Accounting and Finance: Present Value, Annuity, Future Value, Taxation and Investment Returns

VerifiedAdded on 2023/06/14

|17

|3291

|343

AI Summary

This article covers topics related to Accounting and Finance such as Present Value, Annuity, Future Value, Taxation and Investment Returns. It includes calculations and analysis for better understanding.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the University

Author Note

Accounting and finance

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................3

Requirement c:.......................................................................................................................3

Answer to Question 2:................................................................................................................4

Requirement i:........................................................................................................................4

Requirement ii:.......................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................8

Requirement i:........................................................................................................................8

Requirement ii:.......................................................................................................................9

Requirement iii:....................................................................................................................10

Requirement iv:....................................................................................................................10

Requirement v:.....................................................................................................................11

Requirement vi:....................................................................................................................11

Requirement vii:...................................................................................................................12

Requirement viii:..................................................................................................................12

Requirement ix:....................................................................................................................13

References list:.........................................................................................................................14

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................3

Requirement c:.......................................................................................................................3

Answer to Question 2:................................................................................................................4

Requirement i:........................................................................................................................4

Requirement ii:.......................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................8

Requirement i:........................................................................................................................8

Requirement ii:.......................................................................................................................9

Requirement iii:....................................................................................................................10

Requirement iv:....................................................................................................................10

Requirement v:.....................................................................................................................11

Requirement vi:....................................................................................................................11

Requirement vii:...................................................................................................................12

Requirement viii:..................................................................................................................12

Requirement ix:....................................................................................................................13

References list:.........................................................................................................................14

2

ACCOUNTING AND FINANCE

Answer to Question 1:

Requirement a:

Sandy would receive a stream of cash flows within the next 4 years. Therefore, it is

necessary to determine the discounted values of the expected cash flow stream for computing

the present value of the whole investment. The formula of discounted cash flow is shown

below:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

By using the stated formula, the present value of the investment is calculated below:

ΣDCF = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 400

(1+9 % )1 + 800

(1+9 %)2 + 500

(1+9 % )3 + 400

(1+9 % )4 + 300

(1+9 % )5

= 400

1.09 + 800

1.188 + 500

1.295 + 400

1.412 + 300

1.539

= 366.97+673.34 +386.09+283.37+194.98

= 1904.76

As per the above calculations, it can be stated that Sandy has to pay $1,904.76 for the

investment option to earn the given cash flow streams.

ACCOUNTING AND FINANCE

Answer to Question 1:

Requirement a:

Sandy would receive a stream of cash flows within the next 4 years. Therefore, it is

necessary to determine the discounted values of the expected cash flow stream for computing

the present value of the whole investment. The formula of discounted cash flow is shown

below:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

By using the stated formula, the present value of the investment is calculated below:

ΣDCF = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 400

(1+9 % )1 + 800

(1+9 %)2 + 500

(1+9 % )3 + 400

(1+9 % )4 + 300

(1+9 % )5

= 400

1.09 + 800

1.188 + 500

1.295 + 400

1.412 + 300

1.539

= 366.97+673.34 +386.09+283.37+194.98

= 1904.76

As per the above calculations, it can be stated that Sandy has to pay $1,904.76 for the

investment option to earn the given cash flow streams.

3

ACCOUNTING AND FINANCE

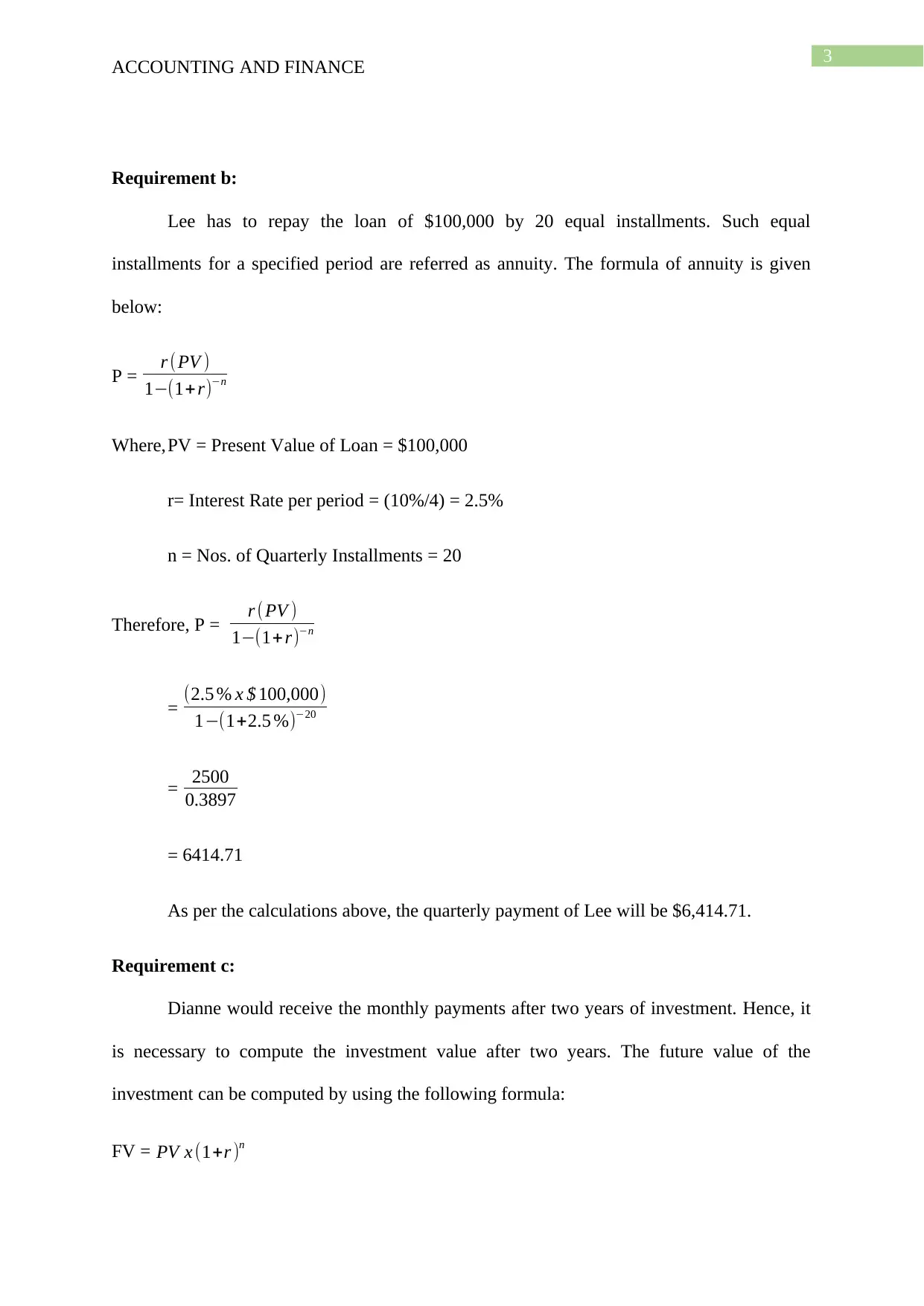

Requirement b:

Lee has to repay the loan of $100,000 by 20 equal installments. Such equal

installments for a specified period are referred as annuity. The formula of annuity is given

below:

P = r (PV )

1−(1+r)−n

Where,PV = Present Value of Loan = $100,000

r= Interest Rate per period = (10%/4) = 2.5%

n = Nos. of Quarterly Installments = 20

Therefore, P = r (PV )

1−(1+ r)−n

= (2.5 % x $ 100,000)

1−(1+2.5 %)−20

= 2500

0.3897

= 6414.71

As per the calculations above, the quarterly payment of Lee will be $6,414.71.

