Ratio Analysis, Budgeting & Financial Decision Making: A Report

VerifiedAdded on 2023/06/10

ACCOUNTING &

FINANCE

1

Paraphrase This Document

Accounting and finance is crucial for making the strategic decision. Financial

ratio is considered to be the metrics that allow the investors and other stakeholders to

analyse the financial performance of the organisation. Budgeting is a very important

factor for any organization to be able to plan the financial activities. The different

between the management accounting and financial accounting is that management

accounting is helpful for the organisation and its competitors for the analysation of

trends and performance whereas, financial accounting is requirement of the

organisation for meeting the corporate governance. The current study has involved

calculation of project A & B by involving NPV and payback period method of capital

budgeting which is depicting that project A is beneficial.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION..........................................................................................................................4

MAIN BODY..................................................................................................................................4

SECTION A...................................................................................................................................4

Profitability Ratios................................................................................................................4

Efficiency ratios.....................................................................................................................6

Liquidity Ratios......................................................................................................................8

Investment ratios...............................................................................................................10

Financial Structure ratios................................................................................................11

SECTION B.................................................................................................................................13

Analysing objectives of budgeting for Manor Ltd...................................................13

Differences between financial and management accounting...........................13

3................................................................................................................................................14

a) Payback Period for the projects A & B..................................................................14

b) calculating the Net Present Value for the projects A & B..............................15

c) Explaining reason for selecting the project.........................................................16

CONCLUSION............................................................................................................................17

REFERENCES............................................................................................................................18

4

Paraphrase This Document

Account and finance are the crucial for gaining the relevant

information regarding the prevailing performance in the monetary terms

that provides assistance in making strategic decision. In the current era, it

is important for the organization to pay attention on having the h relevant

practice of accounting & finance in turn accomplishing the organizational

objective of higher strategic decision by considering all crucial aspects to

get competitiveness. The current report will focus on presenting the

calculation of different ratios so that significant insights about Trust plc

performance can be derived. Present report will emphasize on analysing the

objectives of budgeting to Manor LTD, differentiation between financial &

management accounting can be evaluated. This will focus on calculating

payback period and NPV for choosing which project is best.

MAIN BODY

SECTION A

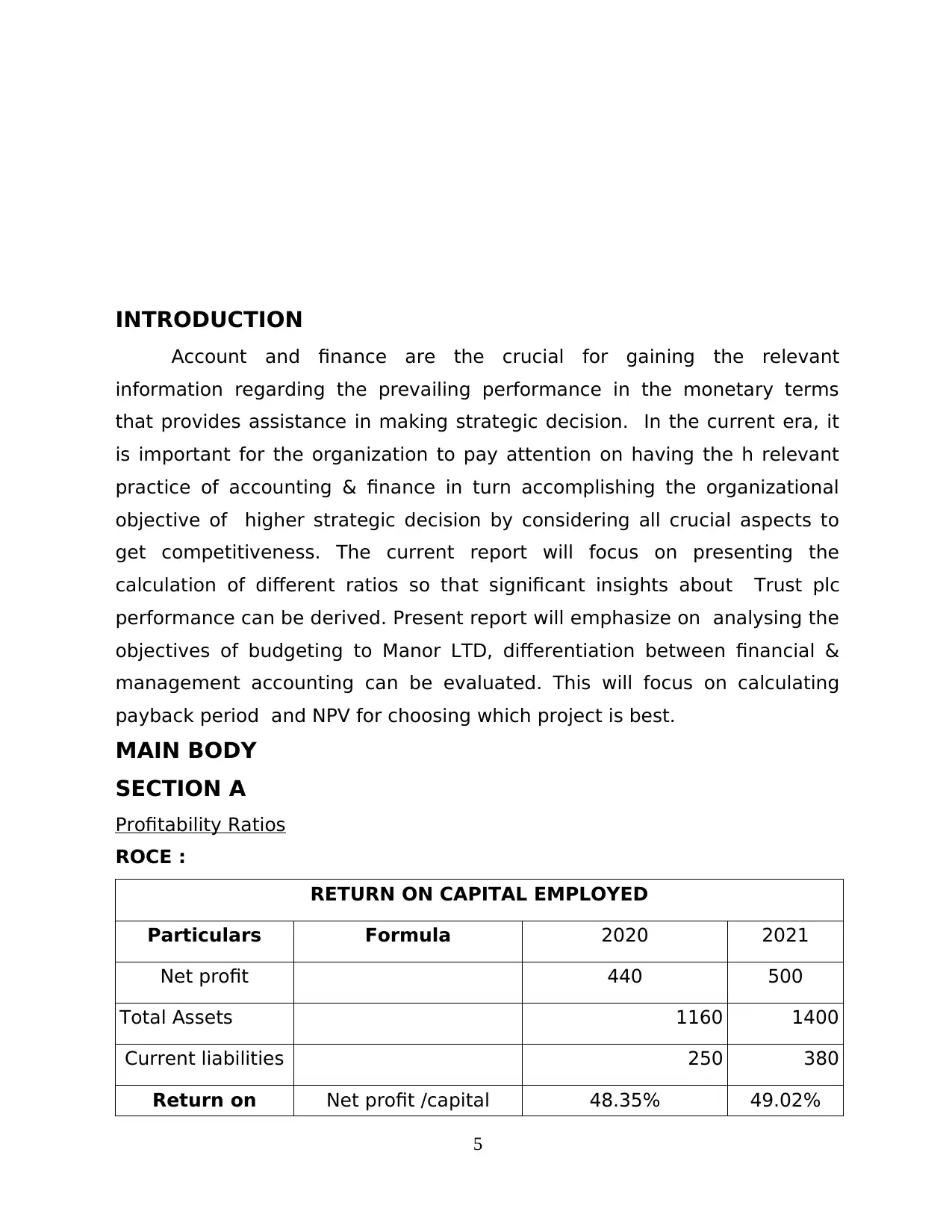

Profitability Ratios

ROCE :

RETURN ON CAPITAL EMPLOYED

Particulars Formula 2020 2021

Net profit 440 500

Total Assets 1160 1400

Current liabilities 250 380

Return on Net profit /capital 48.35% 49.02%

5

employed employed * 100

Return on capital employed is the financial ratio which is utilized for

the assessment of the company's profitability and the capital efficiency

(Rashid, 2018). It can also be said that this ratio is helpful for understanding

how well the company is able to generate profit from the use of its capital.

The calculation shows that the ROCE ratio for this organization has improved

slightly in comparison to that of 2020 in 2021. This indicates the increase in

the capabilities of the organization for utilization of its assets effectively.

This is the financial metric that indicates the growth of the organization and

helps it to attract more investors in order to gain competitive advantage. In

order improve this ratio this organization would need to increase its profit by

enhanced sales.

