Capital Budgeting Methods and Practices

VerifiedAdded on 2020/04/07

|11

|1707

|37

AI Summary

This assignment delves into the world of capital budgeting, examining the methods and practices employed by companies to evaluate and select investment projects. It encourages a critical analysis of research papers exploring factors influencing capital budgeting decisions, including hurdle rates and risk adjustment techniques. The assignment aims to provide a comprehensive understanding of how companies approach long-term investment planning.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING & FINANCE

Accounting & Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting & Finance

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING & FINANCE

Table of Contents

Answer to Part A:............................................................................................................................2

Requirement 1:.............................................................................................................................2

Requirement 2:.............................................................................................................................4

Requirement 3:.............................................................................................................................4

Answer to PART B:.........................................................................................................................5

Introduction:................................................................................................................................5

Analysis of APN’s capital structure:...........................................................................................5

Computation of After-Tax WACC:.............................................................................................6

Analysis of financial ratio of APN:.............................................................................................6

APN outdoor group and its competitor performance:.................................................................6

Capital structure of APN Outdoor group:....................................................................................7

Conclusion:..................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Answer to Part A:............................................................................................................................2

Requirement 1:.............................................................................................................................2

Requirement 2:.............................................................................................................................4

Requirement 3:.............................................................................................................................4

Answer to PART B:.........................................................................................................................5

Introduction:................................................................................................................................5

Analysis of APN’s capital structure:...........................................................................................5

Computation of After-Tax WACC:.............................................................................................6

Analysis of financial ratio of APN:.............................................................................................6

APN outdoor group and its competitor performance:.................................................................6

Capital structure of APN Outdoor group:....................................................................................7

Conclusion:..................................................................................................................................8

References........................................................................................................................................9

2ACCOUNTING & FINANCE

Answer to Part A:

Requirement 1:

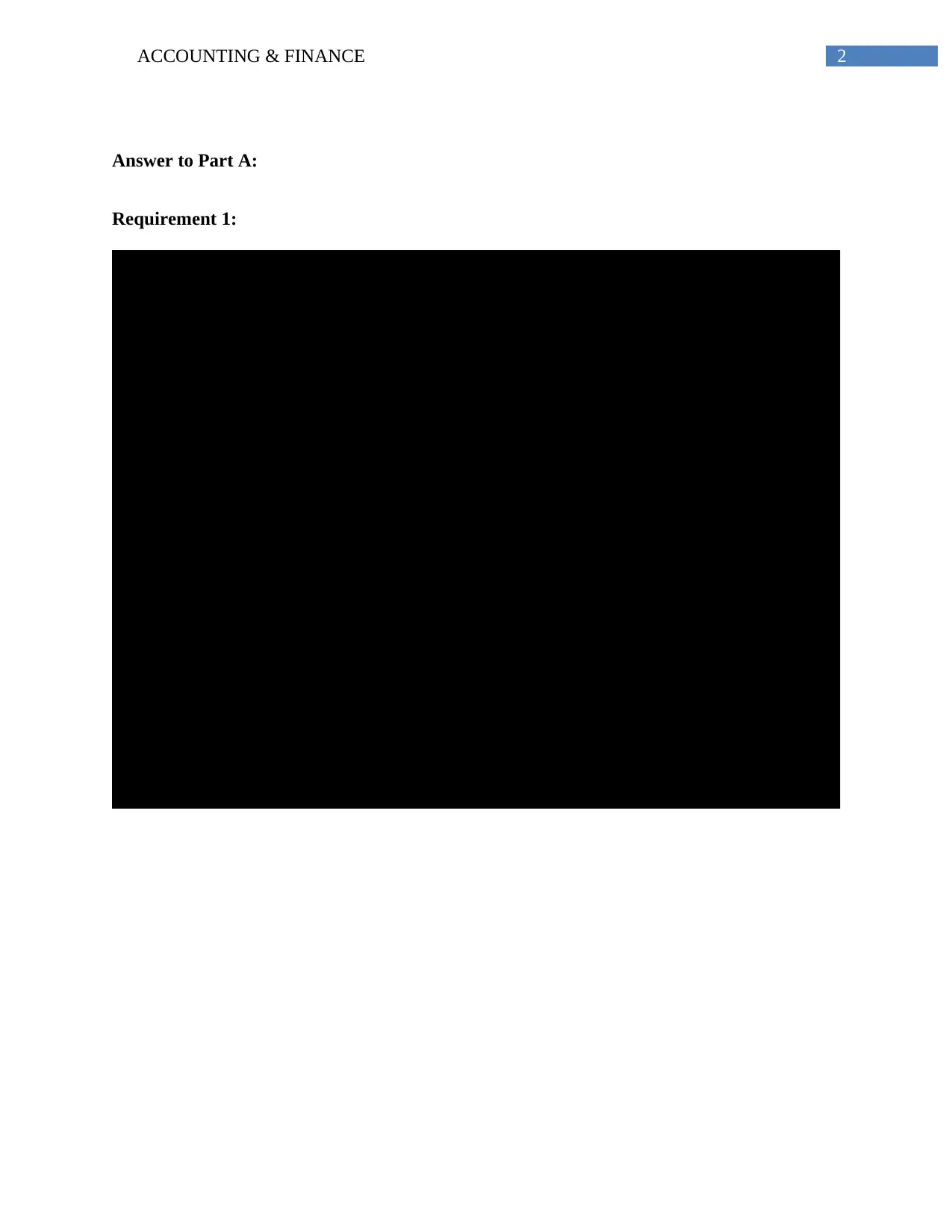

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

Answer to Part A:

Requirement 1:

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

3ACCOUNTING & FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING & FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

Requirement 2:

The decisions associated to the capital budgeting has been seen to include several

projections for the given scenario. The evaluations depicted above have been seen to be related

to the estimation of the various types of the free cash flow for the project. The application of the

other techniques has been evident with the inclusions of payback period and ARR which may

used to determine the risk in the project (Hall & Westerman, 2013).

Requirement 3:

The calculations projected above have been able to consider the various considerations

for the positive NPV and PI of 191.89%. The positive NPV has been further indicated with the

