Accounting Exercises: Stock Options, Restricted Stock & EPS Analysis

VerifiedAdded on 2023/05/30

|6

|599

|117

Homework Assignment

AI Summary

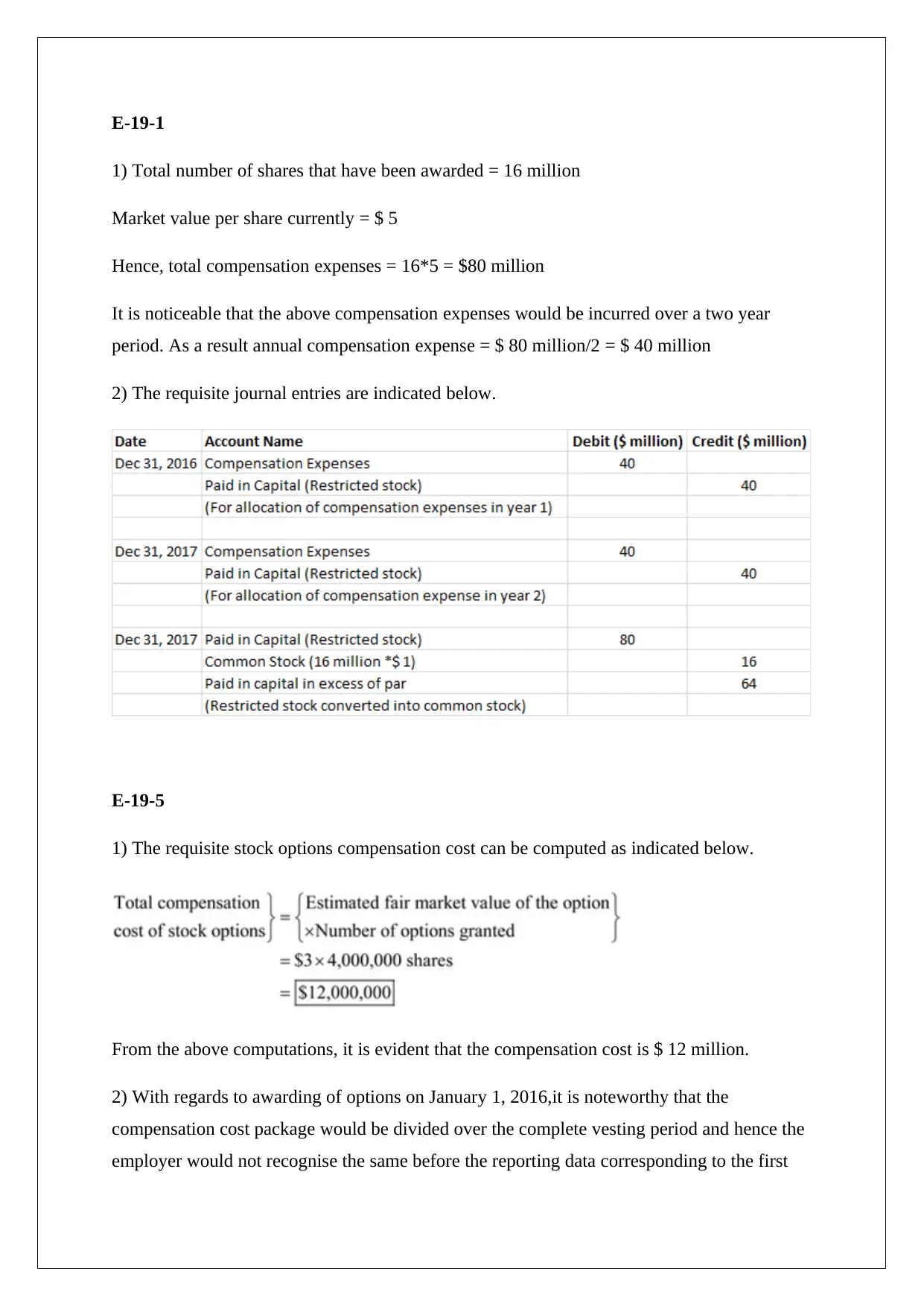

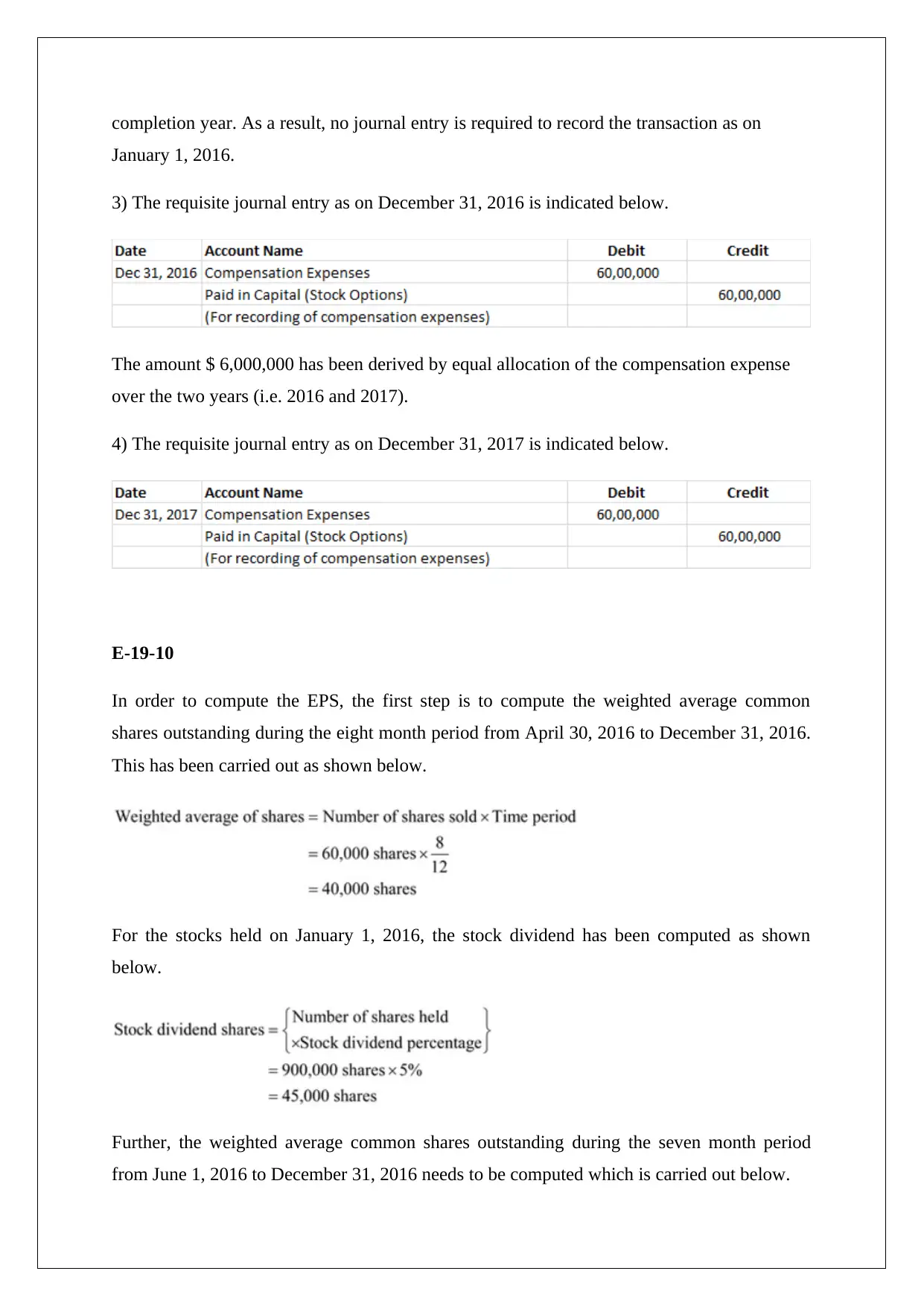

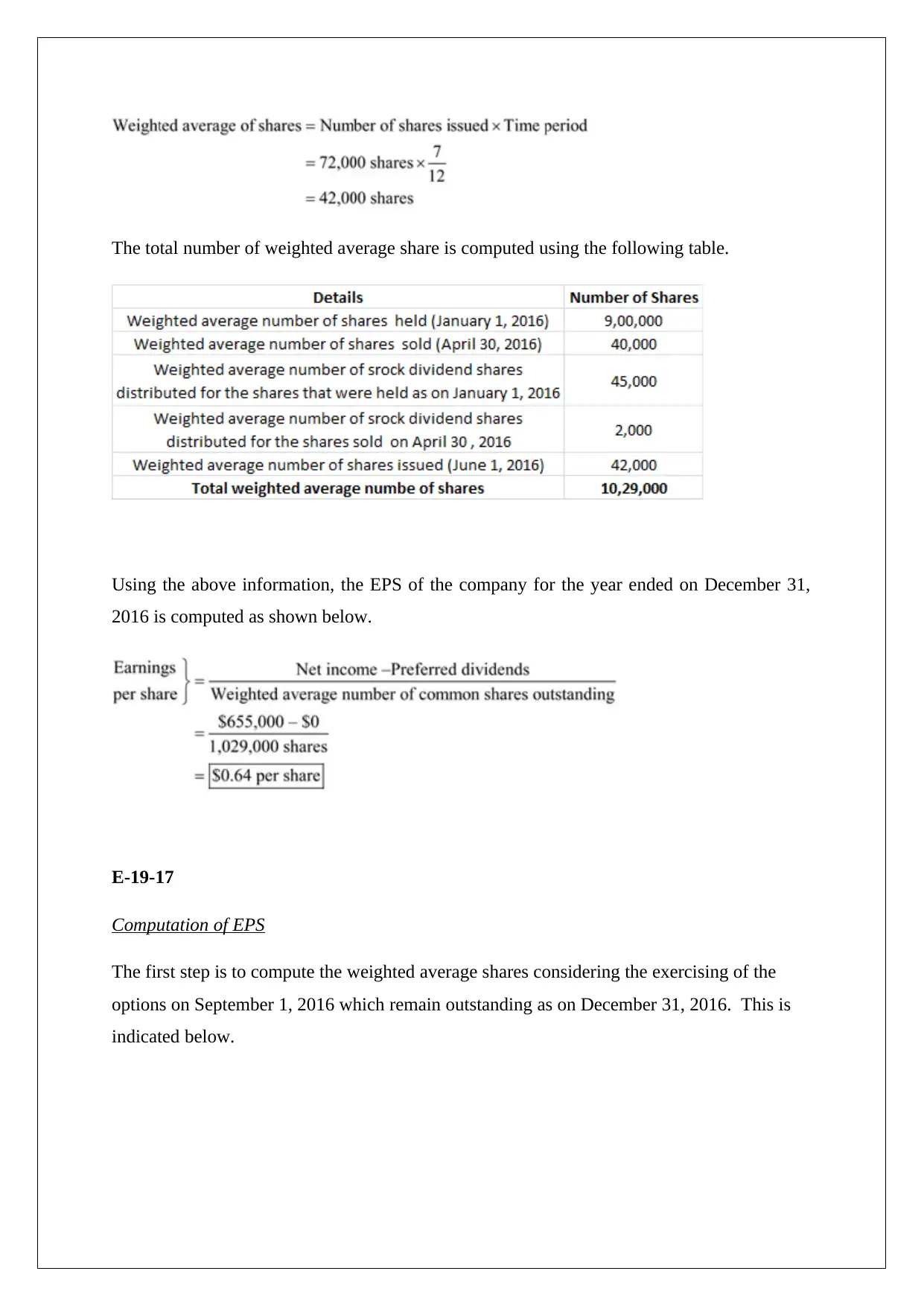

