S-ACC515 Investment Analysis and Corporate Finance - CSU

VerifiedAdded on 2023/06/04

|14

|1862

|320

Homework Assignment

AI Summary

This assignment covers several key areas in accounting and finance, including investment analysis, loan repayment calculations, and portfolio management. It begins by calculating the present value of a stream of cash flows to determine the appropriate investment amount. The assignm...

ACCOUNTING & FINANCE

Student Name

[Pick the date]

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

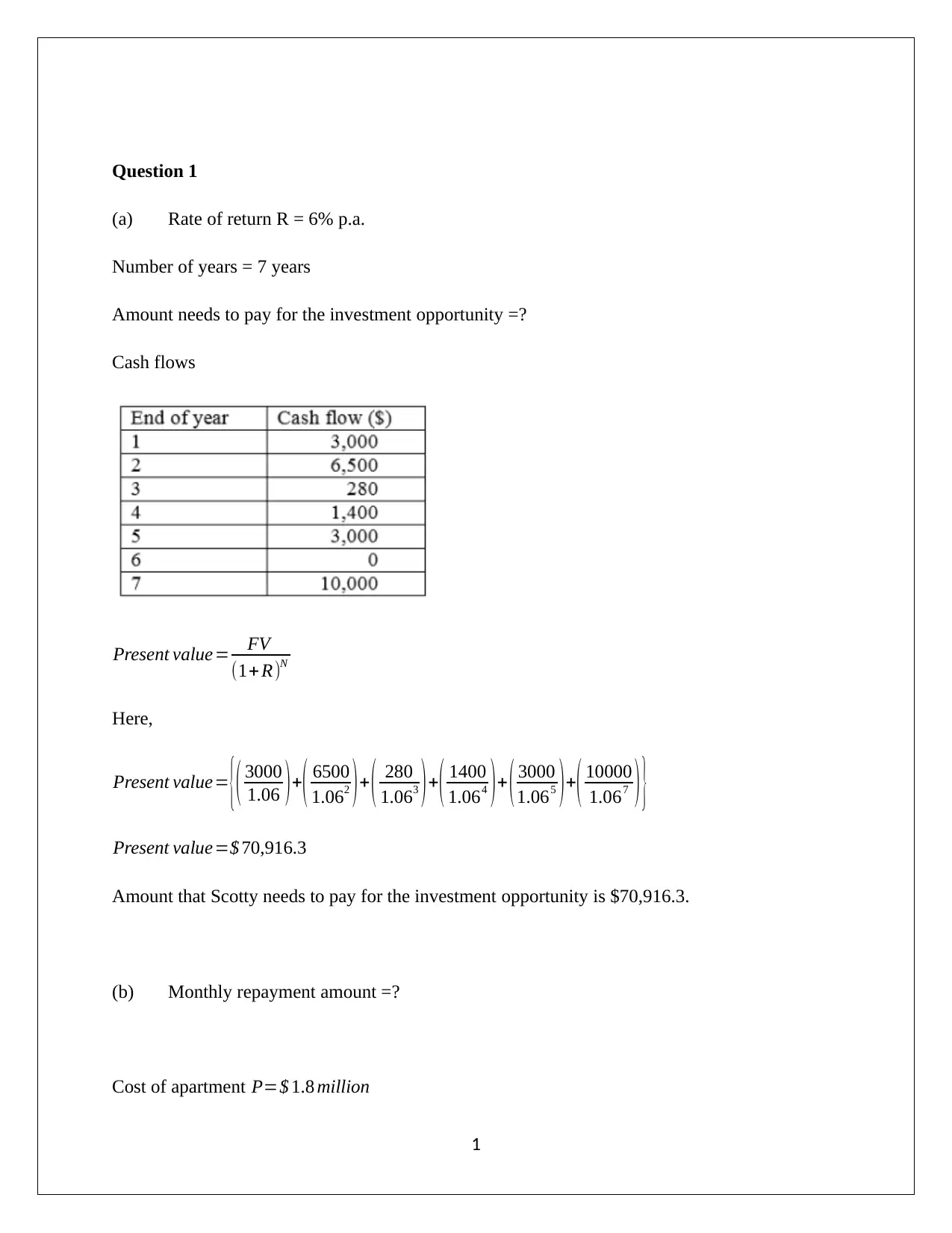

Question 1

(a) Rate of return R = 6% p.a.

Number of years = 7 years

Amount needs to pay for the investment opportunity =?

Cash flows

Present value= FV

(1+ R)N

Here,

Present value= {( 3000

1.06 ) +

( 6500

1.062 ) + ( 280

1.063 ) +

( 1400

1.064 ) + ( 3000

1.065 ) +

( 10000

1.067 ) }

Present value=$ 70,916.3

Amount that Scotty needs to pay for the investment opportunity is $70,916.3.

(b) Monthly repayment amount =?

Cost of apartment P=$ 1.8 million

1

(a) Rate of return R = 6% p.a.

Number of years = 7 years

Amount needs to pay for the investment opportunity =?

Cash flows

Present value= FV

(1+ R)N

Here,

Present value= {( 3000

1.06 ) +

( 6500

1.062 ) + ( 280

1.063 ) +

( 1400

1.064 ) + ( 3000

1.065 ) +

( 10000

1.067 ) }

Present value=$ 70,916.3

Amount that Scotty needs to pay for the investment opportunity is $70,916.3.

(b) Monthly repayment amount =?

Cost of apartment P=$ 1.8 million

1

Nominal interest rate of loan R=5 % p . a.∨0.4167 per month

Time period N¿ 30 years∨360 months

The relevant formula is shown below.

Monthly repayment amount= P∗R∗( 1+ R )N

(1+R )N −1 = ( 1800000 )∗( 0.004167 )∗( 1+ 0.004167 )360

( 1+0.004167 )360 =$ 9,662.79

(c) (i) Future value of monthly saving deposits =?

Future value of lump sum deposit =?

Ben has amount to invest = $50,000

Total monthly payment = N=(35∗12)=420

Interest rate R=7 %p.a ¿ 0.5833 per month

Monthly payment amount =$1500

These monthly payment would be as annuity payment for total period of 25 years. Further, it has

been assumed that first payment will either be started from today or at the starting period.

