Analysis of Impairment and Lease Accounting in Financial Reporting

VerifiedAdded on 2020/05/16

|13

|2398

|124

Report

AI Summary

This report provides a comprehensive analysis of impairment and lease accounting practices, focusing on the application of relevant accounting standards. The report begins with an examination of impaired assets, specifically goodwill, and the impairment testing procedures outlined in AASB 136. It delves into the accounting treatment of impairment expenditure, including key estimates, assumptions, and the subjectivity involved in the process. The analysis extends to fair value measurement as per IFRS 13. The second part of the report assesses former accounting standards for leases, contrasting them with the views of IASB chairmen, and explaining the reasons behind the increase in off-balance sheet lease liabilities. It discusses the arguments surrounding former lease accounting standards, particularly in the airline industry, and explores the causes of the new accounting standard's unpopularity. The report concludes by highlighting the expected benefits of the new standard, emphasizing its potential to improve financial statement presentation and facilitate better-informed investment decisions. The report references AMP Limited's annual reports to illustrate practical applications of these accounting principles.

Advance Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................5

Task A..............................................................................................................................................5

Impaired Assets...........................................................................................................................5

Impairment Testing......................................................................................................................5

Accounting treatment of Impairment Expenditure......................................................................6

Key Estimates and assumption relating to impairment expenditure...........................................8

Subjectivity involved in impairment testing procedure...............................................................8

Analysis of impairment testing....................................................................................................8

New insights learned about impairment testing...........................................................................9

Fair value measurement...............................................................................................................9

Task B..............................................................................................................................................9

Assessment of former accounting standard for lease in accordance with view of chairmen of

IASB............................................................................................................................................9

The reason behind the increase in off-balance sheet lease liabilities in comparison to debt

reported on the balance sheet.......................................................................................................9

Argument relating to former accounting standard lease regarding airlines companies.............10

Reason and cause behind unpopularity of new accounting standard relating to lease..............10

Reason due to which new accounting standard is expected to be better...................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction......................................................................................................................................5

Task A..............................................................................................................................................5

Impaired Assets...........................................................................................................................5

Impairment Testing......................................................................................................................5

Accounting treatment of Impairment Expenditure......................................................................6

Key Estimates and assumption relating to impairment expenditure...........................................8

Subjectivity involved in impairment testing procedure...............................................................8

Analysis of impairment testing....................................................................................................8

New insights learned about impairment testing...........................................................................9

Fair value measurement...............................................................................................................9

Task B..............................................................................................................................................9

Assessment of former accounting standard for lease in accordance with view of chairmen of

IASB............................................................................................................................................9

The reason behind the increase in off-balance sheet lease liabilities in comparison to debt

reported on the balance sheet.......................................................................................................9

Argument relating to former accounting standard lease regarding airlines companies.............10

Reason and cause behind unpopularity of new accounting standard relating to lease..............10

Reason due to which new accounting standard is expected to be better...................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LIST OF FIGURES

Figure 1: Notes relating to Impairment of Intangibles....................................................................5

Figure 2: Impairment Loss for the year...........................................................................................6

Figure 1: Notes relating to Impairment of Intangibles....................................................................5

Figure 2: Impairment Loss for the year...........................................................................................6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

