Accounting Assignment

VerifiedAdded on 2023/06/15

|7

|1625

|160

AI Summary

This Accounting Assignment includes solved questions in excel file, Cost-Volume-profit Graph, Break-even point, Quality of Income, Income over cash flow from operations, AAP's financial metrics and comparing performance measures.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: ACCOUNTING ASSIGNMENT

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting Assignment 1

Part 1

Question 1-4 solved in excel file

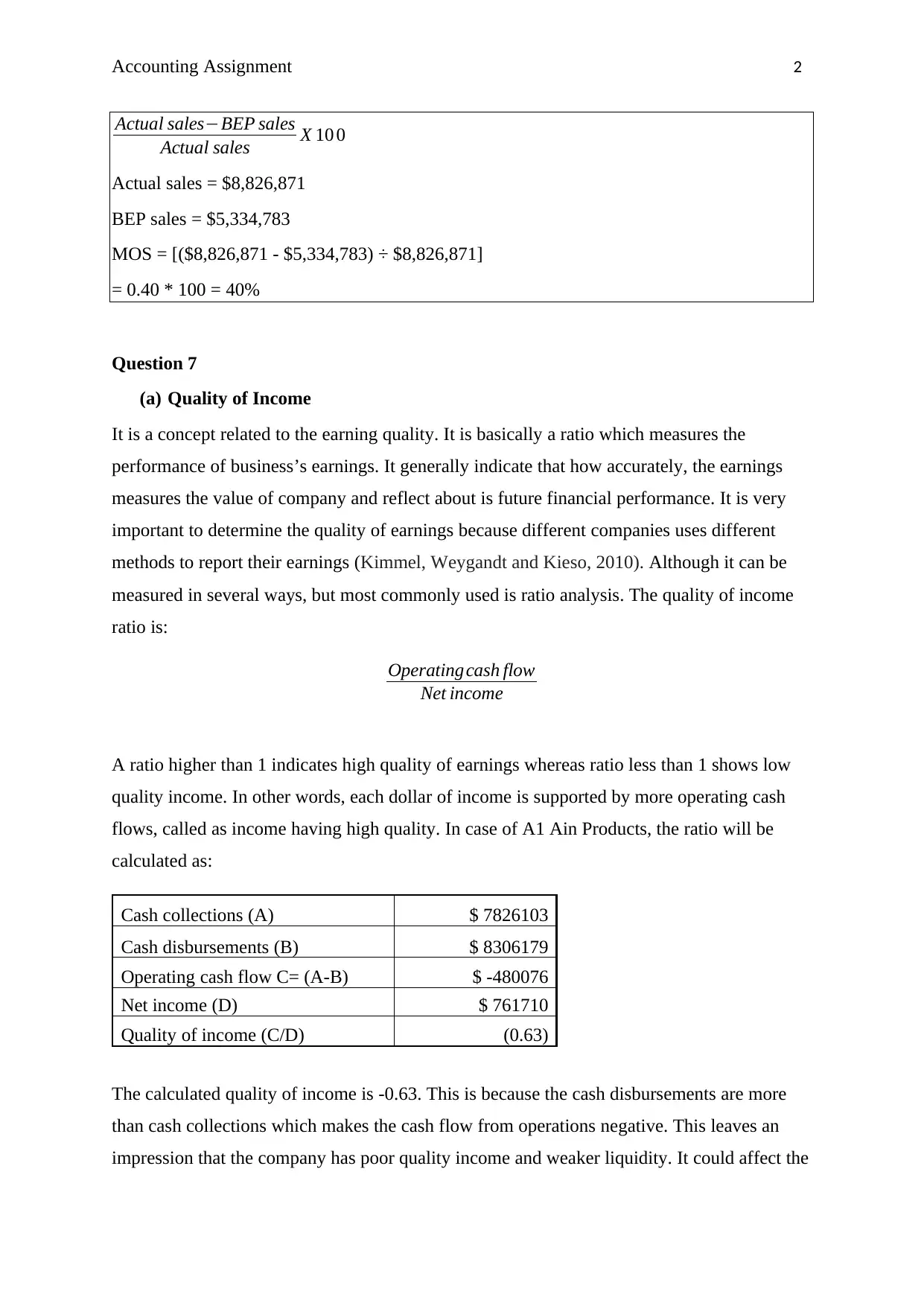

Question 5

Cost-Volume-profit Graph

- 5,000 10,000 15,000 20,000 25,000 30,000

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

$9,000,000

A1 Ain Products

Revenue Fixed Costs Total Costs

Units

Dollars

Question 6

Break-even point in sales dollar is calculated by dividing the firm’s fixed expenses with its

contribution margin ratio. The ratio is a difference between company’s sales and variable

expenses, described in percentage form (Rajasekaran, 2010).

Sales = $8,826,871

Variable expenses = $6,831,399

Contribution Margin = ($8,826,871 - $6,831,399) ÷ $8,826,871

= 0.23

Fixed expenses = $1,227,000

BEP in sales dollar = ($1,227,000 ÷ 0.23) = $5,334,783

Margin of safety ratio is calculated by subtracting BEP sales from actual sales and then

dividing the amount with current sales level. The formula is as follows:

Part 1

Question 1-4 solved in excel file

Question 5

Cost-Volume-profit Graph

- 5,000 10,000 15,000 20,000 25,000 30,000

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

$9,000,000

A1 Ain Products

Revenue Fixed Costs Total Costs

Units

Dollars

Question 6

Break-even point in sales dollar is calculated by dividing the firm’s fixed expenses with its

contribution margin ratio. The ratio is a difference between company’s sales and variable

expenses, described in percentage form (Rajasekaran, 2010).

Sales = $8,826,871

Variable expenses = $6,831,399

