BACT105 Business Accounting: Financial Statement Analysis Report

VerifiedAdded on 2023/06/07

|12

|2396

|79

Report

AI Summary

This report provides a comprehensive analysis of business accounting principles, focusing on adjusting entries and the preparation of financial statements. It begins with an explanation of adjusting journal entries, detailing their purpose and necessity in accrual accounting. The report then presents a revised trial balance incorporating these adjustments, followed by the creation of an income statement and balance sheet. Furthermore, it differentiates between adjusting and closing journal entries, highlighting their respective roles in the accounting cycle. The report also includes a statement of changes in equity and detailed calculations for depreciation expenses. This document, contributed by a student, is available on Desklib, where you can find a variety of study resources including past papers and solved assignments.

Business Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

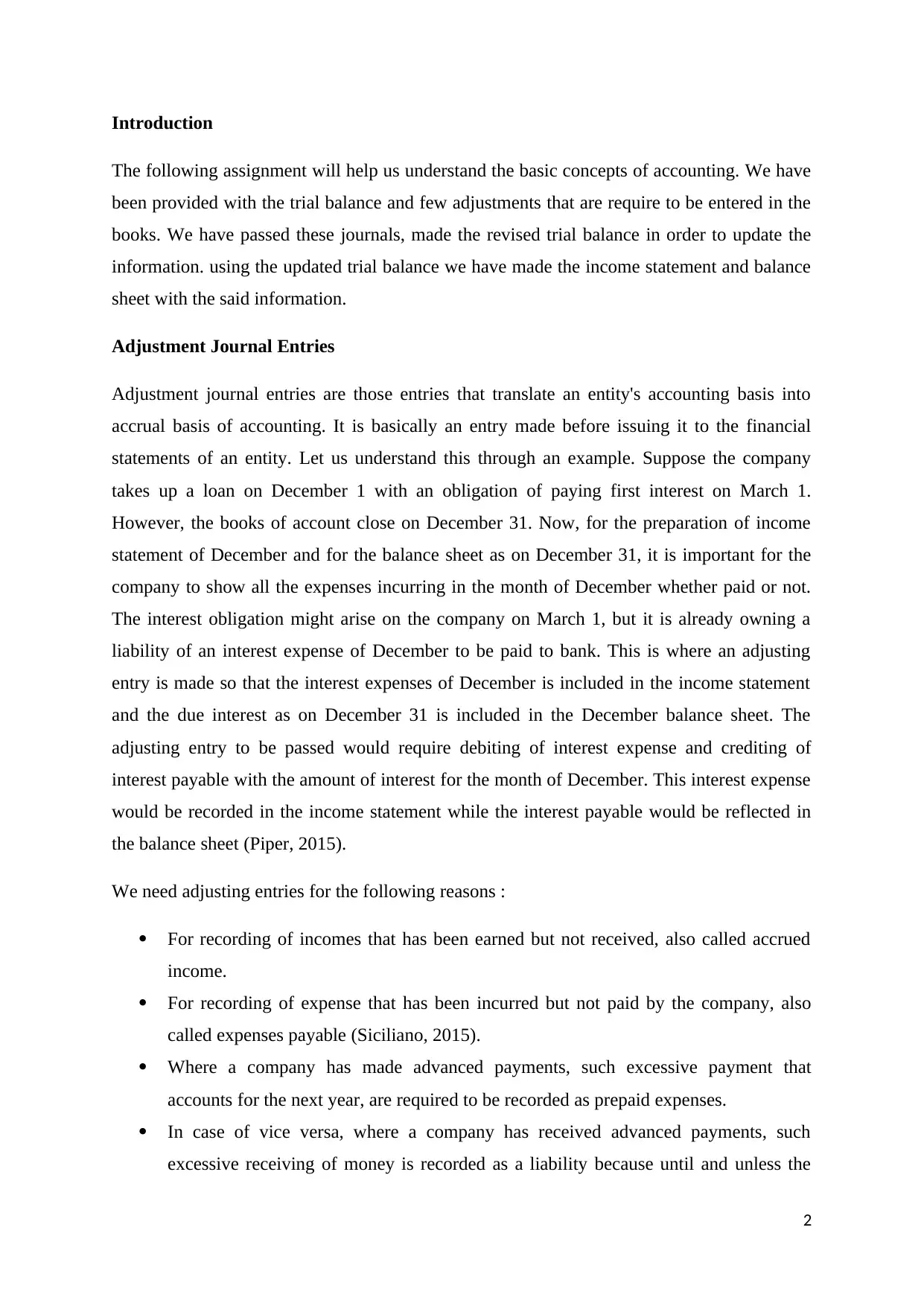

Introduction

The following assignment will help us understand the basic concepts of accounting. We have

been provided with the trial balance and few adjustments that are require to be entered in the

books. We have passed these journals, made the revised trial balance in order to update the

information. using the updated trial balance we have made the income statement and balance

sheet with the said information.

Adjustment Journal Entries

Adjustment journal entries are those entries that translate an entity's accounting basis into

accrual basis of accounting. It is basically an entry made before issuing it to the financial

statements of an entity. Let us understand this through an example. Suppose the company

takes up a loan on December 1 with an obligation of paying first interest on March 1.

However, the books of account close on December 31. Now, for the preparation of income

statement of December and for the balance sheet as on December 31, it is important for the

company to show all the expenses incurring in the month of December whether paid or not.

The interest obligation might arise on the company on March 1, but it is already owning a

liability of an interest expense of December to be paid to bank. This is where an adjusting

entry is made so that the interest expenses of December is included in the income statement

and the due interest as on December 31 is included in the December balance sheet. The

adjusting entry to be passed would require debiting of interest expense and crediting of

interest payable with the amount of interest for the month of December. This interest expense

would be recorded in the income statement while the interest payable would be reflected in

the balance sheet (Piper, 2015).

We need adjusting entries for the following reasons :

For recording of incomes that has been earned but not received, also called accrued

income.

For recording of expense that has been incurred but not paid by the company, also

called expenses payable (Siciliano, 2015).

Where a company has made advanced payments, such excessive payment that

accounts for the next year, are required to be recorded as prepaid expenses.

In case of vice versa, where a company has received advanced payments, such

excessive receiving of money is recorded as a liability because until and unless the

2

The following assignment will help us understand the basic concepts of accounting. We have

been provided with the trial balance and few adjustments that are require to be entered in the

books. We have passed these journals, made the revised trial balance in order to update the

information. using the updated trial balance we have made the income statement and balance

sheet with the said information.

Adjustment Journal Entries

Adjustment journal entries are those entries that translate an entity's accounting basis into

accrual basis of accounting. It is basically an entry made before issuing it to the financial

statements of an entity. Let us understand this through an example. Suppose the company

takes up a loan on December 1 with an obligation of paying first interest on March 1.

However, the books of account close on December 31. Now, for the preparation of income

statement of December and for the balance sheet as on December 31, it is important for the

company to show all the expenses incurring in the month of December whether paid or not.

The interest obligation might arise on the company on March 1, but it is already owning a

liability of an interest expense of December to be paid to bank. This is where an adjusting

entry is made so that the interest expenses of December is included in the income statement

and the due interest as on December 31 is included in the December balance sheet. The

adjusting entry to be passed would require debiting of interest expense and crediting of

interest payable with the amount of interest for the month of December. This interest expense

would be recorded in the income statement while the interest payable would be reflected in

the balance sheet (Piper, 2015).

We need adjusting entries for the following reasons :

For recording of incomes that has been earned but not received, also called accrued

income.

For recording of expense that has been incurred but not paid by the company, also

called expenses payable (Siciliano, 2015).

Where a company has made advanced payments, such excessive payment that

accounts for the next year, are required to be recorded as prepaid expenses.