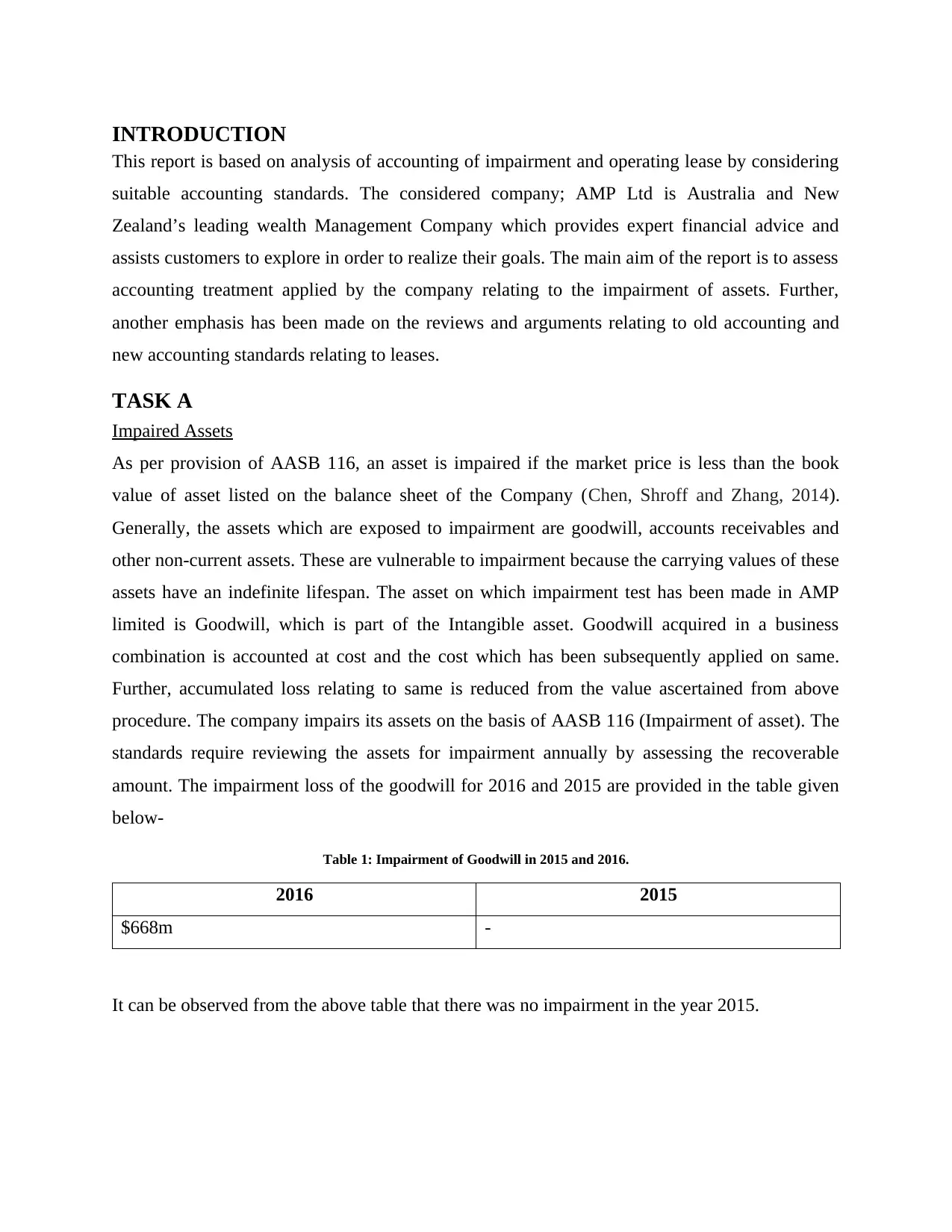

INTRODUCTION

This report is based on analysis of accounting of impairment and operating lease by considering

suitable accounting standards. The considered company; AMP Ltd is Australia and New

Zealand’s leading wealth Management Company which provides expert financial advice and

assists customers to explore in order to realize their goals. The main aim of the report is to assess

accounting treatment applied by the company relating to the impairment of assets. Further,

another emphasis has been made on the reviews and arguments relating to old accounting and

new accounting standards relating to leases.

TASK A

Impaired Assets

As per provision of AASB 116, an asset is impaired if the market price is less than the book

value of asset listed on the balance sheet of the Company (Chen, Shroff and Zhang, 2014).

Generally, the assets which are exposed to impairment are goodwill, accounts receivables and

other non-current assets. These are vulnerable to impairment because the carrying values of these

assets have an indefinite lifespan. The asset on which impairment test has been made in AMP

limited is Goodwill, which is part of the Intangible asset. Goodwill acquired in a business

combination is accounted at cost and the cost which has been subsequently applied on same.

Further, accumulated loss relating to same is reduced from the value ascertained from above

procedure. The company impairs its assets on the basis of AASB 116 (Impairment of asset). The

standards require reviewing the assets for impairment annually by assessing the recoverable

amount. The impairment loss of the goodwill for 2016 and 2015 are provided in the table given

below-

Table 1: Impairment of Goodwill in 2015 and 2016.

2016 2015

$668m -

It can be observed from the above table that there was no impairment in the year 2015.

