Finance Assignment: Interest Rates, Taxation, and Investment Analysis

VerifiedAdded on 2023/04/19

|14

|1587

|284

Homework Assignment

AI Summary

This finance assignment solution provides a detailed analysis of various financial concepts. It begins with the calculation of effective interest rates for different payment options, followed by the determination of monthly contributions for an annuity. The assignment then delves into the Australian taxation system, specifically the dividend imputation system, comparing it to the classical taxation system. It illustrates the impact of corporate tax rates and imputation credits on shareholders. Furthermore, the assignment includes calculations of monthly and annual holding period returns, standard deviation, and the application of the CAPM model for stock valuation. It also covers portfolio analysis, including the determination of optimal portfolio weights and an investment recommendation based on the analysis of index performance and individual stocks.

ACCOUNTING & FINANCE

[Document subtitle]

[DATE]

[Company name]

[Company address]

[Document subtitle]

[DATE]

[Company name]

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

(a) (i) Effective interest rate would be taken into consideration to find the suitable payment

option for Jayne.

Option 1

It includes a nominal interest rate of 4.55% per annum which compounded weekly.

Option 2

It includes a nominal interest rate of 4.75% per annum which compounded weekly.

It can be observed from the above computation that effective interest rate comes out to be

inferior for option 1 (when nominal interest rate is 4.55%). Therefore, it Jayne should use

option 1 payment option.

(ii) The total number of weeks for the instalment amount has been calculated through the

formula as shown below.

1

(a) (i) Effective interest rate would be taken into consideration to find the suitable payment

option for Jayne.

Option 1

It includes a nominal interest rate of 4.55% per annum which compounded weekly.

Option 2

It includes a nominal interest rate of 4.75% per annum which compounded weekly.

It can be observed from the above computation that effective interest rate comes out to be

inferior for option 1 (when nominal interest rate is 4.55%). Therefore, it Jayne should use

option 1 payment option.

(ii) The total number of weeks for the instalment amount has been calculated through the

formula as shown below.

1

Hence, there would be 657.85 weeks.

(b) (i) Contribution in every month = $X

FV of annuity (after 18 years) =$200,000

Jennifer is contributing 30% of the total amount and therefore, the monthly payment is

computed below.

Monthly payment = 30% of P = 0.30 * 734.11 = $220.2

(ii) The total payment that Jennifer would get at the age of 28 years has been computed as

highlighted below.

On her 18th birthday, the total amount remains to Jennifer

2

(b) (i) Contribution in every month = $X

FV of annuity (after 18 years) =$200,000

Jennifer is contributing 30% of the total amount and therefore, the monthly payment is

computed below.

Monthly payment = 30% of P = 0.30 * 734.11 = $220.2

(ii) The total payment that Jennifer would get at the age of 28 years has been computed as

highlighted below.