Requirement c:

Dianne would receive the monthly payments after two years of investment. Hence, it

is necessary to compute the investment value after two years. The future value of the

investment can be computed by using the following formula:

FV = PV x (1+r )n

ACCOUNTING AND FINANCE

Requirement b:

Lee has to repay the loan of $100,000 by 20 equal installments. Such equal

installments for a specified period are referred as annuity. The formula of annuity is given

below:

P = r (PV )

1−(1+r)−n

Where,PV = Present Value of Loan = $100,000

r= Interest Rate per period = (10%/4) = 2.5%

n = Nos. of Quarterly Installments = 20

Therefore, P = r (PV )

1−(1+ r)−n

= (2.5 % x $ 100,000)

1−(1+2.5 %)−20

= 2500

0.3897

= 6414.71

As per the calculations above, the quarterly payment of Lee will be $6,414.71.

Requirement c:

Dianne would receive the monthly payments after two years of investment. Hence, it

is necessary to compute the investment value after two years. The future value of the

investment can be computed by using the following formula:

FV = PV x (1+r )n

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ACCOUNTING AND FINANCE

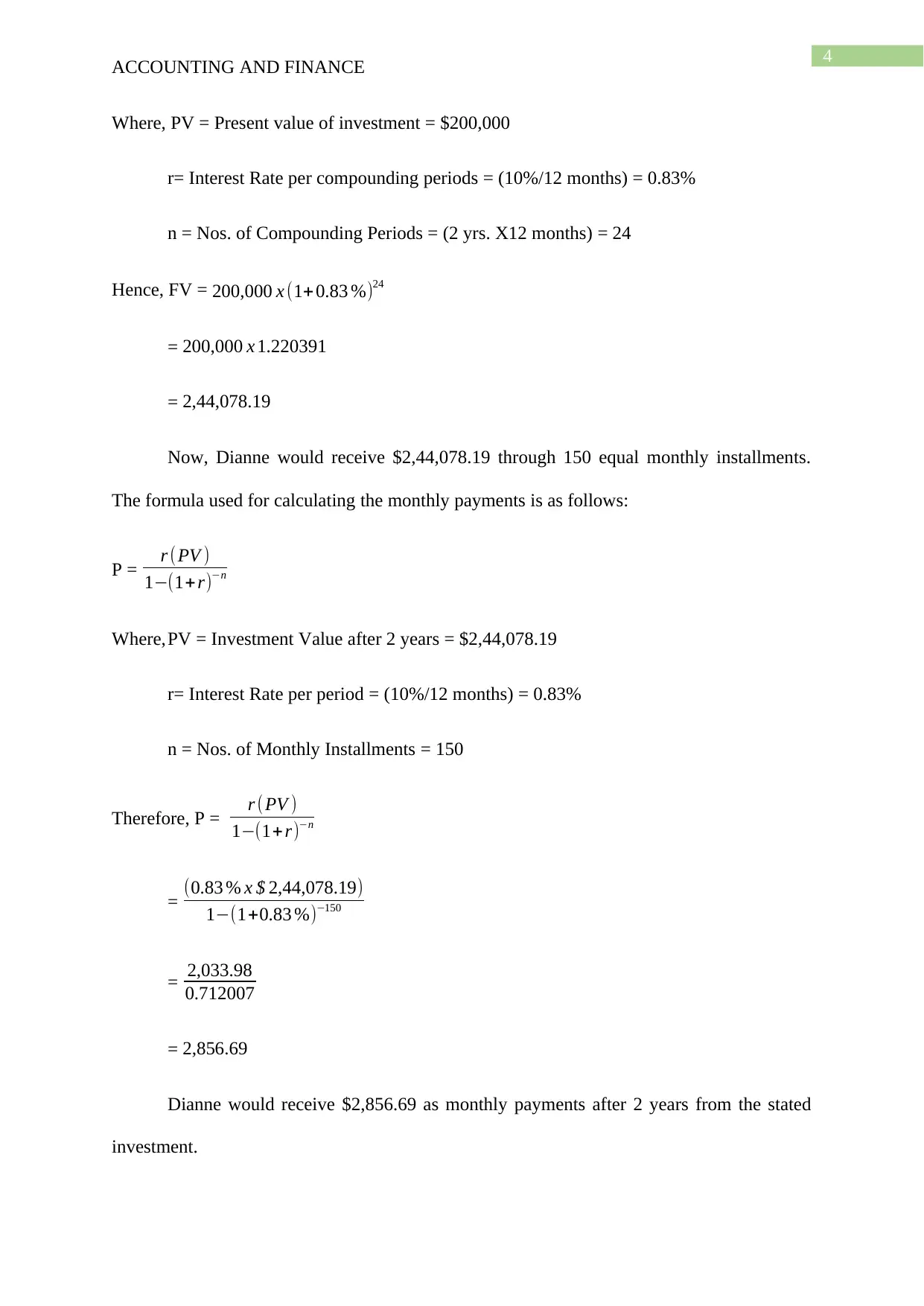

Where, PV = Present value of investment = $200,000

r= Interest Rate per compounding periods = (10%/12 months) = 0.83%

n = Nos. of Compounding Periods = (2 yrs. X12 months) = 24

Hence, FV = 200,000 x (1+ 0.83 %)24

= 200,000 x 1.220391

= 2,44,078.19

Now, Dianne would receive $2,44,078.19 through 150 equal monthly installments.

The formula used for calculating the monthly payments is as follows:

P = r (PV )

1−(1+r)−n

Where,PV = Investment Value after 2 years = $2,44,078.19

r= Interest Rate per period = (10%/12 months) = 0.83%

n = Nos. of Monthly Installments = 150

Therefore, P = r (PV )

1−(1+ r)−n

= (0.83 % x $ 2,44,078.19)

1−(1+0.83 %)−150

= 2,033.98

0.712007

= 2,856.69

Dianne would receive $2,856.69 as monthly payments after 2 years from the stated

investment.

ACCOUNTING AND FINANCE

Where, PV = Present value of investment = $200,000

r= Interest Rate per compounding periods = (10%/12 months) = 0.83%

n = Nos. of Compounding Periods = (2 yrs. X12 months) = 24

Hence, FV = 200,000 x (1+ 0.83 %)24

= 200,000 x 1.220391

= 2,44,078.19

Now, Dianne would receive $2,44,078.19 through 150 equal monthly installments.

The formula used for calculating the monthly payments is as follows:

P = r (PV )

1−(1+r)−n

Where,PV = Investment Value after 2 years = $2,44,078.19

r= Interest Rate per period = (10%/12 months) = 0.83%

n = Nos. of Monthly Installments = 150

Therefore, P = r (PV )

1−(1+ r)−n

= (0.83 % x $ 2,44,078.19)

1−(1+0.83 %)−150

= 2,033.98

0.712007

= 2,856.69

Dianne would receive $2,856.69 as monthly payments after 2 years from the stated

investment.

