Accounting and Finance: Investment Analysis, Tax Policy & Returns

VerifiedAdded on 2023/06/14

|13

|2725

|190

Homework Assignment

AI Summary

This assignment delves into various aspects of accounting and finance, beginning with calculating the present value of an investment opportunity and determining the quarterly payments for a loan. It further explores the potential impacts of the Australian federal government's decision to reduce the corporate tax rate from 30% to 25%, discussing both the advantages, such as attracting foreign investment and increasing savings, and the disadvantages, including potential negative impacts on national income. Additionally, the assignment involves a portfolio analysis using Capital Asset Pricing Model (CAPM) and Security Market Line (SML) with shares of BHP Billiton and NAB, comparing their average monthly returns, variation, and recommending BHP Billiton as the preferred investment choice based on higher average monthly returns. The analysis includes calculations of monthly returns, annual holding period returns, standard deviation, beta, expected return, and portfolio return and beta, providing a comprehensive overview of investment and tax-related financial concepts.

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the Student:

Name of the University:

Author Note:

Accounting and finance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................2

Part c:.....................................................................................................................................3

Answer to Question 2:................................................................................................................3

Part i:......................................................................................................................................3

Part ii:.....................................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to Question 4:................................................................................................................7

Part i:......................................................................................................................................7

Part ii:.....................................................................................................................................7

Part iii:....................................................................................................................................8

Part iv:....................................................................................................................................8

Part v:.....................................................................................................................................9

Part vi:....................................................................................................................................9

Part vii:...................................................................................................................................9

Part viii:................................................................................................................................10

Part ix:..................................................................................................................................10

References................................................................................................................................12

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................2

Part c:.....................................................................................................................................3

Answer to Question 2:................................................................................................................3

Part i:......................................................................................................................................3

Part ii:.....................................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to Question 4:................................................................................................................7

Part i:......................................................................................................................................7

Part ii:.....................................................................................................................................7

Part iii:....................................................................................................................................8

Part iv:....................................................................................................................................8

Part v:.....................................................................................................................................9

Part vi:....................................................................................................................................9

Part vii:...................................................................................................................................9

Part viii:................................................................................................................................10

Part ix:..................................................................................................................................10

References................................................................................................................................12