In case of vice versa, where a company has received advanced payments, such

excessive receiving of money is recorded as a liability because until and unless the

2

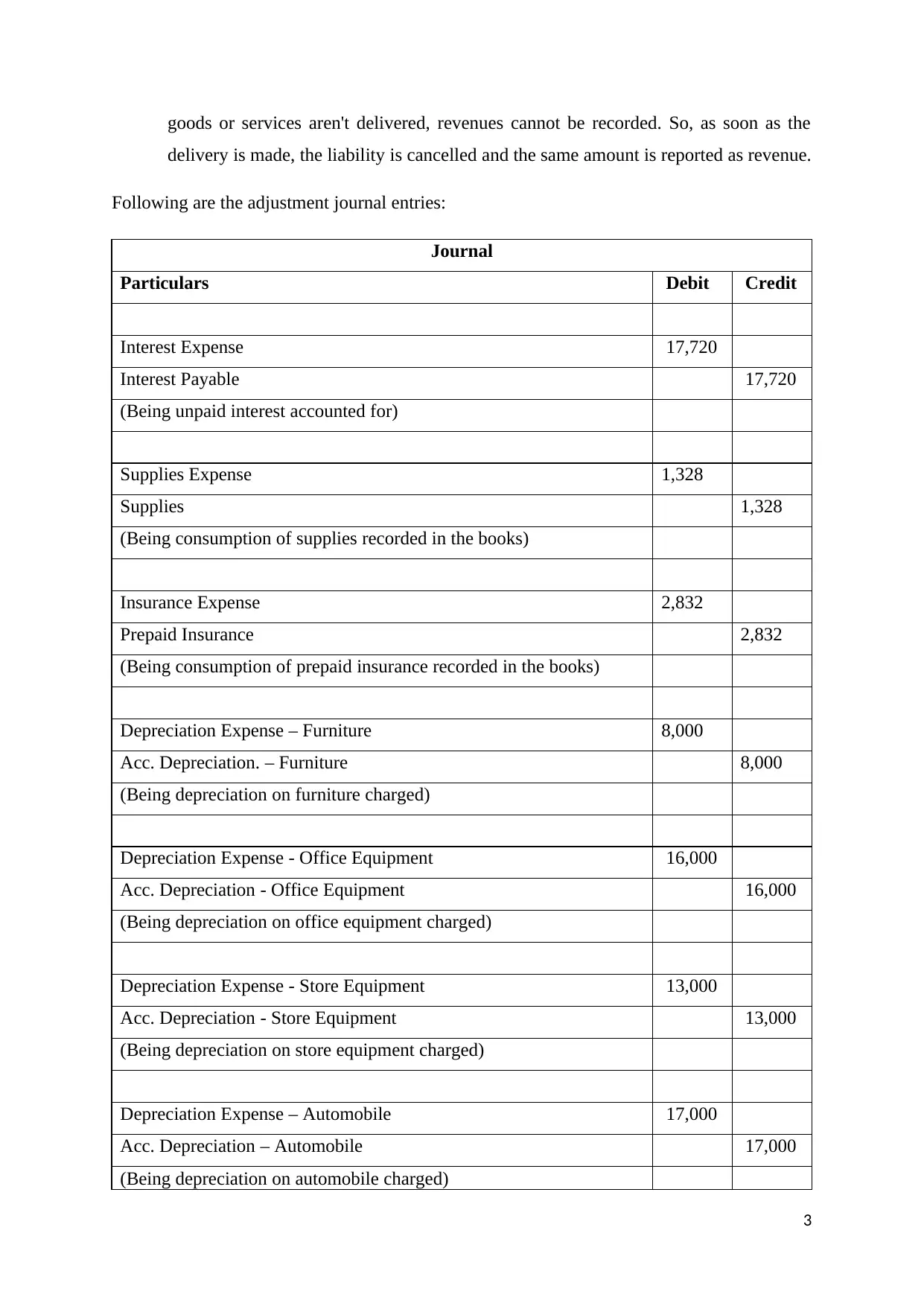

goods or services aren't delivered, revenues cannot be recorded. So, as soon as the

delivery is made, the liability is cancelled and the same amount is reported as revenue.

Following are the adjustment journal entries:

Journal

Particulars Debit Credit

Interest Expense 17,720

Interest Payable 17,720

(Being unpaid interest accounted for)

Supplies Expense 1,328

Supplies 1,328

(Being consumption of supplies recorded in the books)

Insurance Expense 2,832

Prepaid Insurance 2,832

(Being consumption of prepaid insurance recorded in the books)

Depreciation Expense – Furniture 8,000

Acc. Depreciation. – Furniture 8,000

(Being depreciation on furniture charged)

Depreciation Expense - Office Equipment 16,000

Acc. Depreciation - Office Equipment 16,000

(Being depreciation on office equipment charged)

Depreciation Expense - Store Equipment 13,000

Acc. Depreciation - Store Equipment 13,000

(Being depreciation on store equipment charged)

Depreciation Expense – Automobile 17,000

Acc. Depreciation – Automobile 17,000

(Being depreciation on automobile charged)

3

delivery is made, the liability is cancelled and the same amount is reported as revenue.

Following are the adjustment journal entries:

Journal

Particulars Debit Credit

Interest Expense 17,720

Interest Payable 17,720

(Being unpaid interest accounted for)

Supplies Expense 1,328

Supplies 1,328

(Being consumption of supplies recorded in the books)

Insurance Expense 2,832

Prepaid Insurance 2,832

(Being consumption of prepaid insurance recorded in the books)

Depreciation Expense – Furniture 8,000

Acc. Depreciation. – Furniture 8,000

(Being depreciation on furniture charged)

Depreciation Expense - Office Equipment 16,000

Acc. Depreciation - Office Equipment 16,000

(Being depreciation on office equipment charged)

Depreciation Expense - Store Equipment 13,000

Acc. Depreciation - Store Equipment 13,000

(Being depreciation on store equipment charged)

Depreciation Expense – Automobile 17,000

Acc. Depreciation – Automobile 17,000

(Being depreciation on automobile charged)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

