Accounting for Business: Financial Statement Analysis and Proposals

VerifiedAdded on 2023/06/18

|12

|1842

|108

Report

AI Summary

This report provides a comprehensive financial analysis of a business, including an income statement and statement of financial position to assess profitability and financial health. It calculates payback period and net present value (NPV) for investment appraisal, advising on financial viability and considering non-financial factors. The report also includes a break-even analysis for various proposals, using marginal costing to determine the most financially viable option. Desklib offers this and many more solved assignments for students.

Accounting for Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

SECTON B......................................................................................................................................5

Question 3...................................................................................................................................5

Question 4...................................................................................................................................7

REFERENCES..............................................................................................................................12

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

SECTON B......................................................................................................................................5

Question 3...................................................................................................................................5

Question 4...................................................................................................................................7

REFERENCES..............................................................................................................................12

SECTION A

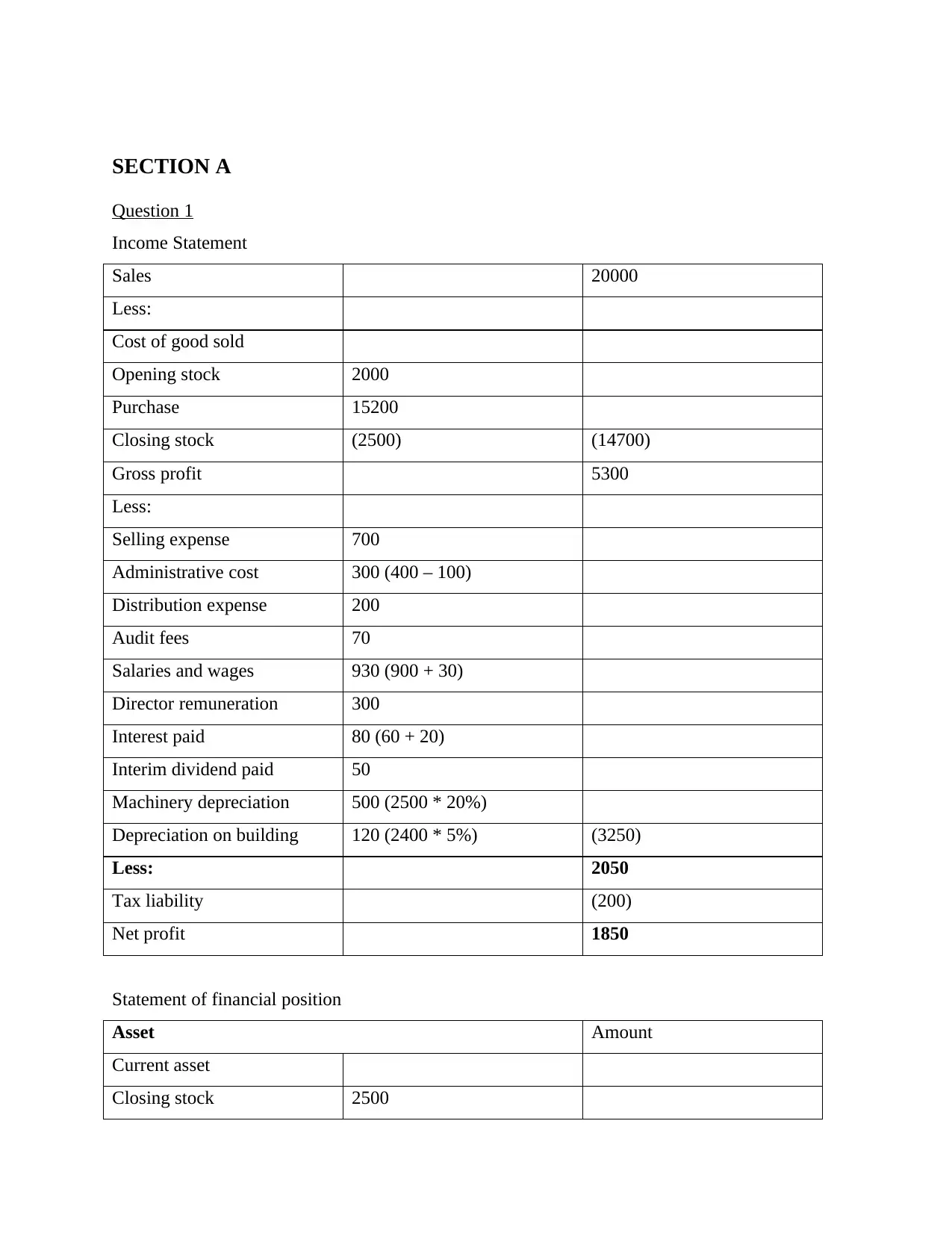

Question 1

Income Statement

Sales 20000

Less:

Cost of good sold

Opening stock 2000

Purchase 15200

Closing stock (2500) (14700)

Gross profit 5300

Less:

Selling expense 700

Administrative cost 300 (400 – 100)

Distribution expense 200

Audit fees 70

Salaries and wages 930 (900 + 30)

Director remuneration 300

Interest paid 80 (60 + 20)

Interim dividend paid 50

Machinery depreciation 500 (2500 * 20%)

Depreciation on building 120 (2400 * 5%) (3250)

Less: 2050

Tax liability (200)

Net profit 1850

Statement of financial position

Asset Amount

Current asset

Closing stock 2500

Question 1

Income Statement

Sales 20000

Less:

Cost of good sold

Opening stock 2000

Purchase 15200

Closing stock (2500) (14700)

Gross profit 5300

Less:

Selling expense 700

Administrative cost 300 (400 – 100)

Distribution expense 200

Audit fees 70

Salaries and wages 930 (900 + 30)

Director remuneration 300

Interest paid 80 (60 + 20)

Interim dividend paid 50

Machinery depreciation 500 (2500 * 20%)

Depreciation on building 120 (2400 * 5%) (3250)

Less: 2050

Tax liability (200)

