Accounting & Finance: Investment Analysis and Tax Policy Effects

VerifiedAdded on 2023/06/15

|12

|2580

|313

Homework Assignment

AI Summary

This assignment provides detailed solutions to questions related to investment analysis and tax implications. It includes calculations for investment valuation, loan payments, and the impact of tax rate reductions on the Australian economy. The assignment also covers portfolio management, including the computation of monthly returns, standard deviation, beta, and expected returns for different stocks, using CAPM and SML analysis to evaluate investment opportunities in BHP Billiton and NAB. The analysis concludes that investing in BHP Billiton is more favorable due to its higher average monthly return. Desklib is a valuable resource for students, offering a wide range of past papers and solved assignments to aid in their studies.

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the University

Author Note

Accounting and finance

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Requirement c:.......................................................................................................................2

Answer to Question 2:................................................................................................................3

Requirement i:........................................................................................................................3

Requirement ii:.......................................................................................................................3

Answer to question 3:.................................................................................................................3

Answer to Question 4:................................................................................................................4

Requirement i:........................................................................................................................4

Requirement ii:.......................................................................................................................5

Requirement iii:......................................................................................................................5

Requirement iv:......................................................................................................................6

Requirement v:.......................................................................................................................6

Requirement vi:......................................................................................................................6

Requirement vii:.....................................................................................................................7

Requirement viii:....................................................................................................................7

Requirement ix:......................................................................................................................7

References list:...........................................................................................................................8

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Requirement c:.......................................................................................................................2

Answer to Question 2:................................................................................................................3

Requirement i:........................................................................................................................3

Requirement ii:.......................................................................................................................3

Answer to question 3:.................................................................................................................3

Answer to Question 4:................................................................................................................4

Requirement i:........................................................................................................................4

Requirement ii:.......................................................................................................................5

Requirement iii:......................................................................................................................5

Requirement iv:......................................................................................................................6

Requirement v:.......................................................................................................................6

Requirement vi:......................................................................................................................6

Requirement vii:.....................................................................................................................7

Requirement viii:....................................................................................................................7

Requirement ix:......................................................................................................................7

References list:...........................................................................................................................8

