Accounting Coursework: Tesco Plc and LMU Plc Financial Analysis Report

VerifiedAdded on 2020/10/05

|12

|1884

|318

Report

AI Summary

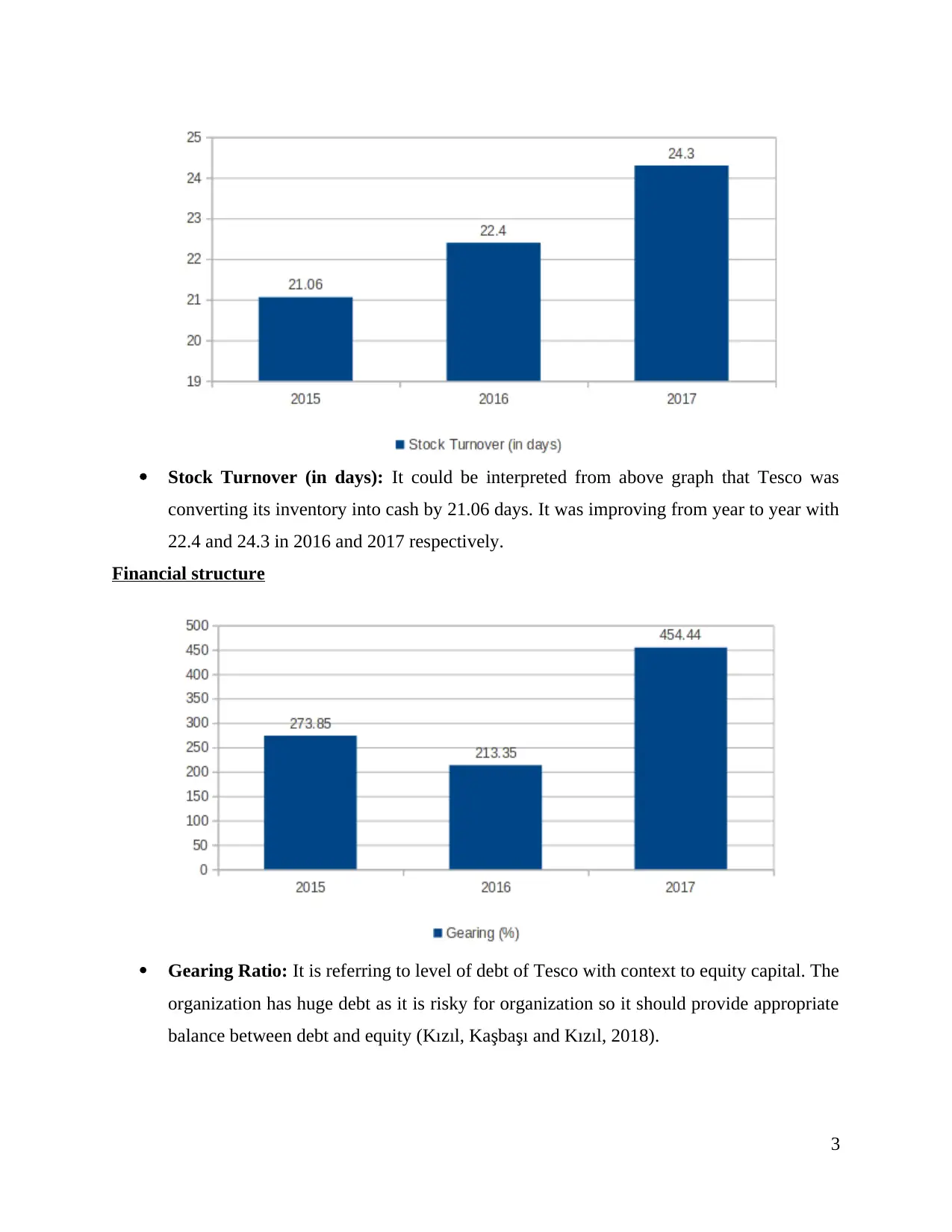

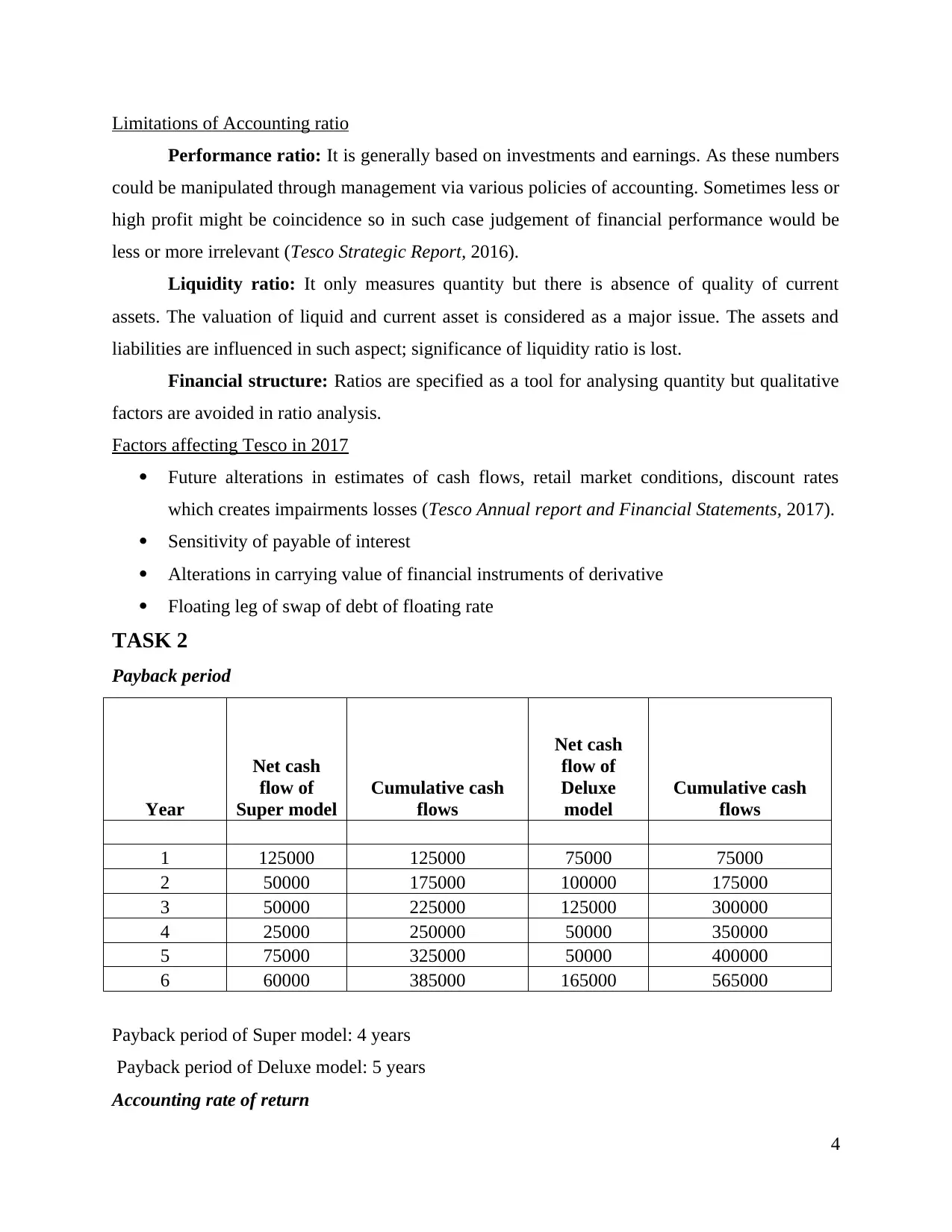