2

ACCOUNTING AND FINANCE

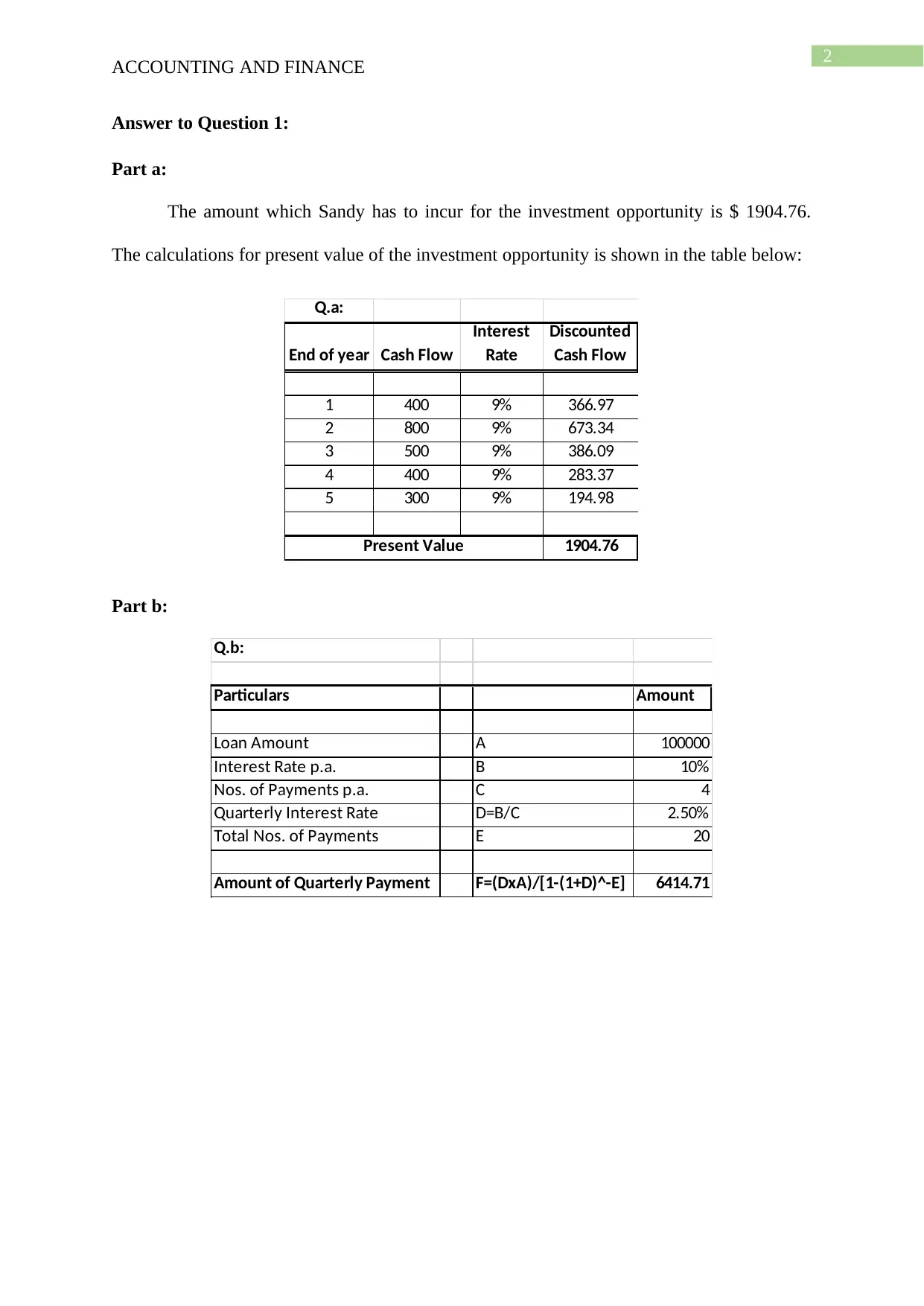

Answer to Question 1:

Part a:

The amount which Sandy has to incur for the investment opportunity is $ 1904.76.

The calculations for present value of the investment opportunity is shown in the table below:

Q.a:

End of year Cash Flow

Interest

Rate

Discounted

Cash Flow

1 400 9% 366.97

2 800 9% 673.34

3 500 9% 386.09

4 400 9% 283.37

5 300 9% 194.98

1904.76Present Value

Part b:

Q.b:

Particulars Amount

Loan Amount A 100000

Interest Rate p.a. B 10%

Nos. of Payments p.a. C 4

Quarterly Interest Rate D=B/C 2.50%

Total Nos. of Payments E 20

Amount of Quarterly Payment F=(DxA)/[1-(1+D)^-E] 6414.71

ACCOUNTING AND FINANCE

Answer to Question 1:

Part a:

The amount which Sandy has to incur for the investment opportunity is $ 1904.76.

The calculations for present value of the investment opportunity is shown in the table below:

Q.a:

End of year Cash Flow

Interest

Rate

Discounted

Cash Flow

1 400 9% 366.97

2 800 9% 673.34

3 500 9% 386.09

4 400 9% 283.37

5 300 9% 194.98

1904.76Present Value

Part b:

Q.b:

Particulars Amount

Loan Amount A 100000

Interest Rate p.a. B 10%

Nos. of Payments p.a. C 4

Quarterly Interest Rate D=B/C 2.50%

Total Nos. of Payments E 20

Amount of Quarterly Payment F=(DxA)/[1-(1+D)^-E] 6414.71

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE

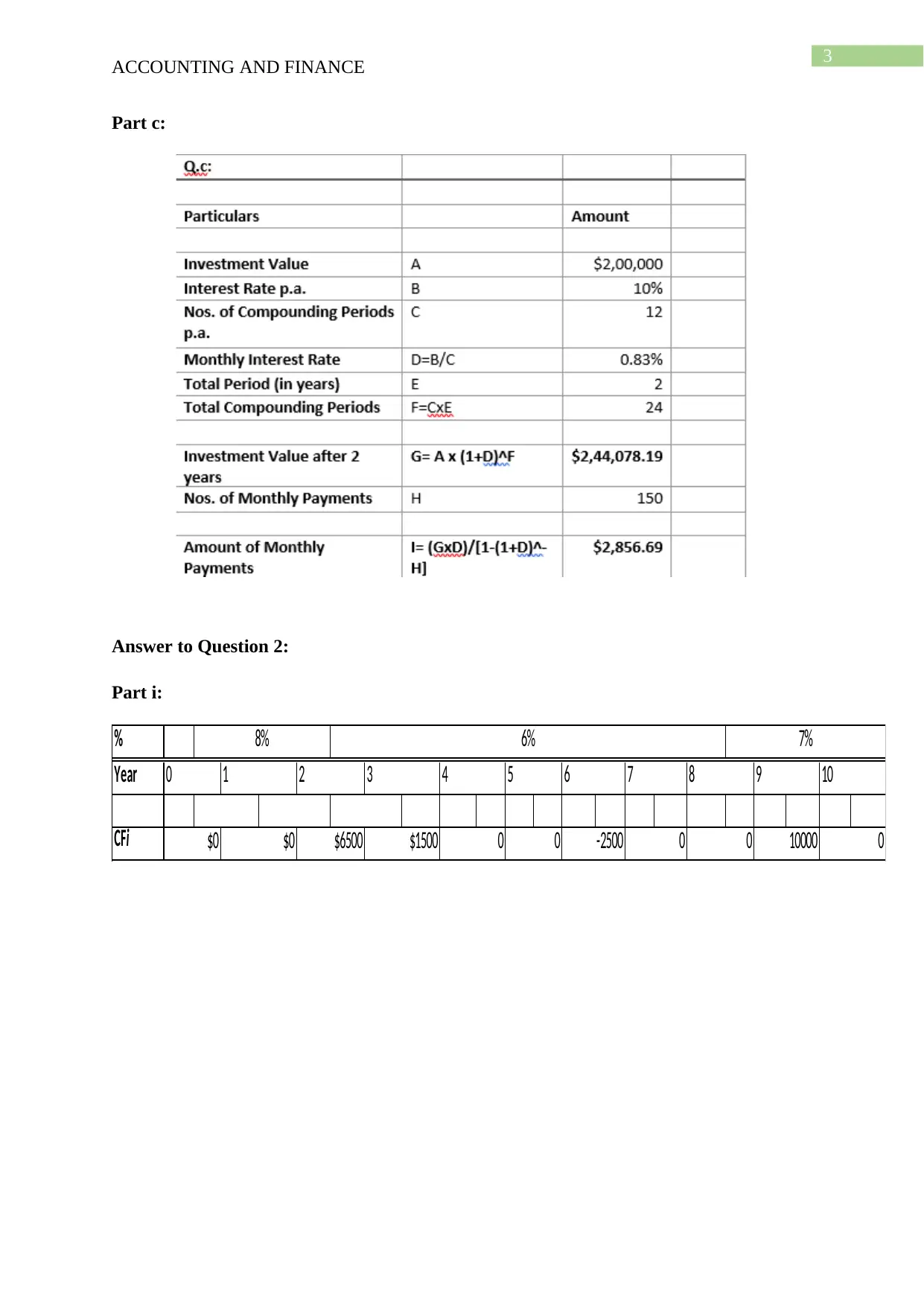

Part c:

Answer to Question 2:

Part i:

%

Year

CFi 10000 0

6% 7%

6 7 8 9 10

0 0 -2500 0 0

5

8%

3

$1500

4

$0

0

$0

1 2

$6500

ACCOUNTING AND FINANCE

Part c:

Answer to Question 2:

Part i:

%

Year

CFi 10000 0

6% 7%

6 7 8 9 10

0 0 -2500 0 0

5

8%

3

$1500

4

$0

0

$0

1 2

$6500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE

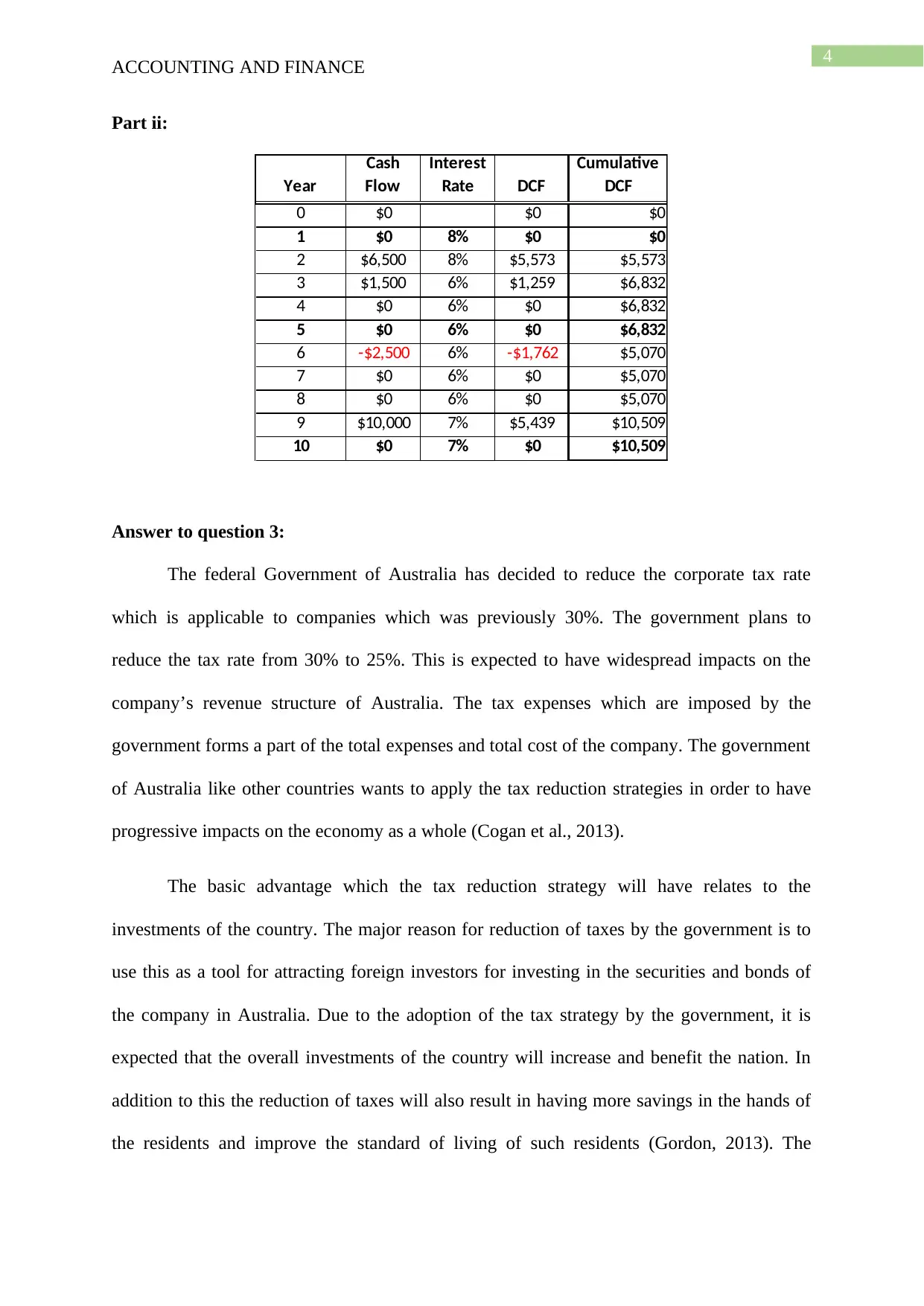

Part ii:

Year

Cash

Flow

Interest

Rate DCF

Cumulative

DCF

0 $0 $0 $0

1 $0 8% $0 $0

2 $6,500 8% $5,573 $5,573

3 $1,500 6% $1,259 $6,832

4 $0 6% $0 $6,832

5 $0 6% $0 $6,832

6 -$2,500 6% -$1,762 $5,070

7 $0 6% $0 $5,070

8 $0 6% $0 $5,070

9 $10,000 7% $5,439 $10,509

10 $0 7% $0 $10,509

Answer to question 3:

The federal Government of Australia has decided to reduce the corporate tax rate

which is applicable to companies which was previously 30%. The government plans to

reduce the tax rate from 30% to 25%. This is expected to have widespread impacts on the

company’s revenue structure of Australia. The tax expenses which are imposed by the

government forms a part of the total expenses and total cost of the company. The government

of Australia like other countries wants to apply the tax reduction strategies in order to have

progressive impacts on the economy as a whole (Cogan et al., 2013).

The basic advantage which the tax reduction strategy will have relates to the

investments of the country. The major reason for reduction of taxes by the government is to

use this as a tool for attracting foreign investors for investing in the securities and bonds of

the company in Australia. Due to the adoption of the tax strategy by the government, it is

expected that the overall investments of the country will increase and benefit the nation. In

addition to this the reduction of taxes will also result in having more savings in the hands of

the residents and improve the standard of living of such residents (Gordon, 2013). The

ACCOUNTING AND FINANCE

Part ii:

Year

Cash

Flow

Interest

Rate DCF

Cumulative

DCF

0 $0 $0 $0

1 $0 8% $0 $0

2 $6,500 8% $5,573 $5,573

3 $1,500 6% $1,259 $6,832

4 $0 6% $0 $6,832

5 $0 6% $0 $6,832

6 -$2,500 6% -$1,762 $5,070

7 $0 6% $0 $5,070

8 $0 6% $0 $5,070

9 $10,000 7% $5,439 $10,509

10 $0 7% $0 $10,509

Answer to question 3:

The federal Government of Australia has decided to reduce the corporate tax rate

which is applicable to companies which was previously 30%. The government plans to

reduce the tax rate from 30% to 25%. This is expected to have widespread impacts on the

company’s revenue structure of Australia. The tax expenses which are imposed by the

government forms a part of the total expenses and total cost of the company. The government

of Australia like other countries wants to apply the tax reduction strategies in order to have

progressive impacts on the economy as a whole (Cogan et al., 2013).

The basic advantage which the tax reduction strategy will have relates to the

investments of the country. The major reason for reduction of taxes by the government is to

use this as a tool for attracting foreign investors for investing in the securities and bonds of

the company in Australia. Due to the adoption of the tax strategy by the government, it is

expected that the overall investments of the country will increase and benefit the nation. In

addition to this the reduction of taxes will also result in having more savings in the hands of

the residents and improve the standard of living of such residents (Gordon, 2013). The

5

ACCOUNTING AND FINANCE

savings which is generated due to the reduction in tax rate will result in individuals having

additional money in their hands which can be used by the individual for savings, further

investments or for consumption and thus the overall standard of living of the residents will

definitely (Diener, Tay & Oishi, 2013). In the case of companies, the reduced tax imposed on

them will result in the companies having more amount of profits for the companies which can

be used by the companies for investments in securities of other companies, kept as a reserve

or retained profits. Moreover, the company has the option to distribute such profits among the

share holders of the company. Thus, it can lead to growth of the companies and also the

overall development of the economy as a whole. In addition to this, the it will provide an

impetus to the companies that the government is providing them with an opportunity to earn

more profits and grow. In such a situation the companies will make use of all the efforts that

can lead to growth and development of the company and also the development of the

economy. The reduction in the tax expenses of the company also implies that the total costs

which is incurred by the companies will also reduce and thereby the company will also

reduce the cost of the products which it manufactures (Erceg & Lindé, 2013). Thus, it can be

seen that the reduction of the tax rate by the government will have an advantageous chain

effect on every resident of the country. Then there is the basic advantage where the overall

foreign investments of the country increase and there is massive inflow of cash in the

economy which can be used for the development of the country as a whole.

