Report on Costing Techniques: GSK's Financial Analysis

VerifiedAdded on 2022/08/19

|9

|2171

|24

Report

AI Summary

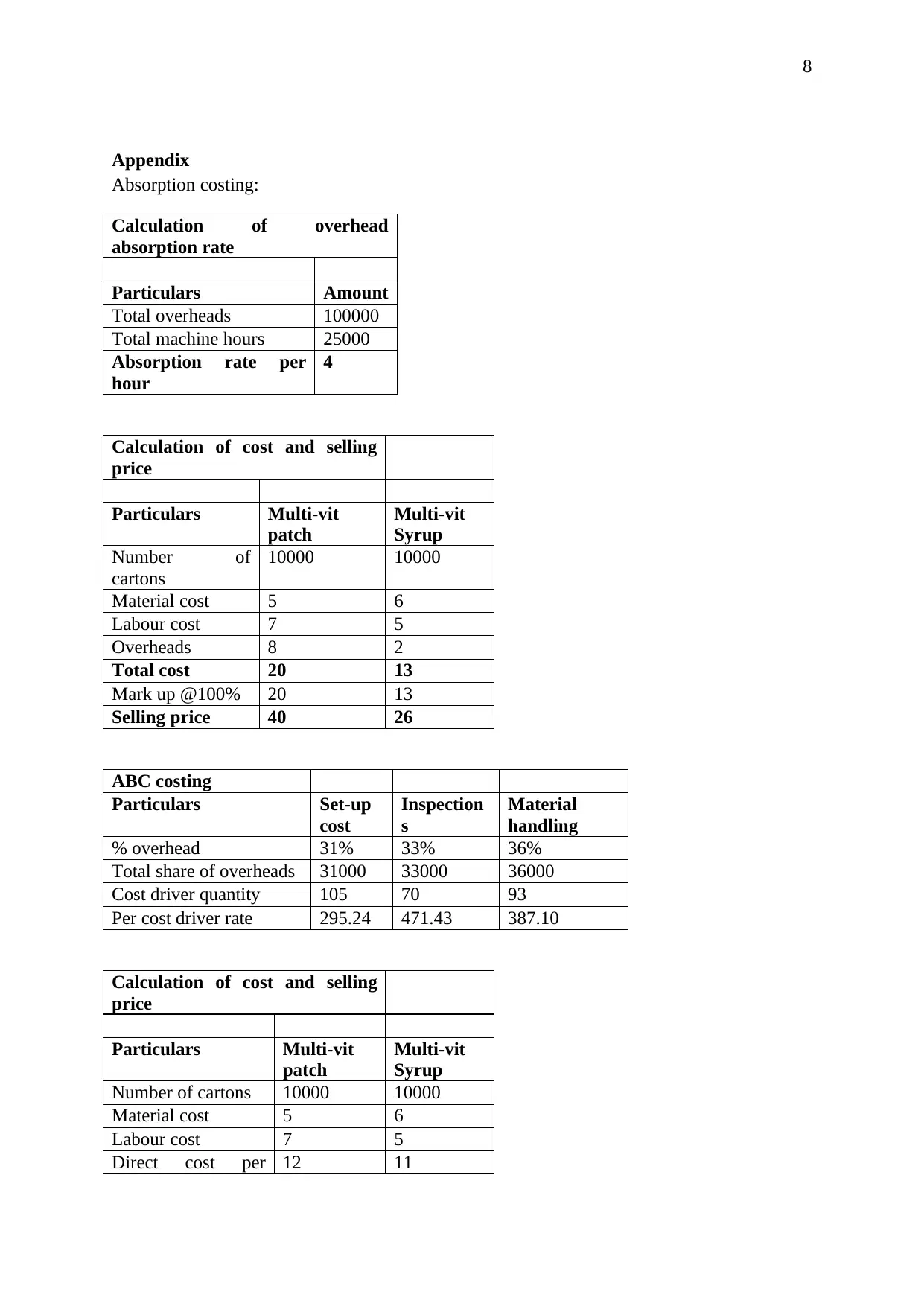

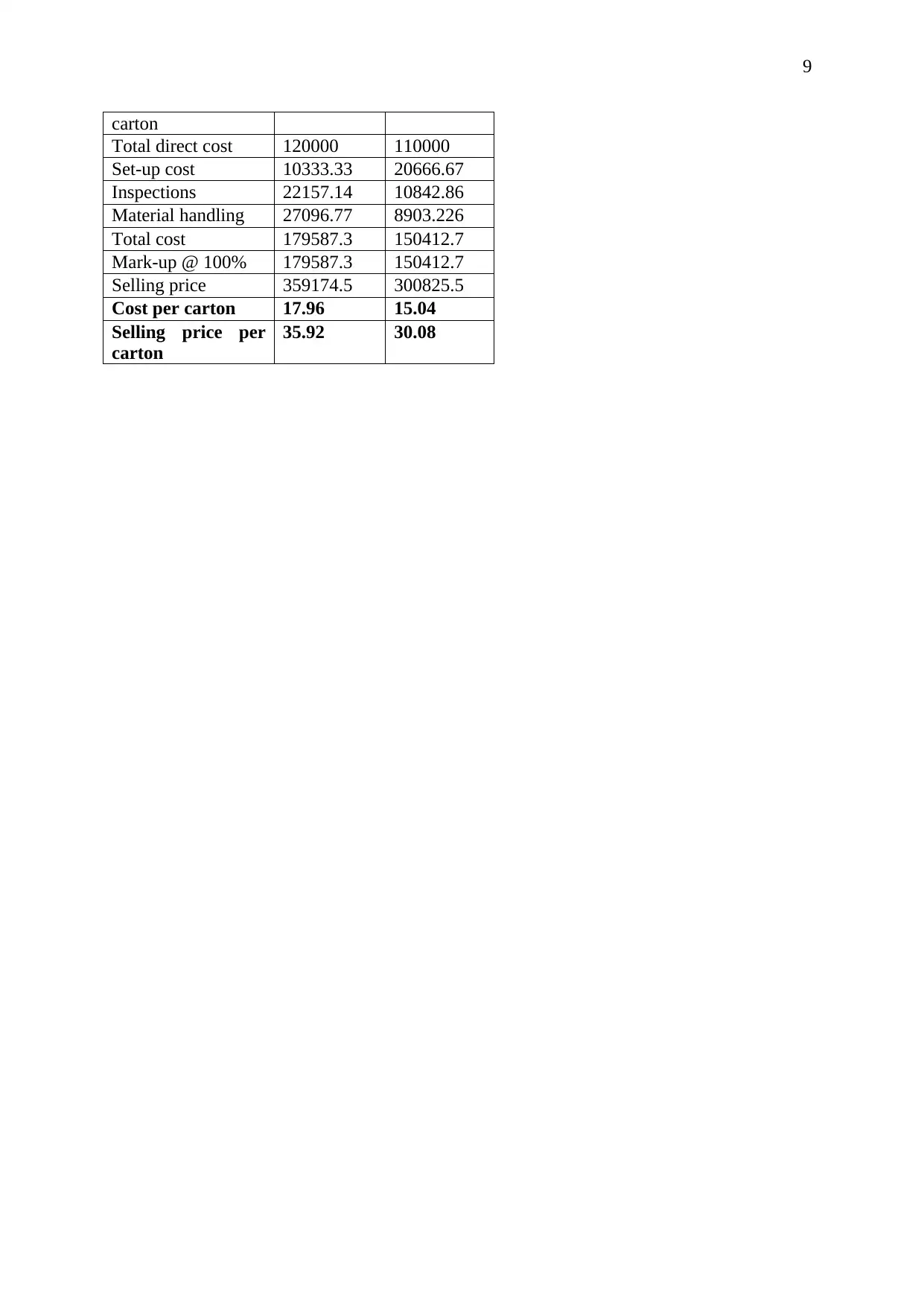

This report provides a detailed analysis of costing techniques, specifically focusing on absorption costing and activity-based costing (ABC), within the context of a business case study involving GSK. The report begins by outlining the nature, source, and purpose of management information, emphasizing its importance in business decision-making. It then delves into the specifics of absorption costing, explaining how overhead costs are allocated based on a single factor, and compares it to ABC, which allocates costs based on activities. The report includes calculations, comparing the costs and selling prices derived from both methods for two GSK products, the multi-vit patch and multi-vit syrup. It interprets the findings, recommending ABC as a more reliable method due to its detailed approach to overhead allocation. The conclusion reinforces the significance of management accounting techniques in business operations and highlights the benefits of ABC for accurate cost determination and informed pricing strategies. The appendix provides detailed calculations for both costing methods.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.