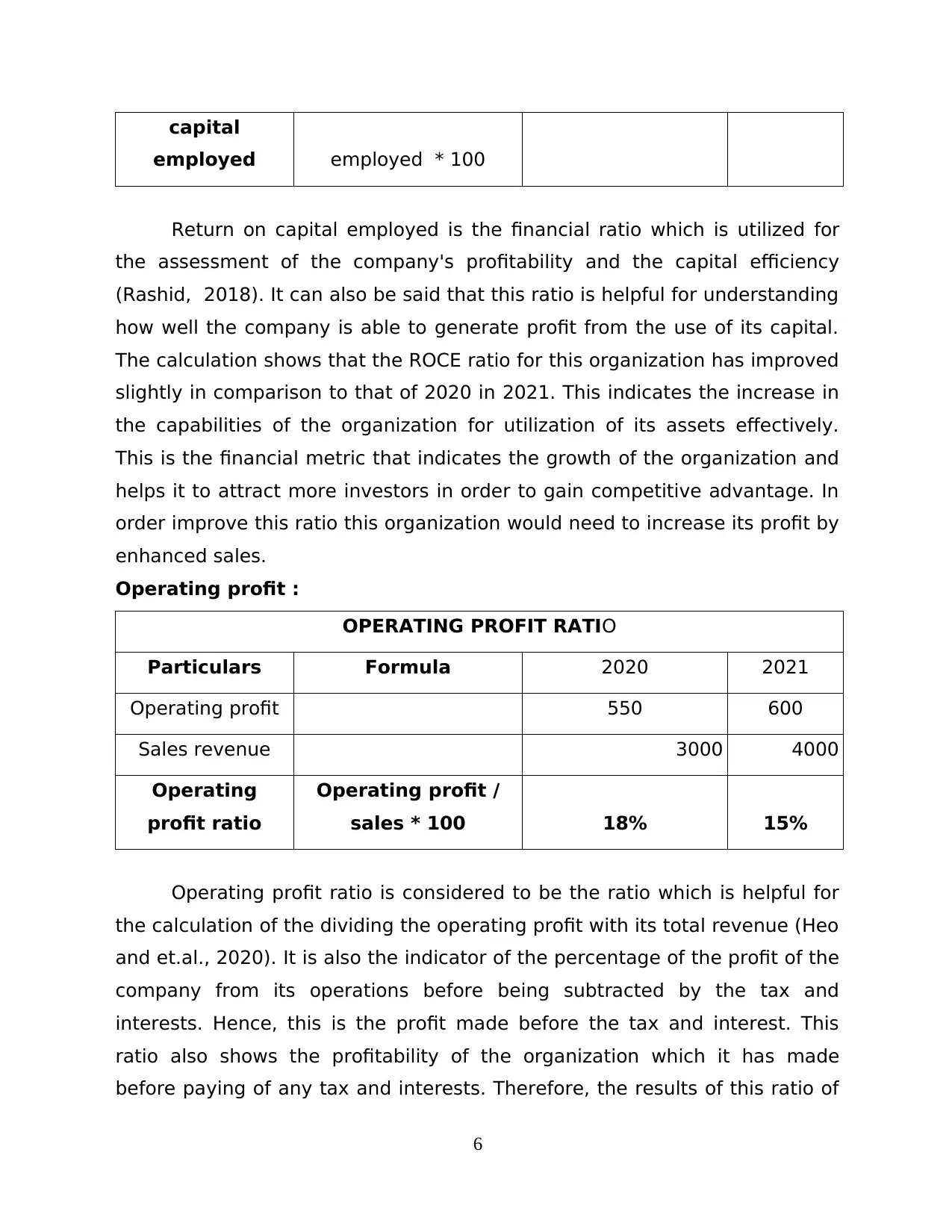

Operating profit :

OPERATING PROFIT RATIO

Particulars Formula 2020 2021

Operating profit 550 600

Sales revenue 3000 4000

Operating

profit ratio

Operating profit /

sales * 100 18% 15%

Operating profit ratio is considered to be the ratio which is helpful for

the calculation of the dividing the operating profit with its total revenue (Heo

and et.al., 2020). It is also the indicator of the percentage of the profit of the

company from its operations before being subtracted by the tax and

interests. Hence, this is the profit made before the tax and interest. This

ratio also shows the profitability of the organization which it has made

before paying of any tax and interests. Therefore, the results of this ratio of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

