Superstore Ltd Financial Statement Analysis and Accounting Treatment

VerifiedAdded on 2023/06/08

|23

|2540

|398

Report

AI Summary

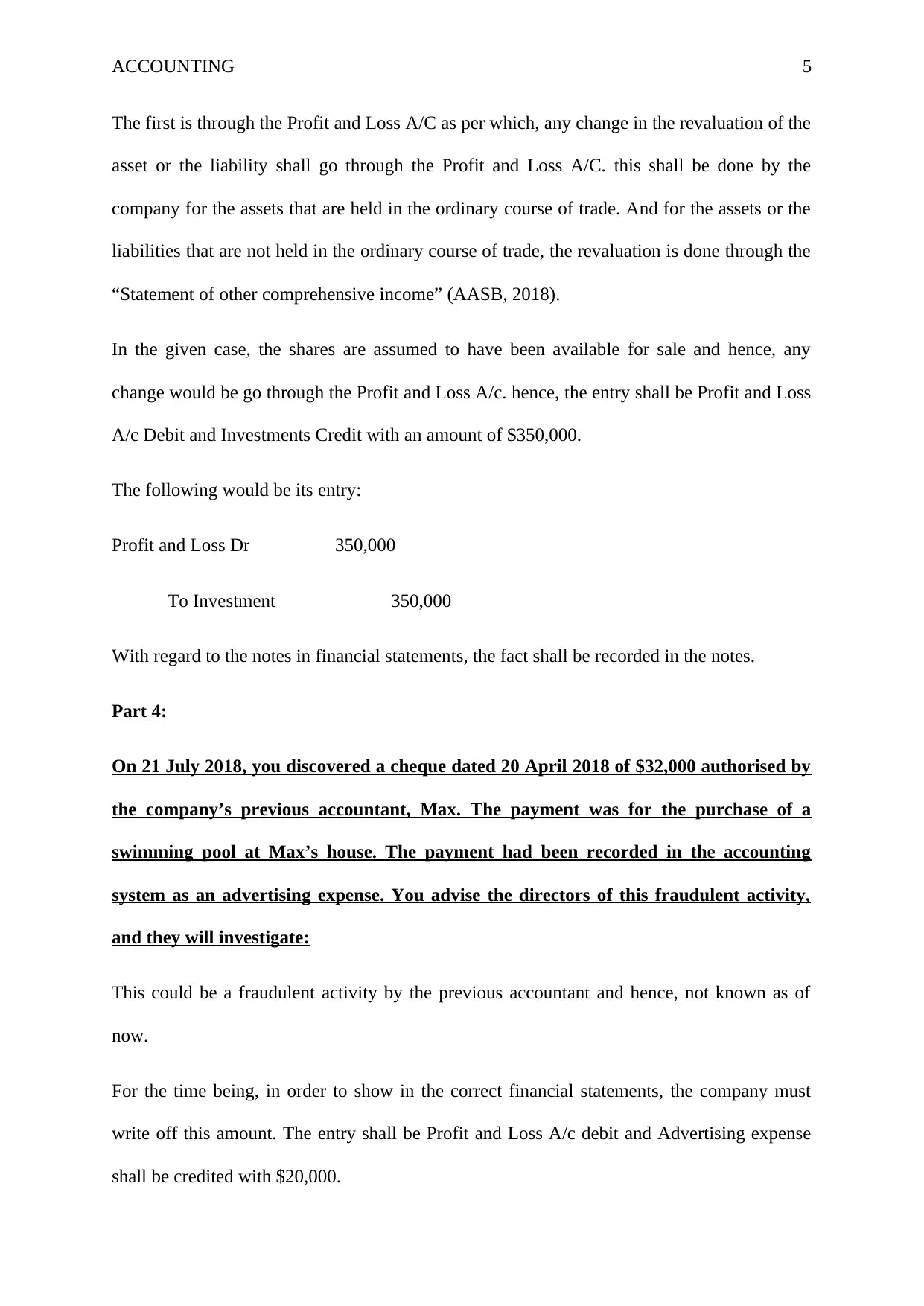

