Accounting and Finance: Investment Appraisal, Statements & Analysis

VerifiedAdded on 2023/06/16

Paraphrase This Document

INTRODUCTION...........................................................................................................................3

QUESTION 1 –TOM & JERRY LIMITED....................................................................................3

Preparing statement of profitability and Financial Position by following the given transactions

.....................................................................................................................................................3

QUESTION 2 – FIDEL & ANA LIMITED....................................................................................3

a. Assessing contribution that each electric kettle will make referring the given scenario.........3

b. Computing break-even point and margin of safety.................................................................3

c. Calculating profit which firm will make if it produces and sells 48,000 electric kettles........3

d. Analyzing whether proposed strategy for Stockstone Ltd is good or not................................3

e. Explain the underpinning assumptions associated with the break-even model.......................3

QUESTION 3 – BIMBAGU PLC...................................................................................................3

a. Assessing the viability of new machine for Bimbagu Plc using investment appraisal tool....3

b. Analyzing the key merits and limitations of the differing investment appraisal techniques...5

c. Explaining the key benefits and limitations budgets as a strategic planning tool...................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

Accounting may be defined as a process which is undertaken by manager for recording

transactions associated with business. With regards to business organization, accounting and

finance is highly significant as it furnishes information about company’s position as well as

performance. In order to meet information need of stakeholders every publicly listed firm

prepares and publish accounting statements at the end of year. For the purpose of effective

decision making and performance enhancement accounting team lays high level of emphasis on

evaluating each & every alternative available for investment purpose. The present report is based

on different case scenarios which will provide deeper insight about the concept of break-even

analysis and investment appraisal techniques. It highlights profitability and liabilities as well as

Tom & Jerry by preparing financial statements. Further, it entails the contribution of break-even

analysis in decision making pertaining to sales and production. Report also depicts the use of

capital budgeting technique in the selection of project which suitable for investment purpose.

Along with this, it also exhibits the strength and weakness related to each technique of

investment appraisal.

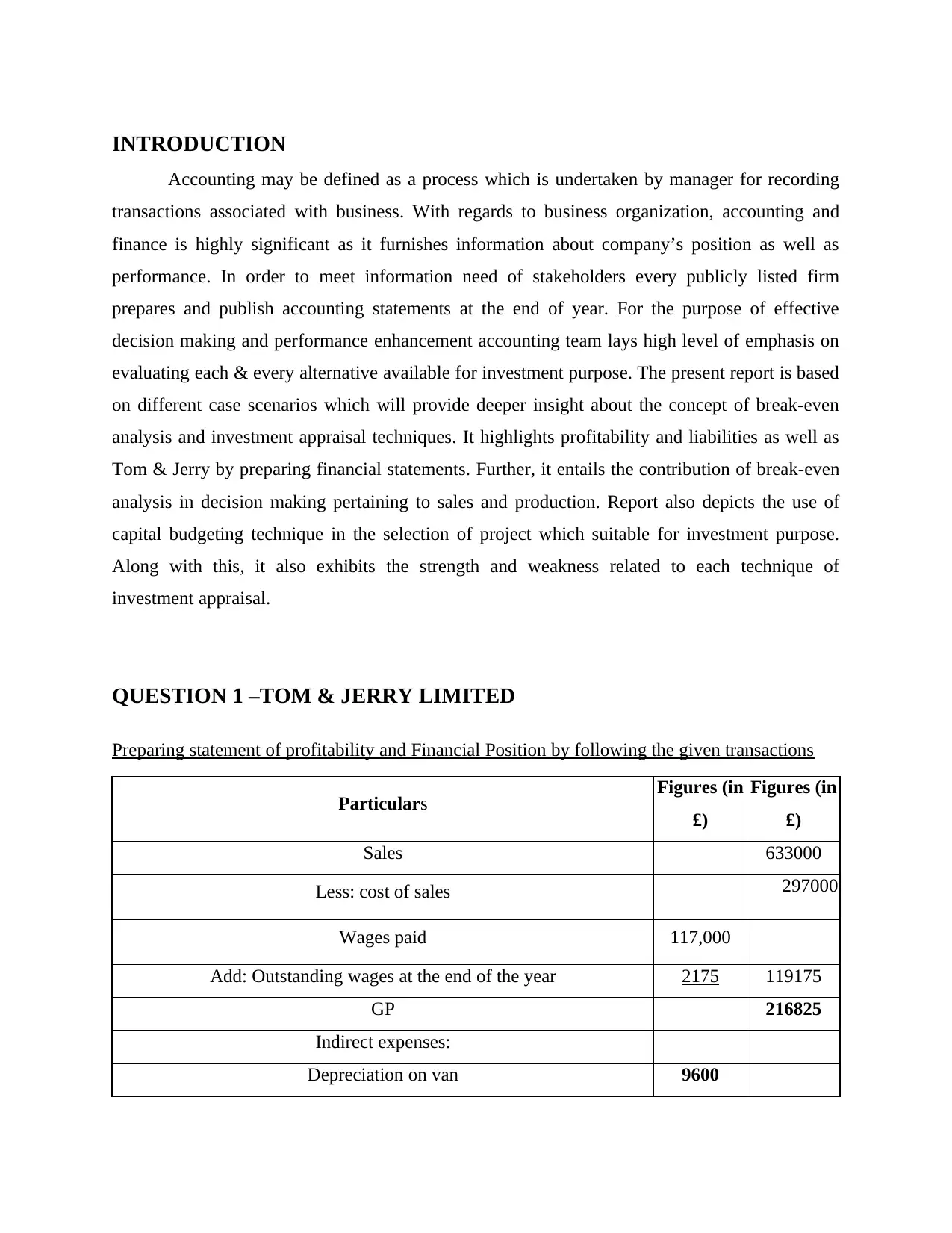

QUESTION 1 –TOM & JERRY LIMITED

Preparing statement of profitability and Financial Position by following the given transactions

Particulars Figures (in

£)

Figures (in

£)

Sales 633000

Less: cost of sales 297000

Wages paid 117,000

Add: Outstanding wages at the end of the year 2175 119175

GP 216825

Indirect expenses:

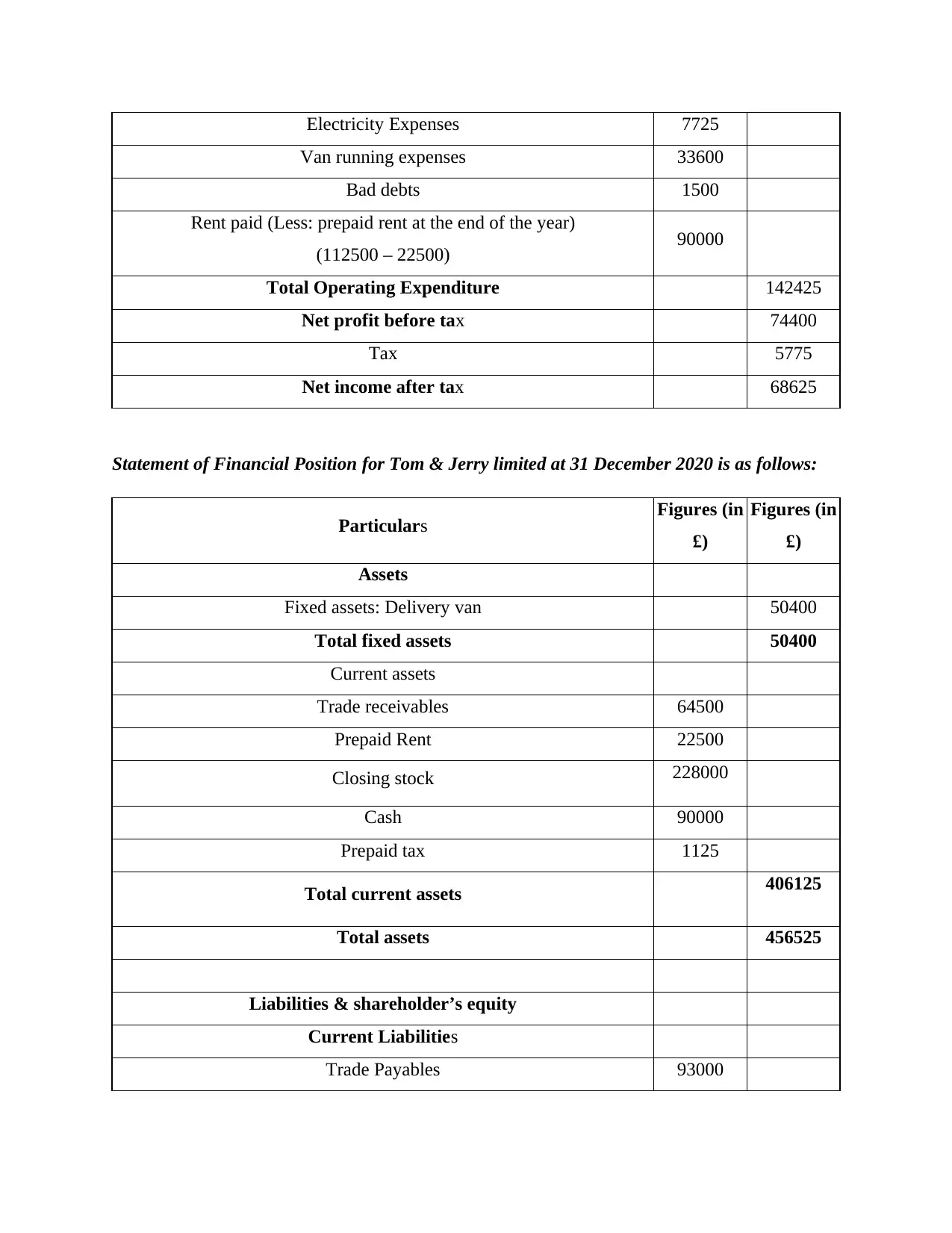

Depreciation on van 9600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Van running expenses 33600

