Accounting and Finance Report: Racca Ltd and Rockham Plc Analysis

VerifiedAdded on 2023/06/07

|14

|3538

|109

Report

AI Summary

This report, prepared for an Introduction to Accounting and Finance course, encompasses three main parts. Part 1 focuses on the preparation of financial statements, including the income statement and statement of financial position for Racca Limited. Part 2 delves into marginal costing, calculating contribution, break-even points, and margin of safety, with a case study on Stockstone Ltd, evaluating a new marketing strategy. Part 3 explores capital investment techniques, including net present value, payback period, and accounting rate of return, with a case study on Rockham Plc, offering investment recommendations and discussing the advantages and disadvantages of budgets. The report provides detailed calculations, analysis, and recommendations based on the application of these accounting and finance principles.

Introduction to

Accounting and Finance

Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Part 1 ...............................................................................................................................................1

Income statement.........................................................................................................................2

Statement of financial position ...................................................................................................2

PART 2............................................................................................................................................3

a) calculation of contribution ......................................................................................................3

b) Calculation of break even point (BEP) and margin of safety (MOS) in terms of revenue and

units :............................................................................................................................................3

c ) Computation of profit for Stockstone Ltd when they produce 48000 electric kettle ............4

Evaluation of new strategy whether to adopt this or not for Stockstone Ltd...............................4

E ) Assumptions of break even model and analysis of the model used successfully in different

types of business :........................................................................................................................5

PART 3............................................................................................................................................6

Part C – Rockham Plc. ....................................................................................................................6

a. The calculations of various appraisal techniques.....................................................................6

b. Investment appraisal techniques ............................................................................................8

c. The advantages and disadvantages of budgets.........................................................................9

CONCLUSIONS............................................................................................................................10

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Part 1 ...............................................................................................................................................1

Income statement.........................................................................................................................2

Statement of financial position ...................................................................................................2

PART 2............................................................................................................................................3

a) calculation of contribution ......................................................................................................3

b) Calculation of break even point (BEP) and margin of safety (MOS) in terms of revenue and

units :............................................................................................................................................3

c ) Computation of profit for Stockstone Ltd when they produce 48000 electric kettle ............4

Evaluation of new strategy whether to adopt this or not for Stockstone Ltd...............................4

E ) Assumptions of break even model and analysis of the model used successfully in different

types of business :........................................................................................................................5

PART 3............................................................................................................................................6

Part C – Rockham Plc. ....................................................................................................................6

a. The calculations of various appraisal techniques.....................................................................6

b. Investment appraisal techniques ............................................................................................8

c. The advantages and disadvantages of budgets.........................................................................9

CONCLUSIONS............................................................................................................................10

REFERENCES..............................................................................................................................10

INTRODUCTION

Accounting is a method of maintaining records, classifying and summarizing transactions and

interpreting results to the interested parties and making reports. On the other hand, finance is

defined as monetary transactions which are occurred during the year. Financial accounting refers

to the particular branch of accounting system which helps in preparing financial statement which

includes income statement, balance sheet and cash flow statement (Adler and Dixon, 2021). This

report segregate into three parts in which first part consists of preparing income statement and

balance sheet. Second part involves around marginal costing in which calculation of

contribution, break even point and margin of safety. In the end, report includes calculation of

capital investment techniques and recommendations and some benefits and demerits of

investment techniques. There is key merits and limitations of budget also discussed in this

written report.

Part 1

Financial statements are the type of written records which means that activities of business and

performance of financial of an organisation. For every organisation, financial statements

comprises of statement of position, income statement and cash flow statement. The main benefits

of financial statements are to ascertaining whether a enterprise has the ability to pay its debts and

to find out the company's financial ratios through the use of financial statements. But have some

demerits also which is it can be easily manipulated which leads to false information to the

outsiders. Financial statements are based on the historical nature which might get lead to future

results of a company.

One of the economic statements is the stability sheet. It indicates an entity's belongings,

liabilities, and stockholders' fairness as of the record date. In this record, the whole of all

belongings should healthy the blended overall of all liabilities and fairness. The asset facts at the

stability sheet is subdivided into modern-day and long-time period belongings. Similarly, the

legal responsibility facts is subdivided into modern-day and long-time period liabilities

(Bradbury and Scott, 2021). This stratification is beneficial for figuring out the liquidity of a

Accounting is a method of maintaining records, classifying and summarizing transactions and

interpreting results to the interested parties and making reports. On the other hand, finance is

defined as monetary transactions which are occurred during the year. Financial accounting refers

to the particular branch of accounting system which helps in preparing financial statement which

includes income statement, balance sheet and cash flow statement (Adler and Dixon, 2021). This

report segregate into three parts in which first part consists of preparing income statement and

balance sheet. Second part involves around marginal costing in which calculation of

contribution, break even point and margin of safety. In the end, report includes calculation of

capital investment techniques and recommendations and some benefits and demerits of

investment techniques. There is key merits and limitations of budget also discussed in this

written report.

Part 1

Financial statements are the type of written records which means that activities of business and

performance of financial of an organisation. For every organisation, financial statements

comprises of statement of position, income statement and cash flow statement. The main benefits

of financial statements are to ascertaining whether a enterprise has the ability to pay its debts and

to find out the company's financial ratios through the use of financial statements. But have some

demerits also which is it can be easily manipulated which leads to false information to the

outsiders. Financial statements are based on the historical nature which might get lead to future

results of a company.

One of the economic statements is the stability sheet. It indicates an entity's belongings,

liabilities, and stockholders' fairness as of the record date. In this record, the whole of all

belongings should healthy the blended overall of all liabilities and fairness. The asset facts at the

stability sheet is subdivided into modern-day and long-time period belongings. Similarly, the

legal responsibility facts is subdivided into modern-day and long-time period liabilities

(Bradbury and Scott, 2021). This stratification is beneficial for figuring out the liquidity of a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