5

ACCOUNTING AND FINANCE

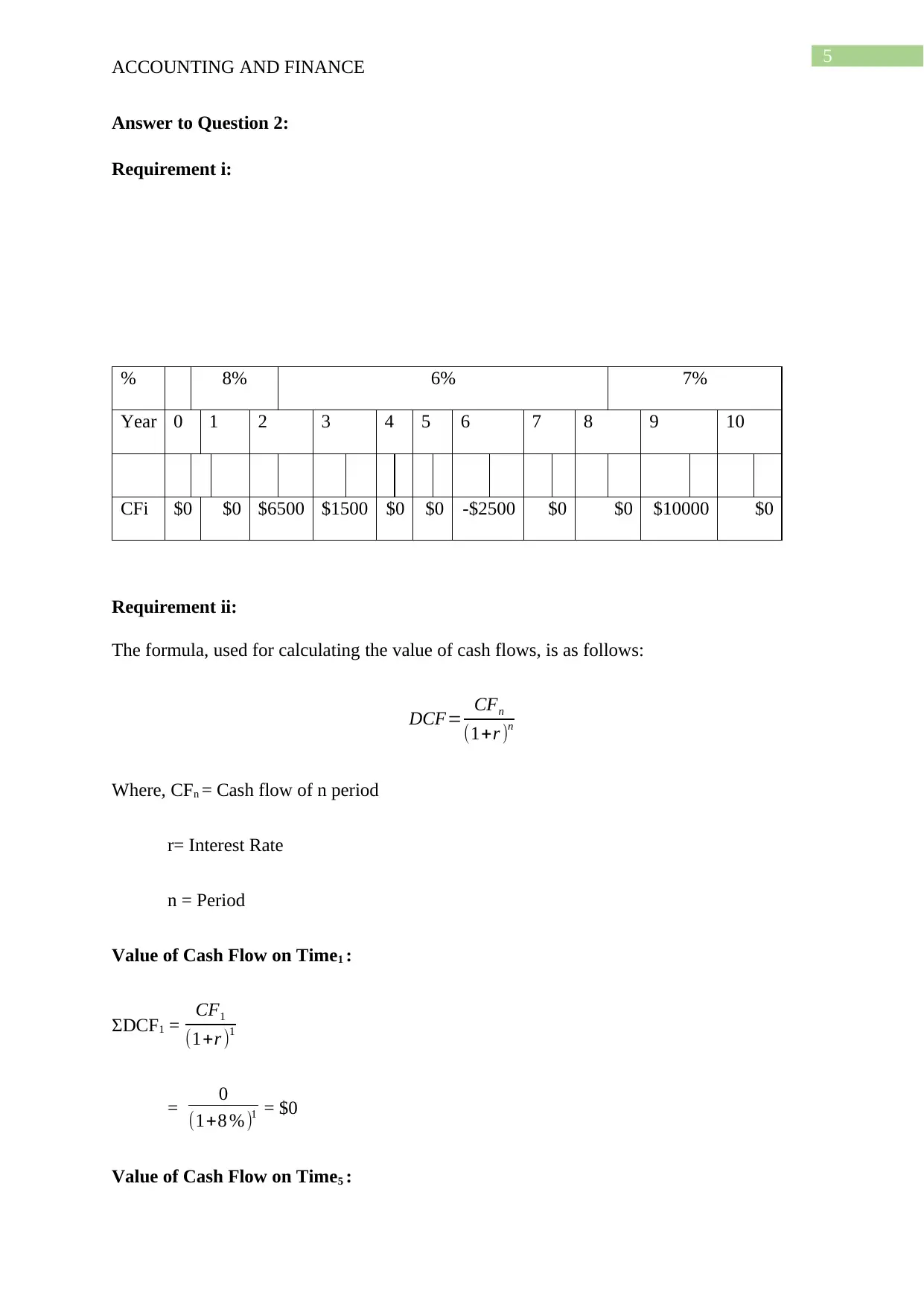

Answer to Question 2:

Requirement i:

% 8% 6% 7%

Year 0 1 2 3 4 5 6 7 8 9 10

CFi $0 $0 $6500 $1500 $0 $0 -$2500 $0 $0 $10000 $0

Requirement ii:

The formula, used for calculating the value of cash flows, is as follows:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

Value of Cash Flow on Time1 :

ΣDCF1 = CF1

(1+r )1

= 0

(1+8 % )1 = $0

Value of Cash Flow on Time5 :

ACCOUNTING AND FINANCE

Answer to Question 2:

Requirement i:

% 8% 6% 7%

Year 0 1 2 3 4 5 6 7 8 9 10

CFi $0 $0 $6500 $1500 $0 $0 -$2500 $0 $0 $10000 $0

Requirement ii:

The formula, used for calculating the value of cash flows, is as follows:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

Value of Cash Flow on Time1 :

ΣDCF1 = CF1

(1+r )1

= 0

(1+8 % )1 = $0

Value of Cash Flow on Time5 :

