UGB 163: Financial Statement Analysis and Investment Appraisal

VerifiedAdded on 2023/06/16

|14

|3574

|58

Report

AI Summary

This report provides a comprehensive financial analysis of Tom and Jerry Ltd., including the preparation of an income statement and balance sheet for the year ending December 31, 2020. It calculates key financial metrics such as gross profit, net profit, and total assets and liabilities. The report also ...

UGB 163 Introduction

to Accounting and

Finance

to Accounting and

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Accounting is defined as a method in which day to day record of certain task is being handled

and on other side when ansh defined as a why the term that emphasize on managing the assets

and liabilities of the particular business. Both the terms are basically important for the business

as they are are helps in installation the financial position of an organisation. Accuracy in these

aspects helps in knowing the particular knowledge and the growth of the business which can we

take its effective decision. This report is is inducted into parts the first question is deal with the

preparation of income statement and balance sheet. second question will give the solution for

analysing the break even point and the margin of safety additional e analyse whether the

different types of budgets are related for all type of business or not. Third question will evaluate

the project for deciding that whether should be accepted or not and also analysed the advantage

and disadvantage of various techniques of investment appraisal. It also assess the pros and cons

of budget for making the business plan.

TASK

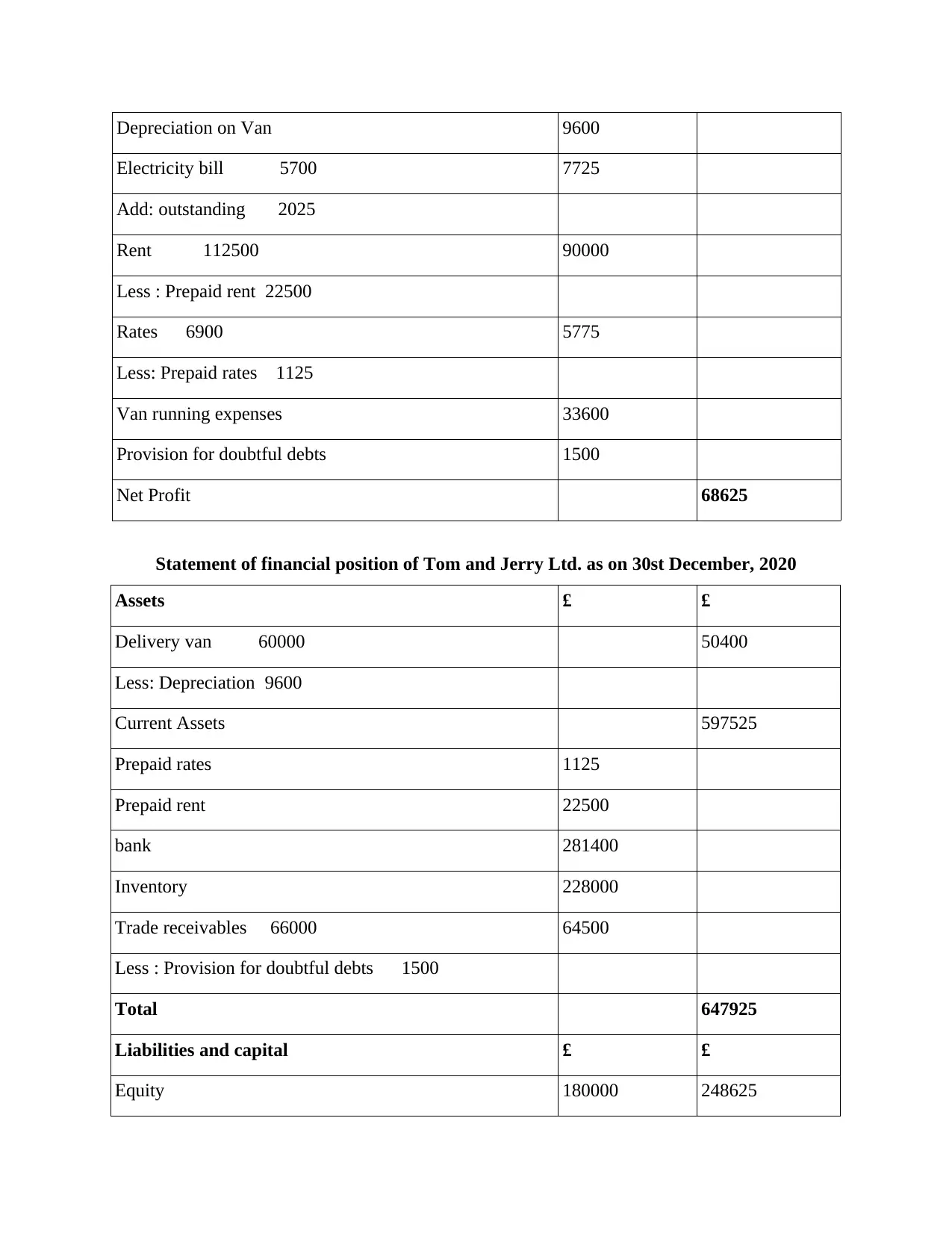

Question 1: Produce an income statement and balance sheet of Tom and Jerry Ltd.

Profit and loss account of Tom and Jerry Ltd. for the year ending 30st December, 2020

Particulars £ £

Sales revenue 633000

- Cash sales 504000

- Credit sales 129000

Less: Cost of goods sold 644175

Purchases (486000 + 39000) 525000

Wages 117000 119175

Add: Outstanding 2175

Add: Closing Stock 228000

Gross Profit 216825

Less: Operating Expenses 148200

Accounting is defined as a method in which day to day record of certain task is being handled

and on other side when ansh defined as a why the term that emphasize on managing the assets

and liabilities of the particular business. Both the terms are basically important for the business

as they are are helps in installation the financial position of an organisation. Accuracy in these

aspects helps in knowing the particular knowledge and the growth of the business which can we

take its effective decision. This report is is inducted into parts the first question is deal with the

preparation of income statement and balance sheet. second question will give the solution for

analysing the break even point and the margin of safety additional e analyse whether the

different types of budgets are related for all type of business or not. Third question will evaluate

the project for deciding that whether should be accepted or not and also analysed the advantage

and disadvantage of various techniques of investment appraisal. It also assess the pros and cons

of budget for making the business plan.

TASK

Question 1: Produce an income statement and balance sheet of Tom and Jerry Ltd.