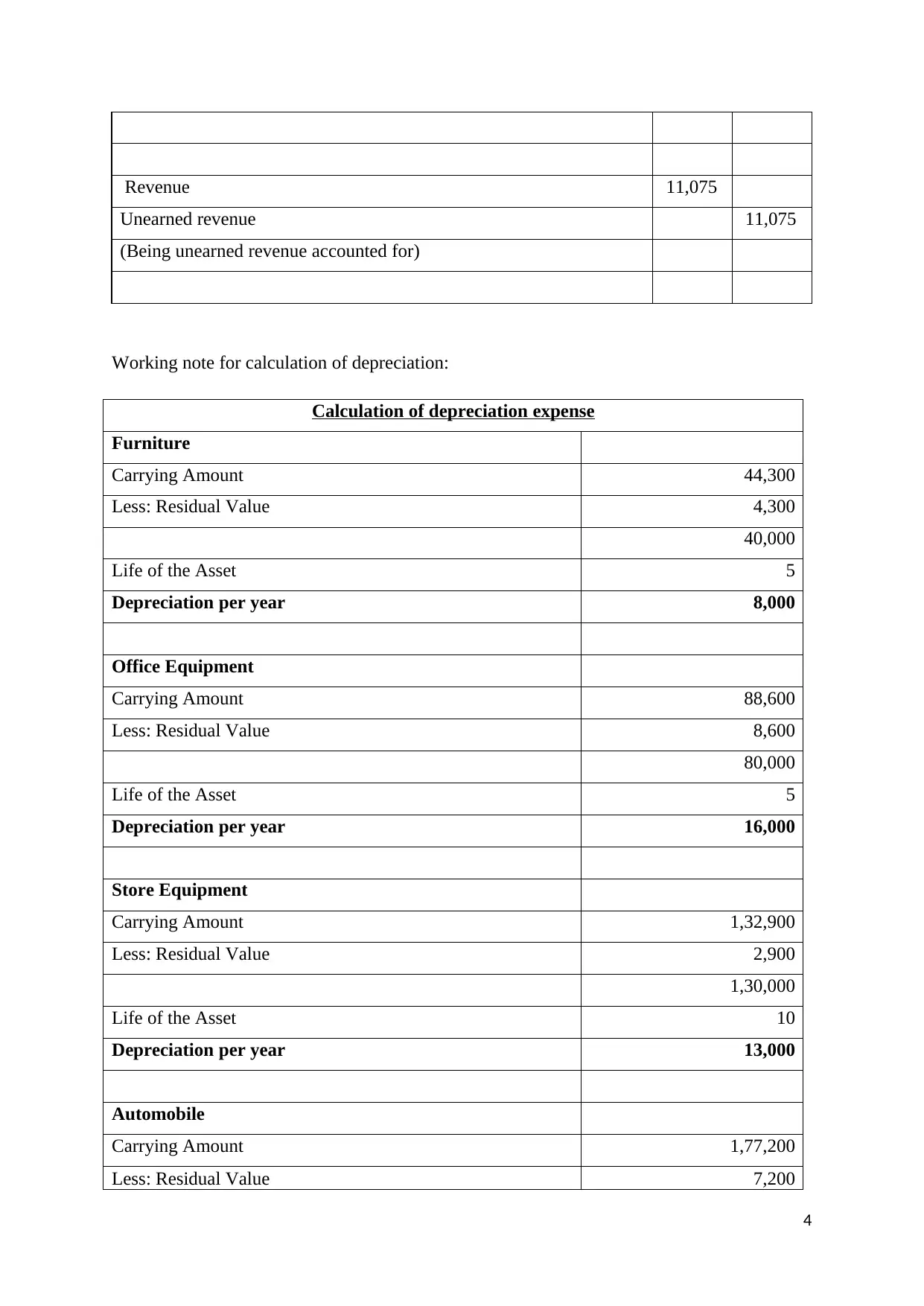

Revenue 11,075

Unearned revenue 11,075

(Being unearned revenue accounted for)

Working note for calculation of depreciation:

Calculation of depreciation expense

Furniture

Carrying Amount 44,300

Less: Residual Value 4,300

40,000

Life of the Asset 5

Depreciation per year 8,000

Office Equipment

Carrying Amount 88,600

Less: Residual Value 8,600

80,000

Life of the Asset 5

Depreciation per year 16,000

Store Equipment

Carrying Amount 1,32,900

Less: Residual Value 2,900

1,30,000

Life of the Asset 10

Depreciation per year 13,000

Automobile

Carrying Amount 1,77,200

Less: Residual Value 7,200

4

Unearned revenue 11,075

(Being unearned revenue accounted for)

Working note for calculation of depreciation:

Calculation of depreciation expense

Furniture

Carrying Amount 44,300

Less: Residual Value 4,300

40,000

Life of the Asset 5

Depreciation per year 8,000

Office Equipment

Carrying Amount 88,600

Less: Residual Value 8,600

80,000

Life of the Asset 5

Depreciation per year 16,000

Store Equipment

Carrying Amount 1,32,900

Less: Residual Value 2,900

1,30,000

Life of the Asset 10

Depreciation per year 13,000

Automobile

Carrying Amount 1,77,200

Less: Residual Value 7,200

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

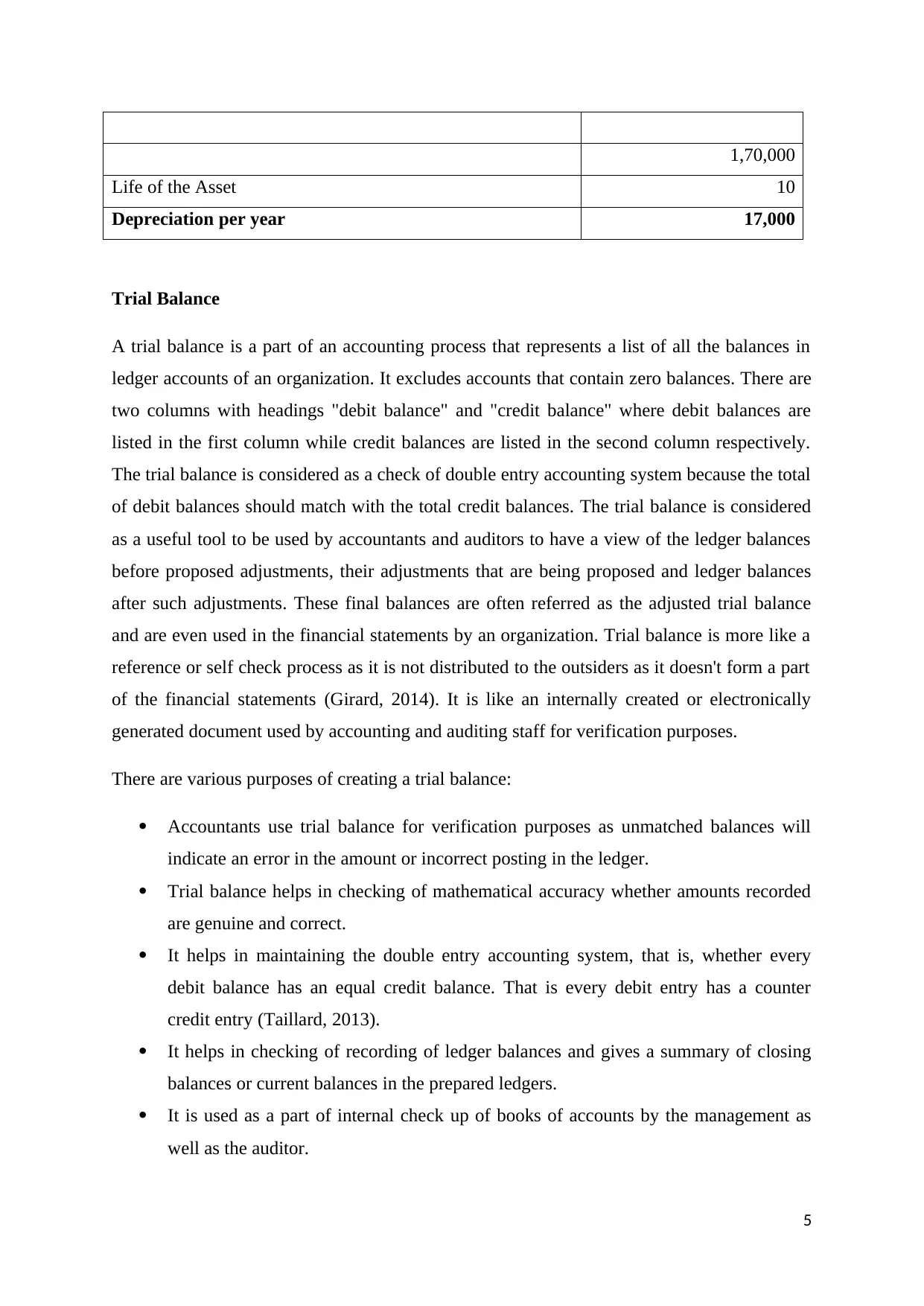

1,70,000

Life of the Asset 10

Depreciation per year 17,000

Trial Balance

A trial balance is a part of an accounting process that represents a list of all the balances in

ledger accounts of an organization. It excludes accounts that contain zero balances. There are

two columns with headings "debit balance" and "credit balance" where debit balances are

listed in the first column while credit balances are listed in the second column respectively.

The trial balance is considered as a check of double entry accounting system because the total

of debit balances should match with the total credit balances. The trial balance is considered

as a useful tool to be used by accountants and auditors to have a view of the ledger balances

before proposed adjustments, their adjustments that are being proposed and ledger balances

after such adjustments. These final balances are often referred as the adjusted trial balance

and are even used in the financial statements by an organization. Trial balance is more like a

reference or self check process as it is not distributed to the outsiders as it doesn't form a part

of the financial statements (Girard, 2014). It is like an internally created or electronically

generated document used by accounting and auditing staff for verification purposes.

