Capital Budgeting for Saturn Petcare & ARB Corp Financial Report

VerifiedAdded on 2023/06/14

|20

|4073

|475

Report

AI Summary

This report analyzes Saturn Petcare Australia and New Zealand's project selection between Bathurst and Wodonga, recommending Wodonga based on NPV, payback period, and profitability index. It also examines ARB Corporation Limited's capital structure, noting its 100% equity financing, calculates its WACC and CAPM, and compares it with competitor Bell Equipment Limited. Key financial ratios of ARB Corporation are analyzed, revealing declining liquidity and return on equity, alongside an increasing debt-equity ratio. The report concludes with recommendations for ARB Corporation to improve its capital structure, focus on shareholder wealth maximization, and maintain liquidity, highlighting that Desklib provides access to similar solved assignments and study resources.

0ACCOUNTING AND FINANCE

Accounting and Finance

Student Name

University Name

Accounting and Finance

Student Name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Answer to Part A.........................................................................................................................3

Selection among the projects...........................................................................................................3

Product Cannibalization...................................................................................................................4

Capital budgeting options available to compensate excess sales....................................................4

Original value of the vacant Wodonga to be considered or not......................................................4

Answer to Part B..............................................................................................................................5

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................5

Answer to 2i)...................................................................................................................................5

Current capital structure of the firm ARB Corporation Limited.....................................................5

WACC of the organization ARB Corporation Limited...................................................................6

CAPM..............................................................................................................................................6

Answer to 2ii) Comparison of the capital structure of ARB Corporation Limited with its

competitor........................................................................................................................................6

Answer to 2iii) Analysis of Key Financial Ratios of ARB Corporation Limited...........................6

Answer to 2iv): ARB Corporation Limited capital structure comparison over the years...............8

Answer to 2v) Maximizing wealth for shareholders.......................................................................9

Table of Contents

Answer to Part A.........................................................................................................................3

Selection among the projects...........................................................................................................3

Product Cannibalization...................................................................................................................4

Capital budgeting options available to compensate excess sales....................................................4

Original value of the vacant Wodonga to be considered or not......................................................4

Answer to Part B..............................................................................................................................5

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................5

Answer to 2i)...................................................................................................................................5

Current capital structure of the firm ARB Corporation Limited.....................................................5

WACC of the organization ARB Corporation Limited...................................................................6

CAPM..............................................................................................................................................6

Answer to 2ii) Comparison of the capital structure of ARB Corporation Limited with its

competitor........................................................................................................................................6

Answer to 2iii) Analysis of Key Financial Ratios of ARB Corporation Limited...........................6

Answer to 2iv): ARB Corporation Limited capital structure comparison over the years...............8

Answer to 2v) Maximizing wealth for shareholders.......................................................................9

2ACCOUNTING AND FINANCE

Answer to 2vi) Conclusion and recommendations..........................................................................9

References......................................................................................................................................10

Appendices................................................................................................................................11

Answer to 2vi) Conclusion and recommendations..........................................................................9

References......................................................................................................................................10

Appendices................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

Answer to Part A

Selection among the projects

In the given case study, the organization Saturn Petcare Australia and New Zealand has

two alternative projects to be selected. The Demand and Strategy Finance director of the

organization, Nathan Quinlivan want to select one of the two projects based on capital budgeting

analysis. The major findings from both the projects is as follows:-

Important Information

Two projects to be considered Bathurst and Wodonga

Sales Growth Rate 10%

Margin After conversion Rate 30%

Expected Return on Investment 22%

Initial Investment $27,500,000

Expected life 10years

Existing dry food factory for Bathurst 8000000

Table 1: Key information about the projects

The calculation of capital budgeting for both the projects has been shown in Appendix 1.

