Financial and Management Accounting: Analysis and Techniques

VerifiedAdded on 2023/06/18

|8

|1657

|339

Report

AI Summary

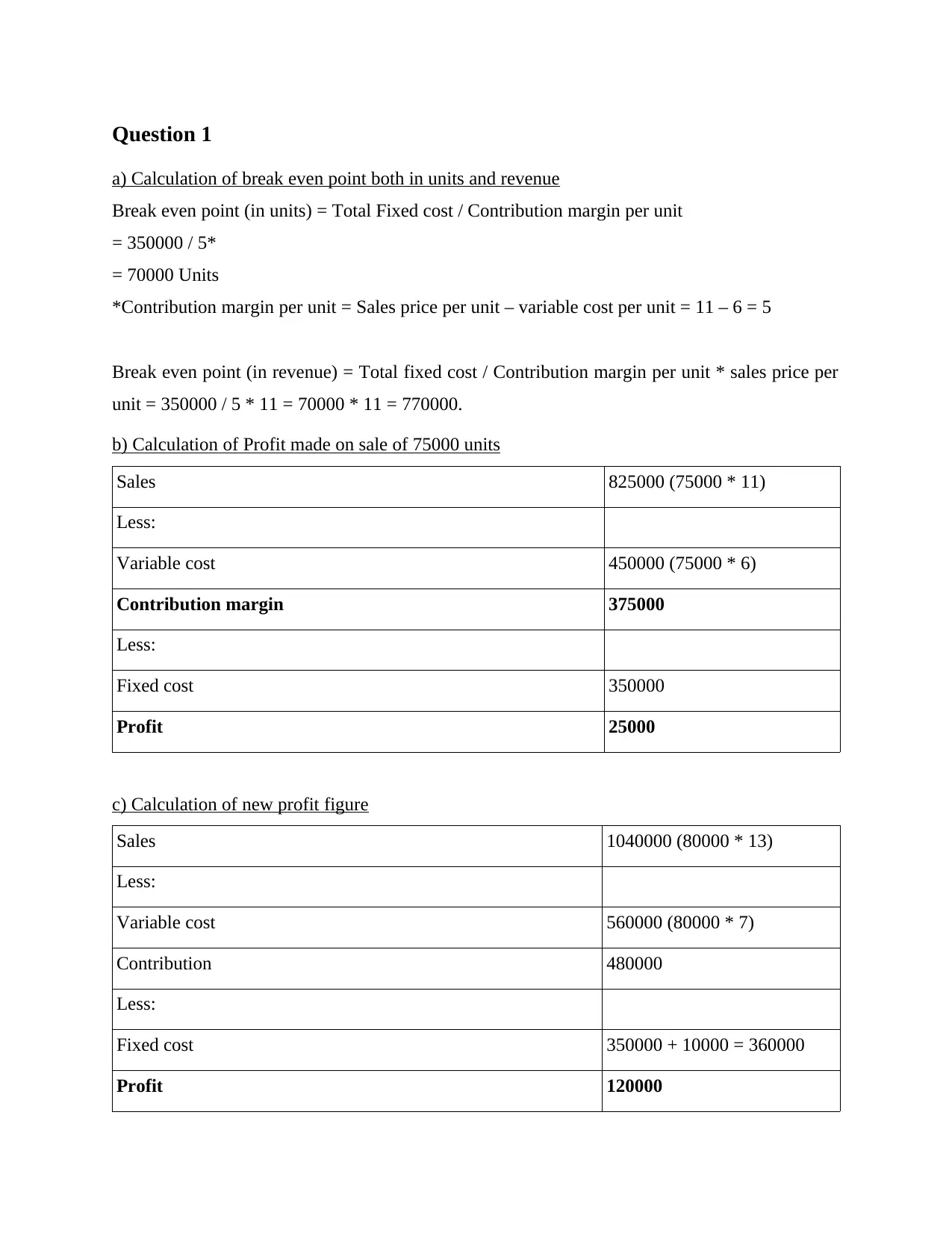

This report provides a detailed analysis of accounting principles, focusing on break-even analysis and management accounting techniques. It includes calculations for break-even points in units and revenue, profit calculations at different sales levels, and an exploration of the limitations of break-even analysis. The report also discusses the importance of management accounting in business operations, highlighting its role in planning, decision-making, and strategic management. A comparison between management and financial accounting is presented, emphasizing their differences in objectives, regulatory requirements, and data orientation. Finally, the report examines three key techniques used by management accountants—forecasting and trend analysis, product costing and inventory valuation, and capital budgeting—explaining how these tools aid in achieving management accounting objectives. Desklib offers this and many more solved assignments for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.