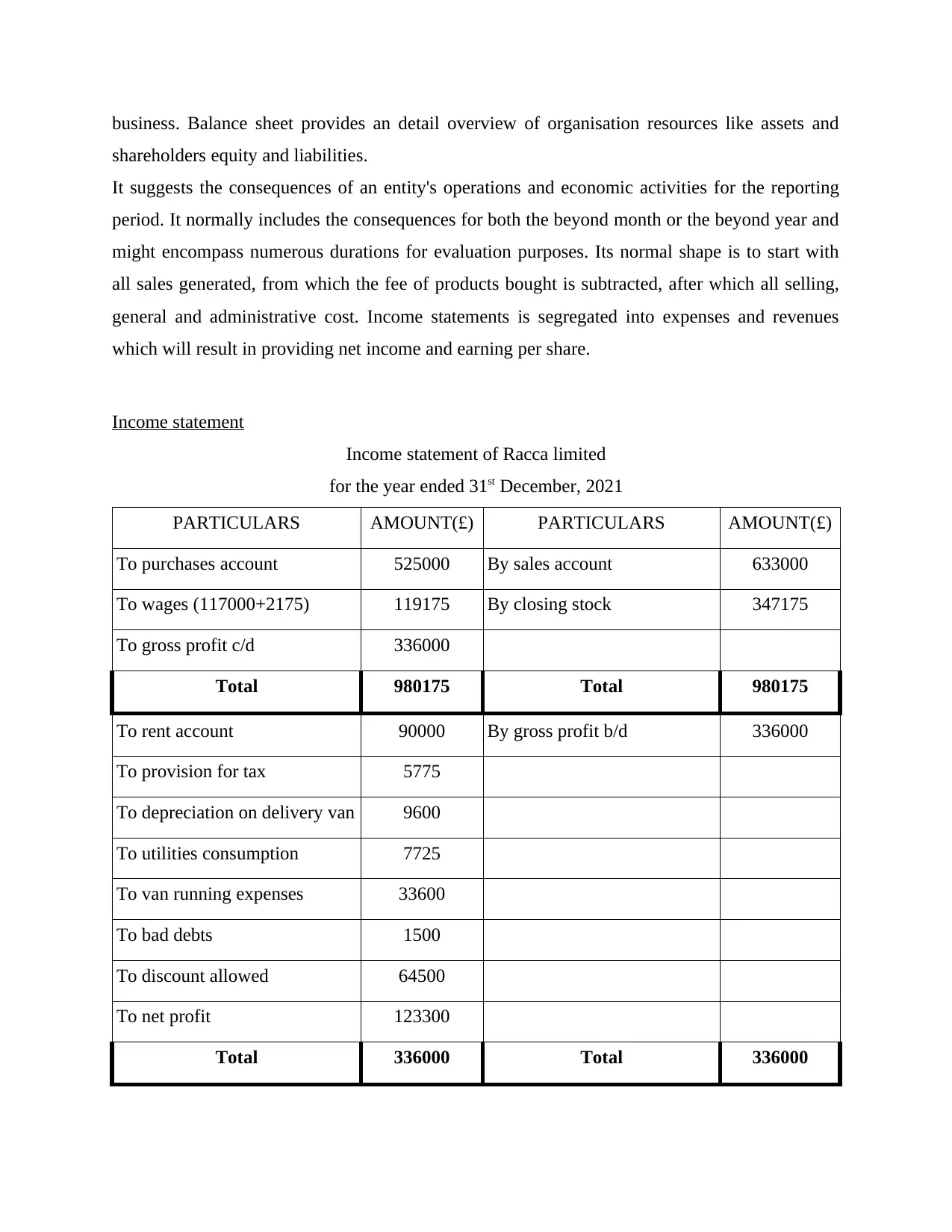

business. Balance sheet provides an detail overview of organisation resources like assets and

shareholders equity and liabilities.

It suggests the consequences of an entity's operations and economic activities for the reporting

period. It normally includes the consequences for both the beyond month or the beyond year and

might encompass numerous durations for evaluation purposes. Its normal shape is to start with

all sales generated, from which the fee of products bought is subtracted, after which all selling,

general and administrative cost. Income statements is segregated into expenses and revenues

which will result in providing net income and earning per share.

Income statement

Income statement of Racca limited

for the year ended 31st December, 2021

PARTICULARS AMOUNT(£) PARTICULARS AMOUNT(£)

To purchases account 525000 By sales account 633000

To wages (117000+2175) 119175 By closing stock 347175

To gross profit c/d 336000

Total 980175 Total 980175

To rent account 90000 By gross profit b/d 336000

To provision for tax 5775

To depreciation on delivery van 9600

To utilities consumption 7725

To van running expenses 33600

To bad debts 1500

To discount allowed 64500

To net profit 123300

Total 336000 Total 336000

shareholders equity and liabilities.

It suggests the consequences of an entity's operations and economic activities for the reporting

period. It normally includes the consequences for both the beyond month or the beyond year and

might encompass numerous durations for evaluation purposes. Its normal shape is to start with

all sales generated, from which the fee of products bought is subtracted, after which all selling,

general and administrative cost. Income statements is segregated into expenses and revenues

which will result in providing net income and earning per share.

Income statement

Income statement of Racca limited

for the year ended 31st December, 2021

PARTICULARS AMOUNT(£) PARTICULARS AMOUNT(£)

To purchases account 525000 By sales account 633000

To wages (117000+2175) 119175 By closing stock 347175

To gross profit c/d 336000

Total 980175 Total 980175

To rent account 90000 By gross profit b/d 336000

To provision for tax 5775

To depreciation on delivery van 9600

To utilities consumption 7725

To van running expenses 33600

To bad debts 1500

To discount allowed 64500

To net profit 123300

Total 336000 Total 336000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

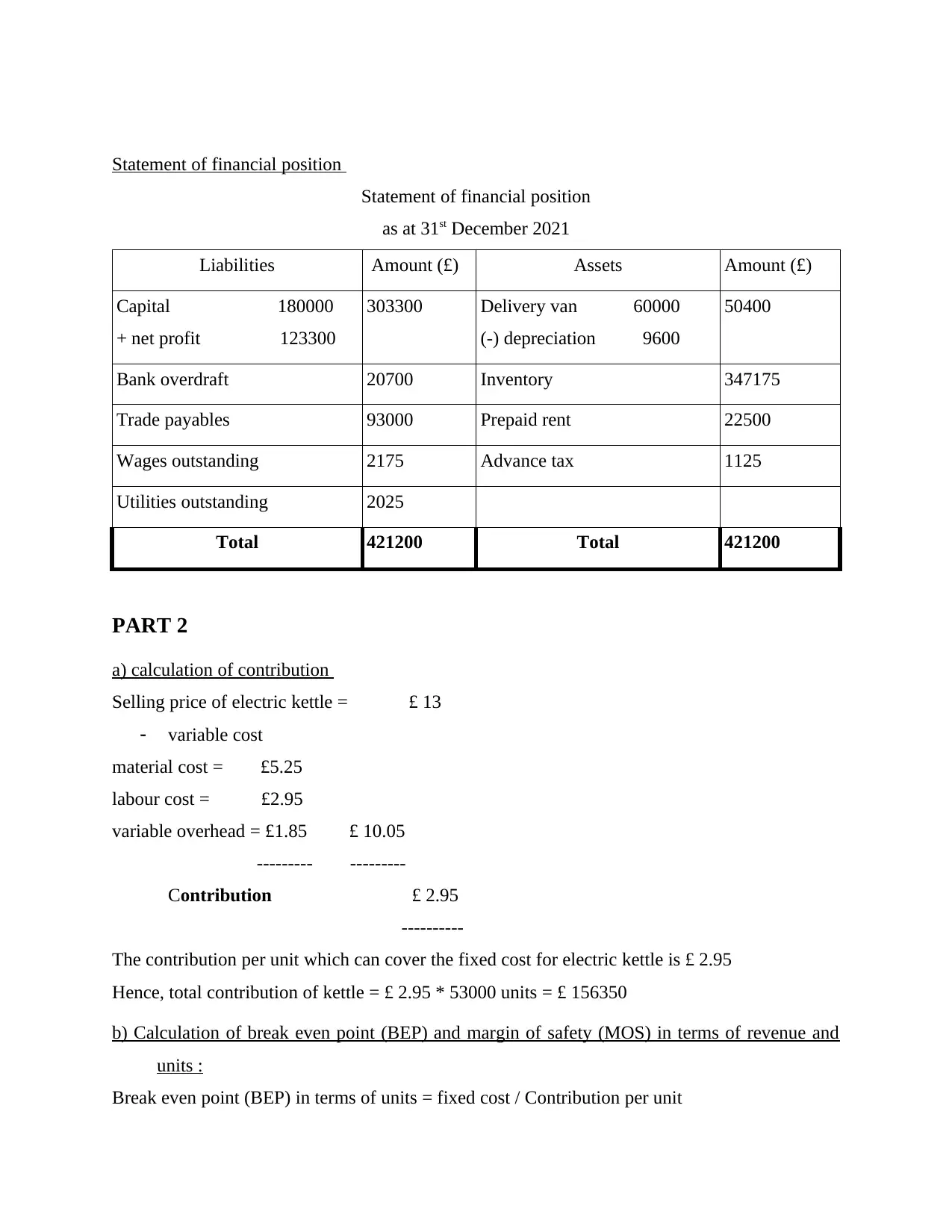

Statement of financial position

Statement of financial position

as at 31st December 2021

Liabilities Amount (£) Assets Amount (£)