From the calculation, it can be inferred that, the organization needs to select Wodonga project for

their new manufacturing production line. Firstly, net project value (NPV) of the project is

$9,594,827 while in case of Bathurst, NPV is just $5,844,567. In addition to this, payback period

for Wodonga project is 3.45, while in case of Bathurst, it is 3.86. Similarly, profitability index

for Wodonga is 1.35, while in case of Bathurst, it is 1.18. Therefore, it can be inferred that

Wodonga project will be more profitable for Saturn as it can recover its initial investment of 27.5

million quickly than in case of Bathurst. Appendix 1 also reflects after tax cash flows of both the

projects. The detailed summary is as follows:-

Answer to Part A

Selection among the projects

In the given case study, the organization Saturn Petcare Australia and New Zealand has

two alternative projects to be selected. The Demand and Strategy Finance director of the

organization, Nathan Quinlivan want to select one of the two projects based on capital budgeting

analysis. The major findings from both the projects is as follows:-

Important Information

Two projects to be considered Bathurst and Wodonga

Sales Growth Rate 10%

Margin After conversion Rate 30%

Expected Return on Investment 22%

Initial Investment $27,500,000

Expected life 10years

Existing dry food factory for Bathurst 8000000

Table 1: Key information about the projects

The calculation of capital budgeting for both the projects has been shown in Appendix 1.

From the calculation, it can be inferred that, the organization needs to select Wodonga project for

their new manufacturing production line. Firstly, net project value (NPV) of the project is

$9,594,827 while in case of Bathurst, NPV is just $5,844,567. In addition to this, payback period

for Wodonga project is 3.45, while in case of Bathurst, it is 3.86. Similarly, profitability index

for Wodonga is 1.35, while in case of Bathurst, it is 1.18. Therefore, it can be inferred that

Wodonga project will be more profitable for Saturn as it can recover its initial investment of 27.5

million quickly than in case of Bathurst. Appendix 1 also reflects after tax cash flows of both the

projects. The detailed summary is as follows:-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