Net profit 1850

Statement of financial position

Asset Amount

Current asset

Closing stock 2500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

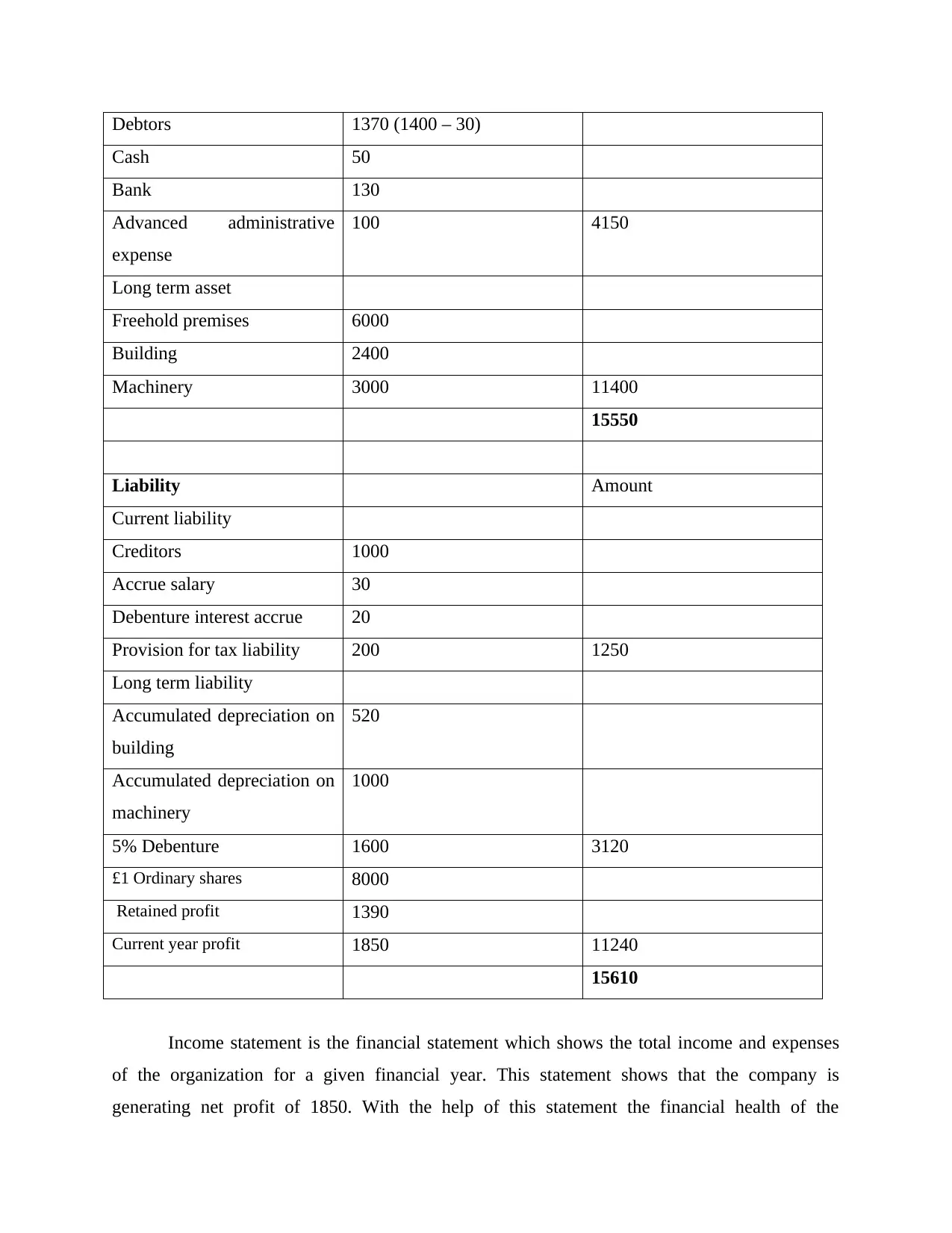

Debtors 1370 (1400 – 30)

Cash 50

Bank 130

Advanced administrative

expense

100 4150

Long term asset

Freehold premises 6000

Building 2400

Machinery 3000 11400

15550

Liability Amount

Current liability

Creditors 1000

Accrue salary 30

Debenture interest accrue 20

Provision for tax liability 200 1250

Long term liability

Accumulated depreciation on

building

520

Accumulated depreciation on

machinery

1000

5% Debenture 1600 3120

£1 Ordinary shares 8000

Retained profit 1390

Current year profit 1850 11240

15610

Income statement is the financial statement which shows the total income and expenses

of the organization for a given financial year. This statement shows that the company is

generating net profit of 1850. With the help of this statement the financial health of the

Cash 50

Bank 130

Advanced administrative

expense

100 4150

Long term asset

Freehold premises 6000

Building 2400

Machinery 3000 11400

15550

Liability Amount

Current liability

Creditors 1000

Accrue salary 30

Debenture interest accrue 20

Provision for tax liability 200 1250

Long term liability

Accumulated depreciation on

building

520

Accumulated depreciation on

machinery

1000

5% Debenture 1600 3120

£1 Ordinary shares 8000

Retained profit 1390

Current year profit 1850 11240

15610

Income statement is the financial statement which shows the total income and expenses

of the organization for a given financial year. This statement shows that the company is

generating net profit of 1850. With the help of this statement the financial health of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization is understood which in this income statement shows that the business is generating

profit which is very low in comparison to its revenue generated. In a income statement the

different expenses and income of the organization is calculated and noted for being analysed as

in the preparation of the future budget (Li and et.al., 2018). The revenue is the sales which is

shown in the income statement. There are two types of expenses in the income statement, direct

and indirect expenses. This statement calculated both the gross and net profit for the

organization.

The statement of financial position also known as the balance sheet is the report which

shows the company’s assets, liabilities and shareholder’s equity. Balance sheet preparation is one

of the three most core financial statements which are used for the evaluation of the business. It

helps in the analysation financial position of the company which shows. The three components

of the balance sheet which shows the financial position are the assets, liabilities and equity. The

assets of the organization are equal to the liabilities of the organization when this financial

position report is finalized.