Contribution Margin = ($8,826,871 - $6,831,399) ÷ $8,826,871

= 0.23

Fixed expenses = $1,227,000

BEP in sales dollar = ($1,227,000 ÷ 0.23) = $5,334,783

Margin of safety ratio is calculated by subtracting BEP sales from actual sales and then

dividing the amount with current sales level. The formula is as follows:

Accounting Assignment 2

Actual sales−BEP sales

Actual sales X 10 0

Actual sales = $8,826,871

BEP sales = $5,334,783

MOS = [($8,826,871 - $5,334,783) ÷ $8,826,871]

= 0.40 * 100 = 40%

Question 7

(a) Quality of Income

It is a concept related to the earning quality. It is basically a ratio which measures the

performance of business’s earnings. It generally indicate that how accurately, the earnings

measures the value of company and reflect about is future financial performance. It is very

important to determine the quality of earnings because different companies uses different

methods to report their earnings (Kimmel, Weygandt and Kieso, 2010). Although it can be

measured in several ways, but most commonly used is ratio analysis. The quality of income

ratio is:

Operatingcash flow

Net income

A ratio higher than 1 indicates high quality of earnings whereas ratio less than 1 shows low

quality income. In other words, each dollar of income is supported by more operating cash

flows, called as income having high quality. In case of A1 Ain Products, the ratio will be

calculated as:

Cash collections (A) $ 7826103

Cash disbursements (B) $ 8306179

Operating cash flow C= (A-B) $ -480076

Net income (D) $ 761710

Quality of income (C/D) (0.63)

The calculated quality of income is -0.63. This is because the cash disbursements are more

than cash collections which makes the cash flow from operations negative. This leaves an

impression that the company has poor quality income and weaker liquidity. It could affect the

Actual sales−BEP sales

Actual sales X 10 0

Actual sales = $8,826,871

BEP sales = $5,334,783

MOS = [($8,826,871 - $5,334,783) ÷ $8,826,871]