This report is based on analysis of accounting of impairment and operating lease by considering

suitable accounting standards. The considered company; AMP Ltd is Australia and New

Zealand’s leading wealth Management Company which provides expert financial advice and

assists customers to explore in order to realize their goals. The main aim of the report is to assess

accounting treatment applied by the company relating to the impairment of assets. Further,

another emphasis has been made on the reviews and arguments relating to old accounting and

new accounting standards relating to leases.

TASK A

Impaired Assets

As per provision of AASB 116, an asset is impaired if the market price is less than the book

value of asset listed on the balance sheet of the Company (Chen, Shroff and Zhang, 2014).

Generally, the assets which are exposed to impairment are goodwill, accounts receivables and

other non-current assets. These are vulnerable to impairment because the carrying values of these

assets have an indefinite lifespan. The asset on which impairment test has been made in AMP

limited is Goodwill, which is part of the Intangible asset. Goodwill acquired in a business

combination is accounted at cost and the cost which has been subsequently applied on same.

Further, accumulated loss relating to same is reduced from the value ascertained from above

procedure. The company impairs its assets on the basis of AASB 116 (Impairment of asset). The

standards require reviewing the assets for impairment annually by assessing the recoverable

amount. The impairment loss of the goodwill for 2016 and 2015 are provided in the table given

below-

Table 1: Impairment of Goodwill in 2015 and 2016.

2016 2015

$668m -

It can be observed from the above table that there was no impairment in the year 2015.

Impairment Testing

AASB 136 has provided provision relating to impairment test that Companies must comply in

order to identify the recoverable amount of assets (Huikku, Mouritsen and Silvola, 2017). For

testing the assets for impairment is important to assess the useful life of the asset. For the

purpose of investment testing, the goodwill that is acquired in a business merger is allocated to

the cash generating units which are expected to benefit the organization in long-term future.

Each unit is to which the goodwill is allocated must be represented at the lowest level in the

entity and must be monitored for the purpose of internal management. The company has

followed the all the procedures of AASB 136 procedure for testing the assets for impairment.