The problems which are associated with the reduction of tax strategies which the

government wants to apply is that it can have negative impacts on the national income of the

country. The income which the country receives from the taxes which are collected forms a

major part of the revenue of the government which is included in the computation of the

national income of the country (Milanovic, 2013). If there is a reduction of taxes then it will

be impacting the national income by lowering it. This may or may not be a problem as the

ACCOUNTING AND FINANCE

savings which is generated due to the reduction in tax rate will result in individuals having

additional money in their hands which can be used by the individual for savings, further

investments or for consumption and thus the overall standard of living of the residents will

definitely (Diener, Tay & Oishi, 2013). In the case of companies, the reduced tax imposed on

them will result in the companies having more amount of profits for the companies which can

be used by the companies for investments in securities of other companies, kept as a reserve

or retained profits. Moreover, the company has the option to distribute such profits among the

share holders of the company. Thus, it can lead to growth of the companies and also the

overall development of the economy as a whole. In addition to this, the it will provide an

impetus to the companies that the government is providing them with an opportunity to earn

more profits and grow. In such a situation the companies will make use of all the efforts that

can lead to growth and development of the company and also the development of the

economy. The reduction in the tax expenses of the company also implies that the total costs

which is incurred by the companies will also reduce and thereby the company will also

reduce the cost of the products which it manufactures (Erceg & Lindé, 2013). Thus, it can be

seen that the reduction of the tax rate by the government will have an advantageous chain

effect on every resident of the country. Then there is the basic advantage where the overall

foreign investments of the country increase and there is massive inflow of cash in the

economy which can be used for the development of the country as a whole.

The problems which are associated with the reduction of tax strategies which the

government wants to apply is that it can have negative impacts on the national income of the

country. The income which the country receives from the taxes which are collected forms a

major part of the revenue of the government which is included in the computation of the

national income of the country (Milanovic, 2013). If there is a reduction of taxes then it will

be impacting the national income by lowering it. This may or may not be a problem as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING AND FINANCE

government expects that the foreign investments which will be taking place due to reduction

in tax rate will cover up for the revenue lost due to reduction in the taxes of the country.

Another problem is that with the reduction of the tax rate of the country, the message send to

the rest of the world will not be appropriate. The reduction of taxes will make the Australian

economy look less competing in nature and might discourage potential investors from abroad

from making investments in the securities of Australian companies. The reduction in the tax

policy of the country might affect the competitiveness of the market in the eyes of foreign

investors and make the market look unattractive in nature. Then there are the low lending

costs which are associated with the investments in business.

The government of Australia also follows the policy of franking of credits which are

beneficial to the lower income group residents of the country. The policy of tax reduction will

have positive impacts on them as well which relates to savings and consumption expenses

incurred by them. Thus, from the above analysis and discussion it is clear that with the

reduction of the tax strategies, not only the companies but also the general residents of the

company as well will benefit. Though there are certain disadvantages which are associated

with the tax rate deduction strategy of the government, however, the benefits which are

related to the same is far more than the disadvantages and can make wide spread

development in the country which is not just in the foreign investments but also improved

standard of living for the residents of the country.

ACCOUNTING AND FINANCE

government expects that the foreign investments which will be taking place due to reduction

in tax rate will cover up for the revenue lost due to reduction in the taxes of the country.

Another problem is that with the reduction of the tax rate of the country, the message send to

the rest of the world will not be appropriate. The reduction of taxes will make the Australian

economy look less competing in nature and might discourage potential investors from abroad

from making investments in the securities of Australian companies. The reduction in the tax

policy of the country might affect the competitiveness of the market in the eyes of foreign

investors and make the market look unattractive in nature. Then there are the low lending

costs which are associated with the investments in business.

The government of Australia also follows the policy of franking of credits which are

beneficial to the lower income group residents of the country. The policy of tax reduction will

have positive impacts on them as well which relates to savings and consumption expenses

incurred by them. Thus, from the above analysis and discussion it is clear that with the

reduction of the tax strategies, not only the companies but also the general residents of the

company as well will benefit. Though there are certain disadvantages which are associated

with the tax rate deduction strategy of the government, however, the benefits which are

related to the same is far more than the disadvantages and can make wide spread

development in the country which is not just in the foreign investments but also improved

standard of living for the residents of the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

