ACT305 Corporate Accounting: Investment Analysis and Consolidation

VerifiedAdded on 2023/06/03

|14

|1290

|328

Homework Assignment

AI Summary

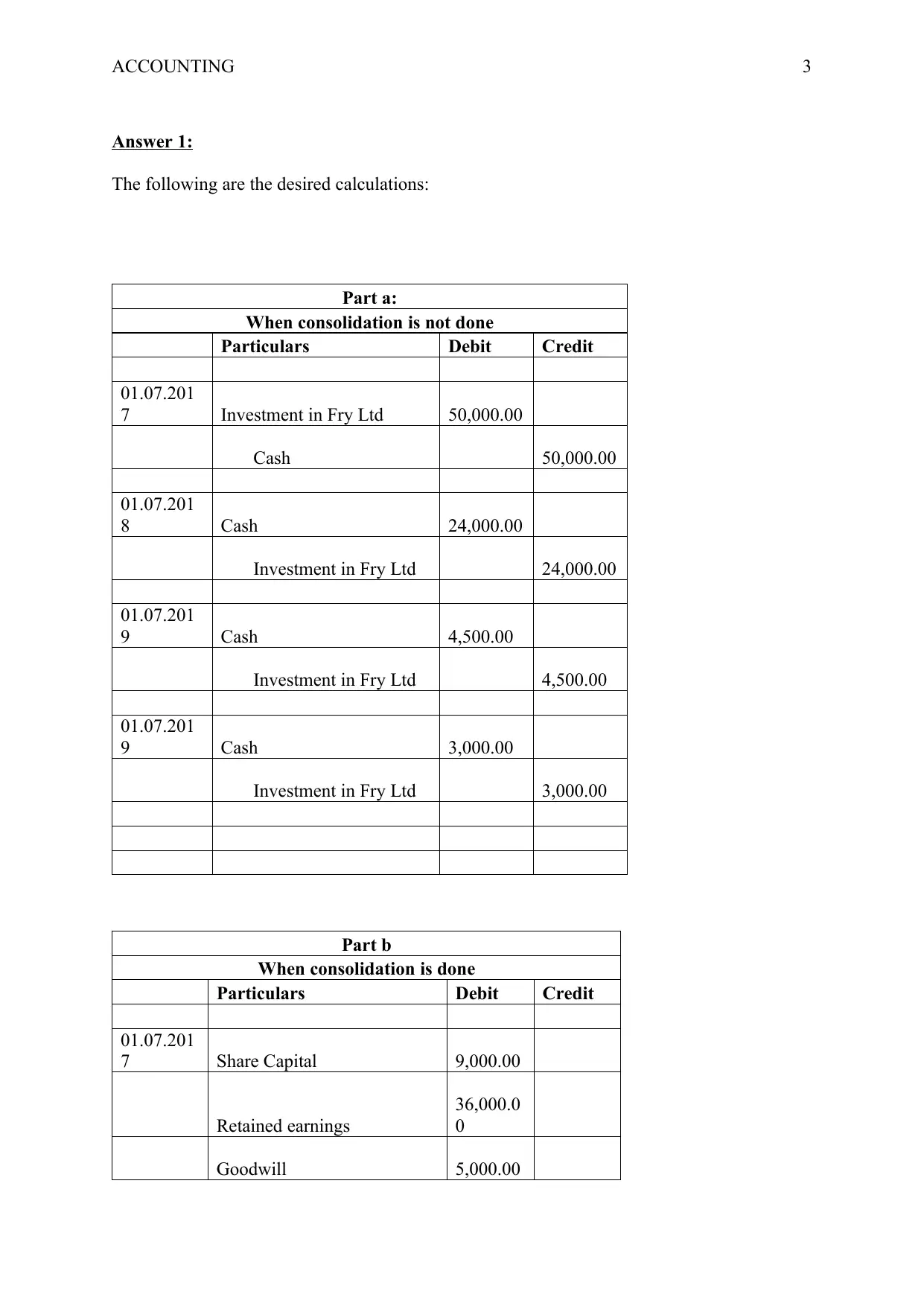