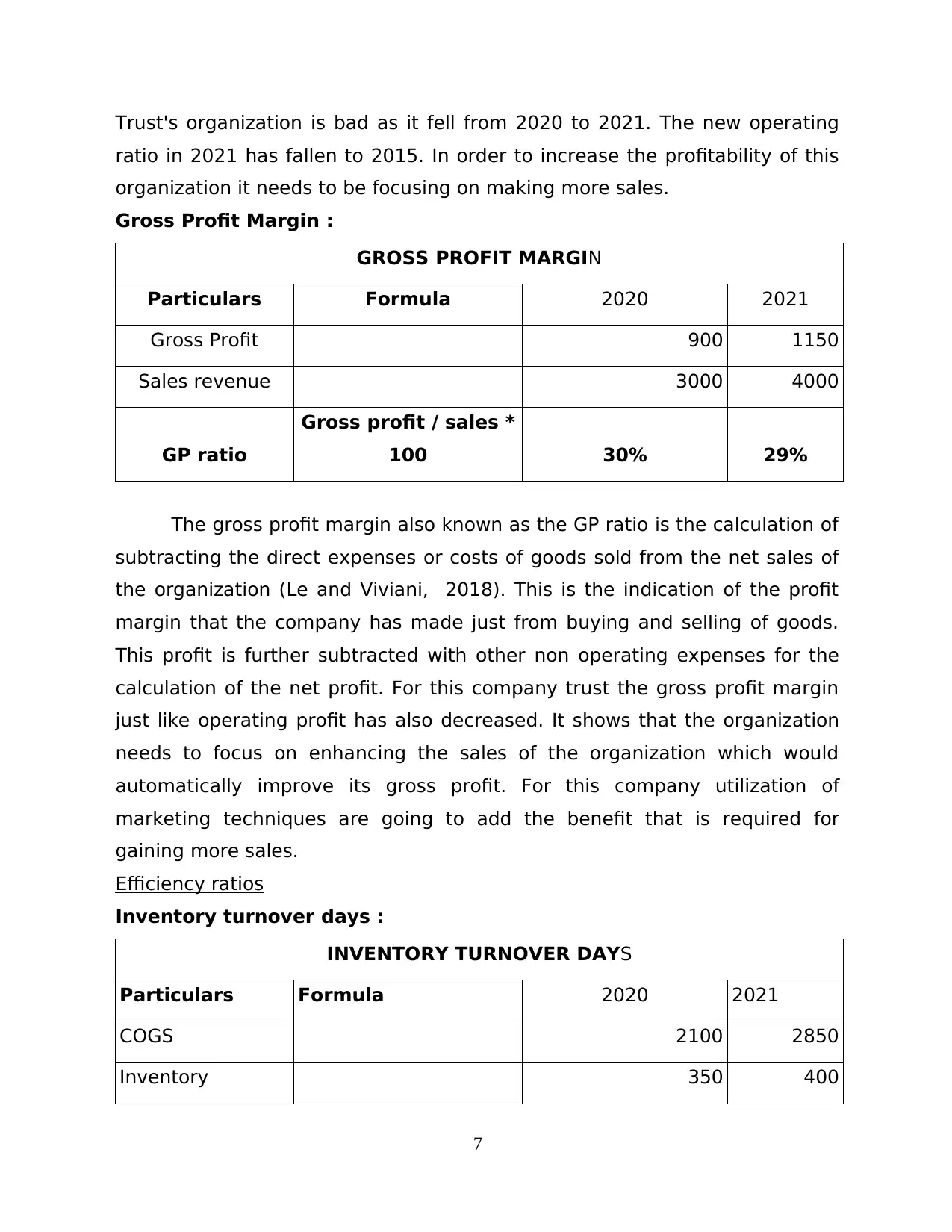

ratio in 2021 has fallen to 2015. In order to increase the profitability of this

organization it needs to be focusing on making more sales.

Gross Profit Margin :

GROSS PROFIT MARGIN

Particulars Formula 2020 2021

Gross Profit 900 1150

Sales revenue 3000 4000

GP ratio

Gross profit / sales *

100 30% 29%

The gross profit margin also known as the GP ratio is the calculation of

subtracting the direct expenses or costs of goods sold from the net sales of

the organization (Le and Viviani, 2018). This is the indication of the profit

margin that the company has made just from buying and selling of goods.

This profit is further subtracted with other non operating expenses for the

calculation of the net profit. For this company trust the gross profit margin

just like operating profit has also decreased. It shows that the organization

needs to focus on enhancing the sales of the organization which would

automatically improve its gross profit. For this company utilization of

marketing techniques are going to add the benefit that is required for

gaining more sales.

Efficiency ratios

Inventory turnover days :

INVENTORY TURNOVER DAYS

Particulars Formula 2020 2021

COGS 2100 2850

Inventory 350 400

7

Paraphrase This Document

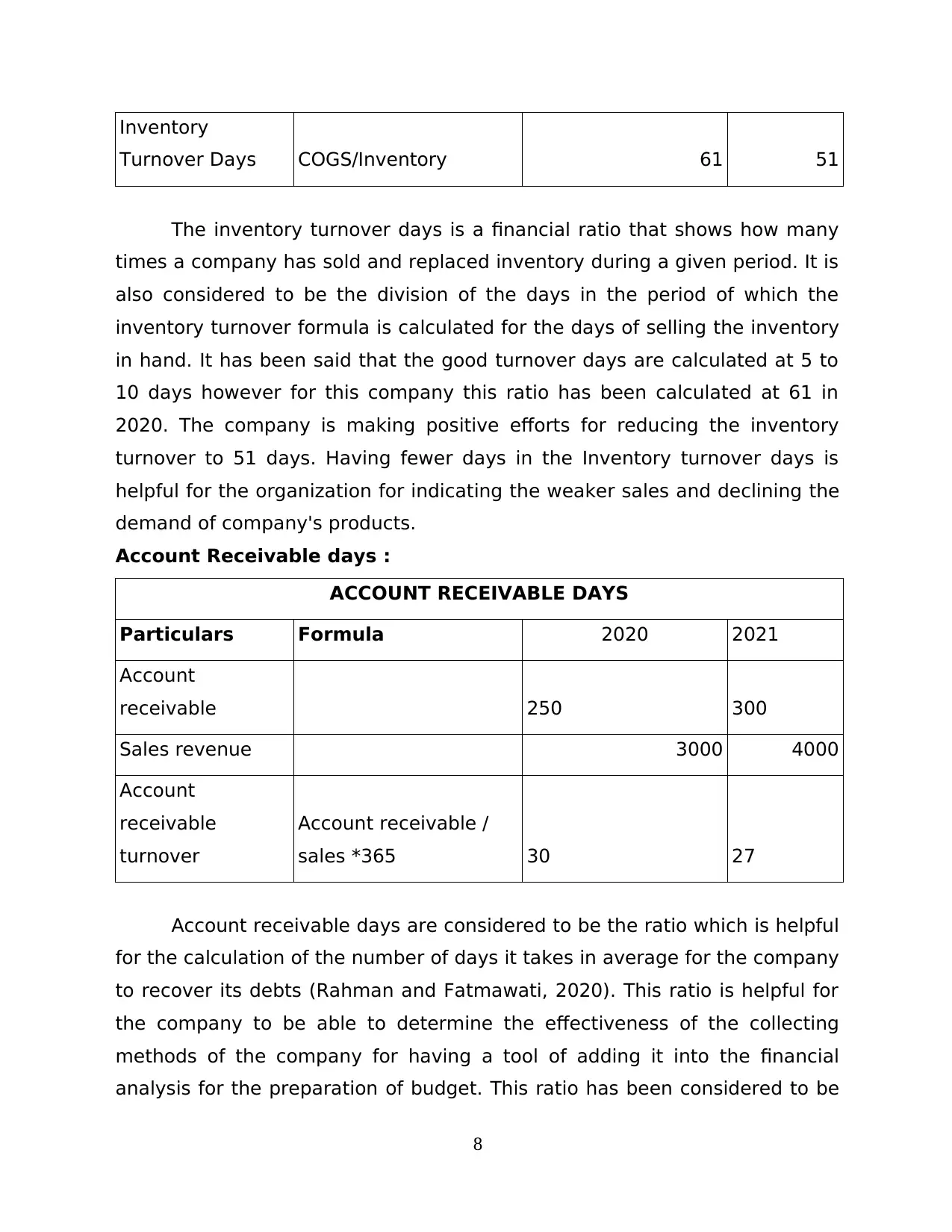

Turnover Days COGS/Inventory 61 51

The inventory turnover days is a financial ratio that shows how many

times a company has sold and replaced inventory during a given period. It is

also considered to be the division of the days in the period of which the

inventory turnover formula is calculated for the days of selling the inventory

in hand. It has been said that the good turnover days are calculated at 5 to

10 days however for this company this ratio has been calculated at 61 in

2020. The company is making positive efforts for reducing the inventory

turnover to 51 days. Having fewer days in the Inventory turnover days is

helpful for the organization for indicating the weaker sales and declining the

demand of company's products.