Bad debts 1500

Rent paid (Less: prepaid rent at the end of the year)

(112500 – 22500) 90000

Total Operating Expenditure 142425

Net profit before tax 74400

Tax 5775

Net income after tax 68625

Statement of Financial Position for Tom & Jerry limited at 31 December 2020 is as follows:

Particulars Figures (in

£)

Figures (in

£)

Assets

Fixed assets: Delivery van 50400

Total fixed assets 50400

Current assets

Trade receivables 64500

Prepaid Rent 22500

Closing stock 228000

Cash 90000

Prepaid tax 1125

Total current assets 406125

Total assets 456525

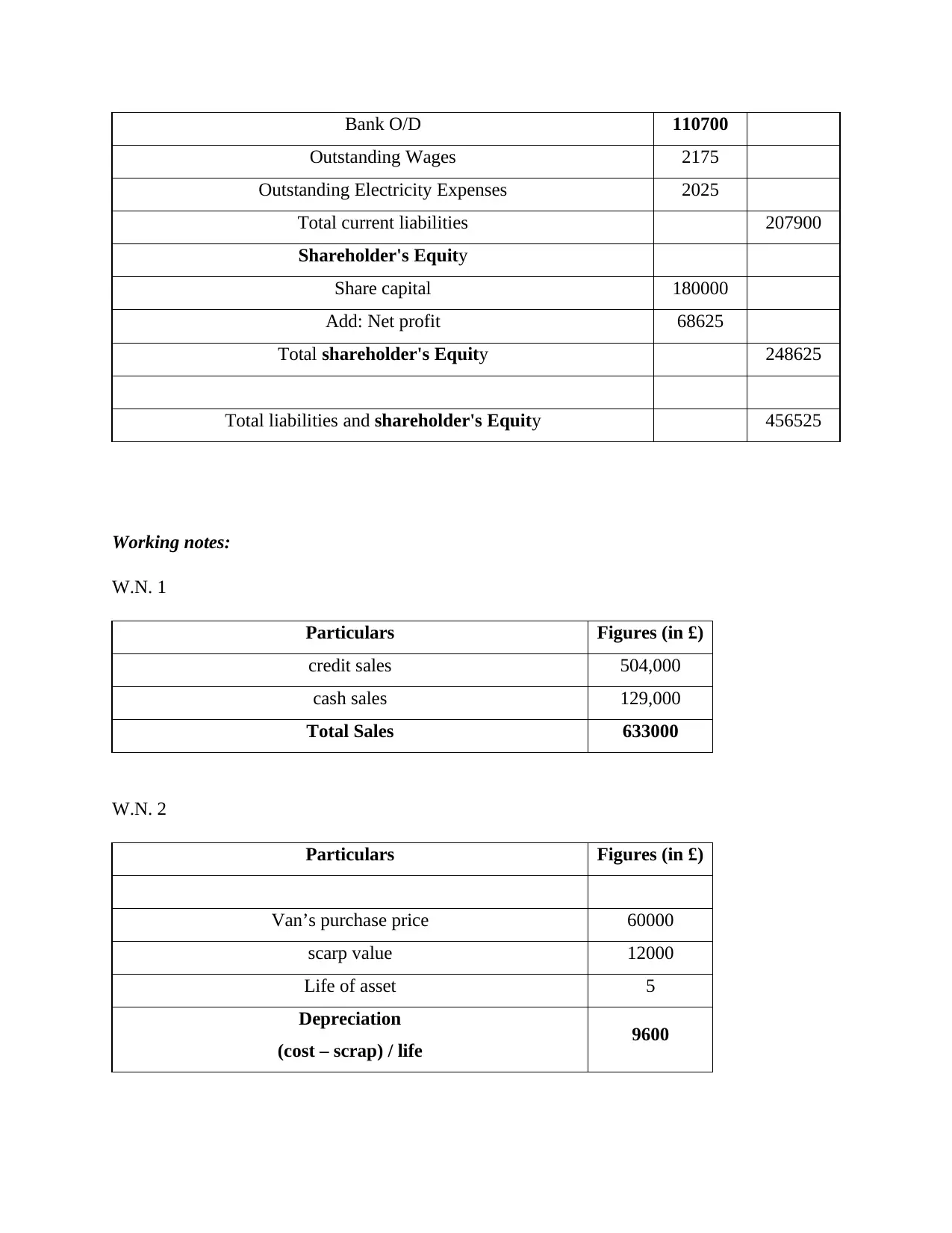

Liabilities & shareholder’s equity

Current Liabilities

Trade Payables 93000

Paraphrase This Document

Outstanding Wages 2175

Outstanding Electricity Expenses 2025

Total current liabilities 207900

Shareholder's Equity

Share capital 180000

Add: Net profit 68625

Total shareholder's Equity 248625

Total liabilities and shareholder's Equity 456525

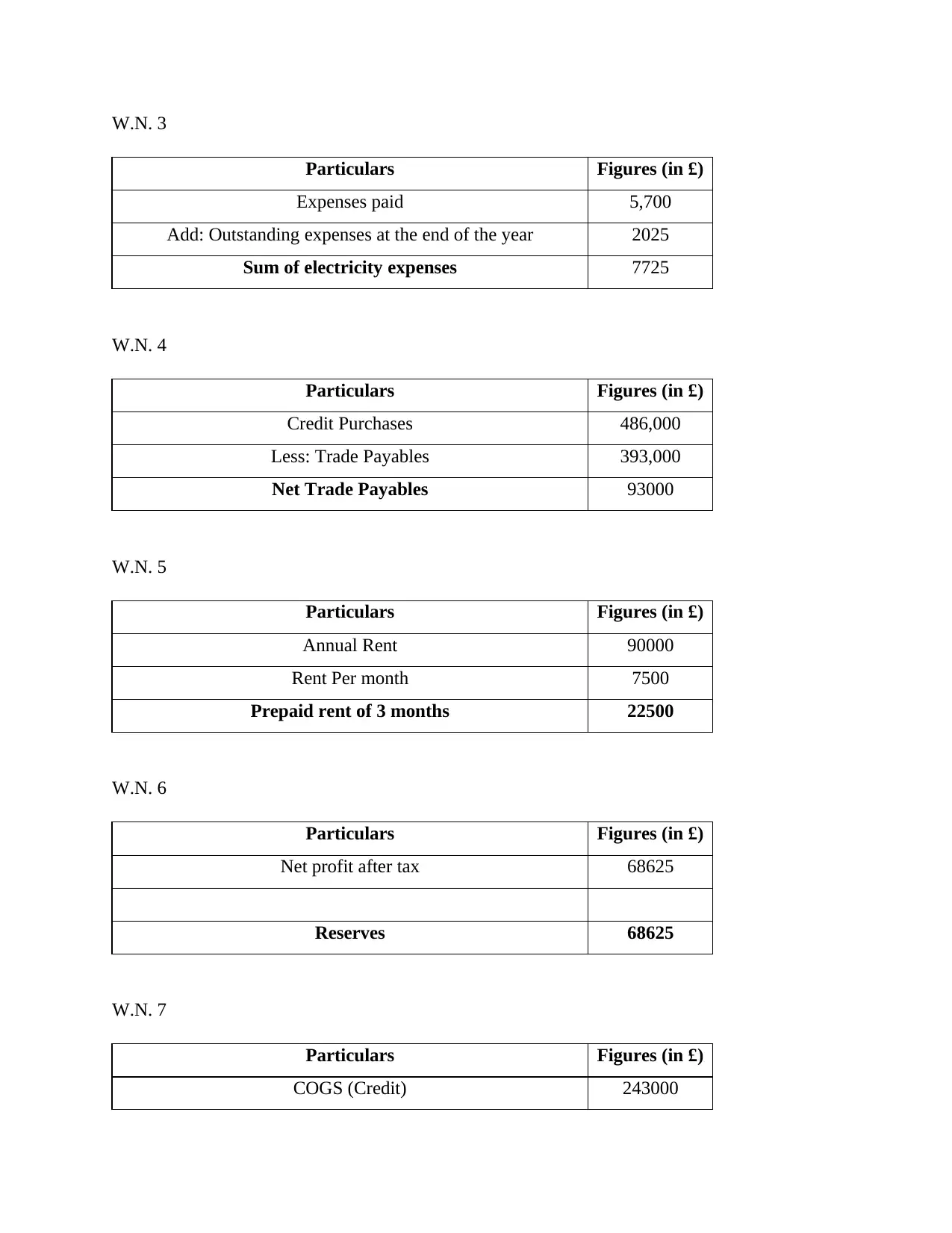

Working notes:

W.N. 1

Particulars Figures (in £)

credit sales 504,000

cash sales 129,000

Total Sales 633000

W.N. 2

Particulars Figures (in £)

Van’s purchase price 60000

scarp value 12000

Life of asset 5

Depreciation

(cost – scrap) / life 9600

Particulars Figures (in £)

Expenses paid 5,700

Add: Outstanding expenses at the end of the year 2025

Sum of electricity expenses 7725

W.N. 4

Particulars Figures (in £)

Credit Purchases 486,000

Less: Trade Payables 393,000

Net Trade Payables 93000

W.N. 5

Particulars Figures (in £)

Annual Rent 90000

Rent Per month 7500

Prepaid rent of 3 months 22500

W.N. 6

Particulars Figures (in £)

Net profit after tax 68625

Reserves 68625

W.N. 7

Particulars Figures (in £)

COGS (Credit) 243000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Cost of sales 297000

Credit Purchases 486000

Cash Purchases 39000

Total Purchases 525000

Closing stock (525000 – 297000) 228000

W.N. 8

Particulars Figures (in £)

Issue of Equity 180000

Receipts from Trade Receivables 438000

Total Receipts 618000

Rent paid 112500

Tax paid

(2400+4500) 6900

Delivery van purchased 60000

Wages paid 117000

Electricity Expenses 5700

Payment to Trade Payables 393000

Van running expenses 33600

Total outflows 728700

Closing bank balance (Bank overdraft) (110700)

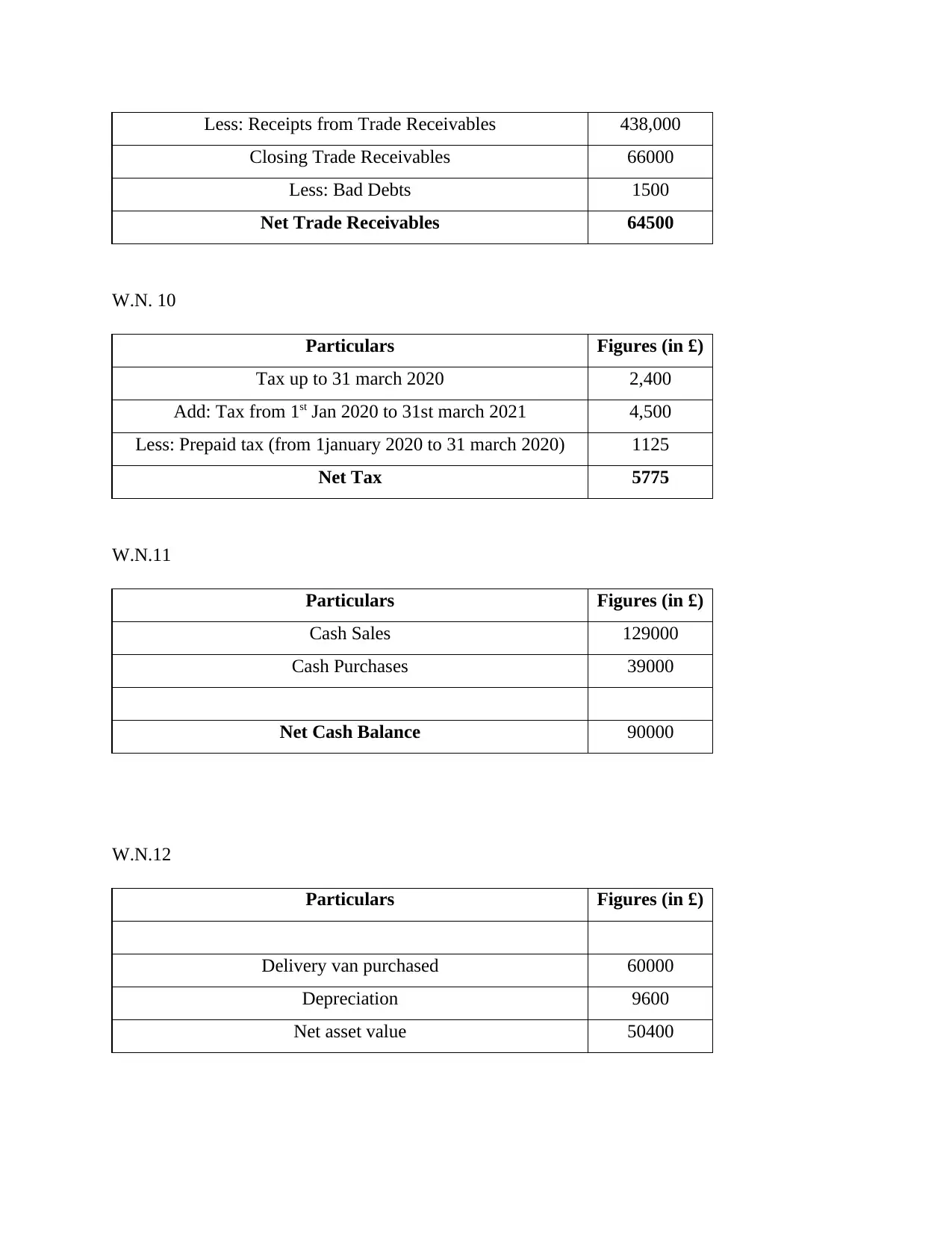

W.N. 9

Particulars Figures (in £)

Credit Sales 504,000

Paraphrase This Document

Closing Trade Receivables 66000

Less: Bad Debts 1500

Net Trade Receivables 64500

W.N. 10

Particulars Figures (in £)

Tax up to 31 march 2020 2,400

Add: Tax from 1st Jan 2020 to 31st march 2021 4,500

Less: Prepaid tax (from 1january 2020 to 31 march 2020) 1125

Net Tax 5775

W.N.11

Particulars Figures (in £)

Cash Sales 129000

Cash Purchases 39000

Net Cash Balance 90000

W.N.12

Particulars Figures (in £)

