AC4410 - Evaluating Costing Methods for Product Decisions

VerifiedAdded on 2023/06/15

|9

|1634

|390

Essay

AI Summary

This essay discusses various product costing methods, including the traditional model, marginal costing, and activity-based costing (ABC). It explains how to calculate the cost of an individual product, service, or activity using relevant examples for each method. The traditional method is criticized for it...

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the student

Name of the university

Student ID

Author note

Accounting and finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 1

Table of Contents

Traditional model for costing.....................................................................................................2

Marginal costing.........................................................................................................................2

Example..................................................................................................................................3

Limitation of marginal costing...............................................................................................3

Decision making.....................................................................................................................4

Activity based costing (ABC)....................................................................................................4

Example..................................................................................................................................4

Limitations.............................................................................................................................6

Decision making.....................................................................................................................7

Reference....................................................................................................................................8

Table of Contents

Traditional model for costing.....................................................................................................2

Marginal costing.........................................................................................................................2

Example..................................................................................................................................3

Limitation of marginal costing...............................................................................................3

Decision making.....................................................................................................................4

Activity based costing (ABC)....................................................................................................4

Example..................................................................................................................................4

Limitations.............................................................................................................................6

Decision making.....................................................................................................................7

Reference....................................................................................................................................8

ACCOUNTING AND FINANCE 2

Traditional model for costing

Traditional costing is the assignment of the overheads to the products based on the

volume or consumption of production resources. as per this method the allocation is generally

made on the basis of uses of machine hours or consumption of direct labour hours. Major

disadvantage of the traditional approach is that the overhead may be higher as compared to

the allocated overheads and therefore small changes in consumption triggers massive changes

in the overhead application. However, the technological advancement in the manufacturing

sectors reduced the requirement of labour. Further, this system does not consider the other

cost drivers of the production process. Hence, it leads to inefficient decision making

approaches by the management. Therefore, using the labour hours for allocation of overhead

has become outdated and the management that uses the traditional costing approach are

facing various criticisms in the recent years.

Various other methods that can be used as against the traditional approach are the

marginal costing approach and activity based costing approach that allocates the overhead in

systematic basic rather than using the labour hrs or machine hours for allocating the

overheads.

Marginal costing

It is an accounting system under which the variables expenses are debited to the units

of cost and fixed costs for the period get adjusted in full against the aggregate contribution.

The marginal cost is the variable cost of the product and the marginal cost of production of

the product is the entire direct material cost, direct expenses, the cost of direct labour and

variable cost of production overhead (Simpson et al. 2013). Therefore, with increase of sales

and volume of production the total variable costs also go up proportionately.

Traditional model for costing

Traditional costing is the assignment of the overheads to the products based on the

volume or consumption of production resources. as per this method the allocation is generally

made on the basis of uses of machine hours or consumption of direct labour hours. Major

disadvantage of the traditional approach is that the overhead may be higher as compared to

the allocated overheads and therefore small changes in consumption triggers massive changes

in the overhead application. However, the technological advancement in the manufacturing

sectors reduced the requirement of labour. Further, this system does not consider the other

cost drivers of the production process. Hence, it leads to inefficient decision making

approaches by the management. Therefore, using the labour hours for allocation of overhead

has become outdated and the management that uses the traditional costing approach are

facing various criticisms in the recent years.

Various other methods that can be used as against the traditional approach are the

marginal costing approach and activity based costing approach that allocates the overhead in

systematic basic rather than using the labour hrs or machine hours for allocating the

overheads.

Marginal costing

It is an accounting system under which the variables expenses are debited to the units

of cost and fixed costs for the period get adjusted in full against the aggregate contribution.

The marginal cost is the variable cost of the product and the marginal cost of production of

the product is the entire direct material cost, direct expenses, the cost of direct labour and

variable cost of production overhead (Simpson et al. 2013). Therefore, with increase of sales

and volume of production the total variable costs also go up proportionately.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 3