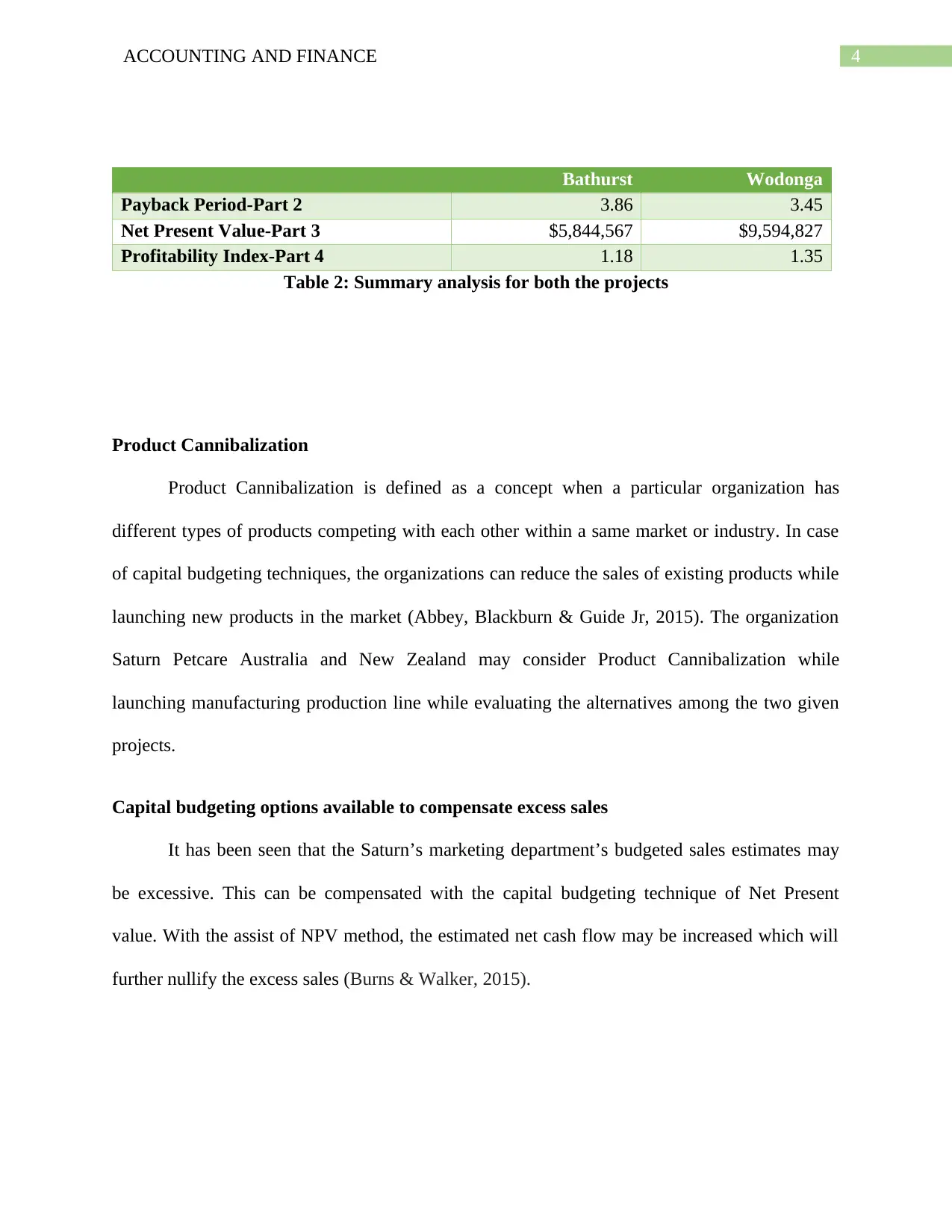

Bathurst Wodonga

Payback Period-Part 2 3.86 3.45

Net Present Value-Part 3 $5,844,567 $9,594,827

Profitability Index-Part 4 1.18 1.35

Table 2: Summary analysis for both the projects

Product Cannibalization

Product Cannibalization is defined as a concept when a particular organization has

different types of products competing with each other within a same market or industry. In case

of capital budgeting techniques, the organizations can reduce the sales of existing products while

launching new products in the market (Abbey, Blackburn & Guide Jr, 2015). The organization

Saturn Petcare Australia and New Zealand may consider Product Cannibalization while

launching manufacturing production line while evaluating the alternatives among the two given

projects.

Capital budgeting options available to compensate excess sales

It has been seen that the Saturn’s marketing department’s budgeted sales estimates may

be excessive. This can be compensated with the capital budgeting technique of Net Present

value. With the assist of NPV method, the estimated net cash flow may be increased which will

further nullify the excess sales (Burns & Walker, 2015).

Bathurst Wodonga

Payback Period-Part 2 3.86 3.45

Net Present Value-Part 3 $5,844,567 $9,594,827

Profitability Index-Part 4 1.18 1.35

Table 2: Summary analysis for both the projects

Product Cannibalization

Product Cannibalization is defined as a concept when a particular organization has

different types of products competing with each other within a same market or industry. In case

of capital budgeting techniques, the organizations can reduce the sales of existing products while

launching new products in the market (Abbey, Blackburn & Guide Jr, 2015). The organization

Saturn Petcare Australia and New Zealand may consider Product Cannibalization while

launching manufacturing production line while evaluating the alternatives among the two given

projects.

Capital budgeting options available to compensate excess sales

It has been seen that the Saturn’s marketing department’s budgeted sales estimates may

be excessive. This can be compensated with the capital budgeting technique of Net Present

value. With the assist of NPV method, the estimated net cash flow may be increased which will

further nullify the excess sales (Burns & Walker, 2015).

5ACCOUNTING AND FINANCE

Original value of the vacant Wodonga to be considered or not

It can be inferred that the Original value of the vacant Wodonga should not been taken

into consideration as the technique of capital budgeting (NPV) only considers costs related to

newly developed sites as initial investment (Brooks,2015). In addition to this, it can be also

inferred that if original value of the vacant Wodonga is included, then, the entire capital

budgeting analysis will be changed and completely wrong, as shown in Appendix 1B.

Answer to Part B

Executive Summary

The given report reflects about the structure of capital of the organization ARB Corporation

Limited. It has been found that the organization has given 100 percent weightage to

shareholder’s equity in its capital structure. However, there are several issues highlighted with

the organization. Based on which, certain recommendations have been suggested.

Introduction

The given report highlights about ARB Corporation Limited and its financial

performance over the years. It has been also compared with one of its competitors in terms of its

capital structure. Based on the analysis, suitable recommendations have been given.

Answer to 2i)

Current capital structure of the firm ARB Corporation Limited

From Appendix 2i, it can be inferred that the organization ARB Corporation Limited

gives 100 percent weightage to equity in its capital structure (Arb.com.au, 2018). There is no

Original value of the vacant Wodonga to be considered or not

It can be inferred that the Original value of the vacant Wodonga should not been taken

into consideration as the technique of capital budgeting (NPV) only considers costs related to

newly developed sites as initial investment (Brooks,2015). In addition to this, it can be also

inferred that if original value of the vacant Wodonga is included, then, the entire capital

budgeting analysis will be changed and completely wrong, as shown in Appendix 1B.

