Comprehensive Report on Accounting and Finance for Business

VerifiedAdded on 2023/06/18

|21

|2478

|307

Report

AI Summary

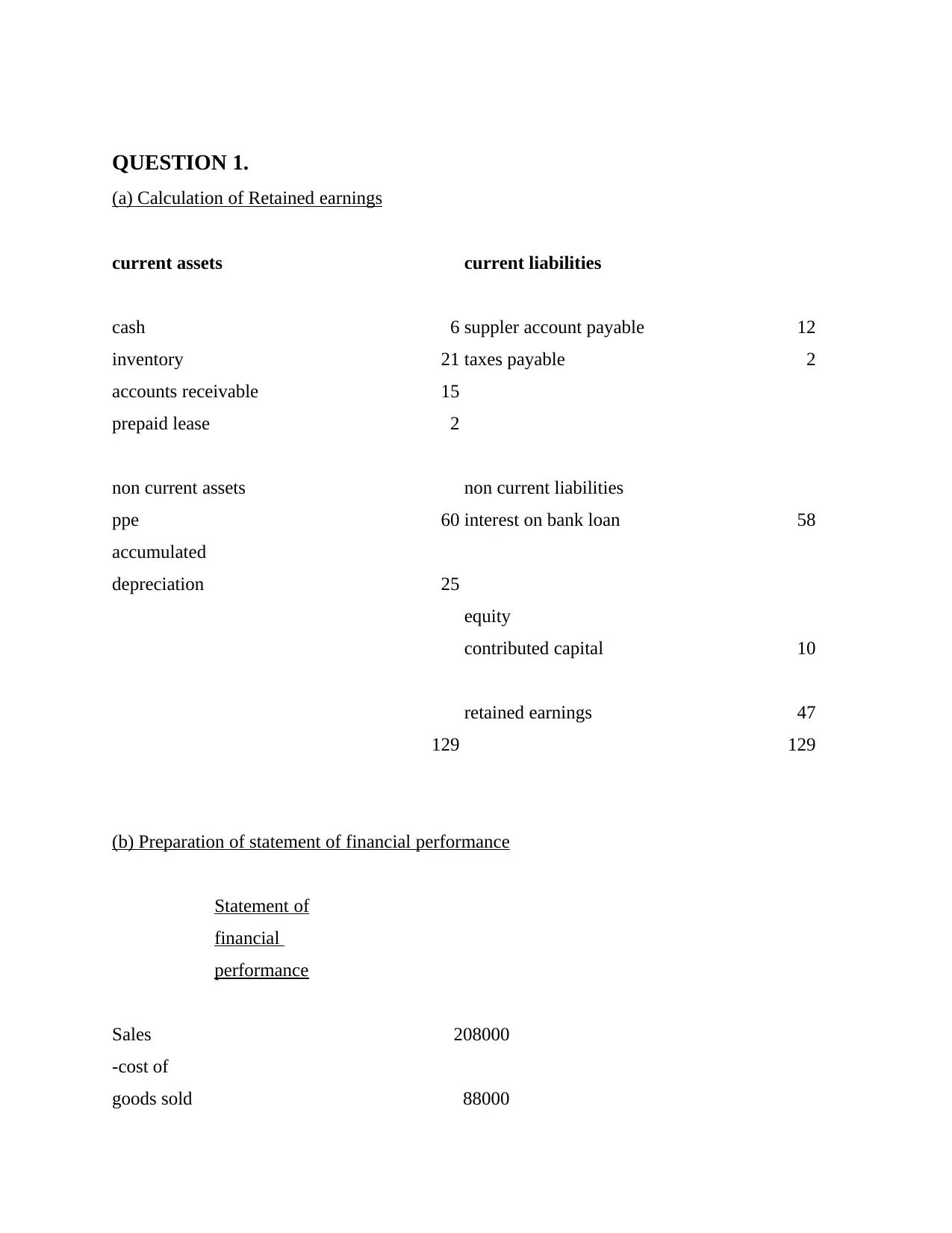

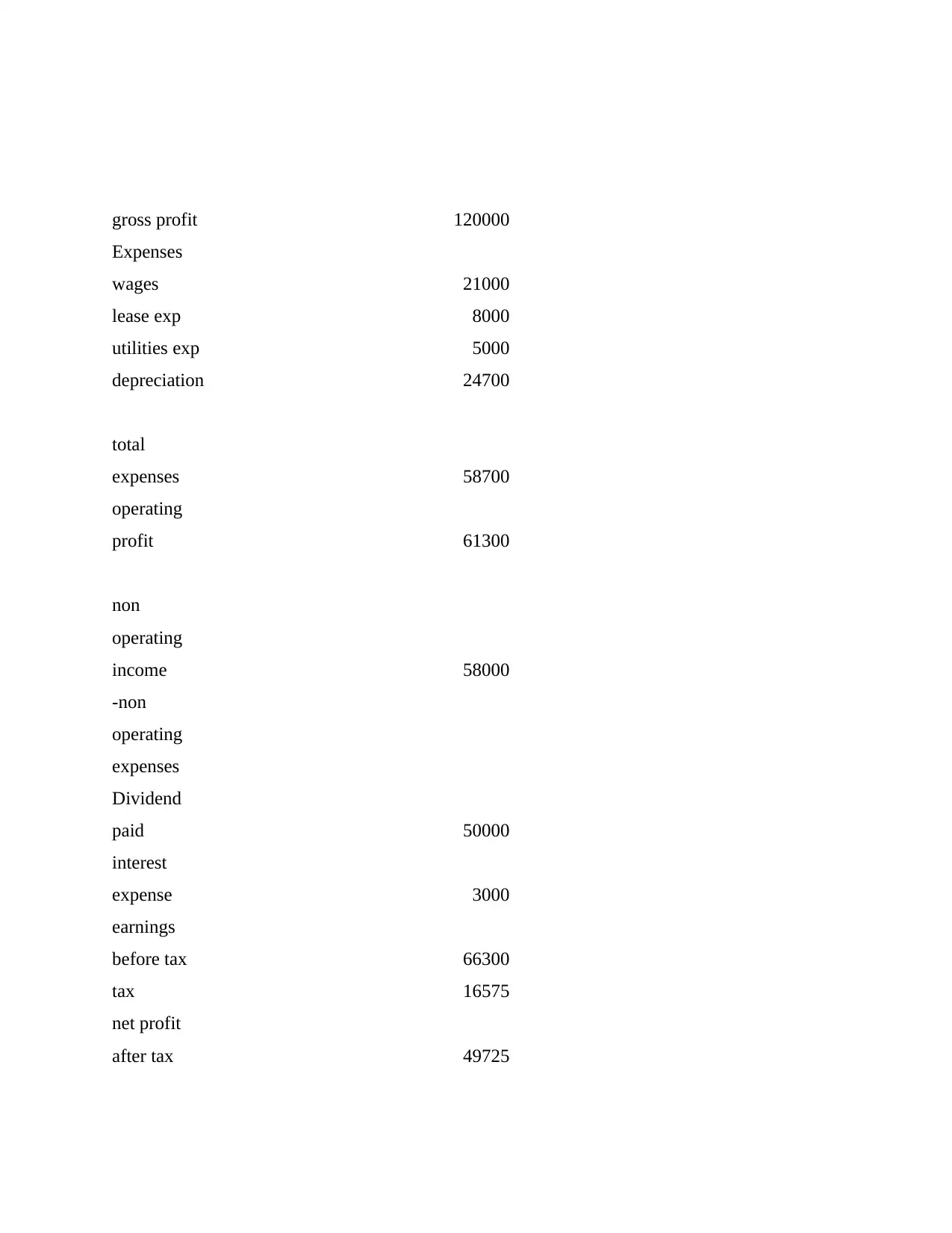