6

ACCOUNTING AND FINANCE

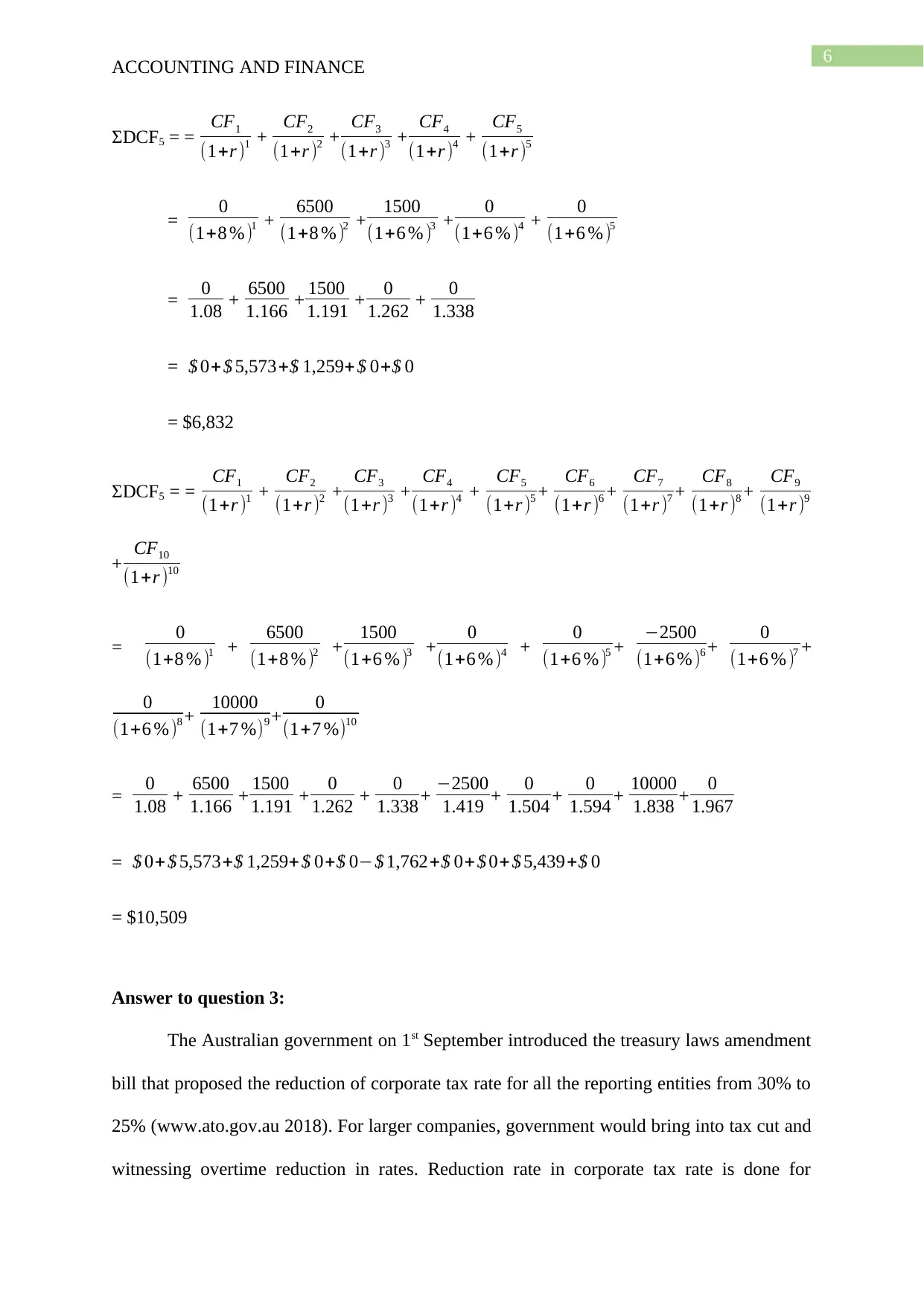

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 0

(1+8 % )1 + 6500

(1+8 %)2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 %)5

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338

= $ 0+$ 5,573+$ 1,259+ $ 0+$ 0

= $6,832

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5 + CF6

(1+r )6 + CF7

(1+r )7 + CF8

(1+r )8 + CF9

(1+r )9

+ CF10

(1+r )10

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5 + −2500

(1+6 % )6 + 0

(1+6 % )7 +

0

(1+6 %)8 + 10000

(1+7 %)9 + 0

(1+7 %)10

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338+ −2500

1.419 + 0

1.504 + 0

1.594 + 10000

1.838 + 0

1.967

= $ 0+ $ 5,573+$ 1,259+$ 0+$ 0−$ 1,762+$ 0+ $ 0+ $ 5,439+$ 0

= $10,509

Answer to question 3:

The Australian government on 1st September introduced the treasury laws amendment

bill that proposed the reduction of corporate tax rate for all the reporting entities from 30% to

25% (www.ato.gov.au 2018). For larger companies, government would bring into tax cut and

witnessing overtime reduction in rates. Reduction rate in corporate tax rate is done for

ACCOUNTING AND FINANCE

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 0

(1+8 % )1 + 6500

(1+8 %)2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 %)5

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338

= $ 0+$ 5,573+$ 1,259+ $ 0+$ 0

= $6,832

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5 + CF6

(1+r )6 + CF7

(1+r )7 + CF8

(1+r )8 + CF9

(1+r )9

+ CF10

(1+r )10

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5 + −2500

(1+6 % )6 + 0

(1+6 % )7 +

0

(1+6 %)8 + 10000

(1+7 %)9 + 0

(1+7 %)10

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338+ −2500

1.419 + 0

1.504 + 0

1.594 + 10000

1.838 + 0

1.967

= $ 0+ $ 5,573+$ 1,259+$ 0+$ 0−$ 1,762+$ 0+ $ 0+ $ 5,439+$ 0

= $10,509

Answer to question 3:

The Australian government on 1st September introduced the treasury laws amendment

bill that proposed the reduction of corporate tax rate for all the reporting entities from 30% to

25% (www.ato.gov.au 2018). For larger companies, government would bring into tax cut and

witnessing overtime reduction in rates. Reduction rate in corporate tax rate is done for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

proposing and encouraging investment mainly highly mobile foreign direct investment. This

reduction in taxation rate would help in lowering would help in increasing income for

Australians in the long-run. Such acceleration in investment is done by building more

productive and larger capital stock and generating knowledge spillovers and technology. Not

only higher growth would be encouraged by building a more productive and larger capital

stock, but it will also help in generating higher wages. It was indicated by some views on

taxation of company that the corporate taxation rate should be reduced to 25% with the

timing that is subjected to fiscal and economic circumstances. At the same time, there should

be introduction of making arrangements for charging for the use of non-renewable sources of

energy. It is indicated by the theoretical concepts that lowering the taxation rate would help in

stimulating wages and investments. A large chunk of reduction in taxation rate of company

would be met immediately by increasing the burden through personal income taxation. The

reason is attributable to the fact that lowering Australian corporate taxation rate would

immediately result in lowering franking credits for domestic shareholders that helps in

offsetting their liabilities of personal income taxation (Stewart, 2017).

Nevertheless, the benefits attributable from any reduction in corporate taxation rate of

Australia would largely go to owner of capital and foreign investors resulting from unique

system of dividend imputation of Australia. Australia is one of the few countries having the

unique system of dividend imputation that effectively helps in lowering the taxation rate and

in this regard, local companies operating in country are delivered with franking credits

indicating that if the company is paying higher taxation rate or more amount of tax less

amount then investors would be paying less (Faff, 2015). Dividend imputation is basically a

mechanism that helps in providing some tax payers credits to residents for company tax that

deemed to have been paid on behalf of company. Dividends are attached to the franking

credits are the actual mechanisms for making delivery of tax credits to residents (Davis,

ACCOUNTING AND FINANCE

proposing and encouraging investment mainly highly mobile foreign direct investment. This

reduction in taxation rate would help in lowering would help in increasing income for

Australians in the long-run. Such acceleration in investment is done by building more

productive and larger capital stock and generating knowledge spillovers and technology. Not

only higher growth would be encouraged by building a more productive and larger capital

stock, but it will also help in generating higher wages. It was indicated by some views on

taxation of company that the corporate taxation rate should be reduced to 25% with the

timing that is subjected to fiscal and economic circumstances. At the same time, there should

be introduction of making arrangements for charging for the use of non-renewable sources of

energy. It is indicated by the theoretical concepts that lowering the taxation rate would help in

stimulating wages and investments. A large chunk of reduction in taxation rate of company

would be met immediately by increasing the burden through personal income taxation. The

reason is attributable to the fact that lowering Australian corporate taxation rate would

immediately result in lowering franking credits for domestic shareholders that helps in

offsetting their liabilities of personal income taxation (Stewart, 2017).