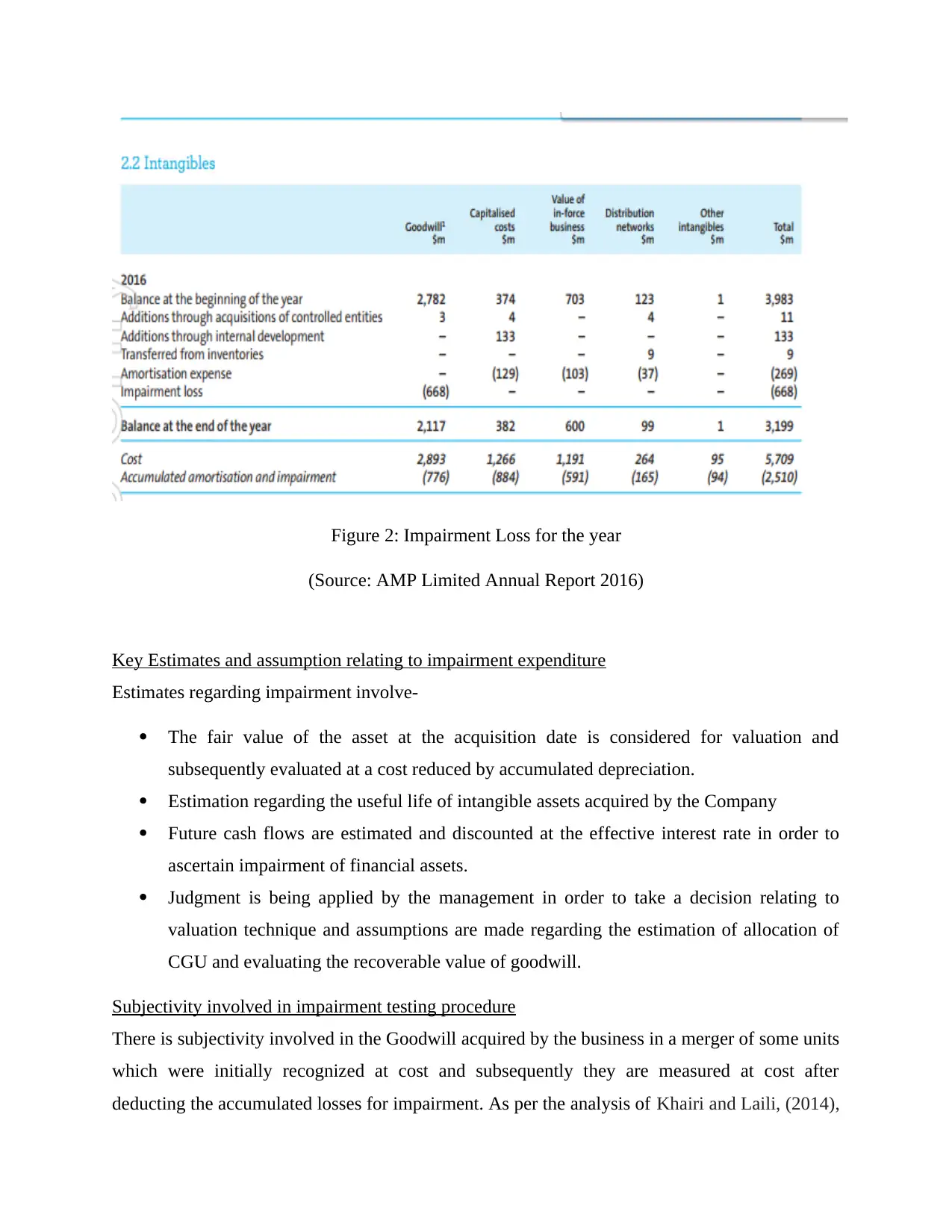

Figure 1: Notes relating to Impairment of Intangibles

(Source: AMP Limited Annual Report, 2016)

Accounting treatment of Impairment Expenditure

The impairment expenditure of the Company of the year 2016 was $668m. Carlin and Finch

(2010), asserted that impairment loss is measured by variation between the carrying amount of

asset and its present recoverable value discounted at effective tax rate (AMP Limited Annual

AASB 136 has provided provision relating to impairment test that Companies must comply in

order to identify the recoverable amount of assets (Huikku, Mouritsen and Silvola, 2017). For

testing the assets for impairment is important to assess the useful life of the asset. For the

purpose of investment testing, the goodwill that is acquired in a business merger is allocated to

the cash generating units which are expected to benefit the organization in long-term future.

Each unit is to which the goodwill is allocated must be represented at the lowest level in the

entity and must be monitored for the purpose of internal management. The company has

followed the all the procedures of AASB 136 procedure for testing the assets for impairment.

Figure 1: Notes relating to Impairment of Intangibles

(Source: AMP Limited Annual Report, 2016)

Accounting treatment of Impairment Expenditure

The impairment expenditure of the Company of the year 2016 was $668m. Carlin and Finch

(2010), asserted that impairment loss is measured by variation between the carrying amount of

asset and its present recoverable value discounted at effective tax rate (AMP Limited Annual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

