly provides all the relevant information

in truthful manner, as the transparency level of in financial report is high, which can help

investors understand the actual financial performance of the company (Liu, Liang and Wang

2015).

Thus, it could be understood that the best possible accounting method that could be

used by organisations is relevantly not possible. However, the accountants all around the

world are indicating to use the principle-based accounting method, as it helps in minimising

the occurrence of manipulations and increases the possibility of modifications that improves

the effectiveness of the annual port. The information in the accounting report needs to be

reliable, comparable and relevant across the reporting periods, which directly indicates that

principle-based accounting method is more appropriate than the rule-based accounting

method (Monroy, Nasiri and Pelaez 2014).

ACCOUNTING APPLICATIONS

9

References:

Braun, G.P., Haynes, C.M., Lewis, T.D. and Taylor, M.H., 2015. Principles-based vs. rules-

based accounting standards: The effects of auditee proposed accounting treatment and

regulatory enforcement on auditor judgments and confidence. Research in Accounting

Regulation, 27(1), pp.45-50.

Fisher, I.E., Garnsey, M.R. and Hughes, M.E., 2016. Natural language processing in

accounting, auditing and finance: A synthesis of the literature with a roadmap for future

research. Intelligent Systems in Accounting, Finance and Management, 23(3), pp.157-214.

Hayes, A.F., 2017. Introduction to mediation, moderation, and conditional process analysis:

A regression-based approach. Guilford Publications.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Liu, L.C., Liang, Q.M. and Wang, Q., 2015. Accounting for China's regional carbon

emissions in 2002 and 2007: production-based versus consumption-based principles. Journal

of Cleaner Production, 103, pp.384-392.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity based costing, time-driven activity

based costing and lean accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer, London.

9

References:

Braun, G.P., Haynes, C.M., Lewis, T.D. and Taylor, M.H., 2015. Principles-based vs. rules-

based accounting standards: The effects of auditee proposed accounting treatment and

regulatory enforcement on auditor judgments and confidence. Research in Accounting

Regulation, 27(1), pp.45-50.

Fisher, I.E., Garnsey, M.R. and Hughes, M.E., 2016. Natural language processing in

accounting, auditing and finance: A synthesis of the literature with a roadmap for future

research. Intelligent Systems in Accounting, Finance and Management, 23(3), pp.157-214.

Hayes, A.F., 2017. Introduction to mediation, moderation, and conditional process analysis:

A regression-based approach. Guilford Publications.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Liu, L.C., Liang, Q.M. and Wang, Q., 2015. Accounting for China's regional carbon

emissions in 2002 and 2007: production-based versus consumption-based principles. Journal

of Cleaner Production, 103, pp.384-392.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity based costing, time-driven activity

based costing and lean accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer, London.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING APPLICATIONS

10

Niklis, D., Doumpos, M. and Zopounidis, C., 2014. Combining market and accounting-based

models for credit scoring using a classification scheme based on support vector

machines. Applied Mathematics and Computation, 234, pp.69-81.

10

Niklis, D., Doumpos, M. and Zopounidis, C., 2014. Combining market and accounting-based

models for credit scoring using a classification scheme based on support vector

machines. Applied Mathematics and Computation, 234, pp.69-81.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.