Analysis of Prepaid Insurance Adjustment in Accounting Essay

VerifiedAdded on 2020/12/18

|5

|741

|111

Essay

AI Summary

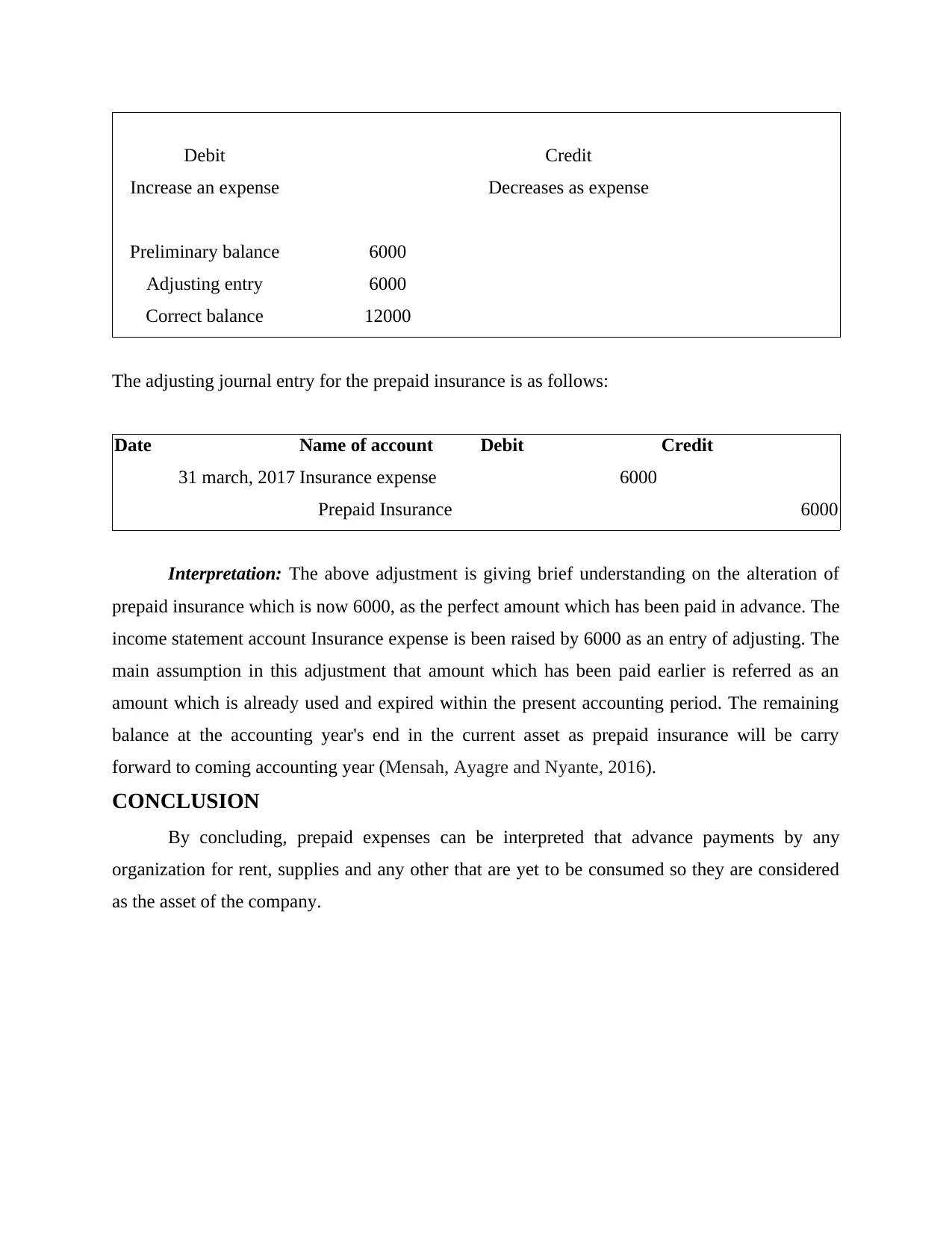

This essay delves into the accounting treatment of prepaid insurance, a current asset representing insurance premiums paid in advance. It explains the adjustment process, focusing on the balance sheet and income statement implications. The essay highlights how the prepaid insurance balance is reduced as the insurance period expires, and the corresponding increase in insurance expense. Using a scenario with a prepaid insurance balance of 6000, the essay details the adjusting journal entry, illustrating the debit to insurance expense and the credit to prepaid insurance. It emphasizes that prepaid expenses are payments made for future consumption and are adjusted at the end of the accounting period. The essay references relevant accounting literature and online resources to support its analysis, providing a comprehensive understanding of prepaid insurance adjustments. The conclusion summarizes the importance of recognizing prepaid expenses as assets until consumed and their subsequent impact on financial statements.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.