Let, the first payment will either be started from today

Future value of annuity= (1+ R )∗P∗ { ( 1+R )N −1

R }=¿ ( 1+0.005833 )∗1500∗[ ( 1+0.005833 )420−1

0.005833 ]

Future value of annuity=$ 2,717,341.13

Future value of monthly saving deposits would be $ 2,717,341.13

Further,

Future value =PV ( 1+ R ) N=50,000 ( 1+0.005833 ) 420=$ 575,307.6

Future value ∑ deposit =$ 2,717,341.13+$ 575,307.6=$ 3,292,648.72

2

Time period N¿ 30 years∨360 months

The relevant formula is shown below.

Monthly repayment amount= P∗R∗( 1+ R )N

(1+R )N −1 = ( 1800000 )∗( 0.004167 )∗( 1+ 0.004167 )360

( 1+0.004167 )360 =$ 9,662.79

(c) (i) Future value of monthly saving deposits =?

Future value of lump sum deposit =?

Ben has amount to invest = $50,000

Total monthly payment = N=(35∗12)=420

Interest rate R=7 %p.a ¿ 0.5833 per month

Monthly payment amount =$1500

These monthly payment would be as annuity payment for total period of 25 years. Further, it has

been assumed that first payment will either be started from today or at the starting period.

Let, the first payment will either be started from today

Future value of annuity= (1+ R )∗P∗ { ( 1+R )N −1

R }=¿ ( 1+0.005833 )∗1500∗[ ( 1+0.005833 )420−1

0.005833 ]

Future value of annuity=$ 2,717,341.13

Future value of monthly saving deposits would be $ 2,717,341.13

Further,

Future value =PV ( 1+ R ) N=50,000 ( 1+0.005833 ) 420=$ 575,307.6

Future value ∑ deposit =$ 2,717,341.13+$ 575,307.6=$ 3,292,648.72

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Future value of lump sum deposit would be $ 3,292,648.72.

(ii) Annual pension that would be received by Ben after retirement =?

Future value of sum amount = $200,000

Rate of interest = 5% p.a.

Number of years = 25 years

Now,

Present value= FV

(1+ R)N = 200000

( 1+0.05 )25

Present value=$ 59060.55

Let x is the amount for which the annuity would be derived for 25 years.

x=$ 3,292,648.72−$ 59060.55=$ 3,233,588.17

Further,

Let y is the annuity amount that after one year of retirement.

Present value of annuity= A [ 1−(1+ R)−N

R ]

A= 3,233,588.1

[ 1−(1+0.05)−25

0.05 ] =$ 229,431

Therefore, the annuity amount after one year of retirement is $229,431.

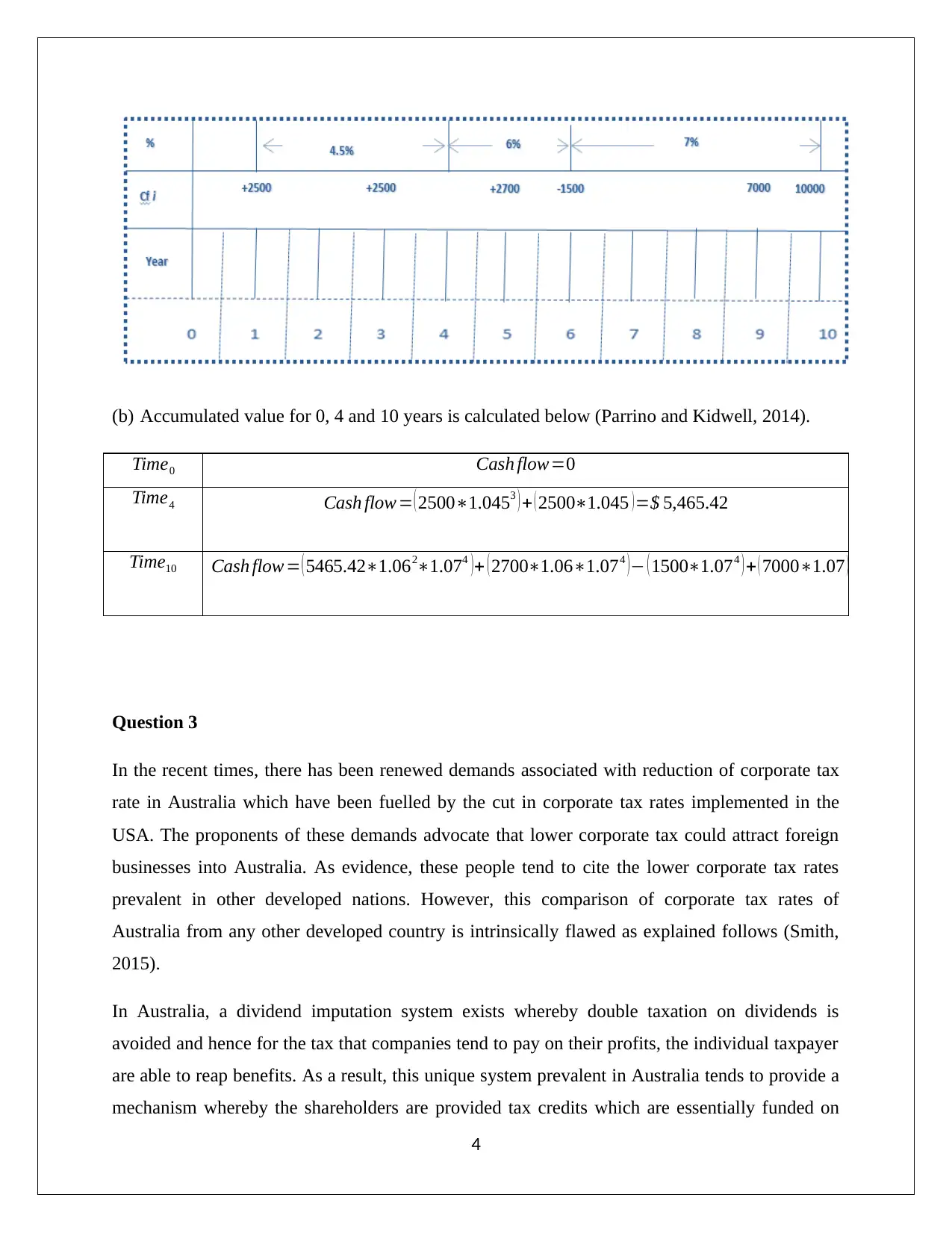

Question 2

(a) Time line of cash flows

3

(ii) Annual pension that would be received by Ben after retirement =?

Future value of sum amount = $200,000

Rate of interest = 5% p.a.