Capital 180000

+ net profit 123300

303300 Delivery van 60000

(-) depreciation 9600

50400

Bank overdraft 20700 Inventory 347175

Trade payables 93000 Prepaid rent 22500

Wages outstanding 2175 Advance tax 1125

Utilities outstanding 2025

Total 421200 Total 421200

PART 2

a) calculation of contribution

Selling price of electric kettle = £ 13

variable cost

material cost = £5.25

labour cost = £2.95

variable overhead = £1.85 £ 10.05

--------- ---------

Contribution £ 2.95

----------

The contribution per unit which can cover the fixed cost for electric kettle is £ 2.95

Hence, total contribution of kettle = £ 2.95 * 53000 units = £ 156350

b) Calculation of break even point (BEP) and margin of safety (MOS) in terms of revenue and

units :

Break even point (BEP) in terms of units = fixed cost / Contribution per unit

Statement of financial position

as at 31st December 2021

Liabilities Amount (£) Assets Amount (£)

Capital 180000

+ net profit 123300

303300 Delivery van 60000

(-) depreciation 9600

50400

Bank overdraft 20700 Inventory 347175

Trade payables 93000 Prepaid rent 22500

Wages outstanding 2175 Advance tax 1125

Utilities outstanding 2025

Total 421200 Total 421200

PART 2

a) calculation of contribution

Selling price of electric kettle = £ 13

variable cost

material cost = £5.25

labour cost = £2.95

variable overhead = £1.85 £ 10.05

--------- ---------

Contribution £ 2.95

----------

The contribution per unit which can cover the fixed cost for electric kettle is £ 2.95

Hence, total contribution of kettle = £ 2.95 * 53000 units = £ 156350

b) Calculation of break even point (BEP) and margin of safety (MOS) in terms of revenue and

units :

Break even point (BEP) in terms of units = fixed cost / Contribution per unit

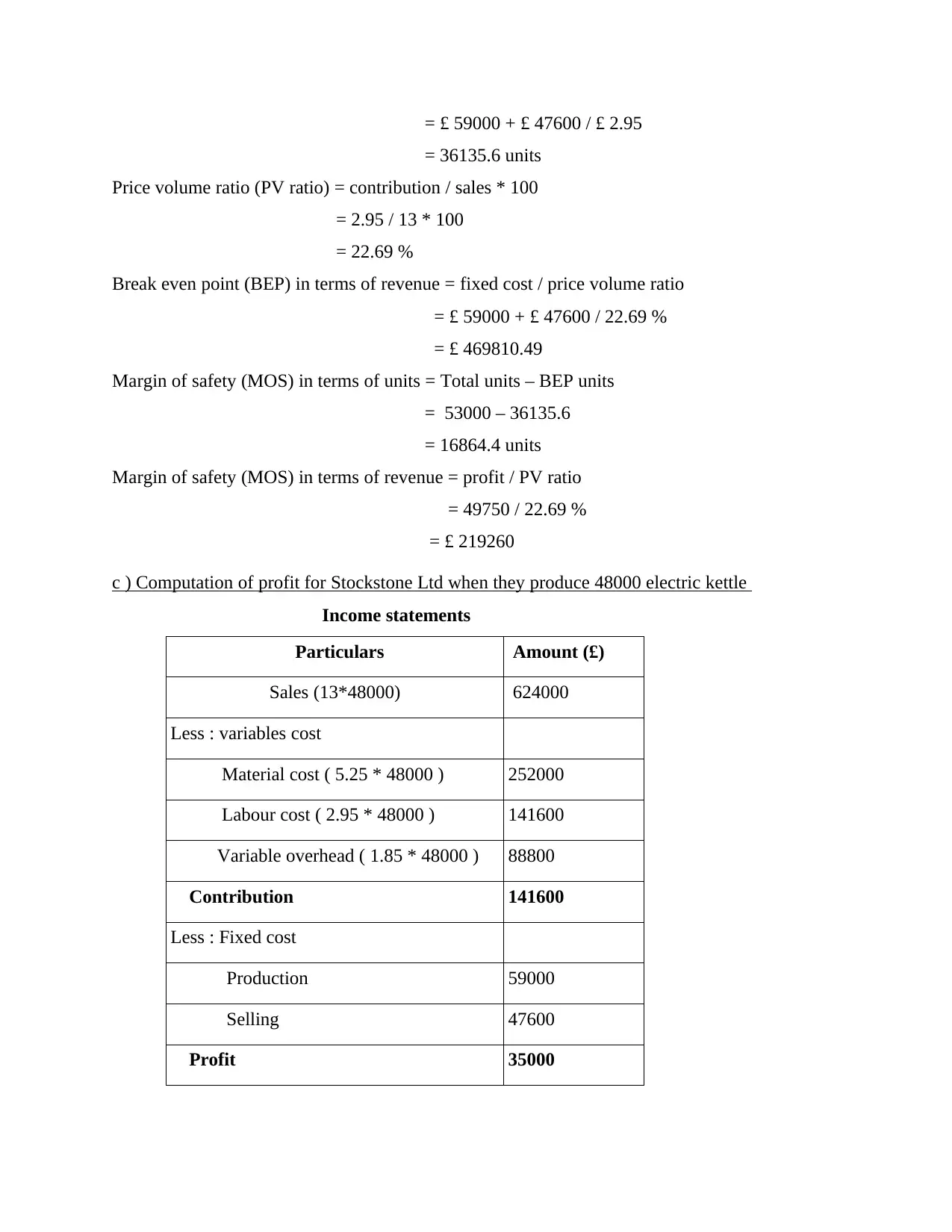

= £ 59000 + £ 47600 / £ 2.95

= 36135.6 units

Price volume ratio (PV ratio) = contribution / sales * 100

= 2.95 / 13 * 100

= 22.69 %

Break even point (BEP) in terms of revenue = fixed cost / price volume ratio

= £ 59000 + £ 47600 / 22.69 %

= £ 469810.49

Margin of safety (MOS) in terms of units = Total units – BEP units

= 53000 – 36135.6

= 16864.4 units

Margin of safety (MOS) in terms of revenue = profit / PV ratio

= 49750 / 22.69 %

= £ 219260

c ) Computation of profit for Stockstone Ltd when they produce 48000 electric kettle

