Detailed Analysis of JB Hi-Fi's Financial Performance and Statements

VerifiedAdded on 2023/01/13

|10

|2837

|76

Report

AI Summary

This report provides a comprehensive financial analysis of JB Hi-Fi Limited, examining its consolidated financial statements and key performance indicators. The analysis begins with an assessment of the total value of various accounts, including cash, inventories, sales revenue, and plant and equipment, along with their normal balances. It then evaluates the different types of revenues generated by the consolidated group, asset classifications, and the number of ordinary shares held. Further, the report determines the group's current liability for dividends, dividend payout ratio, and lists subsidiary companies. The analysis also includes calculations of sales revenue, profit, and their percentage changes, along with an examination of inventory levels, profit margins, and inventory turnover. The report concludes with a discussion of the financial performance of JB Hi-Fi, highlighting its revenue generation, expenditure control, and the importance of promotional activities for increased sales and profitability. Finally, the report provides key financial ratios to assess the financial health of the company.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Assessing total value in the consolidated financial statements...............................................3

2. Determining normal balances for the above listed accounts...................................................3

PART B............................................................................................................................................4

1. Evaluating various type of revenues generated by the consolidated group............................4

2. Assessing how group assets are classified..............................................................................5

3. Determining number of ordinary shares held by JB Hi-Fi Limited in financial year. ...........5

4. Determining group’s current liability for dividends to ordinary shareholders.......................5

5. Dividend payout ratio..............................................................................................................5

PART C............................................................................................................................................6

1. List the subsidiary companies in the JB Hi-Fi Group.............................................................6

2. Determining the value of the group’s sales revenue...............................................................6

3. Determining the group’s final profit.......................................................................................6

4. Evaluating the percentage change in (2) and (3).....................................................................6

5. Determining the total value of inventories on hand................................................................7

6. Calculating profit margins and inventory turnover.................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Assessing total value in the consolidated financial statements...............................................3

2. Determining normal balances for the above listed accounts...................................................3

PART B............................................................................................................................................4

1. Evaluating various type of revenues generated by the consolidated group............................4

2. Assessing how group assets are classified..............................................................................5

3. Determining number of ordinary shares held by JB Hi-Fi Limited in financial year. ...........5

4. Determining group’s current liability for dividends to ordinary shareholders.......................5

5. Dividend payout ratio..............................................................................................................5

PART C............................................................................................................................................6

1. List the subsidiary companies in the JB Hi-Fi Group.............................................................6

2. Determining the value of the group’s sales revenue...............................................................6

3. Determining the group’s final profit.......................................................................................6

4. Evaluating the percentage change in (2) and (3).....................................................................6

5. Determining the total value of inventories on hand................................................................7

6. Calculating profit margins and inventory turnover.................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting is referred to as one of the appropriate process which is useful in

summarizing and interpreting various financial transactions of the company over a specific

period (Birt and et.al., 2019). Accounting helps in summarizing the operations of the company

by understanding its financial position. This study will demonstrate types of revenues which has

been generated within consolidated group. Furthermore, it also demonstrates various range of

questions associated with the JB Hi-Fi Limited.

JB Hi-Fi Limited is considered to be one of the publicly listed Australian retail company

which was founded in the year 1974 by John Barbuto. This company tends to sell various

consumer goods. JB Hi-Fi Limited is listed on the Australian Stock exchange and is also

headquartered in South bank, Melbourne, Australia.

