Accounting Report: Financial and Management Accounting Analysis

VerifiedAdded on 2020/06/06

|17

|3401

|30

Report

AI Summary

This accounting report delves into various aspects of financial and management accounting. It begins by differentiating between financial and management accounting, explaining the roles of stakeholders, and providing examples of financial statement components. The report then analyzes key accounting concepts such as depreciation, equity, and cash flow, offering insights into their significance. It explores ratio analysis, including profitability, liquidity, and solvency ratios, and applies these concepts to a case study of Helena Beauty. Furthermore, the report addresses cost accounting topics, such as calculating variable costs, contribution margins, and break-even points. It also covers pricing strategies, the factors influencing cash management decisions, and the advantages and disadvantages of different sources of finance. The report concludes with a price quotation and a detailed financial analysis, making it a comprehensive resource for understanding accounting principles and their practical applications.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................4

QUESTION 4..................................................................................................................................5

a. Calculating the variable cost per pot........................................................................................5

b. Contribution margin per pot.....................................................................................................6

c. Calculating break-even point...................................................................................................6

d. Assessing whether company should accept or reject the order................................................6

e. Giving conclusion....................................................................................................................7

f. Calculating profit or loss for the month of May.......................................................................7

QUESTION 5..................................................................................................................................8

Preparing a price quotation..........................................................................................................8

QUESTION 6..................................................................................................................................9

a. Assessing the factors that influence the decision making of organization in relation to

holding cash within the business..................................................................................................9

b. Assessing the cost which business unit will incur on the holding of too low level of

inventory......................................................................................................................................9

C. Explain the pros and cons of retained profit source of finance.............................................10

d. Presenting the financial information that a venture capitalists needs to consider when

evaluating investment opportunities..........................................................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................12

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................4

QUESTION 4..................................................................................................................................5

a. Calculating the variable cost per pot........................................................................................5

b. Contribution margin per pot.....................................................................................................6

c. Calculating break-even point...................................................................................................6

d. Assessing whether company should accept or reject the order................................................6

e. Giving conclusion....................................................................................................................7

f. Calculating profit or loss for the month of May.......................................................................7

QUESTION 5..................................................................................................................................8

Preparing a price quotation..........................................................................................................8

QUESTION 6..................................................................................................................................9

a. Assessing the factors that influence the decision making of organization in relation to

holding cash within the business..................................................................................................9

b. Assessing the cost which business unit will incur on the holding of too low level of

inventory......................................................................................................................................9

C. Explain the pros and cons of retained profit source of finance.............................................10

d. Presenting the financial information that a venture capitalists needs to consider when

evaluating investment opportunities..........................................................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is a broad concept which is primarily concerned with

reporting and examining organizational performance for the decisive

business decisions. The current report emphasizes on various financial and

management accounting practices i.e. financial reports, ratio analysis,

budgeting, source of finance, cost calculation and others for the future

growth.

QUESTION 1

(A) Financial accounting collect, gather, organize and report only the result

of financial business activities whereas management accounting deals with

examining both the financial as well as non-financial business performance

for the decisive plans and decisions. Financial accounting reports only

provides quantitative information, for instance, P&L account reports

expenditures and income to reflect net profit whilst balance sheet provides

detail of assets and liabilities to know financial status of the firm (Edwards,

2013). In contrast, in the management accounts, receivable reports not only

inform just the outstanding debt but also inform about the due date, default

in payment and others helps in rationalized credit decisions. On the other

hand, operational reports present target set and actual result of the business

function so that management can compare both and make smart decision.

(B)

(i) Equity/ordinary shareholders are the owners of a public company. They

gain ownership by investing in the firm’s shares and getting voting rights in

the board decisions.

(ii) Lenders, venture capitalists, suppliers, consumers, employees, public,

competitor, taxation authorities and other stakeholders (Gassen, 2014)

(C)

a) Paid up capital: Equity

1

Accounting is a broad concept which is primarily concerned with

reporting and examining organizational performance for the decisive

business decisions. The current report emphasizes on various financial and

management accounting practices i.e. financial reports, ratio analysis,

budgeting, source of finance, cost calculation and others for the future

growth.

QUESTION 1

(A) Financial accounting collect, gather, organize and report only the result

of financial business activities whereas management accounting deals with

examining both the financial as well as non-financial business performance

for the decisive plans and decisions. Financial accounting reports only

provides quantitative information, for instance, P&L account reports

expenditures and income to reflect net profit whilst balance sheet provides

detail of assets and liabilities to know financial status of the firm (Edwards,

2013). In contrast, in the management accounts, receivable reports not only

inform just the outstanding debt but also inform about the due date, default

in payment and others helps in rationalized credit decisions. On the other

hand, operational reports present target set and actual result of the business

function so that management can compare both and make smart decision.

(B)

(i) Equity/ordinary shareholders are the owners of a public company. They

gain ownership by investing in the firm’s shares and getting voting rights in

the board decisions.

(ii) Lenders, venture capitalists, suppliers, consumers, employees, public,

competitor, taxation authorities and other stakeholders (Gassen, 2014)

(C)

a) Paid up capital: Equity

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Bank Loan: Liability

c) Provision for annual leave: Liability

d) Brand names and intellectual property: Assets

e) Accounts receivables: Assets

f) Prepaid insurance premium: Assets

g) Deposits paid by a consumer for work yet to be done: Liability

h) Retained profit: equity

(D)

Statement of Cash flow (SOCF) reflects change in cash balance at two

different balance sheet date however, cash budget demonstrate

whether company will have surplus or deficit of cash.

SOCF present the actual cash inflow & outflow from operational,

financing and investing activities whilst cash budget just provides

estimated result to assess future cash (Peavler, 2016).