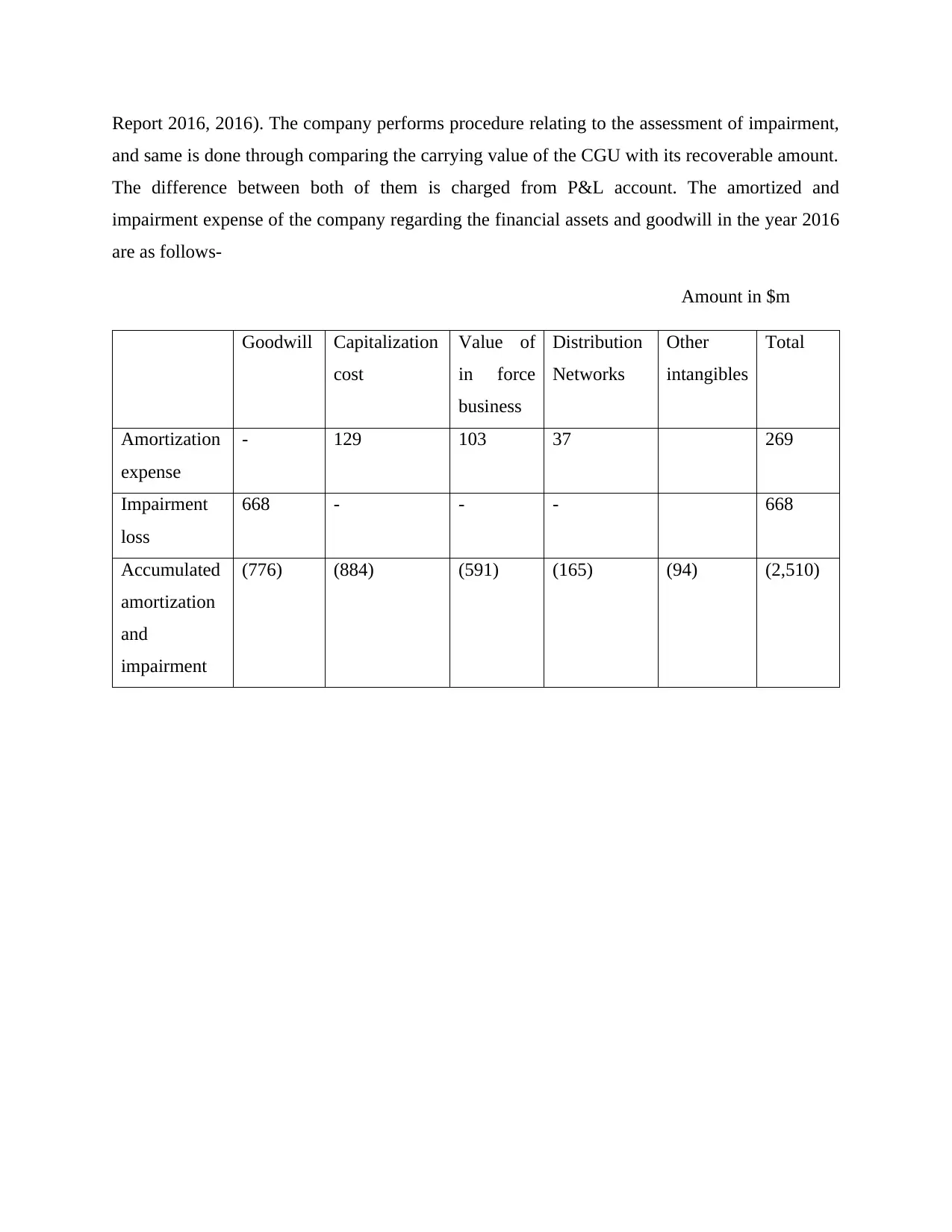

Report 2016, 2016). The company performs procedure relating to the assessment of impairment,

and same is done through comparing the carrying value of the CGU with its recoverable amount.

The difference between both of them is charged from P&L account. The amortized and

impairment expense of the company regarding the financial assets and goodwill in the year 2016

are as follows-

Amount in $m

Goodwill Capitalization

cost

Value of

in force

business

Distribution

Networks

Other

intangibles

Total

Amortization

expense

- 129 103 37 269

Impairment

loss

668 - - - 668

Accumulated

amortization

and

impairment

(776) (884) (591) (165) (94) (2,510)

and same is done through comparing the carrying value of the CGU with its recoverable amount.

The difference between both of them is charged from P&L account. The amortized and

impairment expense of the company regarding the financial assets and goodwill in the year 2016

are as follows-

Amount in $m

Goodwill Capitalization

cost

Value of

in force

business

Distribution

Networks

Other

intangibles

Total

Amortization

expense

- 129 103 37 269

Impairment

loss

668 - - - 668

Accumulated

amortization

and

impairment

(776) (884) (591) (165) (94) (2,510)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Impairment Loss for the year

(Source: AMP Limited Annual Report 2016)

Key Estimates and assumption relating to impairment expenditure

Estimates regarding impairment involve-

The fair value of the asset at the acquisition date is considered for valuation and

subsequently evaluated at a cost reduced by accumulated depreciation.

Estimation regarding the useful life of intangible assets acquired by the Company

Future cash flows are estimated and discounted at the effective interest rate in order to

ascertain impairment of financial assets.

Judgment is being applied by the management in order to take a decision relating to

valuation technique and assumptions are made regarding the estimation of allocation of

CGU and evaluating the recoverable value of goodwill.

Subjectivity involved in impairment testing procedure

There is subjectivity involved in the Goodwill acquired by the business in a merger of some units

which were initially recognized at cost and subsequently they are measured at cost after

deducting the accumulated losses for impairment. As per the analysis of Khairi and Laili, (2014),

(Source: AMP Limited Annual Report 2016)

Key Estimates and assumption relating to impairment expenditure

Estimates regarding impairment involve-

The fair value of the asset at the acquisition date is considered for valuation and

subsequently evaluated at a cost reduced by accumulated depreciation.