On her 18th birthday, the total amount remains to Jennifer

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

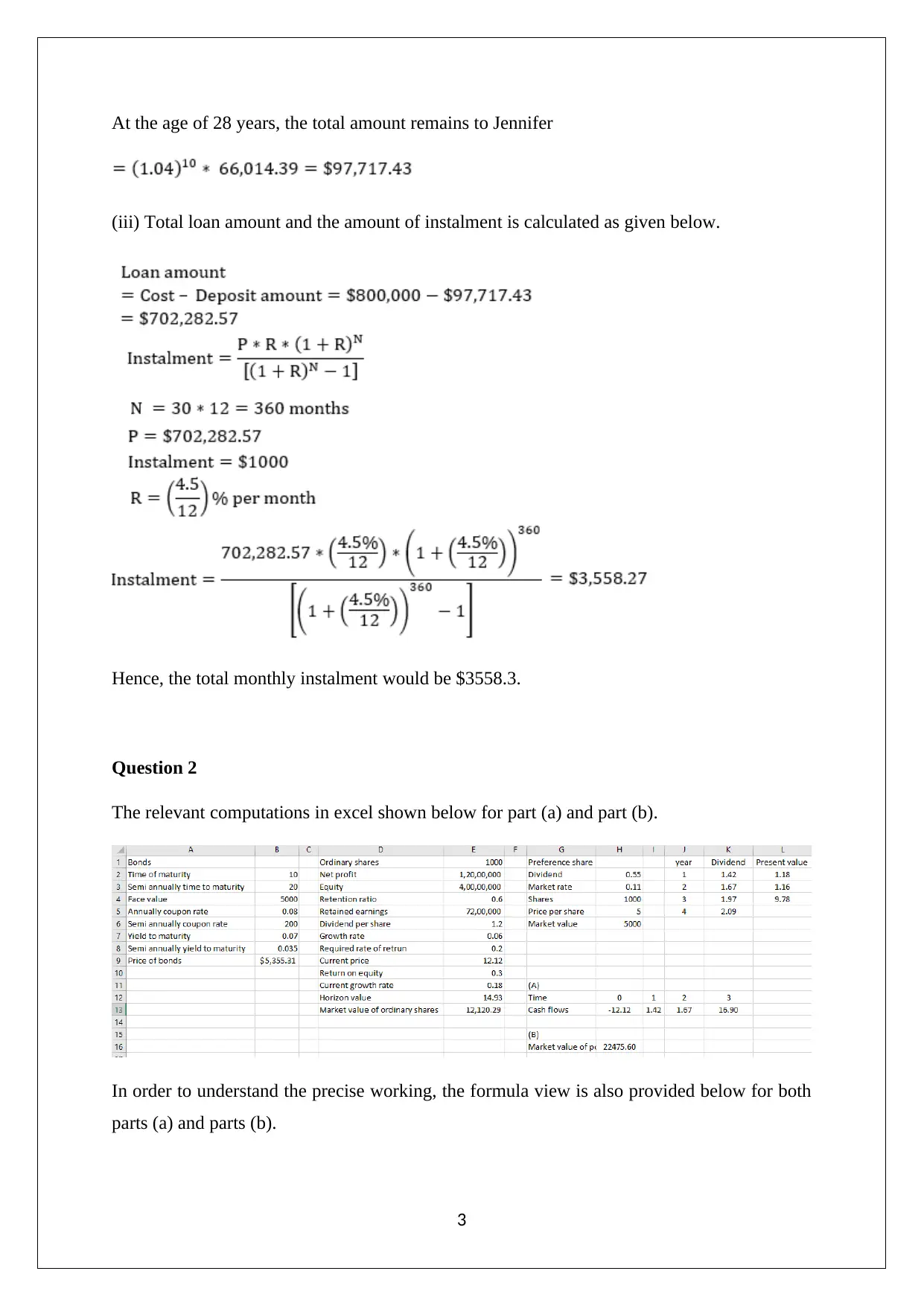

At the age of 28 years, the total amount remains to Jennifer

(iii) Total loan amount and the amount of instalment is calculated as given below.

Hence, the total monthly instalment would be $3558.3.

Question 2

The relevant computations in excel shown below for part (a) and part (b).

In order to understand the precise working, the formula view is also provided below for both

parts (a) and parts (b).

3

(iii) Total loan amount and the amount of instalment is calculated as given below.

Hence, the total monthly instalment would be $3558.3.

Question 2

The relevant computations in excel shown below for part (a) and part (b).

In order to understand the precise working, the formula view is also provided below for both

parts (a) and parts (b).

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

The taxation system prevalent in Australia is unique and different from the classical taxation

system that is prevalent in the developed countries with the noticeable exception of New

Zealand. The key aspect is the3 dividend imputation system which ensures that there is no

double taxation of the corporate profits first at the end of the corporate and secondly at the

end of the shareholders. This goes against the established practice followed in the developed

countries whereby the corporate profits are taxed at the corporate tax rate. Further, when

these companies decide to distribute the surplus post-tax profits as dividends to shareholders,

then the tax is levied on the dividends which are considered as taxable personal income for

the shareholders (Brealey, Myers & Allen, 2014). This practice does against the global

established practice of taxing one income only once and hence imputation credits are given to

the shareholders which ensure that the tax burden on them is minimised. The net impact of

this practice is that the effective tax rates when both the company and shareholders are

considered tend to be significantly lower under the dividend imputation system as compared

to the classical tax system (Petty et. al., 2015).

The above understanding can be illustrated with a numerical example. Firstly, consider the

classical taxation system where the corporate income tax rate is 30% and assume that the

average marginal personal income tax rate for the shareholders is also the same i.e. 30%.