Number of years = 25 years

Now,

Present value= FV

(1+ R)N = 200000

( 1+0.05 )25

Present value=$ 59060.55

Let x is the amount for which the annuity would be derived for 25 years.

x=$ 3,292,648.72−$ 59060.55=$ 3,233,588.17

Further,

Let y is the annuity amount that after one year of retirement.

Present value of annuity= A [ 1−(1+ R)−N

R ]

A= 3,233,588.1

[ 1−(1+0.05)−25

0.05 ] =$ 229,431

Therefore, the annuity amount after one year of retirement is $229,431.

Question 2

(a) Time line of cash flows

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Accumulated value for 0, 4 and 10 years is calculated below (Parrino and Kidwell, 2014).

Time0 Cash flow=0

Time4 Cash flow= ( 2500∗1.0453 ) + ( 2500∗1.045 ) =$ 5,465.42

Time10 Cash flow= ( 5465.42∗1.062∗1.074 ) + ( 2700∗1.06∗1.074 ) − ( 1500∗1.074 ) + ( 7000∗1.07 ) +10000=$ 27

Question 3

In the recent times, there has been renewed demands associated with reduction of corporate tax

rate in Australia which have been fuelled by the cut in corporate tax rates implemented in the

USA. The proponents of these demands advocate that lower corporate tax could attract foreign

businesses into Australia. As evidence, these people tend to cite the lower corporate tax rates

prevalent in other developed nations. However, this comparison of corporate tax rates of

Australia from any other developed country is intrinsically flawed as explained follows (Smith,

2015).

In Australia, a dividend imputation system exists whereby double taxation on dividends is

avoided and hence for the tax that companies tend to pay on their profits, the individual taxpayer

are able to reap benefits. As a result, this unique system prevalent in Australia tends to provide a

mechanism whereby the shareholders are provided tax credits which are essentially funded on

4

Time0 Cash flow=0

Time4 Cash flow= ( 2500∗1.0453 ) + ( 2500∗1.045 ) =$ 5,465.42

Time10 Cash flow= ( 5465.42∗1.062∗1.074 ) + ( 2700∗1.06∗1.074 ) − ( 1500∗1.074 ) + ( 7000∗1.07 ) +10000=$ 27

Question 3

In the recent times, there has been renewed demands associated with reduction of corporate tax

rate in Australia which have been fuelled by the cut in corporate tax rates implemented in the

USA. The proponents of these demands advocate that lower corporate tax could attract foreign

businesses into Australia. As evidence, these people tend to cite the lower corporate tax rates

prevalent in other developed nations. However, this comparison of corporate tax rates of

Australia from any other developed country is intrinsically flawed as explained follows (Smith,

2015).

In Australia, a dividend imputation system exists whereby double taxation on dividends is

avoided and hence for the tax that companies tend to pay on their profits, the individual taxpayer

are able to reap benefits. As a result, this unique system prevalent in Australia tends to provide a

mechanism whereby the shareholders are provided tax credits which are essentially funded on

4

the basis of the corporate tax paid by the company. This particular system tends to differ from

the existing system in other nations since in these nations, double taxation of corporate income is

prevalent. The companies need to pay corporate tax on the generated profits and when dividends

are paid to the shareholders, then even the shareholders are taxed for the dividend income they

receive. Thus, the effective rate of tax in these countries is actually higher than the corresponding

rates currently existing in Australia (Smith, 2015).

This difference can be illustrated through the use of an example. Let us assume that the total

profit of the company is $ 10,000. The corporate tax that that would be paid on this income at

30% would be $3,000. Assuming that the remaining proceeds are given as dividends to the

shareholders and these attract a marginal tax rate of 30%, then additional tax collection of $

2,100 would arise from shareholders. Thereby, the total tax revenue paid on $ 10,000 of

corporate profit amount to $ 5,100 and thereby resulting in a tax rate of 51%. In comparison

Australia requires payment of only $ 3,000 as tax.

Hence, if there is a decrease in the corporate tax rate, then the company would have a higher

amount of surplus cash which it would give as dividends. The franking credits attached to these

would be lower and hence the rebate on corporate tax in case of domestic companies would be

recouped in the form of incremental personal income tax receipts on dividends for shareholders.

As a result, there would not be any impact on the government revenues on account of domestic

companies. However, this would differ dramatically in case of foreign companies as the

incremental cash with the company after paying of corporate tax would be repatriated to the

home country and thus government revenues lost would not be made up (Smith, 2015).

Therefore, it is apparent from above the any reduction in corporate tax rate would be beneficial

for foreign companies only. But, it is imperative to understand that the foreign investment in

Australia is not hampered by the tax rate and would not come gushing in if the corporate tax rate

is lowered. Certain sectors of economy such as agriculture, animal husbandry, mining, services

are also quite developed in Australia and also have presence of foreign players despite the tax

rate. However, there is the lagging manufacturing sector which does not attract foreign

investments owing to high labour cost and unfavourable geographical location. Even if the

corporate tax rate is lowered, it is highly improbable that any meaningful investment would

come on the basis of corporate tax rate cut in the manufacturing sector. Besides, consideration

5

the existing system in other nations since in these nations, double taxation of corporate income is

prevalent. The companies need to pay corporate tax on the generated profits and when dividends

are paid to the shareholders, then even the shareholders are taxed for the dividend income they

receive. Thus, the effective rate of tax in these countries is actually higher than the corresponding

rates currently existing in Australia (Smith, 2015).

This difference can be illustrated through the use of an example. Let us assume that the total

profit of the company is $ 10,000. The corporate tax that that would be paid on this income at

30% would be $3,000. Assuming that the remaining proceeds are given as dividends to the

shareholders and these attract a marginal tax rate of 30%, then additional tax collection of $

2,100 would arise from shareholders. Thereby, the total tax revenue paid on $ 10,000 of

corporate profit amount to $ 5,100 and thereby resulting in a tax rate of 51%. In comparison

Australia requires payment of only $ 3,000 as tax.

Hence, if there is a decrease in the corporate tax rate, then the company would have a higher

amount of surplus cash which it would give as dividends. The franking credits attached to these

would be lower and hence the rebate on corporate tax in case of domestic companies would be

recouped in the form of incremental personal income tax receipts on dividends for shareholders.

As a result, there would not be any impact on the government revenues on account of domestic

companies. However, this would differ dramatically in case of foreign companies as the

incremental cash with the company after paying of corporate tax would be repatriated to the

home country and thus government revenues lost would not be made up (Smith, 2015).