SOCF is prepared yearly by complying with the accounting & reporting

rules like IAS & IFRS, however, cash budget is constructed for shorter

period i.e. quarterly, semi-annually without any legal obligation.

(E) Depreciation means reduction in the assets value over the time due to its

use in the business. It either can be charged following fixed method or

written down value (WDV) method. For instance, an assets at $100,000 has

been bought and estimated life is 5 year, then annual depreciation worth

($100,000/5) = $20,000 will be charged so as to reflect true value of assets

every year.

(F)

Pair Larger Reason

EBIT & Net Profit EBIT EBIT reflect profit before interest and tax

whereas net profit indicates return after

subtracting both interest and tax amount.

2

c) Provision for annual leave: Liability

d) Brand names and intellectual property: Assets

e) Accounts receivables: Assets

f) Prepaid insurance premium: Assets

g) Deposits paid by a consumer for work yet to be done: Liability

h) Retained profit: equity

(D)

Statement of Cash flow (SOCF) reflects change in cash balance at two

different balance sheet date however, cash budget demonstrate

whether company will have surplus or deficit of cash.

SOCF present the actual cash inflow & outflow from operational,

financing and investing activities whilst cash budget just provides

estimated result to assess future cash (Peavler, 2016).

SOCF is prepared yearly by complying with the accounting & reporting

rules like IAS & IFRS, however, cash budget is constructed for shorter

period i.e. quarterly, semi-annually without any legal obligation.

(E) Depreciation means reduction in the assets value over the time due to its

use in the business. It either can be charged following fixed method or

written down value (WDV) method. For instance, an assets at $100,000 has

been bought and estimated life is 5 year, then annual depreciation worth

($100,000/5) = $20,000 will be charged so as to reflect true value of assets

every year.

(F)

Pair Larger Reason

EBIT & Net Profit EBIT EBIT reflect profit before interest and tax

whereas net profit indicates return after

subtracting both interest and tax amount.

2

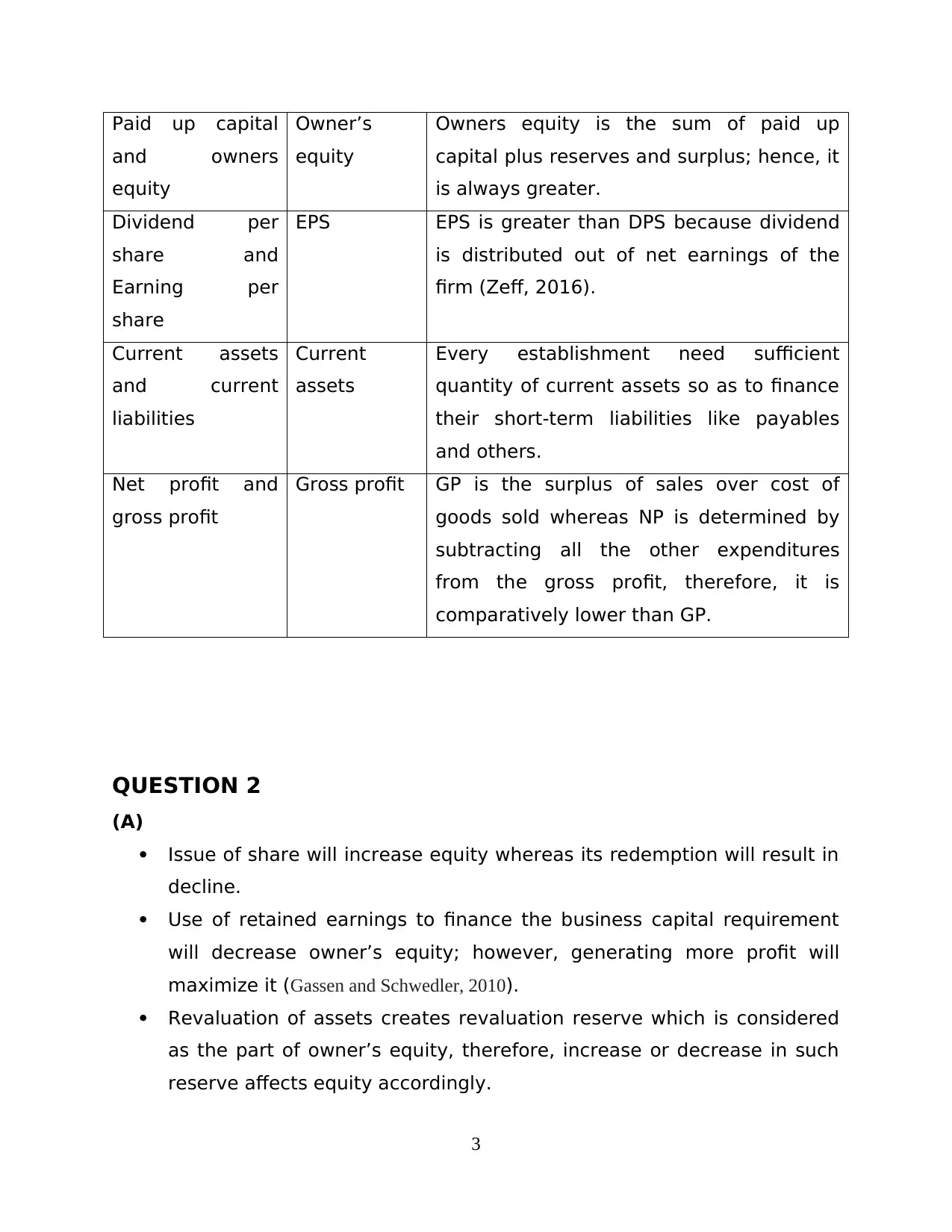

Paid up capital

and owners

equity

Owner’s

equity

Owners equity is the sum of paid up

capital plus reserves and surplus; hence, it

is always greater.

