Detailed Analysis of Financial Performance and Investment Appraisal

VerifiedAdded on 2023/06/14

|18

|3063

|362

Report

AI Summary

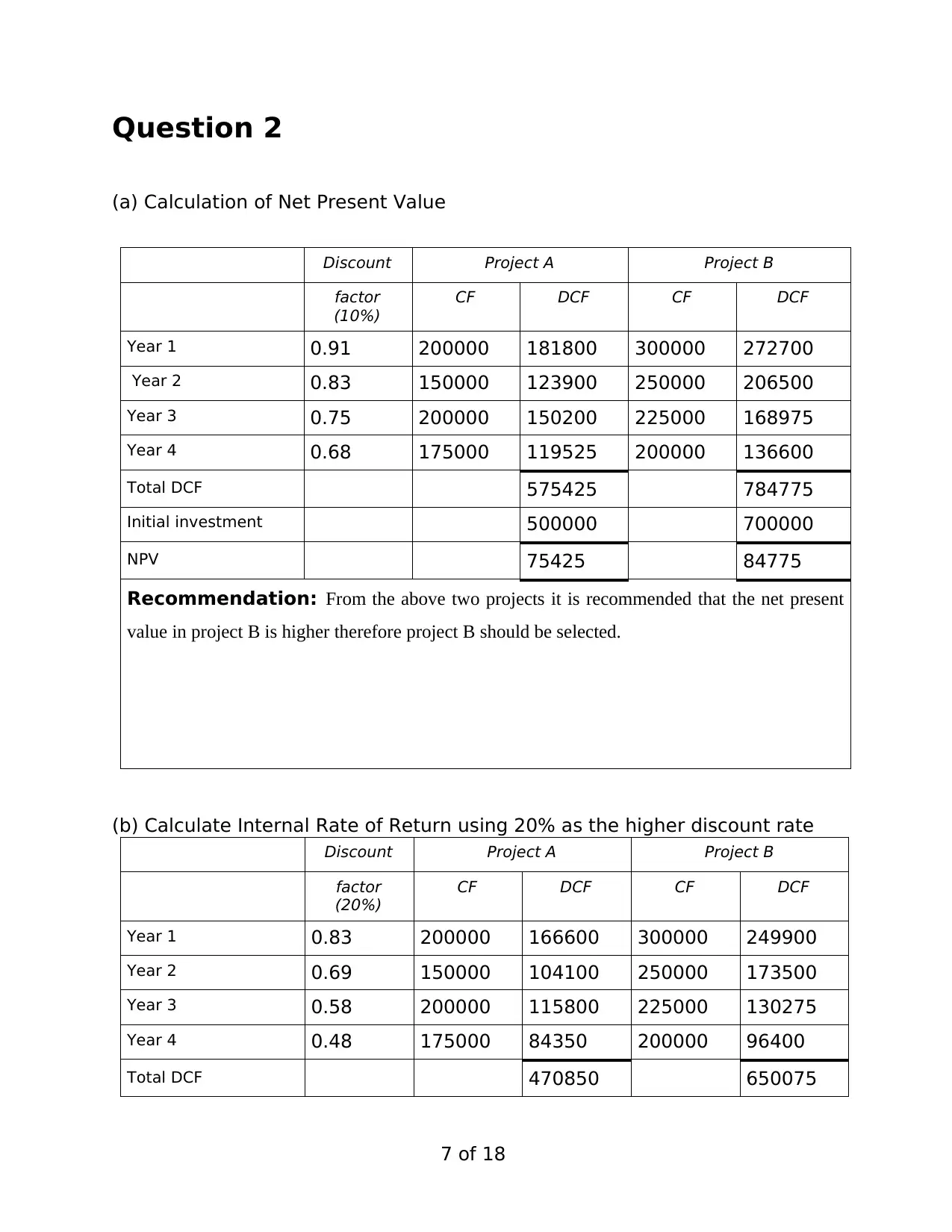

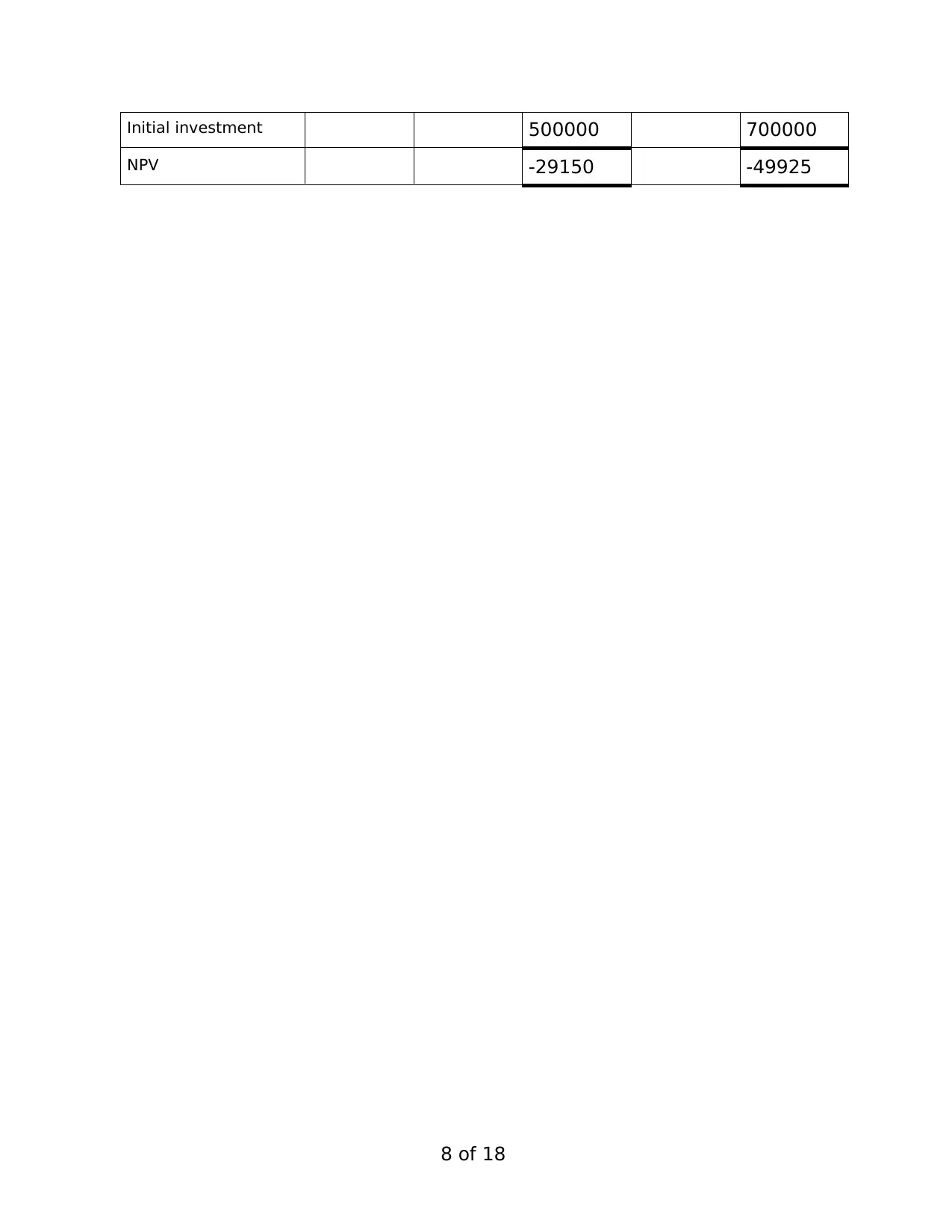

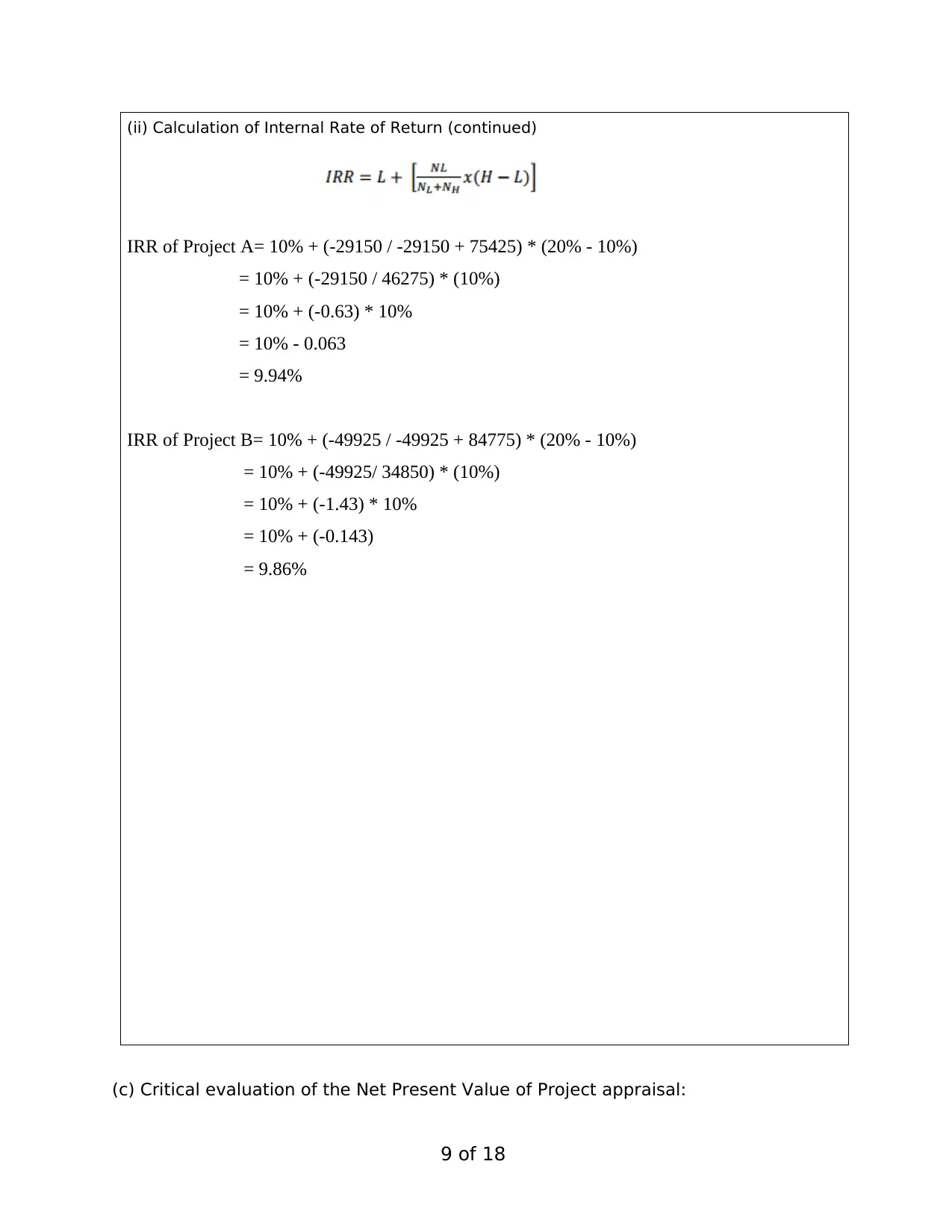

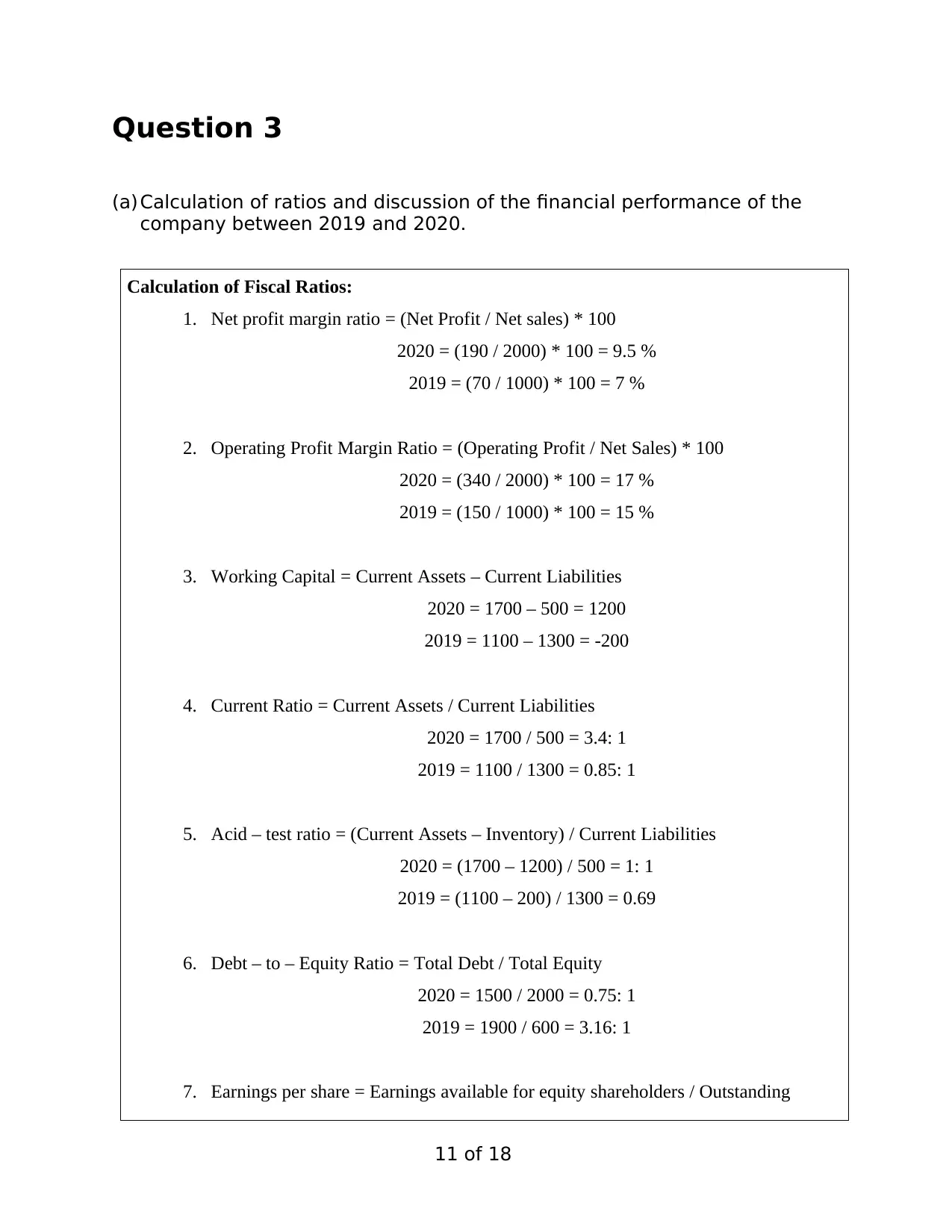

This assignment provides a detailed financial analysis and project appraisal. It includes calculations of budgeted costs using activity-based costing (ABC), a critical evaluation of ABC as a costing method, and how activity-based management can assist in better management decision-making. The assignment also covers project appraisal using Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index, with a critical evaluation of NPV. Furthermore, it includes the calculation of financial ratios to assess the company's performance between 2019 and 2020 and a critical evaluation of the Balanced Scorecard method. Finally, it provides calculations of material and labor variances with explanations, offering a comprehensive overview of financial analysis and performance assessment.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.