Therefore, it is apparent from above the any reduction in corporate tax rate would be beneficial

for foreign companies only. But, it is imperative to understand that the foreign investment in

Australia is not hampered by the tax rate and would not come gushing in if the corporate tax rate

is lowered. Certain sectors of economy such as agriculture, animal husbandry, mining, services

are also quite developed in Australia and also have presence of foreign players despite the tax

rate. However, there is the lagging manufacturing sector which does not attract foreign

investments owing to high labour cost and unfavourable geographical location. Even if the

corporate tax rate is lowered, it is highly improbable that any meaningful investment would

come on the basis of corporate tax rate cut in the manufacturing sector. Besides, consideration

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

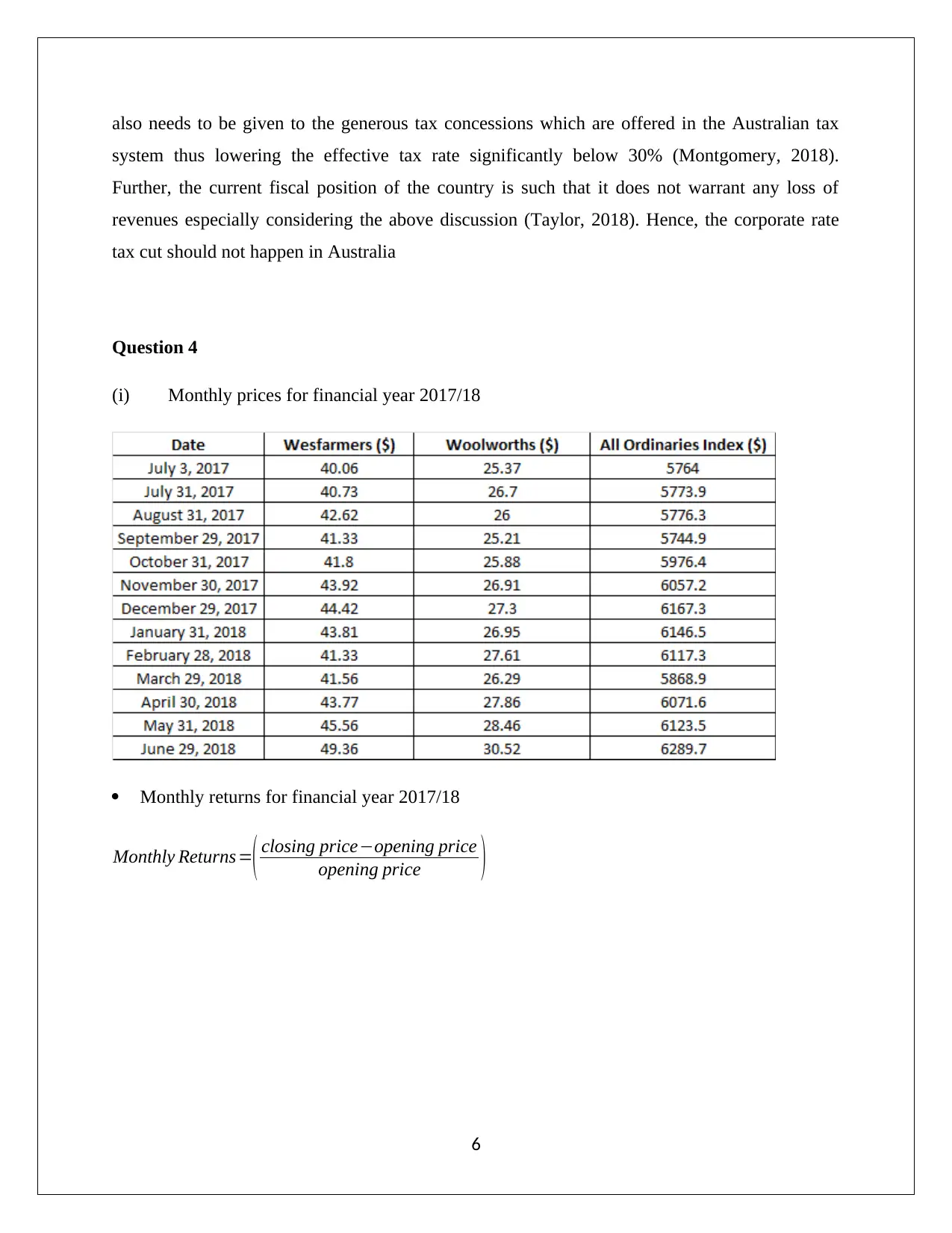

also needs to be given to the generous tax concessions which are offered in the Australian tax

system thus lowering the effective tax rate significantly below 30% (Montgomery, 2018).

Further, the current fiscal position of the country is such that it does not warrant any loss of

revenues especially considering the above discussion (Taylor, 2018). Hence, the corporate rate