There are various purposes of creating a trial balance:

Accountants use trial balance for verification purposes as unmatched balances will

indicate an error in the amount or incorrect posting in the ledger.

Trial balance helps in checking of mathematical accuracy whether amounts recorded

are genuine and correct.

It helps in maintaining the double entry accounting system, that is, whether every

debit balance has an equal credit balance. That is every debit entry has a counter

credit entry (Taillard, 2013).

It helps in checking of recording of ledger balances and gives a summary of closing

balances or current balances in the prepared ledgers.

It is used as a part of internal check up of books of accounts by the management as

well as the auditor.

5

Life of the Asset 10

Depreciation per year 17,000

Trial Balance

A trial balance is a part of an accounting process that represents a list of all the balances in

ledger accounts of an organization. It excludes accounts that contain zero balances. There are

two columns with headings "debit balance" and "credit balance" where debit balances are

listed in the first column while credit balances are listed in the second column respectively.

The trial balance is considered as a check of double entry accounting system because the total

of debit balances should match with the total credit balances. The trial balance is considered

as a useful tool to be used by accountants and auditors to have a view of the ledger balances

before proposed adjustments, their adjustments that are being proposed and ledger balances

after such adjustments. These final balances are often referred as the adjusted trial balance

and are even used in the financial statements by an organization. Trial balance is more like a

reference or self check process as it is not distributed to the outsiders as it doesn't form a part

of the financial statements (Girard, 2014). It is like an internally created or electronically

generated document used by accounting and auditing staff for verification purposes.

There are various purposes of creating a trial balance:

Accountants use trial balance for verification purposes as unmatched balances will

indicate an error in the amount or incorrect posting in the ledger.

Trial balance helps in checking of mathematical accuracy whether amounts recorded

are genuine and correct.

It helps in maintaining the double entry accounting system, that is, whether every

debit balance has an equal credit balance. That is every debit entry has a counter

credit entry (Taillard, 2013).

It helps in checking of recording of ledger balances and gives a summary of closing

balances or current balances in the prepared ledgers.

It is used as a part of internal check up of books of accounts by the management as

well as the auditor.

5

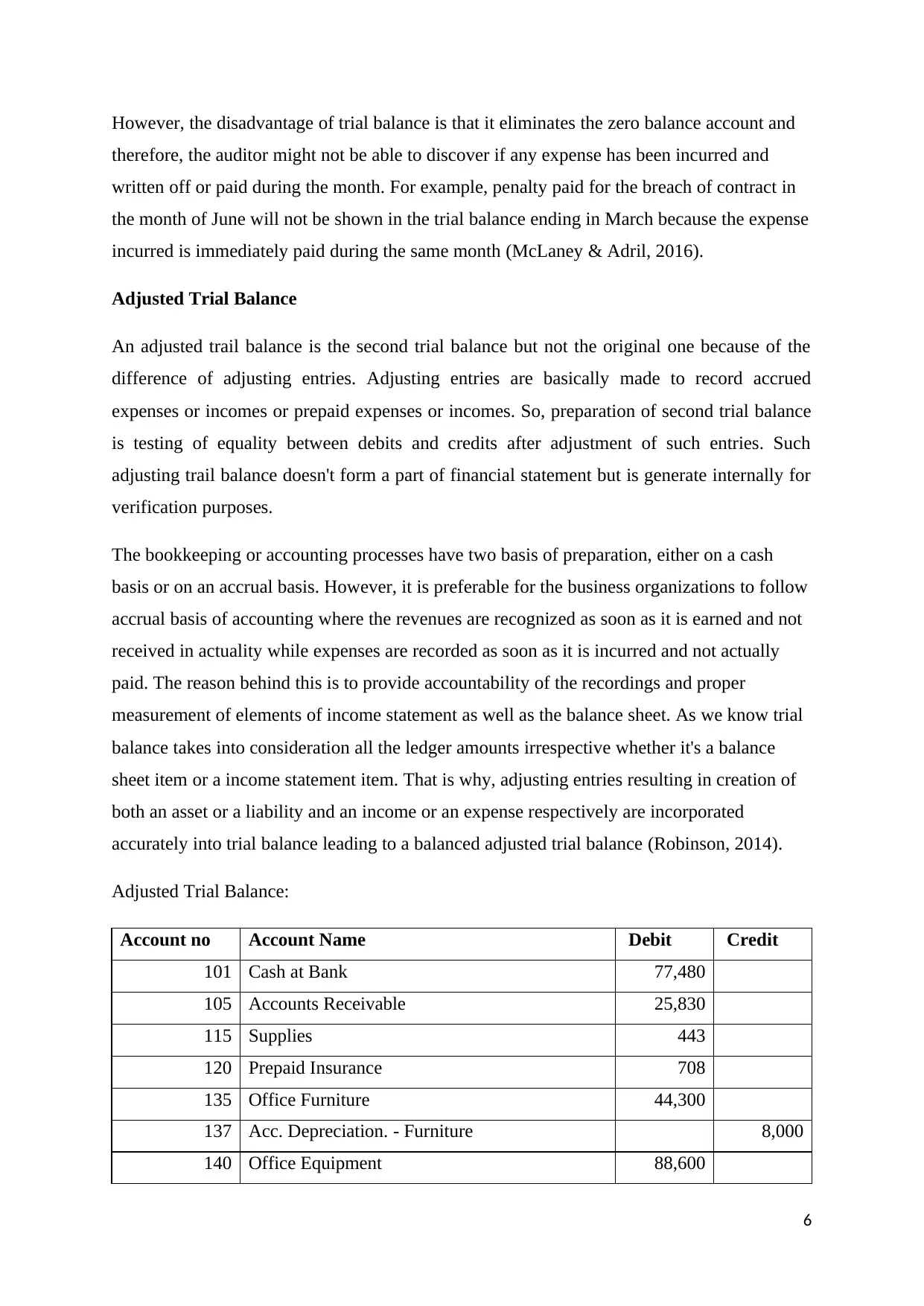

However, the disadvantage of trial balance is that it eliminates the zero balance account and

therefore, the auditor might not be able to discover if any expense has been incurred and

written off or paid during the month. For example, penalty paid for the breach of contract in

the month of June will not be shown in the trial balance ending in March because the expense

incurred is immediately paid during the same month (McLaney & Adril, 2016).

Adjusted Trial Balance

An adjusted trail balance is the second trial balance but not the original one because of the

difference of adjusting entries. Adjusting entries are basically made to record accrued

expenses or incomes or prepaid expenses or incomes. So, preparation of second trial balance

is testing of equality between debits and credits after adjustment of such entries. Such

adjusting trail balance doesn't form a part of financial statement but is generate internally for

verification purposes.

The bookkeeping or accounting processes have two basis of preparation, either on a cash

basis or on an accrual basis. However, it is preferable for the business organizations to follow

accrual basis of accounting where the revenues are recognized as soon as it is earned and not

received in actuality while expenses are recorded as soon as it is incurred and not actually

paid. The reason behind this is to provide accountability of the recordings and proper

measurement of elements of income statement as well as the balance sheet. As we know trial

balance takes into consideration all the ledger amounts irrespective whether it's a balance

sheet item or a income statement item. That is why, adjusting entries resulting in creation of

both an asset or a liability and an income or an expense respectively are incorporated

accurately into trial balance leading to a balanced adjusted trial balance (Robinson, 2014).

Adjusted Trial Balance:

Account no Account Name Debit Credit

101 Cash at Bank 77,480

105 Accounts Receivable 25,830

115 Supplies 443

120 Prepaid Insurance 708

135 Office Furniture 44,300

137 Acc. Depreciation. - Furniture 8,000

140 Office Equipment 88,600

6

therefore, the auditor might not be able to discover if any expense has been incurred and

written off or paid during the month. For example, penalty paid for the breach of contract in

the month of June will not be shown in the trial balance ending in March because the expense

incurred is immediately paid during the same month (McLaney & Adril, 2016).