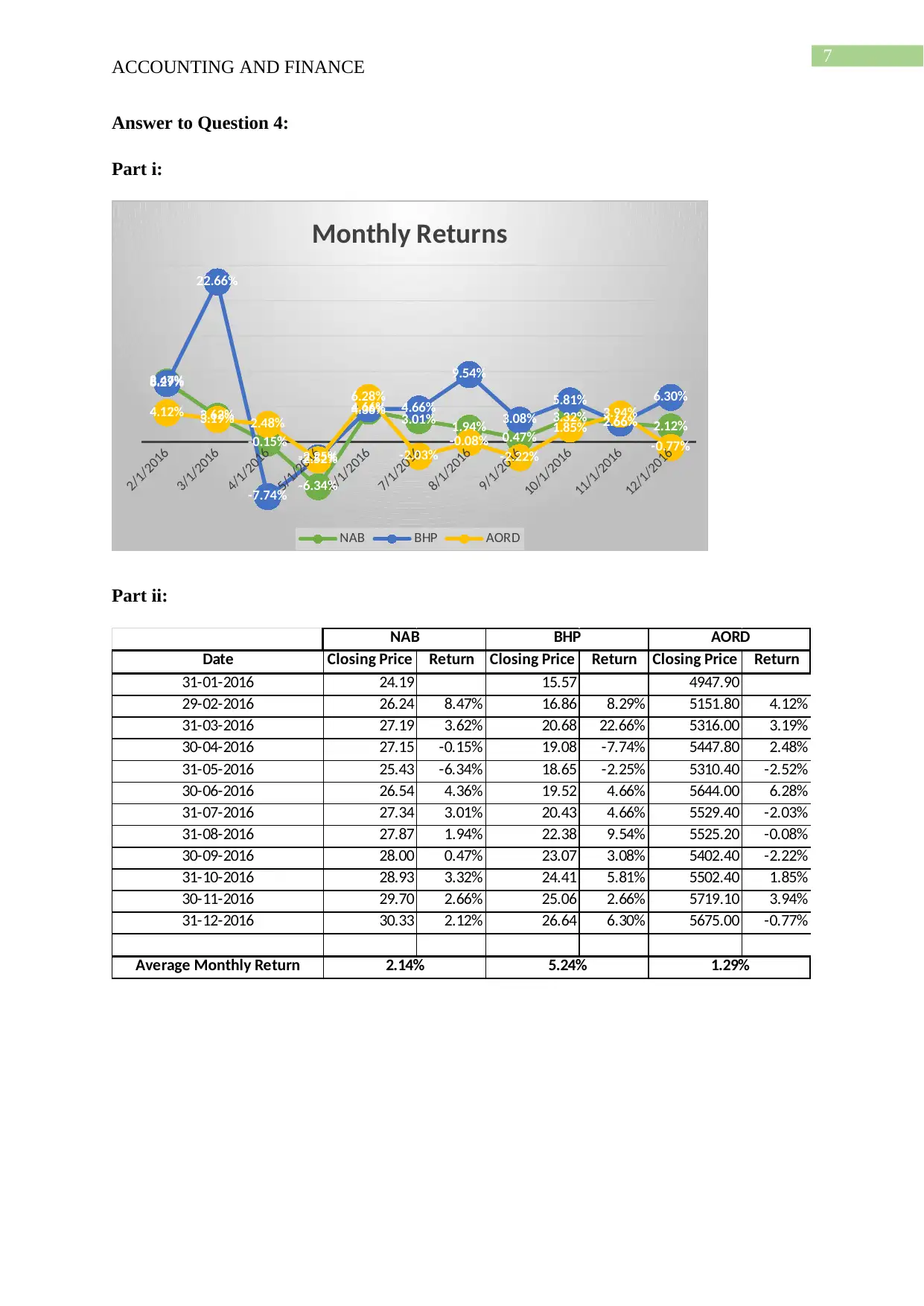

Answer to Question 4:

Part i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

8.47%

3.62%

-0.15%

-6.34%

4.36% 3.01% 1.94% 0.47%

3.32% 2.66% 2.12%

8.29%

22.66%

-7.74%

-2.25%

4.66% 4.66%

9.54%

3.08%

5.81%

2.66%

6.30%

4.12% 3.19% 2.48%

-2.52%

6.28%

-2.03% -0.08%

-2.22%

1.85%

3.94%

-0.77%

Monthly Returns

NAB BHP AORD

Part ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

ACCOUNTING AND FINANCE

Answer to Question 4:

Part i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

8.47%

3.62%

-0.15%

-6.34%

4.36% 3.01% 1.94% 0.47%

3.32% 2.66% 2.12%

8.29%

22.66%

-7.74%

-2.25%

4.66% 4.66%

9.54%

3.08%

5.81%

2.66%

6.30%

4.12% 3.19% 2.48%

-2.52%

6.28%

-2.03% -0.08%

-2.22%

1.85%

3.94%

-0.77%

Monthly Returns

NAB BHP AORD

Part ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

8

ACCOUNTING AND FINANCE

Part iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Part iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

ACCOUNTING AND FINANCE

Part iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Part iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING AND FINANCE