PART A

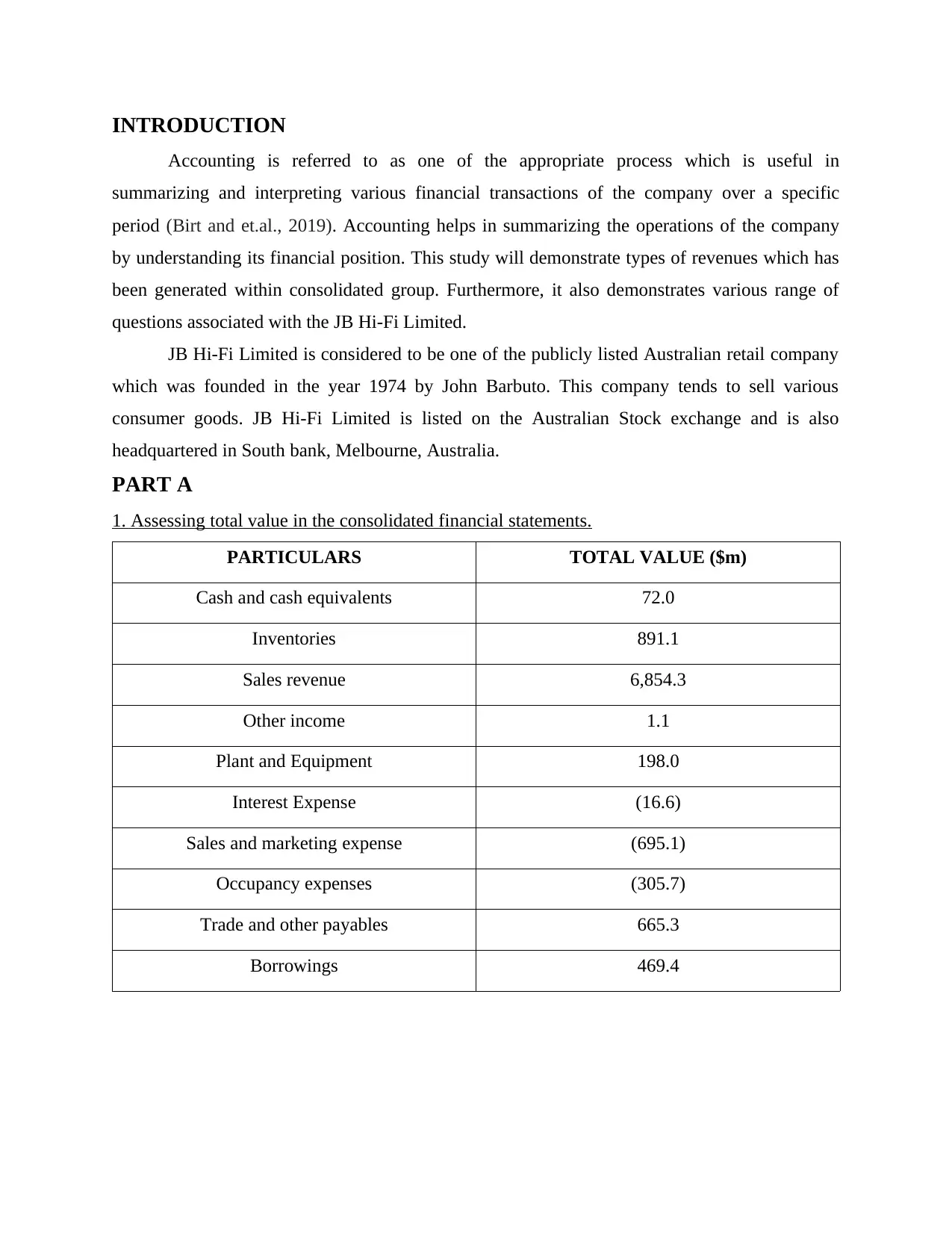

1. Assessing total value in the consolidated financial statements.

PARTICULARS TOTAL VALUE ($m)

Cash and cash equivalents 72.0

Inventories 891.1

Sales revenue 6,854.3

Other income 1.1

Plant and Equipment 198.0

Interest Expense (16.6)

Sales and marketing expense (695.1)

Occupancy expenses (305.7)

Trade and other payables 665.3

Borrowings 469.4

Accounting is referred to as one of the appropriate process which is useful in

summarizing and interpreting various financial transactions of the company over a specific

period (Birt and et.al., 2019). Accounting helps in summarizing the operations of the company

by understanding its financial position. This study will demonstrate types of revenues which has

been generated within consolidated group. Furthermore, it also demonstrates various range of

questions associated with the JB Hi-Fi Limited.

JB Hi-Fi Limited is considered to be one of the publicly listed Australian retail company

which was founded in the year 1974 by John Barbuto. This company tends to sell various

consumer goods. JB Hi-Fi Limited is listed on the Australian Stock exchange and is also

headquartered in South bank, Melbourne, Australia.

PART A

1. Assessing total value in the consolidated financial statements.

PARTICULARS TOTAL VALUE ($m)

Cash and cash equivalents 72.0

Inventories 891.1

Sales revenue 6,854.3

Other income 1.1

Plant and Equipment 198.0

Interest Expense (16.6)

Sales and marketing expense (695.1)

Occupancy expenses (305.7)