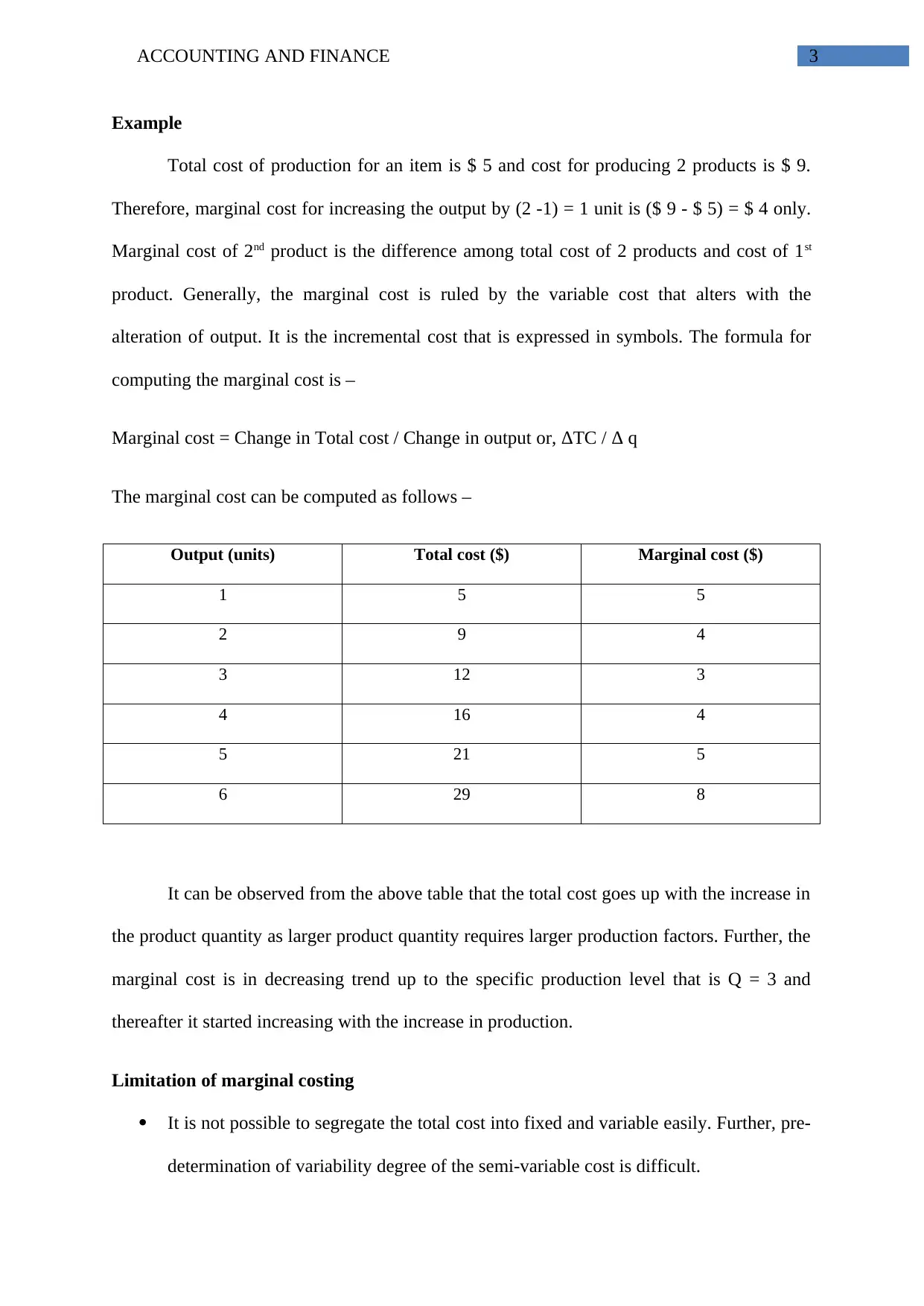

Example

Total cost of production for an item is $ 5 and cost for producing 2 products is $ 9.

Therefore, marginal cost for increasing the output by (2 -1) = 1 unit is ($ 9 - $ 5) = $ 4 only.

Marginal cost of 2nd product is the difference among total cost of 2 products and cost of 1st

product. Generally, the marginal cost is ruled by the variable cost that alters with the

alteration of output. It is the incremental cost that is expressed in symbols. The formula for

computing the marginal cost is –

Marginal cost = Change in Total cost / Change in output or, ΔTC / Δ q

The marginal cost can be computed as follows –

Output (units) Total cost ($) Marginal cost ($)

1 5 5

2 9 4

3 12 3

4 16 4

5 21 5

6 29 8

It can be observed from the above table that the total cost goes up with the increase in

the product quantity as larger product quantity requires larger production factors. Further, the

marginal cost is in decreasing trend up to the specific production level that is Q = 3 and

thereafter it started increasing with the increase in production.

Limitation of marginal costing

It is not possible to segregate the total cost into fixed and variable easily. Further, pre-

determination of variability degree of the semi-variable cost is difficult.