tax cut should not happen in Australia

Question 4

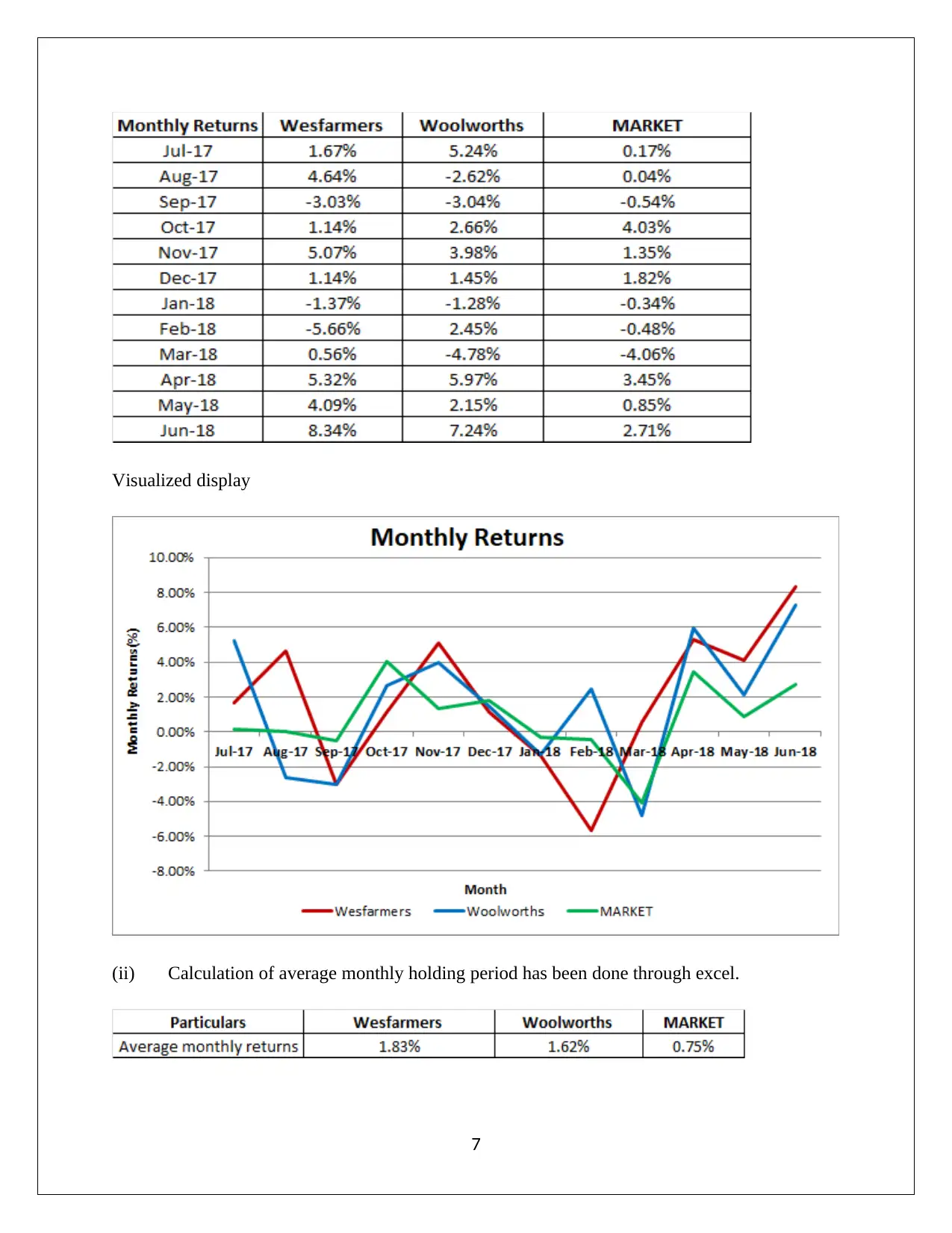

(i) Monthly prices for financial year 2017/18

Monthly returns for financial year 2017/18

Monthly Returns=( closing price−opening price

opening price )

6

system thus lowering the effective tax rate significantly below 30% (Montgomery, 2018).

Further, the current fiscal position of the country is such that it does not warrant any loss of

revenues especially considering the above discussion (Taylor, 2018). Hence, the corporate rate

tax cut should not happen in Australia

Question 4

(i) Monthly prices for financial year 2017/18

Monthly returns for financial year 2017/18

Monthly Returns=( closing price−opening price

opening price )

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Visualized display

(ii) Calculation of average monthly holding period has been done through excel.

7

(ii) Calculation of average monthly holding period has been done through excel.

7

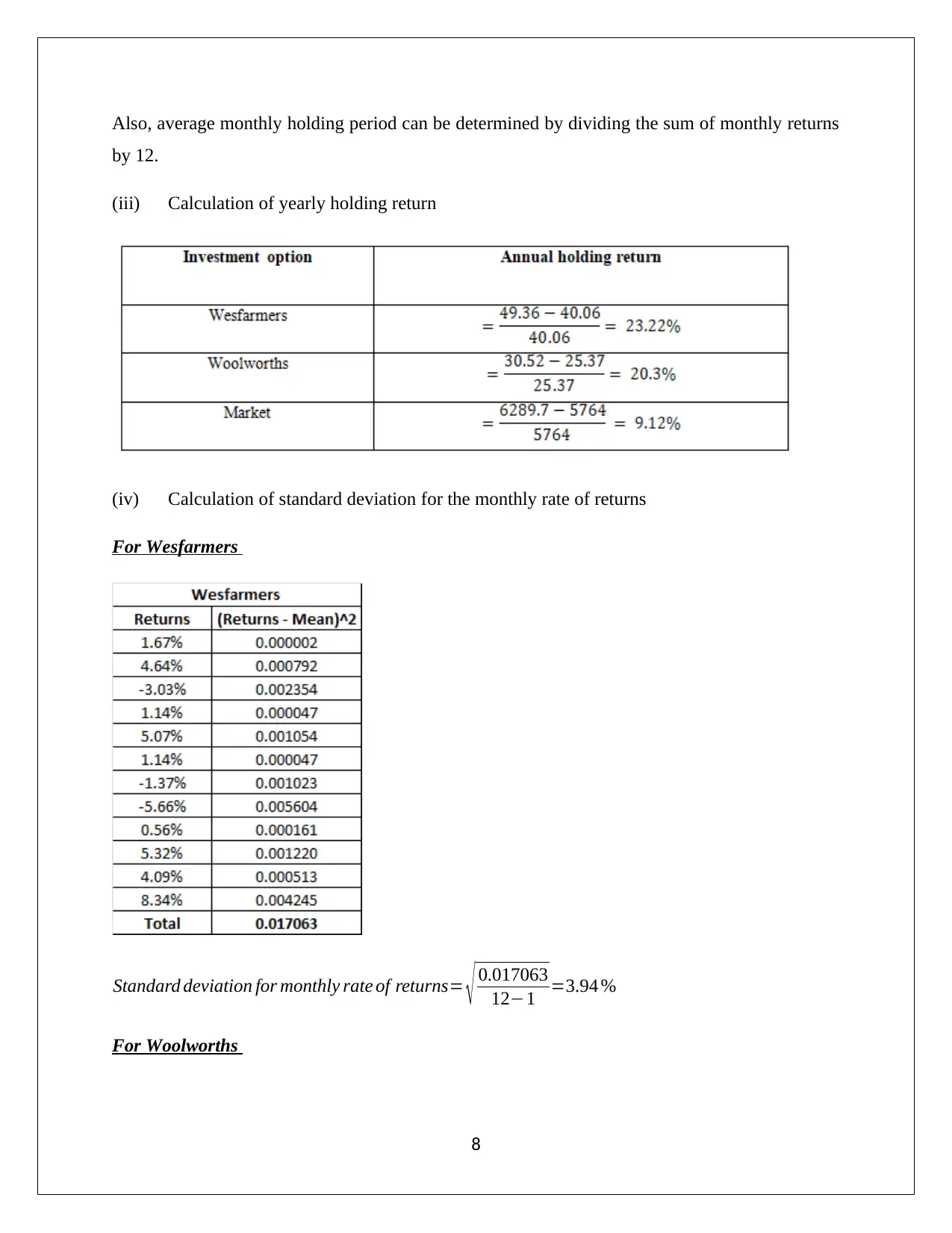

Also, average monthly holding period can be determined by dividing the sum of monthly returns

by 12.