Trade and other payables 665.3

Borrowings 469.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

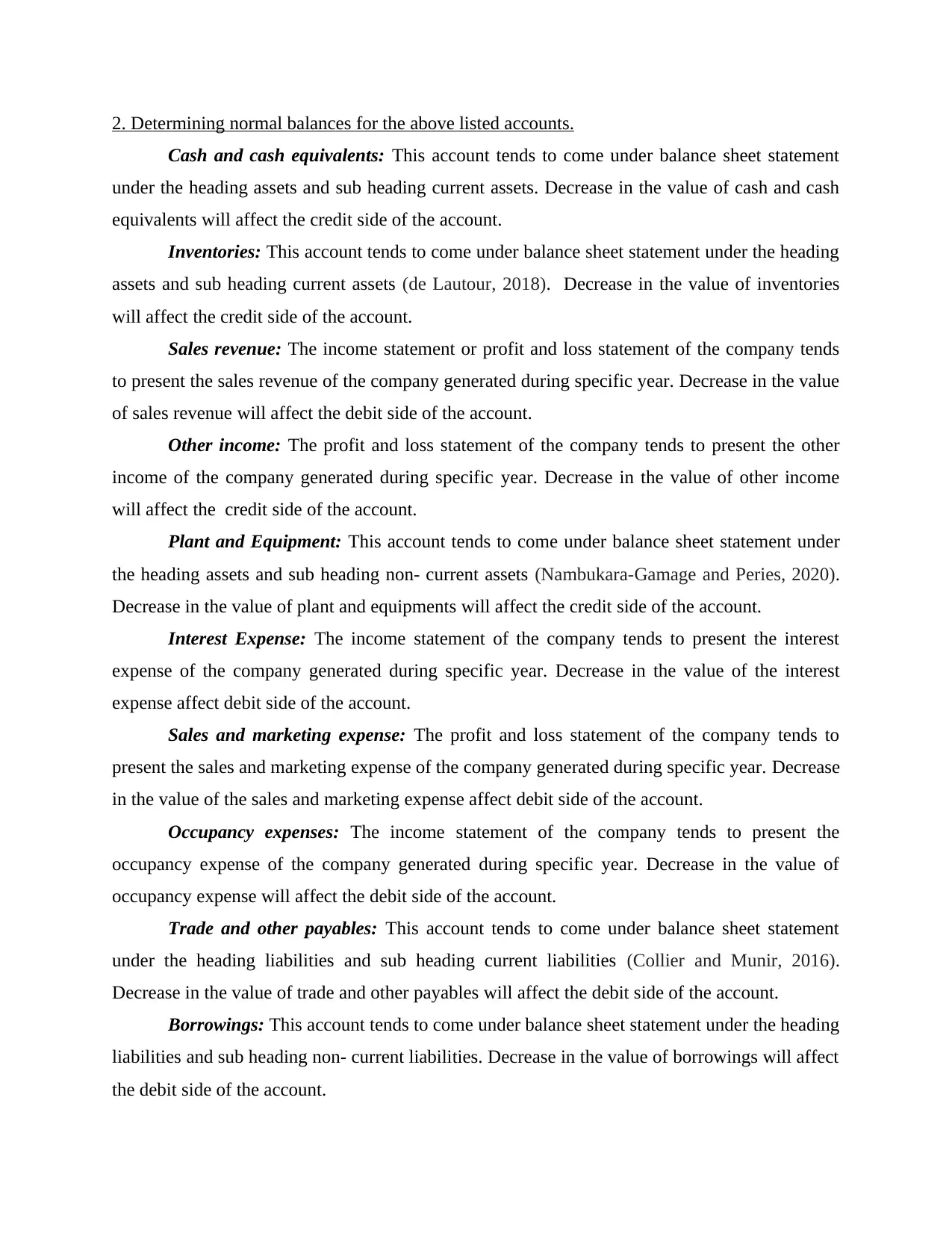

2. Determining normal balances for the above listed accounts.

Cash and cash equivalents: This account tends to come under balance sheet statement

under the heading assets and sub heading current assets. Decrease in the value of cash and cash

equivalents will affect the credit side of the account.

Inventories: This account tends to come under balance sheet statement under the heading

assets and sub heading current assets (de Lautour, 2018). Decrease in the value of inventories

will affect the credit side of the account.

Sales revenue: The income statement or profit and loss statement of the company tends

to present the sales revenue of the company generated during specific year. Decrease in the value

of sales revenue will affect the debit side of the account.

Other income: The profit and loss statement of the company tends to present the other

income of the company generated during specific year. Decrease in the value of other income

will affect the credit side of the account.

Plant and Equipment: This account tends to come under balance sheet statement under

the heading assets and sub heading non- current assets (Nambukara-Gamage and Peries, 2020).

Decrease in the value of plant and equipments will affect the credit side of the account.

Interest Expense: The income statement of the company tends to present the interest

expense of the company generated during specific year. Decrease in the value of the interest

expense affect debit side of the account.

Sales and marketing expense: The profit and loss statement of the company tends to

present the sales and marketing expense of the company generated during specific year. Decrease

in the value of the sales and marketing expense affect debit side of the account.

Occupancy expenses: The income statement of the company tends to present the

occupancy expense of the company generated during specific year. Decrease in the value of

occupancy expense will affect the debit side of the account.

Trade and other payables: This account tends to come under balance sheet statement

under the heading liabilities and sub heading current liabilities (Collier and Munir, 2016).

Decrease in the value of trade and other payables will affect the debit side of the account.

Borrowings: This account tends to come under balance sheet statement under the heading

liabilities and sub heading non- current liabilities. Decrease in the value of borrowings will affect

the debit side of the account.