Profit and loss account of Tom and Jerry Ltd. for the year ending 30st December, 2020

Particulars £ £

Sales revenue 633000

- Cash sales 504000

- Credit sales 129000

Less: Cost of goods sold 644175

Purchases (486000 + 39000) 525000

Wages 117000 119175

Add: Outstanding 2175

Add: Closing Stock 228000

Gross Profit 216825

Less: Operating Expenses 148200

Depreciation on Van 9600

Electricity bill 5700 7725

Add: outstanding 2025

Rent 112500 90000

Less : Prepaid rent 22500

Rates 6900 5775

Less: Prepaid rates 1125

Van running expenses 33600

Provision for doubtful debts 1500

Net Profit 68625

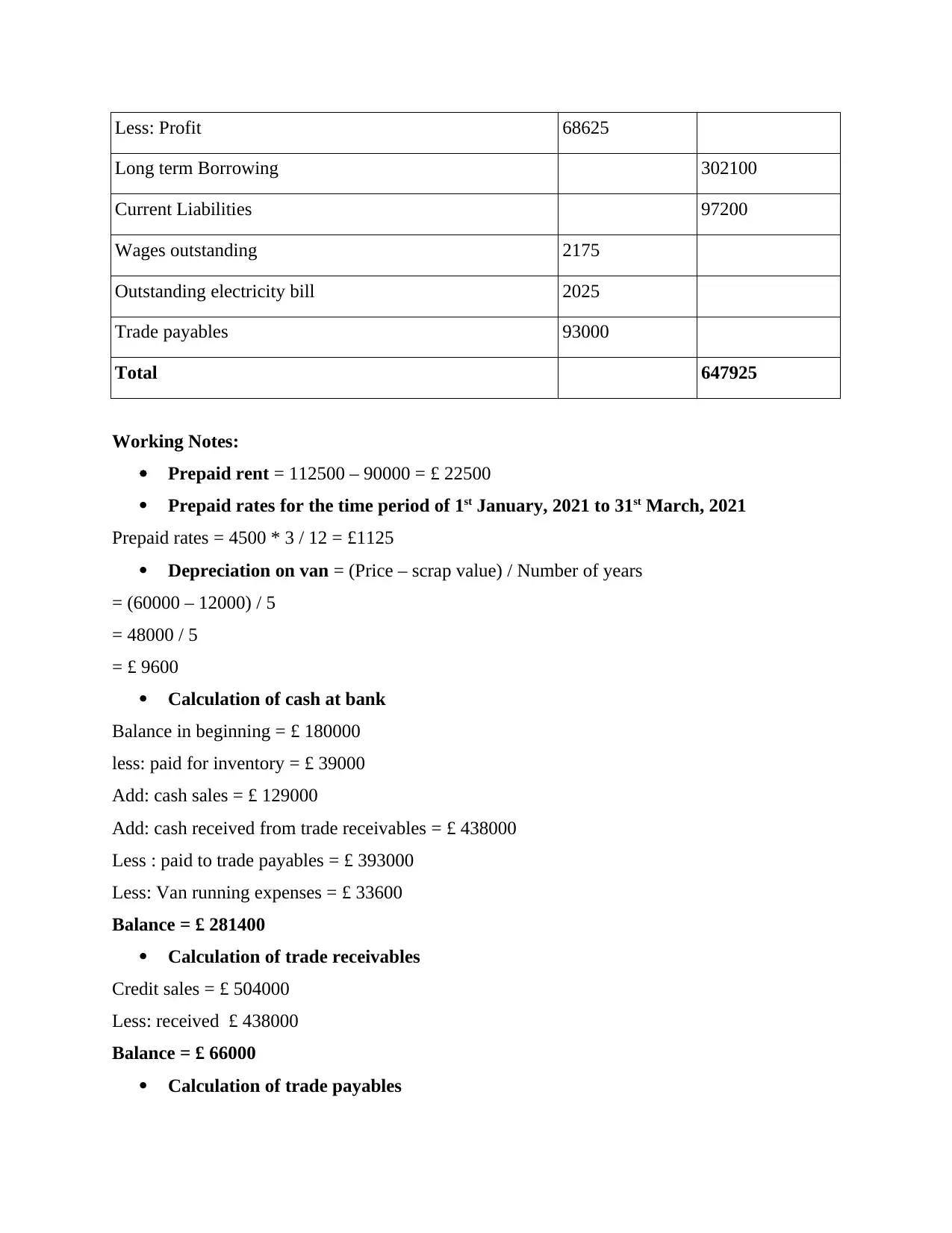

Statement of financial position of Tom and Jerry Ltd. as on 30st December, 2020

Assets £ £

Delivery van 60000 50400

Less: Depreciation 9600

Current Assets 597525

Prepaid rates 1125

Prepaid rent 22500

bank 281400

Inventory 228000

Trade receivables 66000 64500

Less : Provision for doubtful debts 1500

Total 647925

Liabilities and capital £ £

Equity 180000 248625

Electricity bill 5700 7725

Add: outstanding 2025

Rent 112500 90000

Less : Prepaid rent 22500

Rates 6900 5775

Less: Prepaid rates 1125

Van running expenses 33600

Provision for doubtful debts 1500

Net Profit 68625

Statement of financial position of Tom and Jerry Ltd. as on 30st December, 2020

Assets £ £

Delivery van 60000 50400

Less: Depreciation 9600

Current Assets 597525

Prepaid rates 1125

Prepaid rent 22500

bank 281400

Inventory 228000

Trade receivables 66000 64500

Less : Provision for doubtful debts 1500

Total 647925

Liabilities and capital £ £

Equity 180000 248625

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Profit 68625

Long term Borrowing 302100

Current Liabilities 97200

Wages outstanding 2175

Outstanding electricity bill 2025

Trade payables 93000

Total 647925

Working Notes:

Prepaid rent = 112500 – 90000 = £ 22500

Prepaid rates for the time period of 1st January, 2021 to 31st March, 2021

Prepaid rates = 4500 * 3 / 12 = £1125

Depreciation on van = (Price – scrap value) / Number of years

= (60000 – 12000) / 5

= 48000 / 5

= £ 9600

Calculation of cash at bank

Balance in beginning = £ 180000

less: paid for inventory = £ 39000

Add: cash sales = £ 129000

Add: cash received from trade receivables = £ 438000

Less : paid to trade payables = £ 393000

Less: Van running expenses = £ 33600

Balance = £ 281400

Calculation of trade receivables

Credit sales = £ 504000

Less: received £ 438000

Balance = £ 66000

Calculation of trade payables

Long term Borrowing 302100

Current Liabilities 97200

Wages outstanding 2175

Outstanding electricity bill 2025

Trade payables 93000

Total 647925

Working Notes:

Prepaid rent = 112500 – 90000 = £ 22500

Prepaid rates for the time period of 1st January, 2021 to 31st March, 2021

Prepaid rates = 4500 * 3 / 12 = £1125

Depreciation on van = (Price – scrap value) / Number of years

= (60000 – 12000) / 5

= 48000 / 5

= £ 9600

Calculation of cash at bank

Balance in beginning = £ 180000

less: paid for inventory = £ 39000

Add: cash sales = £ 129000

Add: cash received from trade receivables = £ 438000

Less : paid to trade payables = £ 393000

Less: Van running expenses = £ 33600

Balance = £ 281400

Calculation of trade receivables

Credit sales = £ 504000

Less: received £ 438000

Balance = £ 66000

Calculation of trade payables

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

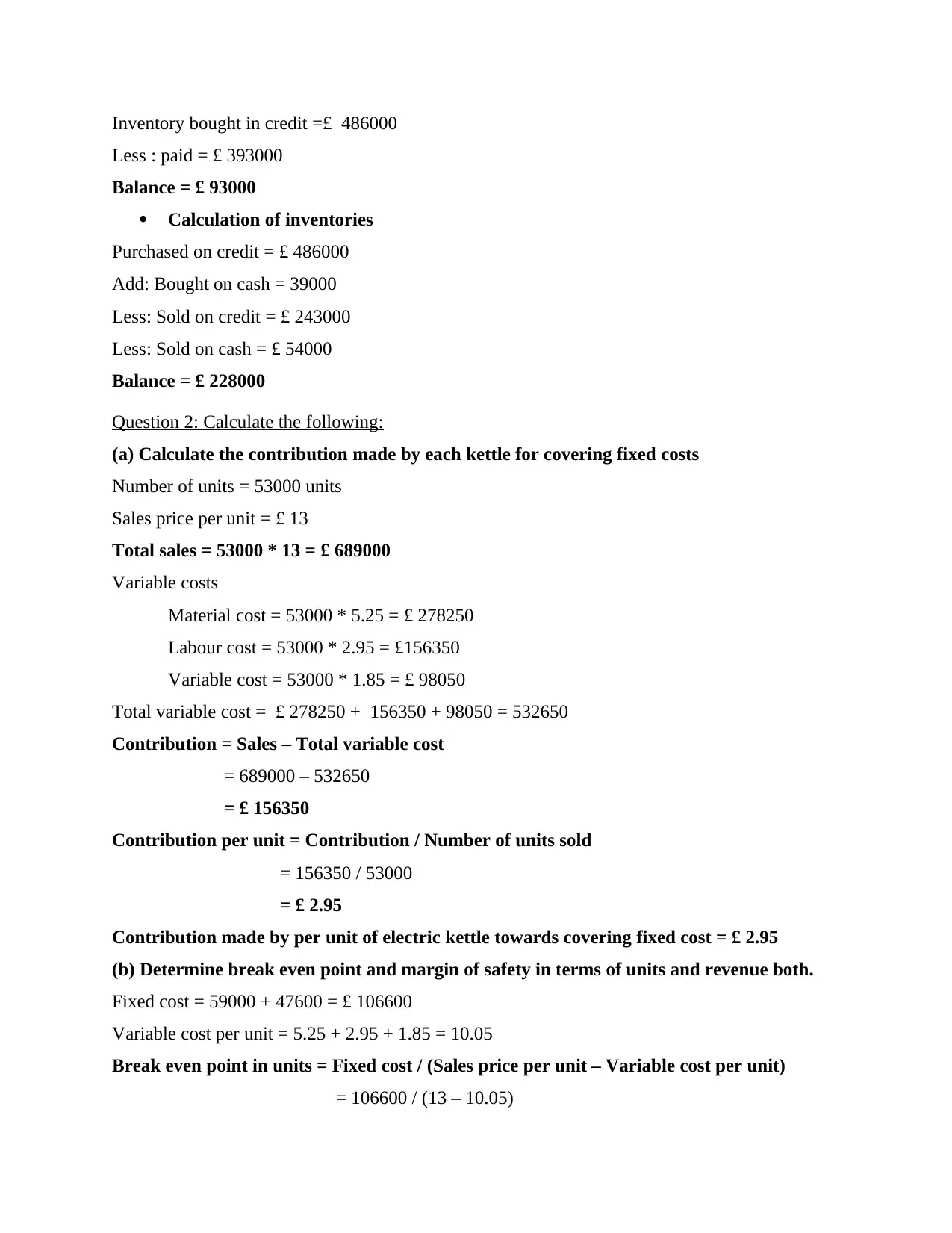

Inventory bought in credit =£ 486000

Less : paid = £ 393000

Balance = £ 93000

Calculation of inventories

Purchased on credit = £ 486000

Add: Bought on cash = 39000

Less: Sold on credit = £ 243000

Less: Sold on cash = £ 54000

Balance = £ 228000

Question 2: Calculate the following:

(a) Calculate the contribution made by each kettle for covering fixed costs

Number of units = 53000 units

Sales price per unit = £ 13

Total sales = 53000 * 13 = £ 689000

Variable costs

Material cost = 53000 * 5.25 = £ 278250

Labour cost = 53000 * 2.95 = £156350

Variable cost = 53000 * 1.85 = £ 98050

Total variable cost = £ 278250 + 156350 + 98050 = 532650

Contribution = Sales – Total variable cost

= 689000 – 532650

= £ 156350

Contribution per unit = Contribution / Number of units sold

= 156350 / 53000

= £ 2.95

Contribution made by per unit of electric kettle towards covering fixed cost = £ 2.95

(b) Determine break even point and margin of safety in terms of units and revenue both.

Fixed cost = 59000 + 47600 = £ 106600

Variable cost per unit = 5.25 + 2.95 + 1.85 = 10.05

Break even point in units = Fixed cost / (Sales price per unit – Variable cost per unit)

= 106600 / (13 – 10.05)

Less : paid = £ 393000

Balance = £ 93000

Calculation of inventories

Purchased on credit = £ 486000

Add: Bought on cash = 39000

Less: Sold on credit = £ 243000

Less: Sold on cash = £ 54000

Balance = £ 228000

Question 2: Calculate the following:

(a) Calculate the contribution made by each kettle for covering fixed costs

Number of units = 53000 units

Sales price per unit = £ 13

Total sales = 53000 * 13 = £ 689000

Variable costs

Material cost = 53000 * 5.25 = £ 278250

Labour cost = 53000 * 2.95 = £156350

Variable cost = 53000 * 1.85 = £ 98050

Total variable cost = £ 278250 + 156350 + 98050 = 532650

Contribution = Sales – Total variable cost

= 689000 – 532650

= £ 156350

Contribution per unit = Contribution / Number of units sold

= 156350 / 53000

= £ 2.95

Contribution made by per unit of electric kettle towards covering fixed cost = £ 2.95

(b) Determine break even point and margin of safety in terms of units and revenue both.