Estimation regarding the useful life of intangible assets acquired by the Company

Future cash flows are estimated and discounted at the effective interest rate in order to

ascertain impairment of financial assets.

Judgment is being applied by the management in order to take a decision relating to

valuation technique and assumptions are made regarding the estimation of allocation of

CGU and evaluating the recoverable value of goodwill.

Subjectivity involved in impairment testing procedure

There is subjectivity involved in the Goodwill acquired by the business in a merger of some units

which were initially recognized at cost and subsequently they are measured at cost after

deducting the accumulated losses for impairment. As per the analysis of Khairi and Laili, (2014),

the Costs of financial assets are capitalized when the asset is created and is capable of delivering

future benefit to the Company. These costs are amortized on the straight-line basis over the

useful life of the asset.

Analysis of impairment testing

On the basis of present analysis; I get to know that impairment testing is significant for

companies as it assist fair disclosure of assets in books of accounts in accordance with their

market value. Interest aspects regarding impairment testing of intangible assets such as the

Goodwill and other assets like distribution networks have a useful life for an indefinite period,

and they are annually tested for impairment. Other intangible assets like the value in force of

business are tested for impairment whenever there are any events or circumstances that indicate

the recoverability of the carrying amount. However; computation and analysis of impairment

loss are bit complex process as the recognition of impairment loss is done when the carrying

amount of asset exceeds the recoverable amount (Khokan, Rahman and Taher, 2014). Analysis

of impairment testing procedure of the Company shows that impairment in the unit of Australian

Wealth Protection; the same is fully impaired which has resulted in an expense of $668m in

2016.

New insights learned about impairment testing

Roberts (2015) asserted that assets are grouped where they cannot be identified individually for

the purpose of impairment. For the purpose of impairment of financial assets, if they are

measured at fair value, the changes in the same are reflected in the consolidated Income

statement, and they are not subjected to any impairment testing. During the assessment I learned

that in case the financial assets are measured at amortized cost, like loans and advances, maturity

investments and other such receivables, then the impairment in these cases is reflected in the

Income statement only when the Group has evidence for the loss incurred.

Fair value measurement

Provisions of IFRS 13 Fair Value Measurement is applicable to accounting transactions that

require fair value measurements or disclosures regarding the same. This standard provides a

framework for measuring fair value and assist with the disclosure of the same. The company

takes in to account the fair value measurement for impairment of intangible assets. For instance,

the in-force business value reflects the fair value of the business in the future that may arise from

future benefit to the Company. These costs are amortized on the straight-line basis over the

useful life of the asset.

Analysis of impairment testing

On the basis of present analysis; I get to know that impairment testing is significant for

companies as it assist fair disclosure of assets in books of accounts in accordance with their

market value. Interest aspects regarding impairment testing of intangible assets such as the

Goodwill and other assets like distribution networks have a useful life for an indefinite period,

and they are annually tested for impairment. Other intangible assets like the value in force of

business are tested for impairment whenever there are any events or circumstances that indicate

the recoverability of the carrying amount. However; computation and analysis of impairment

loss are bit complex process as the recognition of impairment loss is done when the carrying

amount of asset exceeds the recoverable amount (Khokan, Rahman and Taher, 2014). Analysis

of impairment testing procedure of the Company shows that impairment in the unit of Australian

Wealth Protection; the same is fully impaired which has resulted in an expense of $668m in

2016.

New insights learned about impairment testing

Roberts (2015) asserted that assets are grouped where they cannot be identified individually for

the purpose of impairment. For the purpose of impairment of financial assets, if they are

measured at fair value, the changes in the same are reflected in the consolidated Income

statement, and they are not subjected to any impairment testing. During the assessment I learned

that in case the financial assets are measured at amortized cost, like loans and advances, maturity

investments and other such receivables, then the impairment in these cases is reflected in the

Income statement only when the Group has evidence for the loss incurred.

Fair value measurement

Provisions of IFRS 13 Fair Value Measurement is applicable to accounting transactions that

require fair value measurements or disclosures regarding the same. This standard provides a

framework for measuring fair value and assist with the disclosure of the same. The company

takes in to account the fair value measurement for impairment of intangible assets. For instance,

the in-force business value reflects the fair value of the business in the future that may arise from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

current contractual arrangements and other business combination. This value is subjected to

impairment and is initially measured at market value, and later the impairment is recorded with

the difference in carrying amount and the market value.