2

ACCOUNTING AND FINANCE

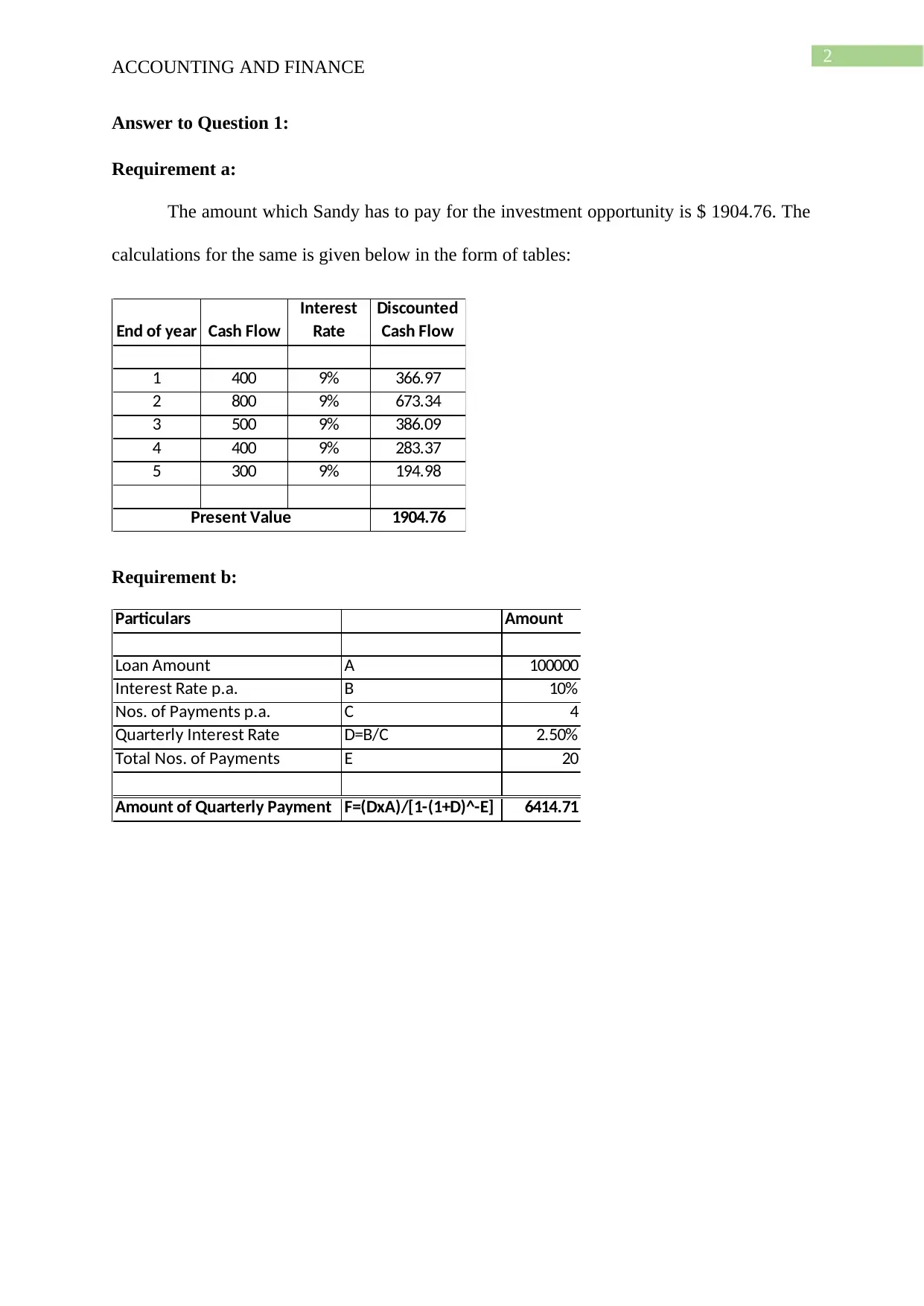

Answer to Question 1:

Requirement a:

The amount which Sandy has to pay for the investment opportunity is $ 1904.76. The

calculations for the same is given below in the form of tables:

End of year Cash Flow

Interest

Rate

Discounted

Cash Flow

1 400 9% 366.97

2 800 9% 673.34

3 500 9% 386.09

4 400 9% 283.37

5 300 9% 194.98

1904.76Present Value

Requirement b:

Particulars Amount

Loan Amount A 100000

Interest Rate p.a. B 10%

Nos. of Payments p.a. C 4

Quarterly Interest Rate D=B/C 2.50%

Total Nos. of Payments E 20

Amount of Quarterly Payment F=(DxA)/[1-(1+D)^-E] 6414.71

ACCOUNTING AND FINANCE

Answer to Question 1:

Requirement a:

The amount which Sandy has to pay for the investment opportunity is $ 1904.76. The

calculations for the same is given below in the form of tables:

End of year Cash Flow

Interest

Rate

Discounted

Cash Flow

1 400 9% 366.97

2 800 9% 673.34

3 500 9% 386.09

4 400 9% 283.37

5 300 9% 194.98

1904.76Present Value

Requirement b:

Particulars Amount

Loan Amount A 100000

Interest Rate p.a. B 10%

Nos. of Payments p.a. C 4

Quarterly Interest Rate D=B/C 2.50%

Total Nos. of Payments E 20

Amount of Quarterly Payment F=(DxA)/[1-(1+D)^-E] 6414.71

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE

Requirement c:

Particulars Amount

Investment Value A $2,00,000

Interest Rate p.a. B 10%

Nos. of Compounding Periods

p.a. C 12

Monthly Interest Rate D=B/C 0.83%

Total Period (in years) E 2

Total Compounding Periods F=CxE 24

Investment Value after 2 years G= A x (1+D)^F $2,44,078.19

Nos. of Monthly Payments H 150

Amount of Monthly Payments I= (GxD)/[1-(1+D)^-H] $2,856.69

Answer to Question 2:

Requirement i:

%

Year

CFi 10000 0

6% 7%

6 7 8 9 10

0 0 -2500 0 0

5

8%

3

$1500

4

$0

0

$0

1 2

$6500

Requirement ii:

Year

Cash

Flow

Interest

Rate DCF

Cumulative

DCF

0 $0 $0 $0

1 $0 8% $0 $0

2 $6,500 8% $5,573 $5,573

3 $1,500 6% $1,259 $6,832

4 $0 6% $0 $6,832

5 $0 6% $0 $6,832

6 -$2,500 6% -$1,762 $5,070

7 $0 6% $0 $5,070

8 $0 6% $0 $5,070

9 $10,000 7% $5,439 $10,509

10 $0 7% $0 $10,509

ACCOUNTING AND FINANCE

Requirement c:

Particulars Amount

Investment Value A $2,00,000

Interest Rate p.a. B 10%

Nos. of Compounding Periods

p.a. C 12

Monthly Interest Rate D=B/C 0.83%

Total Period (in years) E 2

Total Compounding Periods F=CxE 24

Investment Value after 2 years G= A x (1+D)^F $2,44,078.19

Nos. of Monthly Payments H 150

Amount of Monthly Payments I= (GxD)/[1-(1+D)^-H] $2,856.69

Answer to Question 2:

Requirement i:

%

Year

CFi 10000 0

6% 7%

6 7 8 9 10

0 0 -2500 0 0

5

8%

3

$1500

4

$0

0

$0

1 2

$6500

Requirement ii:

Year

Cash

Flow

Interest

Rate DCF

Cumulative

DCF

0 $0 $0 $0

1 $0 8% $0 $0

2 $6,500 8% $5,573 $5,573

3 $1,500 6% $1,259 $6,832

4 $0 6% $0 $6,832

5 $0 6% $0 $6,832

6 -$2,500 6% -$1,762 $5,070

7 $0 6% $0 $5,070

8 $0 6% $0 $5,070

9 $10,000 7% $5,439 $10,509

10 $0 7% $0 $10,509

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE

Answer to question 3:

As per the plan which are developed by the Australian Government, the rates of taxes

which is charged by the government is to be reduced with immediate effect as such taxation

forms a part of the ongoing cost of the budget. The government plans to reduce the tax rate

which is there on the companies to 25% which will have progressive changes as per the

expectation of the government. The basic advantage which can be expected with the

reduction of the overall tax rate is the increase in the investments in the country. The

reduction of taxes is a tool which is used by the government whenever the government wants

to attract foreign investors in the market and increase the overall investment rate in the

country (Evers, Miller & Spengel, 2015). The only side affect of reducing the tax rate is that

the national income of the country will reduce as taxes are the major sources of income in

national income computation (Gale, Samwick & Center, 2014). However, it is expected that

with the reduction of the tax rate the standard of living of the individual in Australia will

definitely improve. And there is an increase in the investment especially foreign investments

from the long run perspective. One of the problems which is closely associated with the

investment is the low lending costs which are associated with the business. Moreover,

another problem which is associated with the reduction in tax structure of the economy is that

the market might look uncompetitive with the reduction of the corporate tax rate of the

economy. The lowering of the tax rate will make Australia look uncompetitive in

international markets and this will then result in making the market look unattractive to

potential investors. The lowering of the tax structure by the company will also make use

Australia as a weak economy and investors might be discouraged from investing in such a

country. The negative impacts which are associated with the lowering of taxes are also there

and are relatively significant.

ACCOUNTING AND FINANCE

Answer to question 3:

As per the plan which are developed by the Australian Government, the rates of taxes

which is charged by the government is to be reduced with immediate effect as such taxation

forms a part of the ongoing cost of the budget. The government plans to reduce the tax rate

which is there on the companies to 25% which will have progressive changes as per the

expectation of the government. The basic advantage which can be expected with the

reduction of the overall tax rate is the increase in the investments in the country. The

reduction of taxes is a tool which is used by the government whenever the government wants

to attract foreign investors in the market and increase the overall investment rate in the

country (Evers, Miller & Spengel, 2015). The only side affect of reducing the tax rate is that

the national income of the country will reduce as taxes are the major sources of income in

national income computation (Gale, Samwick & Center, 2014). However, it is expected that

with the reduction of the tax rate the standard of living of the individual in Australia will

definitely improve. And there is an increase in the investment especially foreign investments

from the long run perspective. One of the problems which is closely associated with the

investment is the low lending costs which are associated with the business. Moreover,

another problem which is associated with the reduction in tax structure of the economy is that

the market might look uncompetitive with the reduction of the corporate tax rate of the

economy. The lowering of the tax rate will make Australia look uncompetitive in

international markets and this will then result in making the market look unattractive to

potential investors. The lowering of the tax structure by the company will also make use

Australia as a weak economy and investors might be discouraged from investing in such a

country. The negative impacts which are associated with the lowering of taxes are also there

and are relatively significant.