Fixed cost = 59000 + 47600 = £ 106600

Variable cost per unit = 5.25 + 2.95 + 1.85 = 10.05

Break even point in units = Fixed cost / (Sales price per unit – Variable cost per unit)

= 106600 / (13 – 10.05)

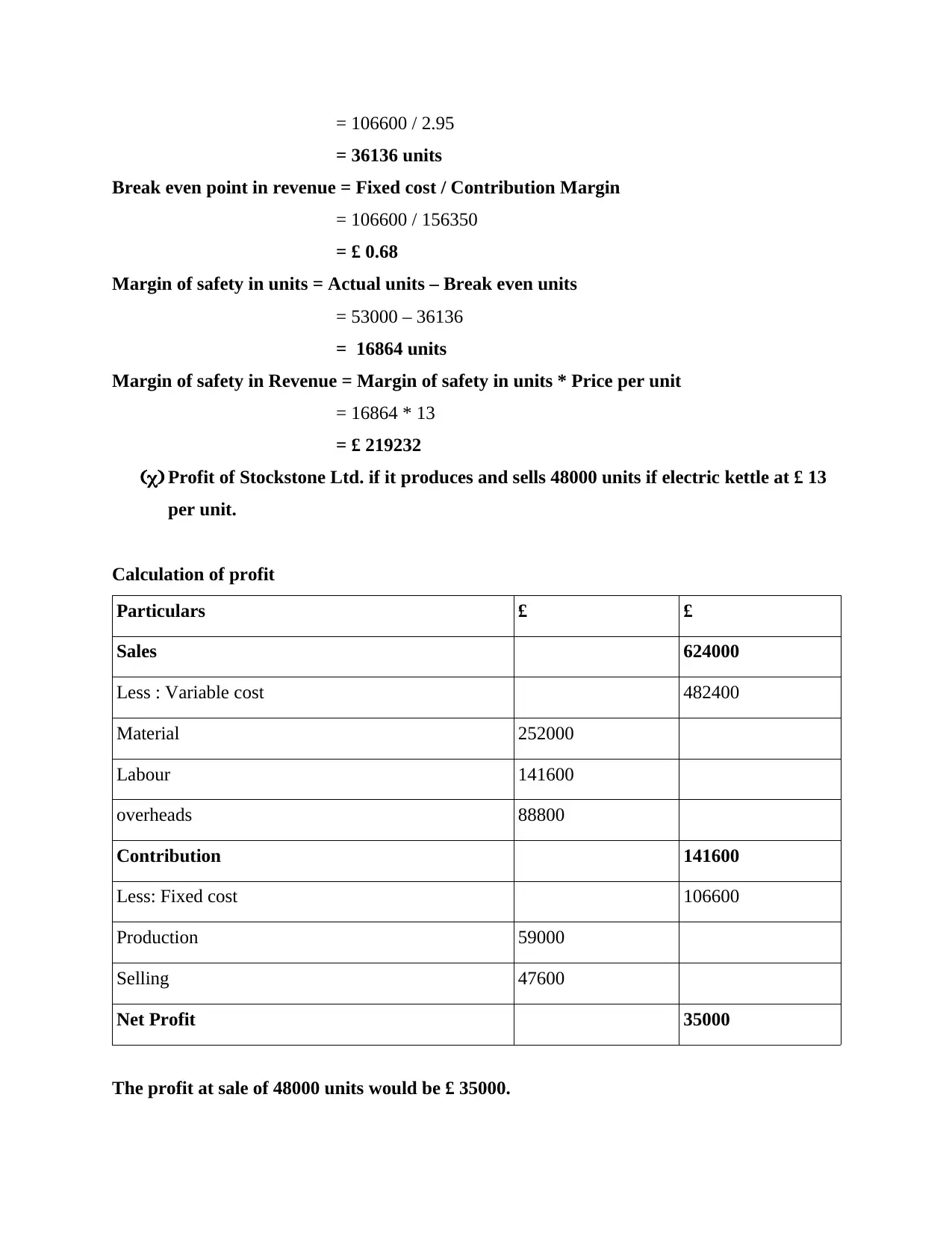

= 106600 / 2.95

= 36136 units

Break even point in revenue = Fixed cost / Contribution Margin

= 106600 / 156350

= £ 0.68

Margin of safety in units = Actual units – Break even units

= 53000 – 36136

= 16864 units

Margin of safety in Revenue = Margin of safety in units * Price per unit

= 16864 * 13

= £ 219232

(c) Profit of Stockstone Ltd. if it produces and sells 48000 units if electric kettle at £ 13

per unit.

Calculation of profit

Particulars £ £

Sales 624000

Less : Variable cost 482400

Material 252000

Labour 141600

overheads 88800

Contribution 141600

Less: Fixed cost 106600

Production 59000

Selling 47600

Net Profit 35000

The profit at sale of 48000 units would be £ 35000.

= 36136 units

Break even point in revenue = Fixed cost / Contribution Margin

= 106600 / 156350

= £ 0.68

Margin of safety in units = Actual units – Break even units

= 53000 – 36136

= 16864 units

Margin of safety in Revenue = Margin of safety in units * Price per unit

= 16864 * 13

= £ 219232

(c) Profit of Stockstone Ltd. if it produces and sells 48000 units if electric kettle at £ 13

per unit.

Calculation of profit

Particulars £ £

Sales 624000

Less : Variable cost 482400

Material 252000

Labour 141600

overheads 88800

Contribution 141600

Less: Fixed cost 106600

Production 59000

Selling 47600

Net Profit 35000

The profit at sale of 48000 units would be £ 35000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