Consider the pre-tax corporate profits as $ 100,000. After payment of corporate tax to the

tune of $ 30,000, the profit after tax comes out as $ 70,000. Assume that all of this is

distributed amongst the shareholders who would collectively pay a personal income tax of $

21,000 which would imply $ 49,000 to be received by the shareholders post tax. In the

process, the effective tax rate has come out as 51%. Now, it is imperative to present the above

scenario in the Australian taxation system. The corporate tax is 30% and hence $ 30,000 is

paid as taxes to yield $ 70,000 as the post-tax income. The whole amount is paid as dividends

4

The taxation system prevalent in Australia is unique and different from the classical taxation

system that is prevalent in the developed countries with the noticeable exception of New

Zealand. The key aspect is the3 dividend imputation system which ensures that there is no

double taxation of the corporate profits first at the end of the corporate and secondly at the

end of the shareholders. This goes against the established practice followed in the developed

countries whereby the corporate profits are taxed at the corporate tax rate. Further, when

these companies decide to distribute the surplus post-tax profits as dividends to shareholders,

then the tax is levied on the dividends which are considered as taxable personal income for

the shareholders (Brealey, Myers & Allen, 2014). This practice does against the global

established practice of taxing one income only once and hence imputation credits are given to

the shareholders which ensure that the tax burden on them is minimised. The net impact of

this practice is that the effective tax rates when both the company and shareholders are

considered tend to be significantly lower under the dividend imputation system as compared

to the classical tax system (Petty et. al., 2015).

The above understanding can be illustrated with a numerical example. Firstly, consider the

classical taxation system where the corporate income tax rate is 30% and assume that the

average marginal personal income tax rate for the shareholders is also the same i.e. 30%.

Consider the pre-tax corporate profits as $ 100,000. After payment of corporate tax to the

tune of $ 30,000, the profit after tax comes out as $ 70,000. Assume that all of this is

distributed amongst the shareholders who would collectively pay a personal income tax of $

21,000 which would imply $ 49,000 to be received by the shareholders post tax. In the

process, the effective tax rate has come out as 51%. Now, it is imperative to present the above

scenario in the Australian taxation system. The corporate tax is 30% and hence $ 30,000 is

paid as taxes to yield $ 70,000 as the post-tax income. The whole amount is paid as dividends

4

under the assumption that the marginal tax rate for the shareholders is 30%. Total imputation

credits that collectively the shareholders would receive is (70000/(1-0.3)) – 70000 = $

30,000. Hence, total representation in the taxable income of shareholders on account of the

dividend would be $ 70,000 + $ 30,000 = $ 100,000. Since the marginal personal income tax

rate is 30%, hence tax on the dividend income is $ 30,000 which is the imputation credit

already available and hence net tax payable by the shareholder is zero. Thus, in this case, the

total post tax cashflow that shareholders would receive would be $ 70,000 making the

effective tax rate as 30% (Parrino & Kidwell, 2014).

Considering the important role that tax plays in business decisions, there is demand from

various businesses (both domestic and foreign) that corporate tax rate should be lowered in

Australia. This has further intensified in the wake of tax cuts by US and some other

developed countries which tend to adhere to the classical taxation system (Taylor, 2018).

However, in this demand, a pivotal aspect that is that even though the developed nations may

have lower corporate tax rate than Australia, but the effective rate would not vary much

owing to the imputation credit system in Australia (Montgomery, 2018). Further, if the

government would indeed take a cut in the corporate tax rate, then the franking credits

available to the shareholders would decline and thereby burden on taxation would shift to the

shareholders, which is not quite advantageous to the domestic companies. However, this

would be highly useful for foreign companies based in Australia which do not tend to pay

dividends to local shareholders but tend to repatriate profits (Smith, 2015).