Answer to Part B

Executive Summary

The given report reflects about the structure of capital of the organization ARB Corporation

Limited. It has been found that the organization has given 100 percent weightage to

shareholder’s equity in its capital structure. However, there are several issues highlighted with

the organization. Based on which, certain recommendations have been suggested.

Introduction

The given report highlights about ARB Corporation Limited and its financial

performance over the years. It has been also compared with one of its competitors in terms of its

capital structure. Based on the analysis, suitable recommendations have been given.

Answer to 2i)

Current capital structure of the firm ARB Corporation Limited

From Appendix 2i, it can be inferred that the organization ARB Corporation Limited

gives 100 percent weightage to equity in its capital structure (Arb.com.au, 2018). There is no

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

sign of debt and therefore, it can be opined that the firm is not exposed to financial risk (Robb &

Robinson, 2014).

WACC of the organization ARB Corporation Limited

From the calculation shown in Appendix 2i, it can be inferred that WACC of ARB Corporation

Limited is 18.05 percent in 2017. In comparison with the previous two years, it can be deduced

that the cost of capital has decreased (19.01 percent in 2016 and 19.39 percent in 2015). This can

be taken as a good sign for the organization as the firm is being successful in minimizing the cost

of capital financing (Zeitun & Tian, 2014).

CAPM

From the calculation shown in Appendix 2i, it can be inferred that, the expected cost of equity is

coming to be 7.9 percent. This can be taken as a good sign for the organization as market rate of

return RM is more than the expected cost of equity (8.54 percent).

Answer to 2ii) Comparison of the capital structure of ARB Corporation Limited with its

competitor

The capital structure of the organization ARB Corporation Limited has been compared

with its competitor Bell Equipment Limited. In case of Bell Equipment Limited, the capital

structure of the firm is mixed of debt and equity (81 percent equity and 19 percent debt). The

total equity of the company is $3,657. While, in case of ARB Corporation Limited, the entire

capital structure is formed on the basis of equity and there is no sign of debt in capital structure.

The total equity of the firm is $272,341.

sign of debt and therefore, it can be opined that the firm is not exposed to financial risk (Robb &

Robinson, 2014).

WACC of the organization ARB Corporation Limited

From the calculation shown in Appendix 2i, it can be inferred that WACC of ARB Corporation

Limited is 18.05 percent in 2017. In comparison with the previous two years, it can be deduced

that the cost of capital has decreased (19.01 percent in 2016 and 19.39 percent in 2015). This can

be taken as a good sign for the organization as the firm is being successful in minimizing the cost

of capital financing (Zeitun & Tian, 2014).

CAPM

From the calculation shown in Appendix 2i, it can be inferred that, the expected cost of equity is

coming to be 7.9 percent. This can be taken as a good sign for the organization as market rate of

return RM is more than the expected cost of equity (8.54 percent).

Answer to 2ii) Comparison of the capital structure of ARB Corporation Limited with its

competitor

The capital structure of the organization ARB Corporation Limited has been compared

with its competitor Bell Equipment Limited. In case of Bell Equipment Limited, the capital

structure of the firm is mixed of debt and equity (81 percent equity and 19 percent debt). The

total equity of the company is $3,657. While, in case of ARB Corporation Limited, the entire

capital structure is formed on the basis of equity and there is no sign of debt in capital structure.

The total equity of the firm is $272,341.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