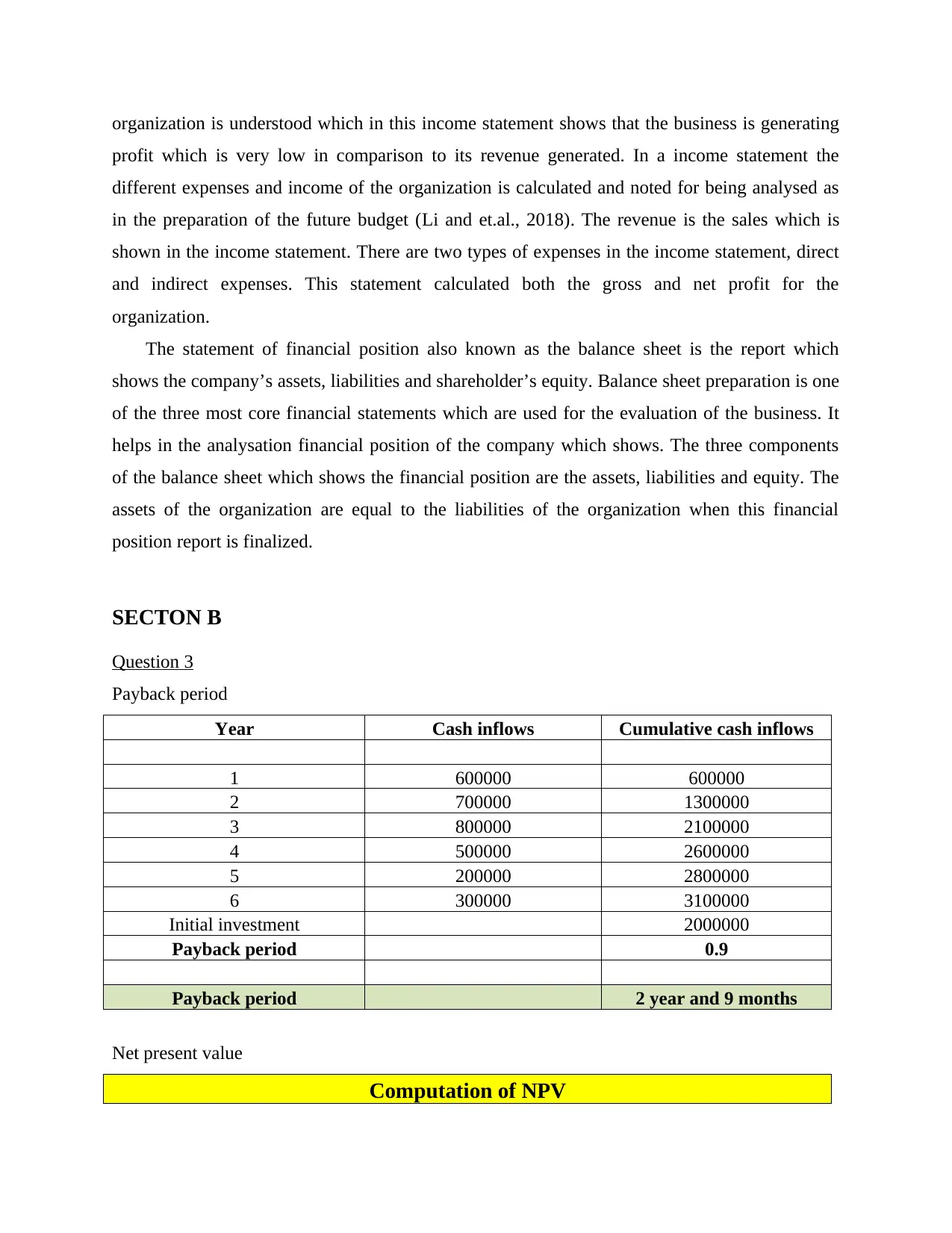

SECTON B

Question 3

Payback period

Year Cash inflows Cumulative cash inflows

1 600000 600000

2 700000 1300000

3 800000 2100000

4 500000 2600000

5 200000 2800000

6 300000 3100000

Initial investment 2000000

Payback period 0.9

Payback period 2 year and 9 months

Net present value

Computation of NPV

profit which is very low in comparison to its revenue generated. In a income statement the

different expenses and income of the organization is calculated and noted for being analysed as

in the preparation of the future budget (Li and et.al., 2018). The revenue is the sales which is

shown in the income statement. There are two types of expenses in the income statement, direct

and indirect expenses. This statement calculated both the gross and net profit for the

organization.

The statement of financial position also known as the balance sheet is the report which

shows the company’s assets, liabilities and shareholder’s equity. Balance sheet preparation is one

of the three most core financial statements which are used for the evaluation of the business. It

helps in the analysation financial position of the company which shows. The three components

of the balance sheet which shows the financial position are the assets, liabilities and equity. The

assets of the organization are equal to the liabilities of the organization when this financial

position report is finalized.