Cash and cash equivalents: This account tends to come under balance sheet statement

under the heading assets and sub heading current assets. Decrease in the value of cash and cash

equivalents will affect the credit side of the account.

Inventories: This account tends to come under balance sheet statement under the heading

assets and sub heading current assets (de Lautour, 2018). Decrease in the value of inventories

will affect the credit side of the account.

Sales revenue: The income statement or profit and loss statement of the company tends

to present the sales revenue of the company generated during specific year. Decrease in the value

of sales revenue will affect the debit side of the account.

Other income: The profit and loss statement of the company tends to present the other

income of the company generated during specific year. Decrease in the value of other income

will affect the credit side of the account.

Plant and Equipment: This account tends to come under balance sheet statement under

the heading assets and sub heading non- current assets (Nambukara-Gamage and Peries, 2020).

Decrease in the value of plant and equipments will affect the credit side of the account.

Interest Expense: The income statement of the company tends to present the interest

expense of the company generated during specific year. Decrease in the value of the interest

expense affect debit side of the account.

Sales and marketing expense: The profit and loss statement of the company tends to

present the sales and marketing expense of the company generated during specific year. Decrease

in the value of the sales and marketing expense affect debit side of the account.

Occupancy expenses: The income statement of the company tends to present the

occupancy expense of the company generated during specific year. Decrease in the value of

occupancy expense will affect the debit side of the account.

Trade and other payables: This account tends to come under balance sheet statement

under the heading liabilities and sub heading current liabilities (Collier and Munir, 2016).

Decrease in the value of trade and other payables will affect the debit side of the account.

Borrowings: This account tends to come under balance sheet statement under the heading

liabilities and sub heading non- current liabilities. Decrease in the value of borrowings will affect

the debit side of the account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