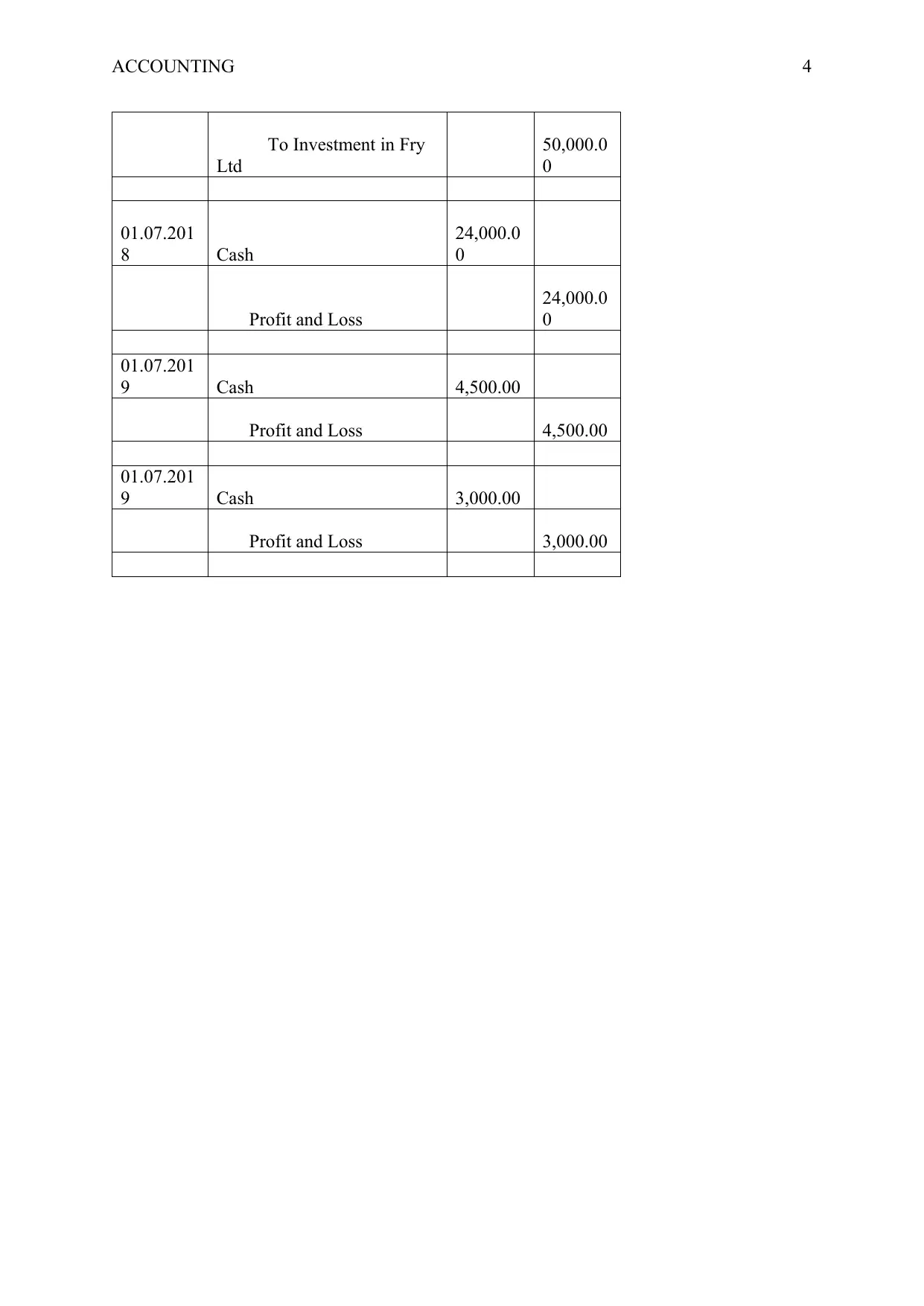

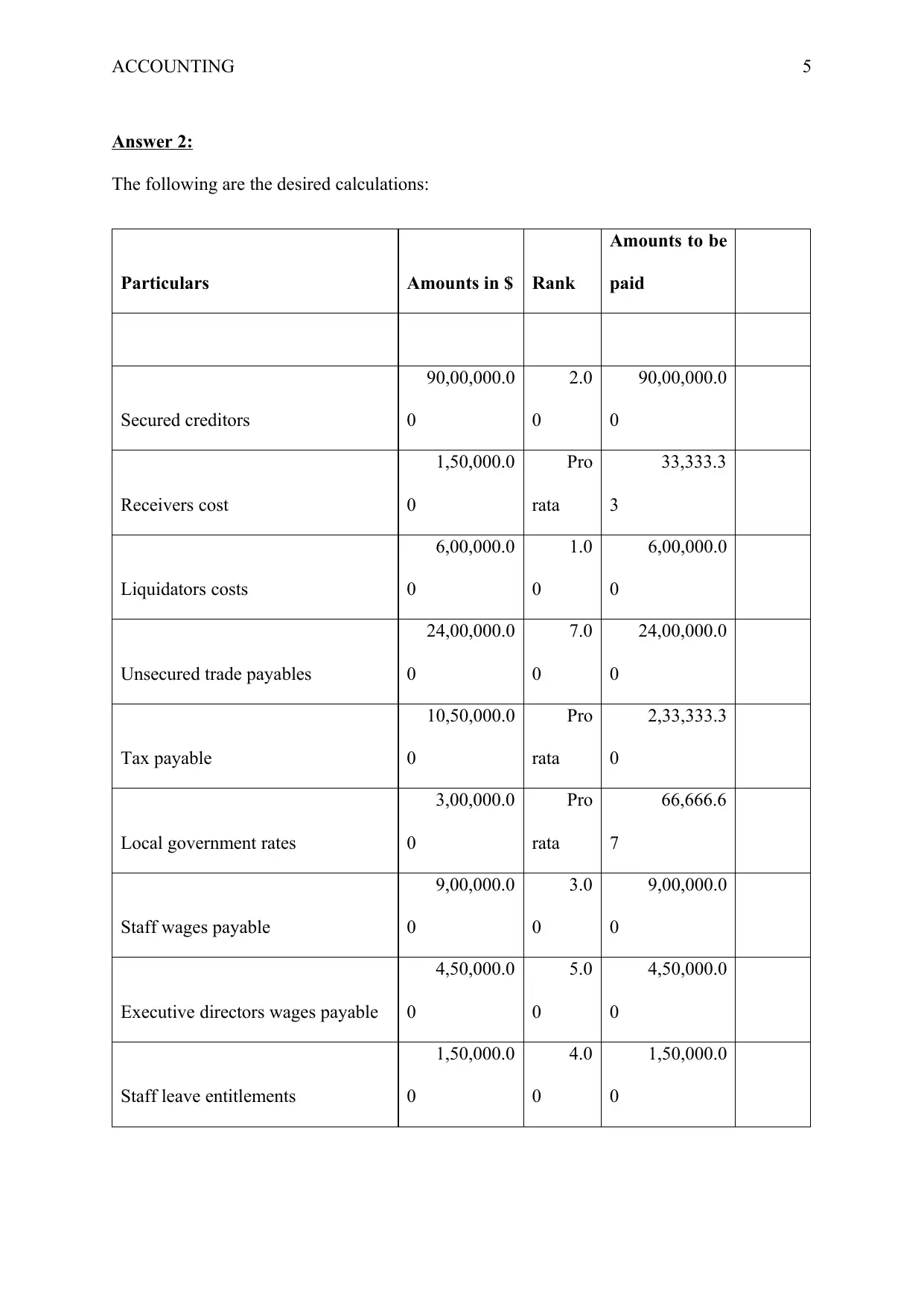

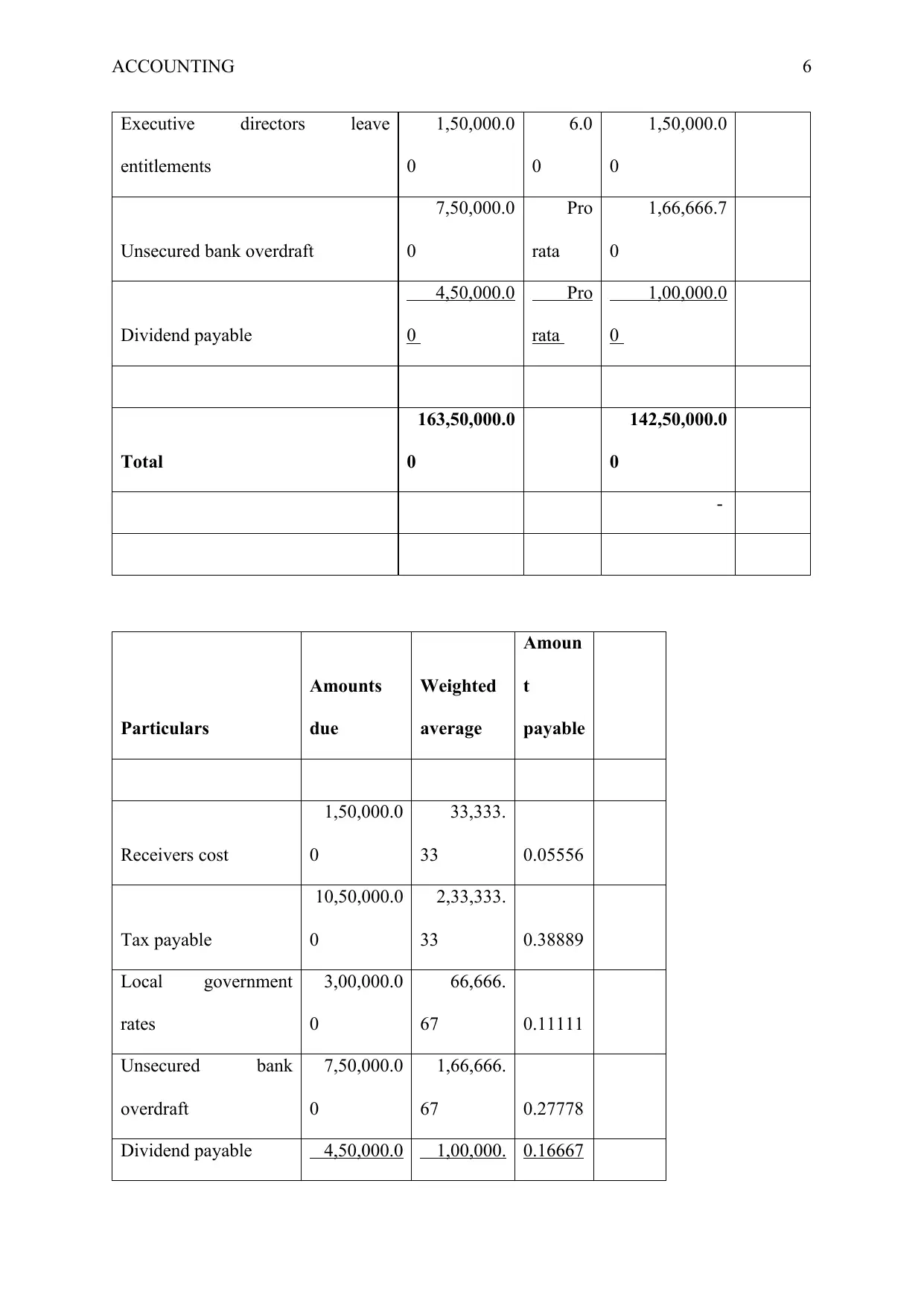

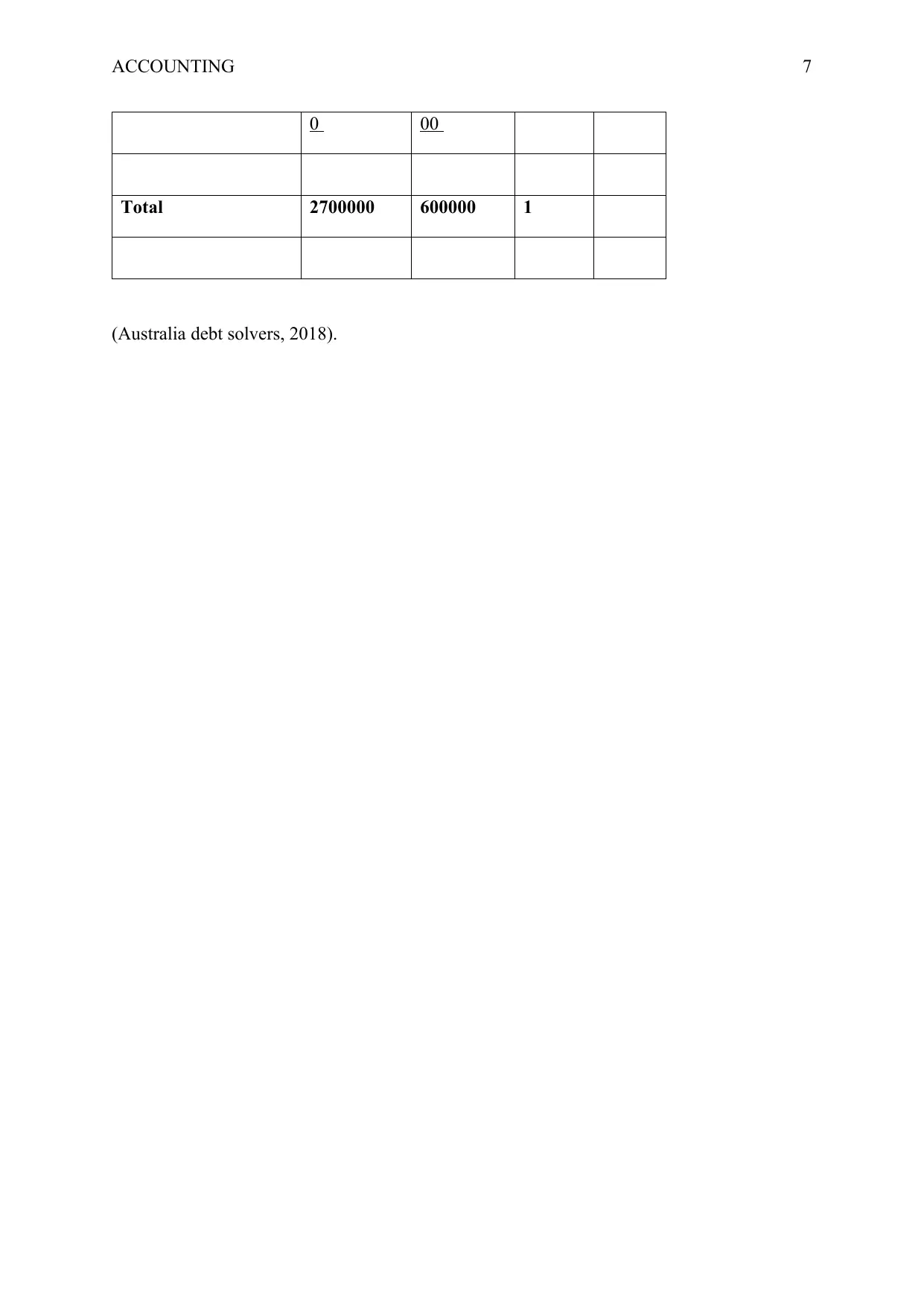