SECTON B

Question 3

Payback period

Year Cash inflows Cumulative cash inflows

1 600000 600000

2 700000 1300000

3 800000 2100000

4 500000 2600000

5 200000 2800000

6 300000 3100000

Initial investment 2000000

Payback period 0.9

Payback period 2 year and 9 months

Net present value

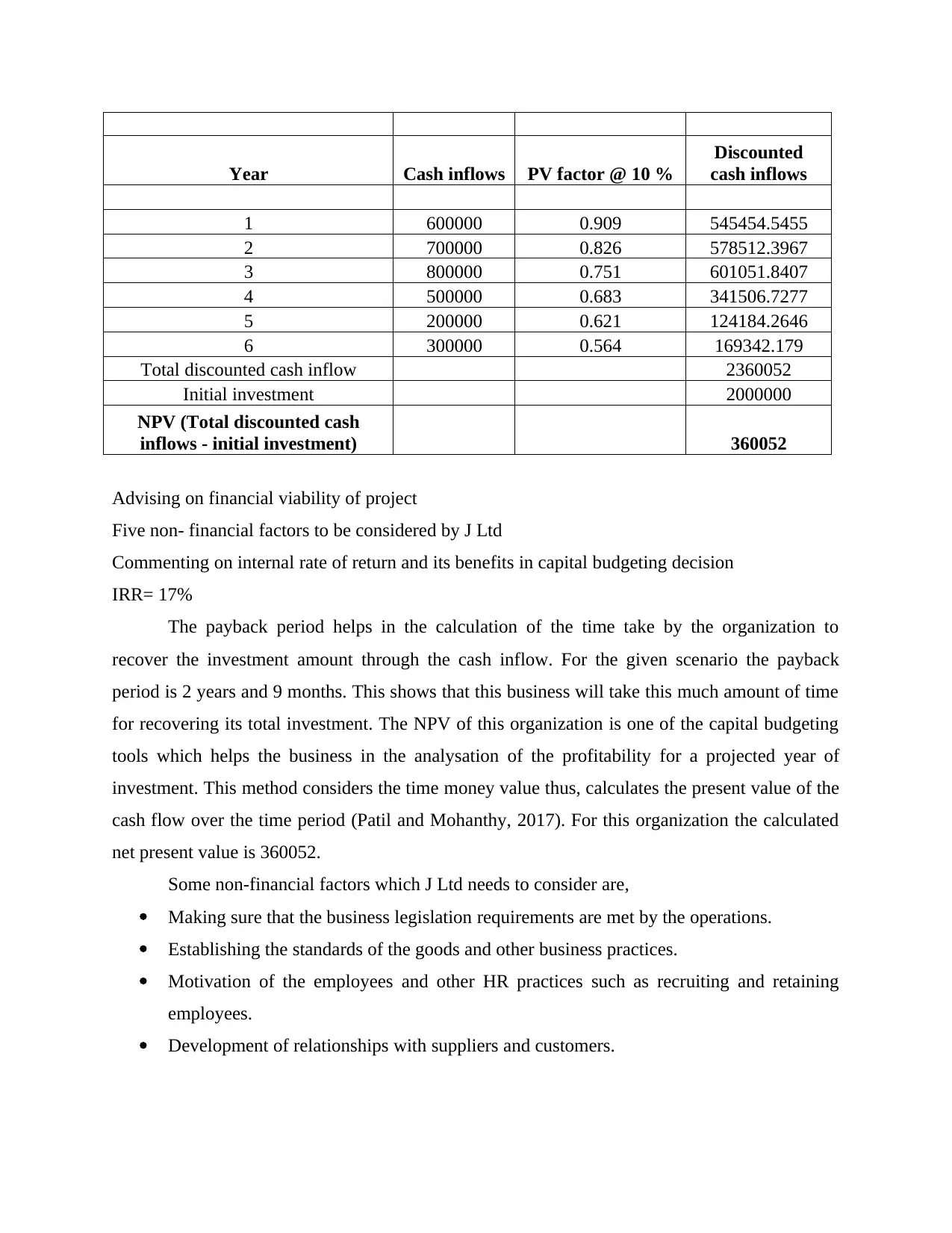

Computation of NPV

Year Cash inflows PV factor @ 10 %

Discounted

cash inflows

1 600000 0.909 545454.5455

2 700000 0.826 578512.3967

3 800000 0.751 601051.8407

4 500000 0.683 341506.7277

5 200000 0.621 124184.2646

6 300000 0.564 169342.179

Total discounted cash inflow 2360052

Initial investment 2000000

NPV (Total discounted cash

inflows - initial investment) 360052

Advising on financial viability of project

Five non- financial factors to be considered by J Ltd

Commenting on internal rate of return and its benefits in capital budgeting decision

IRR= 17%

The payback period helps in the calculation of the time take by the organization to

recover the investment amount through the cash inflow. For the given scenario the payback

period is 2 years and 9 months. This shows that this business will take this much amount of time

for recovering its total investment. The NPV of this organization is one of the capital budgeting

tools which helps the business in the analysation of the profitability for a projected year of

investment. This method considers the time money value thus, calculates the present value of the

cash flow over the time period (Patil and Mohanthy, 2017). For this organization the calculated

net present value is 360052.

Some non-financial factors which J Ltd needs to consider are,

Making sure that the business legislation requirements are met by the operations.

Establishing the standards of the goods and other business practices.

Motivation of the employees and other HR practices such as recruiting and retaining

employees.

Development of relationships with suppliers and customers.

Discounted

cash inflows

1 600000 0.909 545454.5455

2 700000 0.826 578512.3967

3 800000 0.751 601051.8407

4 500000 0.683 341506.7277

5 200000 0.621 124184.2646

6 300000 0.564 169342.179

Total discounted cash inflow 2360052

Initial investment 2000000

NPV (Total discounted cash

inflows - initial investment) 360052

Advising on financial viability of project

Five non- financial factors to be considered by J Ltd

Commenting on internal rate of return and its benefits in capital budgeting decision

IRR= 17%

The payback period helps in the calculation of the time take by the organization to

recover the investment amount through the cash inflow. For the given scenario the payback

period is 2 years and 9 months. This shows that this business will take this much amount of time

for recovering its total investment. The NPV of this organization is one of the capital budgeting

tools which helps the business in the analysation of the profitability for a projected year of

investment. This method considers the time money value thus, calculates the present value of the

cash flow over the time period (Patil and Mohanthy, 2017). For this organization the calculated

net present value is 360052.

Some non-financial factors which J Ltd needs to consider are,

Making sure that the business legislation requirements are met by the operations.

Establishing the standards of the goods and other business practices.

Motivation of the employees and other HR practices such as recruiting and retaining

employees.

Development of relationships with suppliers and customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The internal rate of return is a financial analysis which helps in the estimation of the

profitability of the organization which is the potential investments of the organization. The IRR

is a discount rate which makes the net present value of all the cash flows which for this

organization is 17% in the discounted cash flow analysis.

