ACC506 Task 2B: Financial Statement Analysis and Ratios - R Reed Co.

VerifiedAdded on 2023/06/15

|10

|1382

|335

Report

AI Summary

This report presents a summarized analysis of the financial statements for R Reed Co Pty Ltd, covering the period from July 2016 to June 2017. It includes an income statement, balance sheet, and equity statement, followed by a ratio analysis focusing on liquidity and profitability. The current and quick ratios indicate a strong liquidity position compared to competitors, while the gross profit ratio is within the competitive range. However, the company experienced a net loss due to high operating expenses. The report also discusses different depreciation and inventory valuation methods, as well as internal controls that can be implemented to mitigate financial and operational risks. The analysis highlights the importance of understanding accounting concepts for effective financial statement preparation and presentation.

Running Head: Accounting System

Accounting Concepts

Accounting Concepts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting System 1

Executive summary:

The financial statements of Ryan Reed are presented in the summarised manner in this report.

From the financial statements, the liquidity and profitability position is evaluated using the

ratio analysis technique. The current ratio and quick ratio of the company are showing better

results than the corresponding tentative results of its competing firm which indicates that it

has sound liquidity position. Also, the gross profit of the company is also with the range of

profits earned by its competitors. However, the net profit of the company is negative which

signifies that the company has incurred losses because of spending more amount in operating

expenses than its overall income in the concerned financial year.

Executive summary:

The financial statements of Ryan Reed are presented in the summarised manner in this report.

From the financial statements, the liquidity and profitability position is evaluated using the

ratio analysis technique. The current ratio and quick ratio of the company are showing better

results than the corresponding tentative results of its competing firm which indicates that it

has sound liquidity position. Also, the gross profit of the company is also with the range of

profits earned by its competitors. However, the net profit of the company is negative which

signifies that the company has incurred losses because of spending more amount in operating

expenses than its overall income in the concerned financial year.

Accounting System 2

Table of Contents

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................3

Part a: Summarised Financial Statements.............................................................................................3

Part b: Ratio Analysis.............................................................................................................................5

Part c: Methods of Depreciation...........................................................................................................6

Part d: Methods of Inventory Valuation................................................................................................7

Part e: Internal Controls........................................................................................................................7

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

Table of Contents

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................3

Part a: Summarised Financial Statements.............................................................................................3

Part b: Ratio Analysis.............................................................................................................................5

Part c: Methods of Depreciation...........................................................................................................6

Part d: Methods of Inventory Valuation................................................................................................7

Part e: Internal Controls........................................................................................................................7