TASK B

Assessment of former accounting standard for lease in accordance with view of chairmen of

IASB

In accordance with views presented by the chairman of IASB provision of former accounting

standard of the lease is not able to represent the economic reality of organization to which it

applies. The reason behind the same is that as per the applicable provision operating lease were

recorded as an off-balance-sheet item, but the fact cannot be denied that they create real

liabilities. Thus, the users of the financial statement were not able to access the actual picture of

the organization.

The reason behind the increase in off-balance sheet lease liabilities in comparison to debt

reported on the balance sheet.

The main reason for the same is that like 85% of the total lease were operating lease and due to

this they were accounted as off-balance sheet item and not recorded on the balance sheet. Thus,

the debt which was presented as off-balance sheet item was 66 times greater than the about

present as debt in the balance sheet. In case an asset is acquired through debt financing; liability

relating to same is accounted in the financial statement. However, in case an asset is leased, no

liability is created even though the company is legally obliged to make a future payment relating

to lease. Due to same higher difference can be assessed between debt presented in off-balance

sheet item and debt reported in Balance Sheet.

Argument relating to former accounting standard lease regarding airlines companies

As the details relating to lease were not provided in the balance sheet and major of information

relating to operating lease was provided as off-balance sheet item; in the airline industry, the

fleet was represented in a different manner even though in reality the financial obligations were

same. Thus, investors were not able to compare the existing information available in financial

statements (Edman, 2014). Due to this appropriate investment decision were not made by them

on the basis of information provided in financial statements.

impairment and is initially measured at market value, and later the impairment is recorded with

the difference in carrying amount and the market value.

TASK B

Assessment of former accounting standard for lease in accordance with view of chairmen of

IASB

In accordance with views presented by the chairman of IASB provision of former accounting

standard of the lease is not able to represent the economic reality of organization to which it

applies. The reason behind the same is that as per the applicable provision operating lease were

recorded as an off-balance-sheet item, but the fact cannot be denied that they create real

liabilities. Thus, the users of the financial statement were not able to access the actual picture of

the organization.

The reason behind the increase in off-balance sheet lease liabilities in comparison to debt

reported on the balance sheet.

The main reason for the same is that like 85% of the total lease were operating lease and due to

this they were accounted as off-balance sheet item and not recorded on the balance sheet. Thus,

the debt which was presented as off-balance sheet item was 66 times greater than the about

present as debt in the balance sheet. In case an asset is acquired through debt financing; liability

relating to same is accounted in the financial statement. However, in case an asset is leased, no

liability is created even though the company is legally obliged to make a future payment relating

to lease. Due to same higher difference can be assessed between debt presented in off-balance

sheet item and debt reported in Balance Sheet.

Argument relating to former accounting standard lease regarding airlines companies

As the details relating to lease were not provided in the balance sheet and major of information

relating to operating lease was provided as off-balance sheet item; in the airline industry, the

fleet was represented in a different manner even though in reality the financial obligations were

same. Thus, investors were not able to compare the existing information available in financial

statements (Edman, 2014). Due to this appropriate investment decision were not made by them

on the basis of information provided in financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reason and cause behind unpopularity of new accounting standard relating to lease

The reasons and cause behind unpopularity of new accounting standard relating to lease as

follows:

Removal of cosmetic accounting benefits.

The cost will be applied in order to update system for implementing new accounting

standard.

Reason due to which new accounting standard is expected to be better

In accordance with the provisions of IFRS 16; companies will be able to develop accounting

policies in which leases will be reflected in the balance sheet irrespective of industry in which

they operate. This will result in the better presentation of financial statements, and other reasons

due to which new accounting standard is expected to be better are enumerated as below:

IFRS 16 will not put leasing industry out of business and lease will remain a flexible

source of finance.

Asset and liabilities for the short term will not require complying with the provision.

The new provision will lead to making a better decision as an investor will know about

the actual economic condition of organization (Edman, 2014).

New AS will lead to efficient capital allocation which will assist in economic growth.

CONCLUSION

The study depicts that treatment of impairment of asset is the easy and interesting procedure.