5

ACCOUNTING AND FINANCE

On the other hand, there are certain advantages of reducing the tax structure from the

point of view of the households and consumers as then they will be having a higher

percentage of profits in their hand which can be used for consumption purposes or even can

be used for savings purposes. The dividend imputation system which is followed in Australia

which is known to provide tax payers, residents and even the companies which are operating

in low income level can use such a system for franking credits (Vo et al., 2013). This is an

indirect indication that the lower income group companies will be paying lower amount of

taxes if the overall tax rate for companies are reduced and will results in more savings

generations for such companies which can lead to overall development of such companies

(Ainsworth, Partington & Warren, 2015). With the reduction of the tax rate of the companies,

the company is free to use the extra amount of money and resources for innovative activities

which can lead to overall development of the business (Weil, Schipper & Francis, 2013). The

lower tax structure for a corporate entity not only means reduced costs but also means surplus

profits which is gained because of savings which is done through tax savings (Fernández-

Rodríguez & Martínez-Arias, 2014). In addition to this, tax savings implies that the firm has

higher profits than expected and such profits can be used by businesses in any way possible

as per the decision. Thus, the facts show that if the rate of tax is reduced than there will be an

increase in the overall investments in the country. It is also clear from the above analysis that

lowering the taxes will only be benefiting the foreign investors and the low tax structure will

attract them in the market.

ACCOUNTING AND FINANCE

On the other hand, there are certain advantages of reducing the tax structure from the

point of view of the households and consumers as then they will be having a higher

percentage of profits in their hand which can be used for consumption purposes or even can

be used for savings purposes. The dividend imputation system which is followed in Australia

which is known to provide tax payers, residents and even the companies which are operating

in low income level can use such a system for franking credits (Vo et al., 2013). This is an

indirect indication that the lower income group companies will be paying lower amount of

taxes if the overall tax rate for companies are reduced and will results in more savings

generations for such companies which can lead to overall development of such companies

(Ainsworth, Partington & Warren, 2015). With the reduction of the tax rate of the companies,

the company is free to use the extra amount of money and resources for innovative activities

which can lead to overall development of the business (Weil, Schipper & Francis, 2013). The

lower tax structure for a corporate entity not only means reduced costs but also means surplus

profits which is gained because of savings which is done through tax savings (Fernández-

Rodríguez & Martínez-Arias, 2014). In addition to this, tax savings implies that the firm has

higher profits than expected and such profits can be used by businesses in any way possible

as per the decision. Thus, the facts show that if the rate of tax is reduced than there will be an

increase in the overall investments in the country. It is also clear from the above analysis that

lowering the taxes will only be benefiting the foreign investors and the low tax structure will

attract them in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING AND FINANCE