Dividend per

share and

Earning per

share

EPS EPS is greater than DPS because dividend

is distributed out of net earnings of the

firm (Zeff, 2016).

Current assets

and current

liabilities

Current

assets

Every establishment need sufficient

quantity of current assets so as to finance

their short-term liabilities like payables

and others.

Net profit and

gross profit

Gross profit GP is the surplus of sales over cost of

goods sold whereas NP is determined by

subtracting all the other expenditures

from the gross profit, therefore, it is

comparatively lower than GP.

QUESTION 2

(A)

Issue of share will increase equity whereas its redemption will result in

decline.

Use of retained earnings to finance the business capital requirement

will decrease owner’s equity; however, generating more profit will

maximize it (Gassen and Schwedler, 2010).

Revaluation of assets creates revaluation reserve which is considered

as the part of owner’s equity, therefore, increase or decrease in such

reserve affects equity accordingly.

3

and owners

equity

Owner’s

equity

Owners equity is the sum of paid up

capital plus reserves and surplus; hence, it

is always greater.

Dividend per

share and

Earning per

share

EPS EPS is greater than DPS because dividend

is distributed out of net earnings of the

firm (Zeff, 2016).

Current assets

and current

liabilities

Current

assets

Every establishment need sufficient

quantity of current assets so as to finance

their short-term liabilities like payables

and others.

Net profit and

gross profit

Gross profit GP is the surplus of sales over cost of

goods sold whereas NP is determined by

subtracting all the other expenditures

from the gross profit, therefore, it is

comparatively lower than GP.

QUESTION 2

(A)

Issue of share will increase equity whereas its redemption will result in

decline.

Use of retained earnings to finance the business capital requirement

will decrease owner’s equity; however, generating more profit will

maximize it (Gassen and Schwedler, 2010).

Revaluation of assets creates revaluation reserve which is considered

as the part of owner’s equity, therefore, increase or decrease in such

reserve affects equity accordingly.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Creating distributable reserve like general reserve will give rise to

equity whilst its use will decrease the equity balance.

(B)

To have enough funds to meet sudden capital requirement and to

prevent the business against market uncertainties

To encourage investors to invest funds in the business and if owner will

withdraw and indicate zero balance, then none of the investor will be

ready to take risk (Waegenaere, Sansing and Wielhouwer, 2015)

To satisfy all the stakeholders like fund providers, suppliers, employees

and others that business is profitable

(C)

Although debt is a cheaper financial source because of the presence of

tax shields, still, there are some consequences of it that affects financial

position, enlisted below:

Borrowing excessive funds from bank bring legal requirement for the

entity to pay instalments periodically and affects net profit

In case of inadequate return due to market externalities, firm will not

be able to meet their debt obligation, in such case, it affects market

reputation adversely.

High gearing results in poor long-term solvency as a result, company

might be unable to pay instalments inclusive of interest on time to the

lenders and may goes into bankruptcy

(D)

Reasons for negative operating cash flow

Decline in sales

High cost of sale

High operational expenditures

Increase in current assets i.e. inventory, receivables and others

Decrease in current liabilities i.e. payable

It is necessary for the managerial team of the enterprise to keep track

over daily activities and identify the reasons behind cost overrun and

4

equity whilst its use will decrease the equity balance.

(B)

To have enough funds to meet sudden capital requirement and to

prevent the business against market uncertainties

To encourage investors to invest funds in the business and if owner will

withdraw and indicate zero balance, then none of the investor will be

ready to take risk (Waegenaere, Sansing and Wielhouwer, 2015)

To satisfy all the stakeholders like fund providers, suppliers, employees

and others that business is profitable

(C)

Although debt is a cheaper financial source because of the presence of

tax shields, still, there are some consequences of it that affects financial

position, enlisted below:

Borrowing excessive funds from bank bring legal requirement for the

entity to pay instalments periodically and affects net profit

In case of inadequate return due to market externalities, firm will not

be able to meet their debt obligation, in such case, it affects market

reputation adversely.

High gearing results in poor long-term solvency as a result, company

might be unable to pay instalments inclusive of interest on time to the

lenders and may goes into bankruptcy

(D)

Reasons for negative operating cash flow

Decline in sales

High cost of sale

High operational expenditures

Increase in current assets i.e. inventory, receivables and others

Decrease in current liabilities i.e. payable

It is necessary for the managerial team of the enterprise to keep track

over daily activities and identify the reasons behind cost overrun and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decreasing revenues. They must took cost cutting decisions and monitor

staff activities to minimize the possibility of exceeding expenditures and also

make plans for the revenue maximization, so that, entity will have surplus

cash available to finance operations (Waegenaere, Sansing and Wielhouwer,

2015).