Question 4

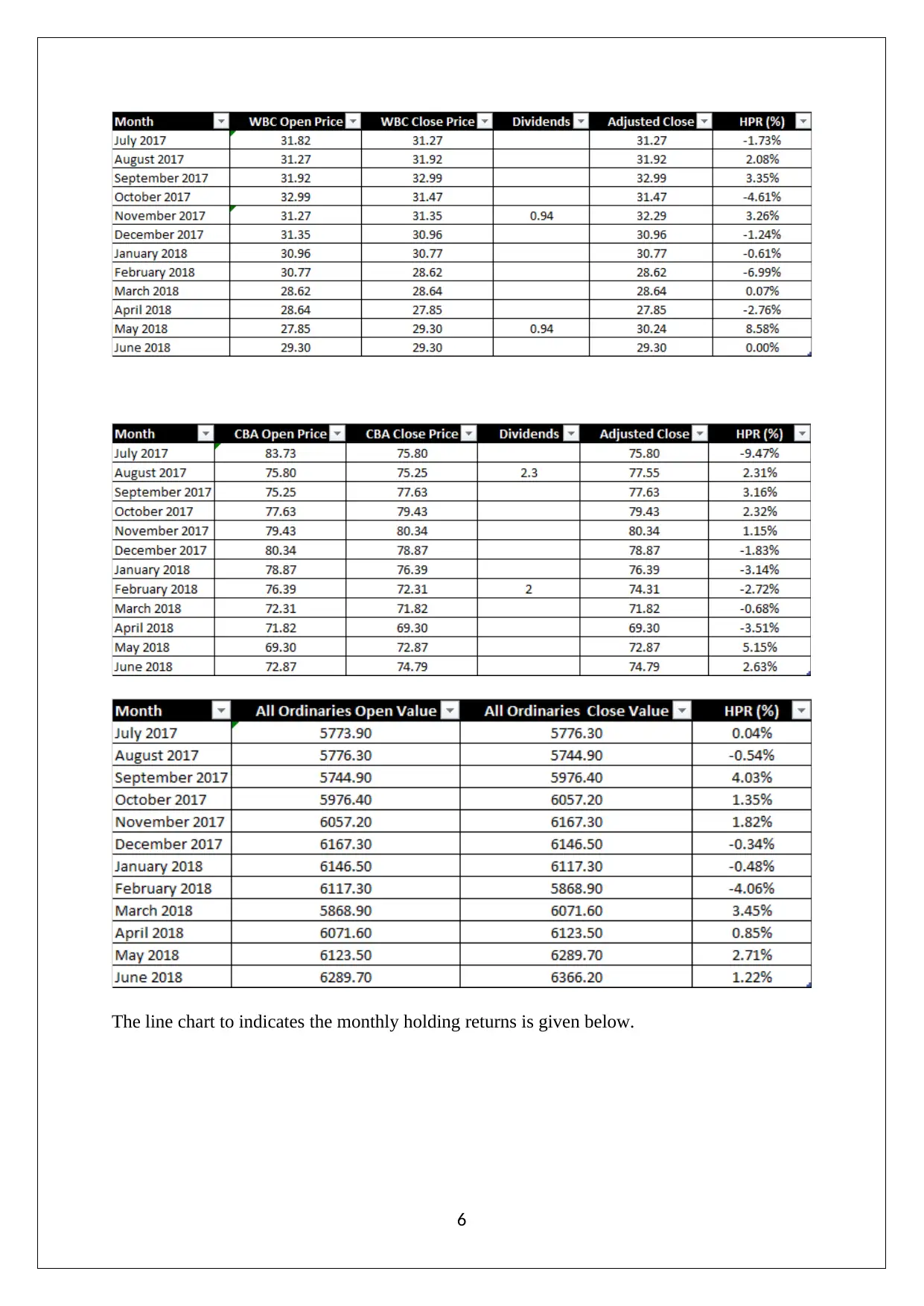

(1) The monthly holding returns has been computed for stocks and index and is shown below

in the table.

Formula used

5

credits that collectively the shareholders would receive is (70000/(1-0.3)) – 70000 = $

30,000. Hence, total representation in the taxable income of shareholders on account of the

dividend would be $ 70,000 + $ 30,000 = $ 100,000. Since the marginal personal income tax

rate is 30%, hence tax on the dividend income is $ 30,000 which is the imputation credit

already available and hence net tax payable by the shareholder is zero. Thus, in this case, the

total post tax cashflow that shareholders would receive would be $ 70,000 making the

effective tax rate as 30% (Parrino & Kidwell, 2014).

Considering the important role that tax plays in business decisions, there is demand from

various businesses (both domestic and foreign) that corporate tax rate should be lowered in

Australia. This has further intensified in the wake of tax cuts by US and some other

developed countries which tend to adhere to the classical taxation system (Taylor, 2018).

However, in this demand, a pivotal aspect that is that even though the developed nations may

have lower corporate tax rate than Australia, but the effective rate would not vary much

owing to the imputation credit system in Australia (Montgomery, 2018). Further, if the

government would indeed take a cut in the corporate tax rate, then the franking credits

available to the shareholders would decline and thereby burden on taxation would shift to the

shareholders, which is not quite advantageous to the domestic companies. However, this

would be highly useful for foreign companies based in Australia which do not tend to pay

dividends to local shareholders but tend to repatriate profits (Smith, 2015).

Question 4

(1) The monthly holding returns has been computed for stocks and index and is shown below

in the table.