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting System 3

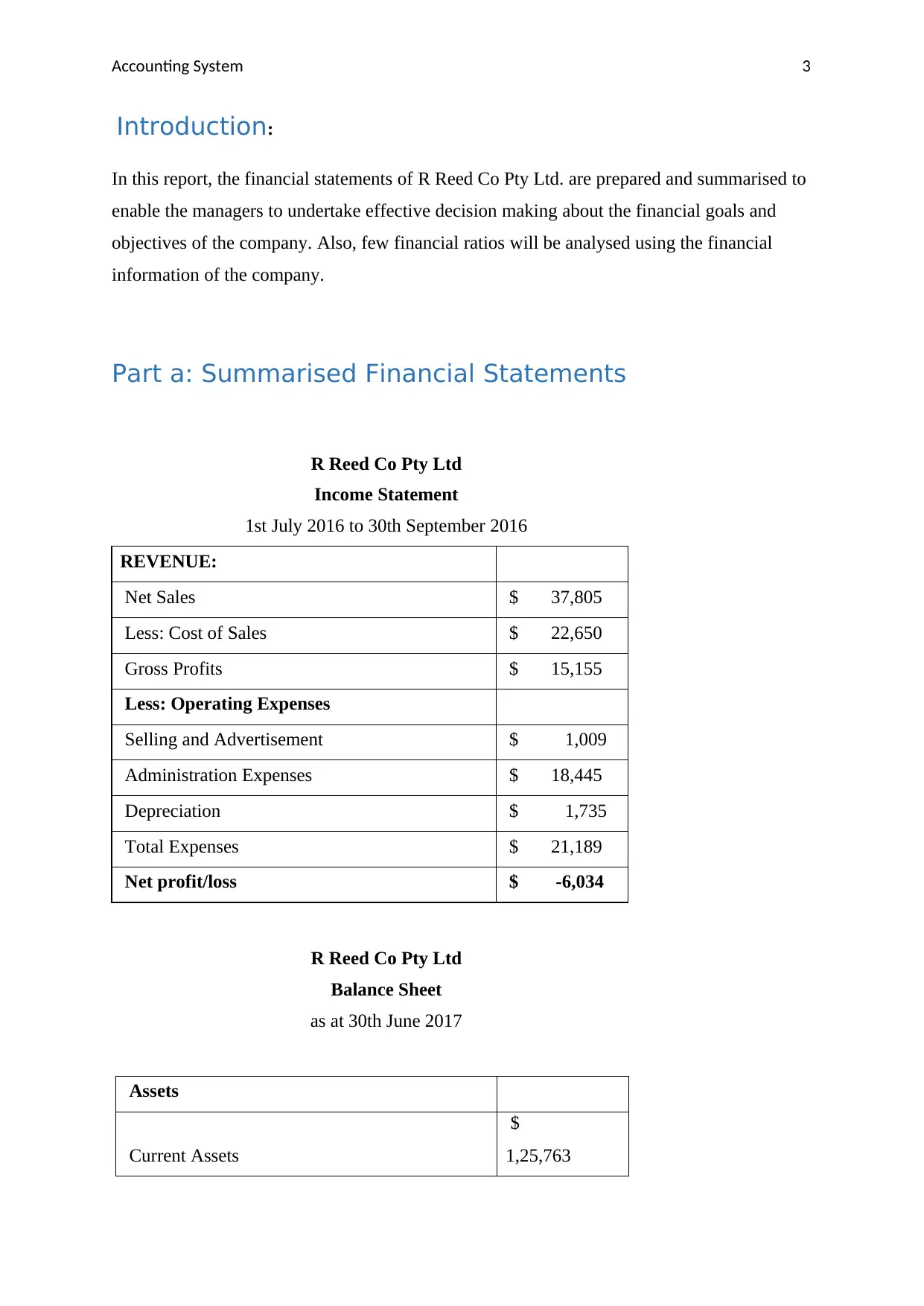

Introduction:

In this report, the financial statements of R Reed Co Pty Ltd. are prepared and summarised to

enable the managers to undertake effective decision making about the financial goals and

objectives of the company. Also, few financial ratios will be analysed using the financial

information of the company.

Part a: Summarised Financial Statements

R Reed Co Pty Ltd

Income Statement

1st July 2016 to 30th September 2016

REVENUE:

Net Sales $ 37,805

Less: Cost of Sales $ 22,650

Gross Profits $ 15,155

Less: Operating Expenses

Selling and Advertisement $ 1,009

Administration Expenses $ 18,445

Depreciation $ 1,735

Total Expenses $ 21,189

Net profit/loss $ -6,034

R Reed Co Pty Ltd

Balance Sheet

as at 30th June 2017

Assets

Current Assets

$

1,25,763

Introduction:

In this report, the financial statements of R Reed Co Pty Ltd. are prepared and summarised to

enable the managers to undertake effective decision making about the financial goals and

objectives of the company. Also, few financial ratios will be analysed using the financial

information of the company.

Part a: Summarised Financial Statements

R Reed Co Pty Ltd

Income Statement

1st July 2016 to 30th September 2016

REVENUE:

Net Sales $ 37,805

Less: Cost of Sales $ 22,650

Gross Profits $ 15,155

Less: Operating Expenses

Selling and Advertisement $ 1,009

Administration Expenses $ 18,445

Depreciation $ 1,735

Total Expenses $ 21,189

Net profit/loss $ -6,034

R Reed Co Pty Ltd

Balance Sheet

as at 30th June 2017

Assets

Current Assets

$

1,25,763

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting System 4

Non- Current Assets

$

4,574

Total Assets

$

1,30,337

Liabilities

Current Liabilities

$

17,872

Non- Current Liabilities

$

-

Total Liabilities

$

17,872

Equities

$

1,12,466

Total of Equities and Liabilities

$

1,30,337

R Reed Co Pty Ltd

Equity Statement

30th June 2017

Beginning Equity

Add Capital Contributions

$

1,25,000

Less: Drawings

-$

6,500

Add: Net Profit

-$

6,034

Non- Current Assets

$

4,574

Total Assets

$

1,30,337

Liabilities

Current Liabilities

$

17,872

Non- Current Liabilities

$

-

Total Liabilities

$

17,872

Equities

$

1,12,466

Total of Equities and Liabilities

$

1,30,337

R Reed Co Pty Ltd

Equity Statement

30th June 2017

Beginning Equity

Add Capital Contributions

$

1,25,000

Less: Drawings

-$

6,500

Add: Net Profit

-$

6,034

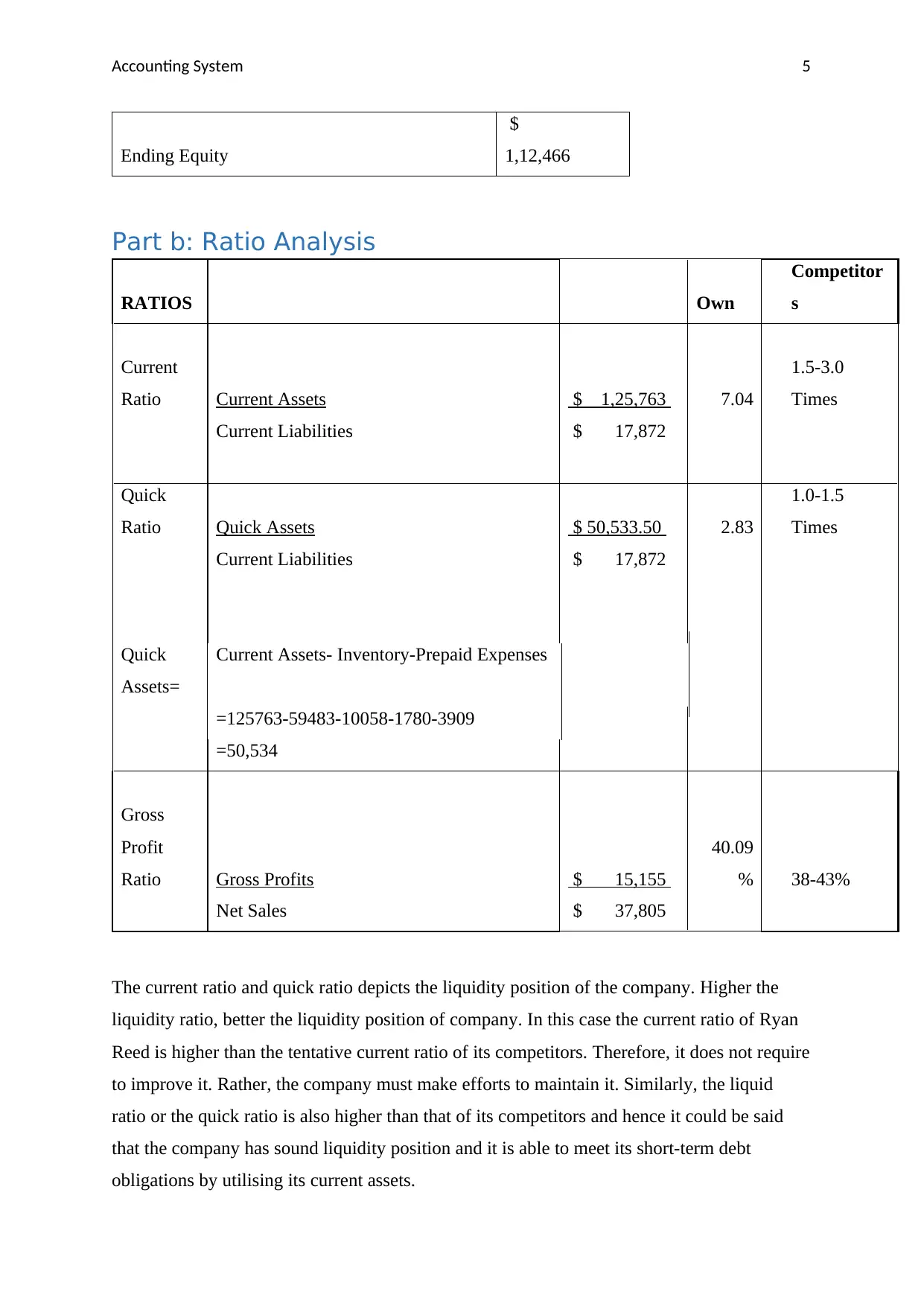

Accounting System 5

Ending Equity

$

1,12,466

Part b: Ratio Analysis

RATIOS Own

Competitor

s

Current

Ratio Current Assets $ 1,25,763 7.04

1.5-3.0

Times

Current Liabilities $ 17,872

Quick

Ratio Quick Assets $ 50,533.50 2.83

1.0-1.5

Times

Current Liabilities $ 17,872

Quick

Assets=

Current Assets- Inventory-Prepaid Expenses

=125763-59483-10058-1780-3909

=50,534

Gross

Profit

Ratio Gross Profits $ 15,155

40.09

% 38-43%

Net Sales $ 37,805

The current ratio and quick ratio depicts the liquidity position of the company. Higher the

liquidity ratio, better the liquidity position of company. In this case the current ratio of Ryan

