Accounting Assignment: Financial Statements and Accrual vs Cash

VerifiedAdded on 2023/06/07

|16

|2594

|406

Homework Assignment

AI Summary

This accounting assignment presents a comprehensive solution to a financial accounting problem. It begins with the creation of a general journal, meticulously recording all transactions for the month of June 2018, followed by the development of a general ledger, which organizes these transactions by account. An unadjusted trial balance is then prepared, summarizing the debit and credit balances. A 10-column worksheet is constructed, incorporating adjustments for the period. Subsequently, an income statement and a balance sheet are generated, providing a snapshot of the company's financial performance and position. Finally, the assignment includes a detailed analysis comparing and contrasting the accrual basis and cash basis of accounting, highlighting their differences and implications for financial reporting, along with the workings to support the calculations.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

General Journal:...............................................................................................................................2

General Ledger:...............................................................................................................................4

Unadjusted Trial Balance:...............................................................................................................8

10-Column Worksheet:..................................................................................................................10

Income Statement:.........................................................................................................................11

Balance Sheet:...............................................................................................................................11

Difference between Accrual Profit & Cash Profit:........................................................................12

Workings:......................................................................................................................................14

Reference.......................................................................................................................................16

Table of Contents

General Journal:...............................................................................................................................2

General Ledger:...............................................................................................................................4

Unadjusted Trial Balance:...............................................................................................................8

10-Column Worksheet:..................................................................................................................10

Income Statement:.........................................................................................................................11

Balance Sheet:...............................................................................................................................11

Difference between Accrual Profit & Cash Profit:........................................................................12

Workings:......................................................................................................................................14

Reference.......................................................................................................................................16

2ACCOUNTING

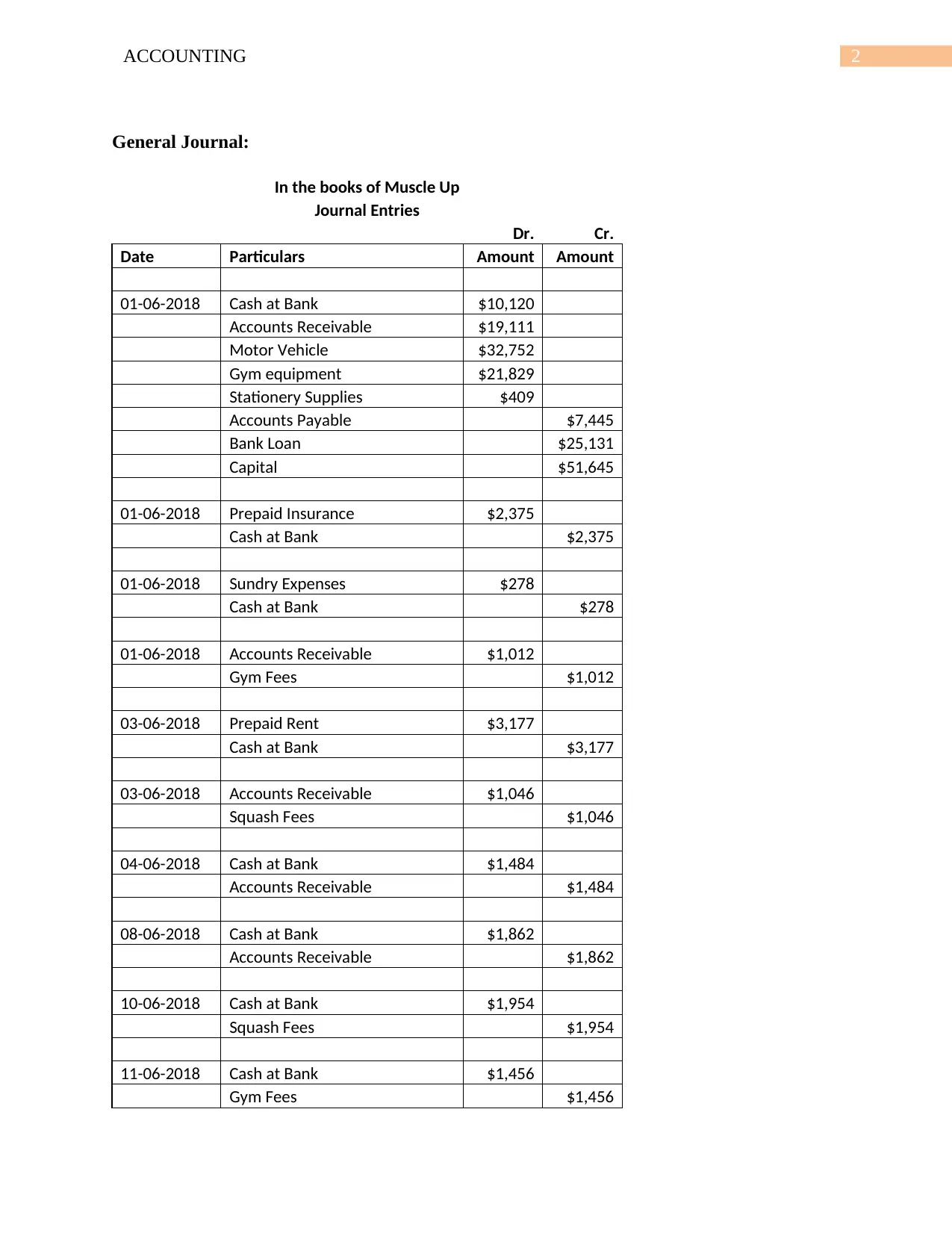

General Journal:

In the books of Muscle Up

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

01-06-2018 Cash at Bank $10,120

Accounts Receivable $19,111

Motor Vehicle $32,752

Gym equipment $21,829

Stationery Supplies $409

Accounts Payable $7,445

Bank Loan $25,131

Capital $51,645

01-06-2018 Prepaid Insurance $2,375

Cash at Bank $2,375

01-06-2018 Sundry Expenses $278

Cash at Bank $278

01-06-2018 Accounts Receivable $1,012

Gym Fees $1,012

03-06-2018 Prepaid Rent $3,177

Cash at Bank $3,177

03-06-2018 Accounts Receivable $1,046

Squash Fees $1,046

04-06-2018 Cash at Bank $1,484

Accounts Receivable $1,484

08-06-2018 Cash at Bank $1,862

Accounts Receivable $1,862

10-06-2018 Cash at Bank $1,954

Squash Fees $1,954

11-06-2018 Cash at Bank $1,456

Gym Fees $1,456

General Journal:

In the books of Muscle Up

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

01-06-2018 Cash at Bank $10,120

Accounts Receivable $19,111

Motor Vehicle $32,752

Gym equipment $21,829

Stationery Supplies $409

Accounts Payable $7,445

Bank Loan $25,131

Capital $51,645

01-06-2018 Prepaid Insurance $2,375

Cash at Bank $2,375

01-06-2018 Sundry Expenses $278

Cash at Bank $278

01-06-2018 Accounts Receivable $1,012

Gym Fees $1,012

03-06-2018 Prepaid Rent $3,177

Cash at Bank $3,177

03-06-2018 Accounts Receivable $1,046

Squash Fees $1,046

04-06-2018 Cash at Bank $1,484

Accounts Receivable $1,484

08-06-2018 Cash at Bank $1,862

Accounts Receivable $1,862

10-06-2018 Cash at Bank $1,954

Squash Fees $1,954

11-06-2018 Cash at Bank $1,456

Gym Fees $1,456

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

12-06-2018 Cash at Bank $2,091

Membership Fees $2,091

13-06-2018 Equipment Hiring Charges $671

Accounts Payable $671

13-06-2018 Accounts Receivable $825

Gym Fees $825

14-06-2018 Accounts Payable $610

Cash at Bank $610

15-06-2018 Wages Expense $2,157

Cash at Bank $2,157

16-06-2018 Advertising Expense $745

Cash at Bank $745

18-06-2018 Cash at Bank $1,860

Squash Fees $1,860

19-06-2018 Stationery Supplies $817

Cash at Bank $817

21-06-2018 Accounts Receivable $1,022

Squash Fees $1,022

21-06-2018 Drawings $879

Cash at Bank $879

24-06-2018 Cash at Bank $3,939

Capital $3,939

24-06-2018 Motor Vehicle Expense $238

Cash at Bank $238

25-06-2018 Accounts Payable $688

Cash at Bank $688

26-06-2018 Cash at Bank $2,103

Membership Fees $2,103

12-06-2018 Cash at Bank $2,091

Membership Fees $2,091

13-06-2018 Equipment Hiring Charges $671

Accounts Payable $671

13-06-2018 Accounts Receivable $825

Gym Fees $825

14-06-2018 Accounts Payable $610

Cash at Bank $610

15-06-2018 Wages Expense $2,157

Cash at Bank $2,157

16-06-2018 Advertising Expense $745

Cash at Bank $745

18-06-2018 Cash at Bank $1,860

Squash Fees $1,860

19-06-2018 Stationery Supplies $817

Cash at Bank $817

21-06-2018 Accounts Receivable $1,022

Squash Fees $1,022

21-06-2018 Drawings $879

Cash at Bank $879

24-06-2018 Cash at Bank $3,939

Capital $3,939

24-06-2018 Motor Vehicle Expense $238

Cash at Bank $238

25-06-2018 Accounts Payable $688

Cash at Bank $688

26-06-2018 Cash at Bank $2,103

Membership Fees $2,103

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

26-06-2018 Advertising Expense $1,132

Accounts Payable $1,132

27-06-2018 Equipment Hiring Charges $463

Cash at Bank $463

29-06-2018 Wages Expenses $2,157

Cash at Bank $2,157

29-06-2018 Cash at Bank $1,587

Gym Fees $1,587

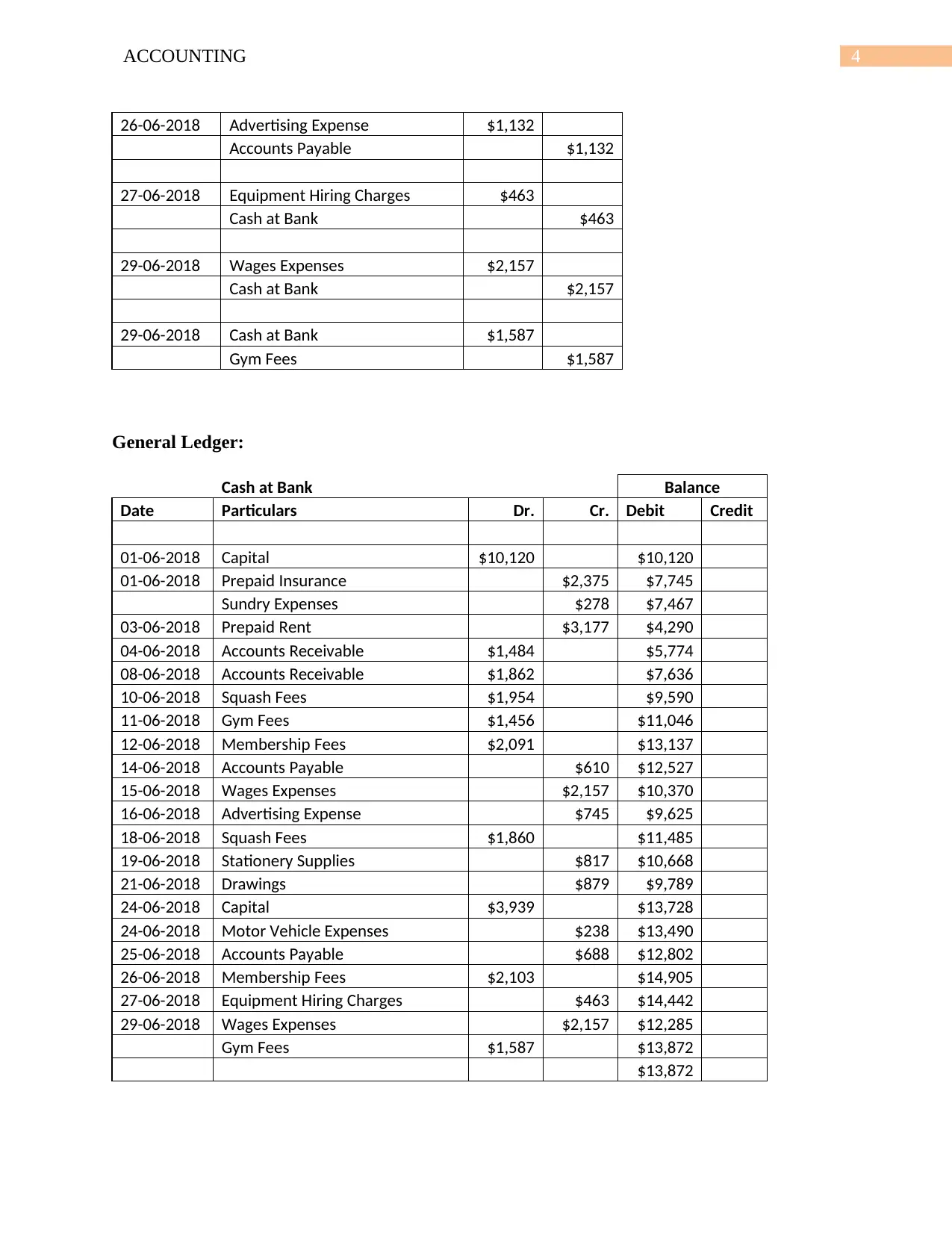

General Ledger:

Cash at Bank Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $10,120 $10,120

01-06-2018 Prepaid Insurance $2,375 $7,745

Sundry Expenses $278 $7,467

03-06-2018 Prepaid Rent $3,177 $4,290

04-06-2018 Accounts Receivable $1,484 $5,774

08-06-2018 Accounts Receivable $1,862 $7,636

10-06-2018 Squash Fees $1,954 $9,590

11-06-2018 Gym Fees $1,456 $11,046

12-06-2018 Membership Fees $2,091 $13,137

14-06-2018 Accounts Payable $610 $12,527

15-06-2018 Wages Expenses $2,157 $10,370

16-06-2018 Advertising Expense $745 $9,625

18-06-2018 Squash Fees $1,860 $11,485

19-06-2018 Stationery Supplies $817 $10,668

21-06-2018 Drawings $879 $9,789

24-06-2018 Capital $3,939 $13,728

24-06-2018 Motor Vehicle Expenses $238 $13,490

25-06-2018 Accounts Payable $688 $12,802

26-06-2018 Membership Fees $2,103 $14,905

27-06-2018 Equipment Hiring Charges $463 $14,442

29-06-2018 Wages Expenses $2,157 $12,285

Gym Fees $1,587 $13,872

$13,872

26-06-2018 Advertising Expense $1,132

Accounts Payable $1,132

27-06-2018 Equipment Hiring Charges $463

Cash at Bank $463

29-06-2018 Wages Expenses $2,157

Cash at Bank $2,157

29-06-2018 Cash at Bank $1,587

Gym Fees $1,587

General Ledger:

Cash at Bank Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $10,120 $10,120

01-06-2018 Prepaid Insurance $2,375 $7,745

Sundry Expenses $278 $7,467

03-06-2018 Prepaid Rent $3,177 $4,290

04-06-2018 Accounts Receivable $1,484 $5,774

08-06-2018 Accounts Receivable $1,862 $7,636

10-06-2018 Squash Fees $1,954 $9,590

11-06-2018 Gym Fees $1,456 $11,046

12-06-2018 Membership Fees $2,091 $13,137

14-06-2018 Accounts Payable $610 $12,527

15-06-2018 Wages Expenses $2,157 $10,370

16-06-2018 Advertising Expense $745 $9,625

18-06-2018 Squash Fees $1,860 $11,485

19-06-2018 Stationery Supplies $817 $10,668

21-06-2018 Drawings $879 $9,789

24-06-2018 Capital $3,939 $13,728

24-06-2018 Motor Vehicle Expenses $238 $13,490

25-06-2018 Accounts Payable $688 $12,802

26-06-2018 Membership Fees $2,103 $14,905

27-06-2018 Equipment Hiring Charges $463 $14,442

29-06-2018 Wages Expenses $2,157 $12,285

Gym Fees $1,587 $13,872

$13,872

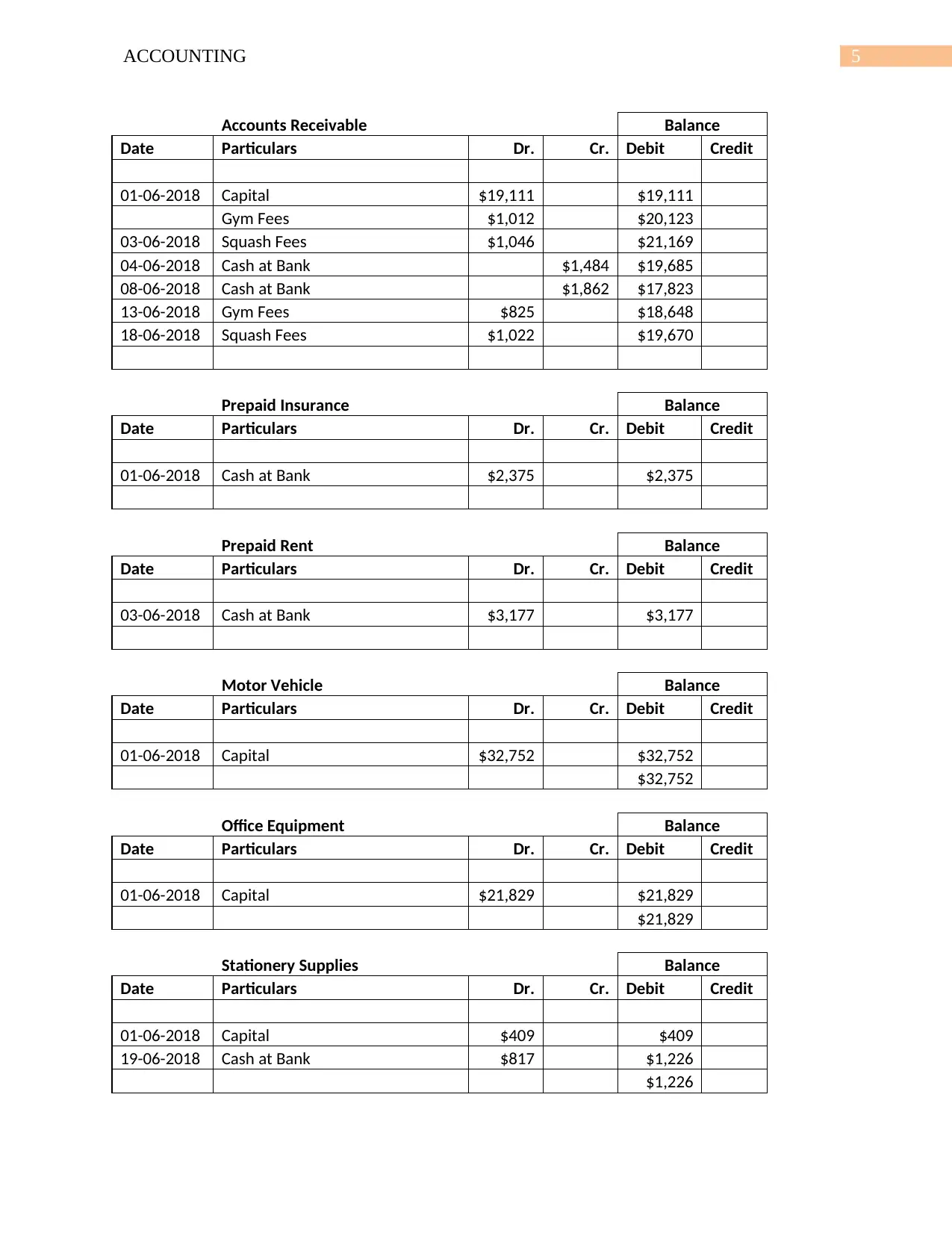

5ACCOUNTING

Accounts Receivable Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $19,111 $19,111