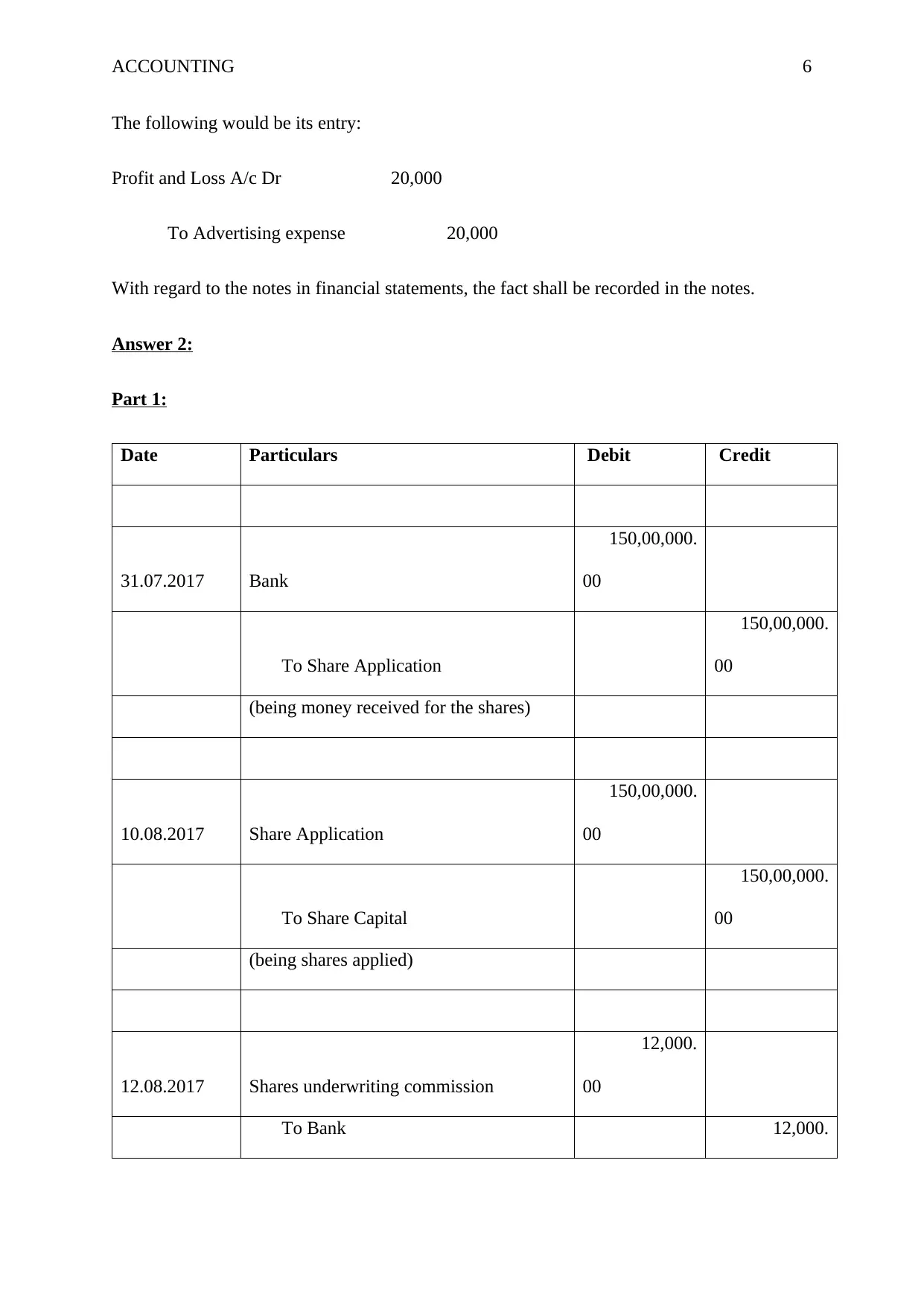

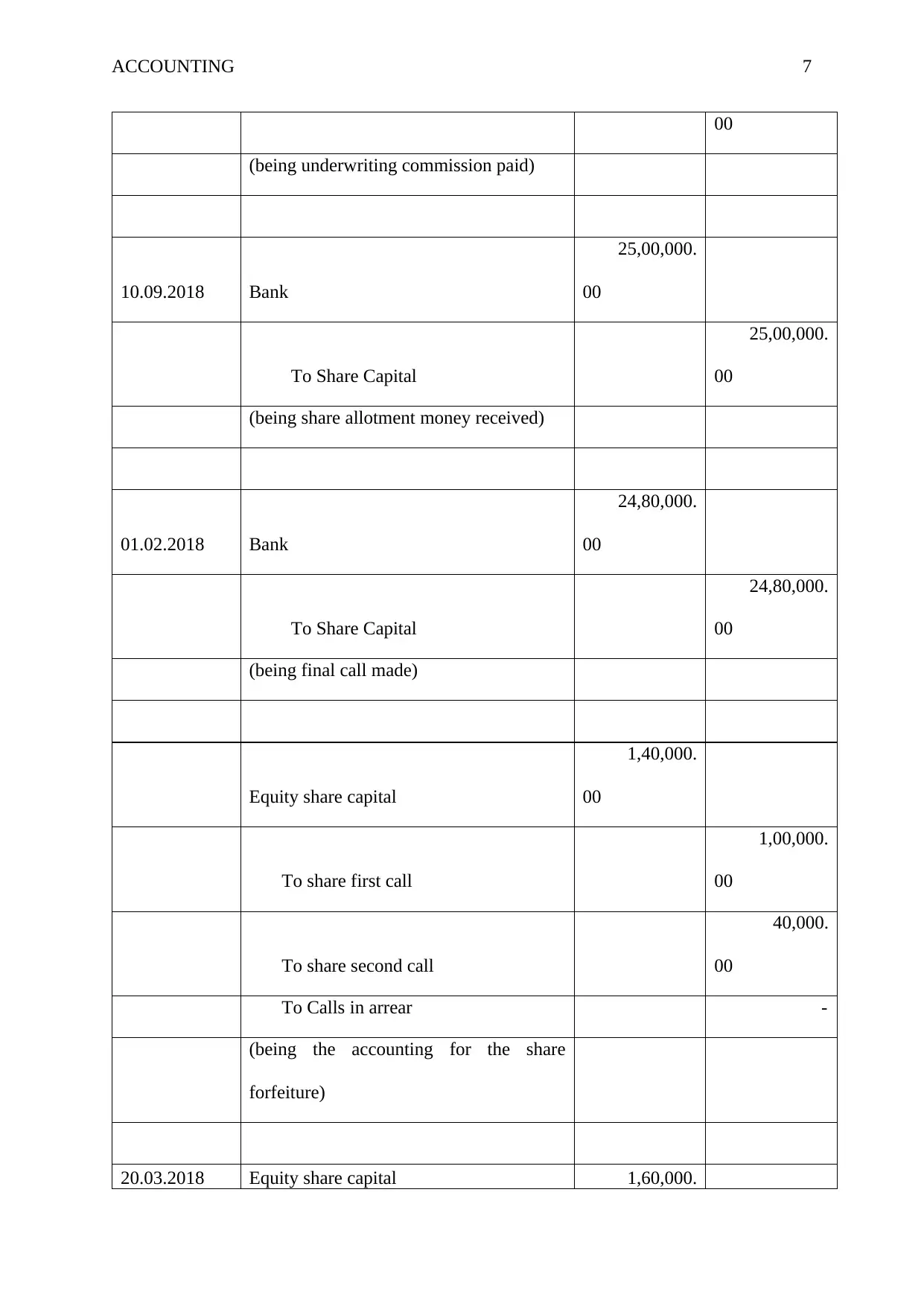

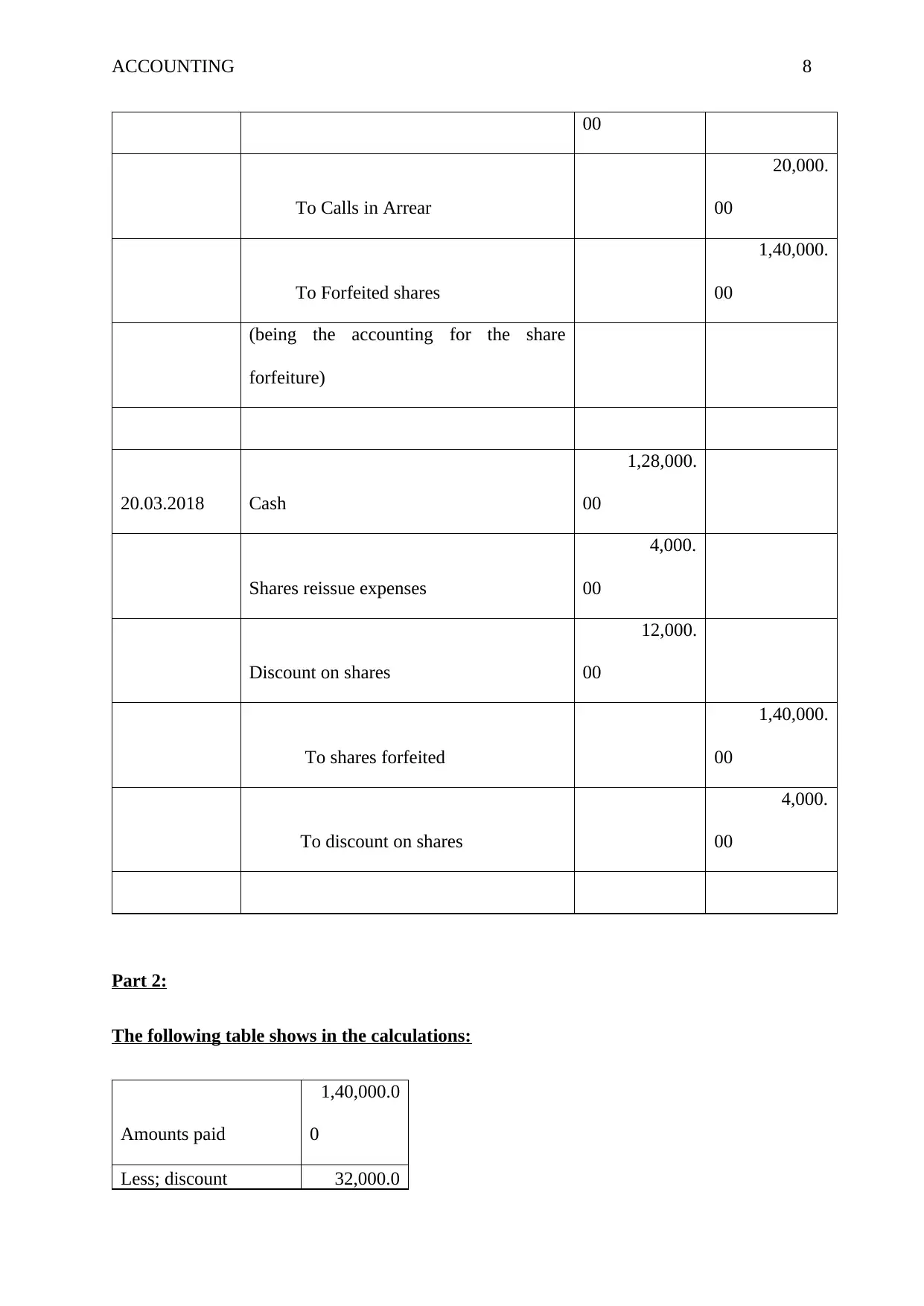