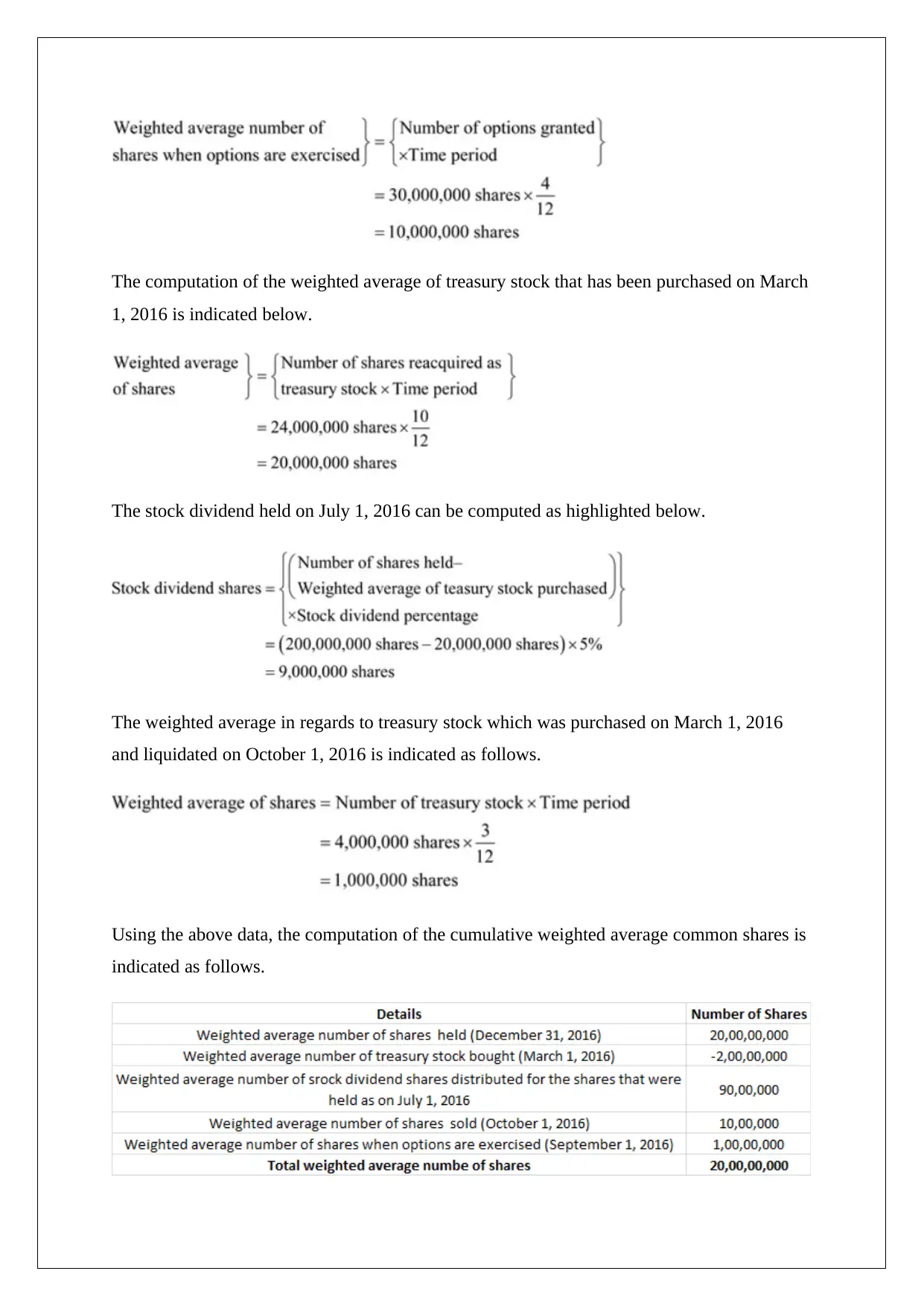

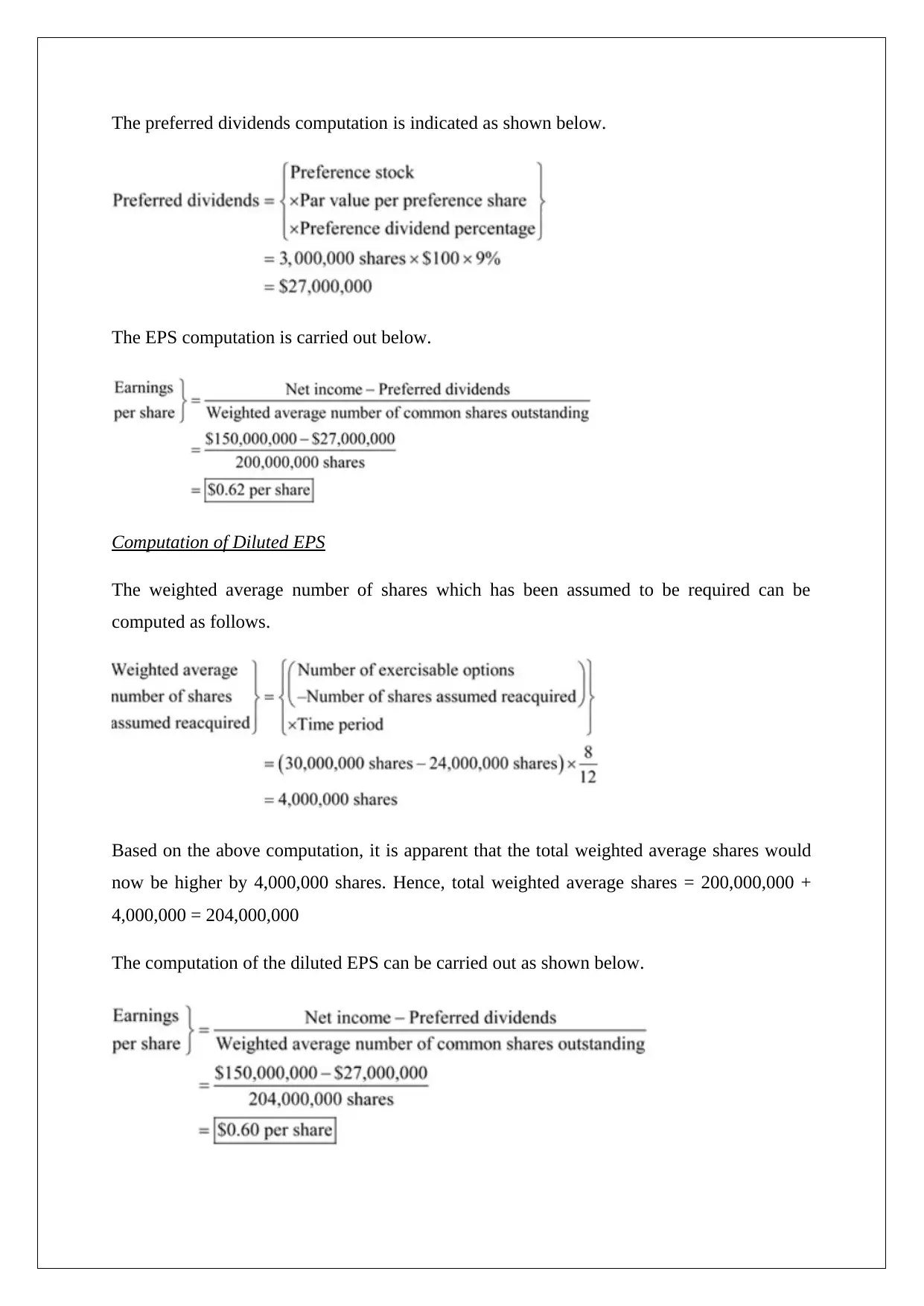

This assignment provides solutions to accounting exercises focusing on stock options, restricted stock awards, and earnings per share (EPS) calculations. It includes journal entries for recording compensation expenses related to restricted stock and stock options, as well as detailed computations for basic and diluted EPS. The exercises cover topics such as determining total compensation cost, allocating compensation expenses over the vesting period, calculating weighted average common shares outstanding, and accounting for stock dividends and treasury stock transactions. The solutions demonstrate the application of accounting principles in share-based compensation and EPS reporting, offering students a comprehensive guide to these complex areas. Desklib provides access to more solved assignments and past papers for students.

1 out of 6

Related Documents

![Financial Statement Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fsl%2F5d5358bf8f1949d98483d05ce8d0e6de.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.