Gym Fees $1,012 $20,123

03-06-2018 Squash Fees $1,046 $21,169

04-06-2018 Cash at Bank $1,484 $19,685

08-06-2018 Cash at Bank $1,862 $17,823

13-06-2018 Gym Fees $825 $18,648

18-06-2018 Squash Fees $1,022 $19,670

Prepaid Insurance Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Cash at Bank $2,375 $2,375

Prepaid Rent Balance

Date Particulars Dr. Cr. Debit Credit

03-06-2018 Cash at Bank $3,177 $3,177

Motor Vehicle Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $32,752 $32,752

$32,752

Office Equipment Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $21,829 $21,829

$21,829

Stationery Supplies Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $409 $409

19-06-2018 Cash at Bank $817 $1,226

$1,226

Accounts Receivable Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $19,111 $19,111

Gym Fees $1,012 $20,123

03-06-2018 Squash Fees $1,046 $21,169

04-06-2018 Cash at Bank $1,484 $19,685

08-06-2018 Cash at Bank $1,862 $17,823

13-06-2018 Gym Fees $825 $18,648

18-06-2018 Squash Fees $1,022 $19,670

Prepaid Insurance Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Cash at Bank $2,375 $2,375

Prepaid Rent Balance

Date Particulars Dr. Cr. Debit Credit

03-06-2018 Cash at Bank $3,177 $3,177

Motor Vehicle Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $32,752 $32,752

$32,752

Office Equipment Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $21,829 $21,829

$21,829

Stationery Supplies Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $409 $409

19-06-2018 Cash at Bank $817 $1,226

$1,226

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

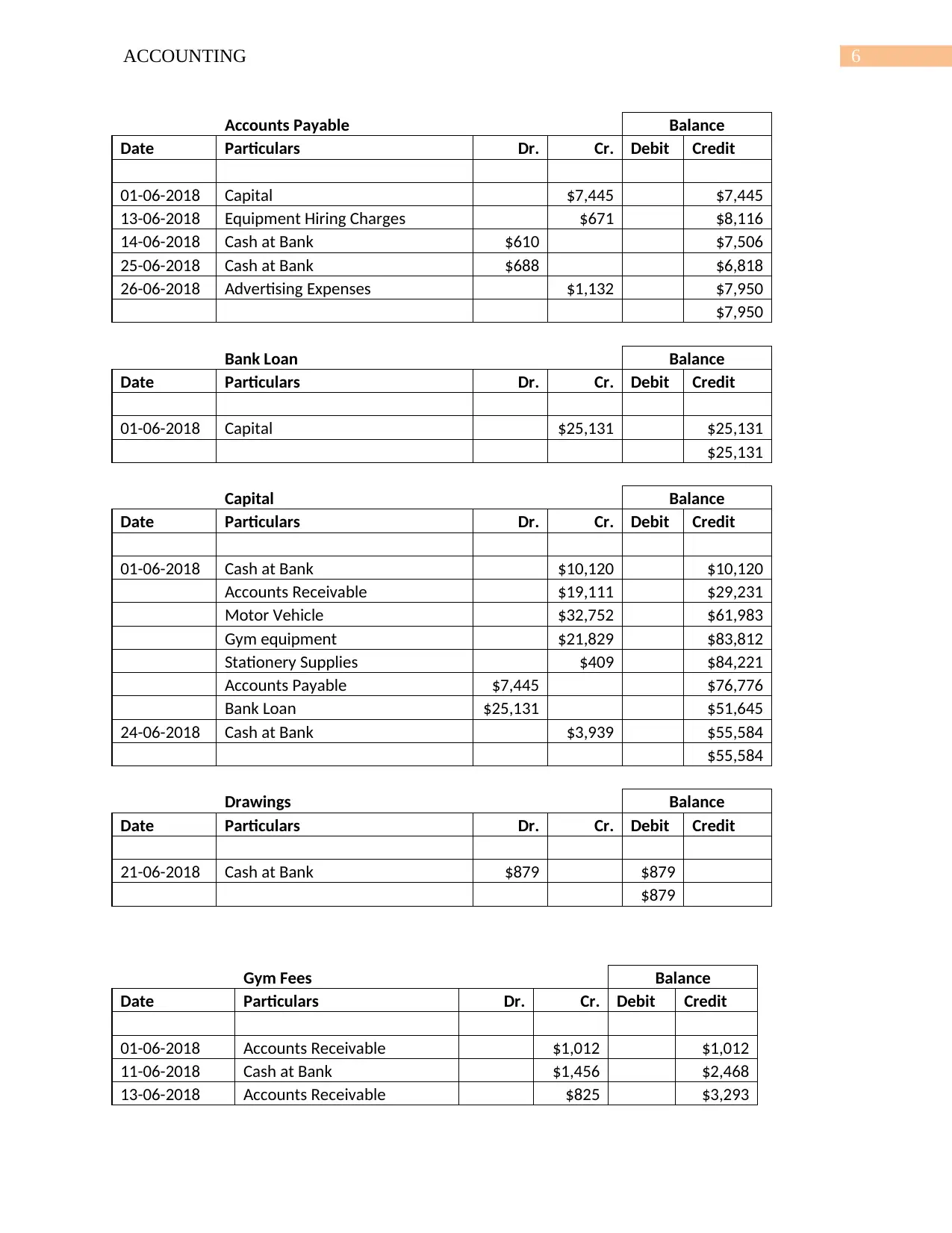

6ACCOUNTING

Accounts Payable Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $7,445 $7,445

13-06-2018 Equipment Hiring Charges $671 $8,116

14-06-2018 Cash at Bank $610 $7,506

25-06-2018 Cash at Bank $688 $6,818

26-06-2018 Advertising Expenses $1,132 $7,950

$7,950

Bank Loan Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $25,131 $25,131

$25,131

Capital Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Cash at Bank $10,120 $10,120