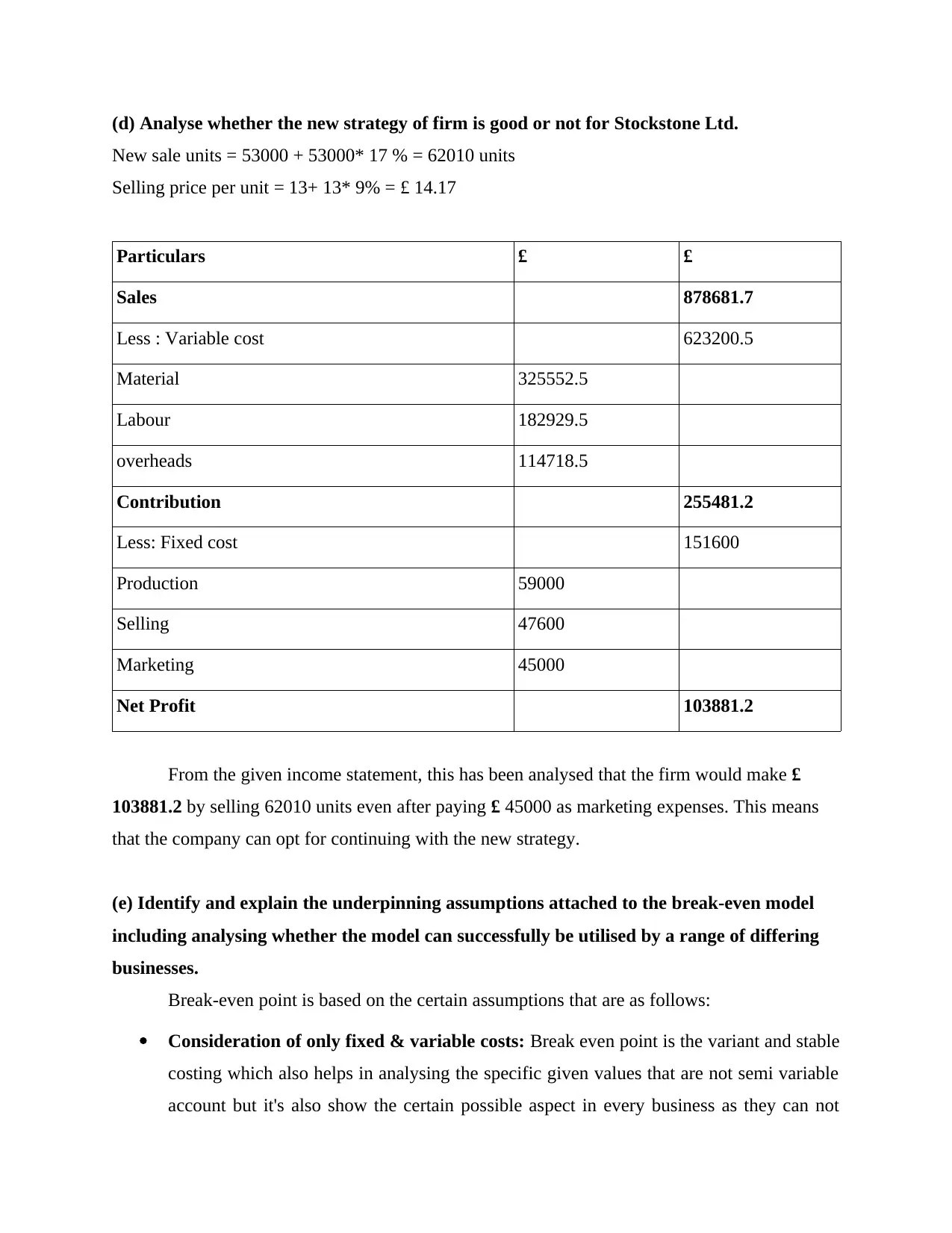

(d) Analyse whether the new strategy of firm is good or not for Stockstone Ltd.

New sale units = 53000 + 53000* 17 % = 62010 units

Selling price per unit = 13+ 13* 9% = £ 14.17

Particulars £ £

Sales 878681.7

Less : Variable cost 623200.5

Material 325552.5

Labour 182929.5

overheads 114718.5

Contribution 255481.2

Less: Fixed cost 151600

Production 59000

Selling 47600

Marketing 45000

Net Profit 103881.2

From the given income statement, this has been analysed that the firm would make £

103881.2 by selling 62010 units even after paying £ 45000 as marketing expenses. This means

that the company can opt for continuing with the new strategy.

(e) Identify and explain the underpinning assumptions attached to the break-even model

including analysing whether the model can successfully be utilised by a range of differing

businesses.

Break-even point is based on the certain assumptions that are as follows:

Consideration of only fixed & variable costs: Break even point is the variant and stable

costing which also helps in analysing the specific given values that are not semi variable

account but it's also show the certain possible aspect in every business as they can not

New sale units = 53000 + 53000* 17 % = 62010 units

Selling price per unit = 13+ 13* 9% = £ 14.17

Particulars £ £

Sales 878681.7

Less : Variable cost 623200.5

Material 325552.5

Labour 182929.5

overheads 114718.5

Contribution 255481.2

Less: Fixed cost 151600

Production 59000

Selling 47600

Marketing 45000

Net Profit 103881.2

From the given income statement, this has been analysed that the firm would make £

103881.2 by selling 62010 units even after paying £ 45000 as marketing expenses. This means

that the company can opt for continuing with the new strategy.

(e) Identify and explain the underpinning assumptions attached to the break-even model

including analysing whether the model can successfully be utilised by a range of differing

businesses.

Break-even point is based on the certain assumptions that are as follows:

Consideration of only fixed & variable costs: Break even point is the variant and stable

costing which also helps in analysing the specific given values that are not semi variable

account but it's also show the certain possible aspect in every business as they can not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