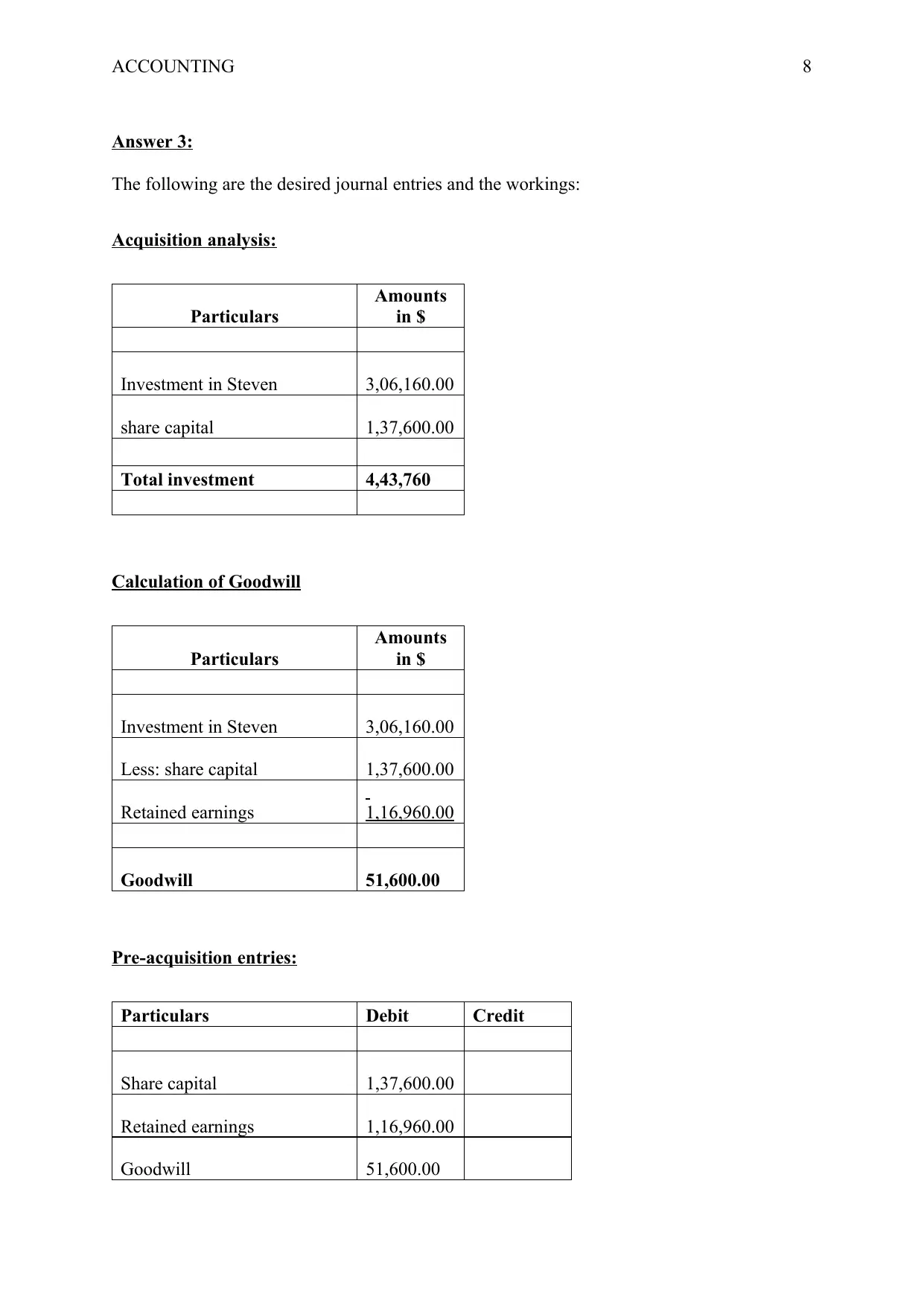

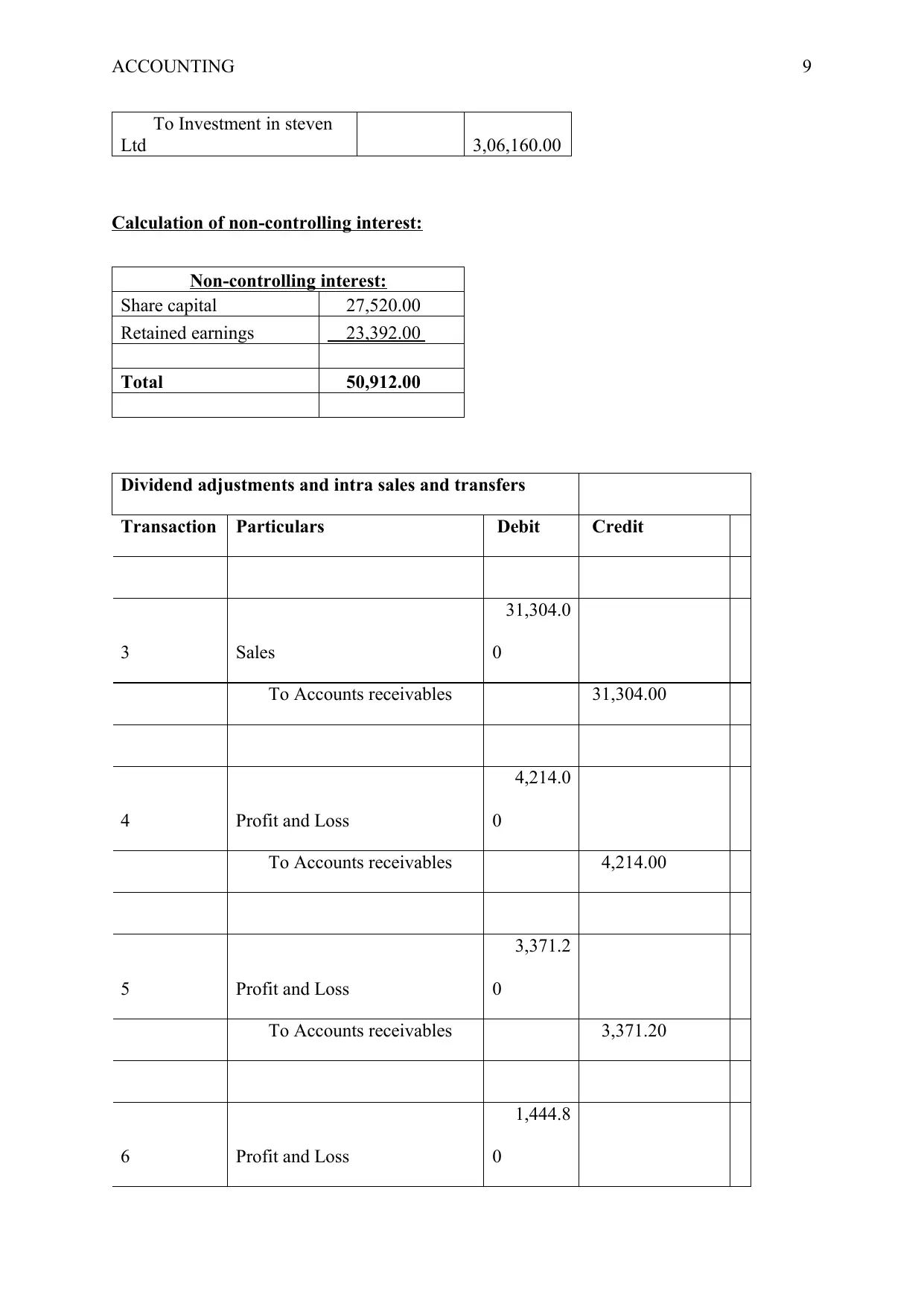

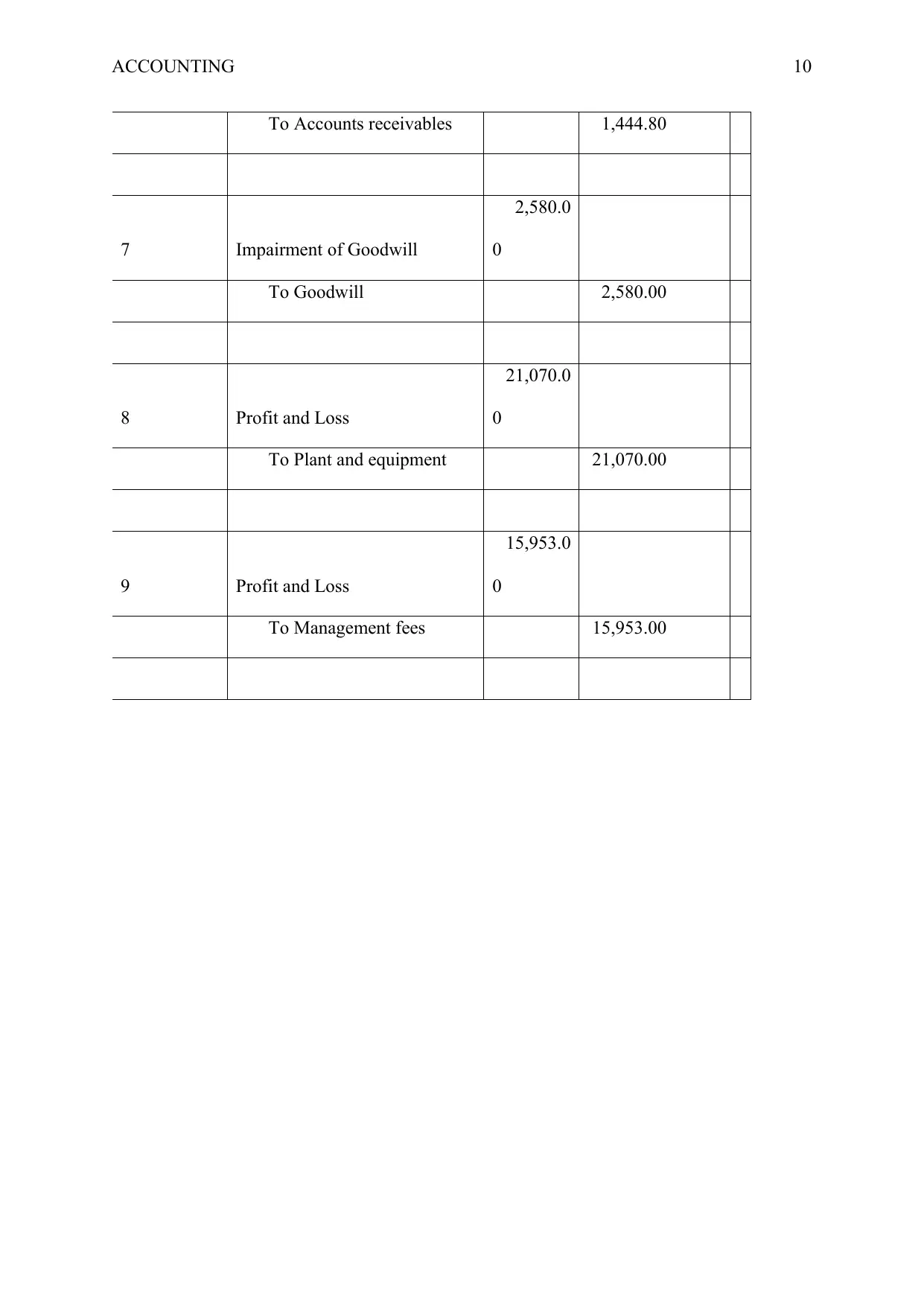

This assignment solution for a Corporate Accounting course (ACT305) covers several key areas, including the accounting treatment of investments, calculations related to liquidation, goodwill, and non-controlling interests. It addresses consolidation issues, including pre-acquisition entries and dividend adjustments. The solution provides detailed calculations and journal entries related to investment in Fry Ltd, secured creditors, staff entitlements, executive director wages, local government rates, and tax payable. It also offers guidance on determining control over investees based on AASB 10 standards, with specific examples related to subsidiary consolidation. The document provides valuable insights and calculations for students studying corporate accounting, and Desklib offers a platform to access more past papers and assignment solutions for similar courses.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.