Account Receivable days :

ACCOUNT RECEIVABLE DAYS

Particulars Formula 2020 2021

Account

receivable 250 300

Sales revenue 3000 4000

Account

receivable

turnover

Account receivable /

sales *365 30 27

Account receivable days are considered to be the ratio which is helpful

for the calculation of the number of days it takes in average for the company

to recover its debts (Rahman and Fatmawati, 2020). This ratio is helpful for

the company to be able to determine the effectiveness of the collecting

methods of the company for having a tool of adding it into the financial

analysis for the preparation of budget. This ratio has been considered to be

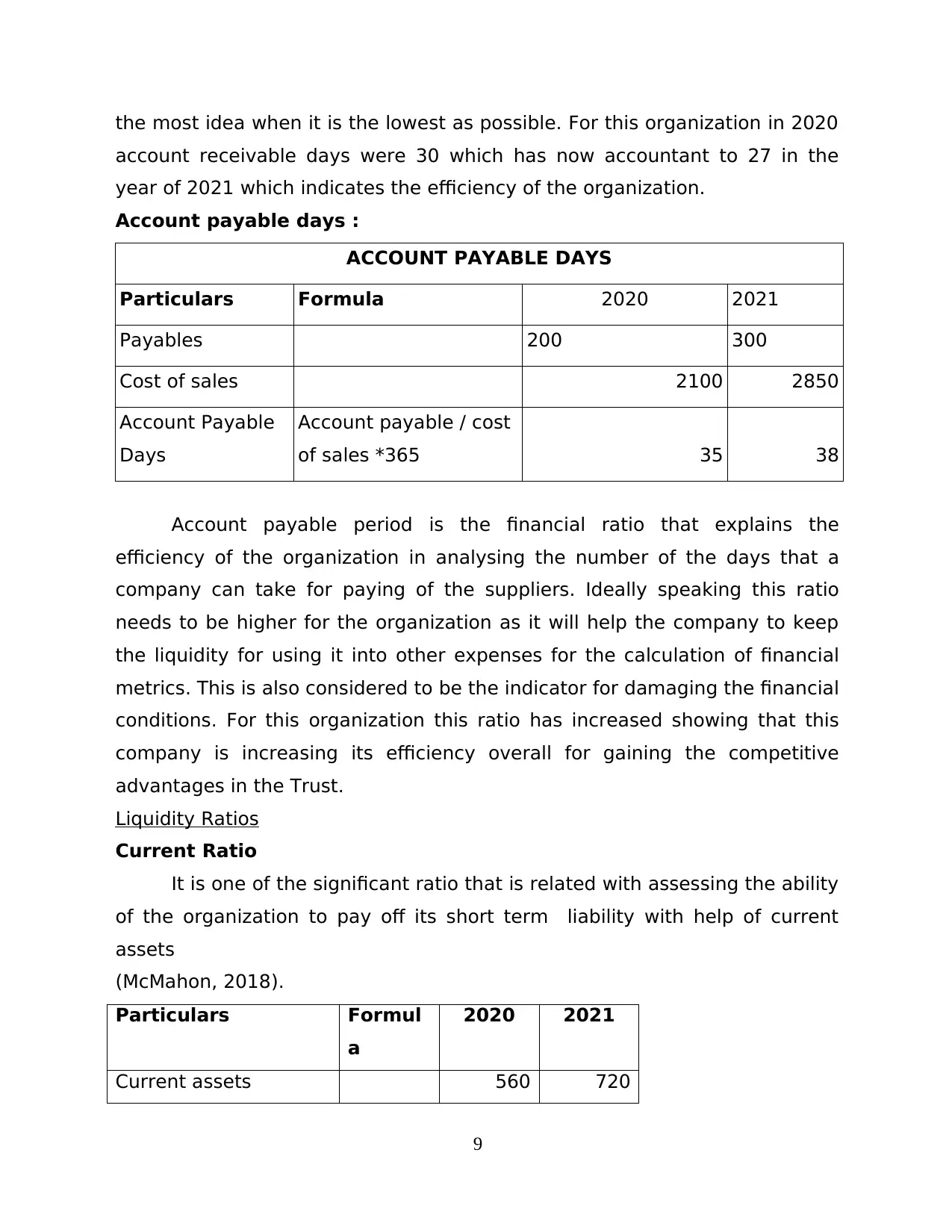

8

account receivable days were 30 which has now accountant to 27 in the

year of 2021 which indicates the efficiency of the organization.

Account payable days :

ACCOUNT PAYABLE DAYS

Particulars Formula 2020 2021

Payables 200 300

Cost of sales 2100 2850

Account Payable

Days

Account payable / cost

of sales *365 35 38

Account payable period is the financial ratio that explains the

efficiency of the organization in analysing the number of the days that a

company can take for paying of the suppliers. Ideally speaking this ratio

needs to be higher for the organization as it will help the company to keep

the liquidity for using it into other expenses for the calculation of financial

metrics. This is also considered to be the indicator for damaging the financial

conditions. For this organization this ratio has increased showing that this

company is increasing its efficiency overall for gaining the competitive

advantages in the Trust.

Liquidity Ratios

Current Ratio

It is one of the significant ratio that is related with assessing the ability

of the organization to pay off its short term liability with help of current

assets

(McMahon, 2018).