= 0.40 * 100 = 40%

Question 7

(a) Quality of Income

It is a concept related to the earning quality. It is basically a ratio which measures the

performance of business’s earnings. It generally indicate that how accurately, the earnings

measures the value of company and reflect about is future financial performance. It is very

important to determine the quality of earnings because different companies uses different

methods to report their earnings (Kimmel, Weygandt and Kieso, 2010). Although it can be

measured in several ways, but most commonly used is ratio analysis. The quality of income

ratio is:

Operatingcash flow

Net income

A ratio higher than 1 indicates high quality of earnings whereas ratio less than 1 shows low

quality income. In other words, each dollar of income is supported by more operating cash

flows, called as income having high quality. In case of A1 Ain Products, the ratio will be

calculated as:

Cash collections (A) $ 7826103

Cash disbursements (B) $ 8306179

Operating cash flow C= (A-B) $ -480076

Net income (D) $ 761710

Quality of income (C/D) (0.63)

The calculated quality of income is -0.63. This is because the cash disbursements are more

than cash collections which makes the cash flow from operations negative. This leaves an

impression that the company has poor quality income and weaker liquidity. It could affect the

Accounting Assignment 3

firm’s financial position to a great extent in future and also its shareholders. The earnings are

not able to generate positive cash flow, which may lead to insolvency in future.

(b) Income over cash flow from operations

Cash flow inflow and outflow of cash in a business. It identifies the amount of cash used and

generated by three kind of business activities known as operating, investing and financing

activities. A company may have highest profits but still can get out of cash due to poor cash

flow (Periasamy, 2009). Net income is basically an accounting difference between the total

revenue and total expense of the firm. It is calculated by subtracting the total expenditure

from total revenue. It is generally known as profit and show the position of company’s

profitability (Knight, 2012).

As far as AAP is concerned, its cash flow from operations is negative that is $ -480076 and

its net income is positive that is $ 761710. This shows that the net income or profit earned is

higher than the cash flow. Reason behind this is lower inventory and higher accounts

receivables at the end, as compared to both the industry average and key competitors. This

raises the probability of making improvements in inventory management and cash

conversions.

The main three components of working capital are accounts receivables, inventories and

accounts payable. Looking at the cash flow statement of A1 Ain Products from external

format, it can be said that company is not using the cash effectively in all these three areas

(Sagner, 2010). The accounts receivables has been increased during the three months which

indicates that company is not timely collecting cash from its debtors. On the other hand,

amount of inventory has also boosted up which reflects that AAP is holding a lot of cash in

its inventory and also have a poor inventory management system. An increase is also noticed

in the accounts payable known as creditors. This is because company’s operations does not

generate enough cash, to set off the creditors. Moreover, its cash collections are also less than

its cash disbursements. All this shows that, AAP may not be effectively using cash in its

business.