Income statements

Particulars Amount (£)

Sales (13*48000) 624000

Less : variables cost

Material cost ( 5.25 * 48000 ) 252000

Labour cost ( 2.95 * 48000 ) 141600

Variable overhead ( 1.85 * 48000 ) 88800

Contribution 141600

Less : Fixed cost

Production 59000

Selling 47600

Profit 35000

= 36135.6 units

Price volume ratio (PV ratio) = contribution / sales * 100

= 2.95 / 13 * 100

= 22.69 %

Break even point (BEP) in terms of revenue = fixed cost / price volume ratio

= £ 59000 + £ 47600 / 22.69 %

= £ 469810.49

Margin of safety (MOS) in terms of units = Total units – BEP units

= 53000 – 36135.6

= 16864.4 units

Margin of safety (MOS) in terms of revenue = profit / PV ratio

= 49750 / 22.69 %

= £ 219260

c ) Computation of profit for Stockstone Ltd when they produce 48000 electric kettle

Income statements

Particulars Amount (£)

Sales (13*48000) 624000

Less : variables cost

Material cost ( 5.25 * 48000 ) 252000

Labour cost ( 2.95 * 48000 ) 141600

Variable overhead ( 1.85 * 48000 ) 88800

Contribution 141600

Less : Fixed cost

Production 59000

Selling 47600

Profit 35000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

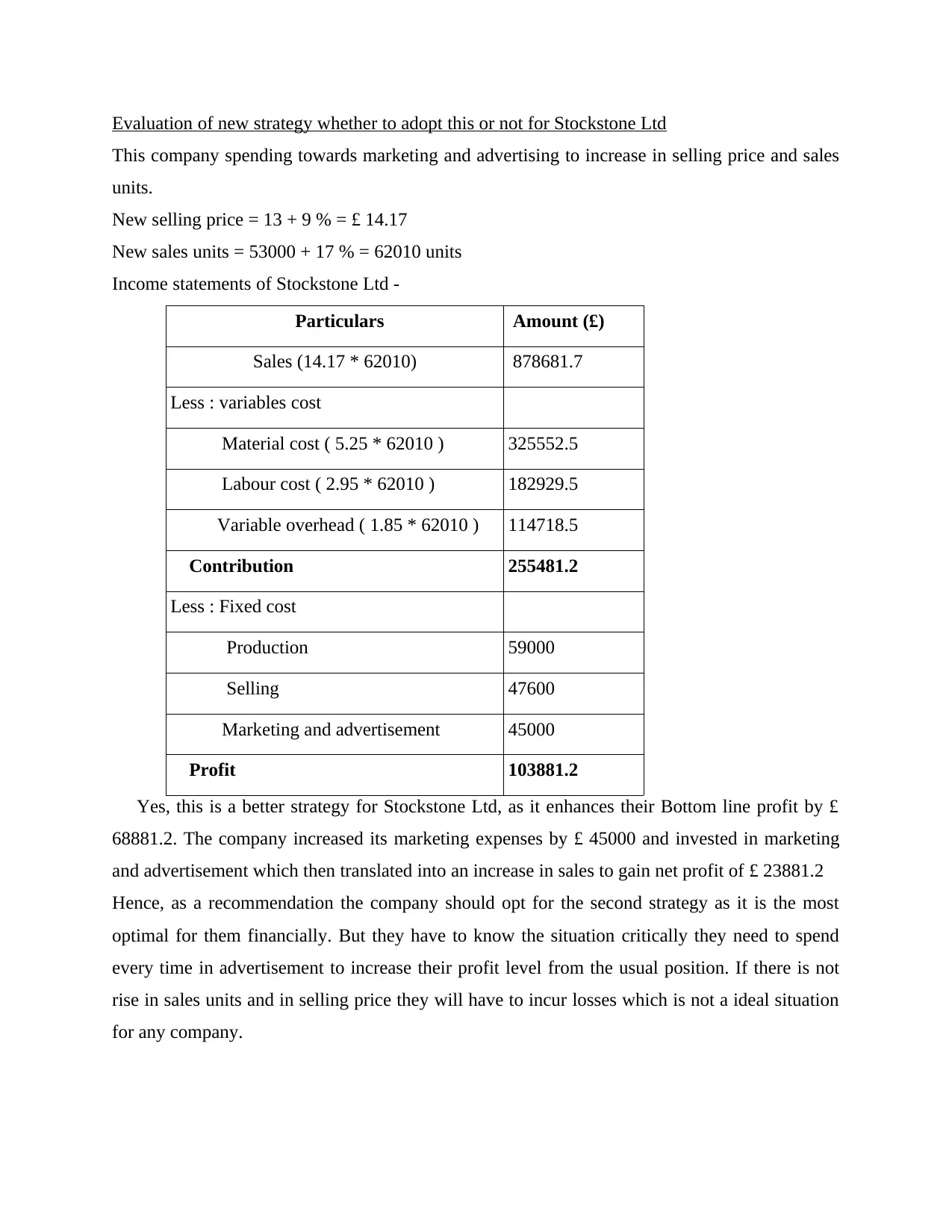

Evaluation of new strategy whether to adopt this or not for Stockstone Ltd

This company spending towards marketing and advertising to increase in selling price and sales

units.

New selling price = 13 + 9 % = £ 14.17

New sales units = 53000 + 17 % = 62010 units

Income statements of Stockstone Ltd -

Particulars Amount (£)

Sales (14.17 * 62010) 878681.7

Less : variables cost

Material cost ( 5.25 * 62010 ) 325552.5

Labour cost ( 2.95 * 62010 ) 182929.5

Variable overhead ( 1.85 * 62010 ) 114718.5

Contribution 255481.2

Less : Fixed cost

Production 59000

Selling 47600

Marketing and advertisement 45000

Profit 103881.2

Yes, this is a better strategy for Stockstone Ltd, as it enhances their Bottom line profit by £

68881.2. The company increased its marketing expenses by £ 45000 and invested in marketing

and advertisement which then translated into an increase in sales to gain net profit of £ 23881.2

Hence, as a recommendation the company should opt for the second strategy as it is the most

optimal for them financially. But they have to know the situation critically they need to spend

every time in advertisement to increase their profit level from the usual position. If there is not

rise in sales units and in selling price they will have to incur losses which is not a ideal situation

for any company.

This company spending towards marketing and advertising to increase in selling price and sales

units.