(iii) Calculation of yearly holding return

(iv) Calculation of standard deviation for the monthly rate of returns

For Wesfarmers

Standard deviation for monthly rate of returns= √ 0.017063

12−1 =3.94 %

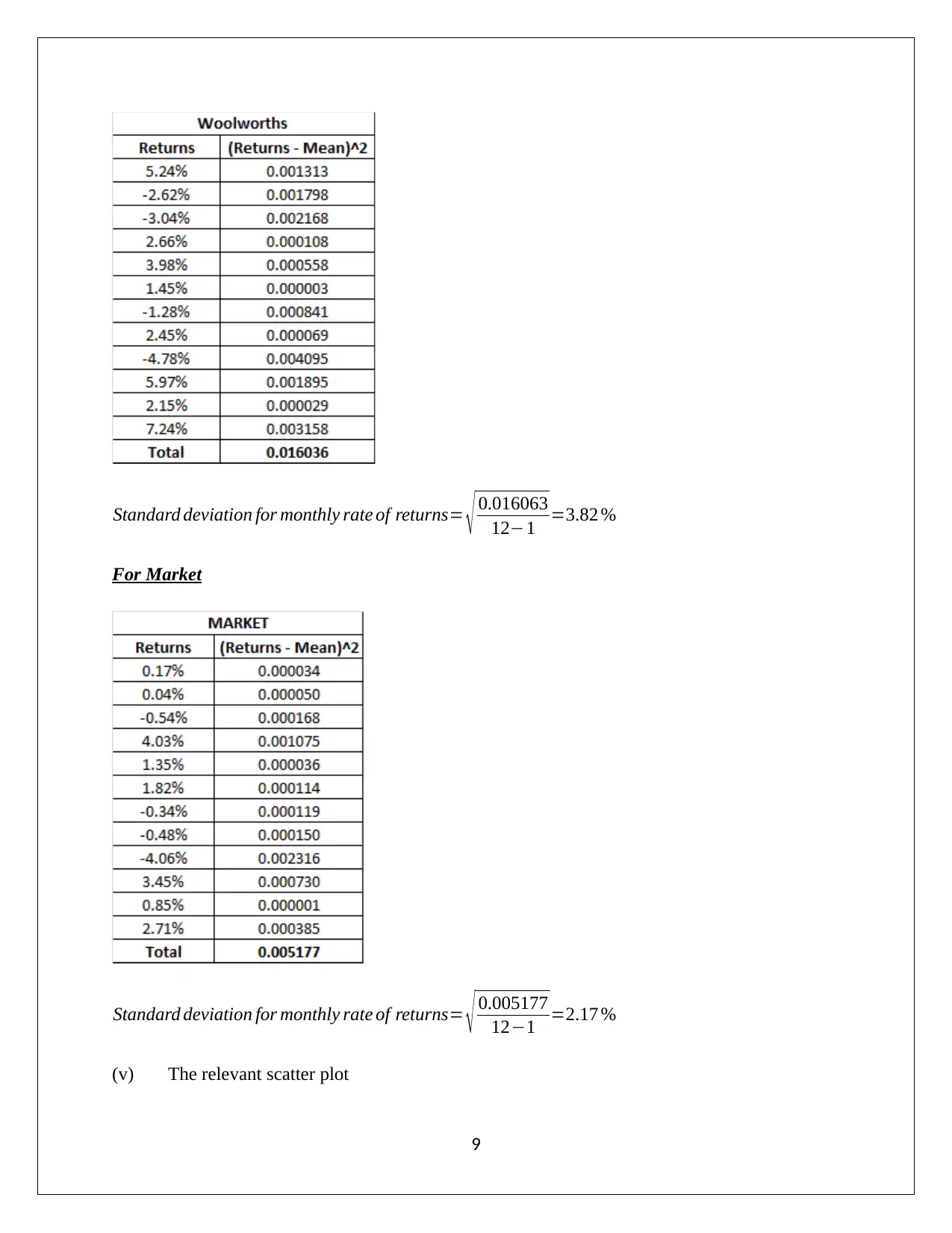

For Woolworths

8

by 12.

(iii) Calculation of yearly holding return

(iv) Calculation of standard deviation for the monthly rate of returns

For Wesfarmers

Standard deviation for monthly rate of returns= √ 0.017063

12−1 =3.94 %

For Woolworths

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard deviation for monthly rate of returns= √ 0.016063