Delivery van purchased 60000

Depreciation 9600

Net asset value 50400

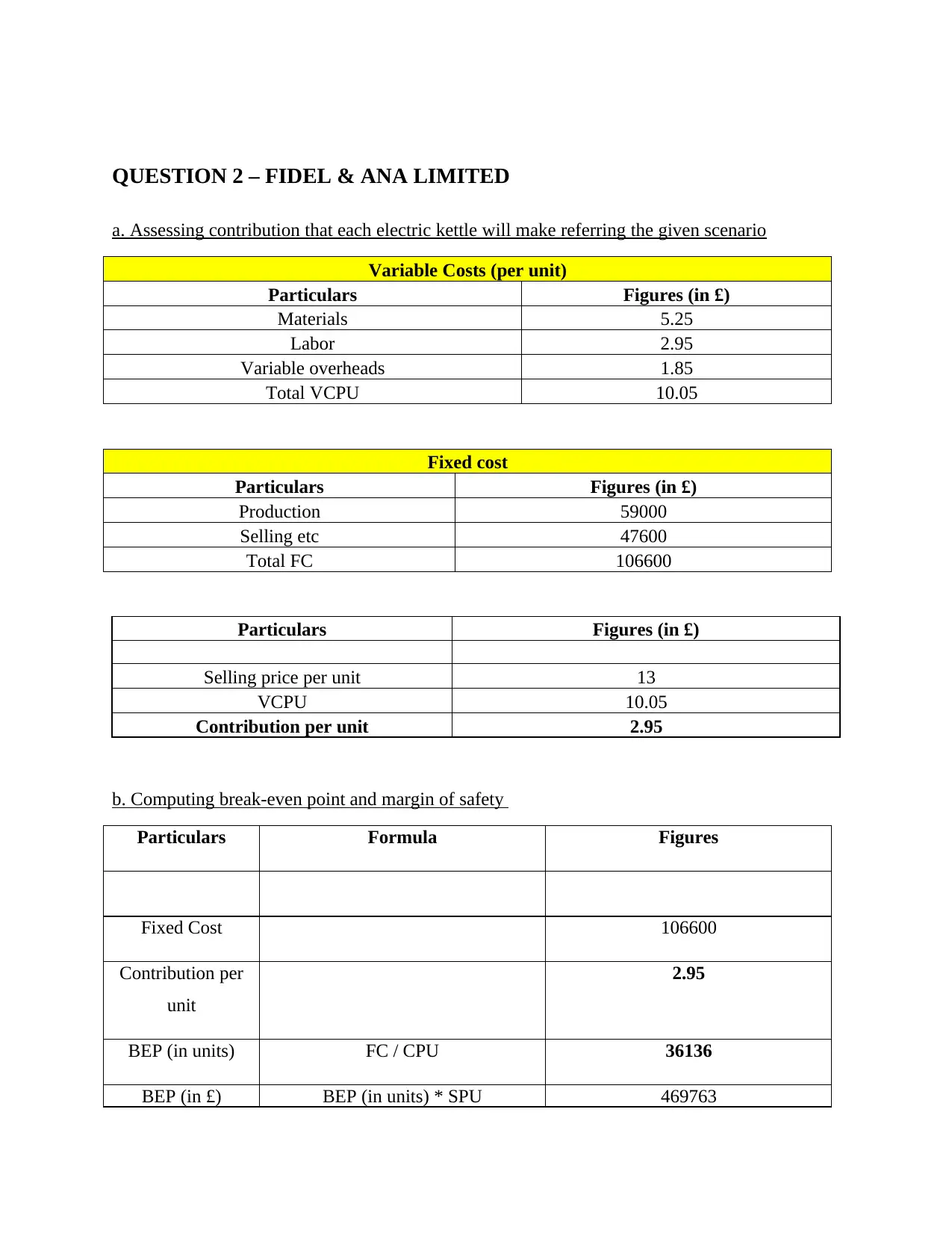

a. Assessing contribution that each electric kettle will make referring the given scenario

Variable Costs (per unit)

Particulars Figures (in £)

Materials 5.25

Labor 2.95

Variable overheads 1.85

Total VCPU 10.05

Fixed cost

Particulars Figures (in £)

Production 59000

Selling etc 47600

Total FC 106600

Particulars Figures (in £)

Selling price per unit 13

VCPU 10.05

Contribution per unit 2.95

b. Computing break-even point and margin of safety

Particulars Formula Figures

Fixed Cost 106600

Contribution per

unit

2.95

BEP (in units) FC / CPU 36136

BEP (in £) BEP (in units) * SPU 469763

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

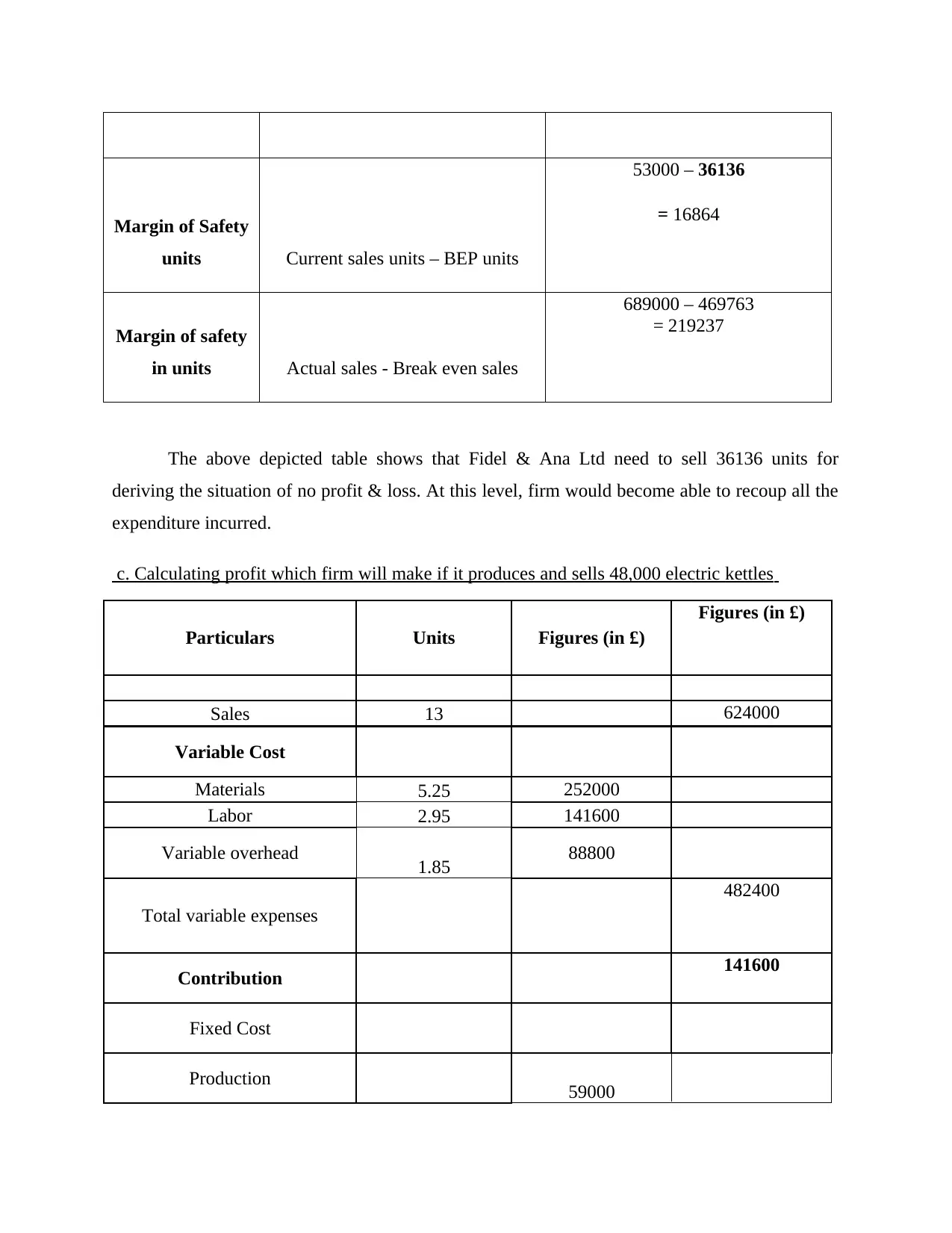

units Current sales units – BEP units

53000 – 36136

= 16864

Margin of safety

in units Actual sales - Break even sales

689000 – 469763

= 219237

The above depicted table shows that Fidel & Ana Ltd need to sell 36136 units for

deriving the situation of no profit & loss. At this level, firm would become able to recoup all the

expenditure incurred.

c. Calculating profit which firm will make if it produces and sells 48,000 electric kettles

Particulars Units Figures (in £)

Figures (in £)