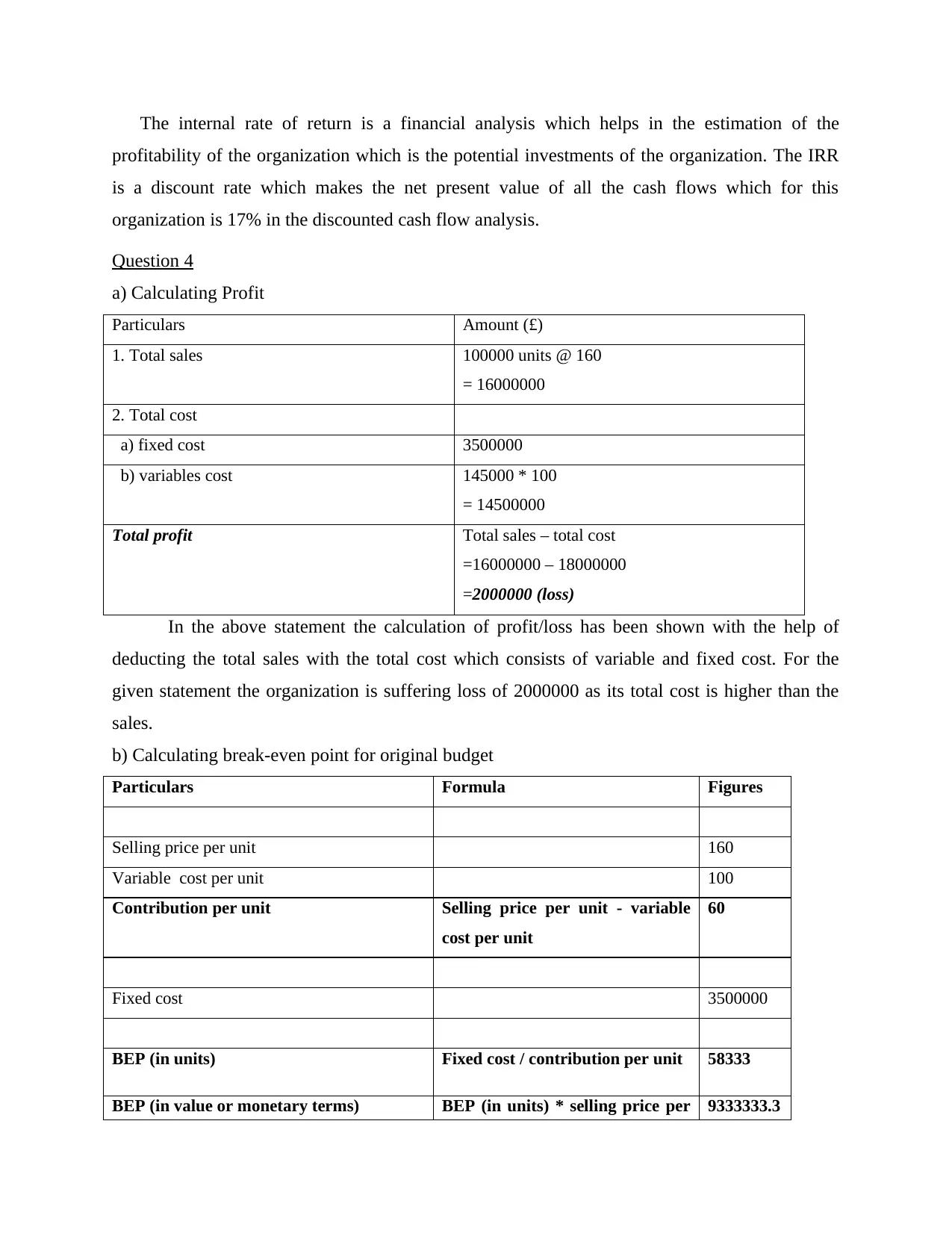

Question 4

a) Calculating Profit

Particulars Amount (£)

1. Total sales 100000 units @ 160

= 16000000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=16000000 – 18000000

=2000000 (loss)

In the above statement the calculation of profit/loss has been shown with the help of

deducting the total sales with the total cost which consists of variable and fixed cost. For the

given statement the organization is suffering loss of 2000000 as its total cost is higher than the

sales.

b) Calculating break-even point for original budget

Particulars Formula Figures

Selling price per unit 160

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

60

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 58333

BEP (in value or monetary terms) BEP (in units) * selling price per 9333333.3

profitability of the organization which is the potential investments of the organization. The IRR

is a discount rate which makes the net present value of all the cash flows which for this

organization is 17% in the discounted cash flow analysis.

Question 4

a) Calculating Profit

Particulars Amount (£)

1. Total sales 100000 units @ 160

= 16000000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=16000000 – 18000000

=2000000 (loss)

In the above statement the calculation of profit/loss has been shown with the help of

deducting the total sales with the total cost which consists of variable and fixed cost. For the

given statement the organization is suffering loss of 2000000 as its total cost is higher than the

sales.

b) Calculating break-even point for original budget

Particulars Formula Figures

Selling price per unit 160

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

60

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 58333

BEP (in value or monetary terms) BEP (in units) * selling price per 9333333.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

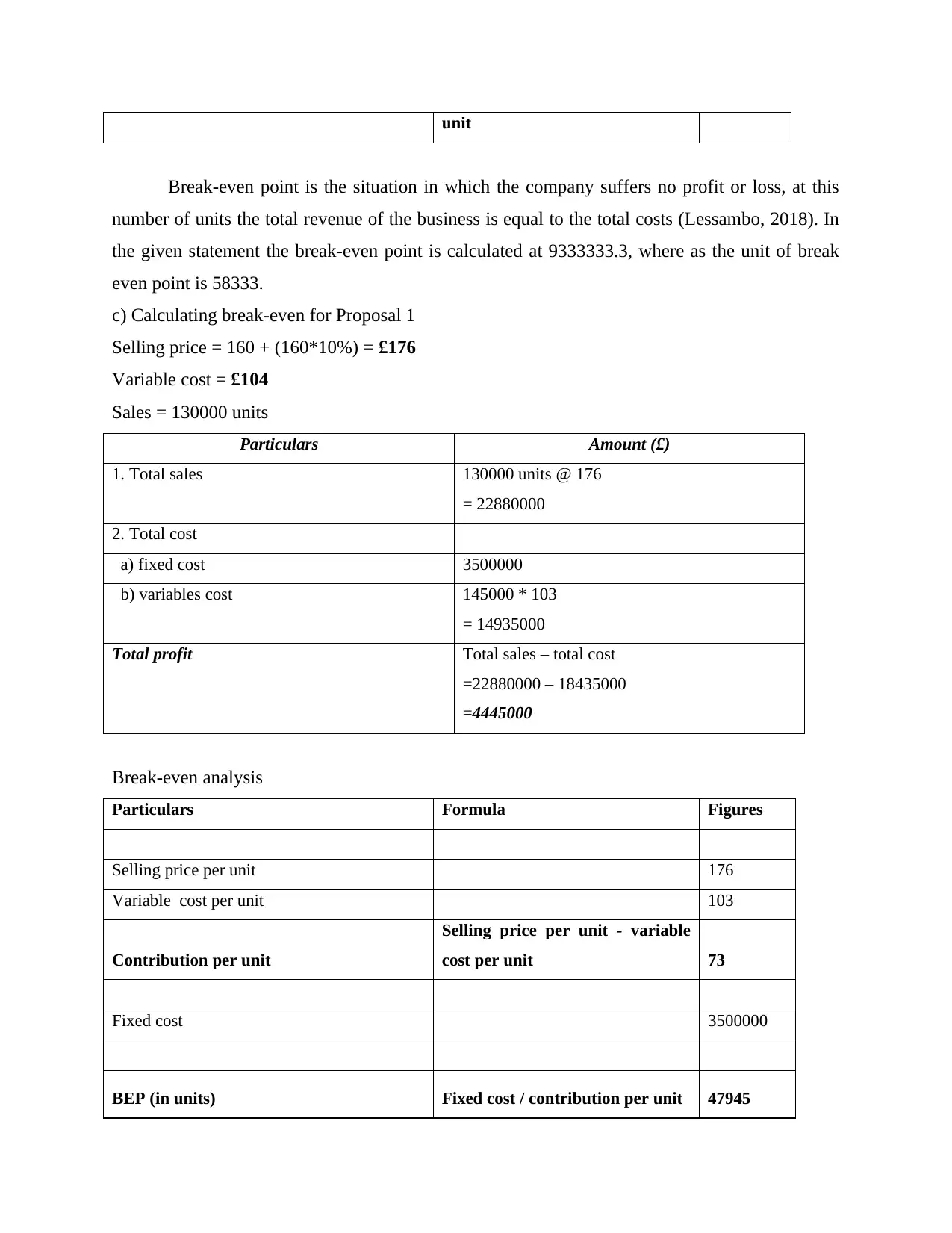

unit

Break-even point is the situation in which the company suffers no profit or loss, at this

number of units the total revenue of the business is equal to the total costs (Lessambo, 2018). In

the given statement the break-even point is calculated at 9333333.3, where as the unit of break

even point is 58333.