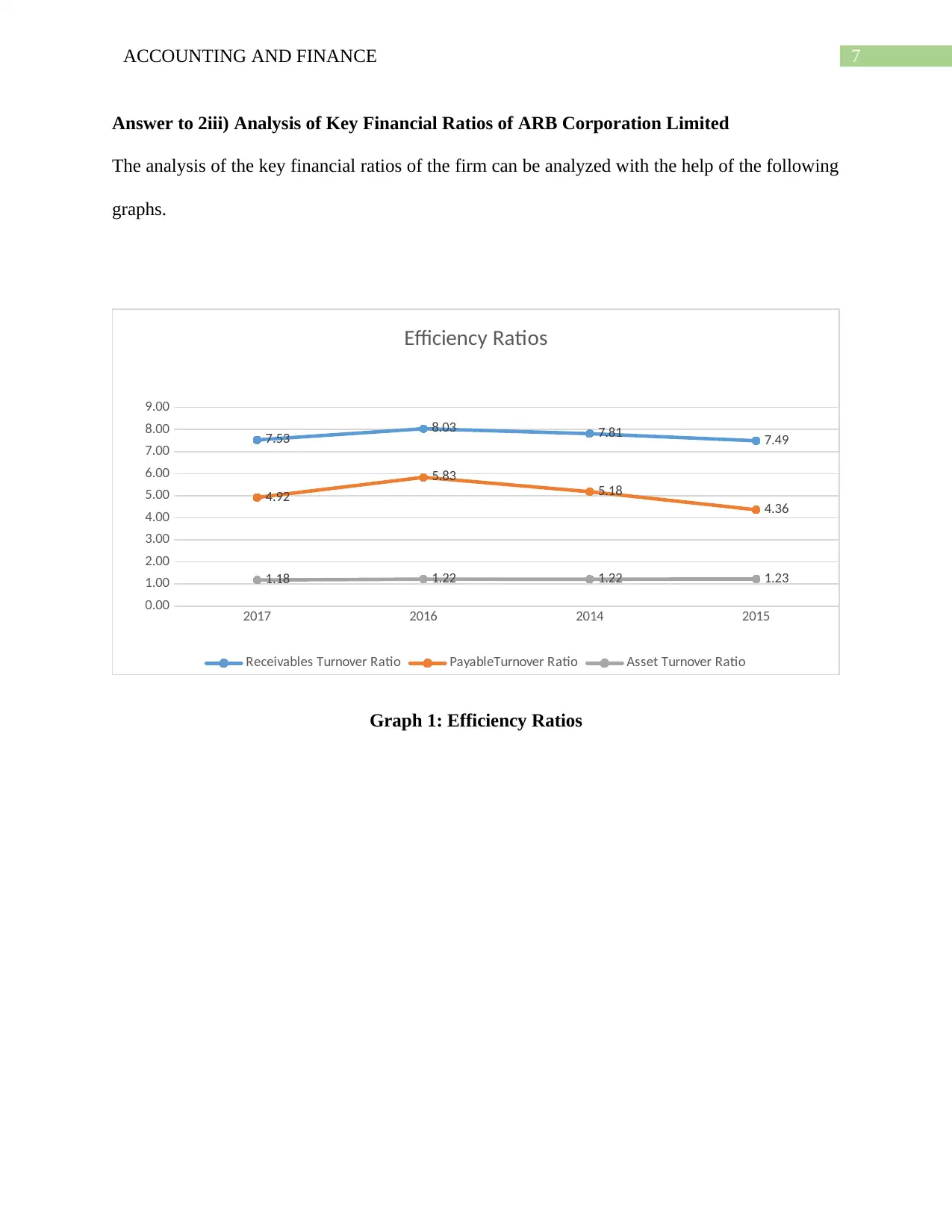

Answer to 2iii) Analysis of Key Financial Ratios of ARB Corporation Limited

The analysis of the key financial ratios of the firm can be analyzed with the help of the following

graphs.

2017 2016 2014 2015

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

7.53 8.03 7.81 7.49

4.92

5.83

5.18

4.36

1.18 1.22 1.22 1.23

Efficiency Ratios

Receivables Turnover Ratio PayableTurnover Ratio Asset Turnover Ratio

Graph 1: Efficiency Ratios

Answer to 2iii) Analysis of Key Financial Ratios of ARB Corporation Limited

The analysis of the key financial ratios of the firm can be analyzed with the help of the following

graphs.