Adjusted Trial Balance

An adjusted trail balance is the second trial balance but not the original one because of the

difference of adjusting entries. Adjusting entries are basically made to record accrued

expenses or incomes or prepaid expenses or incomes. So, preparation of second trial balance

is testing of equality between debits and credits after adjustment of such entries. Such

adjusting trail balance doesn't form a part of financial statement but is generate internally for

verification purposes.

The bookkeeping or accounting processes have two basis of preparation, either on a cash

basis or on an accrual basis. However, it is preferable for the business organizations to follow

accrual basis of accounting where the revenues are recognized as soon as it is earned and not

received in actuality while expenses are recorded as soon as it is incurred and not actually

paid. The reason behind this is to provide accountability of the recordings and proper

measurement of elements of income statement as well as the balance sheet. As we know trial

balance takes into consideration all the ledger amounts irrespective whether it's a balance

sheet item or a income statement item. That is why, adjusting entries resulting in creation of

both an asset or a liability and an income or an expense respectively are incorporated

accurately into trial balance leading to a balanced adjusted trial balance (Robinson, 2014).

Adjusted Trial Balance:

Account no Account Name Debit Credit

101 Cash at Bank 77,480

105 Accounts Receivable 25,830

115 Supplies 443

120 Prepaid Insurance 708

135 Office Furniture 44,300

137 Acc. Depreciation. - Furniture 8,000

140 Office Equipment 88,600

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

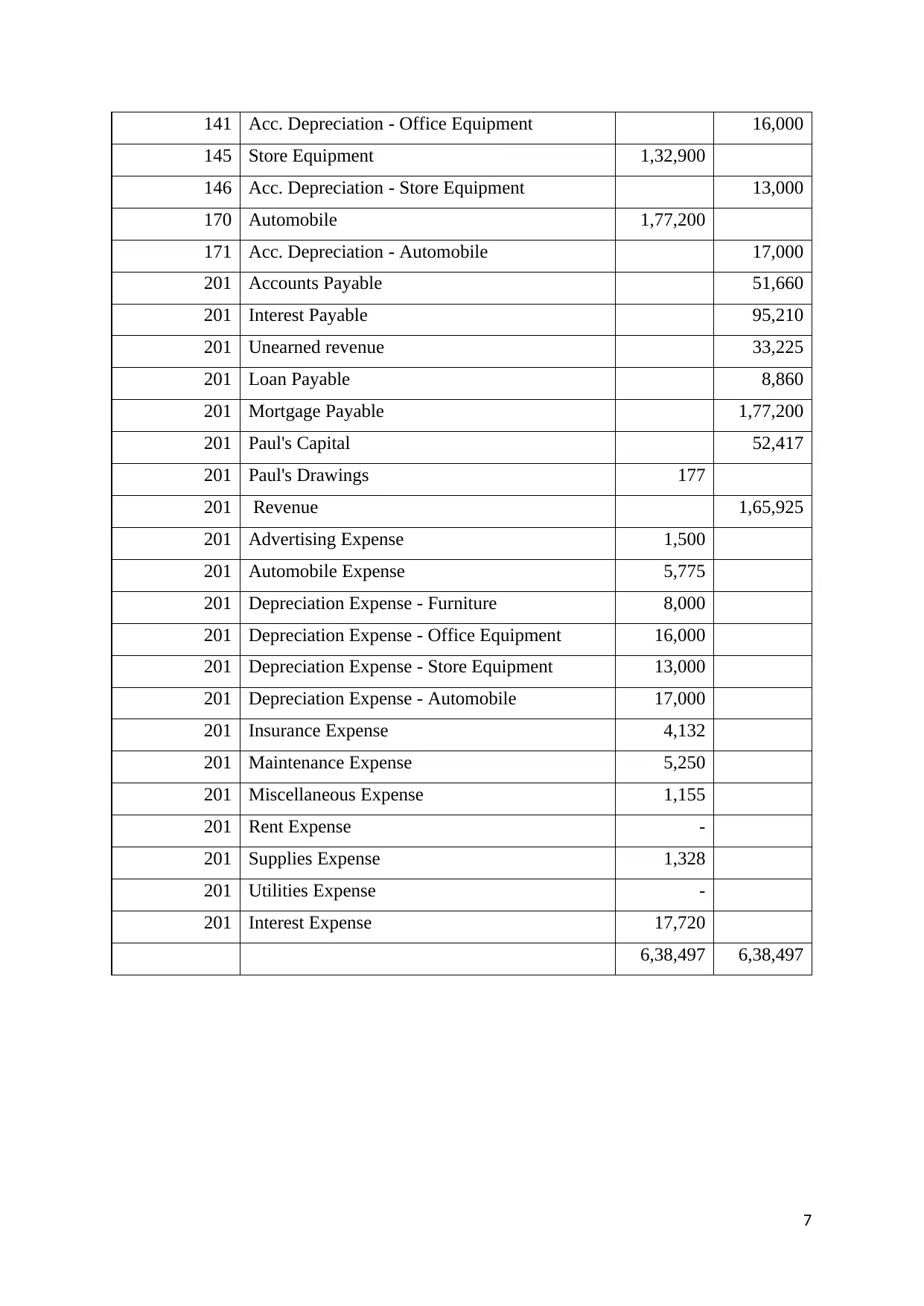

141 Acc. Depreciation - Office Equipment 16,000

145 Store Equipment 1,32,900

146 Acc. Depreciation - Store Equipment 13,000

170 Automobile 1,77,200

171 Acc. Depreciation - Automobile 17,000

201 Accounts Payable 51,660

201 Interest Payable 95,210

201 Unearned revenue 33,225

201 Loan Payable 8,860

201 Mortgage Payable 1,77,200

201 Paul's Capital 52,417

201 Paul's Drawings 177

201 Revenue 1,65,925

201 Advertising Expense 1,500

201 Automobile Expense 5,775

201 Depreciation Expense - Furniture 8,000

201 Depreciation Expense - Office Equipment 16,000

201 Depreciation Expense - Store Equipment 13,000

201 Depreciation Expense - Automobile 17,000

201 Insurance Expense 4,132

201 Maintenance Expense 5,250

201 Miscellaneous Expense 1,155

201 Rent Expense -

201 Supplies Expense 1,328

201 Utilities Expense -

201 Interest Expense 17,720

6,38,497 6,38,497

7

145 Store Equipment 1,32,900

146 Acc. Depreciation - Store Equipment 13,000

170 Automobile 1,77,200

171 Acc. Depreciation - Automobile 17,000

201 Accounts Payable 51,660

201 Interest Payable 95,210

201 Unearned revenue 33,225

201 Loan Payable 8,860

201 Mortgage Payable 1,77,200

201 Paul's Capital 52,417

201 Paul's Drawings 177

201 Revenue 1,65,925

201 Advertising Expense 1,500

201 Automobile Expense 5,775

201 Depreciation Expense - Furniture 8,000

201 Depreciation Expense - Office Equipment 16,000

201 Depreciation Expense - Store Equipment 13,000

201 Depreciation Expense - Automobile 17,000

201 Insurance Expense 4,132

201 Maintenance Expense 5,250

201 Miscellaneous Expense 1,155

201 Rent Expense -

201 Supplies Expense 1,328

201 Utilities Expense -

201 Interest Expense 17,720

6,38,497 6,38,497

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

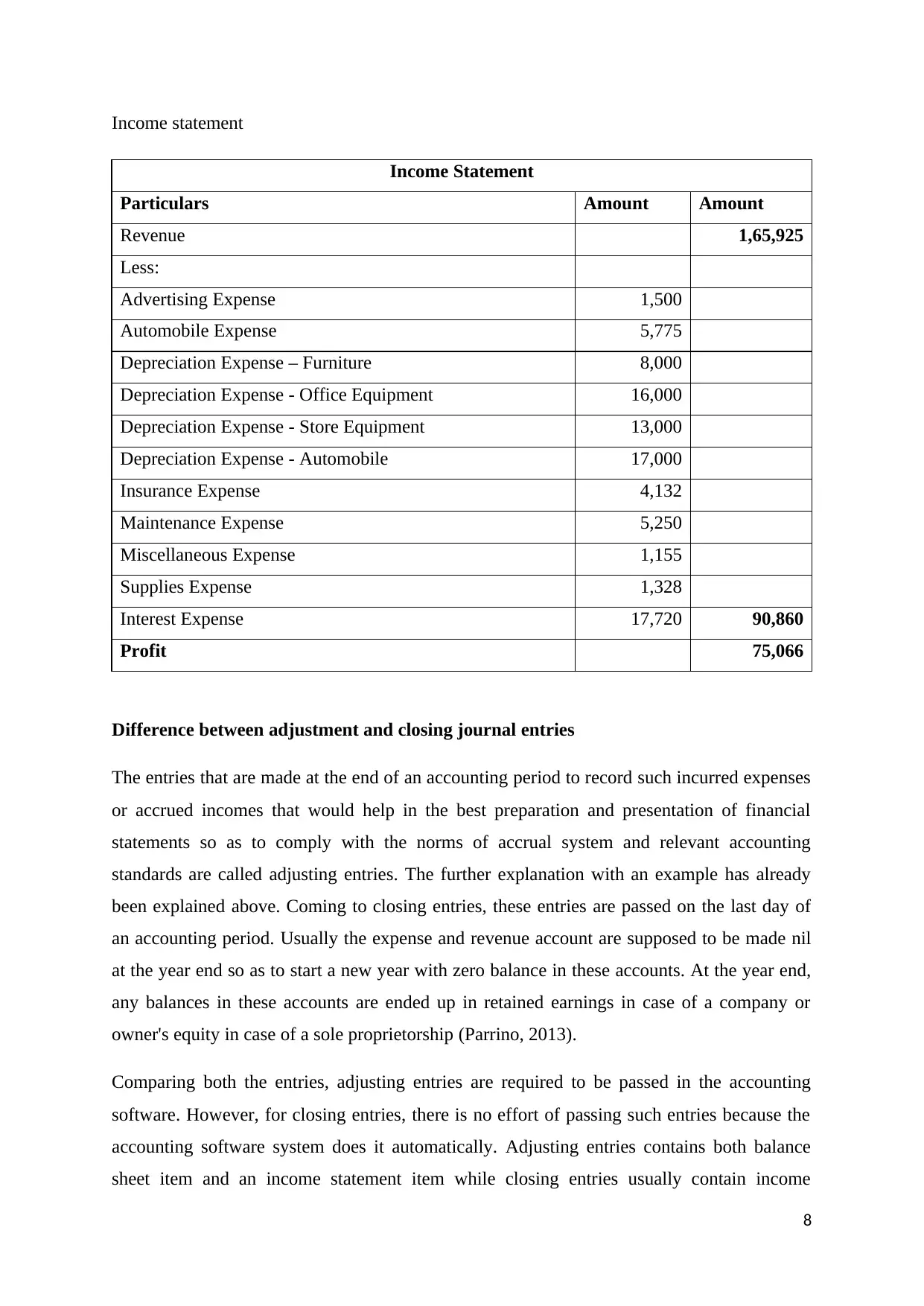

Income statement

Income Statement

Particulars Amount Amount

Revenue 1,65,925

Less:

Advertising Expense 1,500

Automobile Expense 5,775

Depreciation Expense – Furniture 8,000