c) Calculating break-even for Proposal 1

Selling price = 160 + (160*10%) = £176

Variable cost = £104

Sales = 130000 units

Particulars Amount (£)

1. Total sales 130000 units @ 176

= 22880000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 103

= 14935000

Total profit Total sales – total cost

=22880000 – 18435000

=4445000

Break-even analysis

Particulars Formula Figures

Selling price per unit 176

Variable cost per unit 103

Contribution per unit

Selling price per unit - variable

cost per unit 73

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 47945

Break-even point is the situation in which the company suffers no profit or loss, at this

number of units the total revenue of the business is equal to the total costs (Lessambo, 2018). In

the given statement the break-even point is calculated at 9333333.3, where as the unit of break

even point is 58333.

c) Calculating break-even for Proposal 1

Selling price = 160 + (160*10%) = £176

Variable cost = £104

Sales = 130000 units

Particulars Amount (£)

1. Total sales 130000 units @ 176

= 22880000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 103

= 14935000

Total profit Total sales – total cost

=22880000 – 18435000

=4445000

Break-even analysis

Particulars Formula Figures

Selling price per unit 176

Variable cost per unit 103

Contribution per unit

Selling price per unit - variable

cost per unit 73

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 47945

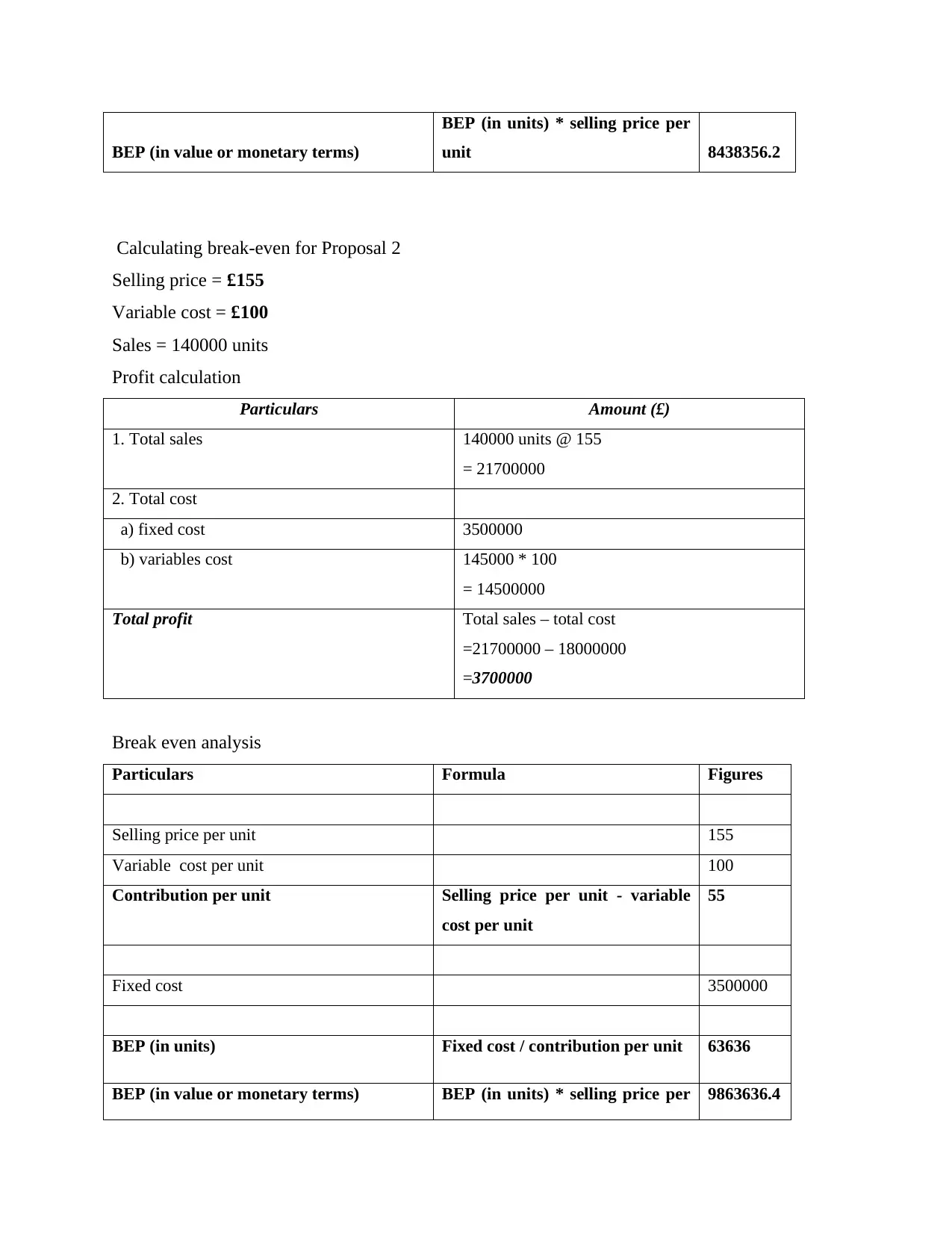

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 8438356.2

Calculating break-even for Proposal 2

Selling price = £155

Variable cost = £100

Sales = 140000 units

Profit calculation

Particulars Amount (£)

1. Total sales 140000 units @ 155

= 21700000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=21700000 – 18000000

=3700000

Break even analysis

Particulars Formula Figures

Selling price per unit 155

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

55

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 63636

BEP (in value or monetary terms) BEP (in units) * selling price per 9863636.4

BEP (in units) * selling price per

unit 8438356.2

Calculating break-even for Proposal 2

Selling price = £155

Variable cost = £100

Sales = 140000 units

Profit calculation

Particulars Amount (£)