2017 2016 2014 2015

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

7.53 8.03 7.81 7.49

4.92

5.83

5.18

4.36

1.18 1.22 1.22 1.23

Efficiency Ratios

Receivables Turnover Ratio PayableTurnover Ratio Asset Turnover Ratio

Graph 1: Efficiency Ratios

8ACCOUNTING AND FINANCE

2017 2016 2014 2015

0.00

0.05

0.10

0.15

0.20

0.25

0.13 0.13 0.13 0.14

0.18 0.19 0.19

0.22

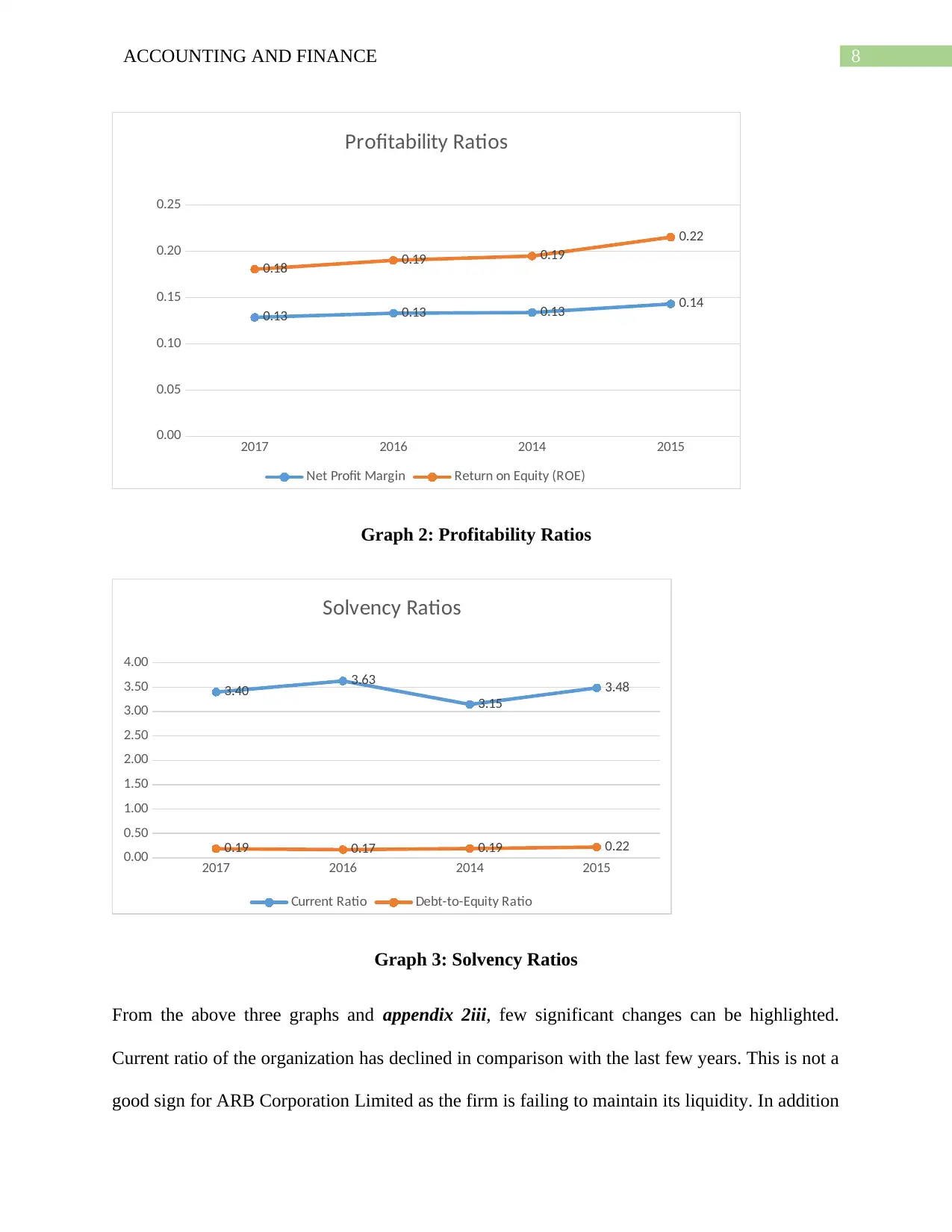

Profitability Ratios

Net Profit Margin Return on Equity (ROE)