Nevertheless, the benefits attributable from any reduction in corporate taxation rate of

Australia would largely go to owner of capital and foreign investors resulting from unique

system of dividend imputation of Australia. Australia is one of the few countries having the

unique system of dividend imputation that effectively helps in lowering the taxation rate and

in this regard, local companies operating in country are delivered with franking credits

indicating that if the company is paying higher taxation rate or more amount of tax less

amount then investors would be paying less (Faff, 2015). Dividend imputation is basically a

mechanism that helps in providing some tax payers credits to residents for company tax that

deemed to have been paid on behalf of company. Dividends are attached to the franking

credits are the actual mechanisms for making delivery of tax credits to residents (Davis,

8

ACCOUNTING AND FINANCE

2016). For the tax residents of Australia, from the perspective of investment, the company

taxation rate is irrelevant. Therefore, the impact of corporate tax rate is quite different

because of system of tax imputation of Australia. For the Australian tax holders, the company

tax rate is effectively a withholding tax as the amount is returned when the dividend payment

is done. Reduction in corporate tax rate would have a direct benefits attributable to foreign

investors and lower rate would attract new foreign investors to Australia. Moreover,

arrangement by other foreign investors to make little payment or no taxation in Australia and

reducing that the statutory rate does not impact them. A lower taxation rate would encourage

investment and investment as potential returns generated would be higher (Loughran &

McDonald, 2016). It is so because in the competitive global market, higher taxation rate

would discourage investment in Australia and thereby dislocating economic activity.

If the corporation tax is highly disproportional, it is indicative of the fact that there

will be lower business creation and fewer jobs. Amount of lower investment in capital would

mean lower productivity and income for workers. For consumers, lower taxation rate would

mean lower price and higher amount of product and services. Over the subsequent years,

lower corporate taxation rate is correlated with skyrocketing revenue and revenue of

government will also increase due to reduction in corporate tax rate of company (Adler &

Stringer, 2016).

Answer to Question 4:

Requirement i:

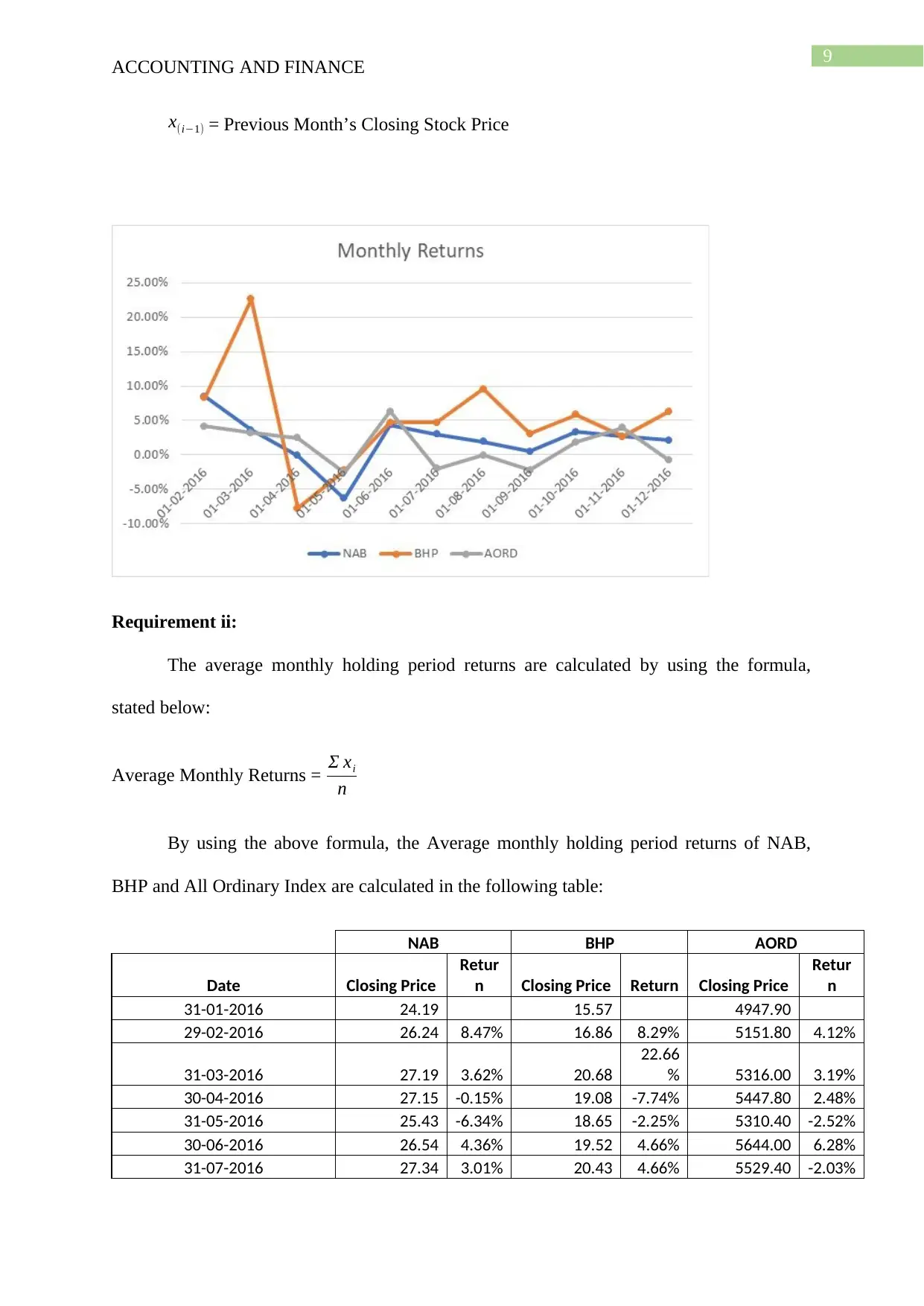

The monthly holding period returns are calculated by using the formula, stated below:

Ri = xi−x(i−1)

x(i−1)

Where, xi = Current Month’s Closing Stock Price

ACCOUNTING AND FINANCE

2016). For the tax residents of Australia, from the perspective of investment, the company

taxation rate is irrelevant. Therefore, the impact of corporate tax rate is quite different

because of system of tax imputation of Australia. For the Australian tax holders, the company

tax rate is effectively a withholding tax as the amount is returned when the dividend payment

is done. Reduction in corporate tax rate would have a direct benefits attributable to foreign

investors and lower rate would attract new foreign investors to Australia. Moreover,

arrangement by other foreign investors to make little payment or no taxation in Australia and

reducing that the statutory rate does not impact them. A lower taxation rate would encourage

investment and investment as potential returns generated would be higher (Loughran &

McDonald, 2016). It is so because in the competitive global market, higher taxation rate

would discourage investment in Australia and thereby dislocating economic activity.

If the corporation tax is highly disproportional, it is indicative of the fact that there

will be lower business creation and fewer jobs. Amount of lower investment in capital would

mean lower productivity and income for workers. For consumers, lower taxation rate would

mean lower price and higher amount of product and services. Over the subsequent years,

lower corporate taxation rate is correlated with skyrocketing revenue and revenue of

government will also increase due to reduction in corporate tax rate of company (Adler &

Stringer, 2016).