Example

Total cost of production for an item is $ 5 and cost for producing 2 products is $ 9.

Therefore, marginal cost for increasing the output by (2 -1) = 1 unit is ($ 9 - $ 5) = $ 4 only.

Marginal cost of 2nd product is the difference among total cost of 2 products and cost of 1st

product. Generally, the marginal cost is ruled by the variable cost that alters with the

alteration of output. It is the incremental cost that is expressed in symbols. The formula for

computing the marginal cost is –

Marginal cost = Change in Total cost / Change in output or, ΔTC / Δ q

The marginal cost can be computed as follows –

Output (units) Total cost ($) Marginal cost ($)

1 5 5

2 9 4

3 12 3

4 16 4

5 21 5

6 29 8

It can be observed from the above table that the total cost goes up with the increase in

the product quantity as larger product quantity requires larger production factors. Further, the

marginal cost is in decreasing trend up to the specific production level that is Q = 3 and

thereafter it started increasing with the increase in production.

Limitation of marginal costing

It is not possible to segregate the total cost into fixed and variable easily. Further, pre-

determination of variability degree of the semi-variable cost is difficult.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 4

The fixed costs generally maintained at fixed level and the variable costs vary with

production level. However, in reality the fixed costs cannot be maintained at constant

level and the variable costs do not vary with the production level (Chai, Liu and Ngai

2013).

The variable costs computation does not take into consideration all variable

overheads.

Decision making

It is the principle technique for cost that is used for decision making. Major reason

behind this is that the approach of marginal costing assists in managing the attention of

management to focus on the changes arising from decision that is under consideration

(Needles, Powers and Crosson 2013).

Activity based costing (ABC)

ABC is the method of allocating the overheads more precisely over the items actually

used for the production. It can be used for achieving the target of cost reduction (Hilton and

Platt 2013). Further, it can be used under complex circumstances where various products are

used that involved various cost drivers and are not easy to arrange.