Question 8

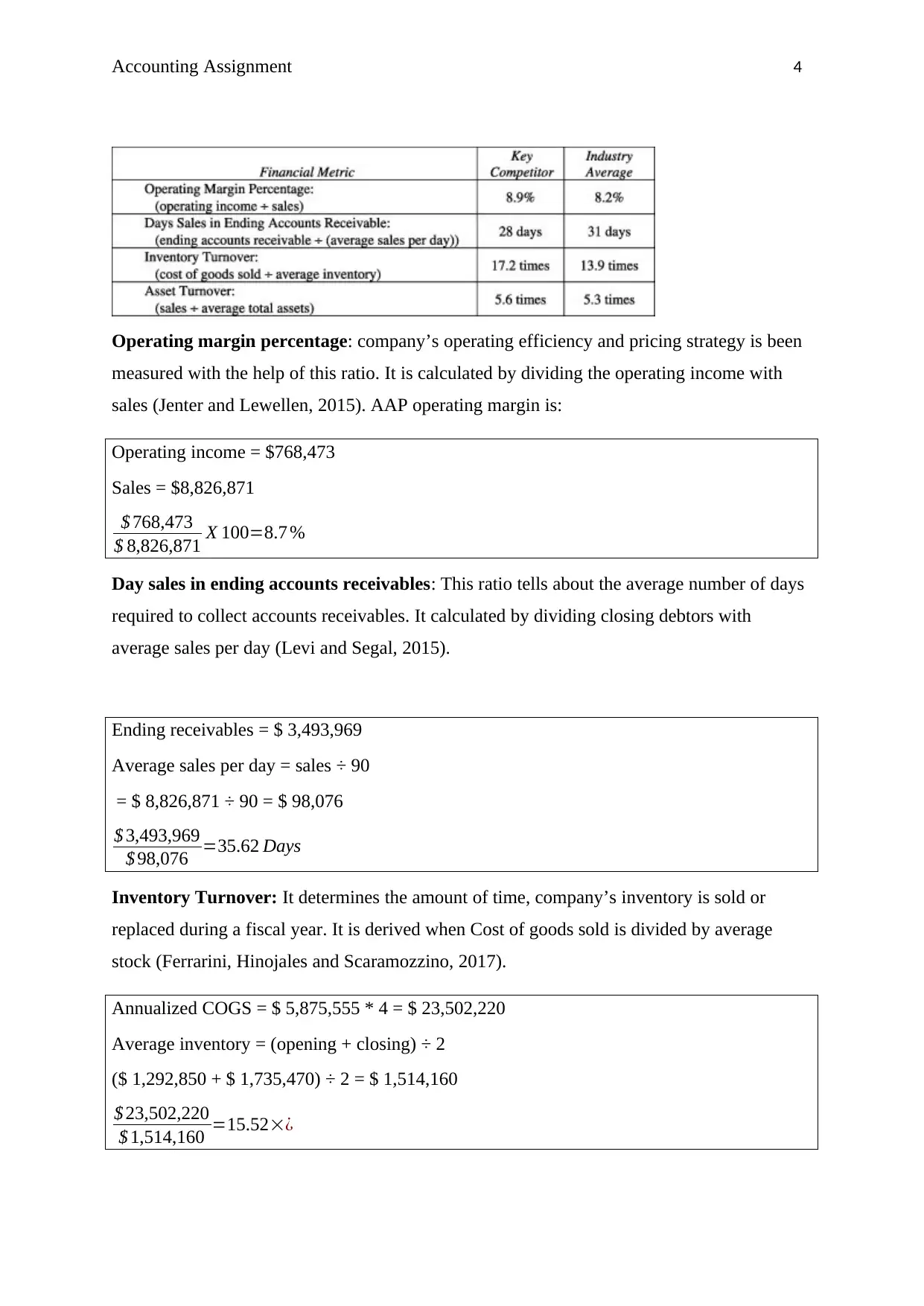

(a) AAP’s financial metrics

According to the review of benchmarking data provided, the financial metrics of AAP for the

projected quarter is been calculated. These are as follows:

firm’s financial position to a great extent in future and also its shareholders. The earnings are

not able to generate positive cash flow, which may lead to insolvency in future.

(b) Income over cash flow from operations

Cash flow inflow and outflow of cash in a business. It identifies the amount of cash used and

generated by three kind of business activities known as operating, investing and financing

activities. A company may have highest profits but still can get out of cash due to poor cash

flow (Periasamy, 2009). Net income is basically an accounting difference between the total

revenue and total expense of the firm. It is calculated by subtracting the total expenditure

from total revenue. It is generally known as profit and show the position of company’s

profitability (Knight, 2012).

As far as AAP is concerned, its cash flow from operations is negative that is $ -480076 and

its net income is positive that is $ 761710. This shows that the net income or profit earned is

higher than the cash flow. Reason behind this is lower inventory and higher accounts

receivables at the end, as compared to both the industry average and key competitors. This

raises the probability of making improvements in inventory management and cash

conversions.