Particulars Formul

a

2020 2021

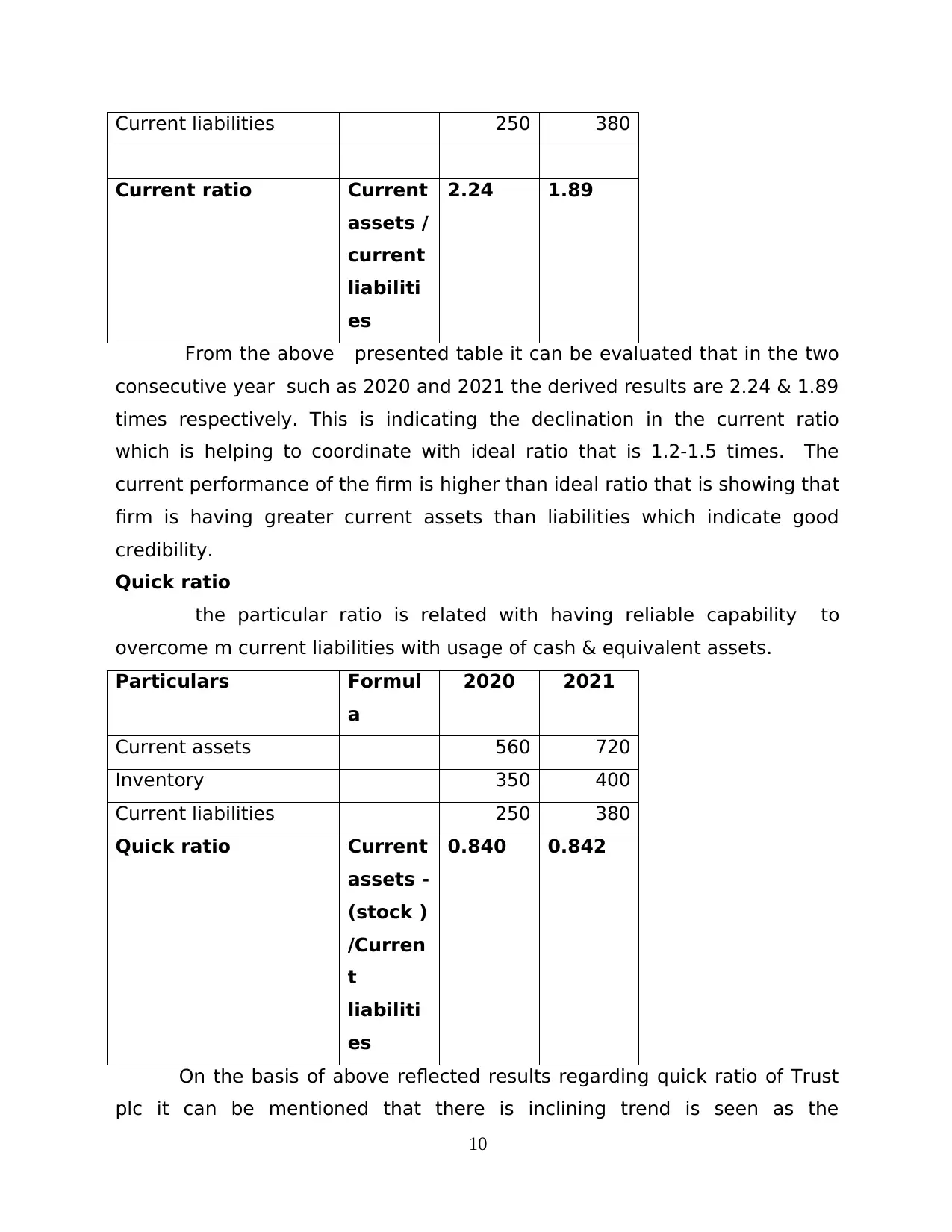

Current assets 560 720

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio Current

assets /

current

liabiliti

es

2.24 1.89

From the above presented table it can be evaluated that in the two

consecutive year such as 2020 and 2021 the derived results are 2.24 & 1.89

times respectively. This is indicating the declination in the current ratio

which is helping to coordinate with ideal ratio that is 1.2-1.5 times. The

current performance of the firm is higher than ideal ratio that is showing that

firm is having greater current assets than liabilities which indicate good

credibility.

Quick ratio

the particular ratio is related with having reliable capability to

overcome m current liabilities with usage of cash & equivalent assets.

Particulars Formul

a

2020 2021

Current assets 560 720

Inventory 350 400

Current liabilities 250 380

Quick ratio Current

assets -

(stock )

/Curren

t

liabiliti

es

0.840 0.842

On the basis of above reflected results regarding quick ratio of Trust

plc it can be mentioned that there is inclining trend is seen as the

10

Paraphrase This Document

current year firm ha improved its performance as compared to year 2020

but lower than ideal ratio that is 1 times. This reflects poor performance of

the company that is required be improved. The firm should pay attention on

taking actions like better strategic planning, inclined sales & inventory

turnover so that improve outcomes can be derived. There are different

types of the stakeholders such as lenders, e creditors, etc that pay attention

on this ratio for making decision so making modification can help in

achieving significant outcome.

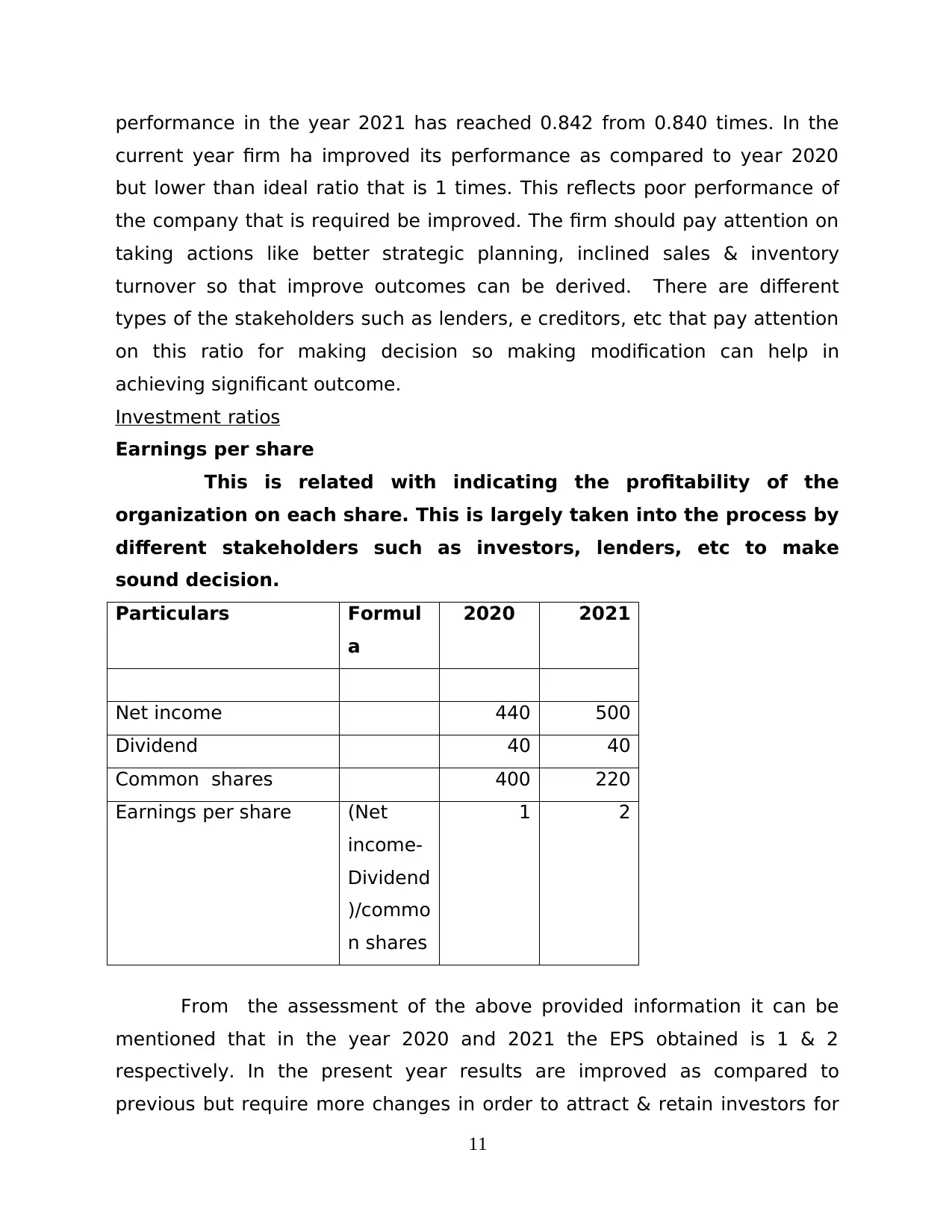

Investment ratios

Earnings per share

This is related with indicating the profitability of the

organization on each share. This is largely taken into the process by

different stakeholders such as investors, lenders, etc to make

sound decision.