QUESTION 3

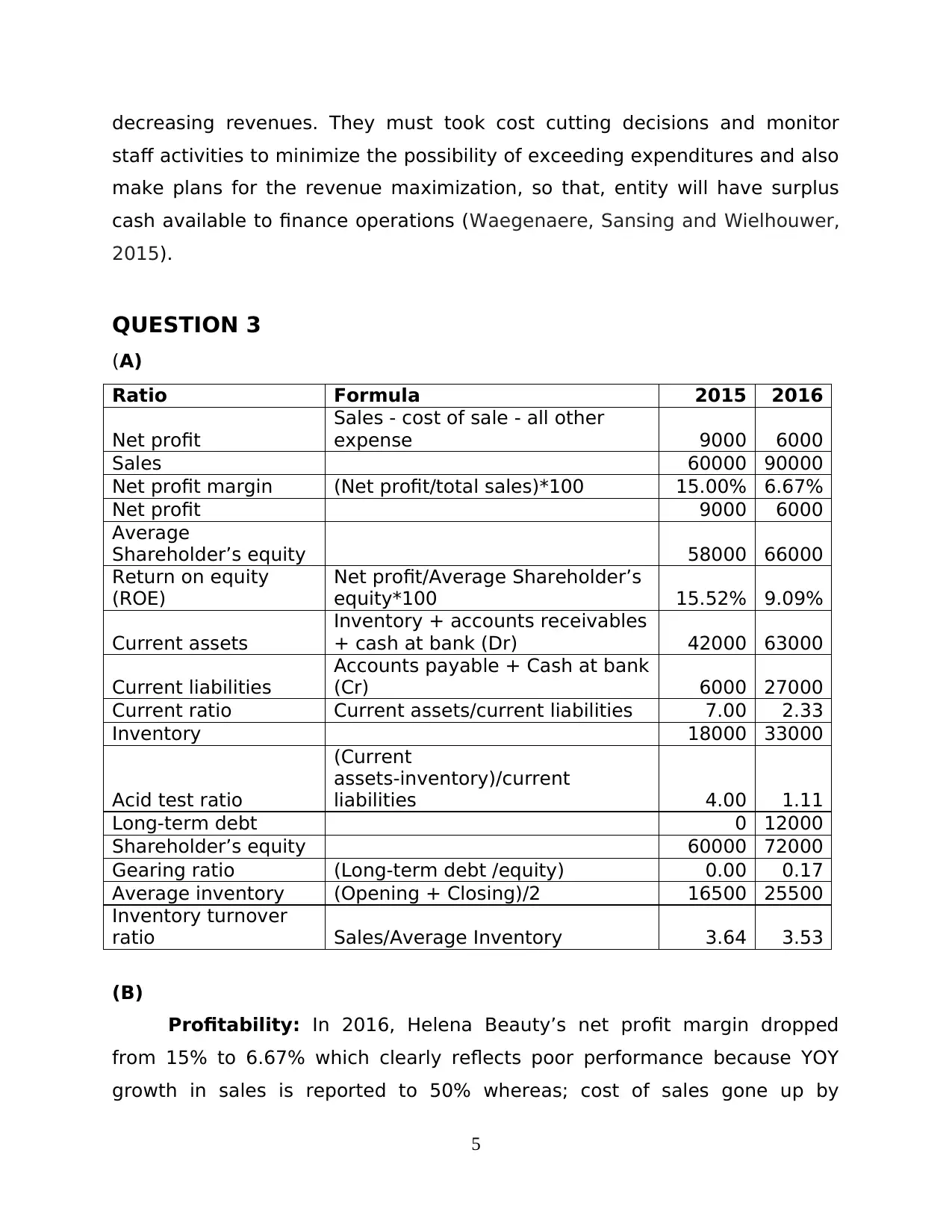

(A)

Ratio Formula 2015 2016

Net profit

Sales - cost of sale - all other

expense 9000 6000

Sales 60000 90000

Net profit margin (Net profit/total sales)*100 15.00% 6.67%

Net profit 9000 6000

Average

Shareholder’s equity 58000 66000

Return on equity

(ROE)

Net profit/Average Shareholder’s

equity*100 15.52% 9.09%

Current assets

Inventory + accounts receivables

+ cash at bank (Dr) 42000 63000

Current liabilities

Accounts payable + Cash at bank

(Cr) 6000 27000

Current ratio Current assets/current liabilities 7.00 2.33

Inventory 18000 33000

Acid test ratio

(Current

assets-inventory)/current

liabilities 4.00 1.11

Long-term debt 0 12000

Shareholder’s equity 60000 72000

Gearing ratio (Long-term debt /equity) 0.00 0.17

Average inventory (Opening + Closing)/2 16500 25500

Inventory turnover

ratio Sales/Average Inventory 3.64 3.53

(B)

Profitability: In 2016, Helena Beauty’s net profit margin dropped

from 15% to 6.67% which clearly reflects poor performance because YOY

growth in sales is reported to 50% whereas; cost of sales gone up by

5

staff activities to minimize the possibility of exceeding expenditures and also

make plans for the revenue maximization, so that, entity will have surplus

cash available to finance operations (Waegenaere, Sansing and Wielhouwer,

2015).

QUESTION 3

(A)

Ratio Formula 2015 2016

Net profit

Sales - cost of sale - all other

expense 9000 6000

Sales 60000 90000

Net profit margin (Net profit/total sales)*100 15.00% 6.67%

Net profit 9000 6000

Average

Shareholder’s equity 58000 66000

Return on equity

(ROE)

Net profit/Average Shareholder’s

equity*100 15.52% 9.09%

Current assets

Inventory + accounts receivables

+ cash at bank (Dr) 42000 63000

Current liabilities

Accounts payable + Cash at bank

(Cr) 6000 27000

Current ratio Current assets/current liabilities 7.00 2.33

Inventory 18000 33000

Acid test ratio

(Current

assets-inventory)/current

liabilities 4.00 1.11

Long-term debt 0 12000

Shareholder’s equity 60000 72000

Gearing ratio (Long-term debt /equity) 0.00 0.17

Average inventory (Opening + Closing)/2 16500 25500

Inventory turnover

ratio Sales/Average Inventory 3.64 3.53

(B)

Profitability: In 2016, Helena Beauty’s net profit margin dropped

from 15% to 6.67% which clearly reflects poor performance because YOY

growth in sales is reported to 50% whereas; cost of sales gone up by

5

61.54%. It may be due to sudden increase in supplier’s charges due to

shortage of supply and high transportation cost. In contrast, inventory

turnover ratio reflects ineffective use of stock to generate sales as it decline

from 3.64 times to 3.53 times. Besides this, operational expenses have been

increased by 75% because of poor monitoring and lack of supervision (Beatty

and Liao, 2014). Due to decrease in net earnings, ROE also came down from

15.52% to 9.09% reflects that firm did not earn good return on equity

invested.