New selling price = 13 + 9 % = £ 14.17

New sales units = 53000 + 17 % = 62010 units

Income statements of Stockstone Ltd -

Particulars Amount (£)

Sales (14.17 * 62010) 878681.7

Less : variables cost

Material cost ( 5.25 * 62010 ) 325552.5

Labour cost ( 2.95 * 62010 ) 182929.5

Variable overhead ( 1.85 * 62010 ) 114718.5

Contribution 255481.2

Less : Fixed cost

Production 59000

Selling 47600

Marketing and advertisement 45000

Profit 103881.2

Yes, this is a better strategy for Stockstone Ltd, as it enhances their Bottom line profit by £

68881.2. The company increased its marketing expenses by £ 45000 and invested in marketing

and advertisement which then translated into an increase in sales to gain net profit of £ 23881.2

Hence, as a recommendation the company should opt for the second strategy as it is the most

optimal for them financially. But they have to know the situation critically they need to spend

every time in advertisement to increase their profit level from the usual position. If there is not

rise in sales units and in selling price they will have to incur losses which is not a ideal situation

for any company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E ) Assumptions of break even model and analysis of the model used successfully in different

types of business :

Break even point is defined as mass of production and volume of gross sales where there exist

situation of no profit no loss (Cai, 2021). It assists company in finding out the relation between

the revenue and cost in accordance with company's output. In other words, in order to gain the

knowledge of break even point its better to understand the relationship between cost,volume and

profit. There exist some of the important use of Break-even is help in determining the effect of

change in volume, profit determination and ascertaining the comparability of profit for each

products. In marginal costing, there have to follow many assumption of implementing break

even point are :

all expenses which incurred in producing goods shall be segregate into variable and fixed

expenses.

For all level of output produced, the fixed expenses incurred irrespective of units sold

will remain constant .

For every change attached with output produced, variable cost will also change in

accordance with units .

The primary assumption for product mix is that it will remain same throughout the

reporting period.

When it comes to selling price it will also remain same for calculating the profit for each

level of output.

The quantity of output of income will coincide with the units produced in order that there

may be no commencing or final stock .

It has been assumed that productivity per labour or employees will remain constant.

But there is shortcoming also for break even analysis are discussed below :

1. As break even calculation is generally based on assumption that all the expenditure is

segregate into fixed and variable cost but in practical terms it is not possible to

accomplish clear cut division of costs(Dean and et.al., 2020).

2. As break-even analysis is purely based on fixed cost remain constant but it will change at

a time when level of activity go beyond a certain level.

3. In practical terms, one product is produced or product mix remain constant is not at all

possible.

types of business :

Break even point is defined as mass of production and volume of gross sales where there exist

situation of no profit no loss (Cai, 2021). It assists company in finding out the relation between

the revenue and cost in accordance with company's output. In other words, in order to gain the

knowledge of break even point its better to understand the relationship between cost,volume and

profit. There exist some of the important use of Break-even is help in determining the effect of

change in volume, profit determination and ascertaining the comparability of profit for each

products. In marginal costing, there have to follow many assumption of implementing break

even point are :

all expenses which incurred in producing goods shall be segregate into variable and fixed

expenses.

For all level of output produced, the fixed expenses incurred irrespective of units sold

will remain constant .

For every change attached with output produced, variable cost will also change in

accordance with units .

The primary assumption for product mix is that it will remain same throughout the

reporting period.

When it comes to selling price it will also remain same for calculating the profit for each

level of output.

The quantity of output of income will coincide with the units produced in order that there

may be no commencing or final stock .

It has been assumed that productivity per labour or employees will remain constant.

But there is shortcoming also for break even analysis are discussed below :

1. As break even calculation is generally based on assumption that all the expenditure is

segregate into fixed and variable cost but in practical terms it is not possible to

accomplish clear cut division of costs(Dean and et.al., 2020).

2. As break-even analysis is purely based on fixed cost remain constant but it will change at

a time when level of activity go beyond a certain level.

3. In practical terms, one product is produced or product mix remain constant is not at all

possible.

4. The basic limitation of break even analysis is that it does not take into account capital

employed which are employ in the business.

The break even model is successfully be utilised in different types of business through it assists

in ascertaining the selling price which will give the desired net income. Break even helps every

business to get their return on capital employed through which they fix their sales units. By

calculating break even model, it will helps in getting comparable analysis between inter firm. It

is highly successful in implementing the break even analysis as it helps management of any

organisation in terms of taking prompt decision making like make or buy decision or introducing

a new market in new market, in forecasting, extend term planning and maintaining profitability

(Faccia and Lootah, 2019). Break even analysis helps in strengthen the business operations and

enhance profit earning capacity without much problem.

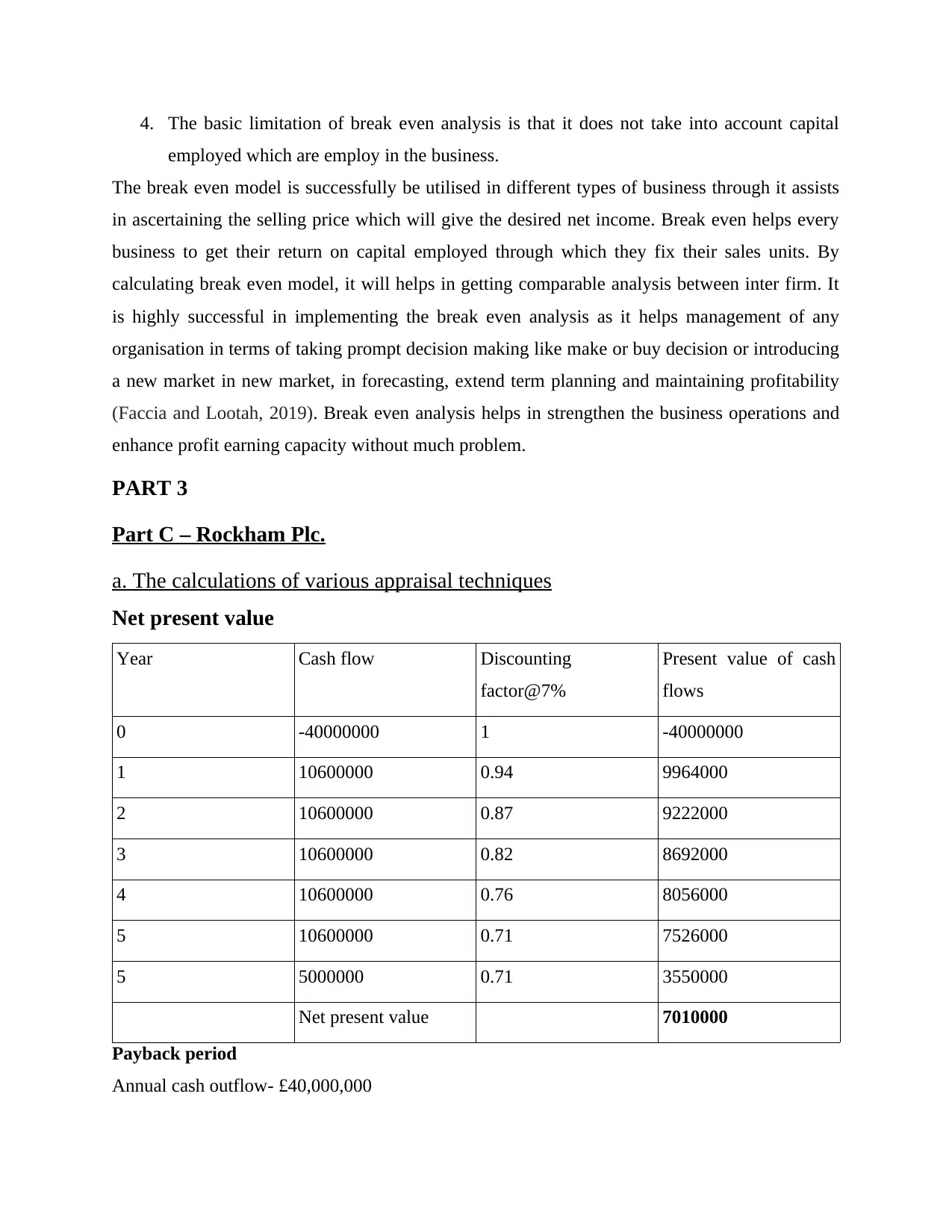

PART 3

Part C – Rockham Plc.

a. The calculations of various appraisal techniques

Net present value

Year Cash flow Discounting

factor@7%

Present value of cash

flows

0 -40000000 1 -40000000

1 10600000 0.94 9964000

2 10600000 0.87 9222000

3 10600000 0.82 8692000

4 10600000 0.76 8056000

5 10600000 0.71 7526000

5 5000000 0.71 3550000

Net present value 7010000

Payback period

Annual cash outflow- £40,000,000

employed which are employ in the business.