Particulars Formul

a

2020 2021

Net income 440 500

Dividend 40 40

Common shares 400 220

Earnings per share (Net

income-

Dividend

)/commo

n shares

1 2

From the assessment of the above provided information it can be

mentioned that in the year 2020 and 2021 the EPS obtained is 1 & 2

respectively. In the present year results are improved as compared to

previous but require more changes in order to attract & retain investors for

11

mentioned that higher earning per share is helpful in gaining the reliable

outcomes so that achieving stable position in sector for maintaining

competitiveness can be derived.

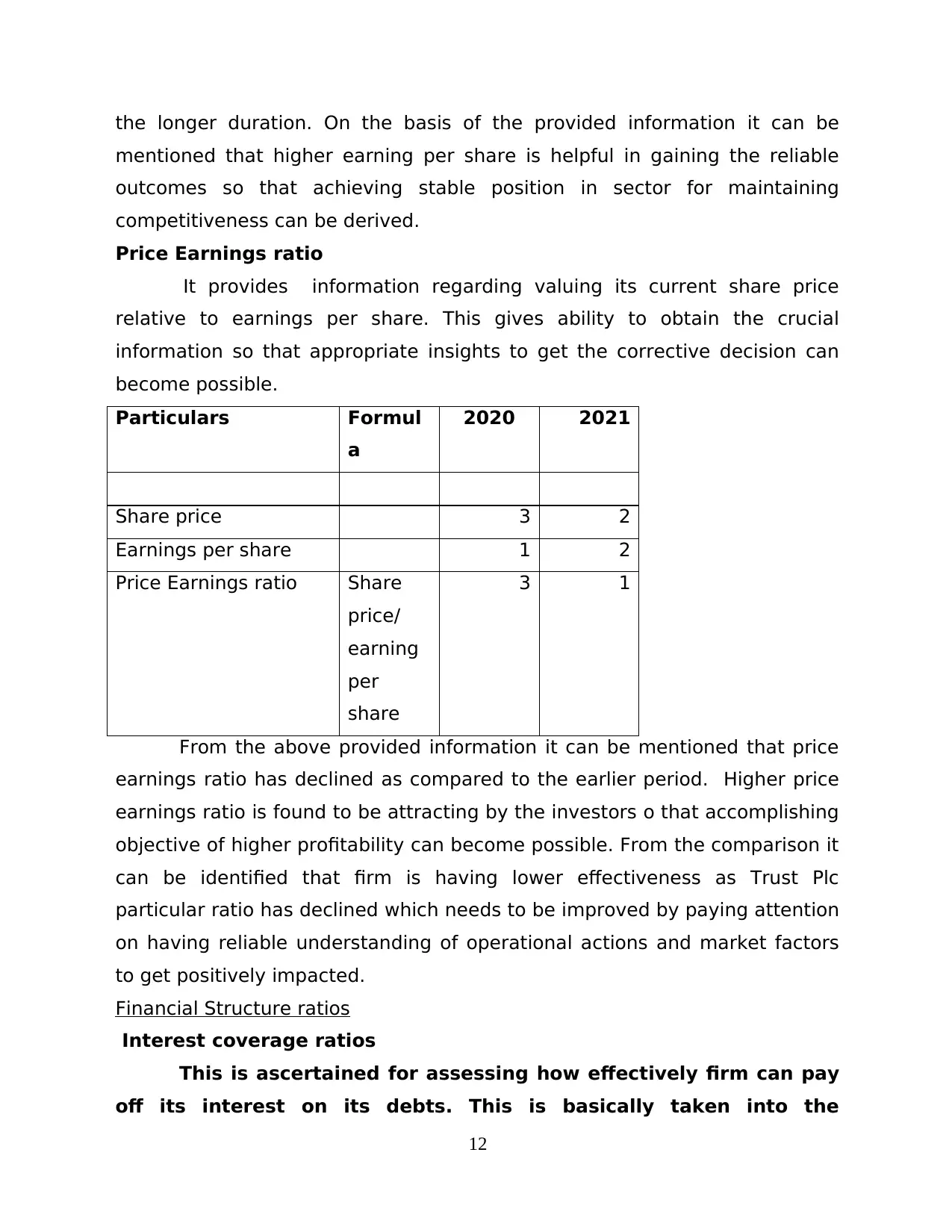

Price Earnings ratio

It provides information regarding valuing its current share price

relative to earnings per share. This gives ability to obtain the crucial

information so that appropriate insights to get the corrective decision can

become possible.

Particulars Formul

a

2020 2021

Share price 3 2

Earnings per share 1 2

Price Earnings ratio Share

price/

earning

per

share

3 1

From the above provided information it can be mentioned that price

earnings ratio has declined as compared to the earlier period. Higher price

earnings ratio is found to be attracting by the investors o that accomplishing

objective of higher profitability can become possible. From the comparison it

can be identified that firm is having lower effectiveness as Trust Plc

particular ratio has declined which needs to be improved by paying attention

on having reliable understanding of operational actions and market factors

to get positively impacted.

Financial Structure ratios

Interest coverage ratios

This is ascertained for assessing how effectively firm can pay

off its interest on its debts. This is basically taken into the

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assessment of firm (Mudzakar, 2021).

Particulars Formul

a

2020 2021

EBIT 550 600

Interest 50 60

Interest coverage

ratios

EBIT/

interest

11 10

From the evaluation of the above provided information it can be

mentioned that interest coverage ratio for the two consecutive period such

as 2020 and 2021 includes 11 & 10 times. This is presenting declination in

the current outcome as compared to the previous which is presenting lower

operating profit that is required to be improved by taking crucial actions.

This is helpful in gaining the information that its ability has declined as

compared to previous which needs to be improved for gaining the

competitive position.

Gearing ratio

Particulars Formul

a

2020 2021

Total debt 550 780

Shareholder's equity 400 400

Debt-equity ratio Long-

term

debt /

shareh

olders

equity

1.375 1.950

This particular ratio is determined to compare how some form of

equity to debt so that financial leverage can be ascertained. The gearing

13

Paraphrase This Document

of the firm in the negative manner, from the assessment of the provided

information it can be mentioned that in the year 2021 the gearing ratio has

inclined which is still indicating that firm is having good performance.

On the basis of the overall performance it can be mentioned that in

the year 2021 the company is performing good but require certain changes

in turn accomplishing the objective of higher profitability & sustainability via

maintaining competitive edge can become possible.

SECTION B

Analysing objectives of budgeting for Manor Ltd

Budgeting for this organization is considered to be a factor which is

responsible for the management of the financial process of the organization

that is helpful for an organization towards the preparation of the budget. The

importance of preparing a budget is very high Manor Ltd. Main objectives of

budgeting has been considered to provide the structure for the organization

which is helpful for the company to guide the direction to the organization

towards the financial goals that it wants to achieve (Bonomi Savignon,

Costumato and Marchese, 2019). It has been considered that the budgeting

process is also very effective for the predicting the cash flows that are

considered to be very useful for the company to growth rapidly. This is also

very effective for the company to predict the view of cash flows and

reasonable budgeting objectives that is helpful for the company to achieve

after the preparation of the budget. Budgeting is the process of allocating

resources that helps the budgeting process to a tool for making the

decisions that are helpful for the allocation of funds in the different business

activities. The process of the budgeting is considered to be the key model

towards the facing the number of possible paths for the creation of a set of

budgeting on the different given scenarios. It has been said to be the factor

that allows the business in the measurement of the performance that helps

in the creating the budget which can be used for the judgement of the

employee performance.