Sales 13 624000

Variable Cost

Materials 5.25 252000

Labor 2.95 141600

Variable overhead 1.85 88800

Total variable expenses

482400

Contribution 141600

Fixed Cost

Production 59000

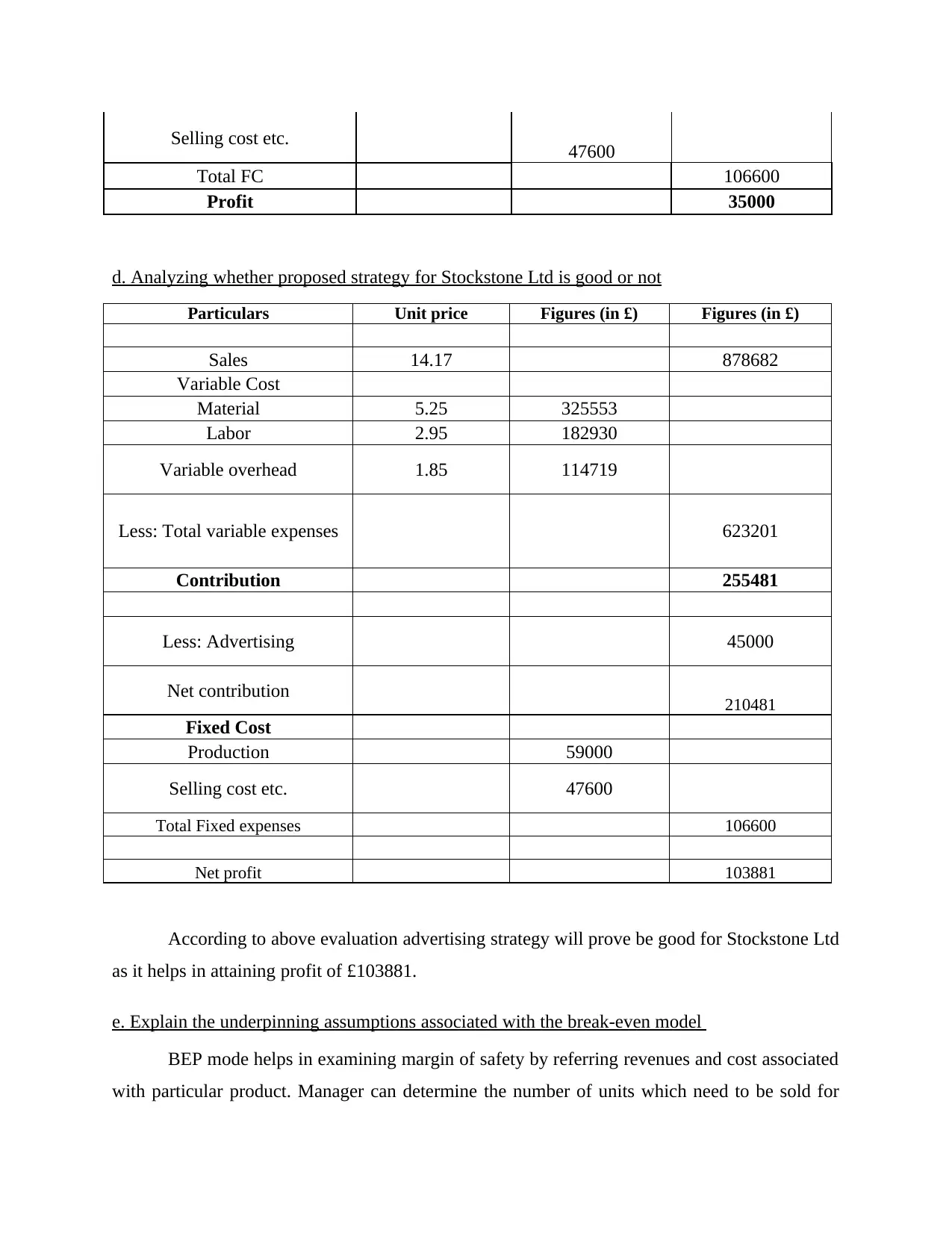

Paraphrase This Document

Total FC 106600

Profit 35000

d. Analyzing whether proposed strategy for Stockstone Ltd is good or not

Particulars Unit price Figures (in £) Figures (in £)

Sales 14.17 878682

Variable Cost

Material 5.25 325553

Labor 2.95 182930

Variable overhead 1.85 114719

Less: Total variable expenses 623201

Contribution 255481

Less: Advertising 45000

Net contribution 210481

Fixed Cost

Production 59000

Selling cost etc. 47600

Total Fixed expenses 106600

Net profit 103881

According to above evaluation advertising strategy will prove be good for Stockstone Ltd

as it helps in attaining profit of £103881.

e. Explain the underpinning assumptions associated with the break-even model

BEP mode helps in examining margin of safety by referring revenues and cost associated

with particular product. Manager can determine the number of units which need to be sold for

BEP is based on several assumption which mentioned below:

Fixed cost, selling price, per employee productivity and product mix remains constant

which is not possible in the dynamic business arena.

It focuses on dividing cost in terms of fixed and variable that associated with production

aspect (Kravchyk, Okur and Kovalenko, 2021). On the contrary to this, firm which

follows BEP model avoids semi-variable cost or expenses.

According to this, Fidel & Ana assumes that no improvement will take place in

technology and efficiency of labor. On the other side, now technological advancements

are taking place more frequently (Fuksa, 2021). Companies make focus on adopting latest

advancement which contributes in effectual business operations.

Cost and revenue shares linear relationship with each other which is also not true.

By doing evaluation it has assessed that BEP model is used by most of the firm with the

motive to assess sales unit and figures require to recover expenses (Sintha, 2020).

Specifically, manufacturing firms like Fidel & Ana undertakes BEP model for profit

planning and taking other strategic decision about business. However, there are some

limitations which affect the usage of BEP. The rationale behind this, all the assessment is

done considering past rather than future (Tannen, 2020). At the time of applying BEP model

accountant of Fide & Ana Ltd should refer limitations related to this model. Through this,

company would become able to make appropriate estimation ad thereby decisions as well.

QUESTION 3 – BIMBAGU PLC.

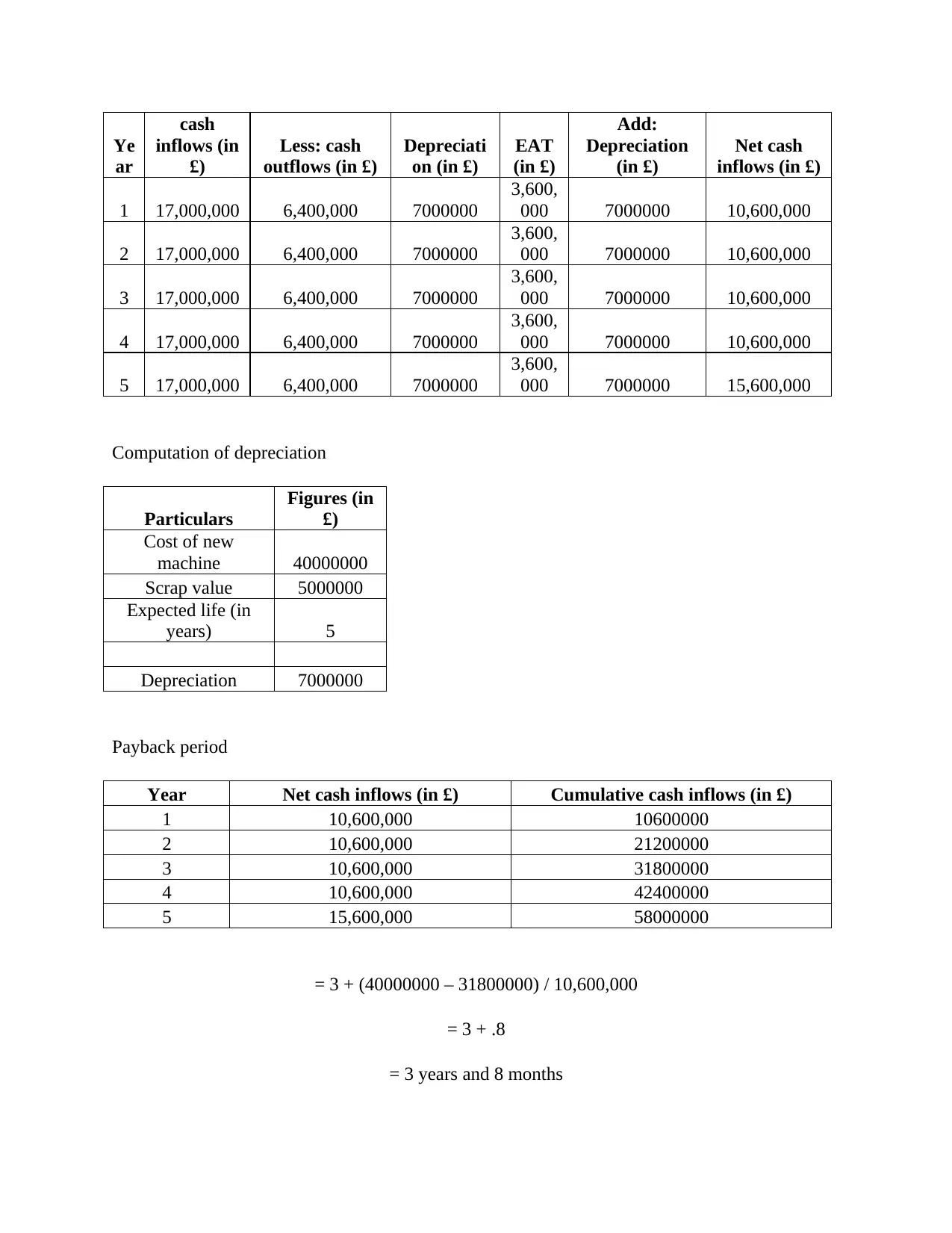

a. Assessing the viability of new machine for Bimbagu Plc using investment appraisal tool

According to the given case scenario, Bimbagu Plc, which manufactures motor parts,

wants to assess the extent to which proposed investment option in new machine will be good. In

this regard, several investment appraisal tools have been applied such as payback, net present

value and average rate of return.