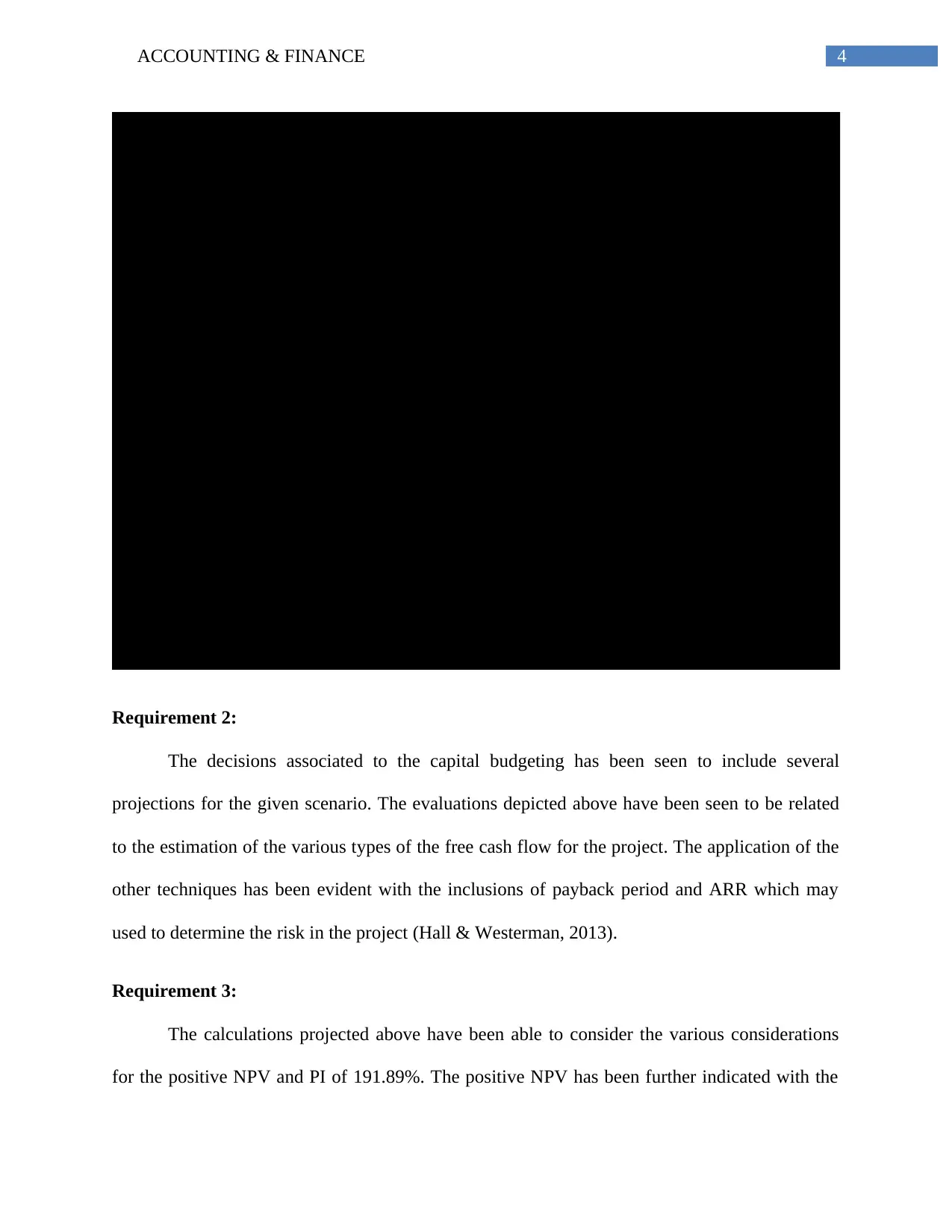

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

Requirement 2:

The decisions associated to the capital budgeting has been seen to include several

projections for the given scenario. The evaluations depicted above have been seen to be related

to the estimation of the various types of the free cash flow for the project. The application of the

other techniques has been evident with the inclusions of payback period and ARR which may

used to determine the risk in the project (Hall & Westerman, 2013).

Requirement 3:

The calculations projected above have been able to consider the various considerations

for the positive NPV and PI of 191.89%. The positive NPV has been further indicated with the

5ACCOUNTING & FINANCE

project viable to be undertaken based on the considered investments. The Cost benefit ratio has

been discerned with the PI value of 191.89%, which has been recognized with future cash flow,

which is seen to be more than the initial investment amount considered by an organization. The

decision for the rejection and the acceptance has been observed with the consideration of Capital

budgeting technique like ARR and payback period (Batra & Verma, 2017).

Answer to PART B:

Introduction:

The preparation of the report has been seen with the APN outdoor capital structure which

has been seen to be duly listed in the ASX. The main consideration of the report has been further

seen to include the calculation based on the WACC and determination of the important financial

ratios for the organization.

Analysis of APN’s capital structure:

The WACC for APO has been calculated with an amount of 8.32%. The extra amount

has been discerned with $181.8 equity which has been considered with rising by APN in year

2016 for capital structure establishment. The Group has been further seen to intend the reduction

in cost of capital by maintaining a minimum amount of the capital structure. The total cost of

capital for APN can be further reduced by the increased proportion of the debt value. Based on

the annual report evaluation in the year 2016, the debt proportion in the capital structure has

decreased (Daunfeldt & Hartwig, 2014). The main rationale for this has been seen with the total

equity which has increased and the different types of the interest bearing liabilities has been seen

to be decreasing in nature. The total value of equity has increased considerably from $ 461525 in

project viable to be undertaken based on the considered investments. The Cost benefit ratio has

been discerned with the PI value of 191.89%, which has been recognized with future cash flow,

which is seen to be more than the initial investment amount considered by an organization. The

decision for the rejection and the acceptance has been observed with the consideration of Capital

budgeting technique like ARR and payback period (Batra & Verma, 2017).

Answer to PART B:

Introduction:

The preparation of the report has been seen with the APN outdoor capital structure which

has been seen to be duly listed in the ASX. The main consideration of the report has been further

seen to include the calculation based on the WACC and determination of the important financial

ratios for the organization.