12−1 =3.82 %

For Market

Standard deviation for monthly rate of returns= √ 0.005177

12−1 =2.17 %

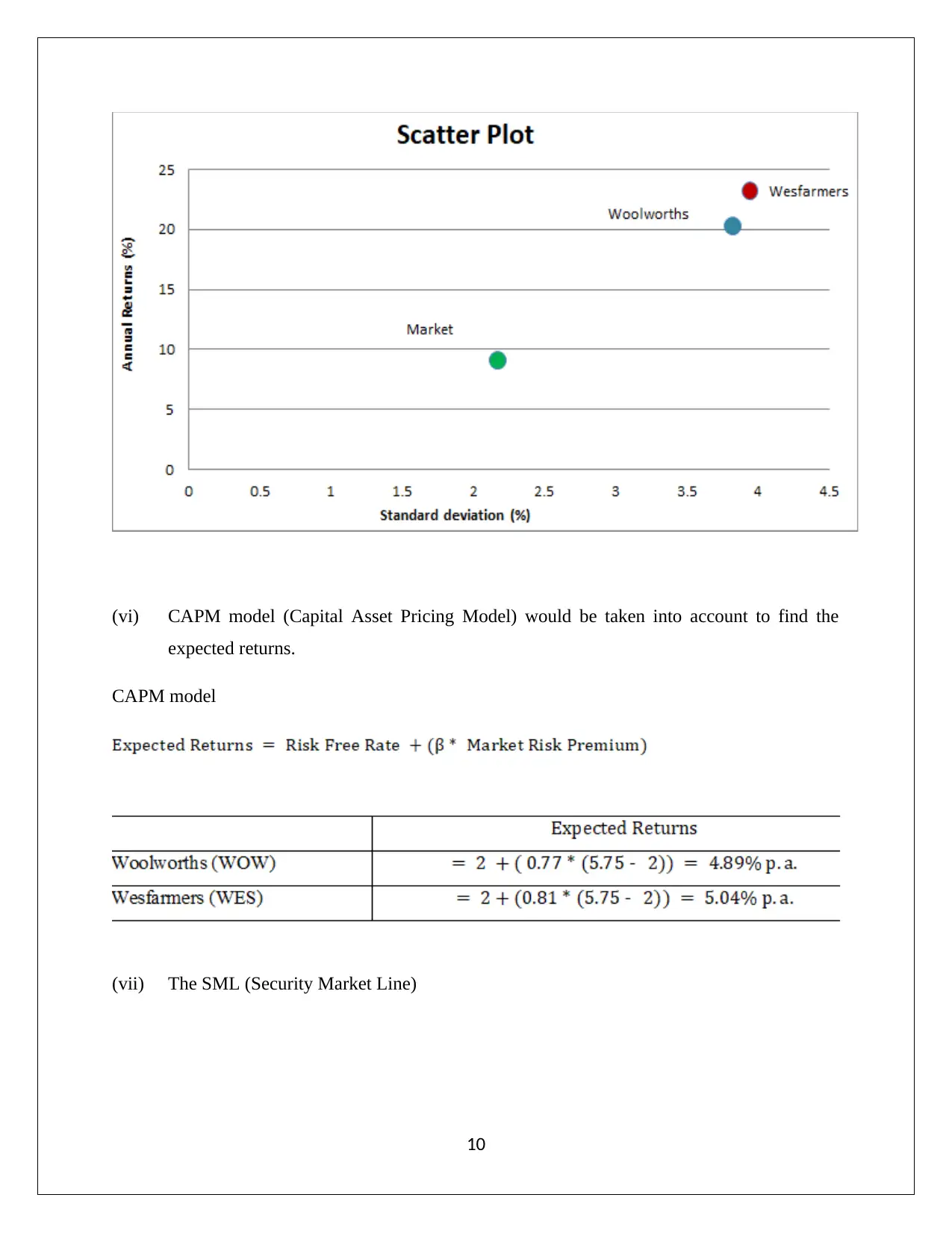

(v) The relevant scatter plot

9

12−1 =3.82 %

For Market

Standard deviation for monthly rate of returns= √ 0.005177

12−1 =2.17 %

(v) The relevant scatter plot

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(vi) CAPM model (Capital Asset Pricing Model) would be taken into account to find the

expected returns.

CAPM model

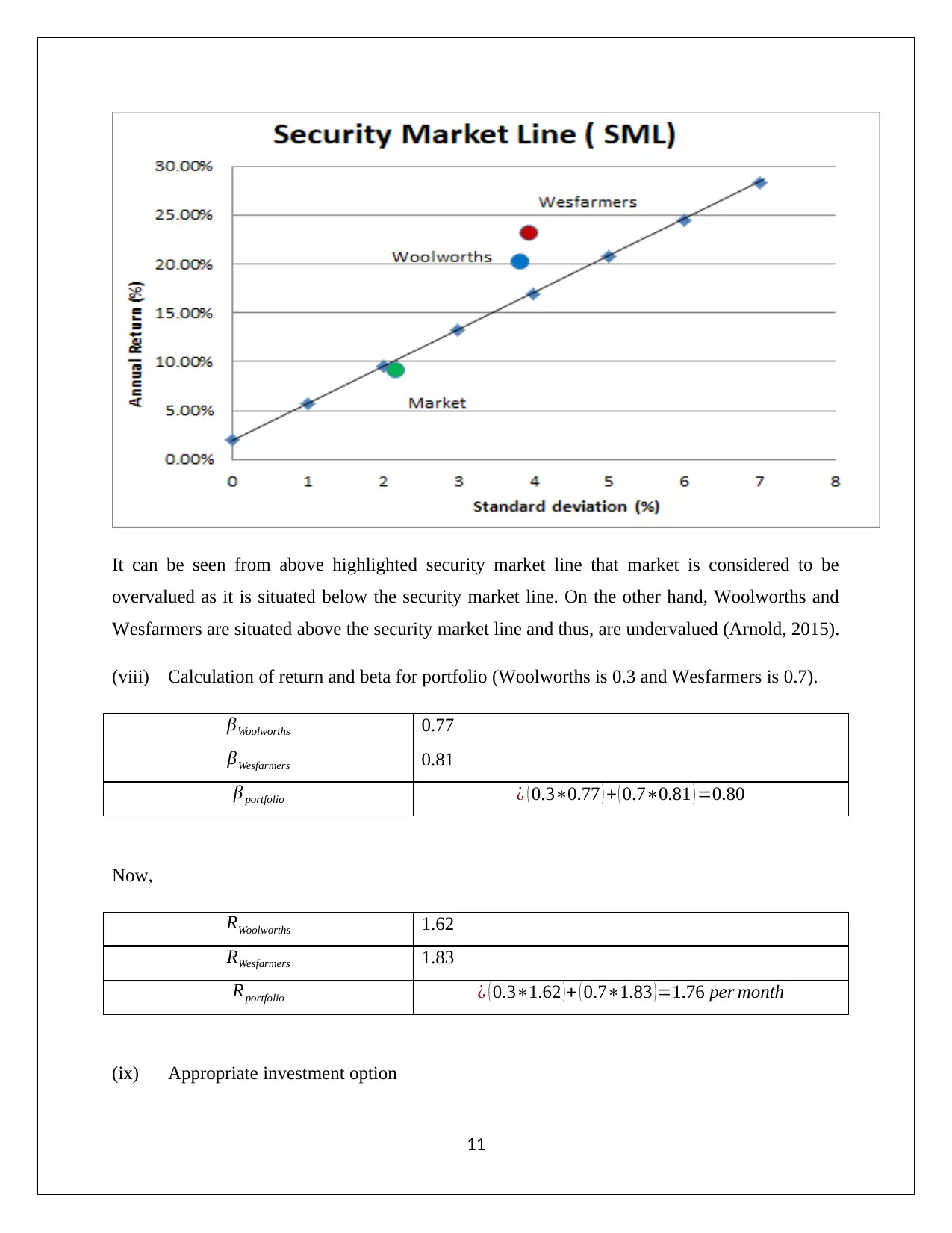

(vii) The SML (Security Market Line)

10

expected returns.