Assessment of Cash inflows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ar

cash

inflows (in

£)

Less: cash

outflows (in £)

Depreciati

on (in £)

EAT

(in £)

Add:

Depreciation

(in £)

Net cash

inflows (in £)

1 17,000,000 6,400,000 7000000

3,600,

000 7000000 10,600,000

2 17,000,000 6,400,000 7000000

3,600,

000 7000000 10,600,000

3 17,000,000 6,400,000 7000000

3,600,

000 7000000 10,600,000

4 17,000,000 6,400,000 7000000

3,600,

000 7000000 10,600,000

5 17,000,000 6,400,000 7000000

3,600,

000 7000000 15,600,000

Computation of depreciation

Particulars

Figures (in

£)

Cost of new

machine 40000000

Scrap value 5000000

Expected life (in

years) 5

Depreciation 7000000

Payback period

Year Net cash inflows (in £) Cumulative cash inflows (in £)

1 10,600,000 10600000

2 10,600,000 21200000

3 10,600,000 31800000

4 10,600,000 42400000

5 15,600,000 58000000

= 3 + (40000000 – 31800000) / 10,600,000

= 3 + .8

= 3 years and 8 months

Paraphrase This Document

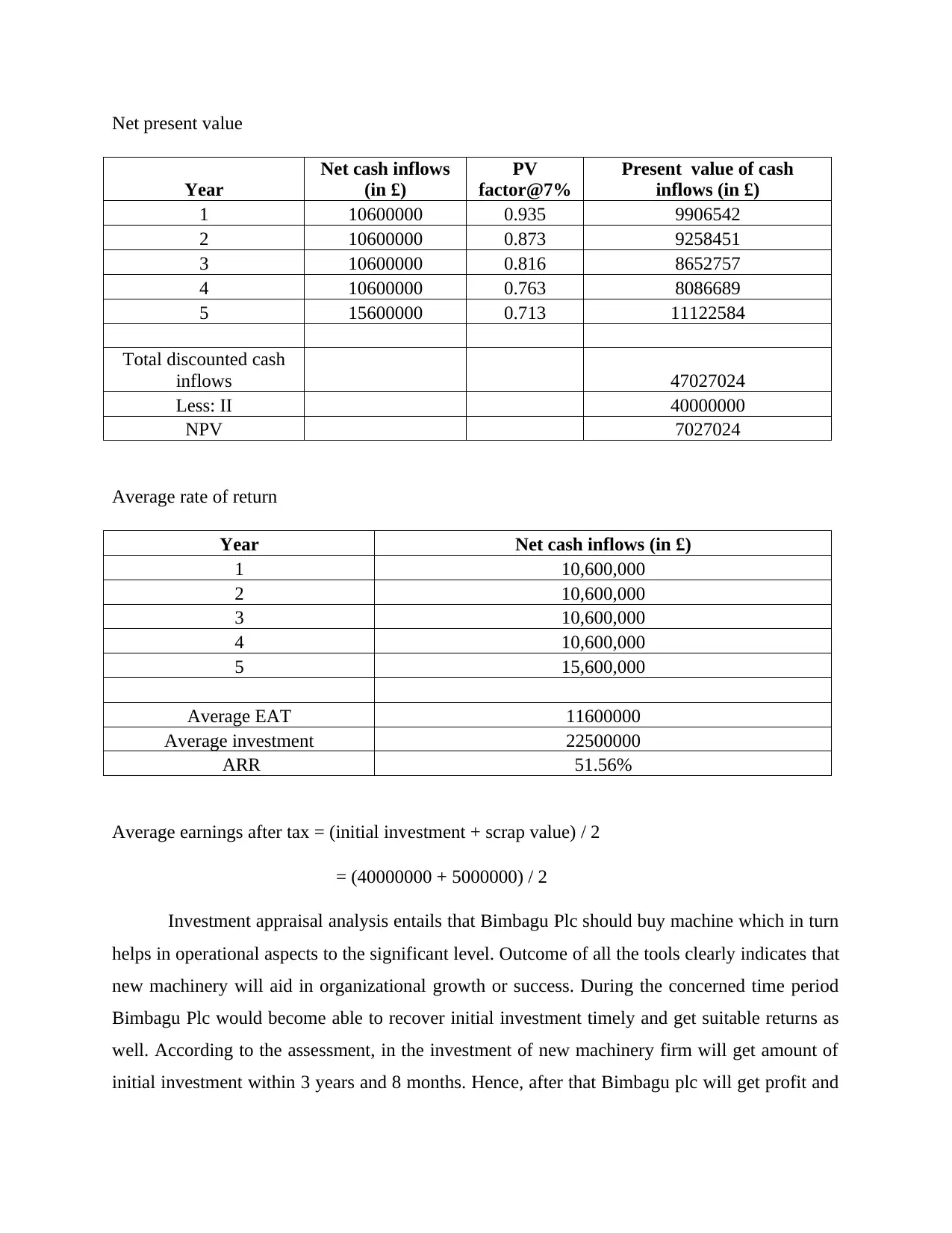

Year

Net cash inflows

(in £)

PV

factor@7%

Present value of cash

inflows (in £)

1 10600000 0.935 9906542

2 10600000 0.873 9258451

3 10600000 0.816 8652757

4 10600000 0.763 8086689

5 15600000 0.713 11122584

Total discounted cash

inflows 47027024

Less: II 40000000

NPV 7027024

Average rate of return

Year Net cash inflows (in £)

1 10,600,000

2 10,600,000

3 10,600,000

4 10,600,000

5 15,600,000

Average EAT 11600000

Average investment 22500000

ARR 51.56%

Average earnings after tax = (initial investment + scrap value) / 2

= (40000000 + 5000000) / 2

Investment appraisal analysis entails that Bimbagu Plc should buy machine which in turn

helps in operational aspects to the significant level. Outcome of all the tools clearly indicates that

new machinery will aid in organizational growth or success. During the concerned time period

Bimbagu Plc would become able to recover initial investment timely and get suitable returns as

well. According to the assessment, in the investment of new machinery firm will get amount of

initial investment within 3 years and 8 months. Hence, after that Bimbagu plc will get profit and

& £7027024 respectively. On the basis of investment appraisal tools business unit should give

priority to the project which has higher NPV and ARR (Baum, Crosby and Devaney, 2021).

Further, NPV method presents solution by taking into account time value of money concept.

Hence, by keeping all the aspects in mind it can be stated that investment opportunity is viable

from quantitative perspective.

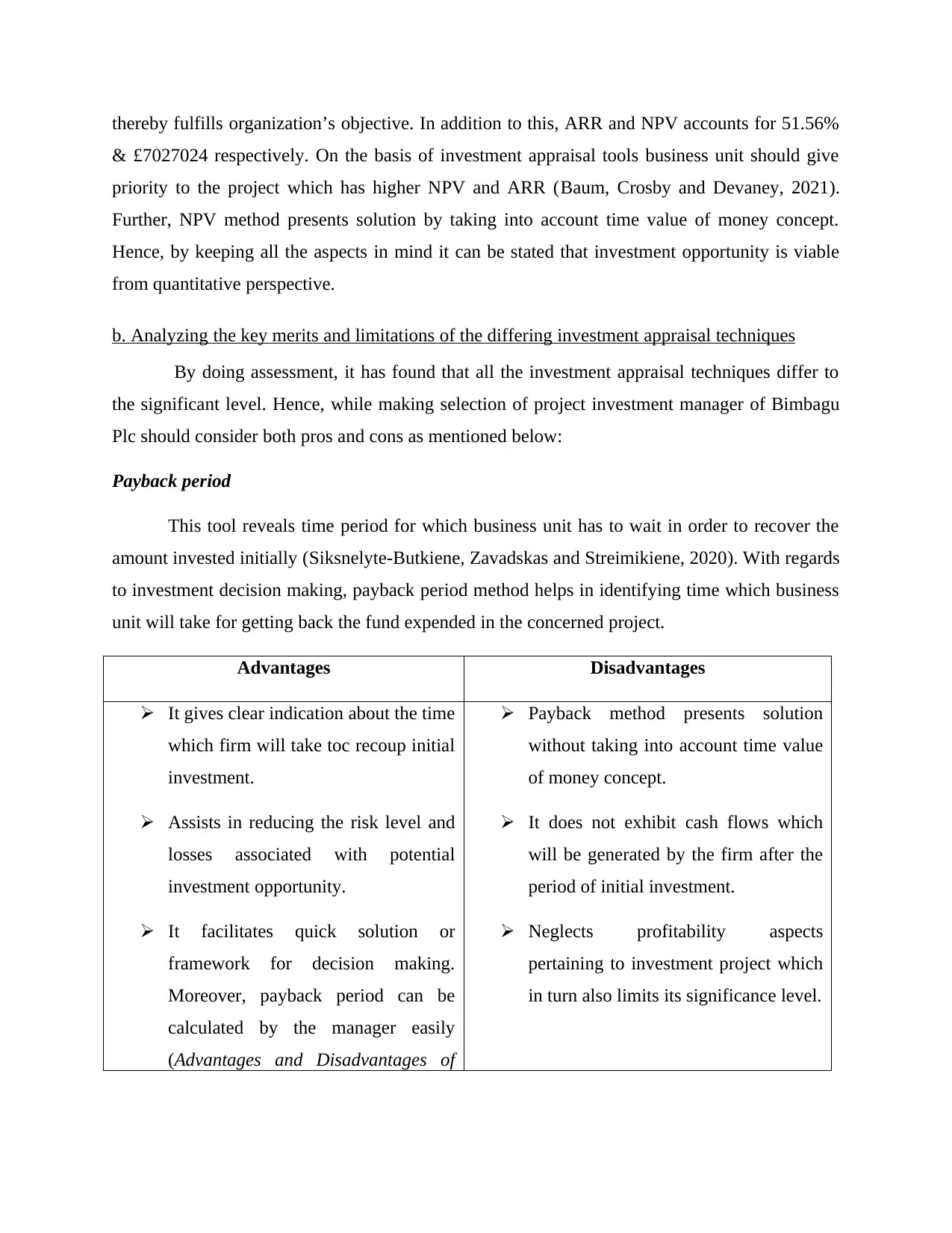

b. Analyzing the key merits and limitations of the differing investment appraisal techniques

By doing assessment, it has found that all the investment appraisal techniques differ to

the significant level. Hence, while making selection of project investment manager of Bimbagu

Plc should consider both pros and cons as mentioned below:

Payback period

This tool reveals time period for which business unit has to wait in order to recover the

amount invested initially (Siksnelyte-Butkiene, Zavadskas and Streimikiene, 2020). With regards

to investment decision making, payback period method helps in identifying time which business

unit will take for getting back the fund expended in the concerned project.