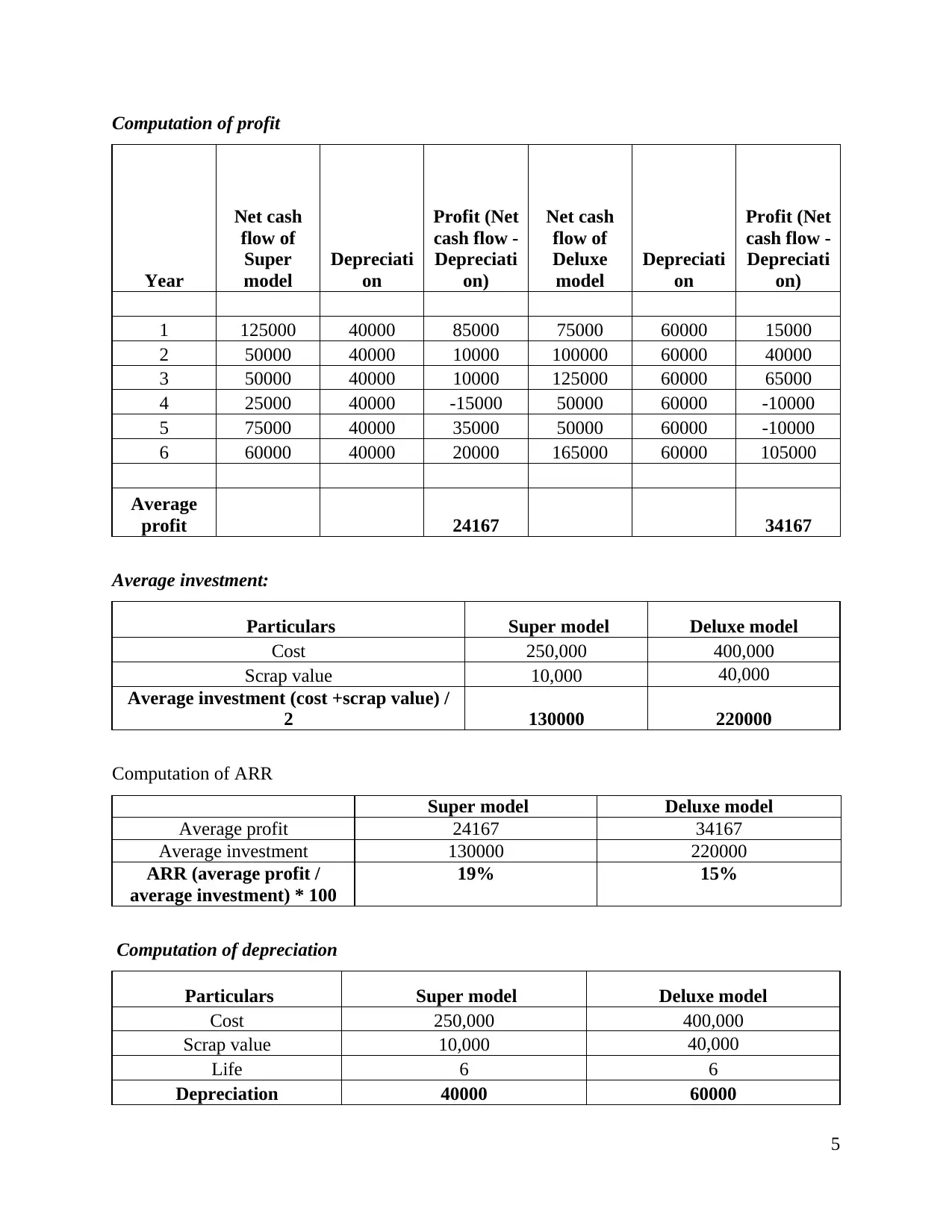

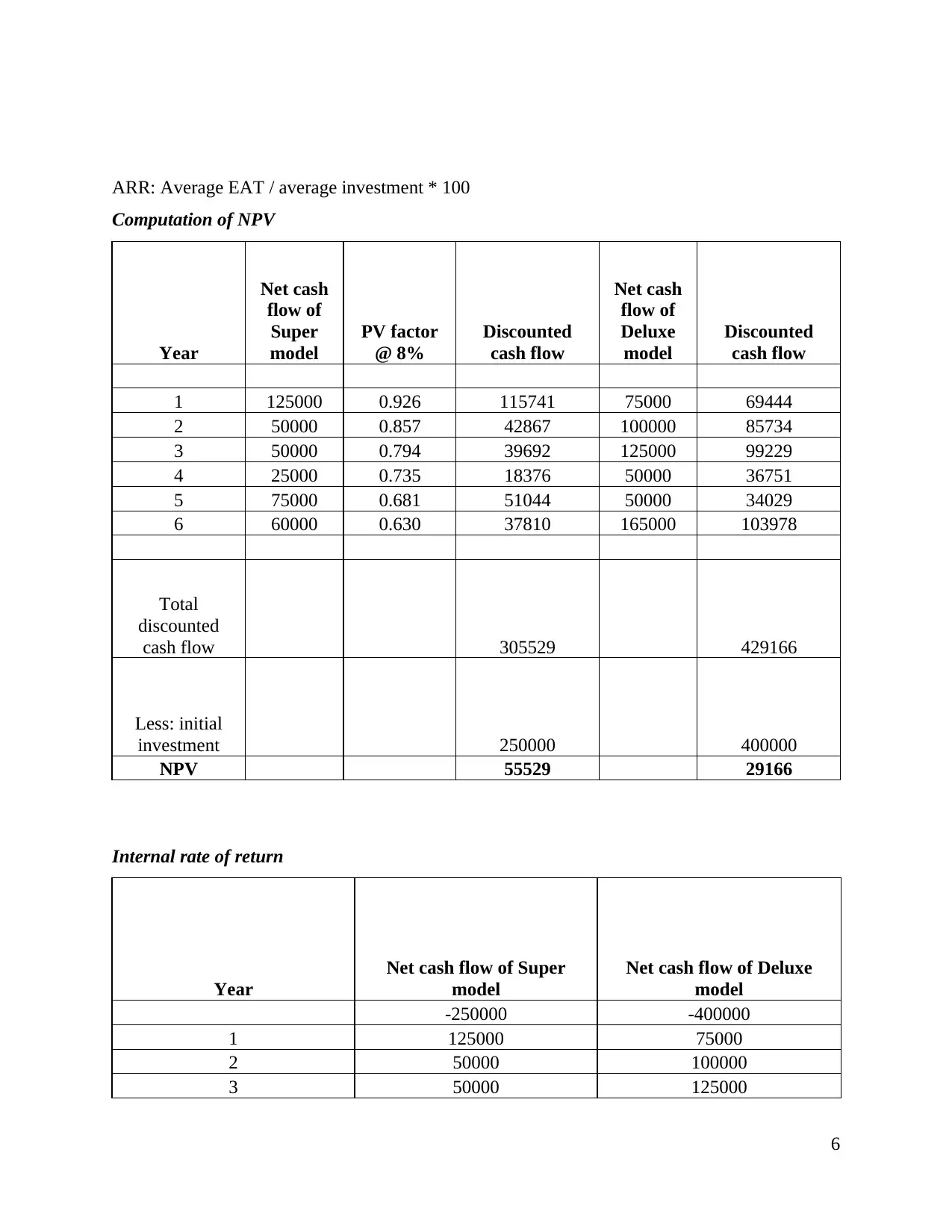

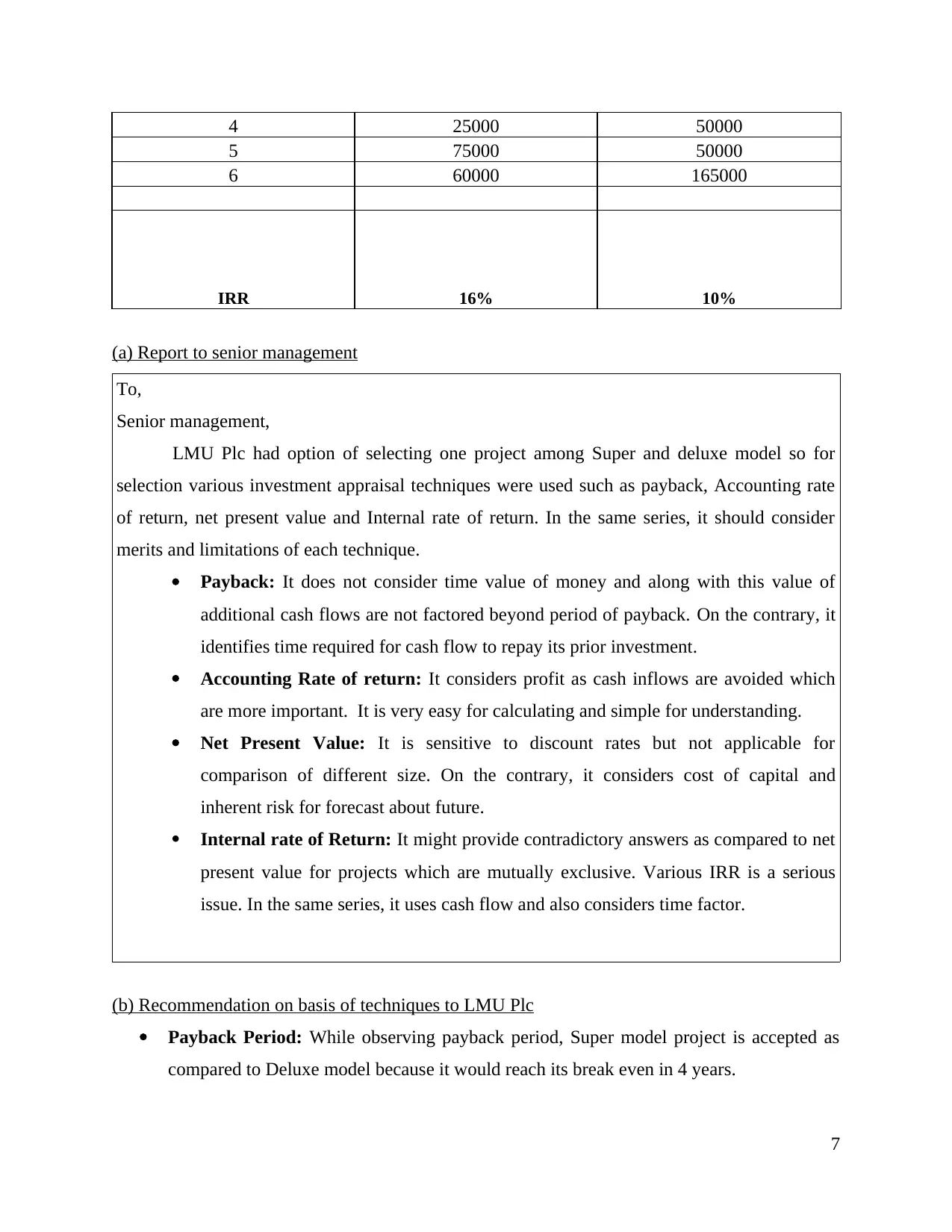

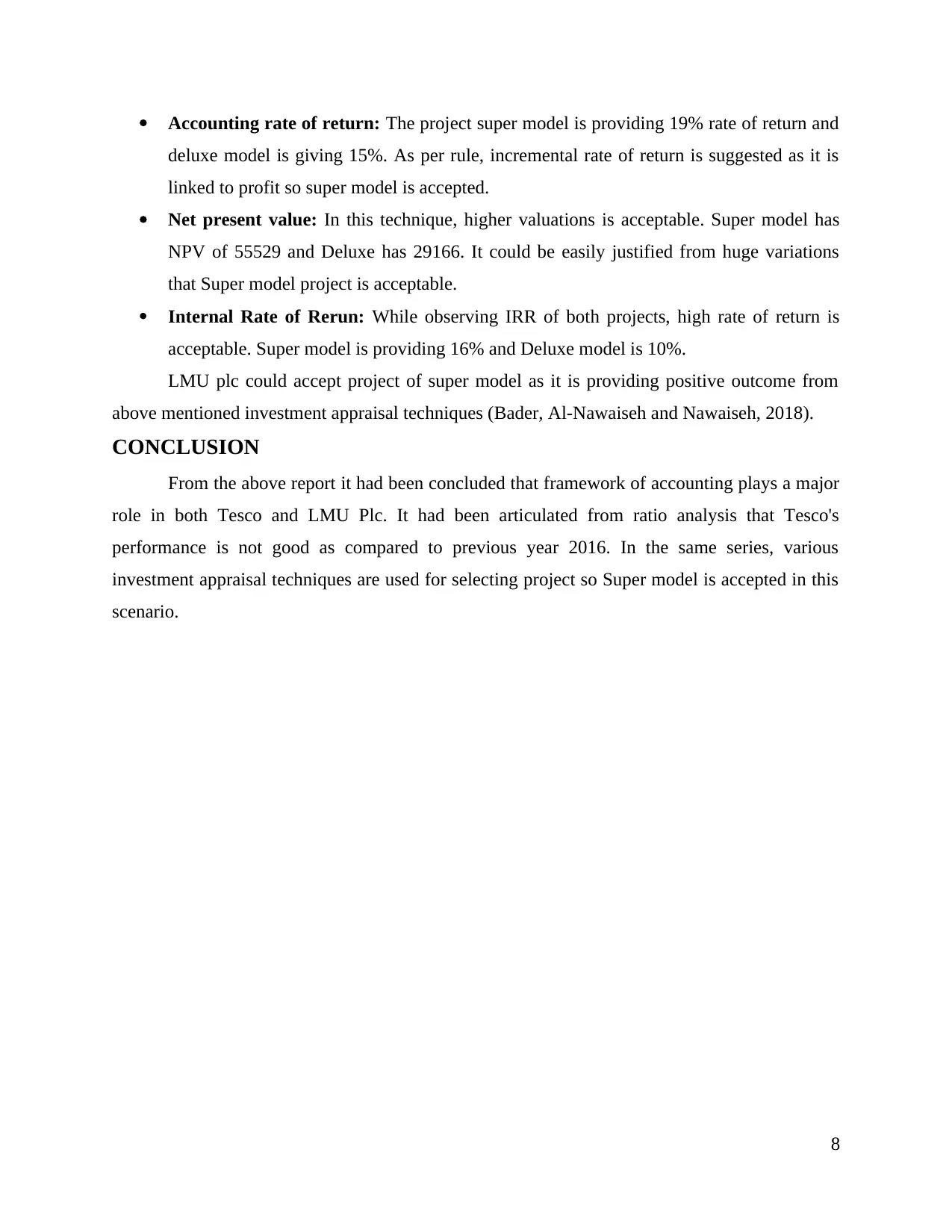

This report provides a comprehensive analysis of the financial performance of Tesco Plc and LMU Plc. The analysis begins with an examination of Tesco Plc's financial health using accounting ratios from 2015 to 2017, including gross profit margin, return on total assets, return on capital employed, current ratio, liquidity ratio, stock turnover, and gearing ratio. It also discusses the limitations of these ratios and factors affecting Tesco in 2017. The report then shifts its focus to LMU Plc, evaluating two investment models (Super and Deluxe) using investment appraisal techniques like payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). The report concludes with recommendations based on these techniques, suggesting the Super model is a more viable investment. The report includes tables and calculations for each technique and references relevant sources.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.