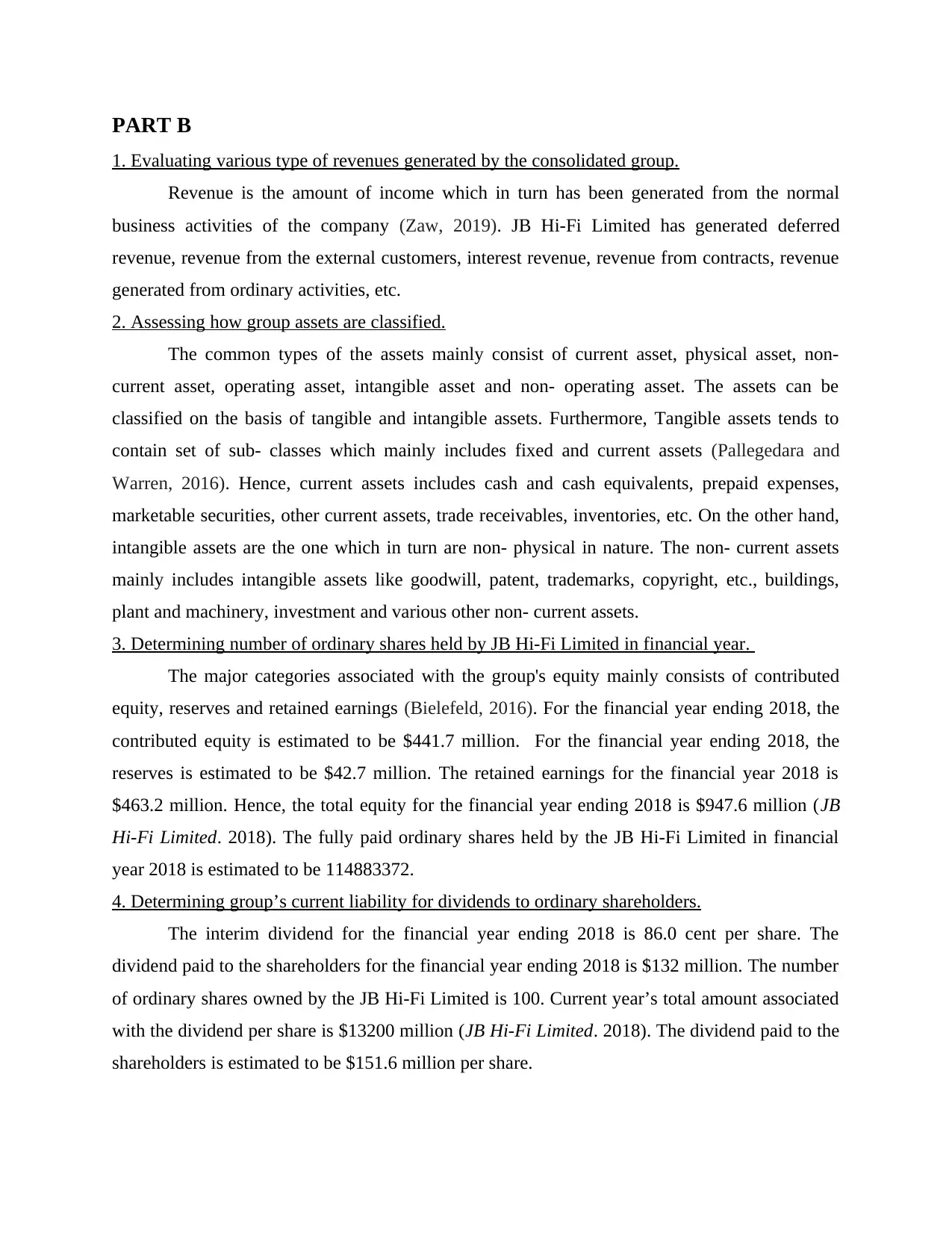

1. Evaluating various type of revenues generated by the consolidated group.

Revenue is the amount of income which in turn has been generated from the normal

business activities of the company (Zaw, 2019). JB Hi-Fi Limited has generated deferred

revenue, revenue from the external customers, interest revenue, revenue from contracts, revenue

generated from ordinary activities, etc.

2. Assessing how group assets are classified.

The common types of the assets mainly consist of current asset, physical asset, non-

current asset, operating asset, intangible asset and non- operating asset. The assets can be

classified on the basis of tangible and intangible assets. Furthermore, Tangible assets tends to

contain set of sub- classes which mainly includes fixed and current assets (Pallegedara and

Warren, 2016). Hence, current assets includes cash and cash equivalents, prepaid expenses,

marketable securities, other current assets, trade receivables, inventories, etc. On the other hand,

intangible assets are the one which in turn are non- physical in nature. The non- current assets

mainly includes intangible assets like goodwill, patent, trademarks, copyright, etc., buildings,

plant and machinery, investment and various other non- current assets.

3. Determining number of ordinary shares held by JB Hi-Fi Limited in financial year.

The major categories associated with the group's equity mainly consists of contributed

equity, reserves and retained earnings (Bielefeld, 2016). For the financial year ending 2018, the

contributed equity is estimated to be $441.7 million. For the financial year ending 2018, the

reserves is estimated to be $42.7 million. The retained earnings for the financial year 2018 is

$463.2 million. Hence, the total equity for the financial year ending 2018 is $947.6 million (JB

Hi-Fi Limited. 2018). The fully paid ordinary shares held by the JB Hi-Fi Limited in financial

year 2018 is estimated to be 114883372.

4. Determining group’s current liability for dividends to ordinary shareholders.

The interim dividend for the financial year ending 2018 is 86.0 cent per share. The

dividend paid to the shareholders for the financial year ending 2018 is $132 million. The number

of ordinary shares owned by the JB Hi-Fi Limited is 100. Current year’s total amount associated

with the dividend per share is $13200 million (JB Hi-Fi Limited. 2018). The dividend paid to the

shareholders is estimated to be $151.6 million per share.

1. Evaluating various type of revenues generated by the consolidated group.

Revenue is the amount of income which in turn has been generated from the normal

business activities of the company (Zaw, 2019). JB Hi-Fi Limited has generated deferred

revenue, revenue from the external customers, interest revenue, revenue from contracts, revenue

generated from ordinary activities, etc.

2. Assessing how group assets are classified.

The common types of the assets mainly consist of current asset, physical asset, non-

current asset, operating asset, intangible asset and non- operating asset. The assets can be

classified on the basis of tangible and intangible assets. Furthermore, Tangible assets tends to

contain set of sub- classes which mainly includes fixed and current assets (Pallegedara and

Warren, 2016). Hence, current assets includes cash and cash equivalents, prepaid expenses,

marketable securities, other current assets, trade receivables, inventories, etc. On the other hand,

intangible assets are the one which in turn are non- physical in nature. The non- current assets

mainly includes intangible assets like goodwill, patent, trademarks, copyright, etc., buildings,

plant and machinery, investment and various other non- current assets.

3. Determining number of ordinary shares held by JB Hi-Fi Limited in financial year.

The major categories associated with the group's equity mainly consists of contributed

equity, reserves and retained earnings (Bielefeld, 2016). For the financial year ending 2018, the

contributed equity is estimated to be $441.7 million. For the financial year ending 2018, the

reserves is estimated to be $42.7 million. The retained earnings for the financial year 2018 is

$463.2 million. Hence, the total equity for the financial year ending 2018 is $947.6 million (JB

Hi-Fi Limited. 2018). The fully paid ordinary shares held by the JB Hi-Fi Limited in financial

year 2018 is estimated to be 114883372.

4. Determining group’s current liability for dividends to ordinary shareholders.

The interim dividend for the financial year ending 2018 is 86.0 cent per share. The

dividend paid to the shareholders for the financial year ending 2018 is $132 million. The number

of ordinary shares owned by the JB Hi-Fi Limited is 100. Current year’s total amount associated

with the dividend per share is $13200 million (JB Hi-Fi Limited. 2018). The dividend paid to the

shareholders is estimated to be $151.6 million per share.