Accounts Receivable $19,111 $29,231

Motor Vehicle $32,752 $61,983

Gym equipment $21,829 $83,812

Stationery Supplies $409 $84,221

Accounts Payable $7,445 $76,776

Bank Loan $25,131 $51,645

24-06-2018 Cash at Bank $3,939 $55,584

$55,584

Drawings Balance

Date Particulars Dr. Cr. Debit Credit

21-06-2018 Cash at Bank $879 $879

$879

Gym Fees Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Accounts Receivable $1,012 $1,012

11-06-2018 Cash at Bank $1,456 $2,468

13-06-2018 Accounts Receivable $825 $3,293

Accounts Payable Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $7,445 $7,445

13-06-2018 Equipment Hiring Charges $671 $8,116

14-06-2018 Cash at Bank $610 $7,506

25-06-2018 Cash at Bank $688 $6,818

26-06-2018 Advertising Expenses $1,132 $7,950

$7,950

Bank Loan Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Capital $25,131 $25,131

$25,131

Capital Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Cash at Bank $10,120 $10,120

Accounts Receivable $19,111 $29,231

Motor Vehicle $32,752 $61,983

Gym equipment $21,829 $83,812

Stationery Supplies $409 $84,221

Accounts Payable $7,445 $76,776

Bank Loan $25,131 $51,645

24-06-2018 Cash at Bank $3,939 $55,584

$55,584

Drawings Balance

Date Particulars Dr. Cr. Debit Credit

21-06-2018 Cash at Bank $879 $879

$879

Gym Fees Balance

Date Particulars Dr. Cr. Debit Credit

01-06-2018 Accounts Receivable $1,012 $1,012

11-06-2018 Cash at Bank $1,456 $2,468

13-06-2018 Accounts Receivable $825 $3,293

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

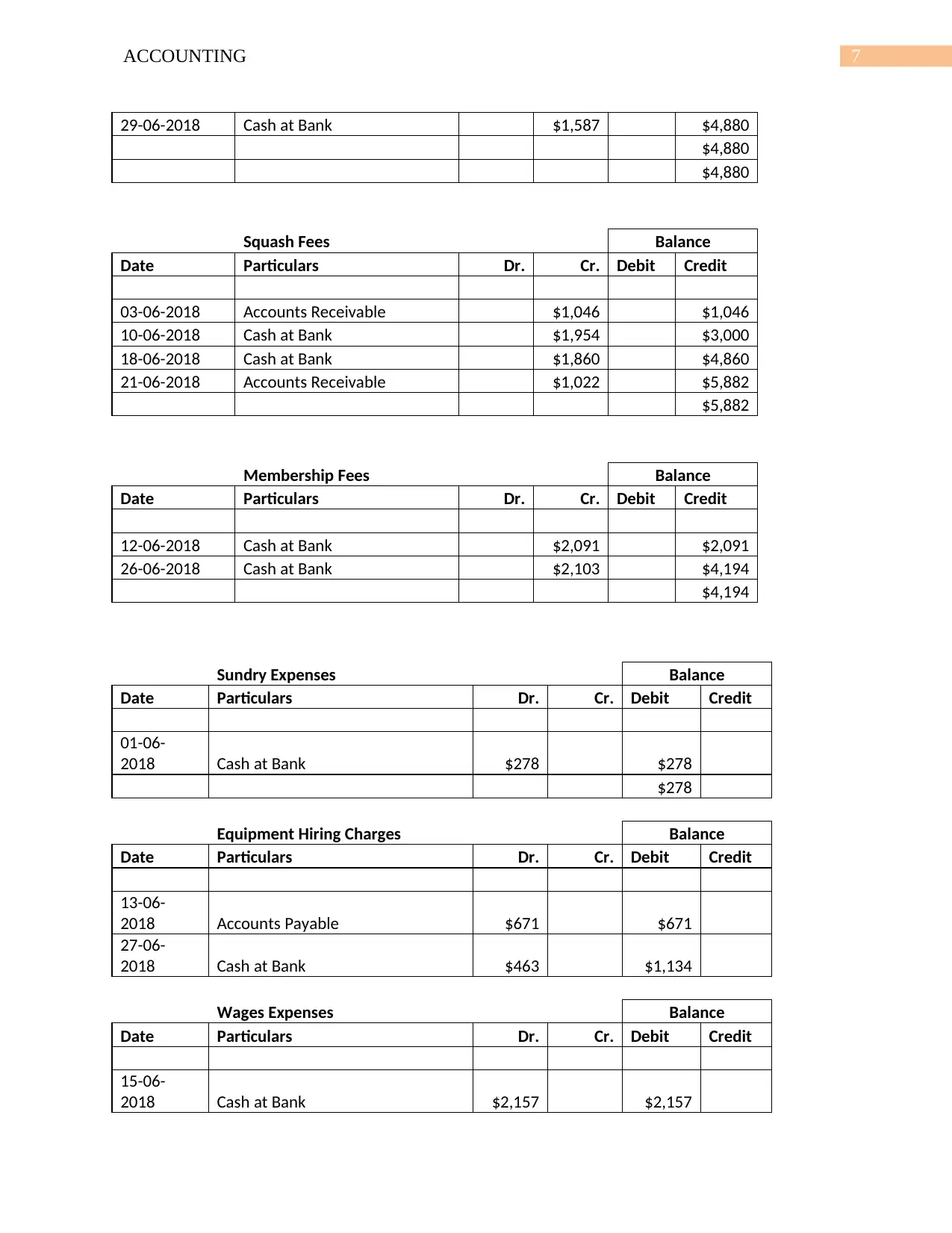

7ACCOUNTING

29-06-2018 Cash at Bank $1,587 $4,880

$4,880

$4,880

Squash Fees Balance

Date Particulars Dr. Cr. Debit Credit

03-06-2018 Accounts Receivable $1,046 $1,046

10-06-2018 Cash at Bank $1,954 $3,000

18-06-2018 Cash at Bank $1,860 $4,860

21-06-2018 Accounts Receivable $1,022 $5,882

$5,882

Membership Fees Balance

Date Particulars Dr. Cr. Debit Credit

12-06-2018 Cash at Bank $2,091 $2,091

26-06-2018 Cash at Bank $2,103 $4,194

$4,194

Sundry Expenses Balance

Date Particulars Dr. Cr. Debit Credit

01-06-

2018 Cash at Bank $278 $278

$278

Equipment Hiring Charges Balance

Date Particulars Dr. Cr. Debit Credit

13-06-

2018 Accounts Payable $671 $671

27-06-

2018 Cash at Bank $463 $1,134

Wages Expenses Balance

Date Particulars Dr. Cr. Debit Credit

15-06-

2018 Cash at Bank $2,157 $2,157

29-06-2018 Cash at Bank $1,587 $4,880

$4,880

$4,880

Squash Fees Balance

Date Particulars Dr. Cr. Debit Credit

03-06-2018 Accounts Receivable $1,046 $1,046

10-06-2018 Cash at Bank $1,954 $3,000

18-06-2018 Cash at Bank $1,860 $4,860

21-06-2018 Accounts Receivable $1,022 $5,882

$5,882

Membership Fees Balance

Date Particulars Dr. Cr. Debit Credit

12-06-2018 Cash at Bank $2,091 $2,091

26-06-2018 Cash at Bank $2,103 $4,194

$4,194

Sundry Expenses Balance

Date Particulars Dr. Cr. Debit Credit

01-06-

2018 Cash at Bank $278 $278

$278

Equipment Hiring Charges Balance

Date Particulars Dr. Cr. Debit Credit

13-06-

2018 Accounts Payable $671 $671

27-06-

2018 Cash at Bank $463 $1,134

Wages Expenses Balance

Date Particulars Dr. Cr. Debit Credit

15-06-

2018 Cash at Bank $2,157 $2,157

8ACCOUNTING

29-06-

2048 Cash at Bank $2,157 $4,314

Advertising Expenses Balance

Date Particulars Dr. Cr. Debit Credit

16-06-

2018 Cash at Bank $745 $745

26-06-

2018 Accounts Payable $1,132 $1,877

Motor Vehicle Expense Balance