The break even model is successfully be utilised in different types of business through it assists

in ascertaining the selling price which will give the desired net income. Break even helps every

business to get their return on capital employed through which they fix their sales units. By

calculating break even model, it will helps in getting comparable analysis between inter firm. It

is highly successful in implementing the break even analysis as it helps management of any

organisation in terms of taking prompt decision making like make or buy decision or introducing

a new market in new market, in forecasting, extend term planning and maintaining profitability

(Faccia and Lootah, 2019). Break even analysis helps in strengthen the business operations and

enhance profit earning capacity without much problem.

PART 3

Part C – Rockham Plc.

a. The calculations of various appraisal techniques

Net present value

Year Cash flow Discounting

factor@7%

Present value of cash

flows

0 -40000000 1 -40000000

1 10600000 0.94 9964000

2 10600000 0.87 9222000

3 10600000 0.82 8692000

4 10600000 0.76 8056000

5 10600000 0.71 7526000

5 5000000 0.71 3550000

Net present value 7010000

Payback period

Annual cash outflow- £40,000,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

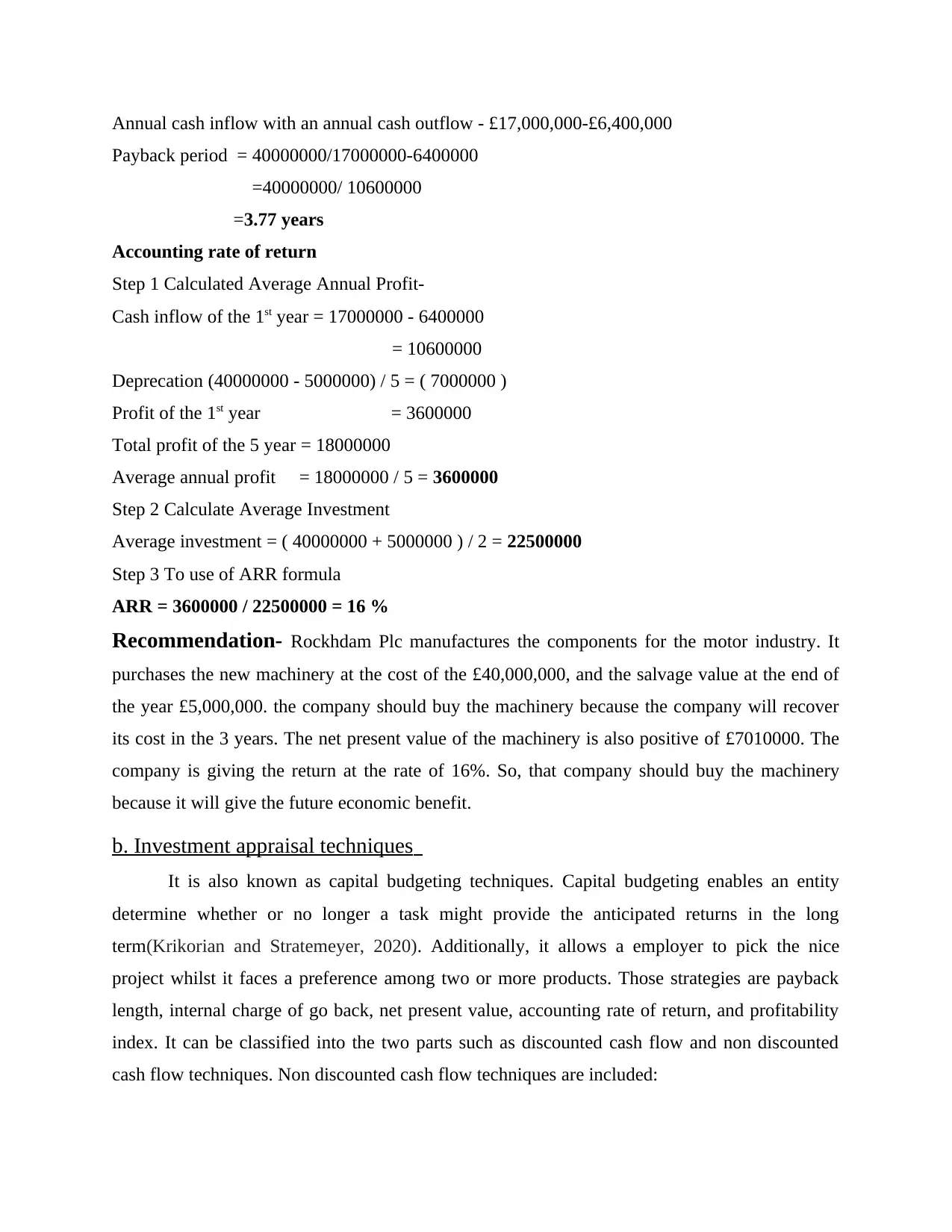

Annual cash inflow with an annual cash outflow - £17,000,000-£6,400,000

Payback period = 40000000/17000000-6400000

=40000000/ 10600000

=3.77 years

Accounting rate of return

Step 1 Calculated Average Annual Profit-

Cash inflow of the 1st year = 17000000 - 6400000

= 10600000

Deprecation (40000000 - 5000000) / 5 = ( 7000000 )

Profit of the 1st year = 3600000

Total profit of the 5 year = 18000000

Average annual profit = 18000000 / 5 = 3600000

Step 2 Calculate Average Investment

Average investment = ( 40000000 + 5000000 ) / 2 = 22500000

Step 3 To use of ARR formula

ARR = 3600000 / 22500000 = 16 %

Recommendation- Rockhdam Plc manufactures the components for the motor industry. It

purchases the new machinery at the cost of the £40,000,000, and the salvage value at the end of

the year £5,000,000. the company should buy the machinery because the company will recover

its cost in the 3 years. The net present value of the machinery is also positive of £7010000. The

company is giving the return at the rate of 16%. So, that company should buy the machinery

because it will give the future economic benefit.

b. Investment appraisal techniques

It is also known as capital budgeting techniques. Capital budgeting enables an entity

determine whether or no longer a task might provide the anticipated returns in the long

term(Krikorian and Stratemeyer, 2020). Additionally, it allows a employer to pick the nice

project whilst it faces a preference among two or more products. Those strategies are payback

length, internal charge of go back, net present value, accounting rate of return, and profitability

index. It can be classified into the two parts such as discounted cash flow and non discounted

cash flow techniques. Non discounted cash flow techniques are included:

Payback period = 40000000/17000000-6400000

=40000000/ 10600000

=3.77 years

Accounting rate of return

Step 1 Calculated Average Annual Profit-

Cash inflow of the 1st year = 17000000 - 6400000

= 10600000

Deprecation (40000000 - 5000000) / 5 = ( 7000000 )

Profit of the 1st year = 3600000

Total profit of the 5 year = 18000000

Average annual profit = 18000000 / 5 = 3600000

Step 2 Calculate Average Investment

Average investment = ( 40000000 + 5000000 ) / 2 = 22500000

Step 3 To use of ARR formula

ARR = 3600000 / 22500000 = 16 %

Recommendation- Rockhdam Plc manufactures the components for the motor industry. It

purchases the new machinery at the cost of the £40,000,000, and the salvage value at the end of

the year £5,000,000. the company should buy the machinery because the company will recover

its cost in the 3 years. The net present value of the machinery is also positive of £7010000. The

company is giving the return at the rate of 16%. So, that company should buy the machinery

because it will give the future economic benefit.

b. Investment appraisal techniques

It is also known as capital budgeting techniques. Capital budgeting enables an entity

determine whether or no longer a task might provide the anticipated returns in the long

term(Krikorian and Stratemeyer, 2020). Additionally, it allows a employer to pick the nice

project whilst it faces a preference among two or more products. Those strategies are payback

length, internal charge of go back, net present value, accounting rate of return, and profitability

index. It can be classified into the two parts such as discounted cash flow and non discounted

cash flow techniques. Non discounted cash flow techniques are included:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

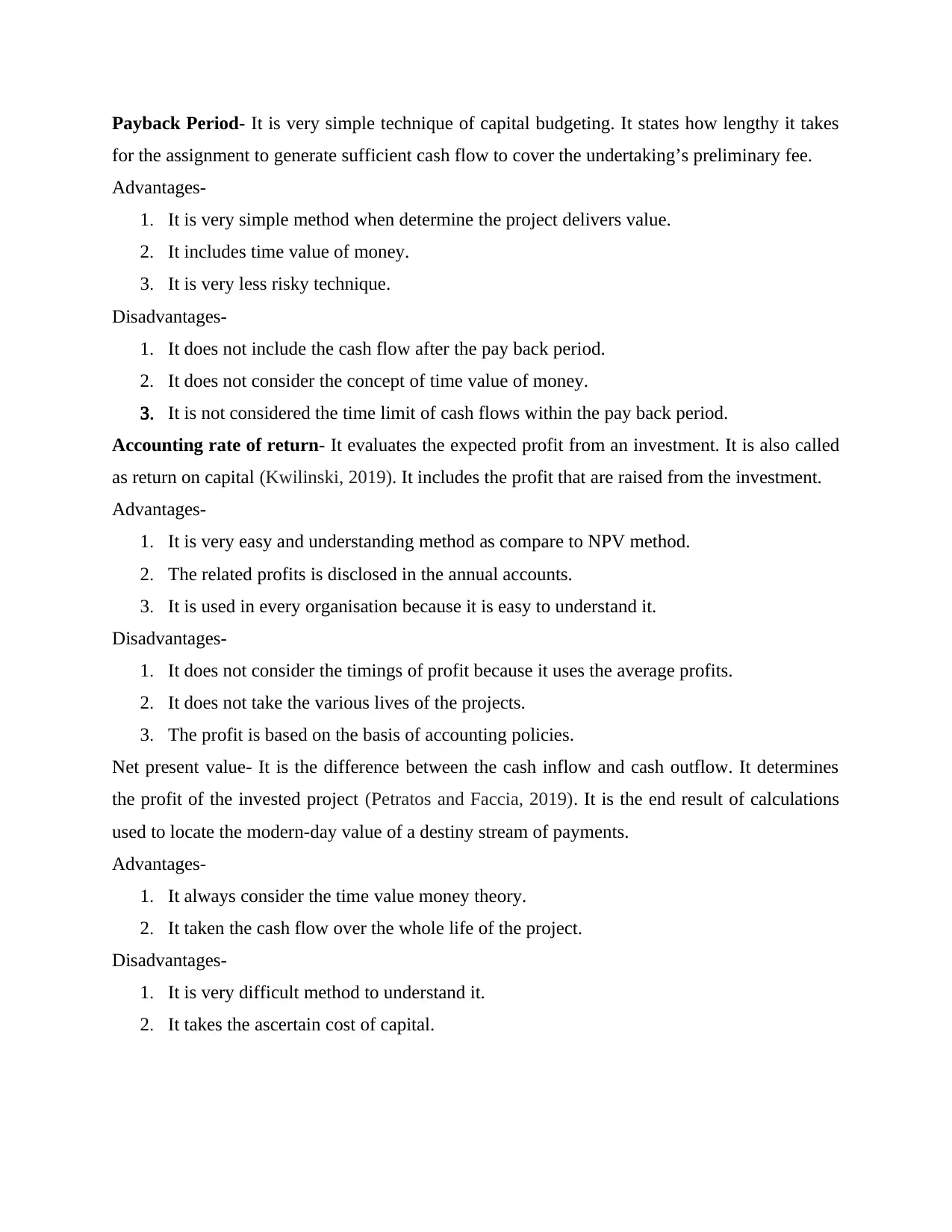

Payback Period- It is very simple technique of capital budgeting. It states how lengthy it takes

for the assignment to generate sufficient cash flow to cover the undertaking’s preliminary fee.

Advantages-

1. It is very simple method when determine the project delivers value.

2. It includes time value of money.

3. It is very less risky technique.

Disadvantages-

1. It does not include the cash flow after the pay back period.

2. It does not consider the concept of time value of money.

3. It is not considered the time limit of cash flows within the pay back period.

Accounting rate of return- It evaluates the expected profit from an investment. It is also called

as return on capital (Kwilinski, 2019). It includes the profit that are raised from the investment.

Advantages-

1. It is very easy and understanding method as compare to NPV method.

2. The related profits is disclosed in the annual accounts.

3. It is used in every organisation because it is easy to understand it.

Disadvantages-

1. It does not consider the timings of profit because it uses the average profits.

2. It does not take the various lives of the projects.

3. The profit is based on the basis of accounting policies.

Net present value- It is the difference between the cash inflow and cash outflow. It determines

the profit of the invested project (Petratos and Faccia, 2019). It is the end result of calculations

used to locate the modern-day value of a destiny stream of payments.

Advantages-

1. It always consider the time value money theory.

2. It taken the cash flow over the whole life of the project.

Disadvantages-

1. It is very difficult method to understand it.

2. It takes the ascertain cost of capital.

for the assignment to generate sufficient cash flow to cover the undertaking’s preliminary fee.

Advantages-

1. It is very simple method when determine the project delivers value.

2. It includes time value of money.

3. It is very less risky technique.

Disadvantages-

1. It does not include the cash flow after the pay back period.

2. It does not consider the concept of time value of money.

3. It is not considered the time limit of cash flows within the pay back period.

Accounting rate of return- It evaluates the expected profit from an investment. It is also called

as return on capital (Kwilinski, 2019). It includes the profit that are raised from the investment.