Analysis of APN’s capital structure:

The WACC for APO has been calculated with an amount of 8.32%. The extra amount

has been discerned with $181.8 equity which has been considered with rising by APN in year

2016 for capital structure establishment. The Group has been further seen to intend the reduction

in cost of capital by maintaining a minimum amount of the capital structure. The total cost of

capital for APN can be further reduced by the increased proportion of the debt value. Based on

the annual report evaluation in the year 2016, the debt proportion in the capital structure has

decreased (Daunfeldt & Hartwig, 2014). The main rationale for this has been seen with the total

equity which has increased and the different types of the interest bearing liabilities has been seen

to be decreasing in nature. The total value of equity has increased considerably from $ 461525 in

6ACCOUNTING & FINANCE

year 2015 to $ 836465 in the same FY. The D/E has been discerned as 38.1 in the year 2016 and

total debt of 27.61 (Nurullah & Kengatharan, 2015).

Computation of After-Tax WACC:

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Analysis of financial ratio of APN:

The net operating cash flow for the entity has been decreased in the previous three years.

In the three years, the total amount of the earnings for the group has been identified as 19% less

than the target. This has been the case mainly for the strategic initiatives in the present year

which has been computed as 0.29. The decrease in the earnings per share has been evaluated as

44.4 in year 2015 to 31.4 in year 2016. The total P/E in 2017 has been observed as 16.92

(Durnev, Morck, & Yeung, 2004).

The liquidity positioning of the company has been discerned based on the cash ratio,

quick ratio and current ratio. The total amount of cash ratio for the company is 0.38 and current

ratio of 1.90 with 1.89 as the quick ratio. The total amount of interest coverage ratio is 25.96 and

the D/A for the same is 0.23 (Dellavigna & Pollet, 2013).

year 2015 to $ 836465 in the same FY. The D/E has been discerned as 38.1 in the year 2016 and

total debt of 27.61 (Nurullah & Kengatharan, 2015).

Computation of After-Tax WACC:

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Analysis of financial ratio of APN:

The net operating cash flow for the entity has been decreased in the previous three years.

In the three years, the total amount of the earnings for the group has been identified as 19% less

than the target. This has been the case mainly for the strategic initiatives in the present year

which has been computed as 0.29. The decrease in the earnings per share has been evaluated as

44.4 in year 2015 to 31.4 in year 2016. The total P/E in 2017 has been observed as 16.92

(Durnev, Morck, & Yeung, 2004).

The liquidity positioning of the company has been discerned based on the cash ratio,

quick ratio and current ratio. The total amount of cash ratio for the company is 0.38 and current

ratio of 1.90 with 1.89 as the quick ratio. The total amount of interest coverage ratio is 25.96 and

the D/A for the same is 0.23 (Dellavigna & Pollet, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING & FINANCE

APN outdoor group and its competitor performance:

Ooh Media is identified as one of the main rival of APN Outdoor group. The capital

structure for the organization has been seen to compose of borrowings and equity. The total

value of the equity has increased with the borrowings. The capital structure for the APN outdoor

has been considered with the combination of both debt and equity in the capital structure of the

company. Despite of this, the dependency in the equity is seen to be more than the debt value

(Li, Peng, & Li, 2015). The capital structure for APN has transformed with time for a period of

more than three years, but this has not increased as per the equity financing. Henceforth, the

capital structure for the organization has been identified with the mix of components for

financing the assets which are seen as debt as well as the equity. APN outdoor has changed over

the year, which is not increasingly related to the borrowing for the equity finance. Henceforth, it

can be said that the capital structure for both Ooh Media and APN Outdoor group has the same

mix of financing assets which is composed of both debt and equity. APN outdoor has been able

to experience a stronger cash flow which has been able to assist in investment funding activity

and favorable return to the shareholder (Baker & English, 2013).