Companies are required to conduct impairment testing at regular time intervals to ensure values

of assets are reflected in fair value, and financial statements are providing viable disclosure of

financial information. Further, the second part of the report depicts that new accounting standard

relating to the lease of assets will lead to a better informed investment decision by investors and

through same management will be able to take appropriate buy decision. It is because; it will

assist better disclosure of financial information by considering off-balance sheet items as well.

The reasons and cause behind unpopularity of new accounting standard relating to lease as

follows:

Removal of cosmetic accounting benefits.

The cost will be applied in order to update system for implementing new accounting

standard.

Reason due to which new accounting standard is expected to be better

In accordance with the provisions of IFRS 16; companies will be able to develop accounting

policies in which leases will be reflected in the balance sheet irrespective of industry in which

they operate. This will result in the better presentation of financial statements, and other reasons

due to which new accounting standard is expected to be better are enumerated as below:

IFRS 16 will not put leasing industry out of business and lease will remain a flexible

source of finance.

Asset and liabilities for the short term will not require complying with the provision.

The new provision will lead to making a better decision as an investor will know about

the actual economic condition of organization (Edman, 2014).

New AS will lead to efficient capital allocation which will assist in economic growth.

CONCLUSION

The study depicts that treatment of impairment of asset is the easy and interesting procedure.

Companies are required to conduct impairment testing at regular time intervals to ensure values

of assets are reflected in fair value, and financial statements are providing viable disclosure of

financial information. Further, the second part of the report depicts that new accounting standard

relating to the lease of assets will lead to a better informed investment decision by investors and

through same management will be able to take appropriate buy decision. It is because; it will

assist better disclosure of financial information by considering off-balance sheet items as well.

REFERENCES

AMP Limited Annual Report 2016. 2016. [PDF]. Available through <

https://www.asx.com.au/asxpdf/20170320/pdf/43gx9bppxvx00n.pdf>. [Accessed on 25th

January 2018].

Carlin, T.M. and Finch, N., 2010. Resisting compliance with IFRS goodwill accounting and

reporting disclosures: Evidence from Australia. Journal of Accounting & Organizational

Change, 6(2), Pp.260-280.

Chen, W., Shroff, P.K. and Zhang, I., 2014. Fair Value Accounting: Consequences of Booking

Market-driven Goodwill Impairment.

Edman B. Leases: Off-Balance Sheet Financing and the Strive for Transparency Today. (2014).

[PDF]. Available through < http://digitalcommons.liberty.edu/cgi/viewcontent.cgi?

article=1247&context=honors>. [Accessed on 25th January 2018]

Huikku, J., Mouritsen, J. and Silvola, H., 2017. Relative reliability and the recognisable firm:

Calculating goodwill impairment value. Accounting, Organizations and Society, 56, pp.68-83.

Khairi, K.F. and Laili, N.H., 2014. Goodwill Impairment Disclosures: A Test for IFRS

Compliance in Malaysia.

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting & Organizational Change, 10(1),

Pp.116-149.

Roberts, R.A., 2015. Goodwill Impairment: A study of Australian Companies 2007-2013.

AMP Limited Annual Report 2016. 2016. [PDF]. Available through <

https://www.asx.com.au/asxpdf/20170320/pdf/43gx9bppxvx00n.pdf>. [Accessed on 25th

January 2018].

Carlin, T.M. and Finch, N., 2010. Resisting compliance with IFRS goodwill accounting and

reporting disclosures: Evidence from Australia. Journal of Accounting & Organizational

Change, 6(2), Pp.260-280.

Chen, W., Shroff, P.K. and Zhang, I., 2014. Fair Value Accounting: Consequences of Booking

Market-driven Goodwill Impairment.

Edman B. Leases: Off-Balance Sheet Financing and the Strive for Transparency Today. (2014).

[PDF]. Available through < http://digitalcommons.liberty.edu/cgi/viewcontent.cgi?

article=1247&context=honors>. [Accessed on 25th January 2018]

Huikku, J., Mouritsen, J. and Silvola, H., 2017. Relative reliability and the recognisable firm:

Calculating goodwill impairment value. Accounting, Organizations and Society, 56, pp.68-83.

Khairi, K.F. and Laili, N.H., 2014. Goodwill Impairment Disclosures: A Test for IFRS

Compliance in Malaysia.

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting & Organizational Change, 10(1),

Pp.116-149.

Roberts, R.A., 2015. Goodwill Impairment: A study of Australian Companies 2007-2013.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.