Advantages-

1. It is very easy and understanding method as compare to NPV method.

2. The related profits is disclosed in the annual accounts.

3. It is used in every organisation because it is easy to understand it.

Disadvantages-

1. It does not consider the timings of profit because it uses the average profits.

2. It does not take the various lives of the projects.

3. The profit is based on the basis of accounting policies.

Net present value- It is the difference between the cash inflow and cash outflow. It determines

the profit of the invested project (Petratos and Faccia, 2019). It is the end result of calculations

used to locate the modern-day value of a destiny stream of payments.

Advantages-

1. It always consider the time value money theory.

2. It taken the cash flow over the whole life of the project.

Disadvantages-

1. It is very difficult method to understand it.

2. It takes the ascertain cost of capital.

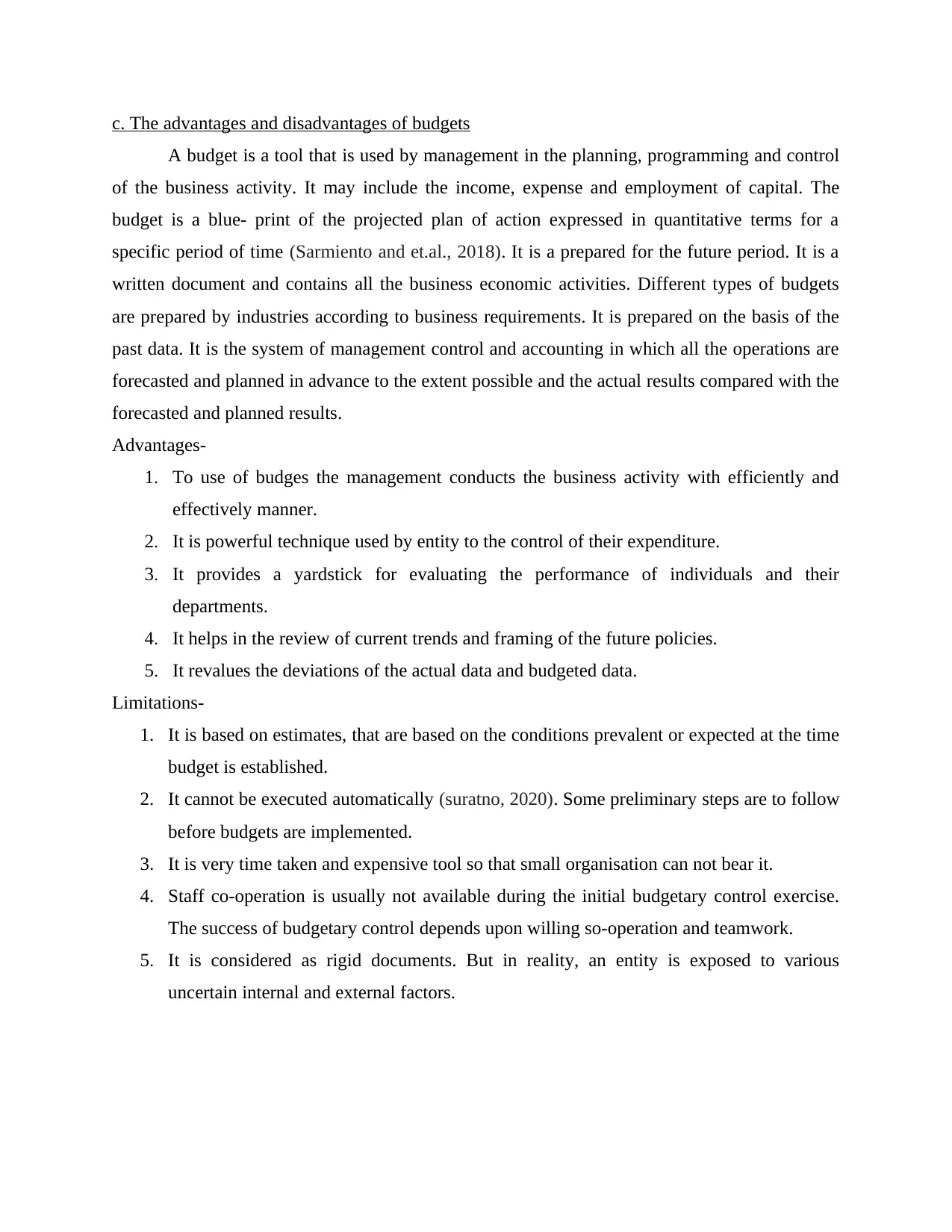

c. The advantages and disadvantages of budgets

A budget is a tool that is used by management in the planning, programming and control

of the business activity. It may include the income, expense and employment of capital. The

budget is a blue- print of the projected plan of action expressed in quantitative terms for a

specific period of time (Sarmiento and et.al., 2018). It is a prepared for the future period. It is a

written document and contains all the business economic activities. Different types of budgets

are prepared by industries according to business requirements. It is prepared on the basis of the

past data. It is the system of management control and accounting in which all the operations are

forecasted and planned in advance to the extent possible and the actual results compared with the

forecasted and planned results.

Advantages-

1. To use of budges the management conducts the business activity with efficiently and

effectively manner.

2. It is powerful technique used by entity to the control of their expenditure.

3. It provides a yardstick for evaluating the performance of individuals and their

departments.

4. It helps in the review of current trends and framing of the future policies.

5. It revalues the deviations of the actual data and budgeted data.

Limitations-

1. It is based on estimates, that are based on the conditions prevalent or expected at the time

budget is established.

2. It cannot be executed automatically (suratno, 2020). Some preliminary steps are to follow

before budgets are implemented.

3. It is very time taken and expensive tool so that small organisation can not bear it.

4. Staff co-operation is usually not available during the initial budgetary control exercise.

The success of budgetary control depends upon willing so-operation and teamwork.

5. It is considered as rigid documents. But in reality, an entity is exposed to various

uncertain internal and external factors.

A budget is a tool that is used by management in the planning, programming and control

of the business activity. It may include the income, expense and employment of capital. The

budget is a blue- print of the projected plan of action expressed in quantitative terms for a

specific period of time (Sarmiento and et.al., 2018). It is a prepared for the future period. It is a

written document and contains all the business economic activities. Different types of budgets

are prepared by industries according to business requirements. It is prepared on the basis of the

past data. It is the system of management control and accounting in which all the operations are

forecasted and planned in advance to the extent possible and the actual results compared with the

forecasted and planned results.

Advantages-

1. To use of budges the management conducts the business activity with efficiently and

effectively manner.

2. It is powerful technique used by entity to the control of their expenditure.

3. It provides a yardstick for evaluating the performance of individuals and their

departments.

4. It helps in the review of current trends and framing of the future policies.

5. It revalues the deviations of the actual data and budgeted data.

Limitations-

1. It is based on estimates, that are based on the conditions prevalent or expected at the time

budget is established.

2. It cannot be executed automatically (suratno, 2020). Some preliminary steps are to follow

before budgets are implemented.

3. It is very time taken and expensive tool so that small organisation can not bear it.

4. Staff co-operation is usually not available during the initial budgetary control exercise.

The success of budgetary control depends upon willing so-operation and teamwork.

5. It is considered as rigid documents. But in reality, an entity is exposed to various

uncertain internal and external factors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.