Depreciation Expense - Office Equipment 16,000

Depreciation Expense - Store Equipment 13,000

Depreciation Expense - Automobile 17,000

Insurance Expense 4,132

Maintenance Expense 5,250

Miscellaneous Expense 1,155

Supplies Expense 1,328

Interest Expense 17,720 90,860

Profit 75,066

Difference between adjustment and closing journal entries

The entries that are made at the end of an accounting period to record such incurred expenses

or accrued incomes that would help in the best preparation and presentation of financial

statements so as to comply with the norms of accrual system and relevant accounting

standards are called adjusting entries. The further explanation with an example has already

been explained above. Coming to closing entries, these entries are passed on the last day of

an accounting period. Usually the expense and revenue account are supposed to be made nil

at the year end so as to start a new year with zero balance in these accounts. At the year end,

any balances in these accounts are ended up in retained earnings in case of a company or

owner's equity in case of a sole proprietorship (Parrino, 2013).

Comparing both the entries, adjusting entries are required to be passed in the accounting

software. However, for closing entries, there is no effort of passing such entries because the

accounting software system does it automatically. Adjusting entries contains both balance

sheet item and an income statement item while closing entries usually contain income

8

Income Statement

Particulars Amount Amount

Revenue 1,65,925

Less:

Advertising Expense 1,500

Automobile Expense 5,775

Depreciation Expense – Furniture 8,000

Depreciation Expense - Office Equipment 16,000

Depreciation Expense - Store Equipment 13,000

Depreciation Expense - Automobile 17,000

Insurance Expense 4,132

Maintenance Expense 5,250

Miscellaneous Expense 1,155

Supplies Expense 1,328

Interest Expense 17,720 90,860

Profit 75,066

Difference between adjustment and closing journal entries

The entries that are made at the end of an accounting period to record such incurred expenses

or accrued incomes that would help in the best preparation and presentation of financial

statements so as to comply with the norms of accrual system and relevant accounting

standards are called adjusting entries. The further explanation with an example has already

been explained above. Coming to closing entries, these entries are passed on the last day of

an accounting period. Usually the expense and revenue account are supposed to be made nil

at the year end so as to start a new year with zero balance in these accounts. At the year end,

any balances in these accounts are ended up in retained earnings in case of a company or

owner's equity in case of a sole proprietorship (Parrino, 2013).

Comparing both the entries, adjusting entries are required to be passed in the accounting

software. However, for closing entries, there is no effort of passing such entries because the

accounting software system does it automatically. Adjusting entries contains both balance

sheet item and an income statement item while closing entries usually contain income

8

statement items. Closing entries are passed for having a nil balance in the expense and

revenue account while adjusting entries are passed for recognition of accrued incomes and

incurred expenses. Adjusting entries are prior entries and are nullified as soon as the income

is received or expense is paid or goods or services are delivered, etc. However, closing entries

every year's entries (Simpson, 2012).

This is how adjusting entries and closing entries are differentiated. However, both of them are

a part of bookkeeping process for the compliance with the relevant accounting standards.