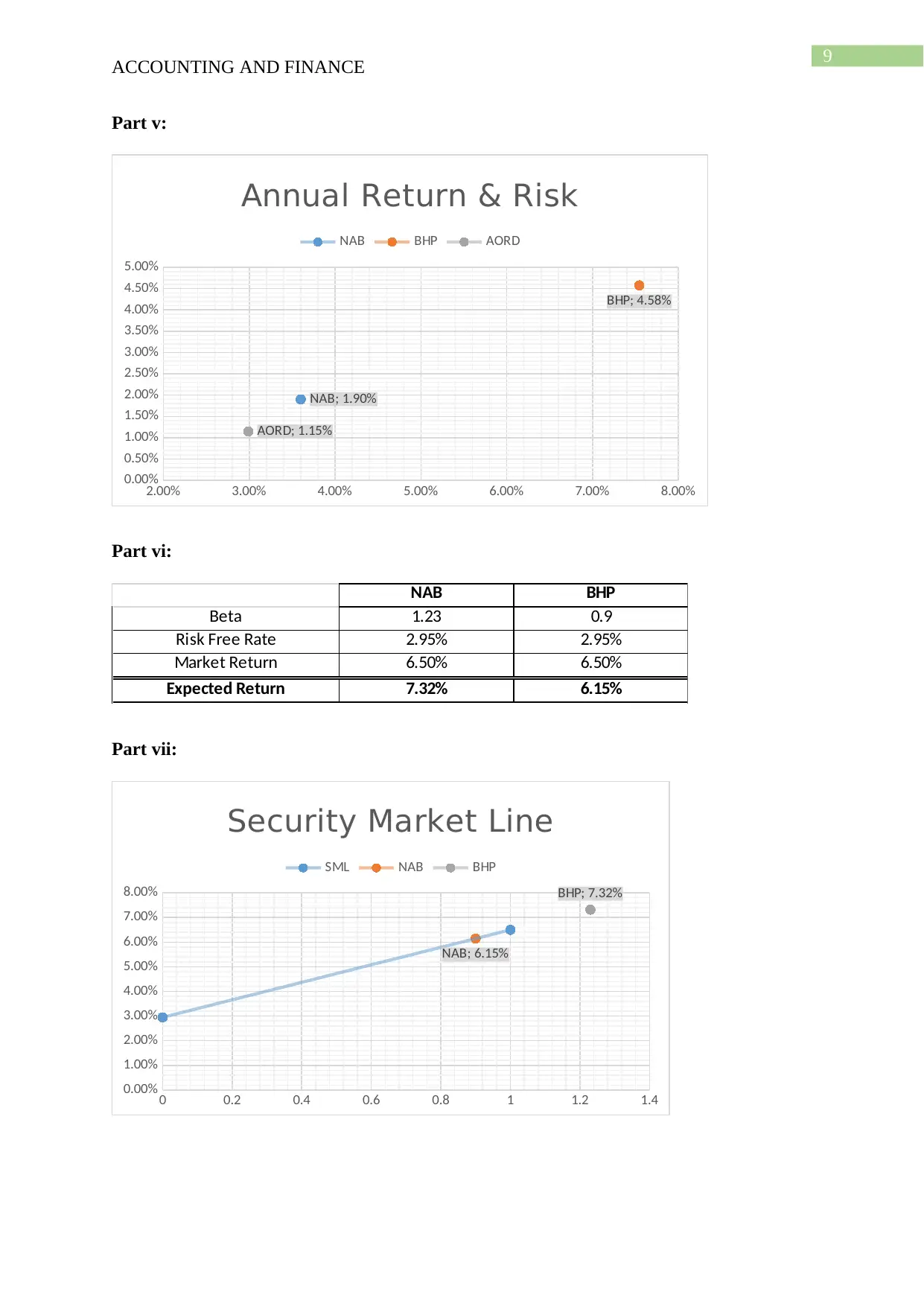

Part v:

2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

AORD; 1.15%

BHP; 4.58%

NAB; 1.90%

Annual Return & Risk

NAB BHP AORD

Part vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Part vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00% BHP; 7.32%

NAB; 6.15%

Security Market Line

SML NAB BHP

ACCOUNTING AND FINANCE

Part v:

2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

AORD; 1.15%

BHP; 4.58%

NAB; 1.90%

Annual Return & Risk

NAB BHP AORD

Part vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Part vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00% BHP; 7.32%