Formula used

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

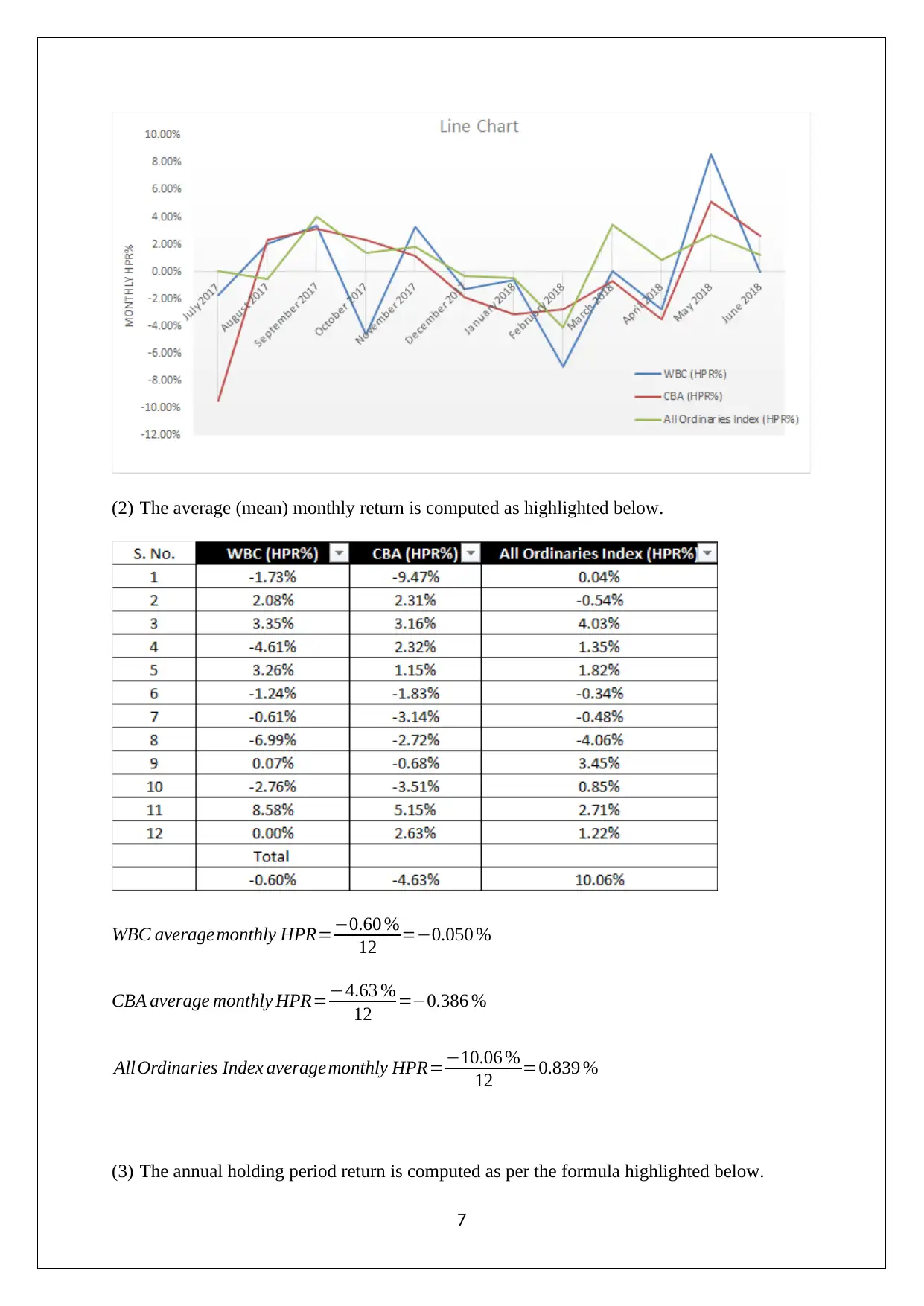

The line chart to indicates the monthly holding returns is given below.

6

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(2) The average (mean) monthly return is computed as highlighted below.

WBC averagemonthly HPR=−0.60 %

12 =−0.050 %

CBA average monthly HPR=−4.63 %

12 =−0.386 %

AllOrdinaries Index averagemonthly HPR=−10.06 %

12 =0.839 %

(3) The annual holding period return is computed as per the formula highlighted below.

7

WBC averagemonthly HPR=−0.60 %

12 =−0.050 %

CBA average monthly HPR=−4.63 %

12 =−0.386 %

AllOrdinaries Index averagemonthly HPR=−10.06 %

12 =0.839 %

(3) The annual holding period return is computed as per the formula highlighted below.