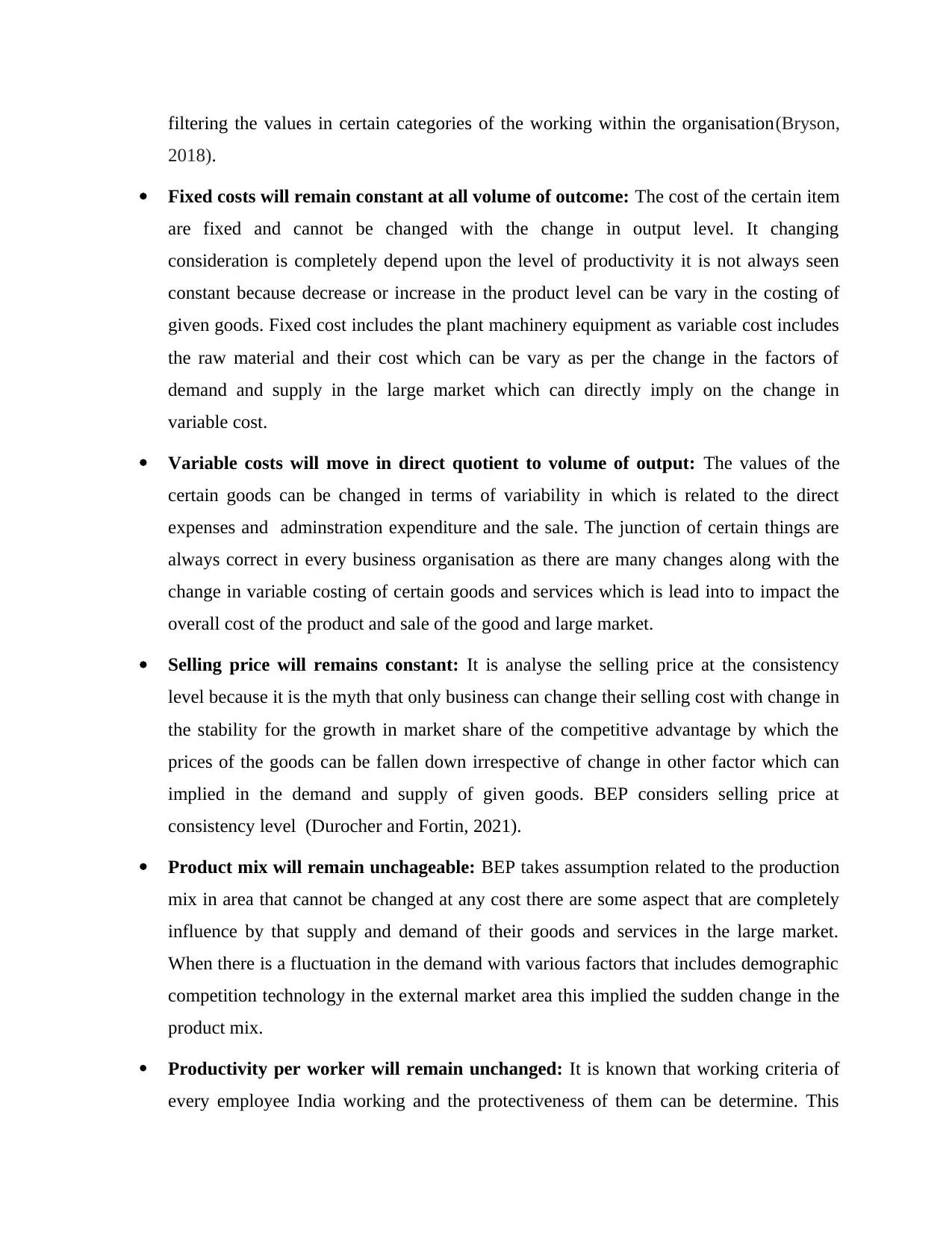

filtering the values in certain categories of the working within the organisation(Bryson,

2018).

Fixed costs will remain constant at all volume of outcome: The cost of the certain item

are fixed and cannot be changed with the change in output level. It changing

consideration is completely depend upon the level of productivity it is not always seen

constant because decrease or increase in the product level can be vary in the costing of

given goods. Fixed cost includes the plant machinery equipment as variable cost includes

the raw material and their cost which can be vary as per the change in the factors of

demand and supply in the large market which can directly imply on the change in

variable cost.

Variable costs will move in direct quotient to volume of output: The values of the

certain goods can be changed in terms of variability in which is related to the direct

expenses and adminstration expenditure and the sale. The junction of certain things are

always correct in every business organisation as there are many changes along with the

change in variable costing of certain goods and services which is lead into to impact the

overall cost of the product and sale of the good and large market.

Selling price will remains constant: It is analyse the selling price at the consistency

level because it is the myth that only business can change their selling cost with change in

the stability for the growth in market share of the competitive advantage by which the

prices of the goods can be fallen down irrespective of change in other factor which can

implied in the demand and supply of given goods. BEP considers selling price at

consistency level (Durocher and Fortin, 2021).

Product mix will remain unchageable: BEP takes assumption related to the production

mix in area that cannot be changed at any cost there are some aspect that are completely

influence by that supply and demand of their goods and services in the large market.

When there is a fluctuation in the demand with various factors that includes demographic

competition technology in the external market area this implied the sudden change in the

product mix.

Productivity per worker will remain unchanged: It is known that working criteria of

every employee India working and the protectiveness of them can be determine. This

2018).

Fixed costs will remain constant at all volume of outcome: The cost of the certain item

are fixed and cannot be changed with the change in output level. It changing

consideration is completely depend upon the level of productivity it is not always seen

constant because decrease or increase in the product level can be vary in the costing of

given goods. Fixed cost includes the plant machinery equipment as variable cost includes

the raw material and their cost which can be vary as per the change in the factors of

demand and supply in the large market which can directly imply on the change in

variable cost.

Variable costs will move in direct quotient to volume of output: The values of the

certain goods can be changed in terms of variability in which is related to the direct

expenses and adminstration expenditure and the sale. The junction of certain things are

always correct in every business organisation as there are many changes along with the

change in variable costing of certain goods and services which is lead into to impact the

overall cost of the product and sale of the good and large market.

Selling price will remains constant: It is analyse the selling price at the consistency

level because it is the myth that only business can change their selling cost with change in

the stability for the growth in market share of the competitive advantage by which the

prices of the goods can be fallen down irrespective of change in other factor which can

implied in the demand and supply of given goods. BEP considers selling price at

consistency level (Durocher and Fortin, 2021).

Product mix will remain unchageable: BEP takes assumption related to the production

mix in area that cannot be changed at any cost there are some aspect that are completely

influence by that supply and demand of their goods and services in the large market.

When there is a fluctuation in the demand with various factors that includes demographic

competition technology in the external market area this implied the sudden change in the

product mix.

Productivity per worker will remain unchanged: It is known that working criteria of

every employee India working and the protectiveness of them can be determine. This

cannot happen in every organisation which consists of certain factor that might only

believe that it can determine the productivity of every individual.

Question 3: Provide solution for the investment appraisal technique

(a) Initial Investment = £ 40000000

Annual cash inflow = £ 17000000

Annual cash outflow = £ 6400000

Payback period = Initial Investment / Net annual cash flow

= 40000000 / 10600000 = 3.774 years

Accounting Rate of Return = (Annual cashflow – Annual Depreciation)/ Initial Investment * 100

= (10600000 – 7000000) / 40000000 * 100 = 9%

Net present Value = present value of annual cash inflow – present value of annual cash outflow

= (1.43 * 17000000) – (1.43 * 6400000)

= 24310000 – 9152000 = £ 15158000

The organisation can except certain offer as it is related to the present value of business which

has more than their investment in the equipments and machine so ARR of the given assignment

is very high which is profitable to the purchase of this project.

(b) Produce a report that explains and analyses the key merits and limitations of the

differing

investment appraisal techniques.

Pay back period- This is the aspects to assess cetain investment by the time's it is the

basic technique which leads to assess the investment and their time period it would take to repaid

within a given set format. It was so analysis at how much time it will take to get the return on

investment within a set period of time.

Merits- This method is less time consuming and leads to have quick decision making.

At the time of analysing payback period it considered the value of money.

It is the easy process which can easily calculate and understand by the companies.

believe that it can determine the productivity of every individual.

Question 3: Provide solution for the investment appraisal technique

(a) Initial Investment = £ 40000000

Annual cash inflow = £ 17000000

Annual cash outflow = £ 6400000

Payback period = Initial Investment / Net annual cash flow

= 40000000 / 10600000 = 3.774 years

Accounting Rate of Return = (Annual cashflow – Annual Depreciation)/ Initial Investment * 100

= (10600000 – 7000000) / 40000000 * 100 = 9%

Net present Value = present value of annual cash inflow – present value of annual cash outflow

= (1.43 * 17000000) – (1.43 * 6400000)

= 24310000 – 9152000 = £ 15158000

The organisation can except certain offer as it is related to the present value of business which

has more than their investment in the equipments and machine so ARR of the given assignment

is very high which is profitable to the purchase of this project.

(b) Produce a report that explains and analyses the key merits and limitations of the

differing

investment appraisal techniques.

Pay back period- This is the aspects to assess cetain investment by the time's it is the

basic technique which leads to assess the investment and their time period it would take to repaid

within a given set format. It was so analysis at how much time it will take to get the return on

investment within a set period of time.