Capital structure of APN Outdoor group:

The capital structure for the organization has been considered to be based on the various

types of the depiction which has been based on the equity and debts as capital for earning as an

alternative for the total value made for the investments with the equivalent risk. WACC is

directly imposed with the financial decision and any change in the capital structure has been

directly influenced as per the WACC. With a higher WACC, there will be increased market

value for the organization and vice versa. The increased value of the market is seen to be

APN outdoor group and its competitor performance:

Ooh Media is identified as one of the main rival of APN Outdoor group. The capital

structure for the organization has been seen to compose of borrowings and equity. The total

value of the equity has increased with the borrowings. The capital structure for the APN outdoor

has been considered with the combination of both debt and equity in the capital structure of the

company. Despite of this, the dependency in the equity is seen to be more than the debt value

(Li, Peng, & Li, 2015). The capital structure for APN has transformed with time for a period of

more than three years, but this has not increased as per the equity financing. Henceforth, the

capital structure for the organization has been identified with the mix of components for

financing the assets which are seen as debt as well as the equity. APN outdoor has changed over

the year, which is not increasingly related to the borrowing for the equity finance. Henceforth, it

can be said that the capital structure for both Ooh Media and APN Outdoor group has the same

mix of financing assets which is composed of both debt and equity. APN outdoor has been able

to experience a stronger cash flow which has been able to assist in investment funding activity

and favorable return to the shareholder (Baker & English, 2013).

Capital structure of APN Outdoor group:

The capital structure for the organization has been considered to be based on the various

types of the depiction which has been based on the equity and debts as capital for earning as an

alternative for the total value made for the investments with the equivalent risk. WACC is

directly imposed with the financial decision and any change in the capital structure has been

directly influenced as per the WACC. With a higher WACC, there will be increased market

value for the organization and vice versa. The increased value of the market is seen to be

8ACCOUNTING & FINANCE

essential for the company to reduce the cost of capital (Brunzell, Liljeblom, & Vaihekoski,

2013).

The company has been able to decrease the cost of capital by increasing the funds based

on least costly source. The cost of capital may be reduced by the company through restructuring

of the capital which cannot exceed the rate of return. The lower amount for the cost of capital

will be able to fund new projects in a cheaper way. The reduction on the cost of capital can be

considered with formulation of new credit line and the common debt loan utilized for financing

the assets including the bank loan, card debt and bonds (Welch & Levi, 2013).

Conclusion:

The main analysis of the capital structure for APN comprise of equity and debentures. It

has been further seen that the company has been able to provide a satisfactory return for the

shareholders and the increased dividend for the shareholders. The earnings and the revenues

before taxed and interest has been seen with an upward trend in generating a satisfactory return

to the shareholders.

essential for the company to reduce the cost of capital (Brunzell, Liljeblom, & Vaihekoski,

2013).

The company has been able to decrease the cost of capital by increasing the funds based

on least costly source. The cost of capital may be reduced by the company through restructuring

of the capital which cannot exceed the rate of return. The lower amount for the cost of capital

will be able to fund new projects in a cheaper way. The reduction on the cost of capital can be

considered with formulation of new credit line and the common debt loan utilized for financing

the assets including the bank loan, card debt and bonds (Welch & Levi, 2013).

Conclusion:

The main analysis of the capital structure for APN comprise of equity and debentures. It

has been further seen that the company has been able to provide a satisfactory return for the

shareholders and the increased dividend for the shareholders. The earnings and the revenues

before taxed and interest has been seen with an upward trend in generating a satisfactory return

to the shareholders.

9ACCOUNTING & FINANCE

References

Baker, H. K., & English, P. (2013). Capital Budgeting: An Overview. In Capital Budgeting

Valuation: Financial Analysis for Today’s Investment Projects (pp. 1–16).

https://doi.org/10.1002/9781118258422.ch1

Batra, R., & Verma, S. (2017). Capital budgeting practices in Indian companies. IIMB

Management Review, 29(1), 29–44. https://doi.org/10.1016/j.iimb.2017.02.001

Brunzell, T., Liljeblom, E., & Vaihekoski, M. (2013). Determinants of capital budgeting

methods and hurdle rates in Nordic firms. Accounting and Finance, 53(1), 85–110.

https://doi.org/10.1111/j.1467-629X.2011.00462.x

Daunfeldt, S.-O., & Hartwig, F. (2014). What Determines the Use of Capital Budgeting