14

There are differences between the financial and management

accounting which is in the relation with the accounting and disclosure for the

end results of the business. The main objective of the managerial accounting

for helping the management for providing the information that is used for

planning the set of goals and evaluate these results for the organization. The

audience which is considered for the producing of information that is helpful

for the management of information that is produced in the organization.

Financial accounting is the factor which is helpful for the organization to

understand the use of external parties which helps the shareholders and

lenders for the management of their accounts. The managerial accounting

helps in the preparation of the reports that is not legally required. In the

financial accounting the certain figures are broken out form materially

significant business units whereas the pertains to individual departments are

in the addition of an entire organization. Focus of this organization is

understood and address the specific format that is able to provide the

comparison of the factors that can be made easy to be compared. This is

also known as the main factor that the accounting reports need

consideration for to develop the legal requirement which provided from the

financial accounting methods. The information provided by financial

accounting is more monetary and verifiable whereas the management

accounting information is based on the company goal and driven

information.

3.

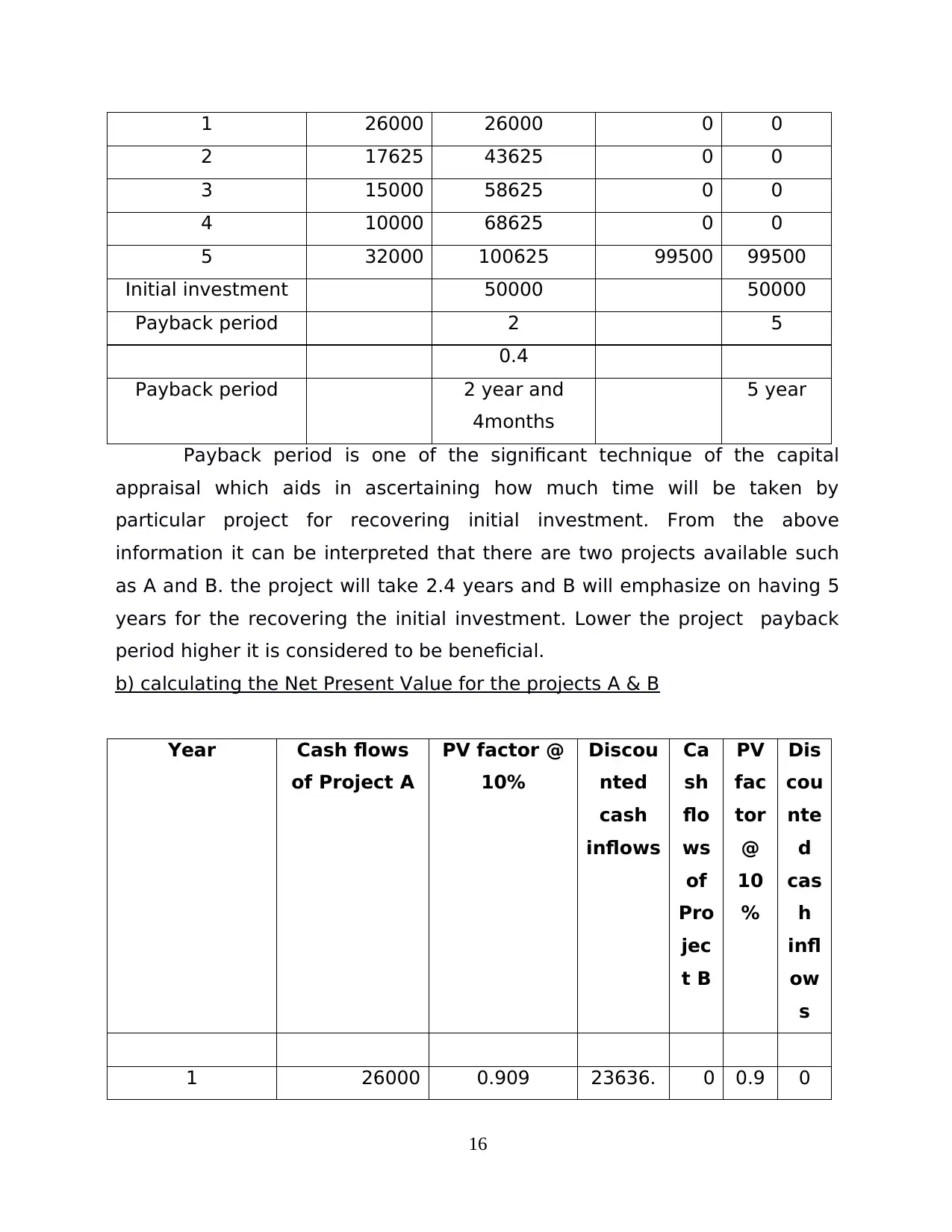

a) Payback Period for the projects A & B

Year Cash

flows of

Project A

Cumulative

cash inflows

Cash

flows of

Project B

Cumulat

ive cash

inflows

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2 17625 43625 0 0

3 15000 58625 0 0

4 10000 68625 0 0

5 32000 100625 99500 99500

Initial investment 50000 50000

Payback period 2 5

0.4

Payback period 2 year and

4months

5 year

Payback period is one of the significant technique of the capital

appraisal which aids in ascertaining how much time will be taken by

particular project for recovering initial investment. From the above

information it can be interpreted that there are two projects available such

as A and B. the project will take 2.4 years and B will emphasize on having 5

years for the recovering the initial investment. Lower the project payback

period higher it is considered to be beneficial.