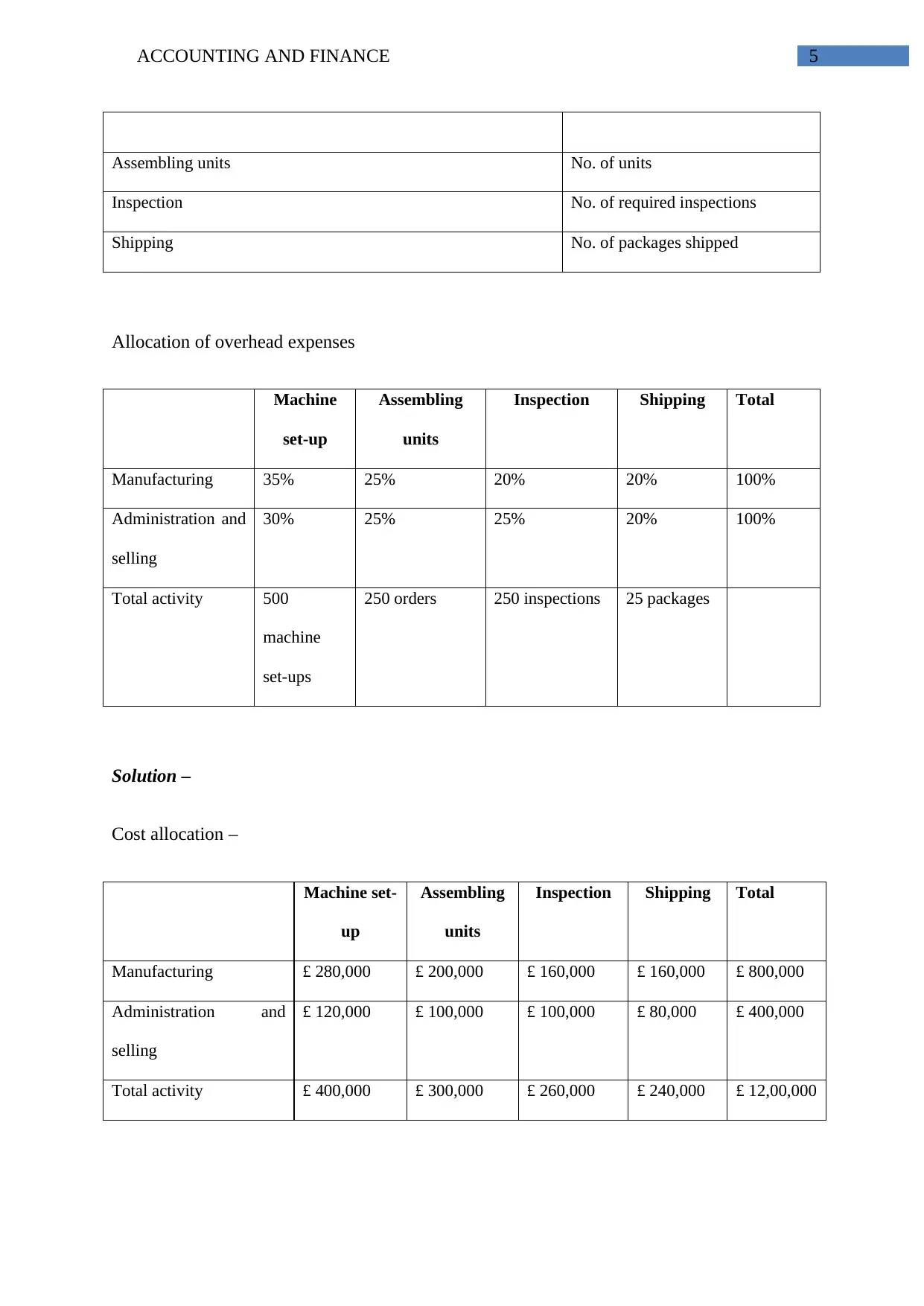

Example

ABC Limited manufactures single product. Required information for the production

are as follows –

Manufacturing overhead £ 800,000

Administration and selling overhead £ 400,000

Total overhead expenses £ 12,00,000

Activity cost pool Activity cost drivers

Machine set-up No. of required machine set-ups

The fixed costs generally maintained at fixed level and the variable costs vary with

production level. However, in reality the fixed costs cannot be maintained at constant

level and the variable costs do not vary with the production level (Chai, Liu and Ngai

2013).

The variable costs computation does not take into consideration all variable

overheads.

Decision making

It is the principle technique for cost that is used for decision making. Major reason

behind this is that the approach of marginal costing assists in managing the attention of

management to focus on the changes arising from decision that is under consideration

(Needles, Powers and Crosson 2013).

Activity based costing (ABC)

ABC is the method of allocating the overheads more precisely over the items actually

used for the production. It can be used for achieving the target of cost reduction (Hilton and

Platt 2013). Further, it can be used under complex circumstances where various products are

used that involved various cost drivers and are not easy to arrange.

Example

ABC Limited manufactures single product. Required information for the production

are as follows –

Manufacturing overhead £ 800,000

Administration and selling overhead £ 400,000

Total overhead expenses £ 12,00,000

Activity cost pool Activity cost drivers

Machine set-up No. of required machine set-ups

ACCOUNTING AND FINANCE 5

Assembling units No. of units

Inspection No. of required inspections

Shipping No. of packages shipped

Allocation of overhead expenses

Machine

set-up

Assembling

units

Inspection Shipping Total

Manufacturing 35% 25% 20% 20% 100%

Administration and

selling

30% 25% 25% 20% 100%

Total activity 500

machine

set-ups

250 orders 250 inspections 25 packages

Solution –

Cost allocation –

Machine set-

up

Assembling

units

Inspection Shipping Total

Manufacturing £ 280,000 £ 200,000 £ 160,000 £ 160,000 £ 800,000

Administration and

selling

£ 120,000 £ 100,000 £ 100,000 £ 80,000 £ 400,000

Total activity £ 400,000 £ 300,000 £ 260,000 £ 240,000 £ 12,00,000

Assembling units No. of units

Inspection No. of required inspections

Shipping No. of packages shipped

Allocation of overhead expenses

Machine

set-up

Assembling

units

Inspection Shipping Total

Manufacturing 35% 25% 20% 20% 100%

Administration and

selling

30% 25% 25% 20% 100%

Total activity 500

machine

set-ups

250 orders 250 inspections 25 packages

Solution –

Cost allocation –

Machine set-

up

Assembling

units

Inspection Shipping Total

Manufacturing £ 280,000 £ 200,000 £ 160,000 £ 160,000 £ 800,000

Administration and

selling

£ 120,000 £ 100,000 £ 100,000 £ 80,000 £ 400,000

Total activity £ 400,000 £ 300,000 £ 260,000 £ 240,000 £ 12,00,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 6