Methods? Evidence from Swedish Listed Companies. Journal of Finance and Economics,

2(4), 12. https://doi.org/10.12691/jfe-2-4-1

Dellavigna, S., & Pollet, J. M. (2013). Capital Budgeting versus Market Timing: An Evaluation

Using Demographics. Journal of Finance, 68(1), 237–270. https://doi.org/10.1111/j.1540-

6261.2012.01799.x

Durnev, A., Morck, R., & Yeung, B. (2004). Value-enhancing capital budgeting and firm-

specific stock return variation. The Journal of Finance, 59(1), 65–105.

https://doi.org/10.1111/j.1540-6261.2004.00627.x

Hall, J. H., & Westerman, W. (2013). Basic Risk Adjustment Techniques in Capital Budgeting.

In Capital Budgeting Valuation: Financial Analysis for Today’s Investment Projects (pp.

References

Baker, H. K., & English, P. (2013). Capital Budgeting: An Overview. In Capital Budgeting

Valuation: Financial Analysis for Today’s Investment Projects (pp. 1–16).

https://doi.org/10.1002/9781118258422.ch1

Batra, R., & Verma, S. (2017). Capital budgeting practices in Indian companies. IIMB

Management Review, 29(1), 29–44. https://doi.org/10.1016/j.iimb.2017.02.001

Brunzell, T., Liljeblom, E., & Vaihekoski, M. (2013). Determinants of capital budgeting

methods and hurdle rates in Nordic firms. Accounting and Finance, 53(1), 85–110.

https://doi.org/10.1111/j.1467-629X.2011.00462.x

Daunfeldt, S.-O., & Hartwig, F. (2014). What Determines the Use of Capital Budgeting

Methods? Evidence from Swedish Listed Companies. Journal of Finance and Economics,

2(4), 12. https://doi.org/10.12691/jfe-2-4-1

Dellavigna, S., & Pollet, J. M. (2013). Capital Budgeting versus Market Timing: An Evaluation

Using Demographics. Journal of Finance, 68(1), 237–270. https://doi.org/10.1111/j.1540-

6261.2012.01799.x

Durnev, A., Morck, R., & Yeung, B. (2004). Value-enhancing capital budgeting and firm-

specific stock return variation. The Journal of Finance, 59(1), 65–105.

https://doi.org/10.1111/j.1540-6261.2004.00627.x

Hall, J. H., & Westerman, W. (2013). Basic Risk Adjustment Techniques in Capital Budgeting.

In Capital Budgeting Valuation: Financial Analysis for Today’s Investment Projects (pp.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING & FINANCE

215–239). https://doi.org/10.1002/9781118258422.ch12

Li, H., Peng, J., & Li, S. (2015). Uncertain programming models for capital budgeting subject to

experts’ estimations. Journal of Intelligent and Fuzzy Systems, 28(2), 725–736.

https://doi.org/10.3233/IFS-141353

Nurullah, M., & Kengatharan, L. (2015). Capital budgeting practices: evidence from Sri Lanka.

Journal of Advances in Management Research, 12(1), 55–82.

https://doi.org/10.1108/JAMR-01-2014-0004

Welch, I., & Levi, Y. (2013). Long-Term Capital Budgeting. SSRN Electronic Journal.

https://doi.org/10.2139/ssrn.2327807

215–239). https://doi.org/10.1002/9781118258422.ch12

Li, H., Peng, J., & Li, S. (2015). Uncertain programming models for capital budgeting subject to

experts’ estimations. Journal of Intelligent and Fuzzy Systems, 28(2), 725–736.

https://doi.org/10.3233/IFS-141353

Nurullah, M., & Kengatharan, L. (2015). Capital budgeting practices: evidence from Sri Lanka.

Journal of Advances in Management Research, 12(1), 55–82.

https://doi.org/10.1108/JAMR-01-2014-0004

Welch, I., & Levi, Y. (2013). Long-Term Capital Budgeting. SSRN Electronic Journal.

https://doi.org/10.2139/ssrn.2327807

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.