5. Dividend payout ratio.

Earning per share is referred to as the ratio which tends to determine the profitability of

the company as compared to the per share of specific stock. On the other hand, dividend per

share tends to show the amount of dividend that in turn has been paid to the shareholders on the

per share. The earning per share of the JB Hi-Fi Limited in financial year 2018 is estimated to be

$203.1 million. The dividend per share of the JB Hi-Fi Limited in financial year 2018 is

estimated to be $132.0 million (JB Hi-Fi Limited. 2018). The total dividend paid for the financial

year 2018 is 132 cents per share. The dividend payout ratio of the JB Hi-Fi Limited in 2018

financial year is estimated to be 65%.

PART C

1. List the subsidiary companies in the JB Hi-Fi Group.

JB Hi-Fi Group tends to have range of subsidiary companies which mainly includes JB

Hi-Fi Group Pty Ltd, Clive Anthony's Pty Ltd, JB Hi-Fi (A) Pty Ltd, R o c k e t R e p l a c e m e n t s

P t y L t d , N e t w o r k N e i g h b o u r h o o d Pty Ltd, JB Hi-Fi Group (NZ) Limited, JB Hi-Fi NZ

Limited. The consolidated financial statements tends to take into consideration the assets and

liabilities of all the subsidiary companies (Johnson, 2017). Subsidiary companies are the entities

which in turn are controlled by the parent company.

2. Determining the value of the group’s sales revenue.

Sales revenue is referred to as the income which in turn has been received by the

company from its sales of the goods and services within the specific financial year. The sales

revenue generated in the financial year 2017 is estimated to be $5628 million (JB Hi-Fi Limited.

2018). The sales revenue generated in the financial year 2018 is estimated to be $6854.3 million.

The percentage change in the sales revenue for the current fiscal year is 21.78%. This has been

calculated as current year sales revenue minus base year sales revenue, divided by the base year

sales revenue multiplied by 100 (6854.3-5628/5628*100).

3. Determining the group’s final profit.

Profit is referred to as the financial gain of the company after taking into consideration

various expenses, interest and tax. This is considered to as the revenue generated from several

business activity within the specific financial year. The profit generated in the financial year

2017 is estimated to be $172.4 million (JB Hi-Fi Limited. 2018). The profit generated in the

financial year 2018 is estimated to be $233.2 million. The percentage change in the profit for the

Earning per share is referred to as the ratio which tends to determine the profitability of

the company as compared to the per share of specific stock. On the other hand, dividend per

share tends to show the amount of dividend that in turn has been paid to the shareholders on the

per share. The earning per share of the JB Hi-Fi Limited in financial year 2018 is estimated to be

$203.1 million. The dividend per share of the JB Hi-Fi Limited in financial year 2018 is

estimated to be $132.0 million (JB Hi-Fi Limited. 2018). The total dividend paid for the financial

year 2018 is 132 cents per share. The dividend payout ratio of the JB Hi-Fi Limited in 2018

financial year is estimated to be 65%.

PART C

1. List the subsidiary companies in the JB Hi-Fi Group.

JB Hi-Fi Group tends to have range of subsidiary companies which mainly includes JB

Hi-Fi Group Pty Ltd, Clive Anthony's Pty Ltd, JB Hi-Fi (A) Pty Ltd, R o c k e t R e p l a c e m e n t s

P t y L t d , N e t w o r k N e i g h b o u r h o o d Pty Ltd, JB Hi-Fi Group (NZ) Limited, JB Hi-Fi NZ

Limited. The consolidated financial statements tends to take into consideration the assets and

liabilities of all the subsidiary companies (Johnson, 2017). Subsidiary companies are the entities

which in turn are controlled by the parent company.

2. Determining the value of the group’s sales revenue.

Sales revenue is referred to as the income which in turn has been received by the

company from its sales of the goods and services within the specific financial year. The sales

revenue generated in the financial year 2017 is estimated to be $5628 million (JB Hi-Fi Limited.

2018). The sales revenue generated in the financial year 2018 is estimated to be $6854.3 million.

The percentage change in the sales revenue for the current fiscal year is 21.78%. This has been

calculated as current year sales revenue minus base year sales revenue, divided by the base year

sales revenue multiplied by 100 (6854.3-5628/5628*100).

3. Determining the group’s final profit.

Profit is referred to as the financial gain of the company after taking into consideration

various expenses, interest and tax. This is considered to as the revenue generated from several

business activity within the specific financial year. The profit generated in the financial year

2017 is estimated to be $172.4 million (JB Hi-Fi Limited. 2018). The profit generated in the

financial year 2018 is estimated to be $233.2 million. The percentage change in the profit for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

current fiscal year is 35.26%. This has been calculated as current year profit minus base year

profit, divided by the base year profit multiplied by 100 (233.2-172.4/172.4*100).