Answer to Question 4:

Requirement i:

The monthly holding period returns are calculated by using the formula, stated below:

Ri = xi−x(i−1)

x(i−1)

Where, xi = Current Month’s Closing Stock Price

9

ACCOUNTING AND FINANCE

x(i−1) = Previous Month’s Closing Stock Price

Requirement ii:

The average monthly holding period returns are calculated by using the formula,

stated below:

Average Monthly Returns = Σ xi

n

By using the above formula, the Average monthly holding period returns of NAB,

BHP and All Ordinary Index are calculated in the following table:

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

ACCOUNTING AND FINANCE

x(i−1) = Previous Month’s Closing Stock Price

Requirement ii:

The average monthly holding period returns are calculated by using the formula,

stated below:

Average Monthly Returns = Σ xi

n

By using the above formula, the Average monthly holding period returns of NAB,

BHP and All Ordinary Index are calculated in the following table:

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ACCOUNTING AND FINANCE

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return 2.14% 5.24% 1.29%

Requirement iii:

The formula of annual holding period return, used in the following table is as follows:

Annual Holding Period Returns = ( ri

rt

)

1

12 – 1

Where, ri = Monthly Return of Last month

rt = Monthly Return of First month

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period

Return 1.90% 4.58% 1.15%

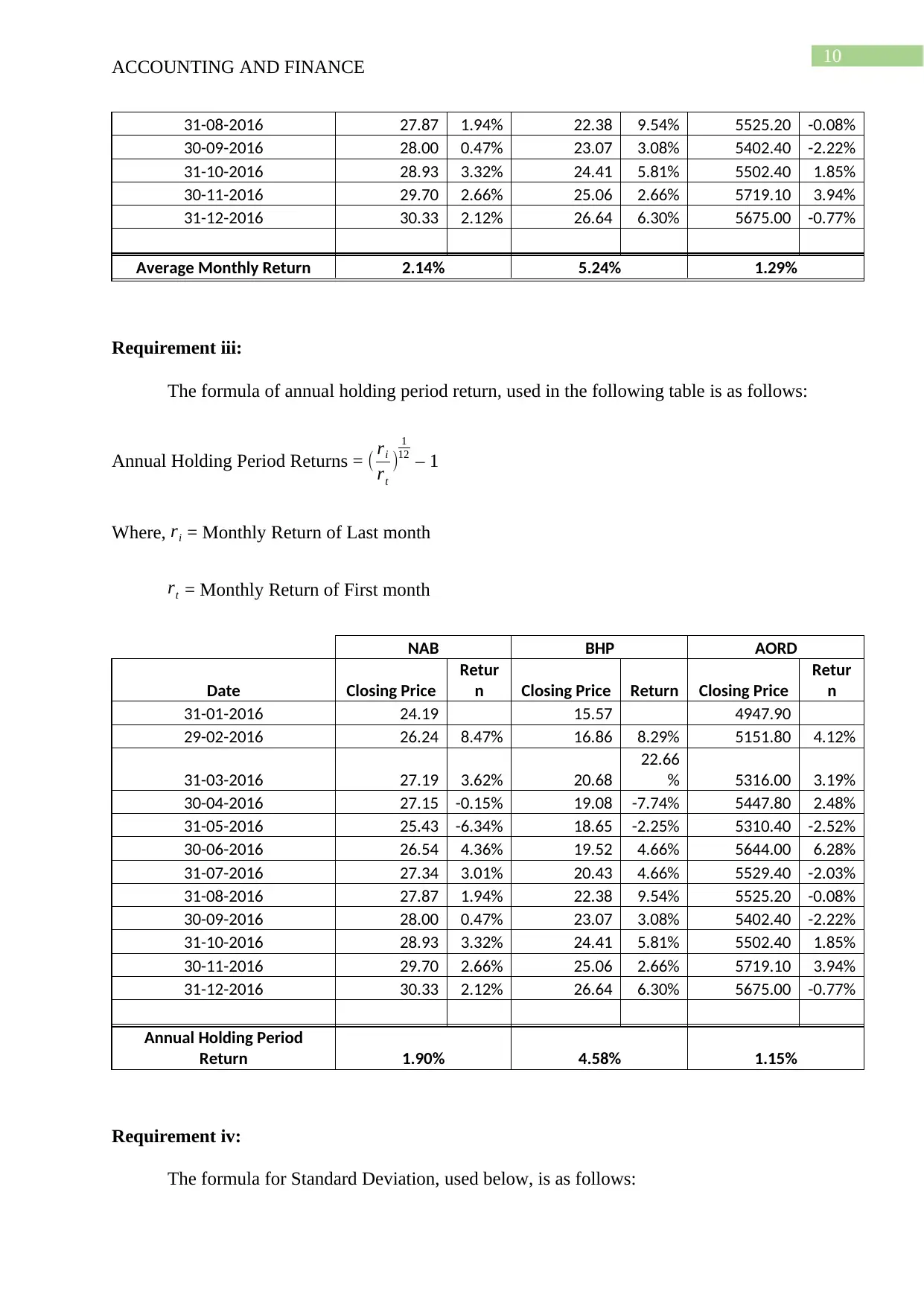

Requirement iv:

The formula for Standard Deviation, used below, is as follows:

ACCOUNTING AND FINANCE

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return 2.14% 5.24% 1.29%

Requirement iii:

The formula of annual holding period return, used in the following table is as follows:

Annual Holding Period Returns = ( ri

rt

)

1

12 – 1

Where, ri = Monthly Return of Last month

rt = Monthly Return of First month

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period

Return 1.90% 4.58% 1.15%

Requirement iv:

The formula for Standard Deviation, used below, is as follows:

11

ACCOUNTING AND FINANCE

S = √ Σ¿ ¿ ¿

Where, ri= Monthly Returns

r = Average Monthly returns

n= Nos. of Monthly Returns

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation 3.60% 7.54% 2.99%

ACCOUNTING AND FINANCE

S = √ Σ¿ ¿ ¿

Where, ri= Monthly Returns

r = Average Monthly returns

n= Nos. of Monthly Returns

NAB BHP AORD

Date Closing Price

Retur

n Closing Price Return Closing Price

Retur

n

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68

22.66

% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation 3.60% 7.54% 2.99%

12

ACCOUNTING AND FINANCE

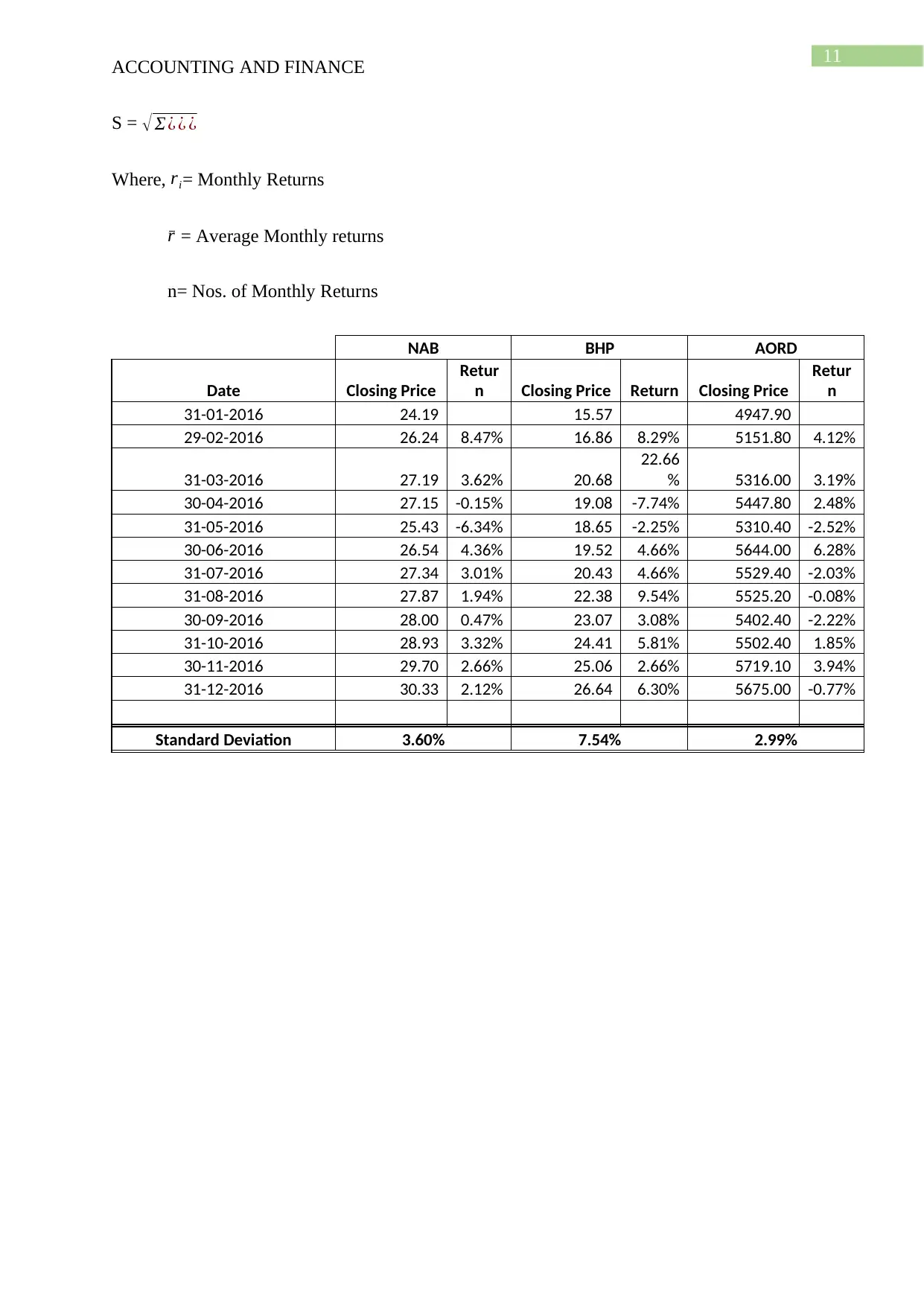

Requirement v:

Requirement vi:

The CAPM Formula for Expected Return is as follows:

Er = rf + (β x rmp)

Where, rf = Risk Free Rate

β= Beta

rmp = Market Risk Premium

NAB BHP

Beta 1.23 0.9

Risk Free Rate 2.95% 2.95%

Market Return 6.50% 6.50%

Expected Return 7.32% 6.15%

ACCOUNTING AND FINANCE

Requirement v:

Requirement vi:

The CAPM Formula for Expected Return is as follows:

Er = rf + (β x rmp)

Where, rf = Risk Free Rate

β= Beta

rmp = Market Risk Premium

NAB BHP

Beta 1.23 0.9

Risk Free Rate 2.95% 2.95%

Market Return 6.50% 6.50%

Expected Return 7.32% 6.15%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

ACCOUNTING AND FINANCE

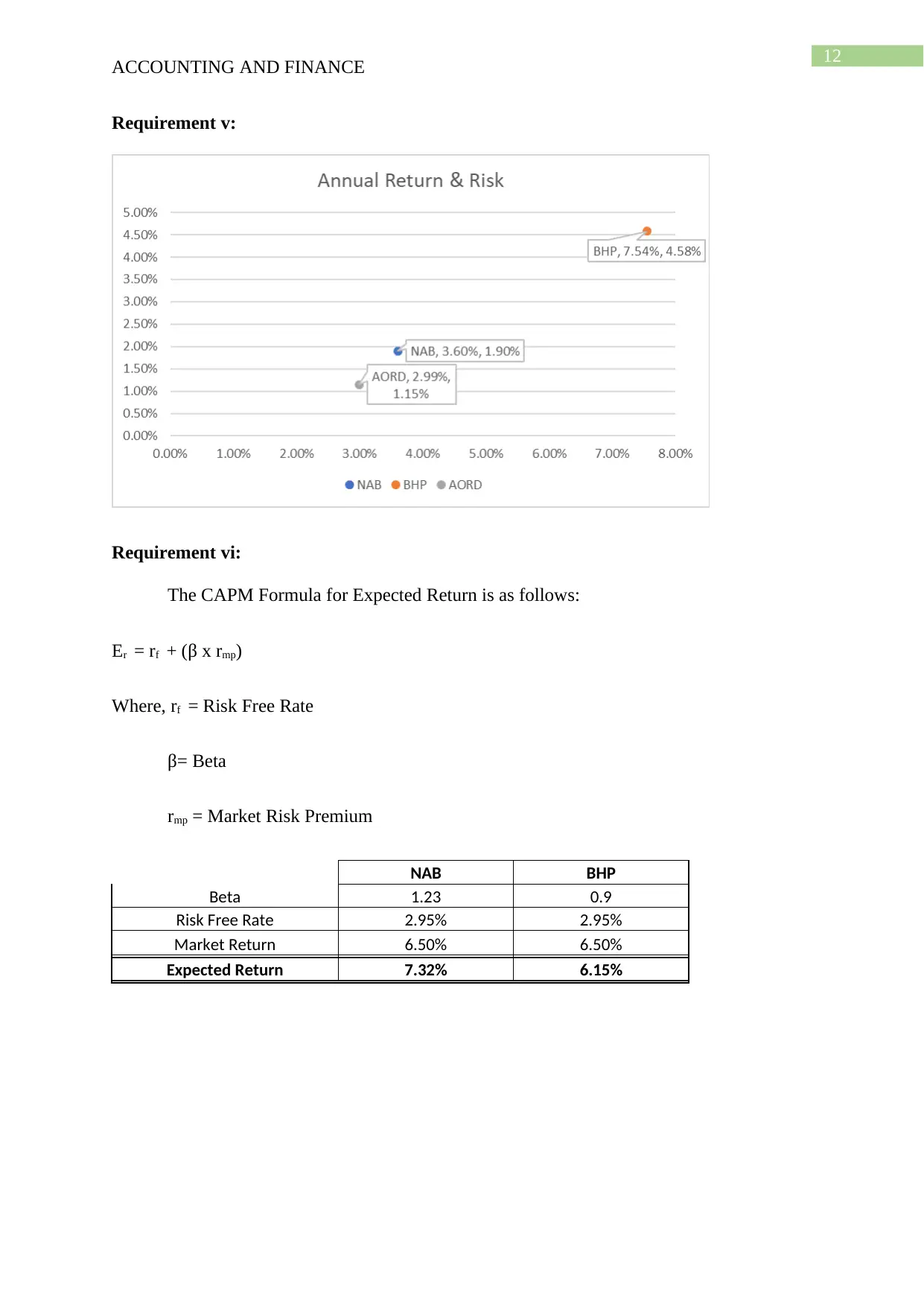

Requirement vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Security Market Line