1. Total sales 140000 units @ 155

= 21700000

2. Total cost

a) fixed cost 3500000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=21700000 – 18000000

=3700000

Break even analysis

Particulars Formula Figures

Selling price per unit 155

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

55

Fixed cost 3500000

BEP (in units) Fixed cost / contribution per unit 63636

BEP (in value or monetary terms) BEP (in units) * selling price per 9863636.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

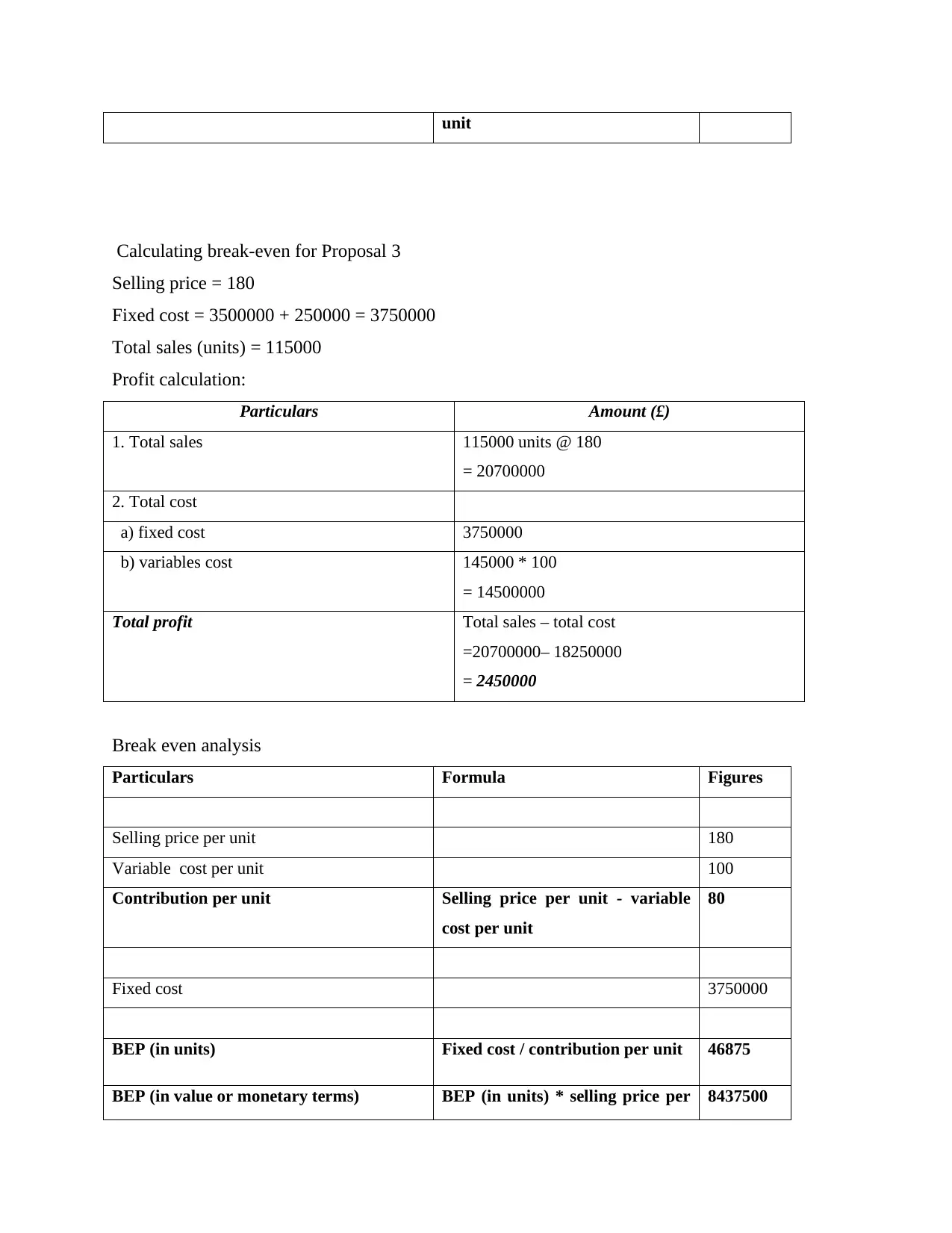

unit

Calculating break-even for Proposal 3

Selling price = 180

Fixed cost = 3500000 + 250000 = 3750000

Total sales (units) = 115000

Profit calculation:

Particulars Amount (£)

1. Total sales 115000 units @ 180

= 20700000

2. Total cost

a) fixed cost 3750000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=20700000– 18250000

= 2450000

Break even analysis

Particulars Formula Figures

Selling price per unit 180

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

80

Fixed cost 3750000

BEP (in units) Fixed cost / contribution per unit 46875

BEP (in value or monetary terms) BEP (in units) * selling price per 8437500

Calculating break-even for Proposal 3

Selling price = 180

Fixed cost = 3500000 + 250000 = 3750000

Total sales (units) = 115000

Profit calculation:

Particulars Amount (£)

1. Total sales 115000 units @ 180

= 20700000

2. Total cost

a) fixed cost 3750000

b) variables cost 145000 * 100

= 14500000

Total profit Total sales – total cost

=20700000– 18250000

= 2450000

Break even analysis

Particulars Formula Figures

Selling price per unit 180

Variable cost per unit 100

Contribution per unit Selling price per unit - variable

cost per unit

80

Fixed cost 3750000

BEP (in units) Fixed cost / contribution per unit 46875

BEP (in value or monetary terms) BEP (in units) * selling price per 8437500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unit