Liquidity: Current ratio resulted down from 7:1 to 2.33:1 and acid test

ratio dropped from 4:1 to 1.11:1 in FY 2016. Although decline ratio indicates

liquidity decrease, still, the ratio is above than industrial benchmark of 2:1

and 1:1, therefore, it can be interpreted that Helena Beauty has sound

liquidity management to pay deferral short-term obligations timely (Zeff,

2016).

Long-term solvency: In 2015, business was financed only through

Helena’s own capital of $60,000 at no debt. However, in following year, firm

had taken a loan amounting to $12,000 in its capital structure which increase

gearing ratio to 0.17. The ratio reflects that financial risk is too low, as

company preferred equity as a main source of capital. Debt/equity ratio is far

below than idle ratio of 0.50:1 which encourage firm to borrow more capital

so as to take tax and trading on equity benefits.

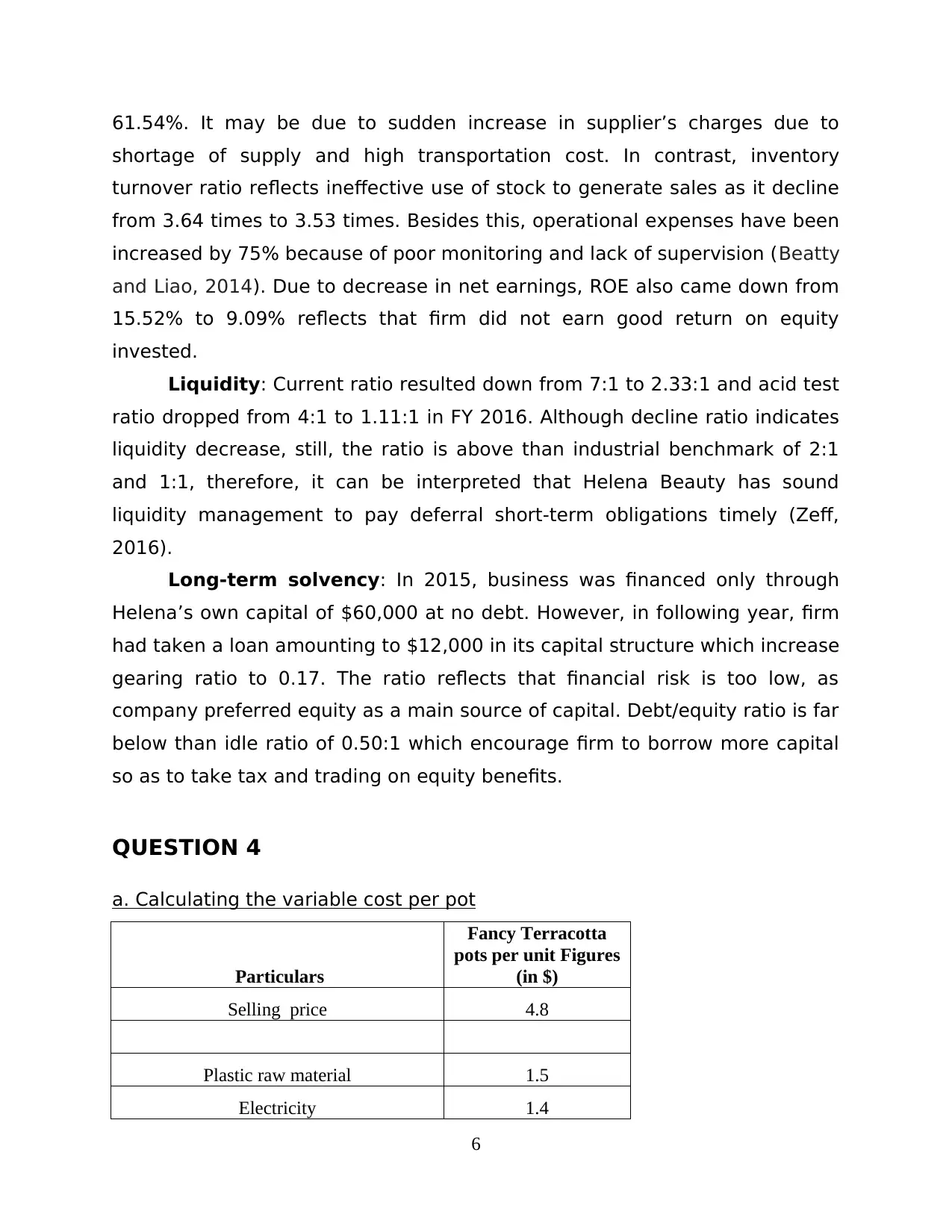

QUESTION 4

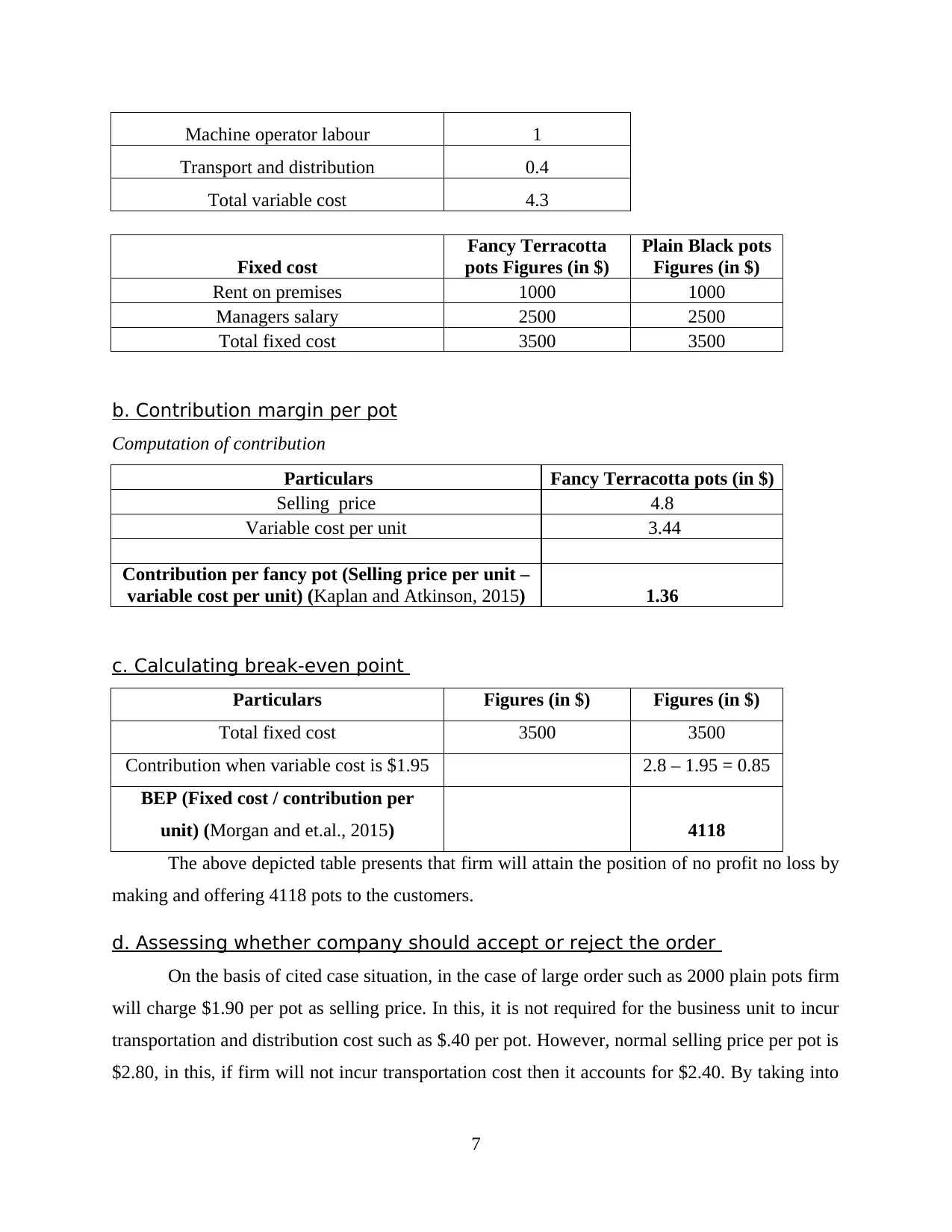

a. Calculating the variable cost per pot

Particulars

Fancy Terracotta

pots per unit Figures

(in $)

Selling price 4.8

Plastic raw material 1.5

Electricity 1.4

6

shortage of supply and high transportation cost. In contrast, inventory

turnover ratio reflects ineffective use of stock to generate sales as it decline

from 3.64 times to 3.53 times. Besides this, operational expenses have been

increased by 75% because of poor monitoring and lack of supervision (Beatty

and Liao, 2014). Due to decrease in net earnings, ROE also came down from

15.52% to 9.09% reflects that firm did not earn good return on equity

invested.

Liquidity: Current ratio resulted down from 7:1 to 2.33:1 and acid test

ratio dropped from 4:1 to 1.11:1 in FY 2016. Although decline ratio indicates

liquidity decrease, still, the ratio is above than industrial benchmark of 2:1

and 1:1, therefore, it can be interpreted that Helena Beauty has sound

liquidity management to pay deferral short-term obligations timely (Zeff,

2016).

Long-term solvency: In 2015, business was financed only through