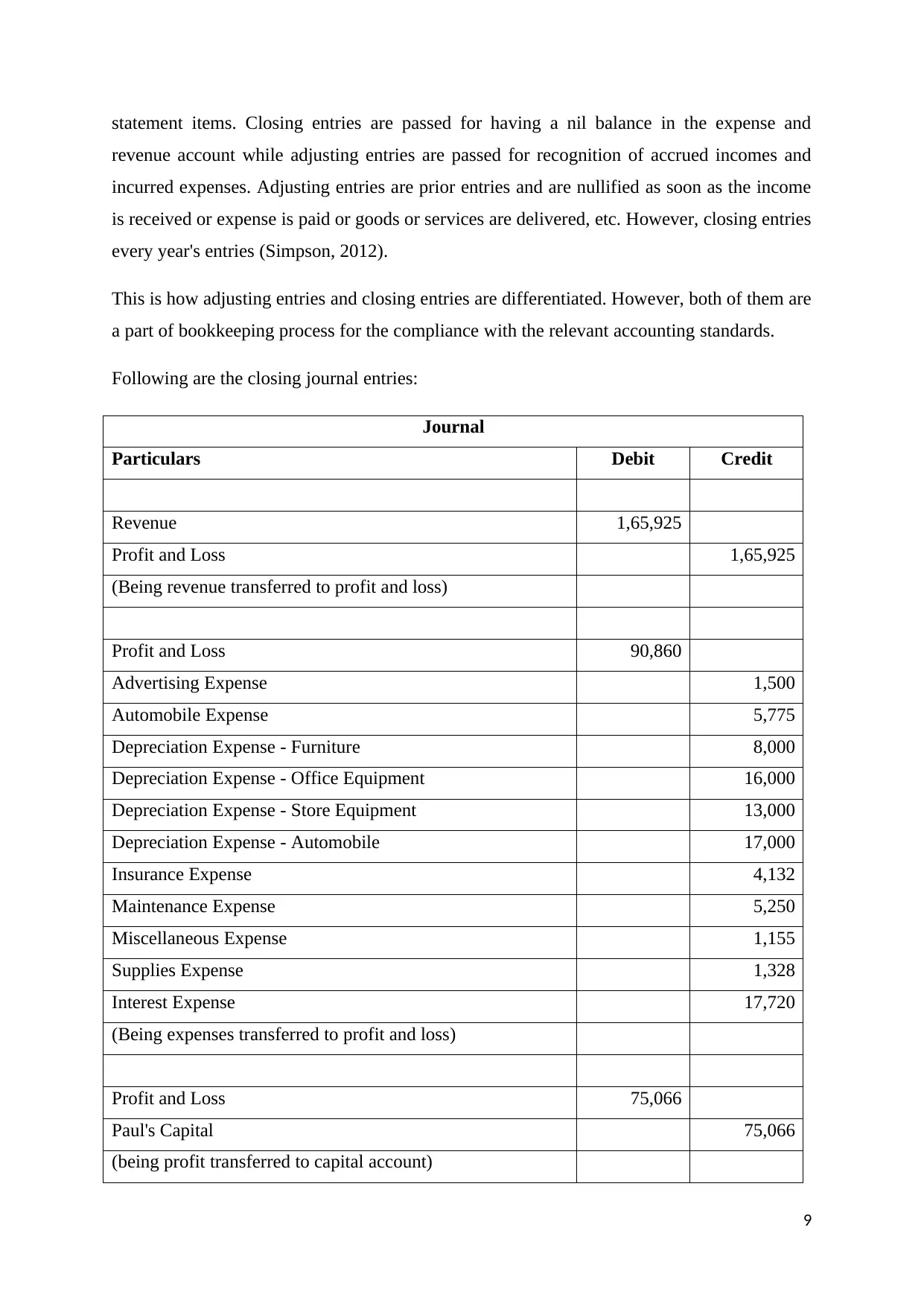

Following are the closing journal entries:

Journal

Particulars Debit Credit

Revenue 1,65,925

Profit and Loss 1,65,925

(Being revenue transferred to profit and loss)

Profit and Loss 90,860

Advertising Expense 1,500

Automobile Expense 5,775

Depreciation Expense - Furniture 8,000

Depreciation Expense - Office Equipment 16,000

Depreciation Expense - Store Equipment 13,000

Depreciation Expense - Automobile 17,000

Insurance Expense 4,132

Maintenance Expense 5,250

Miscellaneous Expense 1,155

Supplies Expense 1,328

Interest Expense 17,720

(Being expenses transferred to profit and loss)

Profit and Loss 75,066

Paul's Capital 75,066

(being profit transferred to capital account)

9

revenue account while adjusting entries are passed for recognition of accrued incomes and

incurred expenses. Adjusting entries are prior entries and are nullified as soon as the income

is received or expense is paid or goods or services are delivered, etc. However, closing entries

every year's entries (Simpson, 2012).

This is how adjusting entries and closing entries are differentiated. However, both of them are

a part of bookkeeping process for the compliance with the relevant accounting standards.

Following are the closing journal entries:

Journal

Particulars Debit Credit

Revenue 1,65,925

Profit and Loss 1,65,925

(Being revenue transferred to profit and loss)

Profit and Loss 90,860

Advertising Expense 1,500

Automobile Expense 5,775

Depreciation Expense - Furniture 8,000

Depreciation Expense - Office Equipment 16,000

Depreciation Expense - Store Equipment 13,000

Depreciation Expense - Automobile 17,000

Insurance Expense 4,132

Maintenance Expense 5,250

Miscellaneous Expense 1,155

Supplies Expense 1,328

Interest Expense 17,720

(Being expenses transferred to profit and loss)

Profit and Loss 75,066

Paul's Capital 75,066

(being profit transferred to capital account)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

