ACC5000 Assignment 2: Accounting Applications and Inventory Costing

VerifiedAdded on 2023/01/05

|8

|1400

|60

Report

AI Summary

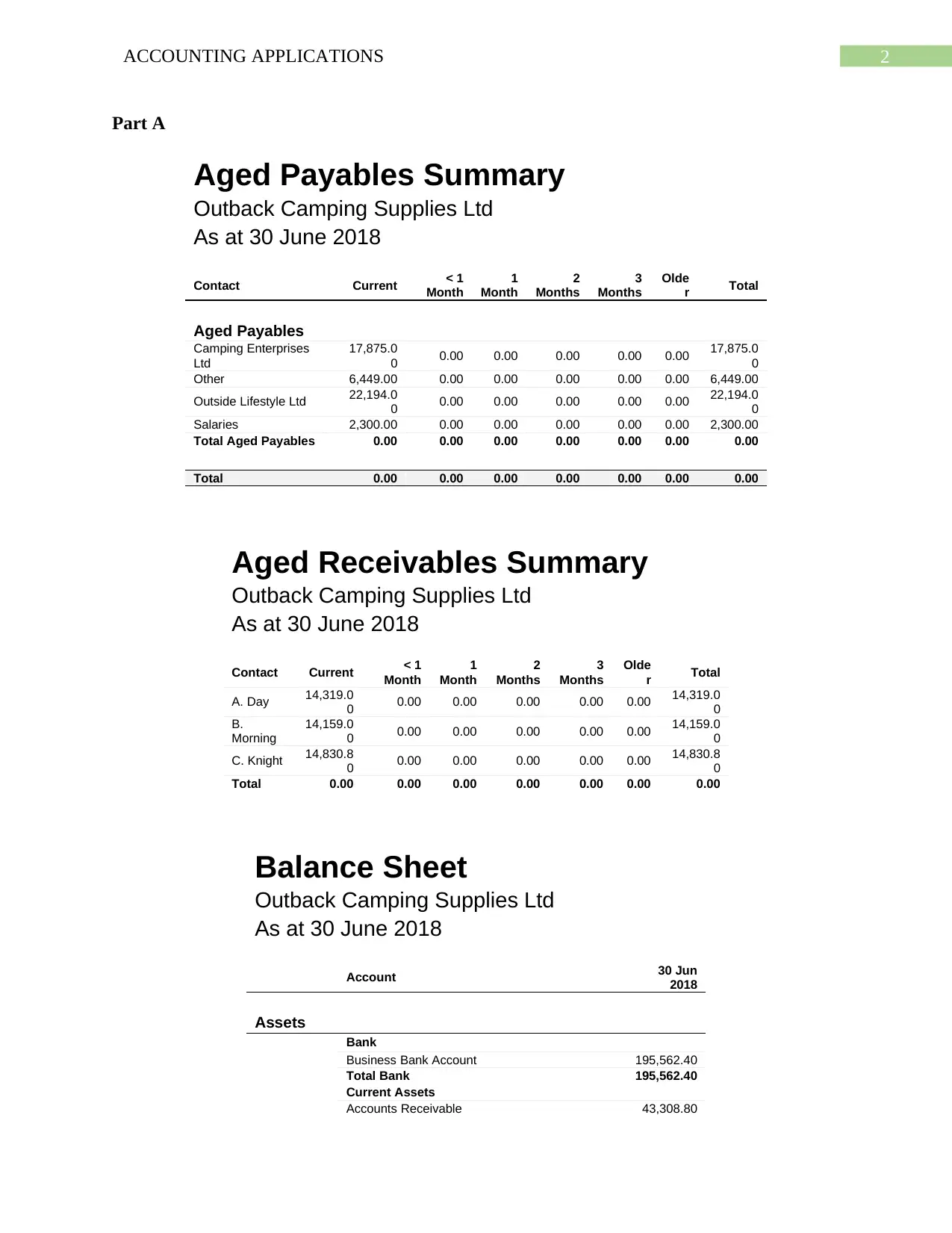

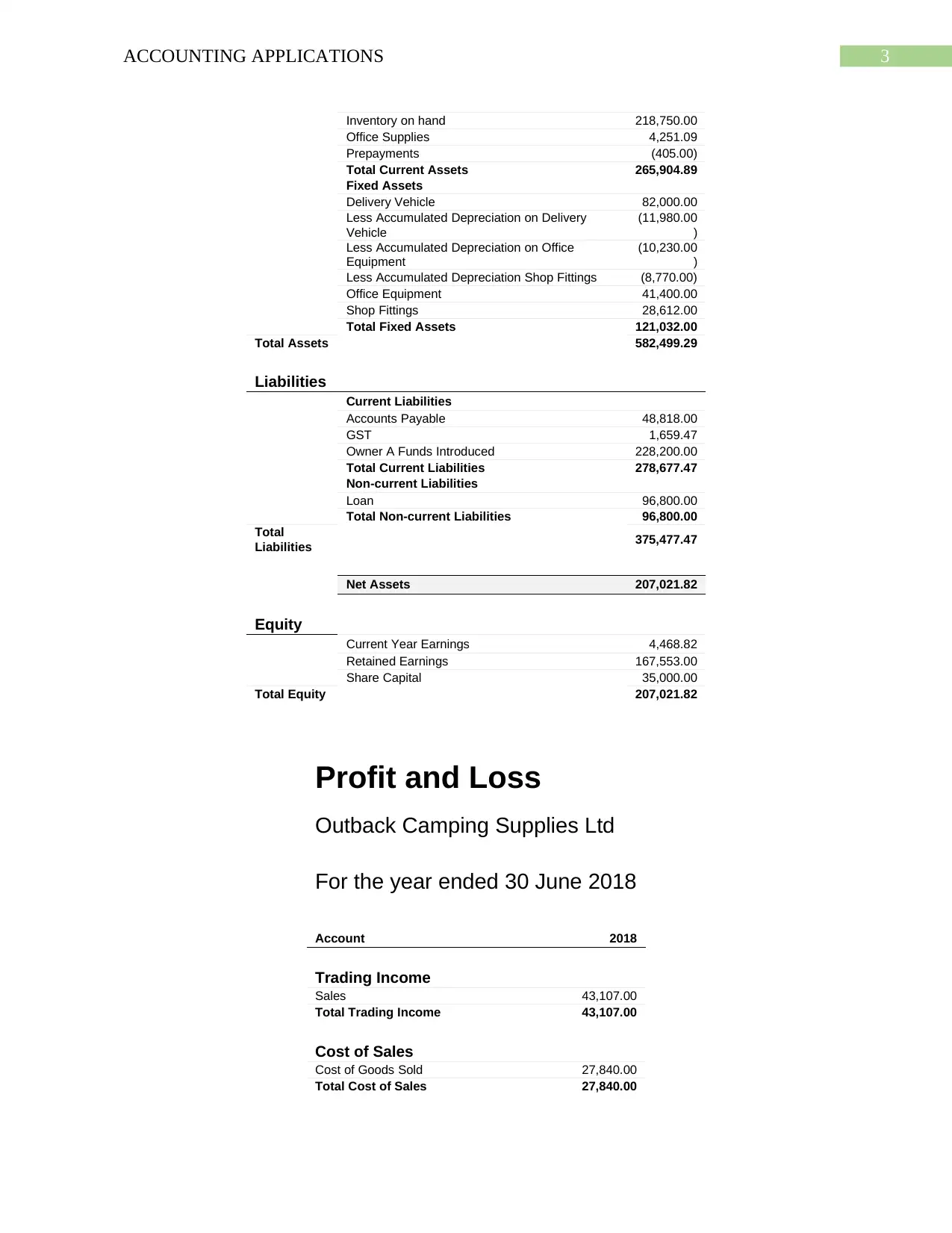

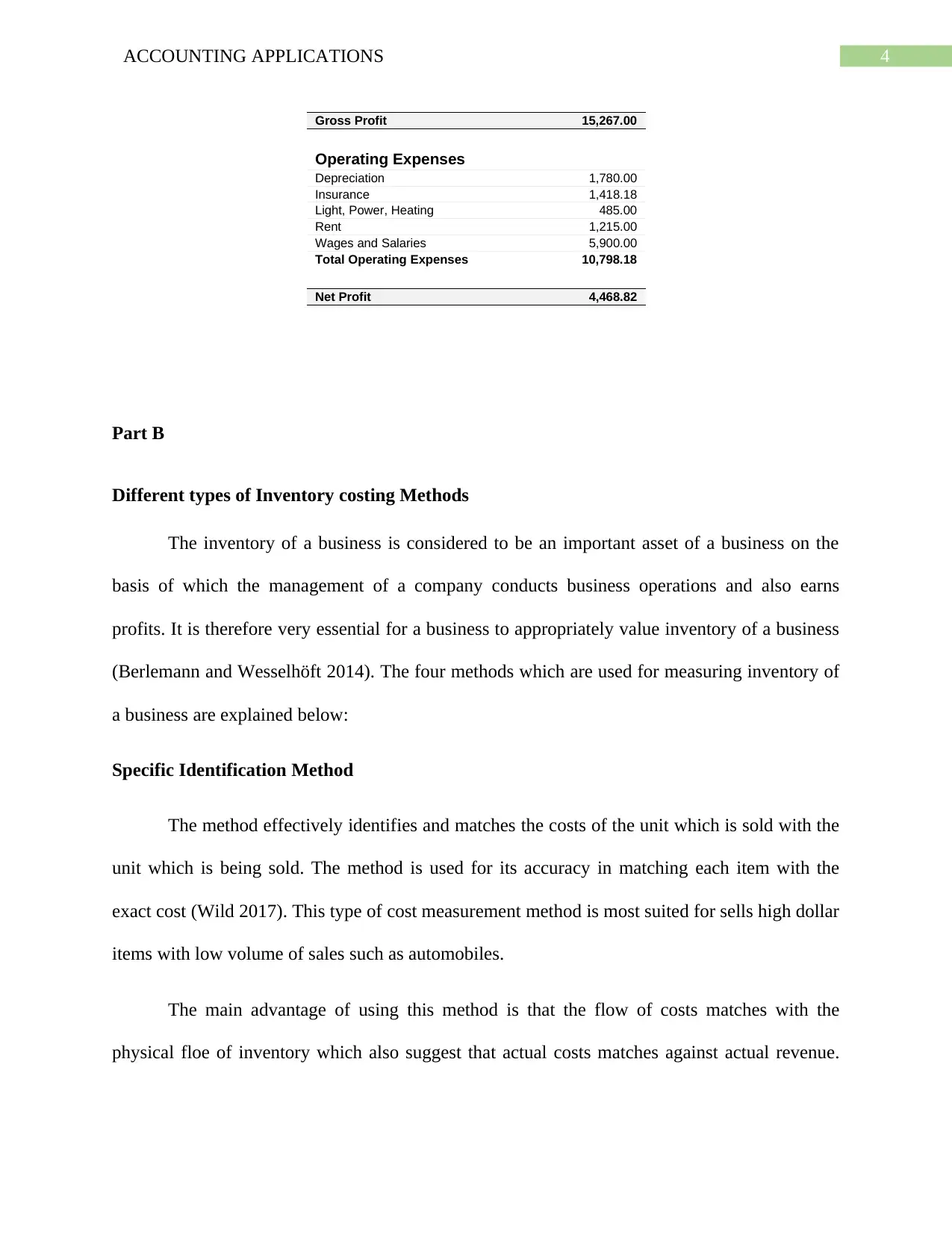

This report, prepared for an accounting course, delves into the application of accounting principles and the analysis of financial statements. Part A presents an aged payables summary, aged receivables summary, a balance sheet, and a profit and loss statement for Outback Camping Supplies Ltd. Part B focuses on different inventory costing methods, including specific identification, FIFO, LIFO, and weighted average methods, comparing their advantages and disadvantages. The report emphasizes the importance of appropriate inventory valuation and concludes that LIFO method is appropriate for valuing inventory. The report also includes references to support the analysis and findings, offering a comprehensive overview of accounting applications and inventory management.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.