Graph 2: Profitability Ratios

2017 2016 2014 2015

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

3.40 3.63

3.15

3.48

0.19 0.17 0.19 0.22

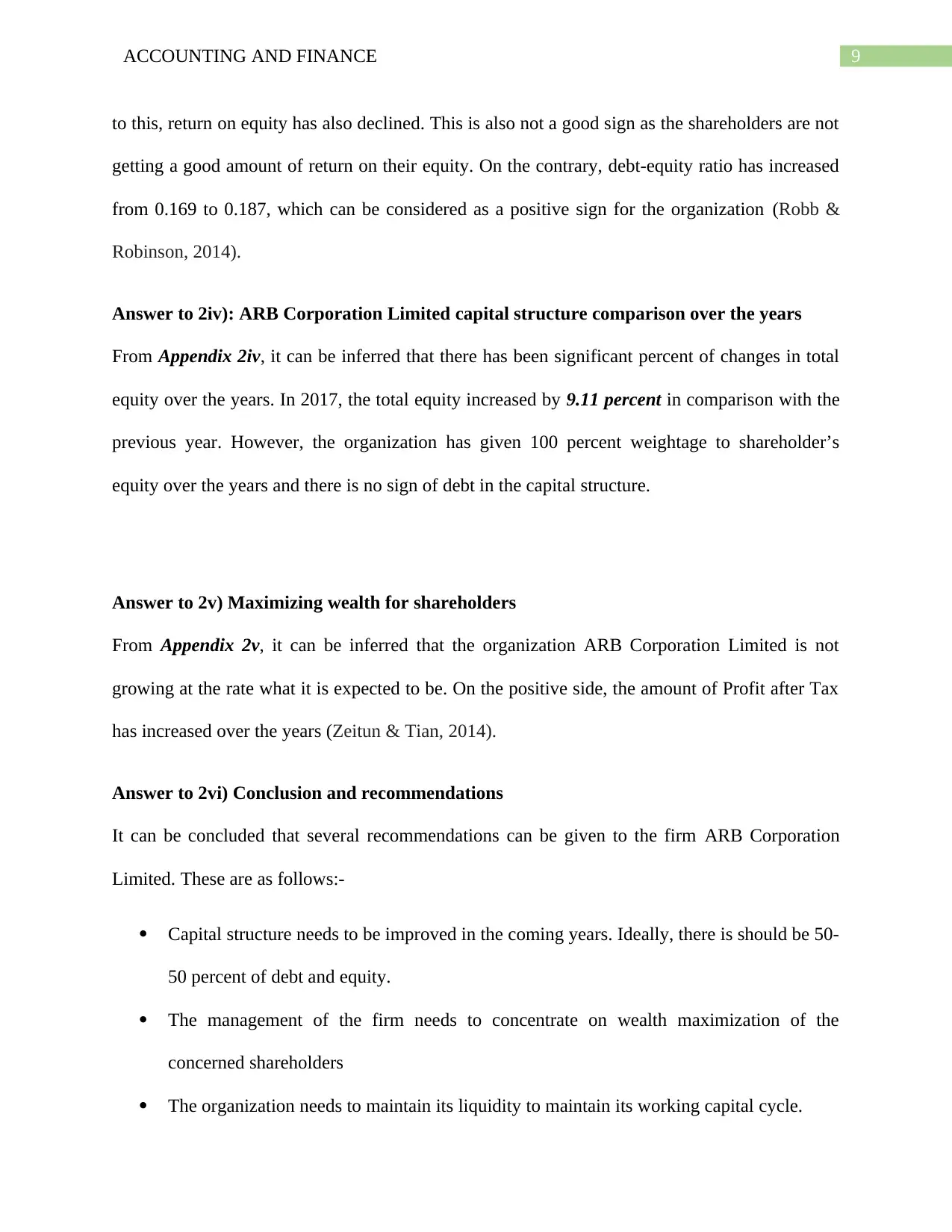

Solvency Ratios

Current Ratio Debt-to-Equity Ratio

Graph 3: Solvency Ratios

From the above three graphs and appendix 2iii, few significant changes can be highlighted.

Current ratio of the organization has declined in comparison with the last few years. This is not a

good sign for ARB Corporation Limited as the firm is failing to maintain its liquidity. In addition

2017 2016 2014 2015

0.00

0.05

0.10

0.15

0.20

0.25

0.13 0.13 0.13 0.14

0.18 0.19 0.19

0.22

Profitability Ratios

Net Profit Margin Return on Equity (ROE)

Graph 2: Profitability Ratios

2017 2016 2014 2015

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

3.40 3.63

3.15

3.48

0.19 0.17 0.19 0.22

Solvency Ratios

Current Ratio Debt-to-Equity Ratio

Graph 3: Solvency Ratios

From the above three graphs and appendix 2iii, few significant changes can be highlighted.