Series2 NAB BHP

Requirement viii:

The formula of Portfolio Return & Portfolio Beta are given below:

Pr = (w1 x r1) + (w2 x r2)

βp = (w1 x β1) + (w2 x β2)

Where, w1 = Weightage of NAB

w2 = Weightage of BHP

r1 = Average Monthly Return of NAB

r2 = Average Monthly Return of BHP

β1 = Beta of NAB

β2 = Beta of BHP

NAB BHP

Beta 1.23 0.9

Portfolio Weightage 30% 70%

Portfolio Return 4.312%

Portfolio Beta 1.00

ACCOUNTING AND FINANCE

Requirement vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Security Market Line

Series2 NAB BHP

Requirement viii:

The formula of Portfolio Return & Portfolio Beta are given below:

Pr = (w1 x r1) + (w2 x r2)

βp = (w1 x β1) + (w2 x β2)

Where, w1 = Weightage of NAB

w2 = Weightage of BHP

r1 = Average Monthly Return of NAB

r2 = Average Monthly Return of BHP

β1 = Beta of NAB

β2 = Beta of BHP

NAB BHP

Beta 1.23 0.9

Portfolio Weightage 30% 70%

Portfolio Return 4.312%

Portfolio Beta 1.00

14

ACCOUNTING AND FINANCE

Requirement ix:

Based on analysis of CAPM and SML, the portfolio of assets in which the investor

would be making investment is in the shares of BHP Billiton and shares of NAB (Beaumont,

2015) It can be seen from the computation that return generated by the portfolio would be

4.312% with value of portfolio beta is 1. However, the average return generated by shares of

BHP is more than that of BHP Billiton Limited. On other hand, the deviation of return

generated from the shares of BHP Billiton is more than that of NAB. Therefore, returns

generated by individual stocks has its own risks and returns and making a portfolio of both

the assets would lead to generation of average monthly return of 1.29% and with annual

holding period of 1.15% and variation of 2.29%.

ACCOUNTING AND FINANCE

Requirement ix:

Based on analysis of CAPM and SML, the portfolio of assets in which the investor

would be making investment is in the shares of BHP Billiton and shares of NAB (Beaumont,

2015) It can be seen from the computation that return generated by the portfolio would be

4.312% with value of portfolio beta is 1. However, the average return generated by shares of

BHP is more than that of BHP Billiton Limited. On other hand, the deviation of return

generated from the shares of BHP Billiton is more than that of NAB. Therefore, returns

generated by individual stocks has its own risks and returns and making a portfolio of both

the assets would lead to generation of average monthly return of 1.29% and with annual

holding period of 1.15% and variation of 2.29%.

15

ACCOUNTING AND FINANCE

References list:

Adler, R., & Stringer, C. (2016). Practitioner mentoring of undergraduate accounting

students: helping prepare students to become accounting professionals. Accounting &

Finance.

Balachandran, B., Henry, D., & Vidanapathirana, B. (2016). Long-Term Price Reaction to

Dividend Reduction in an Imputation Environment–Evidence from Australia.

Balachandran, B., Khan, A., Mather, P., & Theobald, M. (2017). Insider ownership and

dividend policy in an imputation tax environment. Journal of Corporate Finance.

Baykov, A., & Pavuk, O. (2017). Financial Market in the Context of Globalization:

Experience of Economic and Legal Analysis. Accounting and Finance, (1), 120-131.

Beaumont, S. J. (2015). An investigation of the short‐and long‐run relations between

executive cash bonus payments and firm financial performance: a pitch. Accounting

& Finance, 55(2), 337-343.

Davis, K. (2016). DIVIDEND IMPUTATION and the Australian financial system.

Faff, R. W. (2015). A simple template for pitching research. Accounting & Finance, 55(2),

311-336.

Loughran, T., & McDonald, B. (2016). Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), 1187-1230.

Loughran, T., & McDonald, B. (2016). Textual analysis in accounting and finance: A survey.

Journal of Accounting Research, 54(4), 1187-1230.

Ratiu, R. V. (2015). Financial reporting of European banks during the GFC: a pitch.

Accounting & Finance, 55(2), 345-352.

ACCOUNTING AND FINANCE

References list:

Adler, R., & Stringer, C. (2016). Practitioner mentoring of undergraduate accounting

students: helping prepare students to become accounting professionals. Accounting &

Finance.

Balachandran, B., Henry, D., & Vidanapathirana, B. (2016). Long-Term Price Reaction to

Dividend Reduction in an Imputation Environment–Evidence from Australia.

Balachandran, B., Khan, A., Mather, P., & Theobald, M. (2017). Insider ownership and

dividend policy in an imputation tax environment. Journal of Corporate Finance.

Baykov, A., & Pavuk, O. (2017). Financial Market in the Context of Globalization:

Experience of Economic and Legal Analysis. Accounting and Finance, (1), 120-131.

Beaumont, S. J. (2015). An investigation of the short‐and long‐run relations between

executive cash bonus payments and firm financial performance: a pitch. Accounting

& Finance, 55(2), 337-343.

Davis, K. (2016). DIVIDEND IMPUTATION and the Australian financial system.

Faff, R. W. (2015). A simple template for pitching research. Accounting & Finance, 55(2),

311-336.

Loughran, T., & McDonald, B. (2016). Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), 1187-1230.

Loughran, T., & McDonald, B. (2016). Textual analysis in accounting and finance: A survey.

Journal of Accounting Research, 54(4), 1187-1230.

Ratiu, R. V. (2015). Financial reporting of European banks during the GFC: a pitch.

Accounting & Finance, 55(2), 345-352.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

ACCOUNTING AND FINANCE

Reducing the corporate tax rate. (2018). Ato.gov.au. Retrieved 2 April 2018, from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-

for-businesses/Reducing-the-corporate-tax-rate/

Scholes, M. S. (2015). Taxes and business strategy. Prentice Hall.

Stewart, M. (2017). Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41).

Springer, Cham.

Taxpolicy.crawford.anu.edu.au. (2018). Retrieved 2 April 2018, from

https://taxpolicy.crawford.anu.edu.au/sites/default/files/events/attachments/2017-07/

li_and_tran_day_two_25_july_2017.pdf

Unda, L. A. (2015). Board of directors characteristics and credit union financial performance:

a pitch. Accounting & Finance, 55(2), 353-360.

ACCOUNTING AND FINANCE

Reducing the corporate tax rate. (2018). Ato.gov.au. Retrieved 2 April 2018, from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-

for-businesses/Reducing-the-corporate-tax-rate/

Scholes, M. S. (2015). Taxes and business strategy. Prentice Hall.

Stewart, M. (2017). Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41).

Springer, Cham.

Taxpolicy.crawford.anu.edu.au. (2018). Retrieved 2 April 2018, from

https://taxpolicy.crawford.anu.edu.au/sites/default/files/events/attachments/2017-07/

li_and_tran_day_two_25_july_2017.pdf

Unda, L. A. (2015). Board of directors characteristics and credit union financial performance:

a pitch. Accounting & Finance, 55(2), 353-360.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.