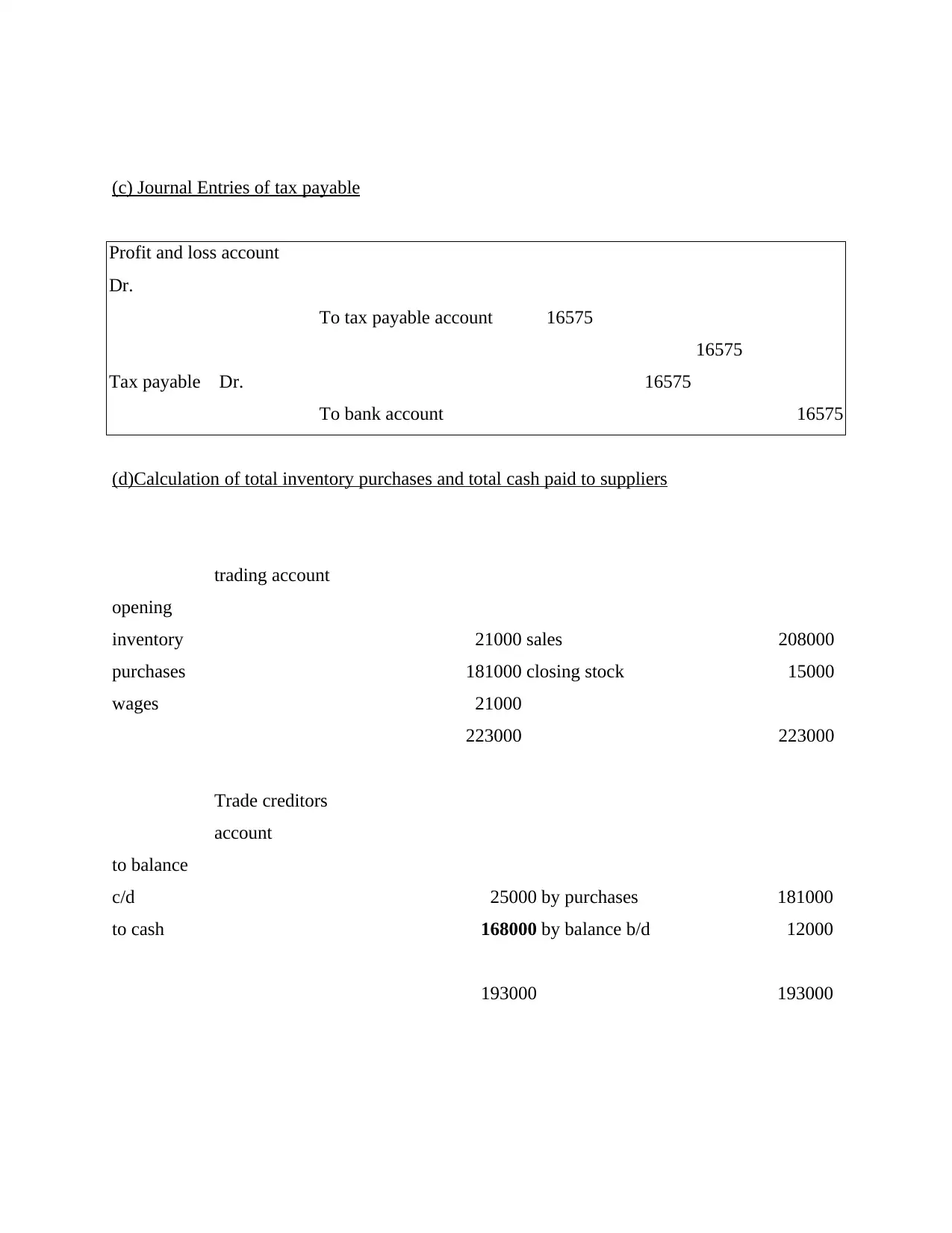

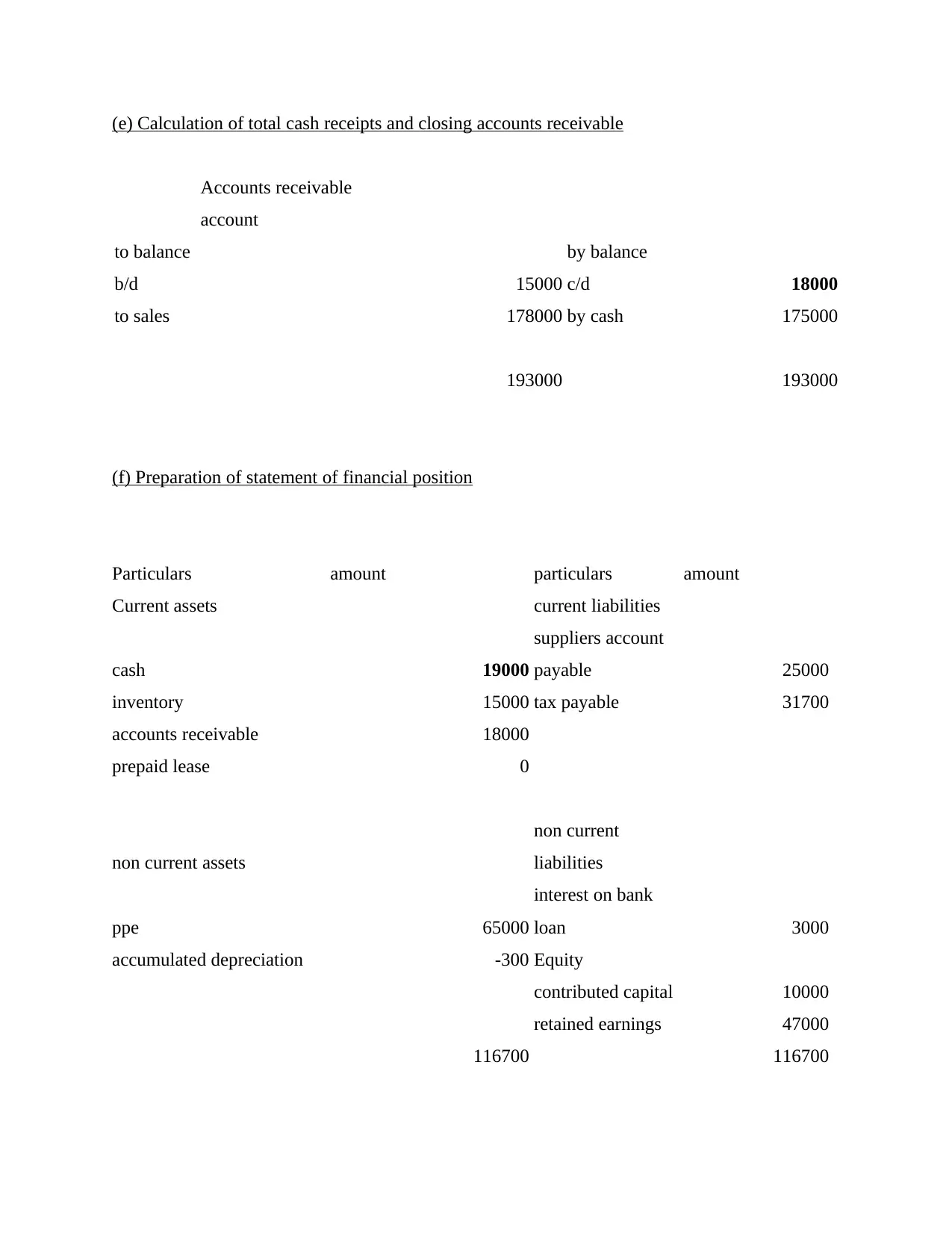

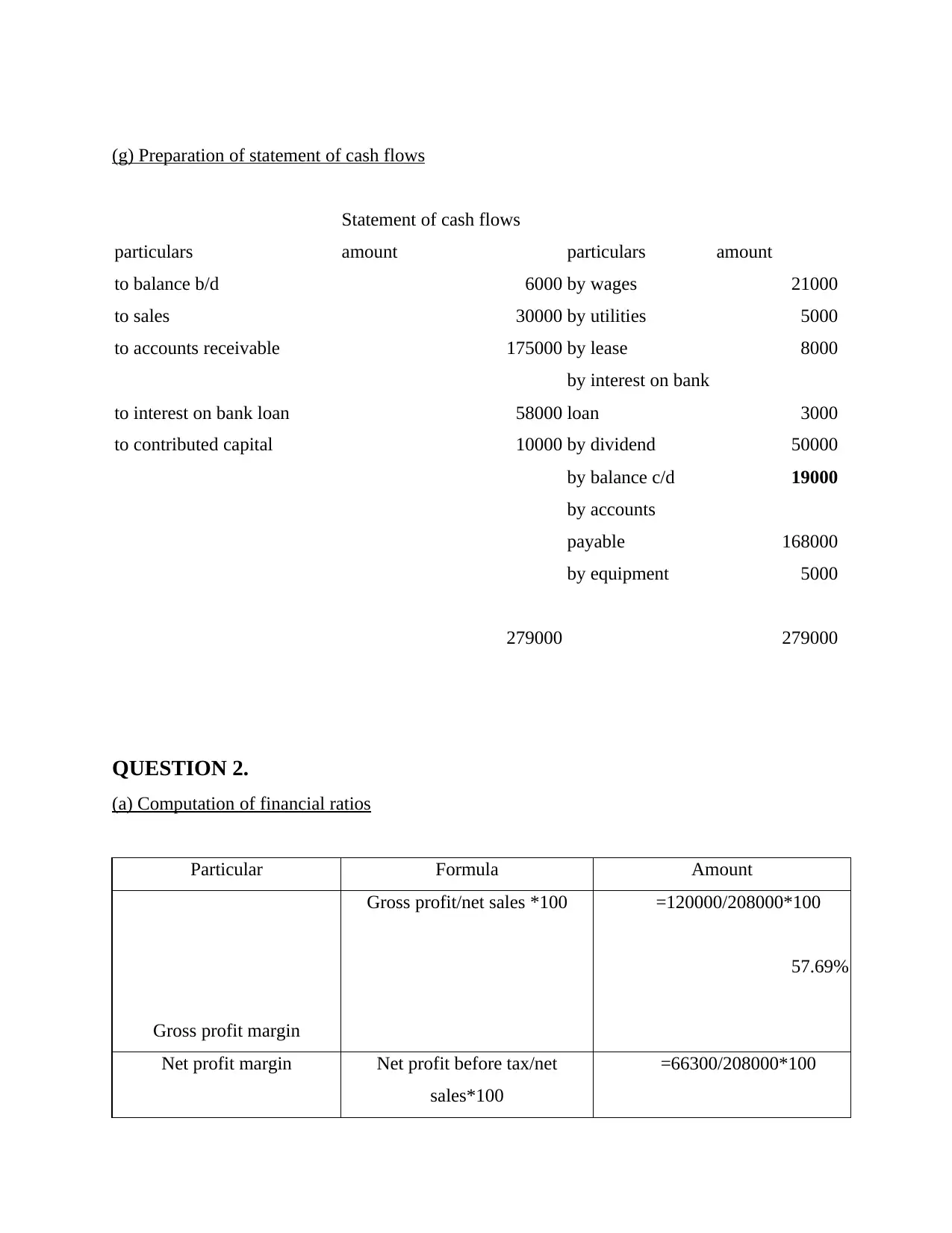

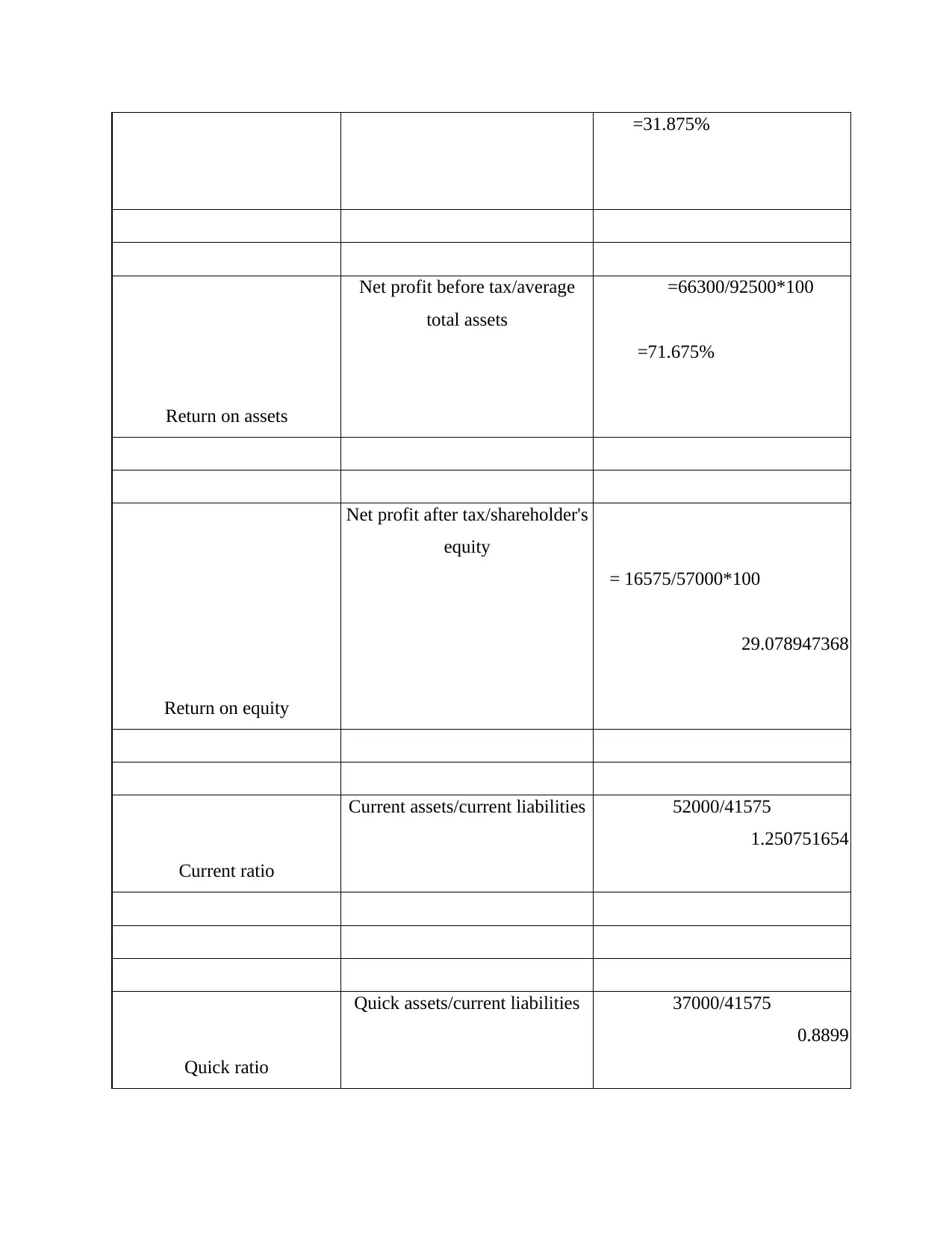