b) calculating the Net Present Value for the projects A & B

Year Cash flows

of Project A

PV factor @

10%

Discou

nted

cash

inflows

Ca

sh

flo

ws

of

Pro

jec

t B

PV

fac

tor

@

10

%

Dis

cou

nte

d

cas

h

infl

ow

s

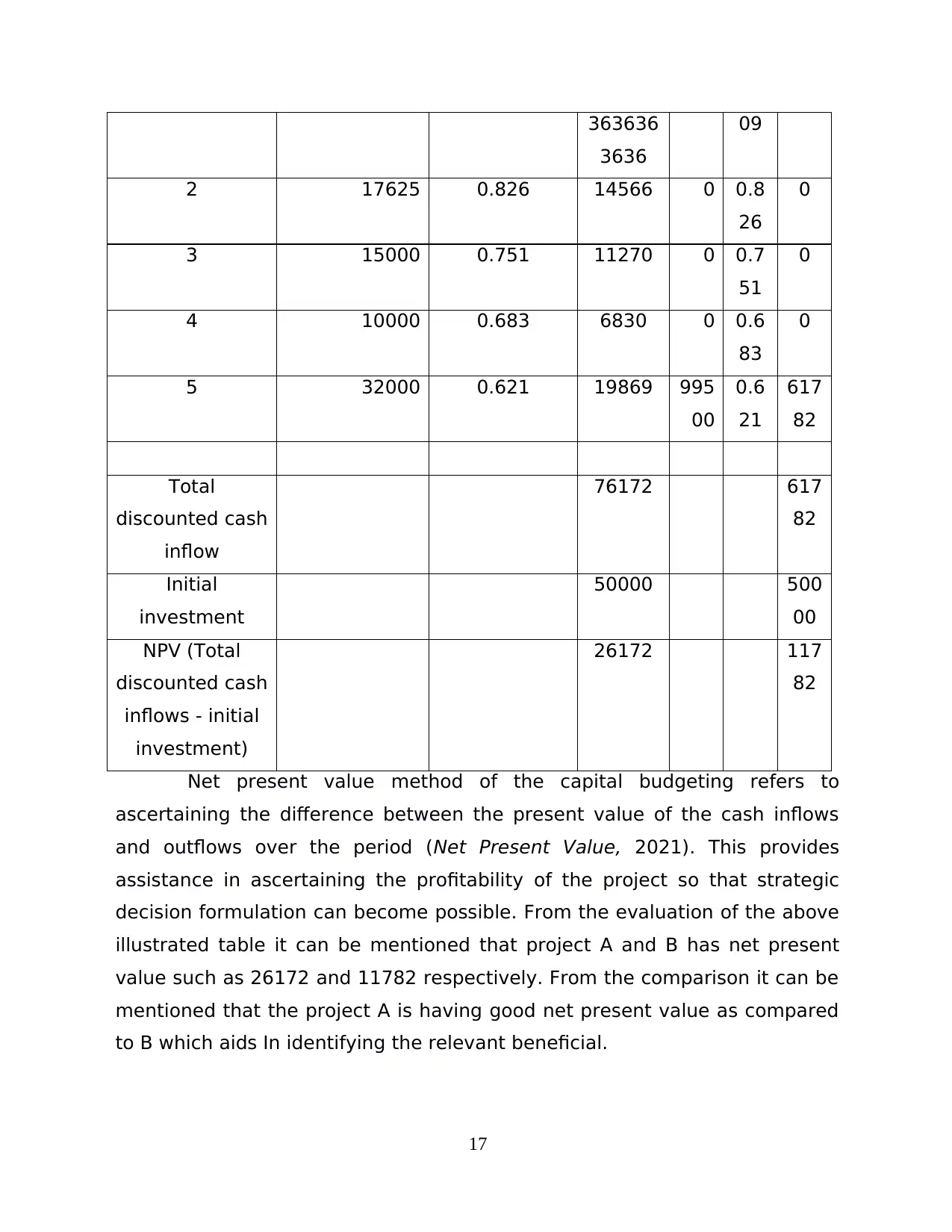

1 26000 0.909 23636. 0 0.9 0

16

Paraphrase This Document

3636

09

2 17625 0.826 14566 0 0.8

26

0

3 15000 0.751 11270 0 0.7

51

0

4 10000 0.683 6830 0 0.6

83

0

5 32000 0.621 19869 995

00

0.6

21

617

82

Total

discounted cash

inflow

76172 617

82

Initial

investment

50000 500

00

NPV (Total

discounted cash

inflows - initial

investment)

26172 117

82

Net present value method of the capital budgeting refers to

ascertaining the difference between the present value of the cash inflows

and outflows over the period (Net Present Value, 2021). This provides

assistance in ascertaining the profitability of the project so that strategic

decision formulation can become possible. From the evaluation of the above

illustrated table it can be mentioned that project A and B has net present

value such as 26172 and 11782 respectively. From the comparison it can be

mentioned that the project A is having good net present value as compared

to B which aids In identifying the relevant beneficial.

17

From the calculation it can be mentioned that project A should be

taken into the consideration as as its payback period is lower. Lower

payback period is helpful in recovering the initial investment in less time as

compared to previous. In addition to this, having good net present value of

project A is depicting that there are higher potential of profitability as

compared to other year. On the basis of this, it can be identified that firm

will be beneficial by using the project A as it is having higher effectiveness

by profitability so that accomplishing greater productiveness can become

possible (Setiany, 2021). This is indicating that firm should focus on project

A as compared to B to meet organizational objectives.

CONCLUSION

With the help of this report it can be concluded that the as per the

profitability Trust has been less effective however, this company has been

able to increase its overall efficiency in the production for better and

enhanced performance. In this report the financial performance of the

organization has been analysed for each of the two years presented from

the financial statements that are provided. This report has also analysed the

budgeting for Manor Ltd and differentiated between the financial and

management accounting, For analysing the viability of the two project A and

B different capital budgeting tools have been used.

18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Books and Journals

Bonomi Savignon, A., Costumato, L. and Marchese, B., 2019. Performance

budgeting in context: an analysis of Italian central administrations.

Administrative Sciences. 9(4). p.79.

Heo, W., and et.al., 2020. Using Artificial Neural Network techniques to

improve the description and prediction of household financial ratios.

Journal of Behavioral and Experimental Finance. 25. p.100273.

Le, H.H. and Viviani, J.L., 2018. Predicting bank failure: An improvement by

implementing a machine-learning approach to classical financial

ratios. Research in International Business and Finance. 44. pp.16-25.

McMahon, S.J., 2018. The linear quadratic model: usage, interpretation and

challenges. Physics in Medicine & Biology. 64(1). p.01TR01.

Mudzakar, M.K., 2021. The Effect Of Return On Asset, Return On Equity,

Earning Per Share, And Price Earning Ratio Toward Stock Return

(Empirical Study Of Transportation). Turkish Journal of Computer and

Mathematics Education (TURCOMAT). 12(8). pp.387-392.

Rahman, T. and Fatmawati, K., 2020. The influence of financial ratios on non

performing financing of the sharia rural banks of Special Region of

Yogyakarta (BPRS DIY) period 2015–2018. Asian Journal of Islamic

Management. 2(1). pp.25-35.

Rashid, C.A., 2018. Efficiency of financial ratios analysis for evaluating

companies’ liquidity. International Journal of Social Sciences &

Educational Studies. 4(4). p.110.

Setiany, E., 2021. The Effect of Investment, Free Cash Flow, Earnings

Management, and Interest Coverage Ratio on Financial

Distress. Journal of Social Science. 2(1). pp.64-69.

Online

Financial Accounting vs. Management Accounting, 2021[Online]. Available

through:

<https://www.diffen.com/difference/Financial_Accounting_vs_Manage

ment_Accounting>

Net Present Value. 2021. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/valuation/net-

present-value-npv/>

19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.