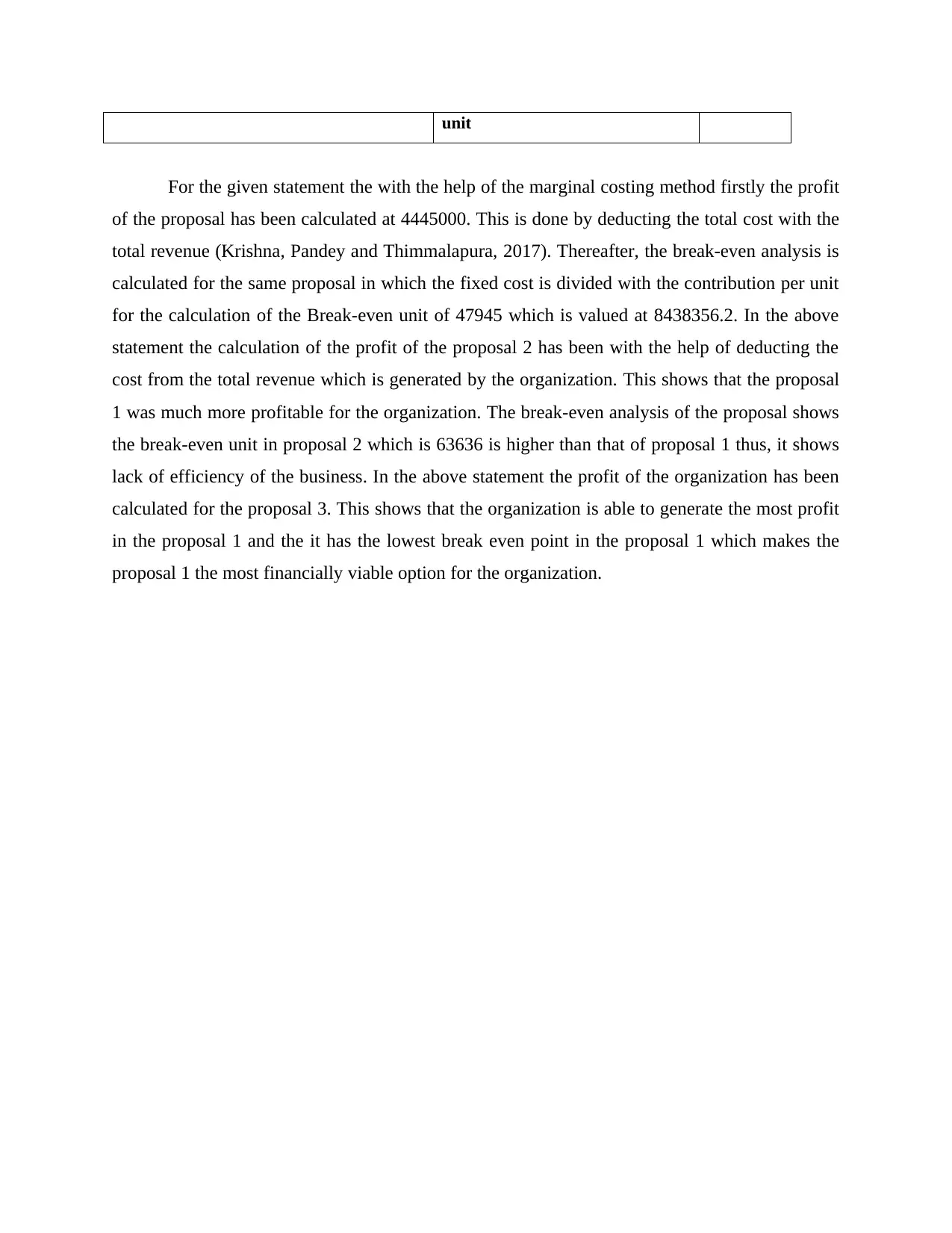

For the given statement the with the help of the marginal costing method firstly the profit

of the proposal has been calculated at 4445000. This is done by deducting the total cost with the

total revenue (Krishna, Pandey and Thimmalapura, 2017). Thereafter, the break-even analysis is

calculated for the same proposal in which the fixed cost is divided with the contribution per unit

for the calculation of the Break-even unit of 47945 which is valued at 8438356.2. In the above

statement the calculation of the profit of the proposal 2 has been with the help of deducting the

cost from the total revenue which is generated by the organization. This shows that the proposal

1 was much more profitable for the organization. The break-even analysis of the proposal shows

the break-even unit in proposal 2 which is 63636 is higher than that of proposal 1 thus, it shows

lack of efficiency of the business. In the above statement the profit of the organization has been

calculated for the proposal 3. This shows that the organization is able to generate the most profit

in the proposal 1 and the it has the lowest break even point in the proposal 1 which makes the

proposal 1 the most financially viable option for the organization.

For the given statement the with the help of the marginal costing method firstly the profit

of the proposal has been calculated at 4445000. This is done by deducting the total cost with the

total revenue (Krishna, Pandey and Thimmalapura, 2017). Thereafter, the break-even analysis is

calculated for the same proposal in which the fixed cost is divided with the contribution per unit

for the calculation of the Break-even unit of 47945 which is valued at 8438356.2. In the above

statement the calculation of the profit of the proposal 2 has been with the help of deducting the

cost from the total revenue which is generated by the organization. This shows that the proposal

1 was much more profitable for the organization. The break-even analysis of the proposal shows

the break-even unit in proposal 2 which is 63636 is higher than that of proposal 1 thus, it shows

lack of efficiency of the business. In the above statement the profit of the organization has been

calculated for the proposal 3. This shows that the organization is able to generate the most profit

in the proposal 1 and the it has the lowest break even point in the proposal 1 which makes the

proposal 1 the most financially viable option for the organization.

REFERENCES

Books and Journals

Krishna, K.M., Pandey, N.K. and Thimmalapura, S., 2017, December. Break-even analysis and

economic viability of powertrain electrification—An analytical approach. In 2017 IEEE

Transportation Electrification Conference (ITEC-India) (pp. 1-6). IEEE.

Lessambo, F.I., 2018. Forecasting Financial Statements’ Analysis. In Financial Statements (pp.

251-258). Palgrave Macmillan, Cham.

Li, J., and et.al., 2018. Financial statements based bank risk aggregation. Review of Quantitative

Finance and Accounting, 50(3), pp.673-694.

Patil, D. and Mohanthy, J.N., 2017. Analysis of Financial Statements in the Sugar Industry.

Available at SSRN 2962855.

Books and Journals

Krishna, K.M., Pandey, N.K. and Thimmalapura, S., 2017, December. Break-even analysis and

economic viability of powertrain electrification—An analytical approach. In 2017 IEEE

Transportation Electrification Conference (ITEC-India) (pp. 1-6). IEEE.

Lessambo, F.I., 2018. Forecasting Financial Statements’ Analysis. In Financial Statements (pp.

251-258). Palgrave Macmillan, Cham.

Li, J., and et.al., 2018. Financial statements based bank risk aggregation. Review of Quantitative

Finance and Accounting, 50(3), pp.673-694.

Patil, D. and Mohanthy, J.N., 2017. Analysis of Financial Statements in the Sugar Industry.

Available at SSRN 2962855.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.