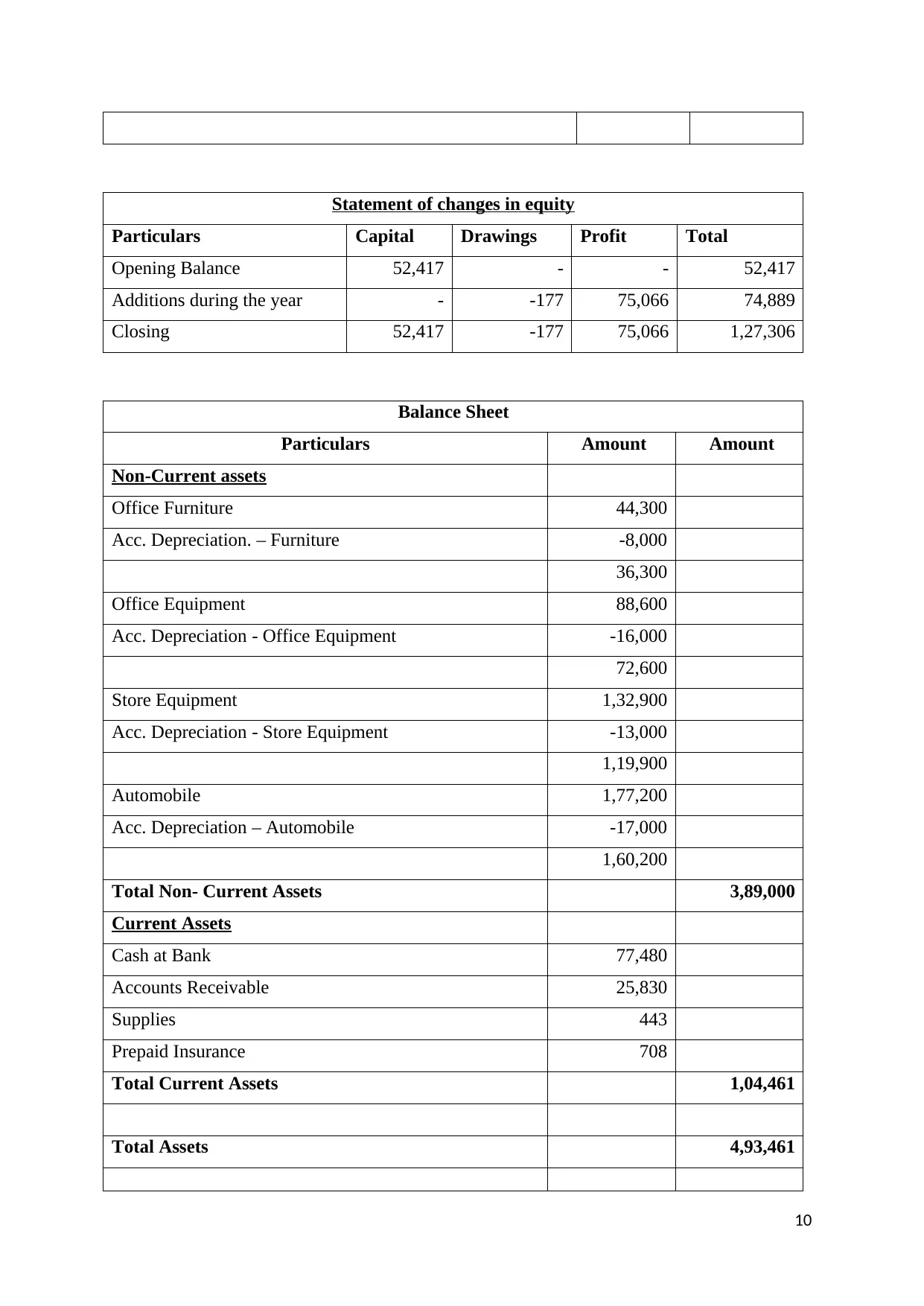

Statement of changes in equity

Particulars Capital Drawings Profit Total

Opening Balance 52,417 - - 52,417

Additions during the year - -177 75,066 74,889

Closing 52,417 -177 75,066 1,27,306

Balance Sheet

Particulars Amount Amount

Non-Current assets

Office Furniture 44,300

Acc. Depreciation. – Furniture -8,000

36,300

Office Equipment 88,600

Acc. Depreciation - Office Equipment -16,000

72,600

Store Equipment 1,32,900

Acc. Depreciation - Store Equipment -13,000

1,19,900

Automobile 1,77,200

Acc. Depreciation – Automobile -17,000

1,60,200

Total Non- Current Assets 3,89,000

Current Assets

Cash at Bank 77,480

Accounts Receivable 25,830

Supplies 443

Prepaid Insurance 708

Total Current Assets 1,04,461

Total Assets 4,93,461

10

Particulars Capital Drawings Profit Total

Opening Balance 52,417 - - 52,417

Additions during the year - -177 75,066 74,889

Closing 52,417 -177 75,066 1,27,306

Balance Sheet

Particulars Amount Amount

Non-Current assets

Office Furniture 44,300

Acc. Depreciation. – Furniture -8,000

36,300

Office Equipment 88,600

Acc. Depreciation - Office Equipment -16,000

72,600

Store Equipment 1,32,900

Acc. Depreciation - Store Equipment -13,000

1,19,900

Automobile 1,77,200

Acc. Depreciation – Automobile -17,000

1,60,200

Total Non- Current Assets 3,89,000

Current Assets

Cash at Bank 77,480

Accounts Receivable 25,830

Supplies 443

Prepaid Insurance 708

Total Current Assets 1,04,461

Total Assets 4,93,461

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

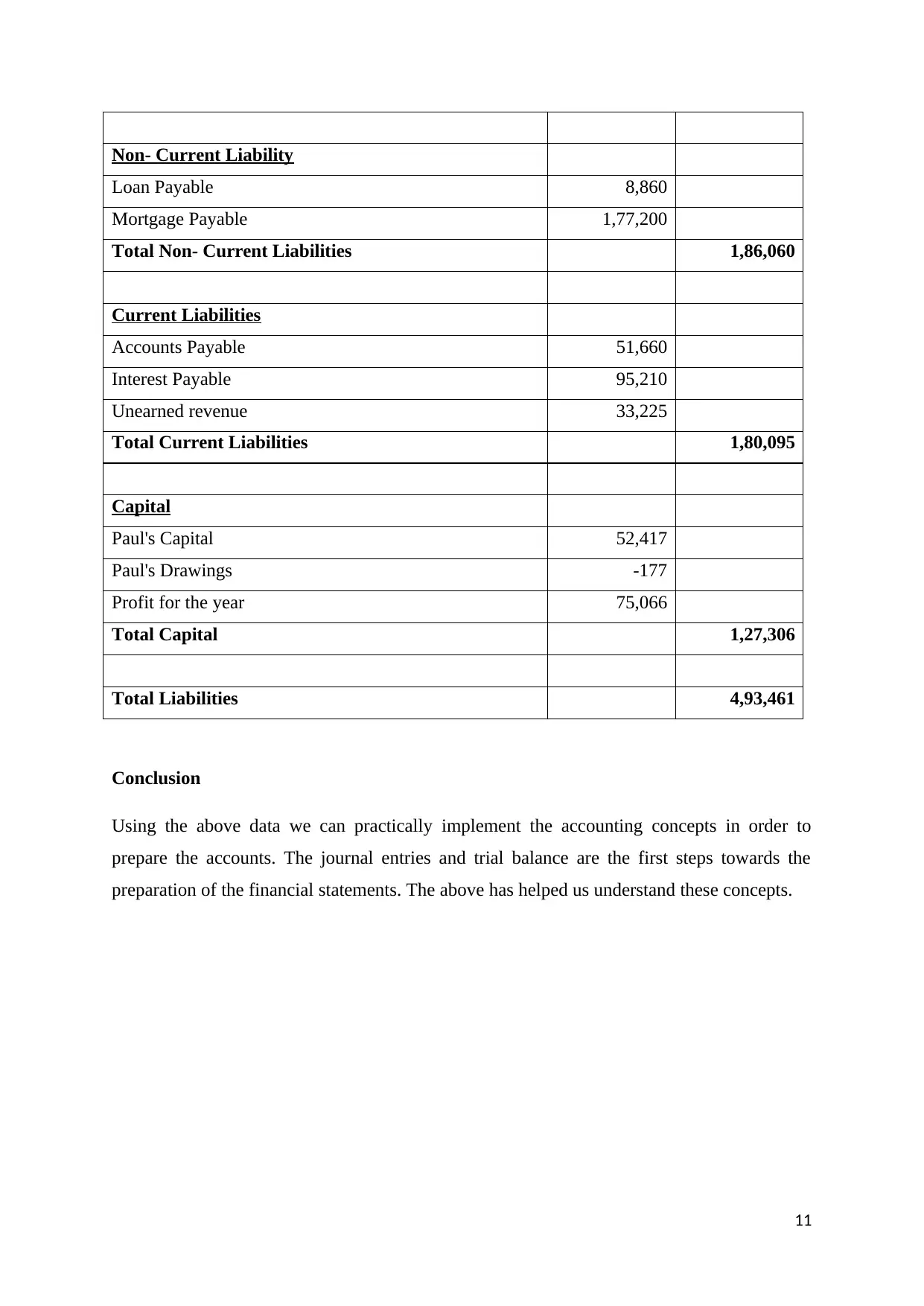

Non- Current Liability

Loan Payable 8,860

Mortgage Payable 1,77,200

Total Non- Current Liabilities 1,86,060

Current Liabilities

Accounts Payable 51,660

Interest Payable 95,210

Unearned revenue 33,225

Total Current Liabilities 1,80,095

Capital

Paul's Capital 52,417

Paul's Drawings -177

Profit for the year 75,066

Total Capital 1,27,306

Total Liabilities 4,93,461

Conclusion

Using the above data we can practically implement the accounting concepts in order to

prepare the accounts. The journal entries and trial balance are the first steps towards the

preparation of the financial statements. The above has helped us understand these concepts.

11

Loan Payable 8,860

Mortgage Payable 1,77,200

Total Non- Current Liabilities 1,86,060

Current Liabilities

Accounts Payable 51,660

Interest Payable 95,210

Unearned revenue 33,225

Total Current Liabilities 1,80,095

Capital

Paul's Capital 52,417

Paul's Drawings -177

Profit for the year 75,066

Total Capital 1,27,306

Total Liabilities 4,93,461

Conclusion

Using the above data we can practically implement the accounting concepts in order to

prepare the accounts. The journal entries and trial balance are the first steps towards the

preparation of the financial statements. The above has helped us understand these concepts.

11

Bibliography

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Parrino, R. (2013). Fundamentals of Corporate Finance, 2nd Edition. Milton: John Wiley &

Sons.

Piper, M. (2015). Accounting made simple. United States: CreateSpace Pub.

Robinson, T. (2014). Business accounting. New York, NY: Prentice Hall.

Siciliano, G. (2015). Finance for Nonfinancial Managers. New York: McGraw-Hill.

Simpson, M. (2012). Financial accounting. Basingstoke: Macmillan Press.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

12

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Parrino, R. (2013). Fundamentals of Corporate Finance, 2nd Edition. Milton: John Wiley &

Sons.

Piper, M. (2015). Accounting made simple. United States: CreateSpace Pub.

Robinson, T. (2014). Business accounting. New York, NY: Prentice Hall.

Siciliano, G. (2015). Finance for Nonfinancial Managers. New York: McGraw-Hill.

Simpson, M. (2012). Financial accounting. Basingstoke: Macmillan Press.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.