4. Evaluating the percentage change in (2) and (3).

The percentage change of the sales revenue is 21.78% in the financial year 2018. But on

the other hand, the percentage change of the profit is 35.26% in the financial year 2018. This in

turn states that, the sales revenue of the company is comparatively good. JB Hi-Fi Group tends to

have good control over the expenditures of the company. This is the reason profit of the

company is higher when compared to the sales revenue (Thongnoppakun, 2018). The company

must in turn focus on more promotional activities in order to increase the sales of the JB Hi-Fi

Ltd. Company. This in turn leads to higher generation of sales and profitability.

5. Determining the total value of inventories on hand.

Inventory is considered to be the raw material which in turn is required by the company

to produce finished goods. Inventories at the end of the year 2017 is estimated to be $859.7

million. Hence, there is an increase in the inventory levels at the end of the year 2018 is

estimated to be $891.1 million (JB Hi-Fi Limited. 2018). The percentage change in the inventory

levels is estimated to be 3.65%. This has been calculated as current year profit minus base year

profit, divided by the base year profit multiplied by 100 (891.1-859.7/859.7*100).

The percentage change in the sales revenue is estimated to be 21.78%. But on the other

hand, the inventory change is estimated to be 3.65%. The inventory turnover of the company

states that, the company tends to focus on increasing their prices for the product and the

customers are willing to buy products at high price because of the good quality goods and

services (Babich, 2016). This in turn results in higher change in the sales revenue when

compared with the inventory turnover.

6. Calculating profit margins and inventory turnover.

Profit margin is referred to as an amount where the revenue generated from the sales tend

to exceed the cost associated with the business. This profitability ratio is useful in assessing the

percentage of sales which has generated profits for the company (Morgan, 2019). The formula of

the profit margin is net sales minus cost of the goods sold which in turn is divided by the net

sales.

Inventory turnover ratio is considered to be another profitability ratio which in turn helps

in determining the number of times company has replaced inventory during specific financial

profit, divided by the base year profit multiplied by 100 (233.2-172.4/172.4*100).

4. Evaluating the percentage change in (2) and (3).

The percentage change of the sales revenue is 21.78% in the financial year 2018. But on

the other hand, the percentage change of the profit is 35.26% in the financial year 2018. This in

turn states that, the sales revenue of the company is comparatively good. JB Hi-Fi Group tends to

have good control over the expenditures of the company. This is the reason profit of the

company is higher when compared to the sales revenue (Thongnoppakun, 2018). The company

must in turn focus on more promotional activities in order to increase the sales of the JB Hi-Fi

Ltd. Company. This in turn leads to higher generation of sales and profitability.

5. Determining the total value of inventories on hand.

Inventory is considered to be the raw material which in turn is required by the company

to produce finished goods. Inventories at the end of the year 2017 is estimated to be $859.7

million. Hence, there is an increase in the inventory levels at the end of the year 2018 is

estimated to be $891.1 million (JB Hi-Fi Limited. 2018). The percentage change in the inventory

levels is estimated to be 3.65%. This has been calculated as current year profit minus base year

profit, divided by the base year profit multiplied by 100 (891.1-859.7/859.7*100).

The percentage change in the sales revenue is estimated to be 21.78%. But on the other

hand, the inventory change is estimated to be 3.65%. The inventory turnover of the company

states that, the company tends to focus on increasing their prices for the product and the

customers are willing to buy products at high price because of the good quality goods and

services (Babich, 2016). This in turn results in higher change in the sales revenue when

compared with the inventory turnover.

6. Calculating profit margins and inventory turnover.

Profit margin is referred to as an amount where the revenue generated from the sales tend

to exceed the cost associated with the business. This profitability ratio is useful in assessing the

percentage of sales which has generated profits for the company (Morgan, 2019). The formula of

the profit margin is net sales minus cost of the goods sold which in turn is divided by the net

sales.

Inventory turnover ratio is considered to be another profitability ratio which in turn helps

in determining the number of times company has replaced inventory during specific financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

period (Howland, 2017). The formula of the inventory turnover is sales divided by the average

inventory.

Profitability ratio analysis

2018

Gross Profit 1470

Net profit 233.2

GP ratio Gross profit / sales * 100 21%

NP ratio Net profit / sales * 100 3%

Efficiency ratio analysis

2018

Cost of goods sold 5384.1

Average Inventory 891.1

Stock turnover ratio (In times) 6.042082819

CONCLUSION

From the above conducted study it has been concluded that, accounting helps in

summarizing the operations of the company by understanding its financial position. This study

examines that, decrease in the cash and cash equivalents and inventories will affect the credit

side of the account. This study demonstrates that, assets can be classified current assets and non-

current assets. Furthermore, it has been summarized that, the profitability of the company is

higher when compared with the sales revenue. The company must focus on more promotional

activities in order to increase the sales of the JB Hi-Fi Ltd. Company. Furthermore, this study

also concludes various profitability ratios.

inventory.