The main three components of working capital are accounts receivables, inventories and

accounts payable. Looking at the cash flow statement of A1 Ain Products from external

format, it can be said that company is not using the cash effectively in all these three areas

(Sagner, 2010). The accounts receivables has been increased during the three months which

indicates that company is not timely collecting cash from its debtors. On the other hand,

amount of inventory has also boosted up which reflects that AAP is holding a lot of cash in

its inventory and also have a poor inventory management system. An increase is also noticed

in the accounts payable known as creditors. This is because company’s operations does not

generate enough cash, to set off the creditors. Moreover, its cash collections are also less than

its cash disbursements. All this shows that, AAP may not be effectively using cash in its

business.

Question 8

(a) AAP’s financial metrics

According to the review of benchmarking data provided, the financial metrics of AAP for the

projected quarter is been calculated. These are as follows:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting Assignment 4

Operating margin percentage: company’s operating efficiency and pricing strategy is been

measured with the help of this ratio. It is calculated by dividing the operating income with

sales (Jenter and Lewellen, 2015). AAP operating margin is:

Operating income = $768,473

Sales = $8,826,871

$ 768,473

$ 8,826,871 X 100=8.7 %

Day sales in ending accounts receivables: This ratio tells about the average number of days

required to collect accounts receivables. It calculated by dividing closing debtors with

average sales per day (Levi and Segal, 2015).

Ending receivables = $ 3,493,969

Average sales per day = sales ÷ 90

= $ 8,826,871 ÷ 90 = $ 98,076

$ 3,493,969

$ 98,076 =35.62 Days

Inventory Turnover: It determines the amount of time, company’s inventory is sold or

replaced during a fiscal year. It is derived when Cost of goods sold is divided by average

stock (Ferrarini, Hinojales and Scaramozzino, 2017).

Annualized COGS = $ 5,875,555 * 4 = $ 23,502,220

Average inventory = (opening + closing) ÷ 2

($ 1,292,850 + $ 1,735,470) ÷ 2 = $ 1,514,160

$ 23,502,220

$ 1,514,160 =15.52׿

Operating margin percentage: company’s operating efficiency and pricing strategy is been

measured with the help of this ratio. It is calculated by dividing the operating income with

sales (Jenter and Lewellen, 2015). AAP operating margin is:

Operating income = $768,473

Sales = $8,826,871

$ 768,473

$ 8,826,871 X 100=8.7 %

Day sales in ending accounts receivables: This ratio tells about the average number of days

required to collect accounts receivables. It calculated by dividing closing debtors with

average sales per day (Levi and Segal, 2015).

Ending receivables = $ 3,493,969

Average sales per day = sales ÷ 90

= $ 8,826,871 ÷ 90 = $ 98,076

$ 3,493,969

$ 98,076 =35.62 Days

Inventory Turnover: It determines the amount of time, company’s inventory is sold or

replaced during a fiscal year. It is derived when Cost of goods sold is divided by average

stock (Ferrarini, Hinojales and Scaramozzino, 2017).

Annualized COGS = $ 5,875,555 * 4 = $ 23,502,220

Average inventory = (opening + closing) ÷ 2

($ 1,292,850 + $ 1,735,470) ÷ 2 = $ 1,514,160

$ 23,502,220

$ 1,514,160 =15.52׿

Accounting Assignment 5

Asset Turnover: It is a commonly used efficiency ratio that determined the amount of sales

generated by the use of assets. To derive it, divide sales by average assets.

Annualized Sales = $8,826,871 * 4 = $ 35,307,484

Average assets = (opening + closing) ÷ 2

($ 5,333,050 + 6,807,939) ÷ 2 = $ 6,070,495

$ 35,307,484

$ 6,070,495 =5.8׿

(b) Comparing performance measures

Starting with the operating margin ratio, AAP’s margin is 0.2% lower than its competitor.