Reed is higher than the tentative current ratio of its competitors. Therefore, it does not require

to improve it. Rather, the company must make efforts to maintain it. Similarly, the liquid

ratio or the quick ratio is also higher than that of its competitors and hence it could be said

that the company has sound liquidity position and it is able to meet its short-term debt

obligations by utilising its current assets.

Ending Equity

$

1,12,466

Part b: Ratio Analysis

RATIOS Own

Competitor

s

Current

Ratio Current Assets $ 1,25,763 7.04

1.5-3.0

Times

Current Liabilities $ 17,872

Quick

Ratio Quick Assets $ 50,533.50 2.83

1.0-1.5

Times

Current Liabilities $ 17,872

Quick

Assets=

Current Assets- Inventory-Prepaid Expenses

=125763-59483-10058-1780-3909

=50,534

Gross

Profit

Ratio Gross Profits $ 15,155

40.09

% 38-43%

Net Sales $ 37,805

The current ratio and quick ratio depicts the liquidity position of the company. Higher the

liquidity ratio, better the liquidity position of company. In this case the current ratio of Ryan

Reed is higher than the tentative current ratio of its competitors. Therefore, it does not require

to improve it. Rather, the company must make efforts to maintain it. Similarly, the liquid

ratio or the quick ratio is also higher than that of its competitors and hence it could be said

that the company has sound liquidity position and it is able to meet its short-term debt

obligations by utilising its current assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting System 6

The gross profit ratio of the Ryan Reed is within the range of competitors and hence it could

be said that company has a good GP ratio. However, it must make efforts to make the GP

ratio reach at the upper level of the range i.e. 43%.

Part c: Methods of Depreciation

Depreciation is an accounting concept where the cost of the asset is reduced every year in a

systematic manner until it becomes zero or negligible so that it can be replaced at the end of

its useful life using the funds accumulated in the name of depreciation. The acquired value of

any fixed asset is reduced to account for the wear and tear nature of such assets and due to

asset obsolescence factor.

Methods of depreciation:

Straight line method:

Under this method the cost of acquisition of asset is evenly distributed to the useful life of

such asset after reducing the estimated salvage value of the asset. Therefore, the amount of

depreciation remains equal in all the years.

Advantage:

Ease of calculation of depreciation amount.

Disadvantage:

It does not take into account the rate at which the asset will actually depreciate in value.

Written down method:

Under this method also, depreciation expense changes every year and it reduced with the

reduction in the carrying amount of the asset. In the initial year of asset acquisition, higher

depreciation is booked and then it reduces (Astami & Tower, 2006).

Advantage:

Accelerated depreciation reduced the tax obligations of current as well as previous years.

Disadvantage:

Complex method of depreciation calculation.

Sum of Years Digits:

The gross profit ratio of the Ryan Reed is within the range of competitors and hence it could

be said that company has a good GP ratio. However, it must make efforts to make the GP

ratio reach at the upper level of the range i.e. 43%.

Part c: Methods of Depreciation

Depreciation is an accounting concept where the cost of the asset is reduced every year in a

systematic manner until it becomes zero or negligible so that it can be replaced at the end of

its useful life using the funds accumulated in the name of depreciation. The acquired value of

any fixed asset is reduced to account for the wear and tear nature of such assets and due to

asset obsolescence factor.

Methods of depreciation:

Straight line method:

Under this method the cost of acquisition of asset is evenly distributed to the useful life of

such asset after reducing the estimated salvage value of the asset. Therefore, the amount of

depreciation remains equal in all the years.

Advantage:

Ease of calculation of depreciation amount.

Disadvantage:

It does not take into account the rate at which the asset will actually depreciate in value.

Written down method:

Under this method also, depreciation expense changes every year and it reduced with the

reduction in the carrying amount of the asset. In the initial year of asset acquisition, higher

depreciation is booked and then it reduces (Astami & Tower, 2006).

Advantage:

Accelerated depreciation reduced the tax obligations of current as well as previous years.

Disadvantage:

Complex method of depreciation calculation.

Sum of Years Digits:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting System 7

Under this method depreciation rate is calculated annually by summing up all the years of

available useful life in each year.

