MBB7008M - Accounting & Finance for Decision Making - YSJU Resit

VerifiedAdded on 2023/06/18

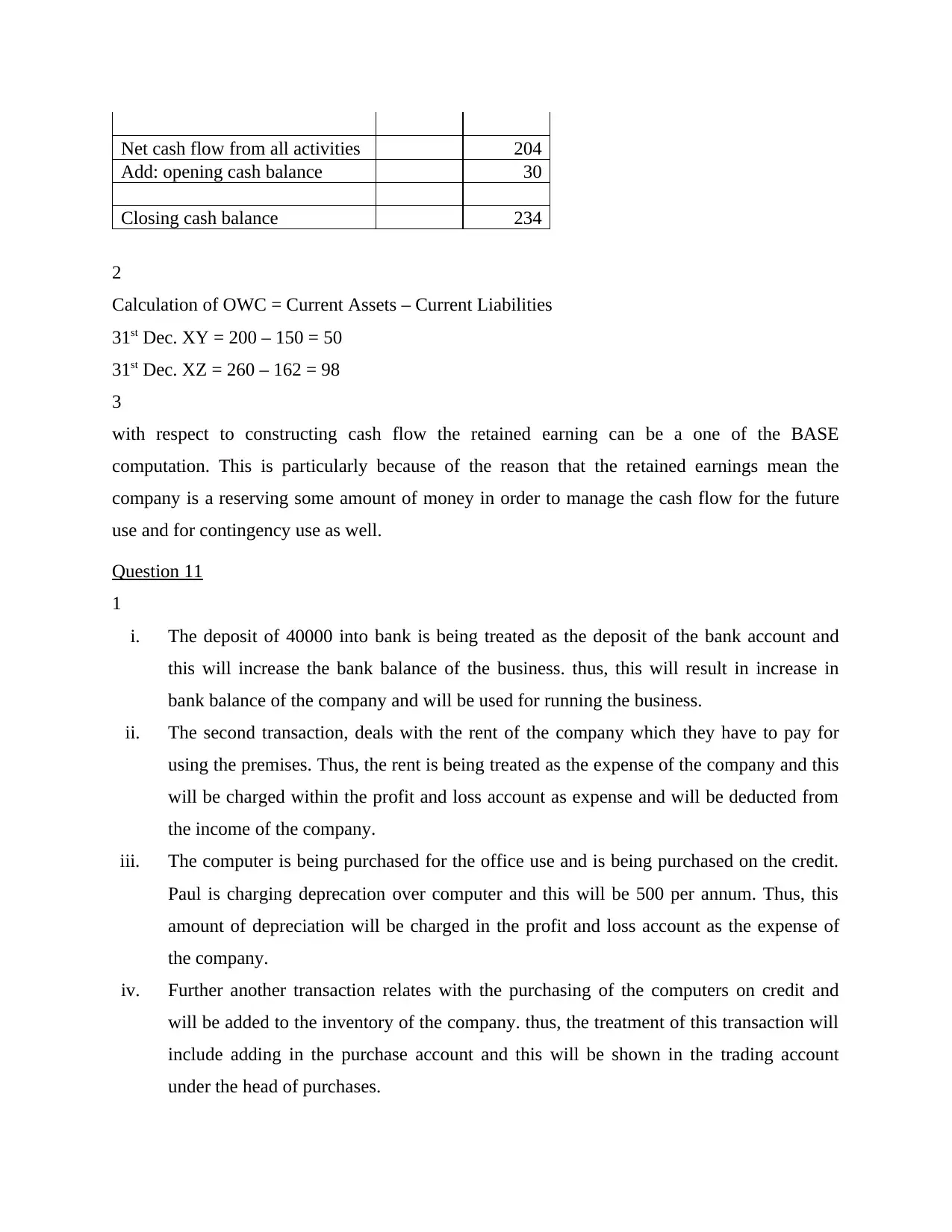

|8

|1292

|320

Homework Assignment

AI Summary

This assignment provides solutions to questions related to accounting and finance for decision-making. It includes multiple-choice answers, calculations of EBITDA, effective tax rates, and cleaned net income. Furthermore, it analyzes the impact of various transactions on a company's equity and prepares a cash flow statement. The assignment also discusses the treatment of different business transactions, such as deposits, rent payments, and the purchase and sale of computers, within the accounting framework, ultimately assessing the financial performance of a hypothetical business scenario. Desklib is a great resource for students looking for similar solved assignments and past papers.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.