Helena’s own capital of $60,000 at no debt. However, in following year, firm

had taken a loan amounting to $12,000 in its capital structure which increase

gearing ratio to 0.17. The ratio reflects that financial risk is too low, as

company preferred equity as a main source of capital. Debt/equity ratio is far

below than idle ratio of 0.50:1 which encourage firm to borrow more capital

so as to take tax and trading on equity benefits.

QUESTION 4

a. Calculating the variable cost per pot

Particulars

Fancy Terracotta

pots per unit Figures

(in $)

Selling price 4.8

Plastic raw material 1.5

Electricity 1.4

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Machine operator labour 1

Transport and distribution 0.4

Total variable cost 4.3

Fixed cost

Fancy Terracotta

pots Figures (in $)

Plain Black pots

Figures (in $)

Rent on premises 1000 1000

Managers salary 2500 2500

Total fixed cost 3500 3500

b. Contribution margin per pot

Computation of contribution

Particulars Fancy Terracotta pots (in $)

Selling price 4.8

Variable cost per unit 3.44

Contribution per fancy pot (Selling price per unit –

variable cost per unit) (Kaplan and Atkinson, 2015) 1.36

c. Calculating break-even point

Particulars Figures (in $) Figures (in $)

Total fixed cost 3500 3500

Contribution when variable cost is $1.95 2.8 – 1.95 = 0.85

BEP (Fixed cost / contribution per

unit) (Morgan and et.al., 2015) 4118

The above depicted table presents that firm will attain the position of no profit no loss by

making and offering 4118 pots to the customers.

d. Assessing whether company should accept or reject the order

On the basis of cited case situation, in the case of large order such as 2000 plain pots firm

will charge $1.90 per pot as selling price. In this, it is not required for the business unit to incur

transportation and distribution cost such as $.40 per pot. However, normal selling price per pot is

$2.80, in this, if firm will not incur transportation cost then it accounts for $2.40. By taking into

7

Transport and distribution 0.4

Total variable cost 4.3

Fixed cost

Fancy Terracotta

pots Figures (in $)