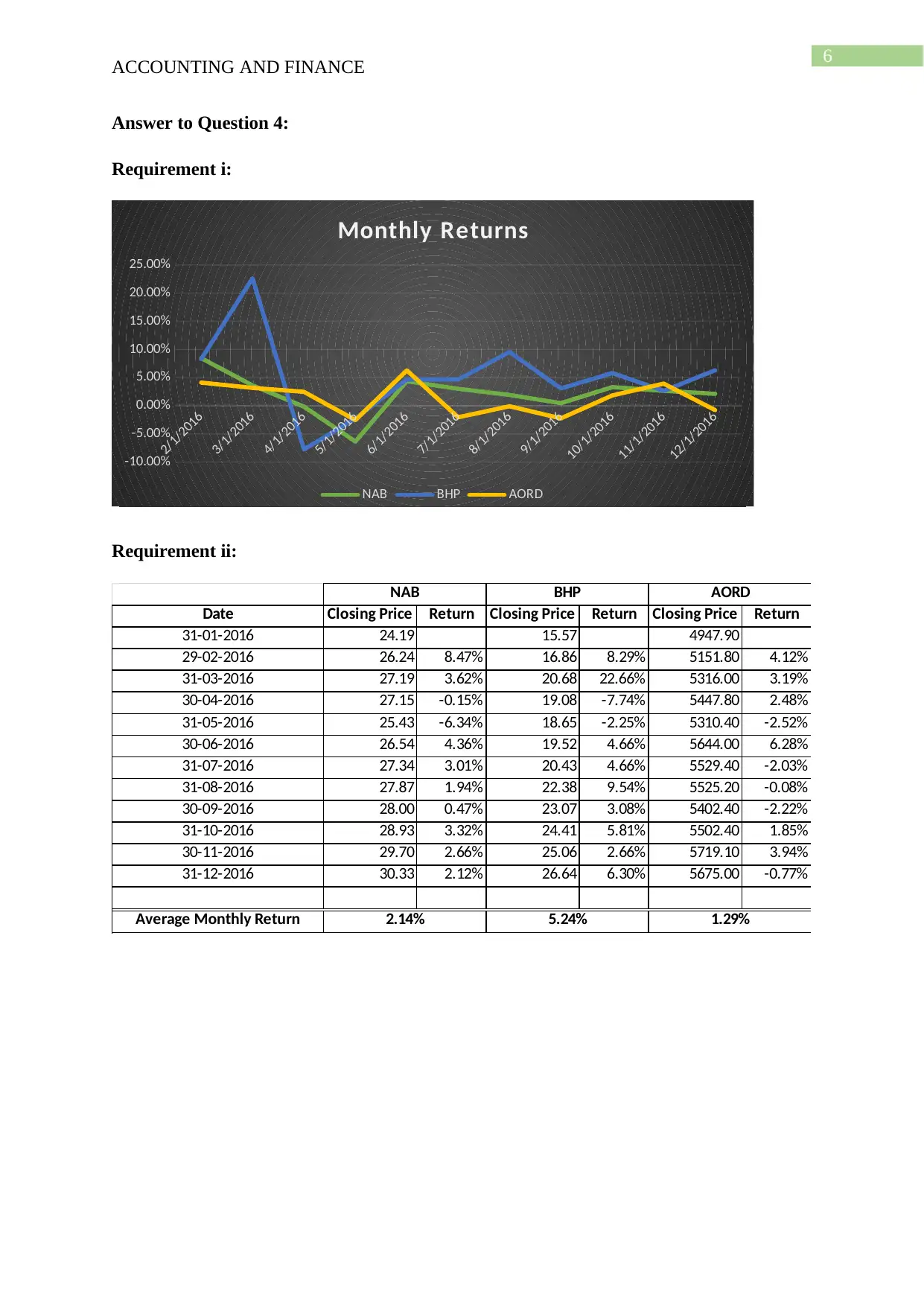

Answer to Question 4:

Requirement i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Monthly Returns

NAB BHP AORD

Requirement ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

ACCOUNTING AND FINANCE

Answer to Question 4:

Requirement i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Monthly Returns

NAB BHP AORD

Requirement ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

Requirement iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Requirement iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

ACCOUNTING AND FINANCE

Requirement iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Requirement iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