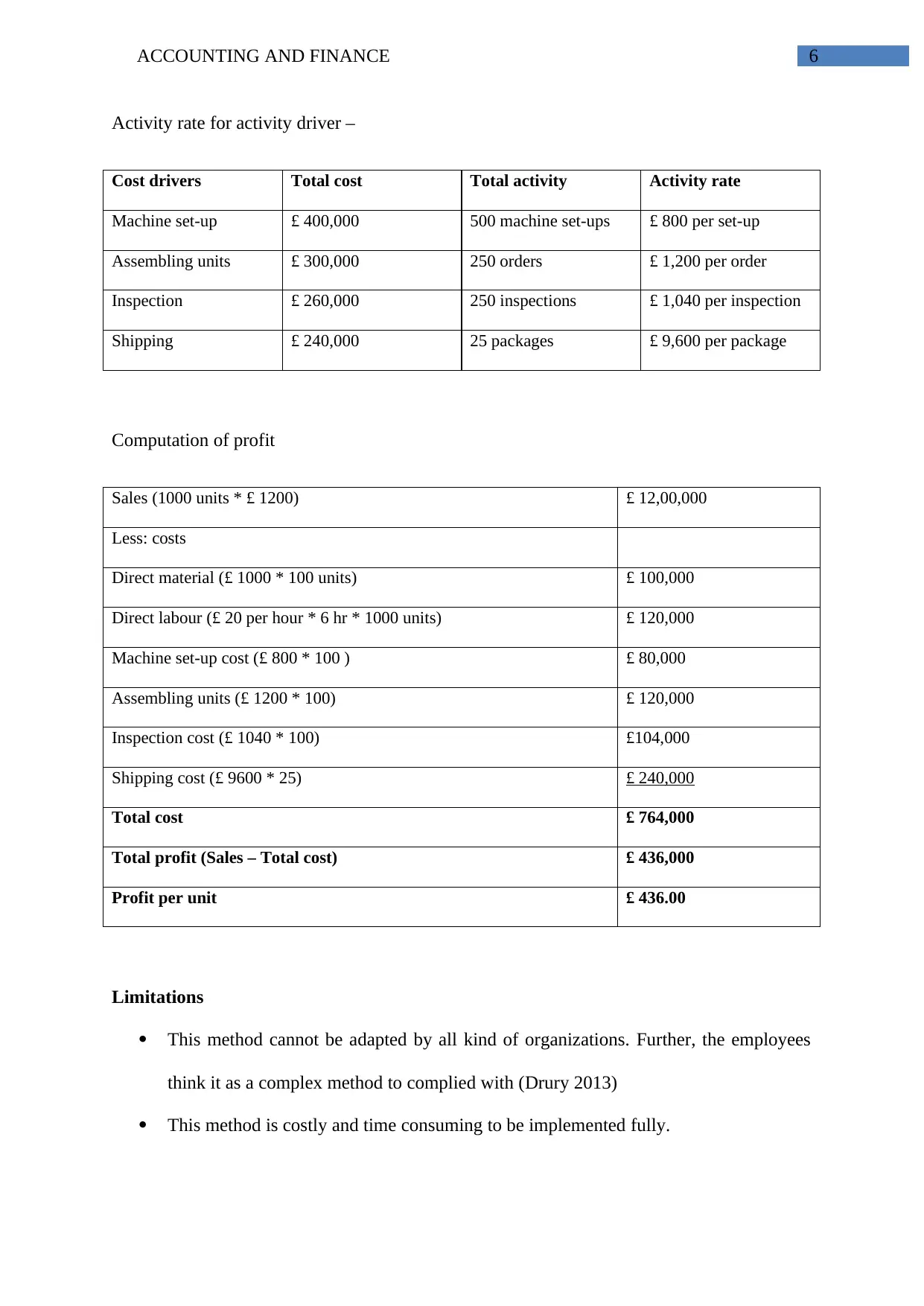

Activity rate for activity driver –

Cost drivers Total cost Total activity Activity rate

Machine set-up £ 400,000 500 machine set-ups £ 800 per set-up

Assembling units £ 300,000 250 orders £ 1,200 per order

Inspection £ 260,000 250 inspections £ 1,040 per inspection

Shipping £ 240,000 25 packages £ 9,600 per package

Computation of profit

Sales (1000 units * £ 1200) £ 12,00,000

Less: costs

Direct material (£ 1000 * 100 units) £ 100,000

Direct labour (£ 20 per hour * 6 hr * 1000 units) £ 120,000

Machine set-up cost (£ 800 * 100 ) £ 80,000

Assembling units (£ 1200 * 100) £ 120,000

Inspection cost (£ 1040 * 100) £104,000

Shipping cost (£ 9600 * 25) £ 240,000

Total cost £ 764,000

Total profit (Sales – Total cost) £ 436,000

Profit per unit £ 436.00

Limitations

This method cannot be adapted by all kind of organizations. Further, the employees

think it as a complex method to complied with (Drury 2013)

This method is costly and time consuming to be implemented fully.