Plain Black pots

Figures (in $)

Rent on premises 1000 1000

Managers salary 2500 2500

Total fixed cost 3500 3500

b. Contribution margin per pot

Computation of contribution

Particulars Fancy Terracotta pots (in $)

Selling price 4.8

Variable cost per unit 3.44

Contribution per fancy pot (Selling price per unit –

variable cost per unit) (Kaplan and Atkinson, 2015) 1.36

c. Calculating break-even point

Particulars Figures (in $) Figures (in $)

Total fixed cost 3500 3500

Contribution when variable cost is $1.95 2.8 – 1.95 = 0.85

BEP (Fixed cost / contribution per

unit) (Morgan and et.al., 2015) 4118

The above depicted table presents that firm will attain the position of no profit no loss by

making and offering 4118 pots to the customers.

d. Assessing whether company should accept or reject the order

On the basis of cited case situation, in the case of large order such as 2000 plain pots firm

will charge $1.90 per pot as selling price. In this, it is not required for the business unit to incur

transportation and distribution cost such as $.40 per pot. However, normal selling price per pot is

$2.80, in this, if firm will not incur transportation cost then it accounts for $2.40. By taking into

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

account such aspect, it can be said that firm should reject the order because it will directly

influence the profit margin of firm.

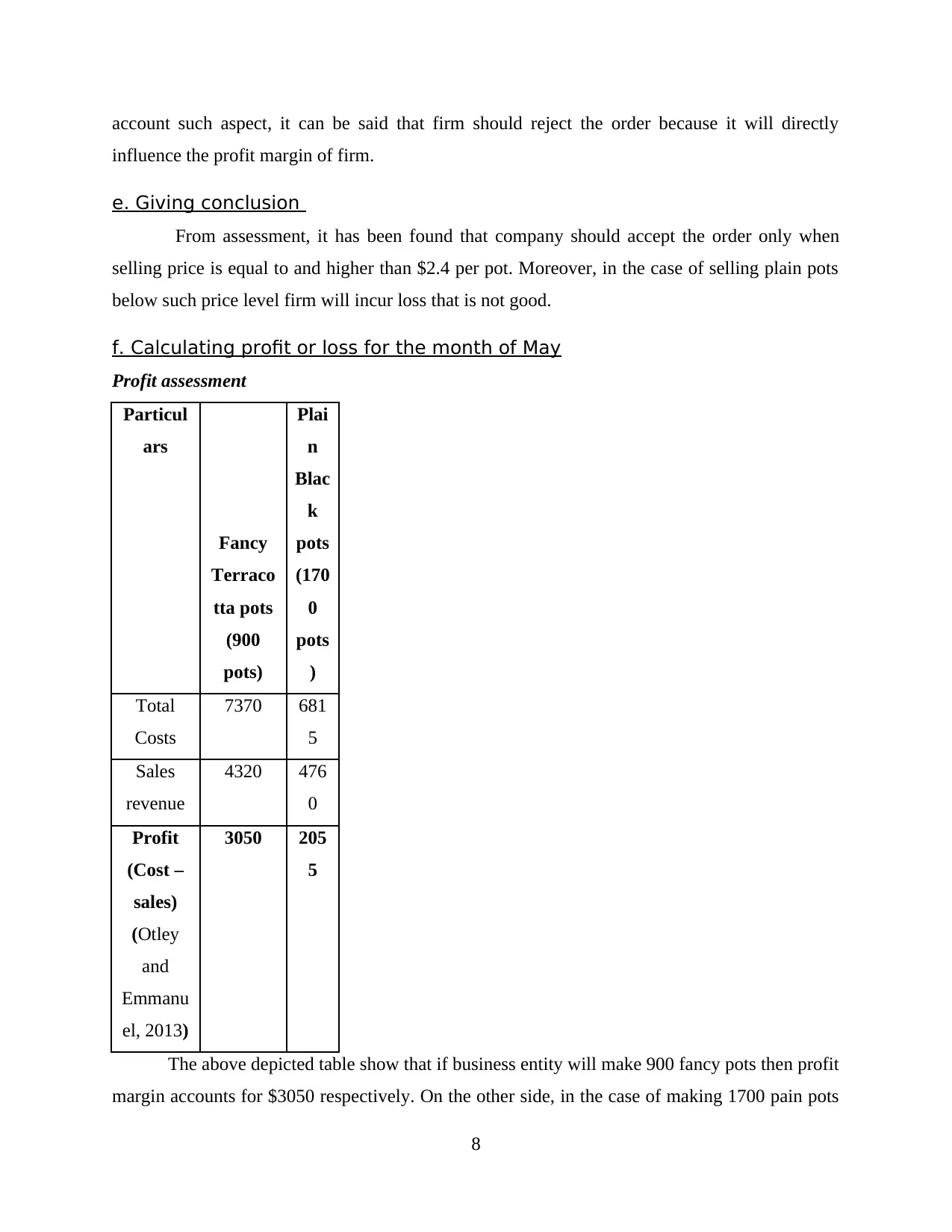

e. Giving conclusion

From assessment, it has been found that company should accept the order only when

selling price is equal to and higher than $2.4 per pot. Moreover, in the case of selling plain pots

below such price level firm will incur loss that is not good.

f. Calculating profit or loss for the month of May

Profit assessment

Particul

ars

Fancy

Terraco

tta pots

(900

pots)

Plai

n

Blac

k

pots

(170

0

pots

)

Total

Costs

7370 681

5

Sales

revenue

4320 476

0

Profit

(Cost –

sales)

(Otley

and

Emmanu

el, 2013)

3050 205

5

The above depicted table show that if business entity will make 900 fancy pots then profit

margin accounts for $3050 respectively. On the other side, in the case of making 1700 pain pots

8

influence the profit margin of firm.

e. Giving conclusion

From assessment, it has been found that company should accept the order only when

selling price is equal to and higher than $2.4 per pot. Moreover, in the case of selling plain pots

below such price level firm will incur loss that is not good.

f. Calculating profit or loss for the month of May

Profit assessment

Particul

ars

Fancy

Terraco

tta pots

(900

pots)

Plai

n

Blac

k

pots

(170

0

pots

)

Total

Costs

7370 681

5

Sales

revenue

4320 476

0

Profit

(Cost –

sales)

(Otley

and

Emmanu

el, 2013)

3050 205

5

The above depicted table show that if business entity will make 900 fancy pots then profit

margin accounts for $3050 respectively. On the other side, in the case of making 1700 pain pots

8

profit will be $2055 significantly. Thus, it can be said that small manufacturing business will

attain higher margin by making 1700 plain pots.