Advantages Disadvantages

It gives clear indication about the time

which firm will take toc recoup initial

investment.

Assists in reducing the risk level and

losses associated with potential

investment opportunity.

It facilitates quick solution or

framework for decision making.

Moreover, payback period can be

calculated by the manager easily

(Advantages and Disadvantages of

Payback method presents solution

without taking into account time value

of money concept.

It does not exhibit cash flows which

will be generated by the firm after the

period of initial investment.

Neglects profitability aspects

pertaining to investment project which

in turn also limits its significance level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

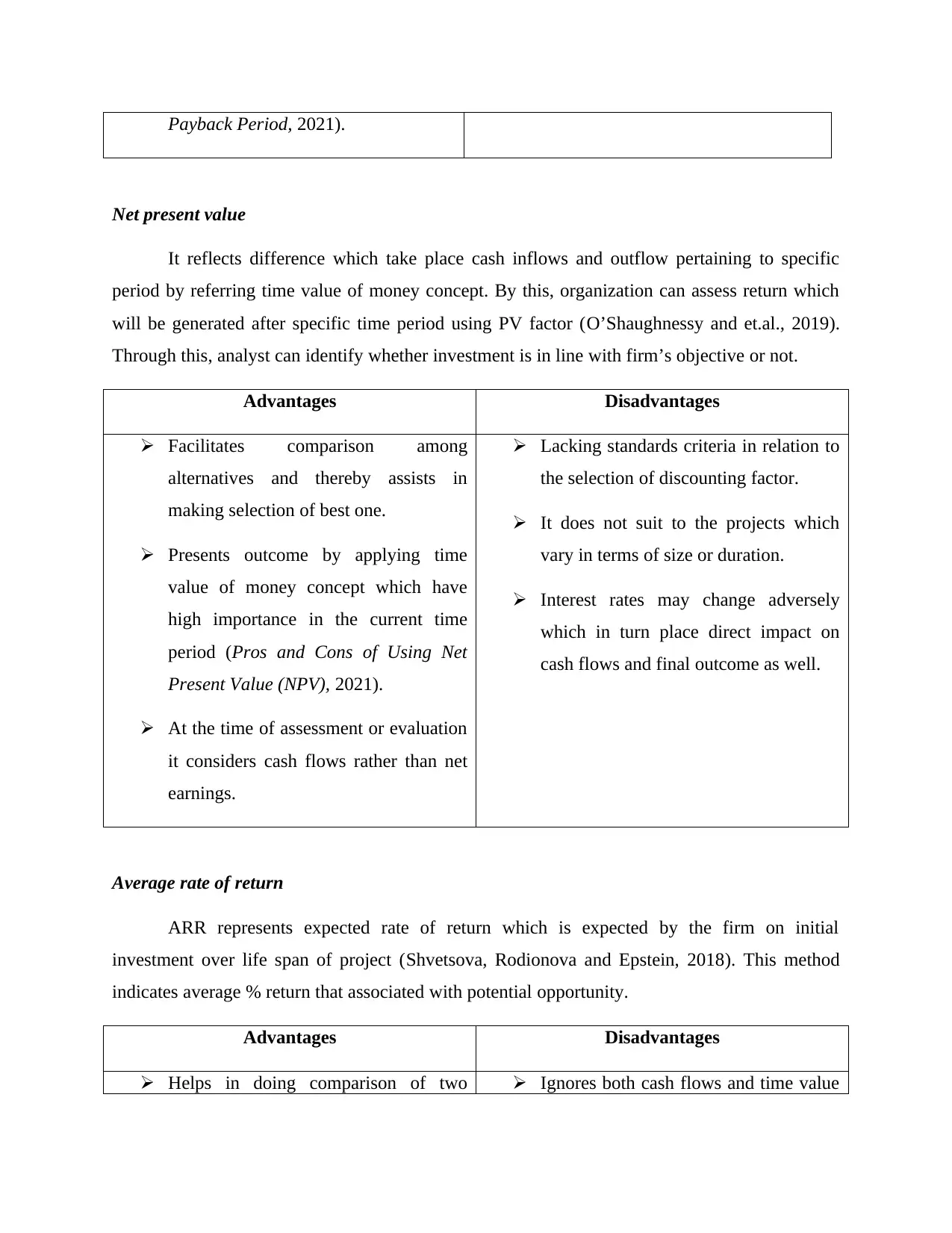

Net present value

It reflects difference which take place cash inflows and outflow pertaining to specific

period by referring time value of money concept. By this, organization can assess return which

will be generated after specific time period using PV factor (O’Shaughnessy and et.al., 2019).

Through this, analyst can identify whether investment is in line with firm’s objective or not.

Advantages Disadvantages

Facilitates comparison among

alternatives and thereby assists in

making selection of best one.

Presents outcome by applying time

value of money concept which have

high importance in the current time

period (Pros and Cons of Using Net

Present Value (NPV), 2021).

At the time of assessment or evaluation

it considers cash flows rather than net

earnings.

Lacking standards criteria in relation to

the selection of discounting factor.

It does not suit to the projects which

vary in terms of size or duration.

Interest rates may change adversely

which in turn place direct impact on

cash flows and final outcome as well.