Profitability ratio analysis

2018

Gross Profit 1470

Net profit 233.2

GP ratio Gross profit / sales * 100 21%

NP ratio Net profit / sales * 100 3%

Efficiency ratio analysis

2018

Cost of goods sold 5384.1

Average Inventory 891.1

Stock turnover ratio (In times) 6.042082819

CONCLUSION

From the above conducted study it has been concluded that, accounting helps in

summarizing the operations of the company by understanding its financial position. This study

examines that, decrease in the cash and cash equivalents and inventories will affect the credit

side of the account. This study demonstrates that, assets can be classified current assets and non-

current assets. Furthermore, it has been summarized that, the profitability of the company is

higher when compared with the sales revenue. The company must focus on more promotional

activities in order to increase the sales of the JB Hi-Fi Ltd. Company. Furthermore, this study

also concludes various profitability ratios.

REFERENCES

Books and Journals

Babich, B., 2016. The Hallelujah effect: philosophical reflections on music, performance

practice, and technology. Routledge.

Bielefeld, S., 2016. Income management and Indigenous women: A new chapter of patriarchal

colonial governance. UNSWLJ. 39. p.843.

Birt, J. and et.al., 2019. Accounting: Business reporting for decision making. John Wiley &

Sons.

Collier, P. M. and Munir, R., 2016. Performance measurement. In Strategic management

accounting. (pp. 235-356). Deakin University.

de Lautour, V. J., 2018. Strategic Management Accounting: Aligning strategy, operations and

finance (Vol. 1). Springer.

Howland, J. ed., 2017. Duke Ellington Studies. Cambridge University Press.

Johnson, B., 2017. Technologized Sonority. In Dark Side of the Tune: Popular Music and

Violence. (pp. 65-80). Routledge.

Morgan, D. ed., 2019. The unconscious in social and political life. Phoenix Publishing House.

Nambukara-Gamage, B. and Peries, S. T., 2020. The Impact of Dividend Policy on Shareholder

Wealth: A Study on the Retailing Industry of Australia. Review of Integrative Business and

Economics Research. 9(1). pp.38-50.

Pallegedara, D. and Warren, M., 2016. Unauthorised Disclosure of Organisational Information

through Social Media: A Policy Perspective. IDIMC 2016. 86.

Thongnoppakun, C., 2018. Are gamers better at anticipatory responding and anticipatory

response inhibition? (Doctoral dissertation, University of Tasmania).

Zaw, P., 2019. Planned manufactured capital investment disclosures in annual and integrated

reports: Evidence from New Zealand and Australian organisations (Doctoral dissertation,

Auckland University of Technology).

Online

Books and Journals

Babich, B., 2016. The Hallelujah effect: philosophical reflections on music, performance

practice, and technology. Routledge.

Bielefeld, S., 2016. Income management and Indigenous women: A new chapter of patriarchal

colonial governance. UNSWLJ. 39. p.843.

Birt, J. and et.al., 2019. Accounting: Business reporting for decision making. John Wiley &

Sons.

Collier, P. M. and Munir, R., 2016. Performance measurement. In Strategic management

accounting. (pp. 235-356). Deakin University.

de Lautour, V. J., 2018. Strategic Management Accounting: Aligning strategy, operations and

finance (Vol. 1). Springer.

Howland, J. ed., 2017. Duke Ellington Studies. Cambridge University Press.

Johnson, B., 2017. Technologized Sonority. In Dark Side of the Tune: Popular Music and

Violence. (pp. 65-80). Routledge.

Morgan, D. ed., 2019. The unconscious in social and political life. Phoenix Publishing House.

Nambukara-Gamage, B. and Peries, S. T., 2020. The Impact of Dividend Policy on Shareholder

Wealth: A Study on the Retailing Industry of Australia. Review of Integrative Business and

Economics Research. 9(1). pp.38-50.

Pallegedara, D. and Warren, M., 2016. Unauthorised Disclosure of Organisational Information

through Social Media: A Policy Perspective. IDIMC 2016. 86.

Thongnoppakun, C., 2018. Are gamers better at anticipatory responding and anticipatory

response inhibition? (Doctoral dissertation, University of Tasmania).

Zaw, P., 2019. Planned manufactured capital investment disclosures in annual and integrated

reports: Evidence from New Zealand and Australian organisations (Doctoral dissertation,

Auckland University of Technology).

Online

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

JB Hi-Fi Limited. 2018. [Online]. Available through:<www.jbhifi.com.au/>

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.