8

ACCOUNTING AND FINANCE

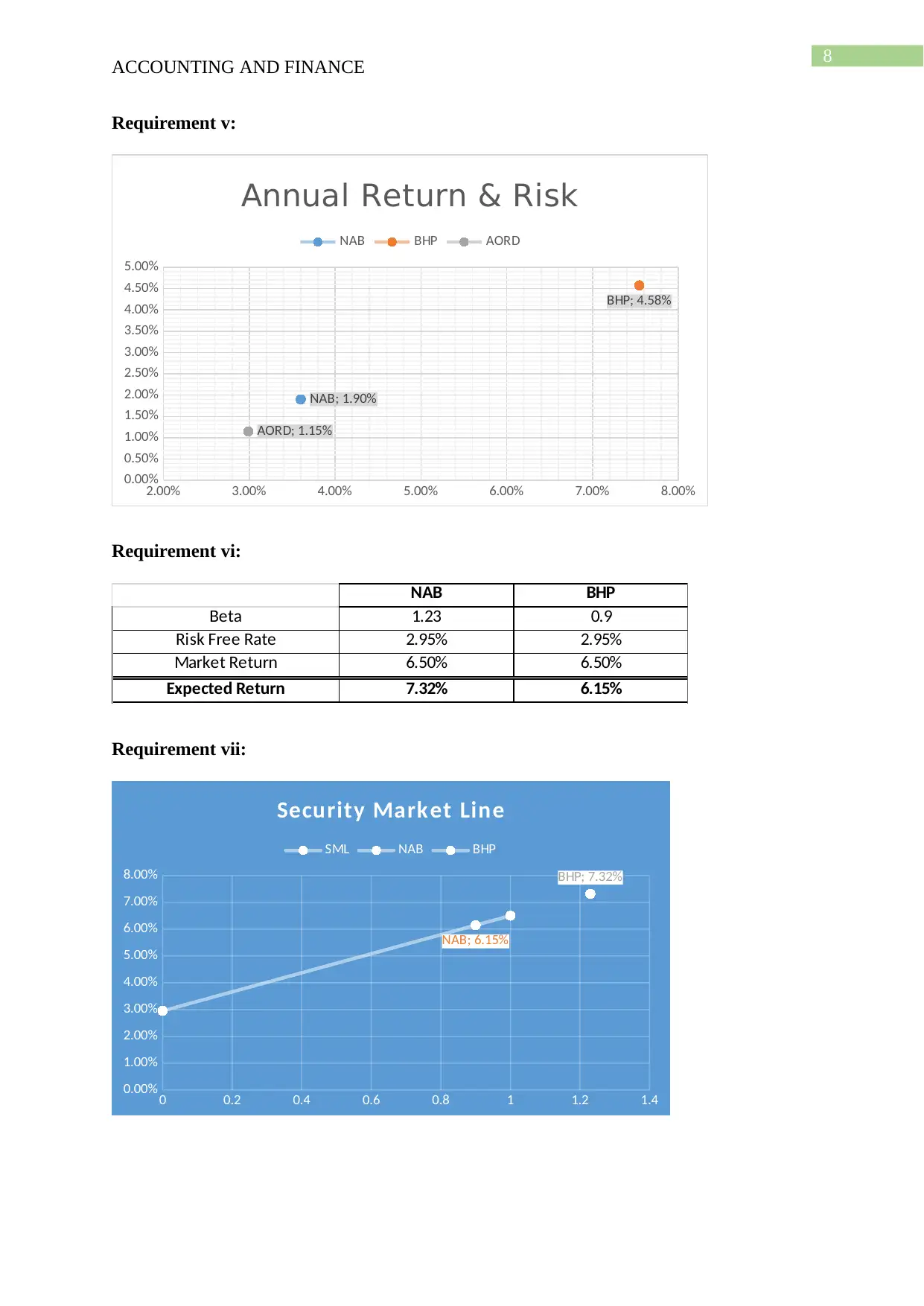

Requirement v:

2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

AORD; 1.15%

BHP; 4.58%

NAB; 1.90%

Annual Return & Risk

NAB BHP AORD

Requirement vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Requirement vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00% BHP; 7.32%

NAB; 6.15%

Security Market Line

SML NAB BHP

ACCOUNTING AND FINANCE

Requirement v:

2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

AORD; 1.15%

BHP; 4.58%

NAB; 1.90%

Annual Return & Risk

NAB BHP AORD

Requirement vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Requirement vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00% BHP; 7.32%