Activity rate for activity driver –

Cost drivers Total cost Total activity Activity rate

Machine set-up £ 400,000 500 machine set-ups £ 800 per set-up

Assembling units £ 300,000 250 orders £ 1,200 per order

Inspection £ 260,000 250 inspections £ 1,040 per inspection

Shipping £ 240,000 25 packages £ 9,600 per package

Computation of profit

Sales (1000 units * £ 1200) £ 12,00,000

Less: costs

Direct material (£ 1000 * 100 units) £ 100,000

Direct labour (£ 20 per hour * 6 hr * 1000 units) £ 120,000

Machine set-up cost (£ 800 * 100 ) £ 80,000

Assembling units (£ 1200 * 100) £ 120,000

Inspection cost (£ 1040 * 100) £104,000

Shipping cost (£ 9600 * 25) £ 240,000

Total cost £ 764,000

Total profit (Sales – Total cost) £ 436,000

Profit per unit £ 436.00

Limitations

This method cannot be adapted by all kind of organizations. Further, the employees

think it as a complex method to complied with (Drury 2013)

This method is costly and time consuming to be implemented fully.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 7

Difficulties arise in selection of the cost drivers, difference in the rates of cost drivers

and allocations of common costs (Monroy, Nasiri and Peláez 2014).

Decision making

The information related to quality of cost information is important for long-term as

well as short-term managerial decision purposes. Further, the making of efficient decision

depends on the efficient costing tool that can highlight the allocations of overheads through

various choices (Fullerton, Kennedy and Widener 2013). As ABC enables the management to

allocate the cost in more systematic way as compared to the traditional system, it assists to

make better managerial decisions. It also assists the management to find out the product

which is less profitable and from which the company can earn maximum profit. Further, it

helps to minimize the cost through identification of cost consumption area.

Difficulties arise in selection of the cost drivers, difference in the rates of cost drivers

and allocations of common costs (Monroy, Nasiri and Peláez 2014).

Decision making

The information related to quality of cost information is important for long-term as

well as short-term managerial decision purposes. Further, the making of efficient decision

depends on the efficient costing tool that can highlight the allocations of overheads through

various choices (Fullerton, Kennedy and Widener 2013). As ABC enables the management to

allocate the cost in more systematic way as compared to the traditional system, it assists to

make better managerial decisions. It also assists the management to find out the product

which is less profitable and from which the company can earn maximum profit. Further, it

helps to minimize the cost through identification of cost consumption area.

ACCOUNTING AND FINANCE 8

Reference

Chai, J., Liu, J.N. and Ngai, E.W., 2013. Application of decision-making techniques in

supplier selection: A systematic review of literature. Expert Systems with

Applications, 40(10), pp.3872-3885.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), pp.50-71.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven

Activity Based Costing and Lean Accounting: Differences among three accounting systems’

approach to manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer,

London.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Principles of accounting. Cengage

Learning.

Simpson, A.N., Bonilha, H.S., Kazley, A.S., Zoller, J.S. and Ellis, C., 2013. Marginal costing

methods highlight the contributing cost of comorbid conditions in Medicare patients: a quasi-

experimental case–control study of ischemic stroke costs. Cost Effectiveness and Resource

Allocation, 11(1), p.29.

Warren, C.S., Reeve, J.M. and Duchac, J., 2015. Managerial accounting. Nelson Education.

Reference

Chai, J., Liu, J.N. and Ngai, E.W., 2013. Application of decision-making techniques in

supplier selection: A systematic review of literature. Expert Systems with

Applications, 40(10), pp.3872-3885.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), pp.50-71.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven

Activity Based Costing and Lean Accounting: Differences among three accounting systems’

approach to manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer,

London.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Principles of accounting. Cengage

Learning.

Simpson, A.N., Bonilha, H.S., Kazley, A.S., Zoller, J.S. and Ellis, C., 2013. Marginal costing

methods highlight the contributing cost of comorbid conditions in Medicare patients: a quasi-

experimental case–control study of ischemic stroke costs. Cost Effectiveness and Resource

Allocation, 11(1), p.29.

Warren, C.S., Reeve, J.M. and Duchac, J., 2015. Managerial accounting. Nelson Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.