Merits- This method is less time consuming and leads to have quick decision making.

At the time of analysing payback period it considered the value of money.

It is the easy process which can easily calculate and understand by the companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage-

It is basically not considered have value of money.

It is not equal and can be biased in the long-term project.

In this status difficult to determine whether the investment will increase the overall value

of form or not.

As per the payback period time it not emphasize on the cash flow.

Accounting rate of return- It is the certain aspect which is used to measure the overall expected

profit from the expenses and its investment arises from the certain percentage of capital invested.

(Lonie, Nixon and Collison, 2018).

Merits- it is based on the accounting profit. Also analyse savings over entire period of their

investment. It also helps in analysing the benefits in the percentage that can be easily compared

with the other assignment.

Limitations

There is no need of other calculations.

It does not analyse the risk associated with the each project.

It is usually overcoming ignore the certain time of money.

It uses accounting profit in order to participate in the certain project.

Net present value- It access the company to make their decisions and allowed them to consider

the given time value of money e and its calculation required all the cash flow related to the

investment will be considered in net. It is related to the certain aspect which helps in knowing the

completion time of uncertain project within a given time.

Merits

It leads to uninstall the the overall wealth of the shareholders within the given money.

As the overall value of the company can be increased by their invested amount(Murata

and Pan, 2018).

It analyse the cash flow and the certain value of money.

Limitations

It is very critical to calculate and analyse

It is basically not considered have value of money.

It is not equal and can be biased in the long-term project.

In this status difficult to determine whether the investment will increase the overall value

of form or not.

As per the payback period time it not emphasize on the cash flow.

Accounting rate of return- It is the certain aspect which is used to measure the overall expected

profit from the expenses and its investment arises from the certain percentage of capital invested.

(Lonie, Nixon and Collison, 2018).

Merits- it is based on the accounting profit. Also analyse savings over entire period of their

investment. It also helps in analysing the benefits in the percentage that can be easily compared

with the other assignment.

Limitations

There is no need of other calculations.

It does not analyse the risk associated with the each project.

It is usually overcoming ignore the certain time of money.

It uses accounting profit in order to participate in the certain project.

Net present value- It access the company to make their decisions and allowed them to consider

the given time value of money e and its calculation required all the cash flow related to the

investment will be considered in net. It is related to the certain aspect which helps in knowing the

completion time of uncertain project within a given time.

Merits

It leads to uninstall the the overall wealth of the shareholders within the given money.

As the overall value of the company can be increased by their invested amount(Murata

and Pan, 2018).

It analyse the cash flow and the certain value of money.

Limitations

It is very critical to calculate and analyse

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The overall results of net present value is based on the discount rate used in expected

interest rate can be accurate.

Internal rate of return- It is related to the interest rate which is having the same value as

expected in the receipt of certain cost of investment within the certain outlet.

Merits

It also analyse the time value of money within the time of calculating IRR.

That is the easy and simplest method to analyse the certain aspect by the business

management.

By this and individual can easily communicate the certain value of project to someone.

Debt is considered the risk which is associated in the cash flow and also analyse the value

of money.

Limitations

There are various positive and negative mixture in the cash flow.

For taking decisions at required the cost of capital.

It leads to sound decisions in comparison to exclusive investment within the project.

Profit ability index- The respective index which refers to the amount which is being and dollar

by their investment. It is generally analysed divide in the present value of expected cash flow in

future by the initial investment in the given assignment.

Merits

It is helpful to communicate and capital rationing in an project.

It can easily analyse the expected return on investment of the given project which is

closely related to the net present value taking certain decision.

Limitations

It candidates to have a wrong decision in comparison to the exclusive investment buy

mutual understanding.

When the different project using certain life then it will be difficult to analyse the overall

profitability index of the project.

interest rate can be accurate.

Internal rate of return- It is related to the interest rate which is having the same value as

expected in the receipt of certain cost of investment within the certain outlet.

Merits

It also analyse the time value of money within the time of calculating IRR.

That is the easy and simplest method to analyse the certain aspect by the business

management.

By this and individual can easily communicate the certain value of project to someone.

Debt is considered the risk which is associated in the cash flow and also analyse the value

of money.

Limitations

There are various positive and negative mixture in the cash flow.

For taking decisions at required the cost of capital.

It leads to sound decisions in comparison to exclusive investment within the project.

Profit ability index- The respective index which refers to the amount which is being and dollar

by their investment. It is generally analysed divide in the present value of expected cash flow in

future by the initial investment in the given assignment.

Merits

It is helpful to communicate and capital rationing in an project.

It can easily analyse the expected return on investment of the given project which is

closely related to the net present value taking certain decision.

Limitations

It candidates to have a wrong decision in comparison to the exclusive investment buy

mutual understanding.

When the different project using certain life then it will be difficult to analyse the overall

profitability index of the project.

(c) Produce a report that identifies and explains the key benefits and limitations of using

budgets as a tool for strategic planning.

A budget is defined as a financial document that can be used by the certain management

in order to meet their income and expenses. It is the general plan format in the future expenses

and analysed where a business can minimise their spending.(Soka, 2020). It shows the financial

resources different use and at the end of the financial year business management can compare

their desire result with the actual spending and analyse the business position in the target market

and gradually work for their further improvement.

It is the significant tool for the business management which helps in grabbing the various source

of income and play a significant role for making the best use of their resources in order to

achieve their set objectives and goals of the company.

The key benefits that can be get by using Budgets are:

Turns strategic plan into action- It is basically analyse the task activities and resources

that are being necessary to to make the strategic plan for upcoming year.

Resource allocation- It also enhance the overall use and fulfill the request that are being

justified and needed for conducting the various business activities for getting better

result.

Plan for spending- This is worked as a certain plan which creates effective emphasize on

controlling expenditure and income of a particular business.

Cost consciousness- It can create attitude of conciseness related to the cost in the

management and keep their resources with best use that how much day can be used to get

a better result.

Problem solving- It give the control and organisation approaches in order to solve the

certain problem that are being accumulated within the organisation.

The limitations of using budgets are:

Judgement based- All the budget are being finalized and made on the decision taken by

the management by effective planning budgeting and forecasting which is not the exact

theory related to the science and this cannot be fixed as the future is not predictable.

Cooperation- the overall succession plan of the budget is mainly depends upon the

cooperation and coordination by all the team members within the organisation. When the

budgets as a tool for strategic planning.

A budget is defined as a financial document that can be used by the certain management

in order to meet their income and expenses. It is the general plan format in the future expenses

and analysed where a business can minimise their spending.(Soka, 2020). It shows the financial

resources different use and at the end of the financial year business management can compare

their desire result with the actual spending and analyse the business position in the target market

and gradually work for their further improvement.