Advantage:

Accelerates depreciation that is recorded in the initial year of asset’s life.

Disadvantage:

Complex method of depreciation calculation.

Part d: Methods of Inventory Valuation

Methods of inventory valuation other than weighted average perpetual stock method:

First in first out:

Under this method, the closing inventory is valued on the assumption that the inventory that

is purchased firstly, it issued to the production earlier than the inventory that is purchased

lately. Therefore, the remaining inventory with the business is valued on the basis of cost of

purchase of last inventories. The balance sheet amount of inventory will be in line with its

current market price if FIFO is used. It may increase or decrease the profitability based on the

last purchase prices of inventory units.

Last in first out:

Under this method inventory is valued on the basis of assumption that the inventory that was

purchased latest is issued to the production firstly and therefore, the closing inventory is

calculated on the basis of cost of purchases of first purchase or earliest date of purchase of

inventory (Lee, 2006). It will result in better matching of sales revenue with costs. It may

increase or decrease the profitability of the company depending upon the purchase prices of

earlier periods.

Part e: Internal Controls

Internal controls are the processes that helps the business organisations to avoid financial and

operational risks so that effective flow of business activities can be continued in long run.

In the present case of Ryan Reed Company, following internal controls can be implemented:

In the areas of high risks or complexities such as receivables management, GST return

preparation and calculation, inventory management, the manager must hire personnel with

requisite knowledge and segregate their duties according to their expertise.

Under this method depreciation rate is calculated annually by summing up all the years of

available useful life in each year.

Advantage:

Accelerates depreciation that is recorded in the initial year of asset’s life.

Disadvantage:

Complex method of depreciation calculation.

Part d: Methods of Inventory Valuation

Methods of inventory valuation other than weighted average perpetual stock method:

First in first out:

Under this method, the closing inventory is valued on the assumption that the inventory that

is purchased firstly, it issued to the production earlier than the inventory that is purchased

lately. Therefore, the remaining inventory with the business is valued on the basis of cost of

purchase of last inventories. The balance sheet amount of inventory will be in line with its

current market price if FIFO is used. It may increase or decrease the profitability based on the

last purchase prices of inventory units.

Last in first out:

Under this method inventory is valued on the basis of assumption that the inventory that was

purchased latest is issued to the production firstly and therefore, the closing inventory is

calculated on the basis of cost of purchases of first purchase or earliest date of purchase of

inventory (Lee, 2006). It will result in better matching of sales revenue with costs. It may

increase or decrease the profitability of the company depending upon the purchase prices of

earlier periods.

Part e: Internal Controls

Internal controls are the processes that helps the business organisations to avoid financial and

operational risks so that effective flow of business activities can be continued in long run.

In the present case of Ryan Reed Company, following internal controls can be implemented:

In the areas of high risks or complexities such as receivables management, GST return

preparation and calculation, inventory management, the manager must hire personnel with

requisite knowledge and segregate their duties according to their expertise.

Accounting System 8

At every month-end, the manager must cross verify its cash records with its bank statements

for all the transactions that are done through banking processes so that any mismatching of

amounts is identified promptly.

Conclusion:

It can be concluded that the understanding of proper accounting concepts is necessary for the

adequate preparation and presentation of financial statements of the company. From the

above ratio analysis the profitability and liquidity position of company is found to be sound.

At every month-end, the manager must cross verify its cash records with its bank statements

for all the transactions that are done through banking processes so that any mismatching of

amounts is identified promptly.

Conclusion:

It can be concluded that the understanding of proper accounting concepts is necessary for the

adequate preparation and presentation of financial statements of the company. From the

above ratio analysis the profitability and liquidity position of company is found to be sound.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting System 9

References:

Astami, E. W., & Tower, G. (2006). Accounting-policy choice and firm characteristics in the

Asia Pacific region: An international empirical test of costly contracting theory. The

International Journal of Accounting, 41(1), 1-21.

Lee, C. C. (2006). Two-warehouse inventory model with deterioration under FIFO

dispatching policy. European Journal of Operational Research, 174(2), 861-873.

References:

Astami, E. W., & Tower, G. (2006). Accounting-policy choice and firm characteristics in the

Asia Pacific region: An international empirical test of costly contracting theory. The

International Journal of Accounting, 41(1), 1-21.

Lee, C. C. (2006). Two-warehouse inventory model with deterioration under FIFO

dispatching policy. European Journal of Operational Research, 174(2), 861-873.

1 out of 10