7

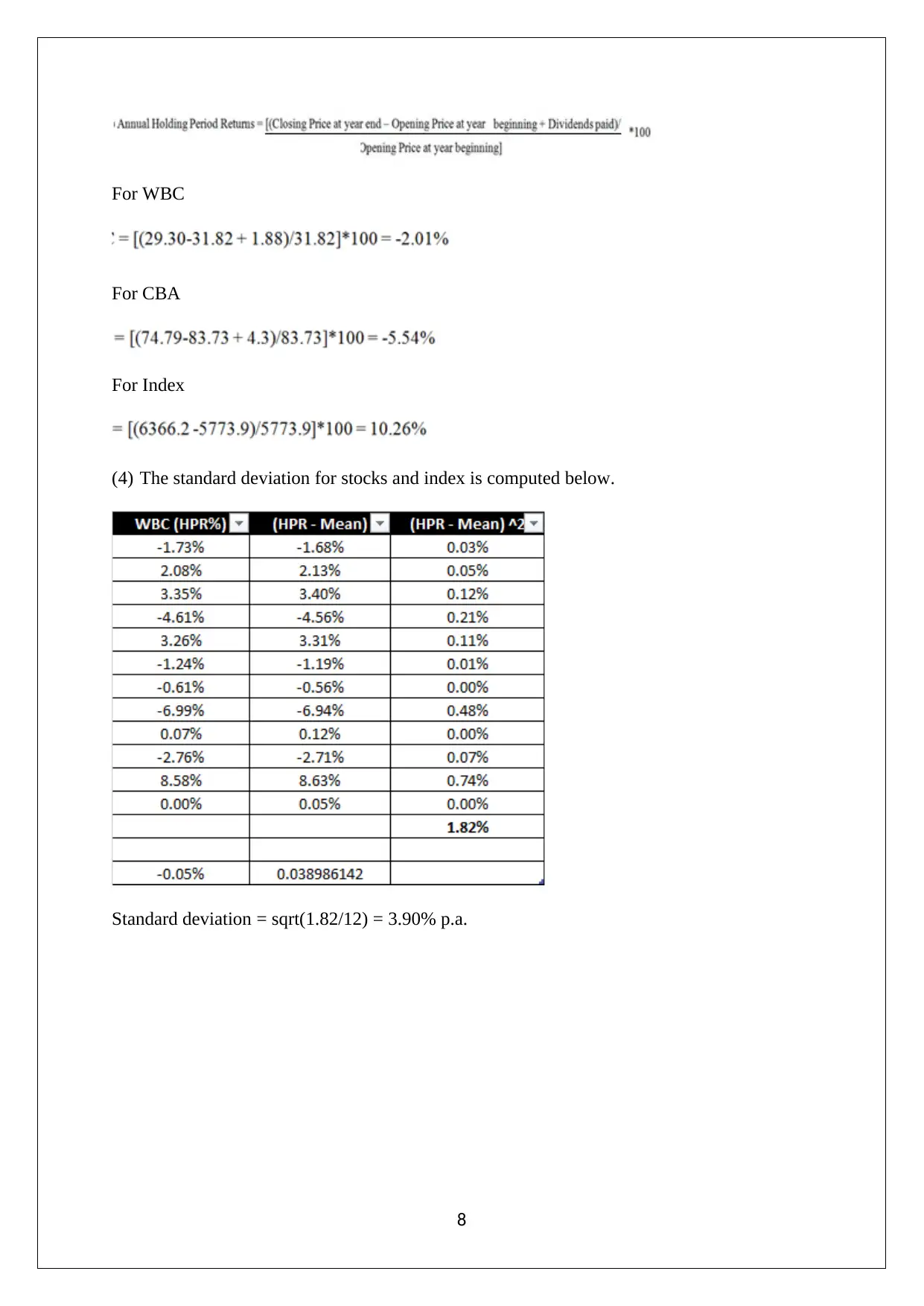

For WBC

For CBA

For Index

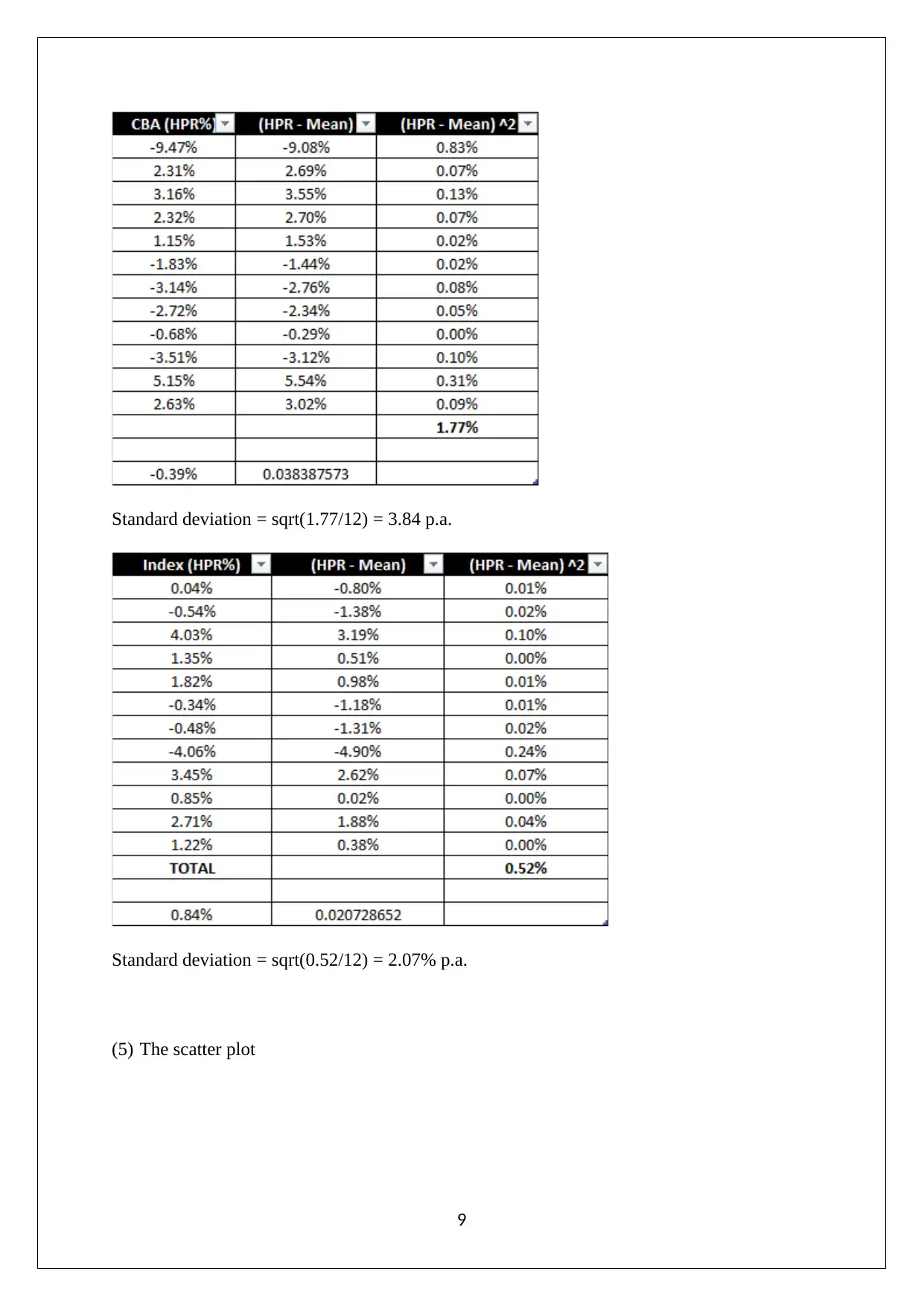

(4) The standard deviation for stocks and index is computed below.

Standard deviation = sqrt(1.82/12) = 3.90% p.a.

8

For CBA

For Index

(4) The standard deviation for stocks and index is computed below.

Standard deviation = sqrt(1.82/12) = 3.90% p.a.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard deviation = sqrt(1.77/12) = 3.84 p.a.

Standard deviation = sqrt(0.52/12) = 2.07% p.a.