It is the significant tool for the business management which helps in grabbing the various source

of income and play a significant role for making the best use of their resources in order to

achieve their set objectives and goals of the company.

The key benefits that can be get by using Budgets are:

Turns strategic plan into action- It is basically analyse the task activities and resources

that are being necessary to to make the strategic plan for upcoming year.

Resource allocation- It also enhance the overall use and fulfill the request that are being

justified and needed for conducting the various business activities for getting better

result.

Plan for spending- This is worked as a certain plan which creates effective emphasize on

controlling expenditure and income of a particular business.

Cost consciousness- It can create attitude of conciseness related to the cost in the

management and keep their resources with best use that how much day can be used to get

a better result.

Problem solving- It give the control and organisation approaches in order to solve the

certain problem that are being accumulated within the organisation.

The limitations of using budgets are:

Judgement based- All the budget are being finalized and made on the decision taken by

the management by effective planning budgeting and forecasting which is not the exact

theory related to the science and this cannot be fixed as the future is not predictable.

Cooperation- the overall succession plan of the budget is mainly depends upon the

cooperation and coordination by all the team members within the organisation. When the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budgeting has failed due to all the decision has been taken by the top management only

which server is execution.(Tannen, 2020).

Tool- It is the certain aspect which not take the consideration in the management as it

helps to make plan and execute in an effective manner within the organisation.

Budget allowance- At the last of the budgeting period when the actual expenses is not

meeting with the invested amount so the employee must be temporary 2 to give more

time so that they can have a better result within the organisation.

Reduces initiative- A rigid budget may reduces initiative and innovation, making it impossible

to obtain money for new ideas. It can also reduce creativity among lower levels of management.

CONCLUSION

From the above report it is concluded that there are certain financial tools which helps in

enhancing the overall business performance. Financial reports also help in building the

knowledge about the overall performance along with its profitability of the company. It is helpful

for assessing the internal and external environment you can use the report for taking their

effective planning and investment related aspect. There are different types of techniques which

helps in analysing the specific project should be acceptable or not so they make the effective use

of time value of money for analysing the correct information and on the basis of such tools

company can prepare the budget. But budget are not helpful for all the the aspect as there are

some function which needs to have differentiation and its application so business must evaluate

their overall performance whether they will be able to cover their invested amount or not. As a

whole these all techniques are helpful for analysing the effectiveness of such tools within the

organisation.

which server is execution.(Tannen, 2020).

Tool- It is the certain aspect which not take the consideration in the management as it

helps to make plan and execute in an effective manner within the organisation.

Budget allowance- At the last of the budgeting period when the actual expenses is not

meeting with the invested amount so the employee must be temporary 2 to give more

time so that they can have a better result within the organisation.

Reduces initiative- A rigid budget may reduces initiative and innovation, making it impossible

to obtain money for new ideas. It can also reduce creativity among lower levels of management.

CONCLUSION

From the above report it is concluded that there are certain financial tools which helps in

enhancing the overall business performance. Financial reports also help in building the

knowledge about the overall performance along with its profitability of the company. It is helpful

for assessing the internal and external environment you can use the report for taking their

effective planning and investment related aspect. There are different types of techniques which

helps in analysing the specific project should be acceptable or not so they make the effective use

of time value of money for analysing the correct information and on the basis of such tools

company can prepare the budget. But budget are not helpful for all the the aspect as there are

some function which needs to have differentiation and its application so business must evaluate

their overall performance whether they will be able to cover their invested amount or not. As a

whole these all techniques are helpful for analysing the effectiveness of such tools within the

organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abernathy, J.L. And et.al., 2019. Financial statement footnote readability and corporate audit

outcomes. Auditing: A Journal of Practice & Theory. 38(2). pp.1-26.

Durocher, S. and Fortin, A., 2021. Financial statement users’ institutional logic. Journal of

Accounting and Public Policy. 40(2). p.106819.

Bryson, J.M., 2018. Strategic planning for public and nonprofit organizations: A guide to

strengthening and sustaining organizational achievement. John Wiley & Sons

Harris, E., Hoang, T. and Ngan, G., 2017. Accounting for capital investment appraisal: time for a

radical change?. In The Routledge Companion to Accounting Information Systems (pp.

173-189). Routledge.

Tannen, M.B., 2020. Introducing Learning by Doing into Ite Break-Even Analysis

Model. Journal of Accounting and Finance. 20(3). pp.11-19.

Lonie, A., Nixon, B. and Collison, D., 2018. Internal and external financial constraints on

investment in innovative technology. In New Technologies and the Firm (pp. 265-291).

Routledge.

Krishna, K.M., Pandey, N.K. and Thimmalapura, S., 2017, December. Break-even analysis and

economic viability of powertrain electrification—An analytical approach. In 2017 IEEE

Transportation Electrification Conference (ITEC-India) (pp. 1-6). IEEE.

Murata, C. and Pan, D., 2018. Budgets on my mind: Changing Budget Allocations to Meet

Teaching and Research Needs.

Soka, I.M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Seifzadeh, M. And et.al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

Vagner, I., 2020. Importance of break even point analysis. In Актуальные вопросы

бухгалтерского учета, анализа и аудита в инновационной экономике (pp. 87-91).

Books and Journals

Abernathy, J.L. And et.al., 2019. Financial statement footnote readability and corporate audit

outcomes. Auditing: A Journal of Practice & Theory. 38(2). pp.1-26.

Durocher, S. and Fortin, A., 2021. Financial statement users’ institutional logic. Journal of

Accounting and Public Policy. 40(2). p.106819.

Bryson, J.M., 2018. Strategic planning for public and nonprofit organizations: A guide to

strengthening and sustaining organizational achievement. John Wiley & Sons

Harris, E., Hoang, T. and Ngan, G., 2017. Accounting for capital investment appraisal: time for a

radical change?. In The Routledge Companion to Accounting Information Systems (pp.

173-189). Routledge.

Tannen, M.B., 2020. Introducing Learning by Doing into Ite Break-Even Analysis

Model. Journal of Accounting and Finance. 20(3). pp.11-19.

Lonie, A., Nixon, B. and Collison, D., 2018. Internal and external financial constraints on

investment in innovative technology. In New Technologies and the Firm (pp. 265-291).

Routledge.

Krishna, K.M., Pandey, N.K. and Thimmalapura, S., 2017, December. Break-even analysis and

economic viability of powertrain electrification—An analytical approach. In 2017 IEEE

Transportation Electrification Conference (ITEC-India) (pp. 1-6). IEEE.

Murata, C. and Pan, D., 2018. Budgets on my mind: Changing Budget Allocations to Meet

Teaching and Research Needs.

Soka, I.M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Seifzadeh, M. And et.al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

Vagner, I., 2020. Importance of break even point analysis. In Актуальные вопросы

бухгалтерского учета, анализа и аудита в инновационной экономике (pp. 87-91).

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.