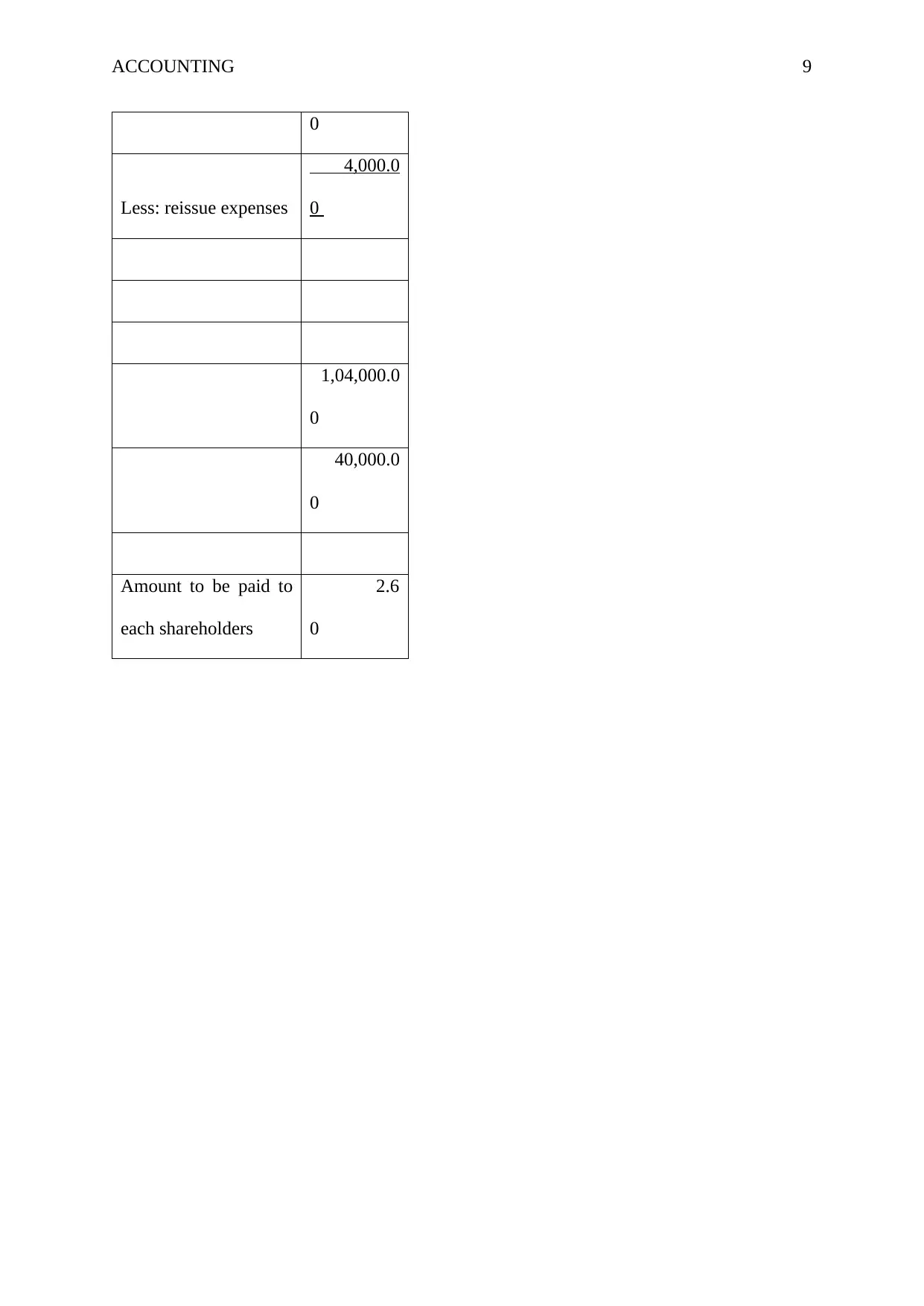

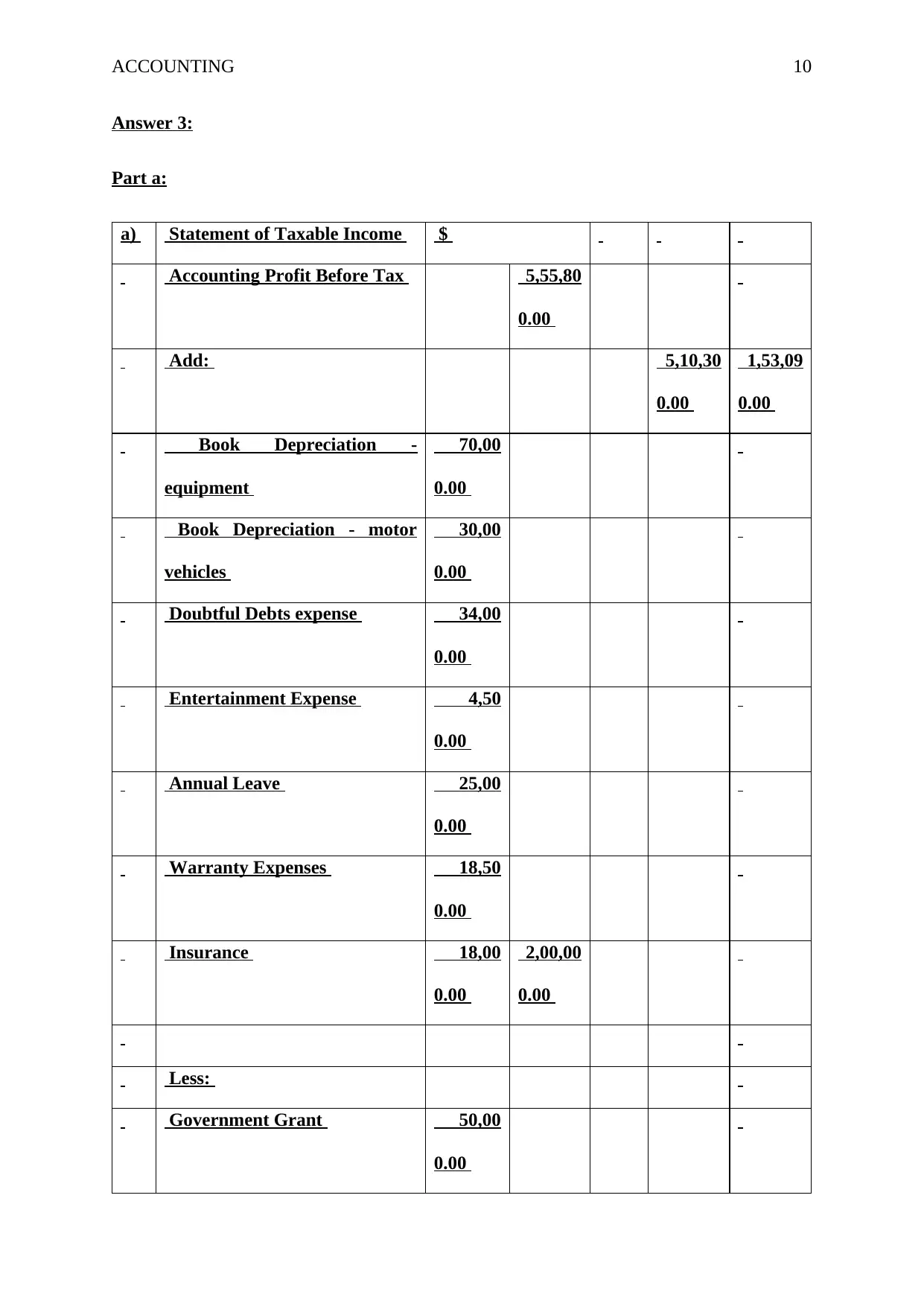

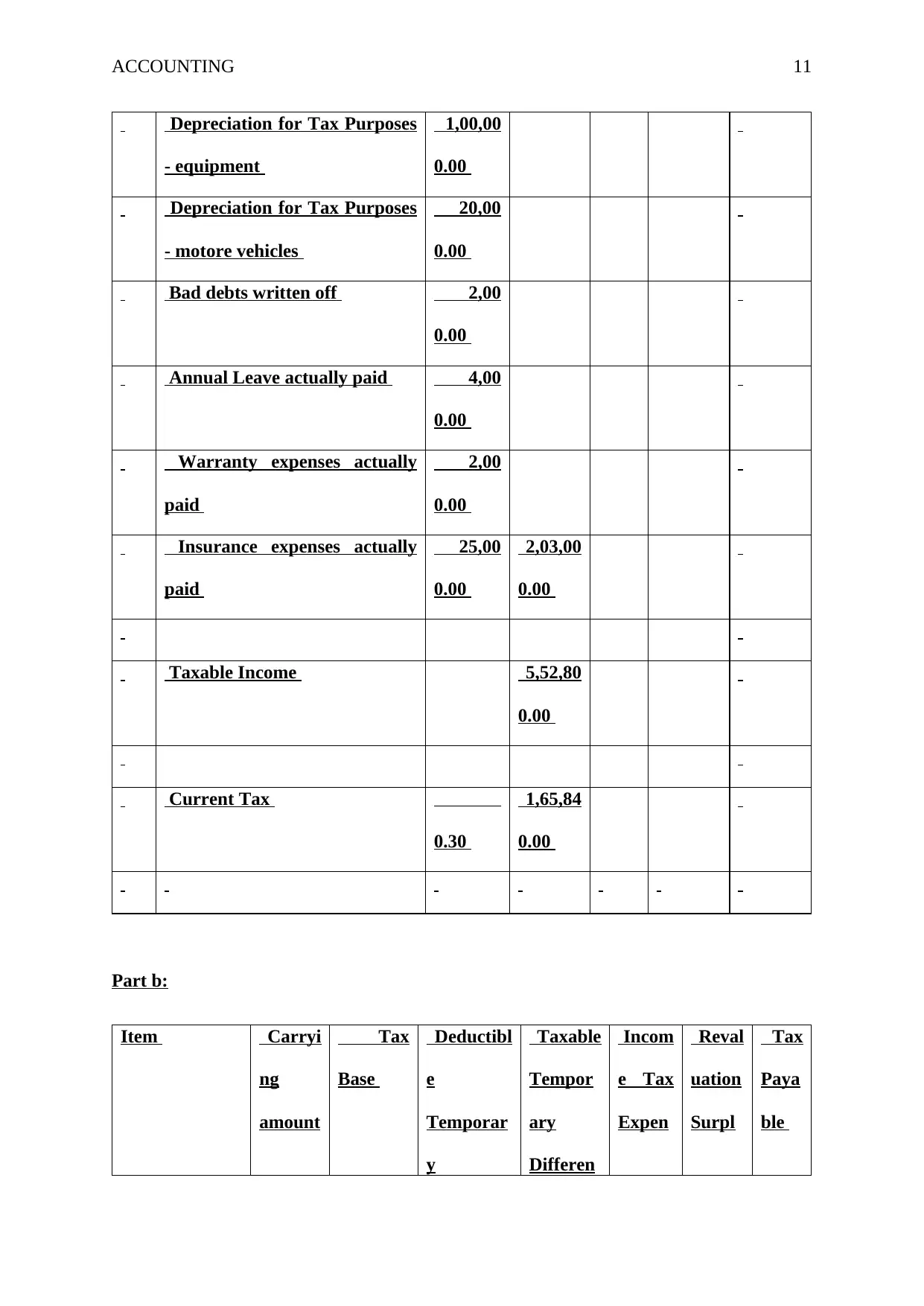

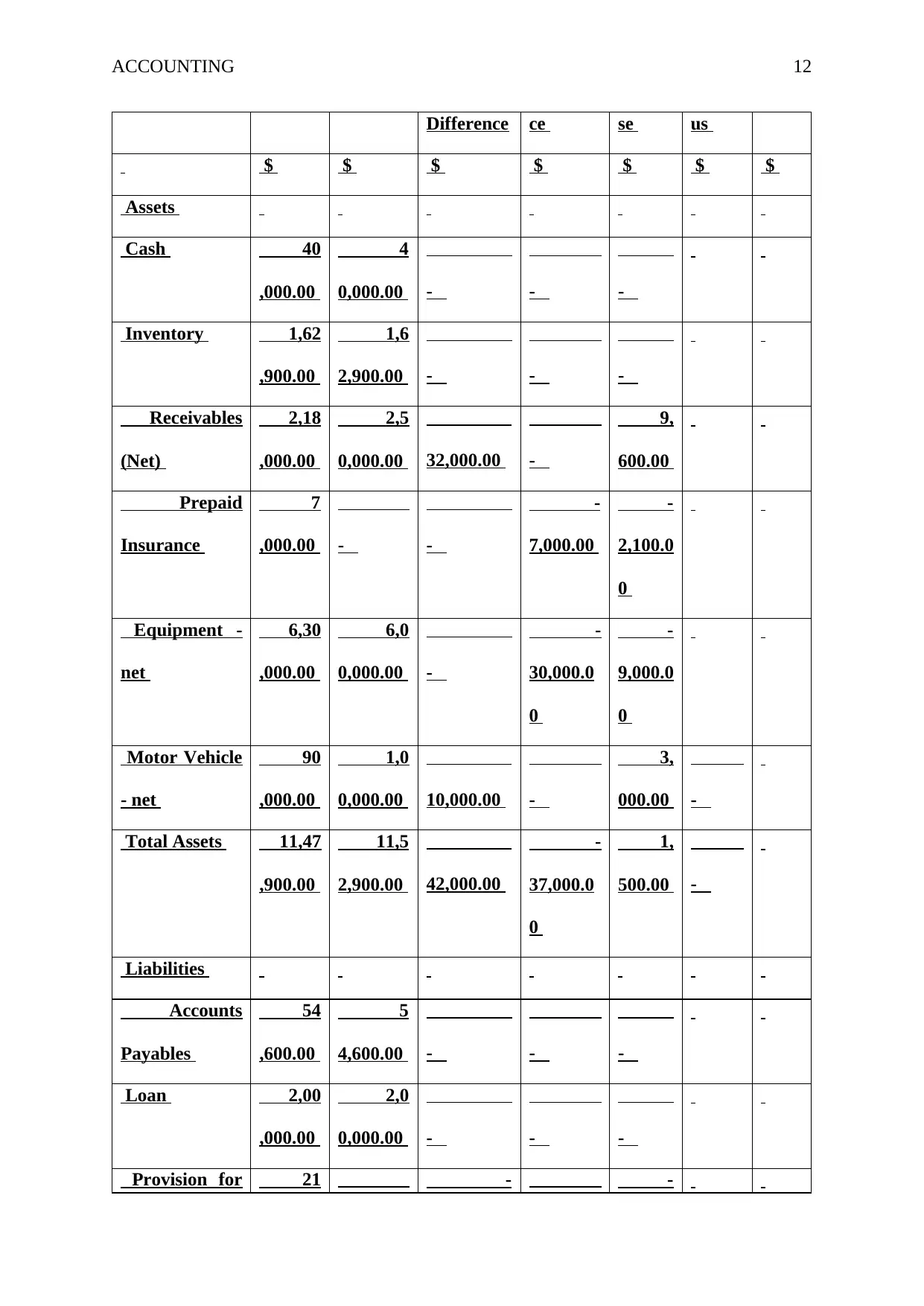

This assignment provides a detailed analysis of various accounting issues faced by Superstore Ltd, including changes in the useful life of manufacturing equipment, unrecorded repair invoices, fluctuations in the value of shares, and fraudulent activities. It explains the correct accounting treatments according to AASB standards, including necessary journal entries and disclosures in the financial statements. The report also covers share capital transactions, tax implications, and the calculation of taxable income, deferred tax assets, and liabilities. Additionally, it addresses the revaluation of equipment and impairment losses on various assets, providing a comprehensive overview of accounting principles and their practical application. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.