NAB; 6.15%

Security Market Line

SML NAB BHP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING AND FINANCE

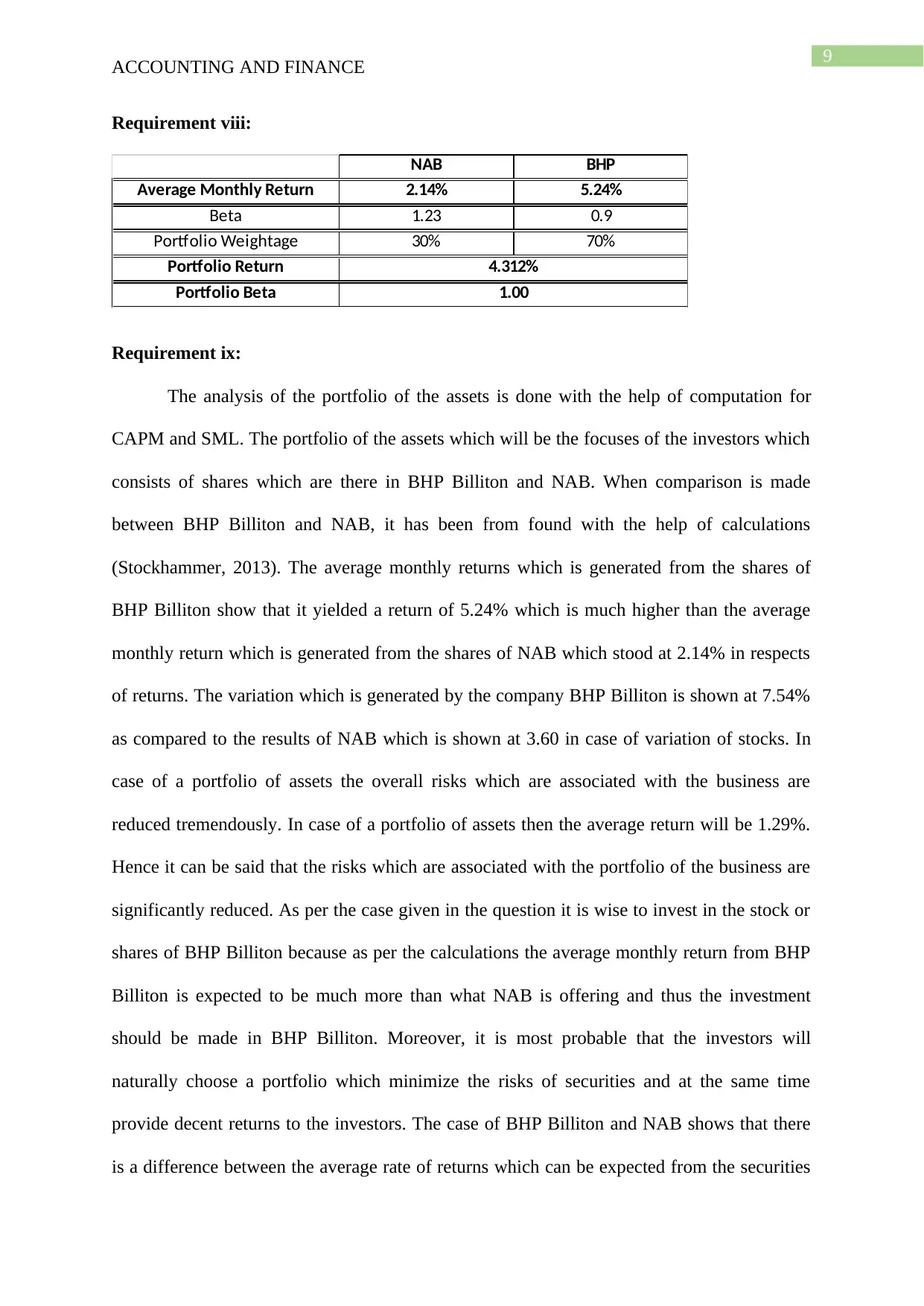

Requirement viii:

Average Monthly Return

Beta

Portfolio Weightage

Portfolio Return

Portfolio Beta

NAB BHP

4.312%

1.00

2.14%

1.23

70%30%

5.24%

0.9

Requirement ix:

The analysis of the portfolio of the assets is done with the help of computation for

CAPM and SML. The portfolio of the assets which will be the focuses of the investors which

consists of shares which are there in BHP Billiton and NAB. When comparison is made

between BHP Billiton and NAB, it has been from found with the help of calculations

(Stockhammer, 2013). The average monthly returns which is generated from the shares of

BHP Billiton show that it yielded a return of 5.24% which is much higher than the average

monthly return which is generated from the shares of NAB which stood at 2.14% in respects

of returns. The variation which is generated by the company BHP Billiton is shown at 7.54%

as compared to the results of NAB which is shown at 3.60 in case of variation of stocks. In

case of a portfolio of assets the overall risks which are associated with the business are

reduced tremendously. In case of a portfolio of assets then the average return will be 1.29%.

Hence it can be said that the risks which are associated with the portfolio of the business are

significantly reduced. As per the case given in the question it is wise to invest in the stock or

shares of BHP Billiton because as per the calculations the average monthly return from BHP

Billiton is expected to be much more than what NAB is offering and thus the investment

should be made in BHP Billiton. Moreover, it is most probable that the investors will

naturally choose a portfolio which minimize the risks of securities and at the same time

provide decent returns to the investors. The case of BHP Billiton and NAB shows that there

is a difference between the average rate of returns which can be expected from the securities

ACCOUNTING AND FINANCE

Requirement viii:

Average Monthly Return

Beta

Portfolio Weightage

Portfolio Return

Portfolio Beta

NAB BHP

4.312%

1.00

2.14%

1.23

70%30%

5.24%

0.9

Requirement ix:

The analysis of the portfolio of the assets is done with the help of computation for

CAPM and SML. The portfolio of the assets which will be the focuses of the investors which

consists of shares which are there in BHP Billiton and NAB. When comparison is made

between BHP Billiton and NAB, it has been from found with the help of calculations

(Stockhammer, 2013). The average monthly returns which is generated from the shares of

BHP Billiton show that it yielded a return of 5.24% which is much higher than the average

monthly return which is generated from the shares of NAB which stood at 2.14% in respects

of returns. The variation which is generated by the company BHP Billiton is shown at 7.54%

as compared to the results of NAB which is shown at 3.60 in case of variation of stocks. In

case of a portfolio of assets the overall risks which are associated with the business are

reduced tremendously. In case of a portfolio of assets then the average return will be 1.29%.