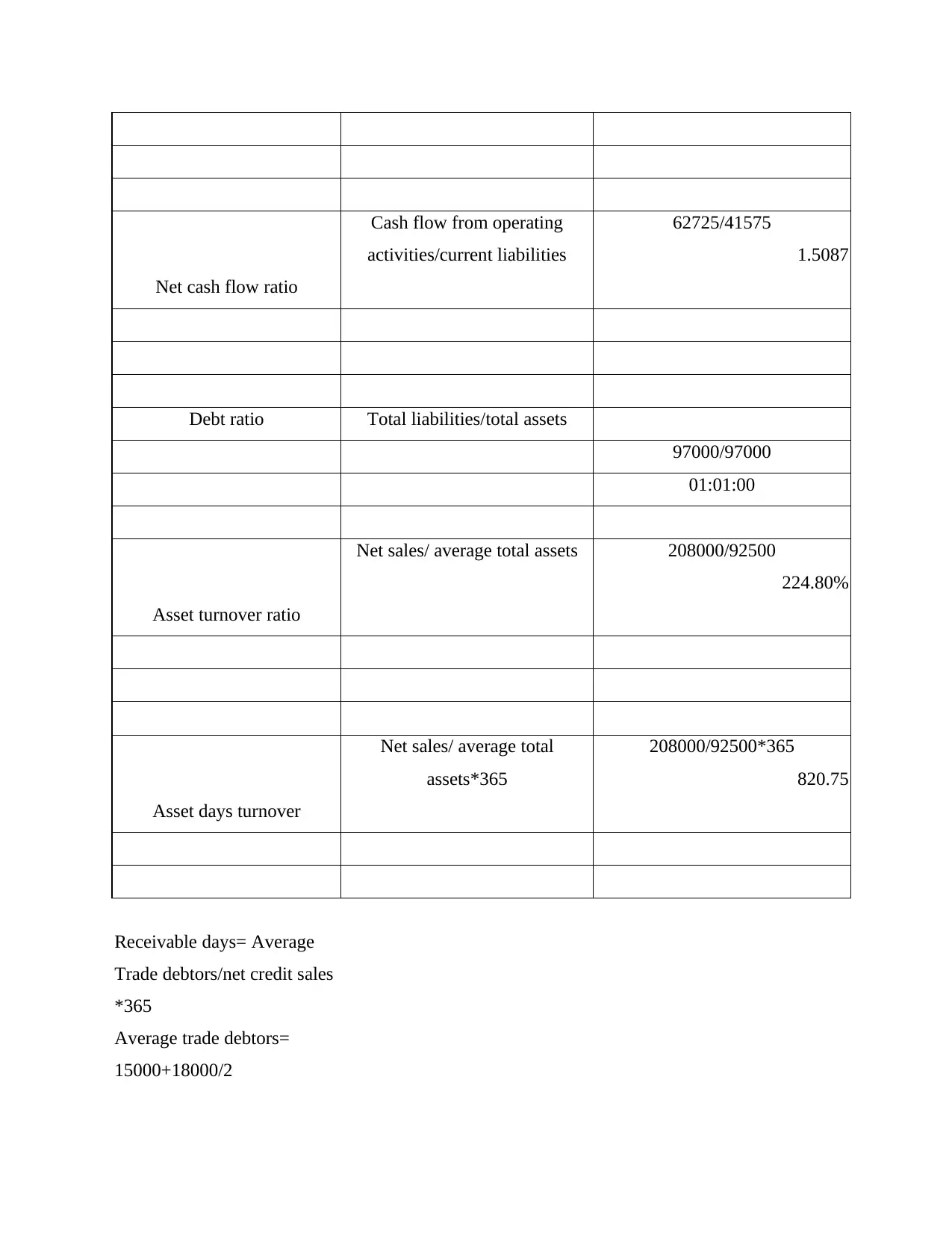

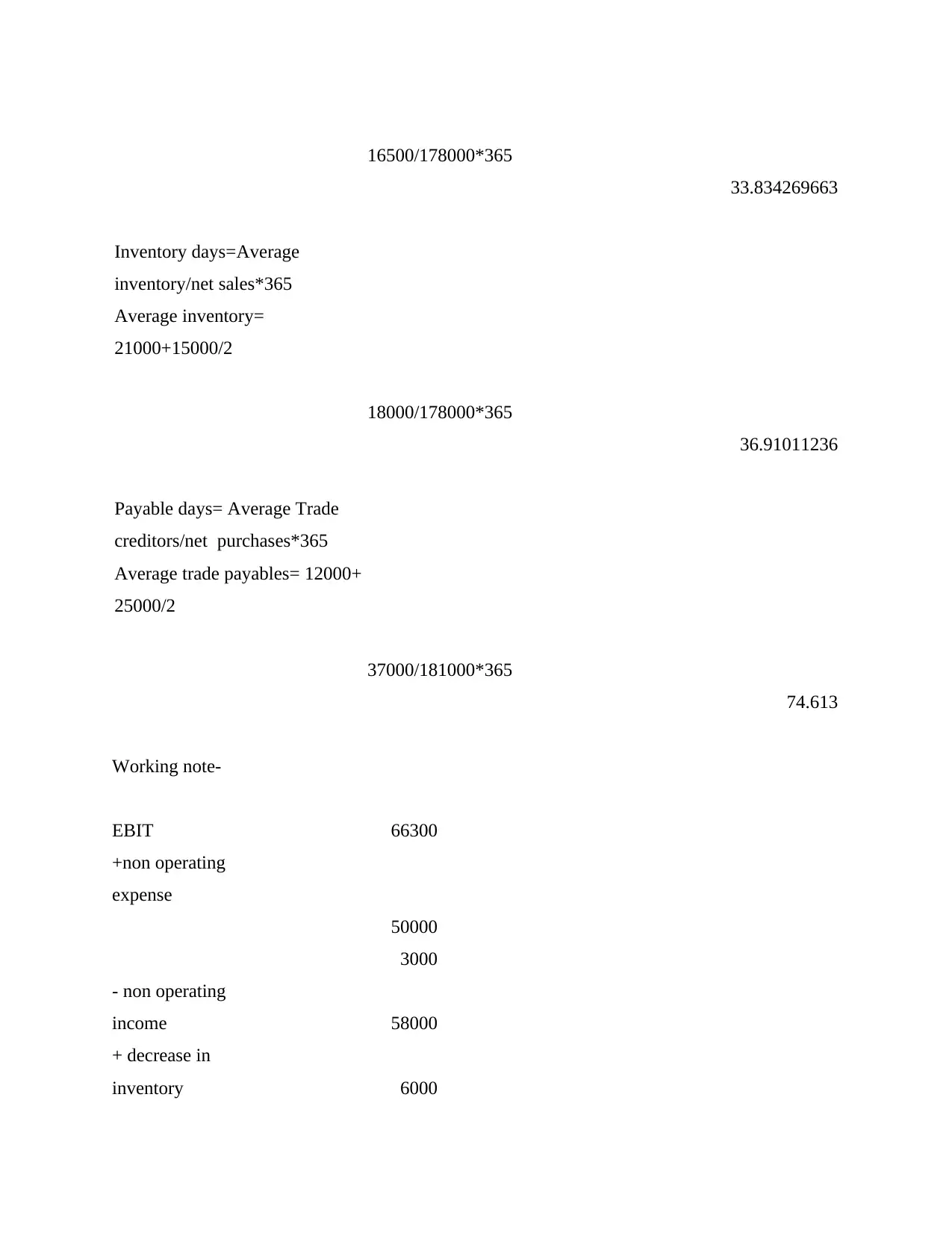

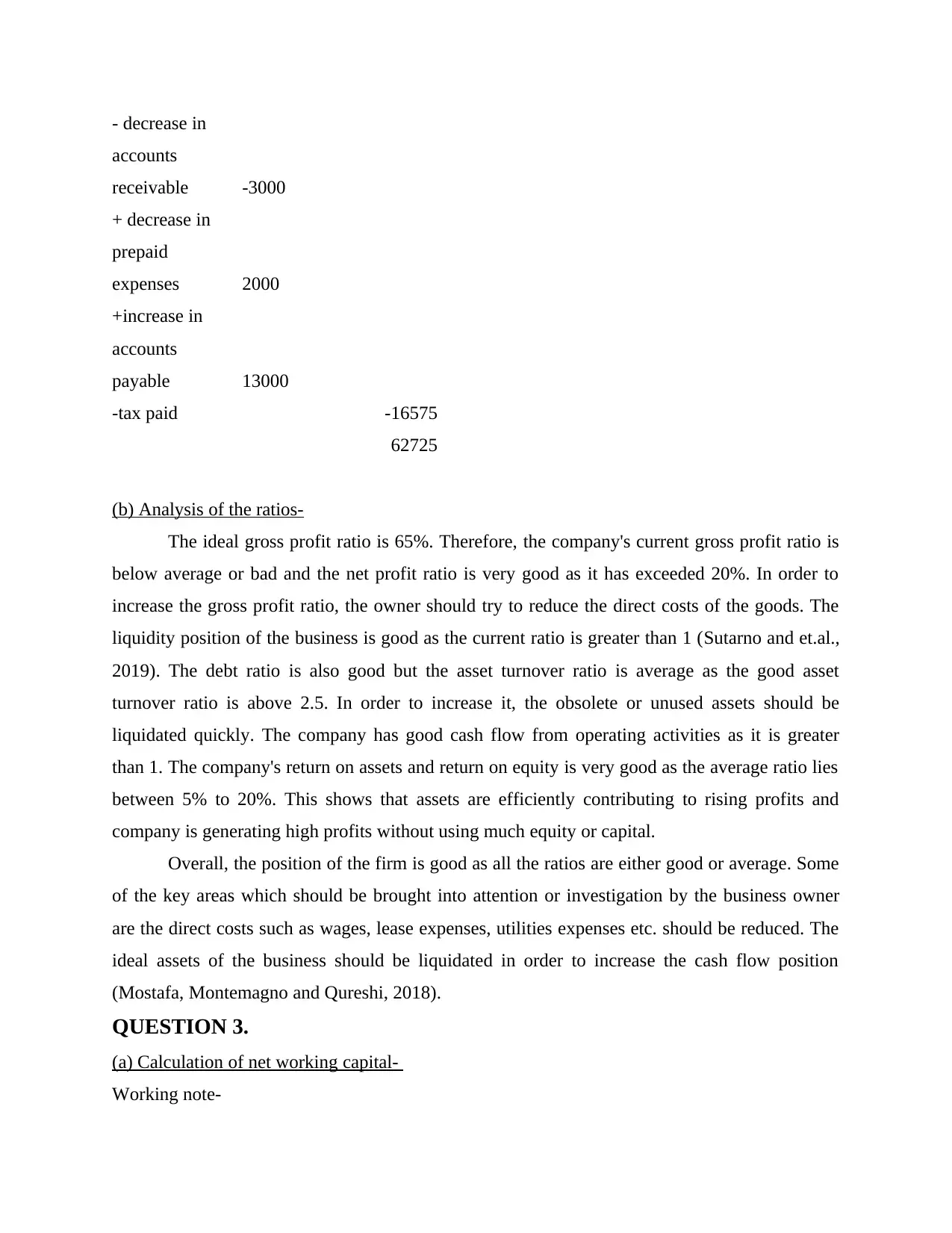

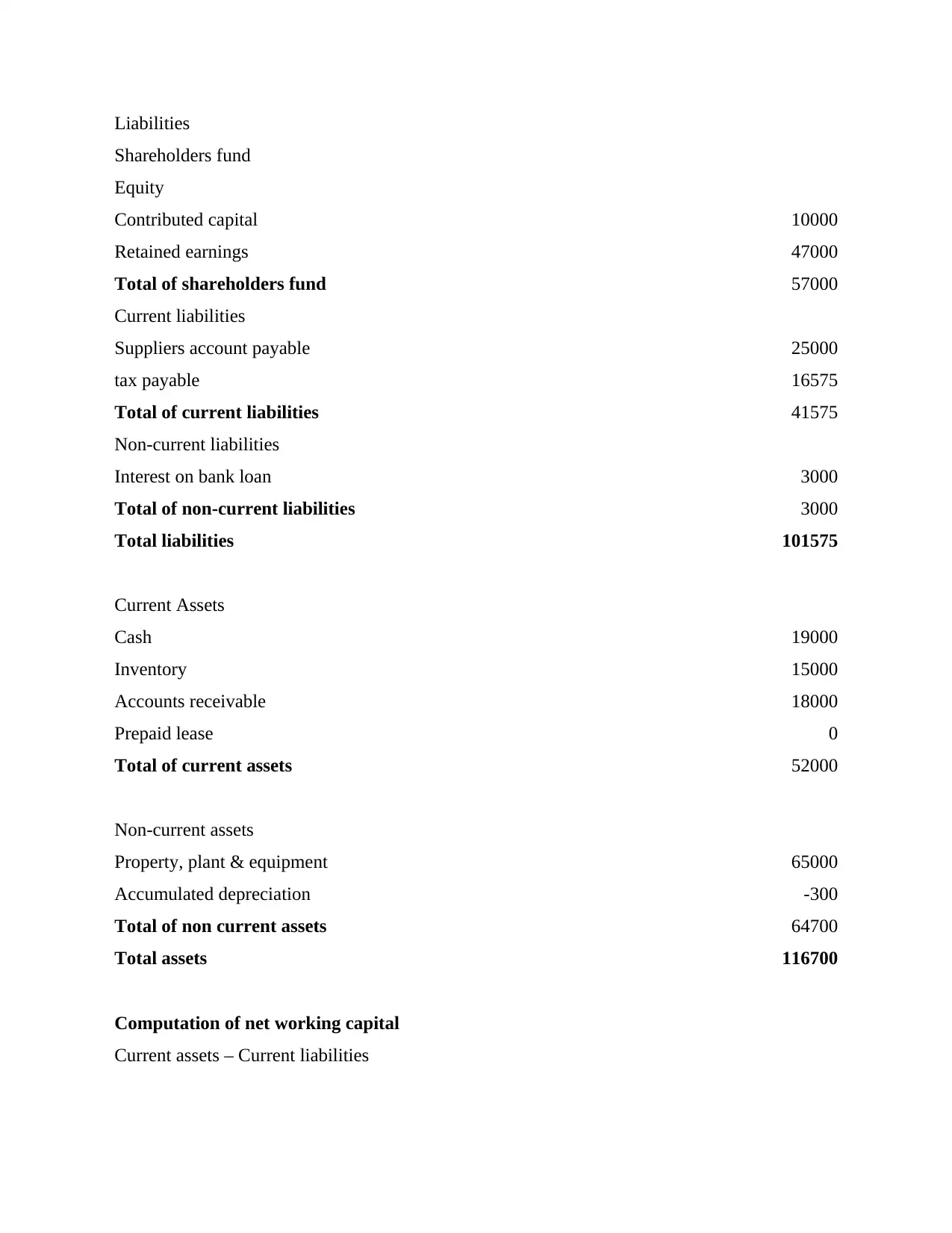

This report provides a comprehensive analysis of accounting and finance for a business, covering various aspects such as the calculation of retained earnings, preparation of the statement of financial performance and cash flows, and journal entries for tax payable. It includes detailed calculations of total inventory purchases, cash paid to suppliers, total cash receipts, and closing accounts receivable. The report also computes and analyzes financial ratios like gross profit margin, net profit margin, return on assets, and debt ratio, offering insights into the company's financial health. Furthermore, it calculates net working capital, cash cycle, and constructs a monthly cash budget. The analysis extends to contribution margin, break-even point, and net present value at different interest rates, providing recommendations for strategic initiatives. Finally, the report evaluates the accounting rate of return and payback period for investment decisions.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.