Date Particulars Dr. Cr. Debit Credit

24-06-

2018 Cash at Bank $238 $238

$238

Unadjusted Trial Balance:

Unadjusted Trial Balance

as on 30 June 2018

Account Unadjusted T/B

DR CR

Cash at Bank $13,872

Accounts Receivable $19,670

Prepaid Insurance $2,375

Prepaid Rent $3,177

Motor Vehicle $32,752

Accumulated Depreciation - Motor Vehicle

Office Equipment $21,829

Accumulated Depreciation - Office Equipment

Stationery Supplies $1,226

Accounts Payable $7,950

Interest Payable

Wages Payable

Bank Loan $25,131

Capital $55,584

Drawings $879

Gym Fees $4,880

Squash Fees $5,882

Membership Fees $4,194

Sundry Expenses $278

29-06-

2048 Cash at Bank $2,157 $4,314

Advertising Expenses Balance

Date Particulars Dr. Cr. Debit Credit

16-06-

2018 Cash at Bank $745 $745

26-06-

2018 Accounts Payable $1,132 $1,877

Motor Vehicle Expense Balance

Date Particulars Dr. Cr. Debit Credit

24-06-

2018 Cash at Bank $238 $238

$238

Unadjusted Trial Balance:

Unadjusted Trial Balance

as on 30 June 2018

Account Unadjusted T/B

DR CR

Cash at Bank $13,872

Accounts Receivable $19,670

Prepaid Insurance $2,375

Prepaid Rent $3,177

Motor Vehicle $32,752

Accumulated Depreciation - Motor Vehicle

Office Equipment $21,829

Accumulated Depreciation - Office Equipment

Stationery Supplies $1,226

Accounts Payable $7,950

Interest Payable

Wages Payable

Bank Loan $25,131

Capital $55,584

Drawings $879

Gym Fees $4,880

Squash Fees $5,882

Membership Fees $4,194

Sundry Expenses $278

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Equipment Hiring Charges $1,134

Wages Expenses $4,314

Advertising Expenses $1,877

Motor Vehicle Expenses $238

Interest Expenses

Depreciation Expenses

Insurance Expenses

Rent Expenses

Supplies Expenses

TOTAL

$1,03,62

1

$1,03,62

1

10-Column Worksheet:

Account

DR CR DR CR DR CR DR CR DR CR

Cash at Bank $13,872 $13,872 $13,872

Accounts Receivable $19,670 $19,670 $19,670

Prepaid Insurance $2,375 $594 $1,781 $1,781

Prepaid Rent $3,177 $635 $2,542 $2,542

Motor Vehicle $32,752 $32,752 $32,752

Accumulated Depreciation - Motor Vehicle $1,148 $1,148 $1,148

Office Equipment $21,829 $21,829 $21,829

Accumulated Depreciation - Office Equipment $4,155 $4,155 $4,155

Stationery Supplies $1,226 $583 $643 $643

Accounts Payable $7,950 $7,950 $7,950

Interest Payable $188 $188 $188

Wages Payable $308 $308 $308

Bank Loan $25,131 $25,131 $25,131

Capital $55,584 $55,584 $55,584

Drawings $879 $879 $879

Gym Fees $4,880 $4,880 $4,880

Squash Fees $5,882 $5,882 $5,882

Membership Fees $4,194 $4,194 $4,194

Sundry Expenses $278 $278 $278

Equipment Hiring Charges $1,134 $1,134 $1,134

Wages Expenses $4,314 $308 $4,622 $4,622

Advertising Expenses $1,877 $1,877 $1,877

Motor Vehicle Expenses $238 $238 $238

Interest Expenses $188 $188 $188

Depreciation Expenses $5,303 $5,303 $5,303

Insurance Expenses $594 $594 $594

Rent Expenses $635 $635 $635

Supplies Expenses $583 $583 $583

Subtotal $15,453 $14,956 $93,968 $94,465

Profit (Loss) -$497 -$497

Total $1,03,621 $1,03,621 $7,612 $7,612 $1,09,421 $1,09,421 $14,956 $14,956 $93,968 $93,968

10 Column Worksheet

Unadjusted T/B Adjustments Adjusted T/B Income Statement Balance Sheet

Equipment Hiring Charges $1,134

Wages Expenses $4,314

Advertising Expenses $1,877

Motor Vehicle Expenses $238

Interest Expenses

Depreciation Expenses

Insurance Expenses

Rent Expenses

Supplies Expenses

TOTAL

$1,03,62

1

$1,03,62

1

10-Column Worksheet:

Account

DR CR DR CR DR CR DR CR DR CR

Cash at Bank $13,872 $13,872 $13,872

Accounts Receivable $19,670 $19,670 $19,670

Prepaid Insurance $2,375 $594 $1,781 $1,781

Prepaid Rent $3,177 $635 $2,542 $2,542

Motor Vehicle $32,752 $32,752 $32,752

Accumulated Depreciation - Motor Vehicle $1,148 $1,148 $1,148

Office Equipment $21,829 $21,829 $21,829

Accumulated Depreciation - Office Equipment $4,155 $4,155 $4,155

Stationery Supplies $1,226 $583 $643 $643

Accounts Payable $7,950 $7,950 $7,950

Interest Payable $188 $188 $188

Wages Payable $308 $308 $308

Bank Loan $25,131 $25,131 $25,131

Capital $55,584 $55,584 $55,584

Drawings $879 $879 $879

Gym Fees $4,880 $4,880 $4,880

Squash Fees $5,882 $5,882 $5,882

Membership Fees $4,194 $4,194 $4,194

Sundry Expenses $278 $278 $278

Equipment Hiring Charges $1,134 $1,134 $1,134

Wages Expenses $4,314 $308 $4,622 $4,622

Advertising Expenses $1,877 $1,877 $1,877

Motor Vehicle Expenses $238 $238 $238

Interest Expenses $188 $188 $188

Depreciation Expenses $5,303 $5,303 $5,303

Insurance Expenses $594 $594 $594

Rent Expenses $635 $635 $635

Supplies Expenses $583 $583 $583

Subtotal $15,453 $14,956 $93,968 $94,465

Profit (Loss) -$497 -$497

Total $1,03,621 $1,03,621 $7,612 $7,612 $1,09,421 $1,09,421 $14,956 $14,956 $93,968 $93,968

10 Column Worksheet

Unadjusted T/B Adjustments Adjusted T/B Income Statement Balance Sheet

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

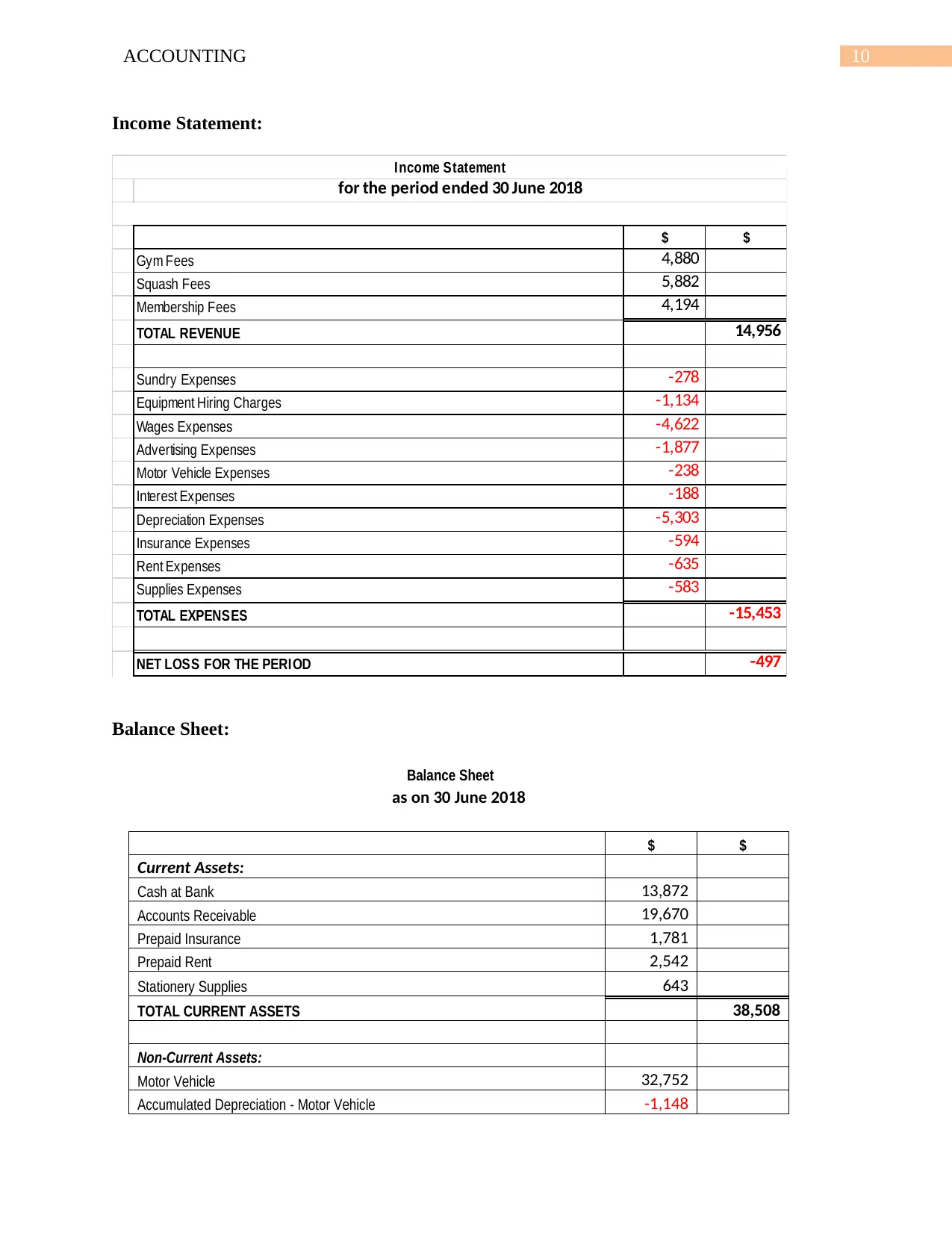

Income Statement:

$ $

Gym Fees 4,880

Squash Fees 5,882

Membership Fees 4,194

TOTAL REVENUE 14,956

Sundry Expenses -278

Equipment Hiring Charges -1,134

Wages Expenses -4,622

Advertising Expenses -1,877

Motor Vehicle Expenses -238

Interest Expenses -188

Depreciation Expenses -5,303

Insurance Expenses -594

Rent Expenses -635

Supplies Expenses -583

TOTAL EXPENSES -15,453

NET LOSS FOR THE PERIOD -497

Income Statement

for the period ended 30 June 2018

Balance Sheet:

Balance Sheet

as on 30 June 2018

$ $

Current Assets:

Cash at Bank 13,872

Accounts Receivable 19,670

Prepaid Insurance 1,781

Prepaid Rent 2,542

Stationery Supplies 643

TOTAL CURRENT ASSETS 38,508

Non-Current Assets:

Motor Vehicle 32,752

Accumulated Depreciation - Motor Vehicle -1,148

Income Statement:

$ $

Gym Fees 4,880

Squash Fees 5,882

Membership Fees 4,194

TOTAL REVENUE 14,956

Sundry Expenses -278

Equipment Hiring Charges -1,134

Wages Expenses -4,622

Advertising Expenses -1,877

Motor Vehicle Expenses -238

Interest Expenses -188

Depreciation Expenses -5,303

Insurance Expenses -594

Rent Expenses -635

Supplies Expenses -583

TOTAL EXPENSES -15,453

NET LOSS FOR THE PERIOD -497

Income Statement

for the period ended 30 June 2018

Balance Sheet:

Balance Sheet

as on 30 June 2018

$ $

Current Assets:

Cash at Bank 13,872

Accounts Receivable 19,670

Prepaid Insurance 1,781

Prepaid Rent 2,542

Stationery Supplies 643

TOTAL CURRENT ASSETS 38,508

Non-Current Assets:

Motor Vehicle 32,752

Accumulated Depreciation - Motor Vehicle -1,148

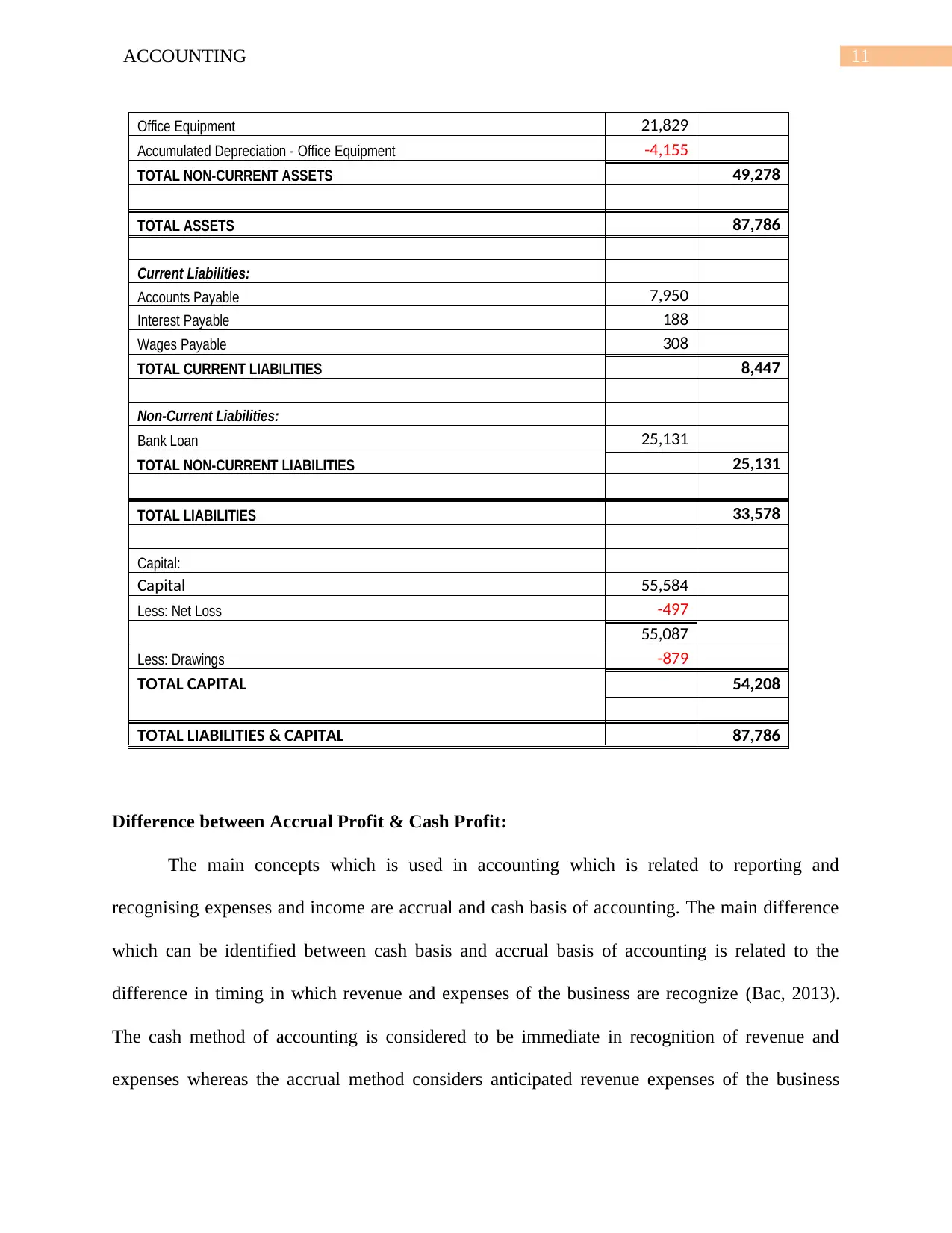

11ACCOUNTING

Office Equipment 21,829

Accumulated Depreciation - Office Equipment -4,155

TOTAL NON-CURRENT ASSETS 49,278

TOTAL ASSETS 87,786

Current Liabilities:

Accounts Payable 7,950

Interest Payable 188

Wages Payable 308

TOTAL CURRENT LIABILITIES 8,447

Non-Current Liabilities:

Bank Loan 25,131

TOTAL NON-CURRENT LIABILITIES 25,131

TOTAL LIABILITIES 33,578

Capital:

Capital 55,584

Less: Net Loss -497

55,087

Less: Drawings -879

TOTAL CAPITAL 54,208

TOTAL LIABILITIES & CAPITAL 87,786

Difference between Accrual Profit & Cash Profit:

The main concepts which is used in accounting which is related to reporting and

recognising expenses and income are accrual and cash basis of accounting. The main difference

which can be identified between cash basis and accrual basis of accounting is related to the

difference in timing in which revenue and expenses of the business are recognize (Bac, 2013).

The cash method of accounting is considered to be immediate in recognition of revenue and

expenses whereas the accrual method considers anticipated revenue expenses of the business

Office Equipment 21,829

Accumulated Depreciation - Office Equipment -4,155

TOTAL NON-CURRENT ASSETS 49,278

TOTAL ASSETS 87,786

Current Liabilities:

Accounts Payable 7,950

Interest Payable 188

Wages Payable 308

TOTAL CURRENT LIABILITIES 8,447

Non-Current Liabilities:

Bank Loan 25,131

TOTAL NON-CURRENT LIABILITIES 25,131

TOTAL LIABILITIES 33,578

Capital:

Capital 55,584

Less: Net Loss -497

55,087

Less: Drawings -879

TOTAL CAPITAL 54,208

TOTAL LIABILITIES & CAPITAL 87,786

Difference between Accrual Profit & Cash Profit:

The main concepts which is used in accounting which is related to reporting and

recognising expenses and income are accrual and cash basis of accounting. The main difference

which can be identified between cash basis and accrual basis of accounting is related to the

difference in timing in which revenue and expenses of the business are recognize (Bac, 2013).

The cash method of accounting is considered to be immediate in recognition of revenue and

expenses whereas the accrual method considers anticipated revenue expenses of the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.