Hence it can be said that the risks which are associated with the portfolio of the business are

significantly reduced. As per the case given in the question it is wise to invest in the stock or

shares of BHP Billiton because as per the calculations the average monthly return from BHP

Billiton is expected to be much more than what NAB is offering and thus the investment

should be made in BHP Billiton. Moreover, it is most probable that the investors will

naturally choose a portfolio which minimize the risks of securities and at the same time

provide decent returns to the investors. The case of BHP Billiton and NAB shows that there

is a difference between the average rate of returns which can be expected from the securities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING AND FINANCE

of both the companies and it is on the basis of this information that the decision of investing

in one of such a shares or portfolio is to be taken (Rutterford & Sotiropoulos, 2016).

ACCOUNTING AND FINANCE

of both the companies and it is on the basis of this information that the decision of investing

in one of such a shares or portfolio is to be taken (Rutterford & Sotiropoulos, 2016).

11

ACCOUNTING AND FINANCE

References list:

Ainsworth, A. B., Partington, G., & Warren, G. (2015). Do franking credits matter?

Exploring the financial implications of dividend imputation.

Evers, L., Miller, H., & Spengel, C. (2015). Intellectual property box regimes: effective tax

rates and tax policy considerations. International Tax and Public Finance, 22(3), 502-530.

Fernández-Rodríguez, E., & Martínez-Arias, A. (2014). Determinants of the effective tax rate

in the BRIC countries. Emerging Markets Finance and Trade, 50(sup3), 214-228.

Gale, W. G., Samwick, A. A., & Center, U. B. T. P. (2014). Effects of income tax changes on

economic growth. Economic Studies, https://www. brookings.

edu/wpcontent/uploads/2016/06/09_Effects_Income_Tax_Changes_Economic_Growth_G

ale_Sa mwick. pdf.

Rutterford, J. & Sotiropoulos, D.P., (2016). Financial diversification before modern portfolio

theory: UK financial advice documents in the late nineteenth and the beginning of the

twentieth century. The European Journal of the History of Economic Thought, 23(6),

pp.919-945.

Stockhammer, E. (2013). Why have wage shares fallen? An analysis of the determinants of

functional income distribution. In Wage-led growth (pp. 40-70). Palgrave Macmillan,

London.

Vo, D., Gellard, B., Mero, S., & Authority, E. R. (2013, April). Estimating the market value

of franking credits: Empirical evidence from Australia. In Conference Paper, Australian

Conference of Economists.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

ACCOUNTING AND FINANCE

References list:

Ainsworth, A. B., Partington, G., & Warren, G. (2015). Do franking credits matter?

Exploring the financial implications of dividend imputation.

Evers, L., Miller, H., & Spengel, C. (2015). Intellectual property box regimes: effective tax

rates and tax policy considerations. International Tax and Public Finance, 22(3), 502-530.

Fernández-Rodríguez, E., & Martínez-Arias, A. (2014). Determinants of the effective tax rate

in the BRIC countries. Emerging Markets Finance and Trade, 50(sup3), 214-228.

Gale, W. G., Samwick, A. A., & Center, U. B. T. P. (2014). Effects of income tax changes on

economic growth. Economic Studies, https://www. brookings.

edu/wpcontent/uploads/2016/06/09_Effects_Income_Tax_Changes_Economic_Growth_G

ale_Sa mwick. pdf.

Rutterford, J. & Sotiropoulos, D.P., (2016). Financial diversification before modern portfolio

theory: UK financial advice documents in the late nineteenth and the beginning of the

twentieth century. The European Journal of the History of Economic Thought, 23(6),

pp.919-945.

Stockhammer, E. (2013). Why have wage shares fallen? An analysis of the determinants of

functional income distribution. In Wage-led growth (pp. 40-70). Palgrave Macmillan,

London.

Vo, D., Gellard, B., Mero, S., & Authority, E. R. (2013, April). Estimating the market value

of franking credits: Empirical evidence from Australia. In Conference Paper, Australian

Conference of Economists.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.