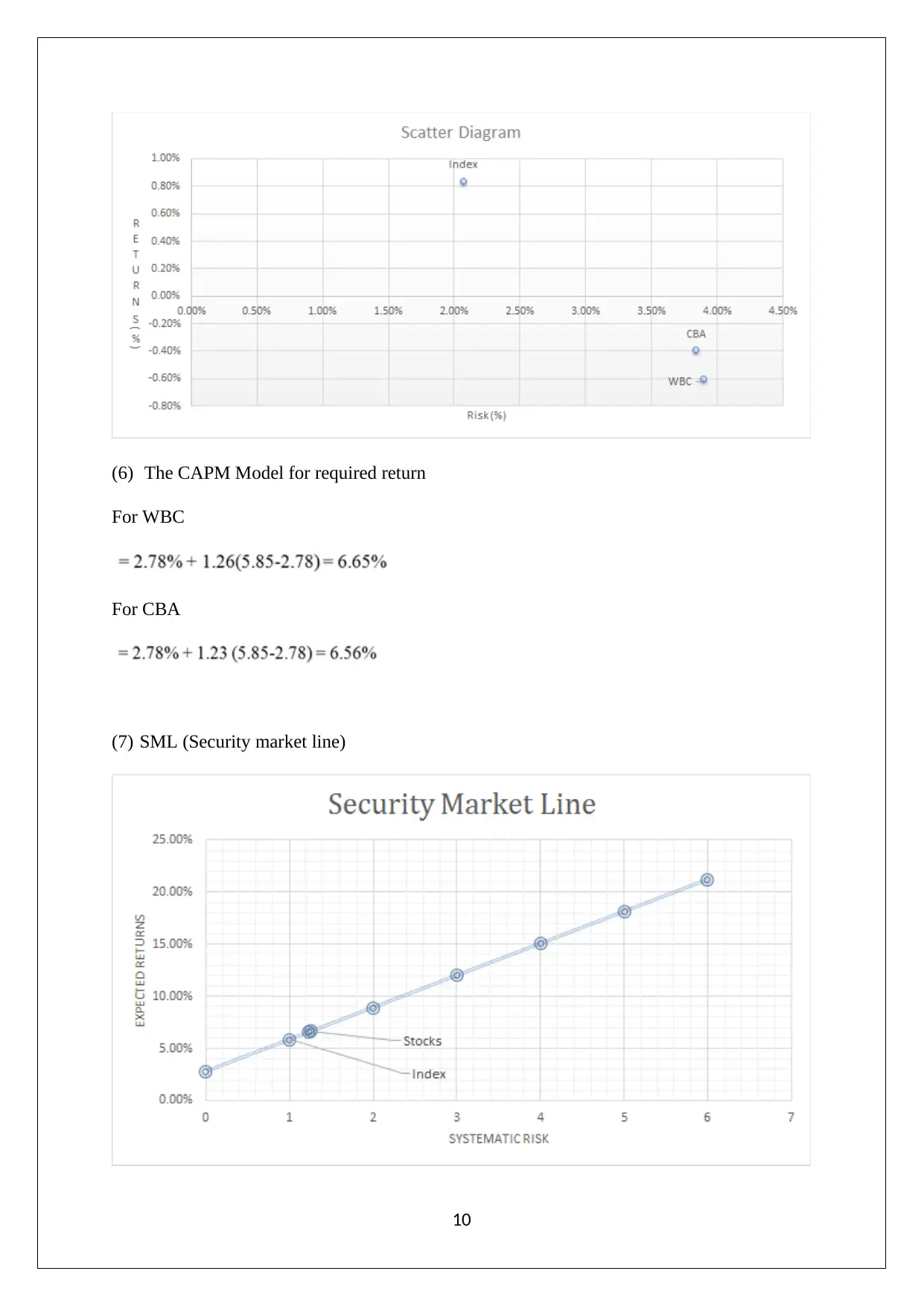

(5) The scatter plot

9

Standard deviation = sqrt(0.52/12) = 2.07% p.a.

(5) The scatter plot

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(6) The CAPM Model for required return

For WBC

For CBA

(7) SML (Security market line)

10

For WBC

For CBA

(7) SML (Security market line)

10

(8) Weightage for WBC stock would be 40% and CBA stock would be 60%.

Return = {60%*(-0.39)} + {40% * (-0.60)} = -0.47 p.m.

Beta value = {60%*(1.23)} + {40% *(1.26)} = 1.242

(9) The above analysis clearly reflects that investment in the Index (i.e. ASX/S&P 200)

would be the most superior option for the investor. This is because the underlying risk

associated with the index is lesser when compared to the individuals stocks or their portfolio.

Additionally, taking the 2017/2018 performance as the benchmark, it is apparent that the

returns are also superior for the index when compared to the individuals stocks or their

portfolio (Brealey, Myers & Allen, 2014).

11

Return = {60%*(-0.39)} + {40% * (-0.60)} = -0.47 p.m.

Beta value = {60%*(1.23)} + {40% *(1.26)} = 1.242

(9) The above analysis clearly reflects that investment in the Index (i.e. ASX/S&P 200)

would be the most superior option for the investor. This is because the underlying risk

associated with the index is lesser when compared to the individuals stocks or their portfolio.

Additionally, taking the 2017/2018 performance as the benchmark, it is apparent that the

returns are also superior for the index when compared to the individuals stocks or their

portfolio (Brealey, Myers & Allen, 2014).

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14