This implies that the company does not operate efficiently. As this ratio indicates operating

efficiency, having a lower margin shows that the firm is not capable enough to control its cost

and expenses as compare to its key competitors. The day sales in ending receivables of AAP

is 35.62 days, which is higher than both its competitor and inventory average. It is 7.5 day

more than its key competitor which implies that the company is not able to collect its debtors

timely and quickly. It is not efficient enough in converting its receivables into cash.

The ITR of A1 Ain Products is almost 2% lower than its competitor but more than the

industry average. This shows that the company’s stock is moving at lower rate, which may

result in risk of inventory obsolescence and will also affect the gross profit of the firm. The

asset turnover ratio of the firm is 0.2 turns higher than its competitor which means that AAP

is pretty much good at converting its assets into cash as compare to its competitor. It is

efficiently using its assets to generate sales.

Asset Turnover: It is a commonly used efficiency ratio that determined the amount of sales

generated by the use of assets. To derive it, divide sales by average assets.

Annualized Sales = $8,826,871 * 4 = $ 35,307,484

Average assets = (opening + closing) ÷ 2

($ 5,333,050 + 6,807,939) ÷ 2 = $ 6,070,495

$ 35,307,484

$ 6,070,495 =5.8׿

(b) Comparing performance measures

Starting with the operating margin ratio, AAP’s margin is 0.2% lower than its competitor.

This implies that the company does not operate efficiently. As this ratio indicates operating

efficiency, having a lower margin shows that the firm is not capable enough to control its cost

and expenses as compare to its key competitors. The day sales in ending receivables of AAP

is 35.62 days, which is higher than both its competitor and inventory average. It is 7.5 day

more than its key competitor which implies that the company is not able to collect its debtors

timely and quickly. It is not efficient enough in converting its receivables into cash.

The ITR of A1 Ain Products is almost 2% lower than its competitor but more than the

industry average. This shows that the company’s stock is moving at lower rate, which may

result in risk of inventory obsolescence and will also affect the gross profit of the firm. The

asset turnover ratio of the firm is 0.2 turns higher than its competitor which means that AAP

is pretty much good at converting its assets into cash as compare to its competitor. It is

efficiently using its assets to generate sales.

Accounting Assignment 6

References

Ferrarini, B., Hinojales, M. and Scaramozzino, P. 2017. Leverage and Capital Structure

Determinants of Chinese Listed Companies.

Jenter, D. and Lewellen, K. 2015. CEO preferences and acquisitions. The Journal of

Finance, 70(6), pp.2813-2852.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2010. Financial accounting: tools for

business decision making. John Wiley & Sons.

Knight, F.H., 2012. Risk, uncertainty and profit. Courier Corporation.

Levi, S. and Segal, B. 2015. The Impact of Debt-Equity Reporting Classifications on the

Firm's Decision to Issue Hybrid Securities. European Accounting Review, 24(4), pp.801-822.

Periasamy, P. 2009. Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Rajasekaran, V., 2010. Cost accounting. Pearson Education India.

Sagner, J., 2010. Essentials of working capital management(Vol. 55). John Wiley & Sons.

References

Ferrarini, B., Hinojales, M. and Scaramozzino, P. 2017. Leverage and Capital Structure

Determinants of Chinese Listed Companies.

Jenter, D. and Lewellen, K. 2015. CEO preferences and acquisitions. The Journal of

Finance, 70(6), pp.2813-2852.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2010. Financial accounting: tools for

business decision making. John Wiley & Sons.

Knight, F.H., 2012. Risk, uncertainty and profit. Courier Corporation.

Levi, S. and Segal, B. 2015. The Impact of Debt-Equity Reporting Classifications on the

Firm's Decision to Issue Hybrid Securities. European Accounting Review, 24(4), pp.801-822.

Periasamy, P. 2009. Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Rajasekaran, V., 2010. Cost accounting. Pearson Education India.

Sagner, J., 2010. Essentials of working capital management(Vol. 55). John Wiley & Sons.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.