CAPM model

(vii) The SML (Security Market Line)

10

It can be seen from above highlighted security market line that market is considered to be

overvalued as it is situated below the security market line. On the other hand, Woolworths and

Wesfarmers are situated above the security market line and thus, are undervalued (Arnold, 2015).

(viii) Calculation of return and beta for portfolio (Woolworths is 0.3 and Wesfarmers is 0.7).

βWoolworths 0.77

βWesfarmers 0.81

β portfolio ¿ ( 0.3∗0.77 ) + ( 0.7∗0.81 ) =0.80

Now,

RWoolworths 1.62

RWesfarmers 1.83

Rportfolio ¿ ( 0.3∗1.62 )+ ( 0.7∗1.83 )=1.76 per month

(ix) Appropriate investment option

11

overvalued as it is situated below the security market line. On the other hand, Woolworths and

Wesfarmers are situated above the security market line and thus, are undervalued (Arnold, 2015).

(viii) Calculation of return and beta for portfolio (Woolworths is 0.3 and Wesfarmers is 0.7).

βWoolworths 0.77

βWesfarmers 0.81

β portfolio ¿ ( 0.3∗0.77 ) + ( 0.7∗0.81 ) =0.80

Now,

RWoolworths 1.62

RWesfarmers 1.83

Rportfolio ¿ ( 0.3∗1.62 )+ ( 0.7∗1.83 )=1.76 per month

(ix) Appropriate investment option

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

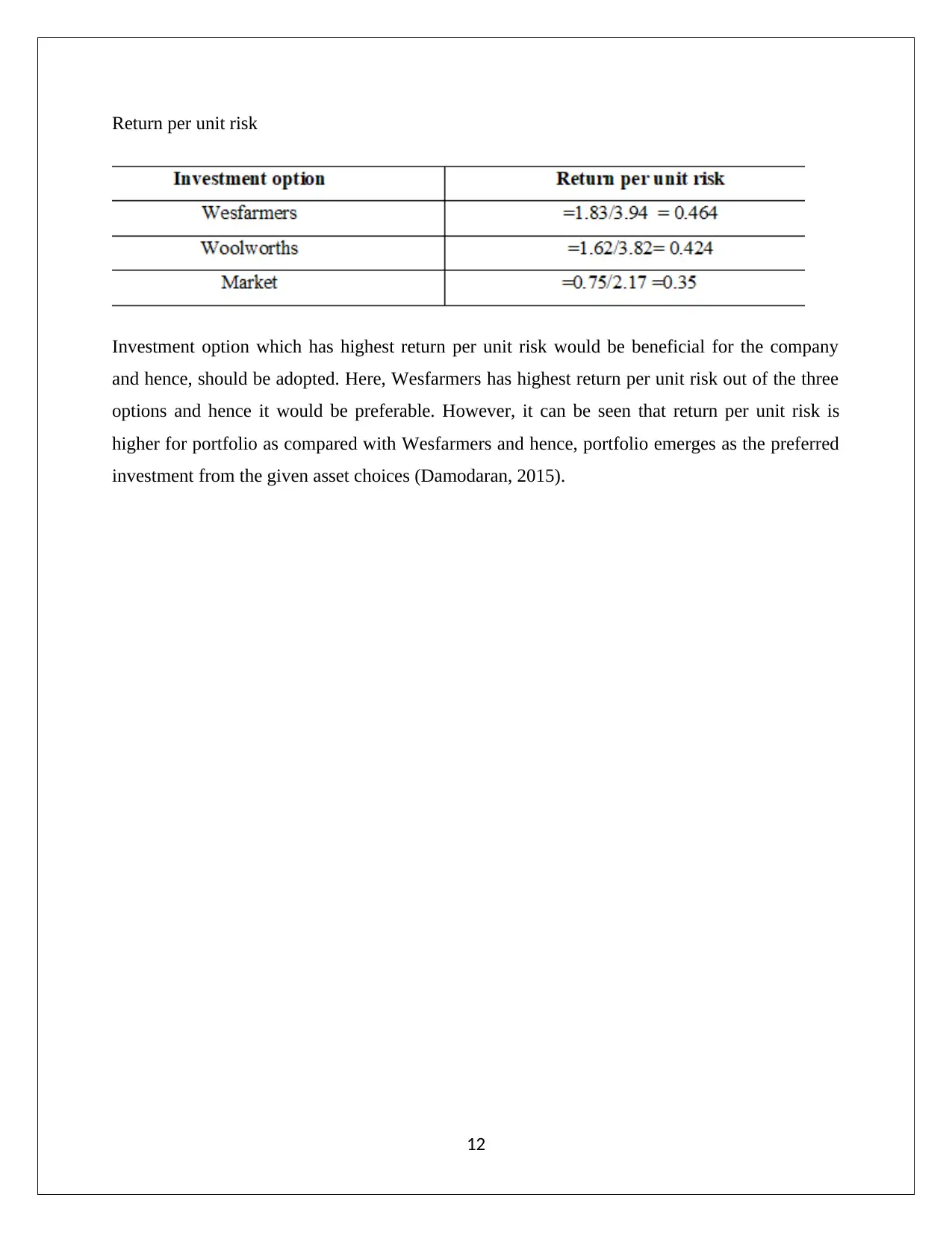

Return per unit risk

Investment option which has highest return per unit risk would be beneficial for the company

and hence, should be adopted. Here, Wesfarmers has highest return per unit risk out of the three

options and hence it would be preferable. However, it can be seen that return per unit risk is

higher for portfolio as compared with Wesfarmers and hence, portfolio emerges as the preferred

investment from the given asset choices (Damodaran, 2015).

12

Investment option which has highest return per unit risk would be beneficial for the company

and hence, should be adopted. Here, Wesfarmers has highest return per unit risk out of the three

options and hence it would be preferable. However, it can be seen that return per unit risk is

higher for portfolio as compared with Wesfarmers and hence, portfolio emerges as the preferred

investment from the given asset choices (Damodaran, 2015).

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley,

John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

Taylor, D. (2018, March 29). Corporate tax cuts: What are the key issues in the

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

13

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley,

John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

Taylor, D. (2018, March 29). Corporate tax cuts: What are the key issues in the

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

13

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.