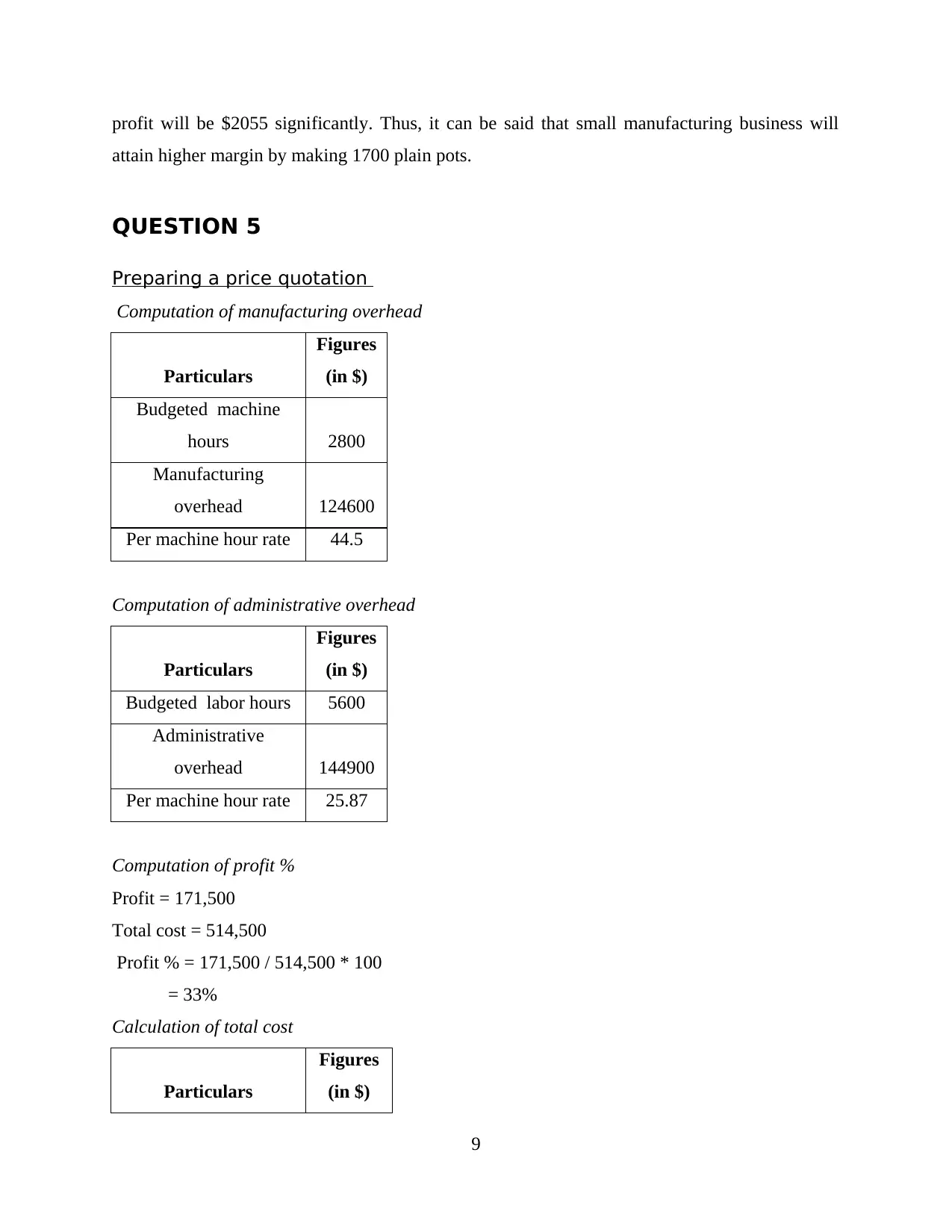

QUESTION 5

Preparing a price quotation

Computation of manufacturing overhead

Particulars

Figures

(in $)

Budgeted machine

hours 2800

Manufacturing

overhead 124600

Per machine hour rate 44.5

Computation of administrative overhead

Particulars

Figures

(in $)

Budgeted labor hours 5600

Administrative

overhead 144900

Per machine hour rate 25.87

Computation of profit %

Profit = 171,500

Total cost = 514,500

Profit % = 171,500 / 514,500 * 100

= 33%

Calculation of total cost

Particulars

Figures

(in $)

9

attain higher margin by making 1700 plain pots.

QUESTION 5

Preparing a price quotation

Computation of manufacturing overhead

Particulars

Figures

(in $)

Budgeted machine

hours 2800

Manufacturing

overhead 124600

Per machine hour rate 44.5

Computation of administrative overhead

Particulars

Figures

(in $)

Budgeted labor hours 5600

Administrative

overhead 144900

Per machine hour rate 25.87

Computation of profit %

Profit = 171,500

Total cost = 514,500

Profit % = 171,500 / 514,500 * 100

= 33%

Calculation of total cost

Particulars

Figures

(in $)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.