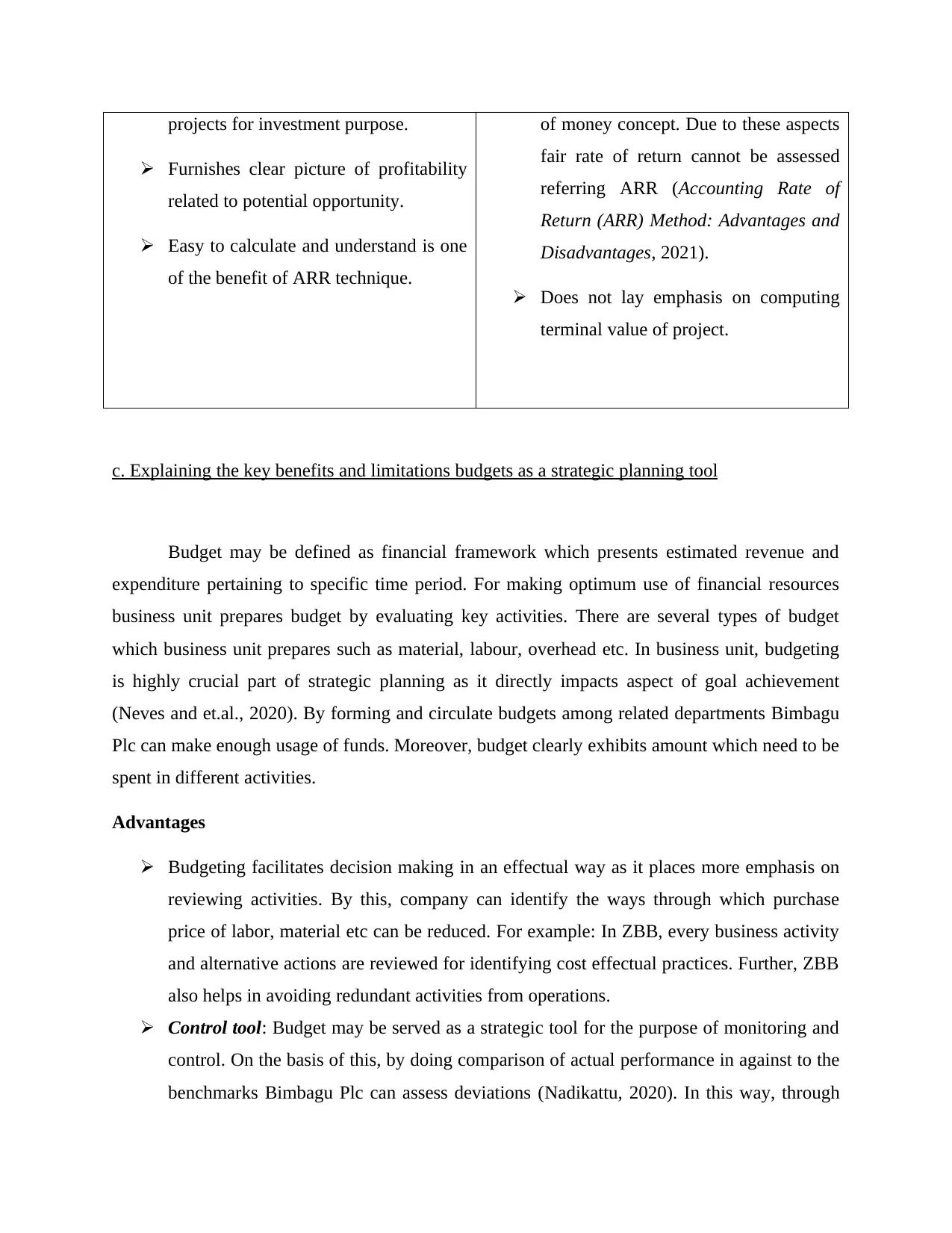

Average rate of return

ARR represents expected rate of return which is expected by the firm on initial

investment over life span of project (Shvetsova, Rodionova and Epstein, 2018). This method

indicates average % return that associated with potential opportunity.

Advantages Disadvantages

Helps in doing comparison of two Ignores both cash flows and time value

Paraphrase This Document

Furnishes clear picture of profitability

related to potential opportunity.

Easy to calculate and understand is one

of the benefit of ARR technique.

of money concept. Due to these aspects

fair rate of return cannot be assessed

referring ARR (Accounting Rate of

Return (ARR) Method: Advantages and

Disadvantages, 2021).

Does not lay emphasis on computing

terminal value of project.

c. Explaining the key benefits and limitations budgets as a strategic planning tool

Budget may be defined as financial framework which presents estimated revenue and

expenditure pertaining to specific time period. For making optimum use of financial resources

business unit prepares budget by evaluating key activities. There are several types of budget

which business unit prepares such as material, labour, overhead etc. In business unit, budgeting

is highly crucial part of strategic planning as it directly impacts aspect of goal achievement

(Neves and et.al., 2020). By forming and circulate budgets among related departments Bimbagu

Plc can make enough usage of funds. Moreover, budget clearly exhibits amount which need to be

spent in different activities.

Advantages

Budgeting facilitates decision making in an effectual way as it places more emphasis on

reviewing activities. By this, company can identify the ways through which purchase

price of labor, material etc can be reduced. For example: In ZBB, every business activity

and alternative actions are reviewed for identifying cost effectual practices. Further, ZBB

also helps in avoiding redundant activities from operations.

Control tool: Budget may be served as a strategic tool for the purpose of monitoring and

control. On the basis of this, by doing comparison of actual performance in against to the

benchmarks Bimbagu Plc can assess deviations (Nadikattu, 2020). In this way, through

Besides this, variance results also help in setting bonus and incentive plan for personnel

appropriately.

Smooth business functioning: Budgeting helps in performing business operations and

functions smoothly as all the departments of business units have clear idea about

expenditure as well as revenue sources. Through this, Bimbagu Plc can make control

over unnecessary expenses and thereby improves resource utilization.

Effectual assessment of profitability: With the help of budgeting company can make

proper assessment of profitability aspect and thereby would become able to do further

planning (The Advantages and Disadvantages of Budgeting, 2021). It provides high level

of assistance to Bimabgu Plc in identifying the extent to which particular product or

service is profitable. On the basis of such analysis management team can make decision

about product or services which need to be dropped.

Assist in planning about funding: Company can do significant planning about funding

by taking into account budgeting process. Moreover, it clearly entails fund which

business unit has as working capital and for investment purpose as well. By reviewing

this, Bimbagu Plc can find fund which firm need to raise for meeting capital requirement.

Disadvantage

It may cause of demotivation among employees if business unit fails to set appropriate

budgeting framework referring inflationary conditions. Moreover, results of variance

analysis are highly depends on budget setting down by higher authority (Petera and

Šoljaková, 2020). In the case of higher variances employees feel demotivated and their

performance affected adversely.

Budgeting is highly time intensive exercise as financial analyst need to collect

information from several departments.

Along with this, budgeting practice is costly because now management team uses

software for the formation of financial framework. If Bimbagu Plc does not have skilled

workforce then it may result into inappropriate framework.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

appropriate in every situation (Falqueto and et.al., 2020). This aspect limits the

significance of budgeting as a tool for strategic planning and development.

Hence, by considering overall evaluation it can be said that budgeting helps in evaluating

revenue, expenses and profitability in the best possible way. By this, firm can take prominent

decisions for business success.

CONCLUSION

By summing up this report, it has been articulated that financial statements clearly exhibit

profitability position of firm pertaining to specific time period. Business unit can evaluate

financial position and performance by preparing financial statements at the end of accounting

period. Besides this, it can be inferred from the evaluation that break-even analysis technique is

highly significant for Fidel & Ana limited. Moreover, it helps firm in taking appropriate

decisions about manufacturing, sales and profitability aspect. Along with this, it can be

mentioned that BEP analysis considers several assumption regarding revenue, cost, quantity etc.

Hence, at the time of applying BEP technique business unit should take into account its

limitations as well. It can be summarized that investment appraisal techniques help in evaluating

option from several perspectives such time duration, return in both percentage and numeric

format. On the basis of analysis, Bimbagu Plc should buy machine for business expansion and

goals achievement. The rationale behind this, through using machinery firm will get positive

returns and recoup investment within suitable time period.

Paraphrase This Document

Books and Journals

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Falqueto, J. M. Z. and et.al., 2020. Strategic planning in higher education institutions: what are

the stakeholders’ roles in the process?. Higher Education. 79(6). pp.1039-1056.

Fuksa, D., 2021. Innovative Method for Calculating the Break-Even for Multi-Assortment

Production. Energies. 14(14). p.4213.

Kravchyk, K. V., Okur, F. and Kovalenko, M. V., 2021. Break-Even Analysis of All-Solid-State

Batteries with Li-Garnet Solid Electrolytes. ACS Energy Letters. 6. pp.2202-2207.

Nadikattu, R. R., 2020. Effective Innovation Management in Strategic Planning. Rahul Reddy

Nadikattu, INTERNATIONAL JOURNAL OF ENGINEERING, SCIENCE AND. 9(5). pp.106-

116.

Neves, M. F. and et.al., 2020. Strategic planning and management of food and agribusiness

chains: the chainplan method (framework). Revista Brasileira de Gestão de Negócios. 21.

pp.628-646.

O’Shaughnessy, S. A. and et.al., 2019. Identifying advantages and disadvantages of variable rate

irrigation: An updated review. Applied Engineering in Agriculture. 35(6). pp.837-852.

Petera, P. and Šoljaková, L., 2020. Use of strategic management accounting techniques by

companies in the Czech Republic. Economic research-ekonomska istraživanja. 33(1). pp.46-

67.

Shvetsova, O. A., Rodionova, E. A. and Epstein, M. Z., 2018. Evaluation of investment projects

under uncertainty: multi-criteria approach using interval data. Entrepreneurship and

Sustainability Issues. 5(4). pp.914-928.

Siksnelyte-Butkiene, I., Zavadskas, E. K. and Streimikiene, D., 2020. Multi-criteria decision-

making (MCDM) for the assessment of renewable energy technologies in a household: A

review. Energies. 13(5). p.1164.

Enterprises. International Journal of Research-Granthaalayah. 8(6).

Tanco, M., Cat, L. and Garat, S., 2019. A break-even analysis for battery electric trucks in Latin

America. Journal of Cleaner Production. 228. pp.1354-1367.

Tannen, M. B., 2020. Introducing Learning by Doing into Ite Break-Even Analysis

Model. Journal of Accounting and Finance. 20(3). pp.11-19.

Online

Accounting Rate of Return (ARR) Method: Advantages and Disadvantages. 2021. Online.

Available through: < https://accountlearning.com/accounting-rate-of-return-method-

advantages-disadvantages/>.

Advantages and Disadvantages of Payback Period. 2021. Online. Available through: <

https://efinancemanagement.com/investment-decisions/advantages-and-disadvantages-of-

payback-period>.

Pros and Cons of Using Net Present Value (NPV). 2021. Online. Available through: <

https://forisk.com/blog/2020/05/31/pros-and-cons-of-using-net-present-value-npv/>.

The Advantages and Disadvantages of Budgeting. 2021. Online. Available through: <

https://www.mbaknol.com/financial-management/the-advantages-and-disadvantages-of-

budgeting/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.