Accounting Homework: Income Statement, Balance Sheet, and Cash Flow

VerifiedAdded on 2022/11/25

|8

|1216

|301

Homework Assignment

AI Summary

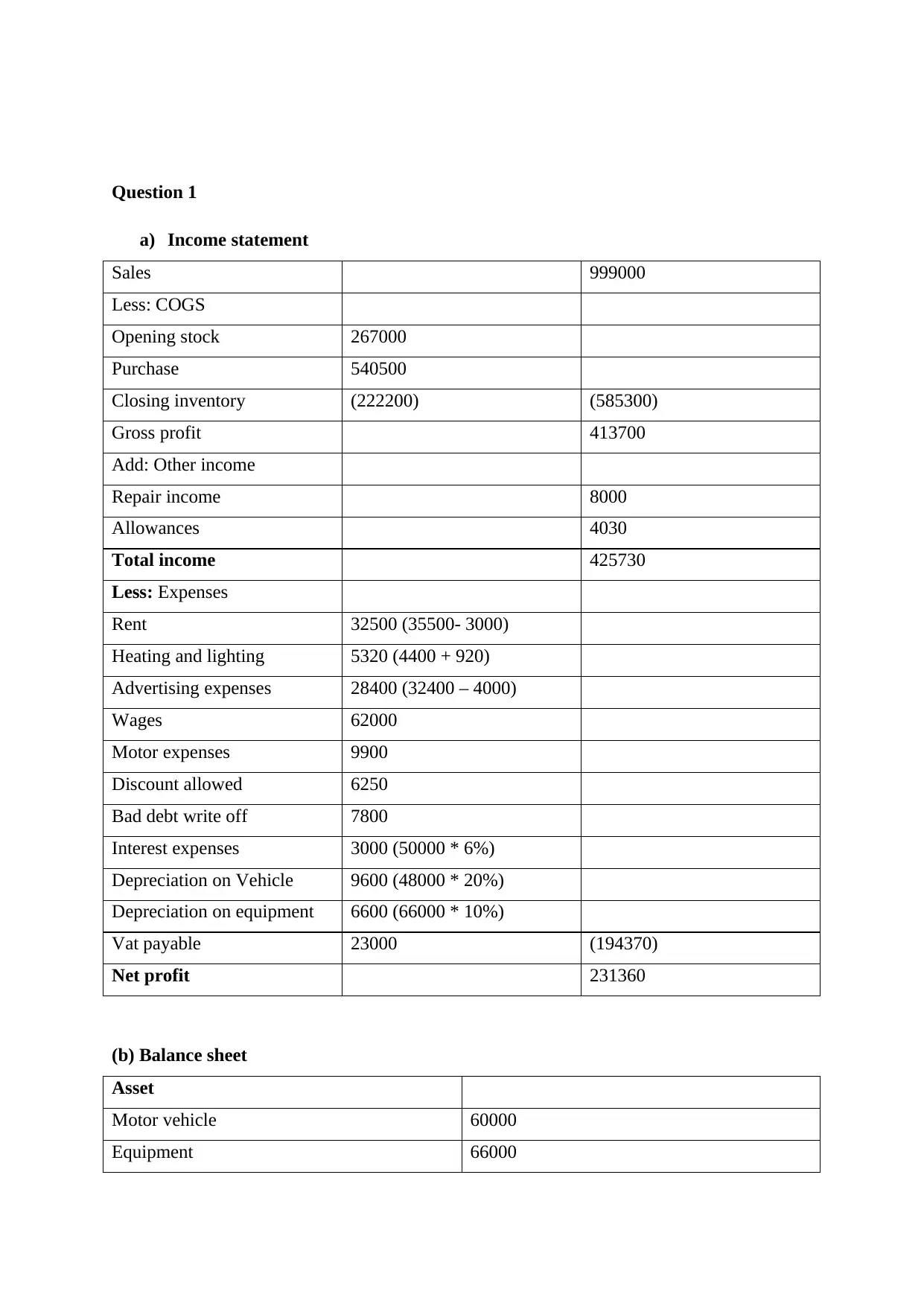

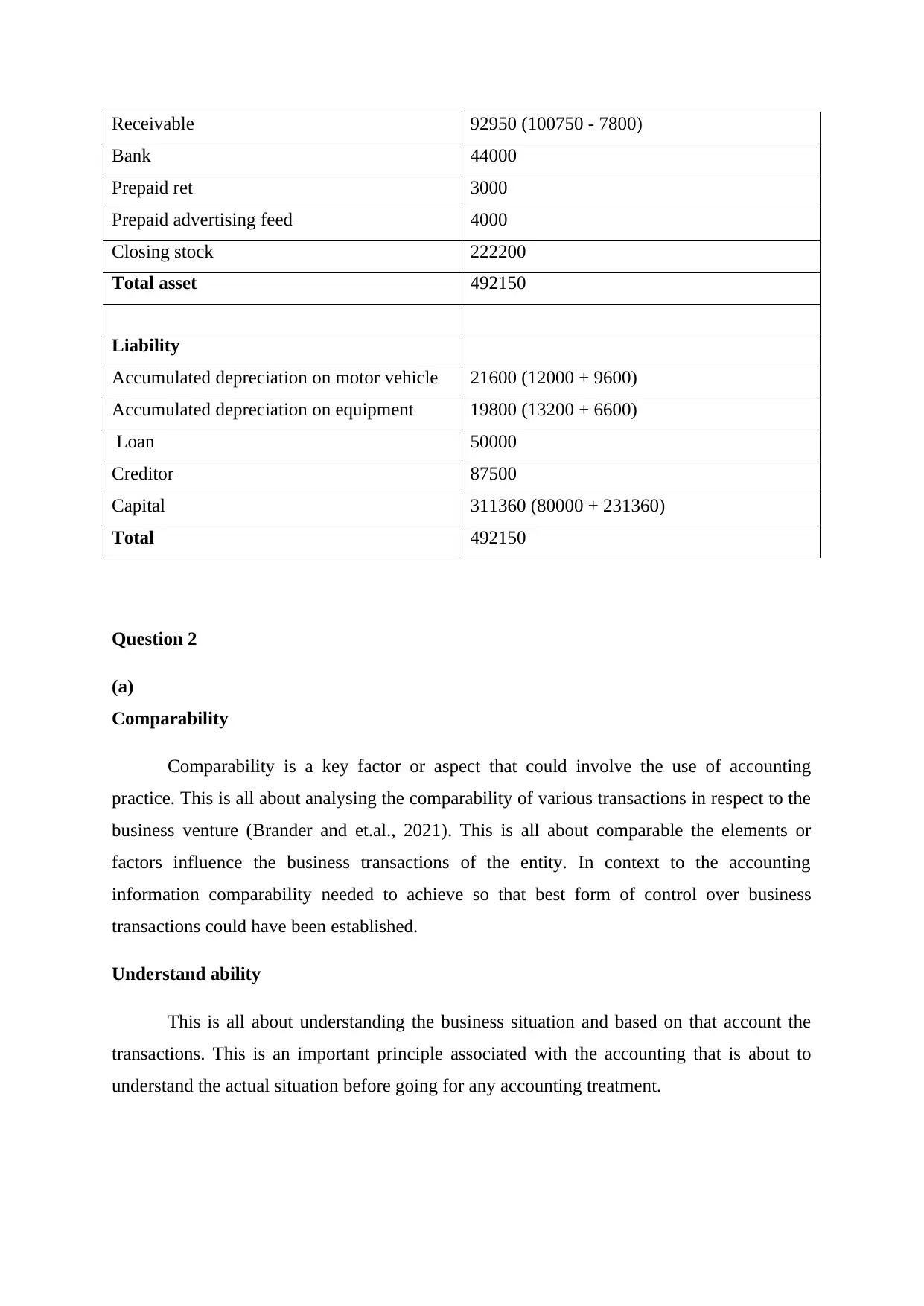

This accounting assignment solution covers various aspects of financial accounting. It begins with the preparation of an income statement and balance sheet, followed by an analysis of accounting concepts such as comparability and understandability. The solution delves into depreciation methods, including straight-line and written-down value methods, and explores the accounting equation's significance. The assignment also includes a cash flow statement, explanation of semi-variable costs, and responsibility accounting. Furthermore, it addresses cost analysis, including fixed and variable costs, opportunity costs, and material, labor, and overhead calculations. Finally, it analyzes sales, variable costs, and fixed costs to determine profit.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.