Current ratio of the organization has declined in comparison with the last few years. This is not a

good sign for ARB Corporation Limited as the firm is failing to maintain its liquidity. In addition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

to this, return on equity has also declined. This is also not a good sign as the shareholders are not

getting a good amount of return on their equity. On the contrary, debt-equity ratio has increased

from 0.169 to 0.187, which can be considered as a positive sign for the organization (Robb &

Robinson, 2014).

Answer to 2iv): ARB Corporation Limited capital structure comparison over the years

From Appendix 2iv, it can be inferred that there has been significant percent of changes in total

equity over the years. In 2017, the total equity increased by 9.11 percent in comparison with the

previous year. However, the organization has given 100 percent weightage to shareholder’s

equity over the years and there is no sign of debt in the capital structure.

Answer to 2v) Maximizing wealth for shareholders

From Appendix 2v, it can be inferred that the organization ARB Corporation Limited is not

growing at the rate what it is expected to be. On the positive side, the amount of Profit after Tax

has increased over the years (Zeitun & Tian, 2014).

Answer to 2vi) Conclusion and recommendations

It can be concluded that several recommendations can be given to the firm ARB Corporation

Limited. These are as follows:-

Capital structure needs to be improved in the coming years. Ideally, there is should be 50-

50 percent of debt and equity.

The management of the firm needs to concentrate on wealth maximization of the

concerned shareholders

The organization needs to maintain its liquidity to maintain its working capital cycle.

to this, return on equity has also declined. This is also not a good sign as the shareholders are not

getting a good amount of return on their equity. On the contrary, debt-equity ratio has increased

from 0.169 to 0.187, which can be considered as a positive sign for the organization (Robb &

Robinson, 2014).

Answer to 2iv): ARB Corporation Limited capital structure comparison over the years

From Appendix 2iv, it can be inferred that there has been significant percent of changes in total

equity over the years. In 2017, the total equity increased by 9.11 percent in comparison with the

previous year. However, the organization has given 100 percent weightage to shareholder’s

equity over the years and there is no sign of debt in the capital structure.

Answer to 2v) Maximizing wealth for shareholders

From Appendix 2v, it can be inferred that the organization ARB Corporation Limited is not

growing at the rate what it is expected to be. On the positive side, the amount of Profit after Tax

has increased over the years (Zeitun & Tian, 2014).

Answer to 2vi) Conclusion and recommendations

It can be concluded that several recommendations can be given to the firm ARB Corporation

Limited. These are as follows:-

Capital structure needs to be improved in the coming years. Ideally, there is should be 50-

50 percent of debt and equity.

The management of the firm needs to concentrate on wealth maximization of the

concerned shareholders

The organization needs to maintain its liquidity to maintain its working capital cycle.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

In this manner, the organization will be able to attain its desired aims and objectives and sustain

with respect to its competitors.

In this manner, the organization will be able to attain its desired aims and objectives and sustain

with respect to its competitors.

11ACCOUNTING AND FINANCE

References

Abbey, J. D., Blackburn, J. D., & Guide Jr, V. D. R. (2015). Optimal pricing for new and

remanufactured products. Journal of Operations Management, 36, 130-146.

ARB 4x4 Accessories - Your partner in adventure. (2018). Retrieved from

https://www.arb.com.au/

Brooks, R. (2015). Financial management: core concepts. Pearson.

Burns, R., & Walker, J. (2015). Capital budgeting surveys: the future is now.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

Zeitun, R., & Tian, G. (2014). Capital structure and corporate performance: evidence from

Jordan.

References

Abbey, J. D., Blackburn, J. D., & Guide Jr, V. D. R. (2015). Optimal pricing for new and

remanufactured products. Journal of Operations Management, 36, 130-146.

ARB 4x4 Accessories - Your partner in adventure. (2018). Retrieved from

https://www.arb.com.au/

Brooks, R. (2015). Financial management: core concepts. Pearson.

Burns, R., & Walker, J. (2015). Capital budgeting surveys: the future is now.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

Zeitun, R., & Tian, G. (2014). Capital structure and corporate performance: evidence from

Jordan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.