NAB; 6.15%

Security Market Line

SML NAB BHP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING AND FINANCE

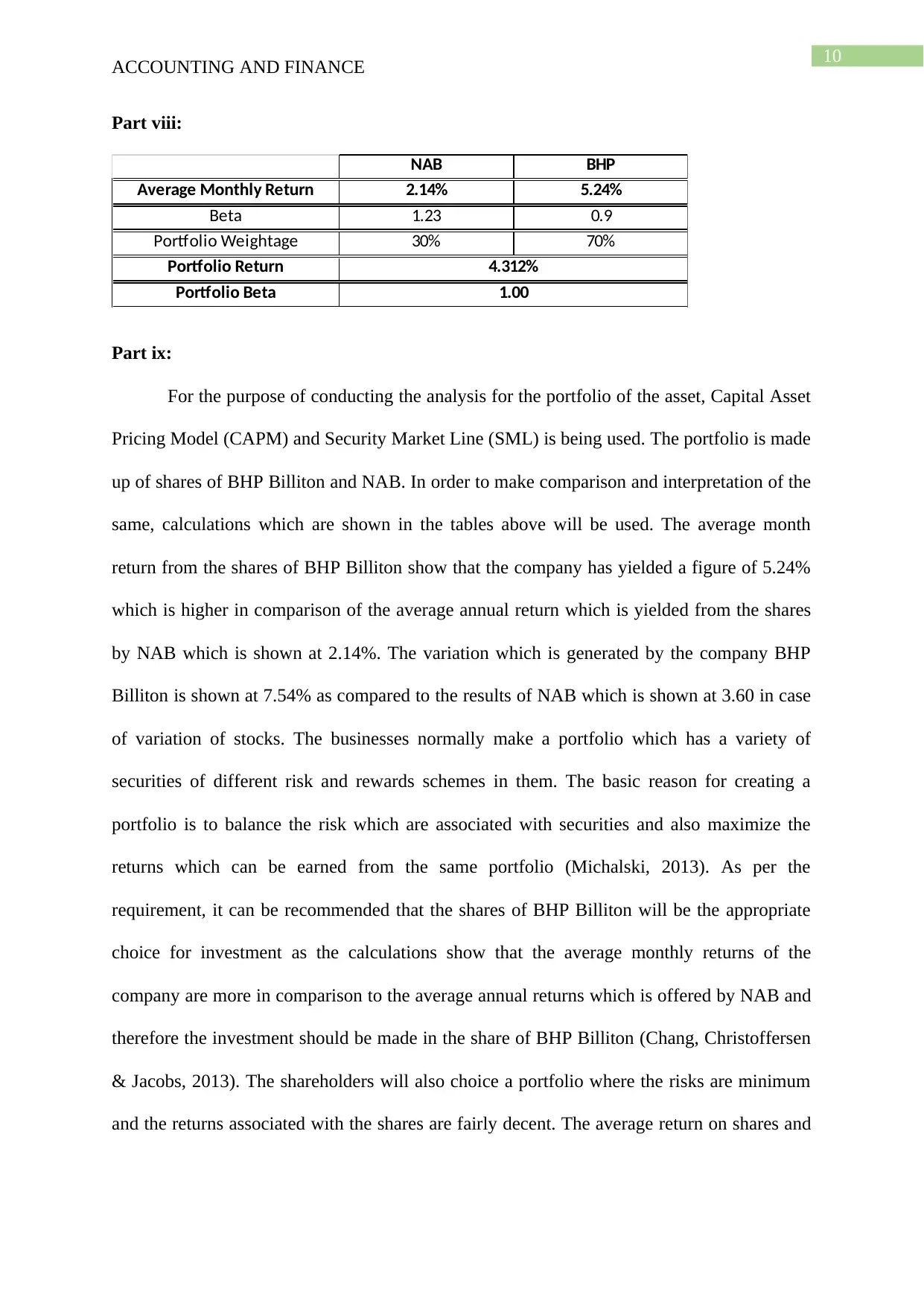

Part viii:

Average Monthly Return

Beta

Portfolio Weightage

Portfolio Return

Portfolio Beta

NAB BHP

4.312%

1.00

2.14%

1.23

70%30%

5.24%

0.9

Part ix:

For the purpose of conducting the analysis for the portfolio of the asset, Capital Asset

Pricing Model (CAPM) and Security Market Line (SML) is being used. The portfolio is made

up of shares of BHP Billiton and NAB. In order to make comparison and interpretation of the

same, calculations which are shown in the tables above will be used. The average month

return from the shares of BHP Billiton show that the company has yielded a figure of 5.24%

which is higher in comparison of the average annual return which is yielded from the shares

by NAB which is shown at 2.14%. The variation which is generated by the company BHP

Billiton is shown at 7.54% as compared to the results of NAB which is shown at 3.60 in case

of variation of stocks. The businesses normally make a portfolio which has a variety of

securities of different risk and rewards schemes in them. The basic reason for creating a

portfolio is to balance the risk which are associated with securities and also maximize the

returns which can be earned from the same portfolio (Michalski, 2013). As per the

requirement, it can be recommended that the shares of BHP Billiton will be the appropriate

choice for investment as the calculations show that the average monthly returns of the

company are more in comparison to the average annual returns which is offered by NAB and

therefore the investment should be made in the share of BHP Billiton (Chang, Christoffersen

& Jacobs, 2013). The shareholders will also choice a portfolio where the risks are minimum

and the returns associated with the shares are fairly decent. The average return on shares and

ACCOUNTING AND FINANCE

Part viii:

Average Monthly Return

Beta

Portfolio Weightage

Portfolio Return

Portfolio Beta

NAB BHP

4.312%

1.00

2.14%

1.23

70%30%

5.24%

0.9

Part ix:

For the purpose of conducting the analysis for the portfolio of the asset, Capital Asset

Pricing Model (CAPM) and Security Market Line (SML) is being used. The portfolio is made

up of shares of BHP Billiton and NAB. In order to make comparison and interpretation of the

same, calculations which are shown in the tables above will be used. The average month

return from the shares of BHP Billiton show that the company has yielded a figure of 5.24%

which is higher in comparison of the average annual return which is yielded from the shares

by NAB which is shown at 2.14%. The variation which is generated by the company BHP

Billiton is shown at 7.54% as compared to the results of NAB which is shown at 3.60 in case

of variation of stocks. The businesses normally make a portfolio which has a variety of

securities of different risk and rewards schemes in them. The basic reason for creating a

portfolio is to balance the risk which are associated with securities and also maximize the

returns which can be earned from the same portfolio (Michalski, 2013). As per the

requirement, it can be recommended that the shares of BHP Billiton will be the appropriate

choice for investment as the calculations show that the average monthly returns of the

company are more in comparison to the average annual returns which is offered by NAB and

therefore the investment should be made in the share of BHP Billiton (Chang, Christoffersen

& Jacobs, 2013). The shareholders will also choice a portfolio where the risks are minimum

and the returns associated with the shares are fairly decent. The average return on shares and

11

ACCOUNTING AND FINANCE

the risks which are associated with the shares are the basis on which various investing

decisions of the shareholders are taken (Hirshleifer, Hsu & Li, 2013).

ACCOUNTING AND FINANCE

the risks which are associated with the shares are the basis on which various investing

decisions of the shareholders are taken (Hirshleifer, Hsu & Li, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.