Accounting & Finance: Solved Questions and Examples

VerifiedAdded on 2023/05/27

|13

|1824

|181

AI Summary

This article contains solved questions and examples related to accounting and finance. It covers topics such as payment options, future value of annuity, Australian taxation system, monthly holding returns, CAPM model, and security market line.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING & FINANCE

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

(a) (i) The appropriate payment option would be decided based on the effective annual rate

(EAR).

EAR for option 1

Nominal interest rate (Compounded weekly) = 4.55% p.a.

EAR= {1+( 4.55

5200 ) }52

−1=4.65 %

EAR for option 2

Nominal interest rate (Compounded weekly) = 4.75% p.a.

EAR= {1+( 4.75

5200 ) }52

−1=4.86 %

It is apparent from the above that effective annual interest rate is lower for option 1 with

nominal interest rate 4.55% compounding annually and hence, it would be a suitable payment

option for Jayne.

(ii) Repayment instalment

Instalment = P∗R∗ (1+R )N

[ ( 1+ R )N −1 ]

P=$ 500,000

R=( 4.55 %

52 ) per week

Instalment =$ 1000

N=?

Now,

1000=

500,000∗( 4.55 %

52 )∗

( 1+ ( 4.55 %

52 )) N

[ ( 1+( 4.55 %

52 ) )

N

−1 ]

N=657.85 weeks

(b) (i)Let X is the total contribution from every month

1

(a) (i) The appropriate payment option would be decided based on the effective annual rate

(EAR).

EAR for option 1

Nominal interest rate (Compounded weekly) = 4.55% p.a.

EAR= {1+( 4.55

5200 ) }52

−1=4.65 %

EAR for option 2

Nominal interest rate (Compounded weekly) = 4.75% p.a.

EAR= {1+( 4.75

5200 ) }52

−1=4.86 %

It is apparent from the above that effective annual interest rate is lower for option 1 with

nominal interest rate 4.55% compounding annually and hence, it would be a suitable payment

option for Jayne.

(ii) Repayment instalment

Instalment = P∗R∗ (1+R )N

[ ( 1+ R )N −1 ]

P=$ 500,000

R=( 4.55 %

52 ) per week

Instalment =$ 1000

N=?

Now,

1000=

500,000∗( 4.55 %

52 )∗

( 1+ ( 4.55 %

52 )) N

[ ( 1+( 4.55 %

52 ) )

N

−1 ]

N=657.85 weeks

(b) (i)Let X is the total contribution from every month

1

Future value of annuity at the end of 18 years period = $200,000

Now,

Periodic payment needs to be determined with the help of formula given below (Parrino &

Kidwell, 2014).

P=? r= ( 2.5

12 )%n= ( 18∗12 ) =216 months , FV of annuity=$ 200,000

200,000=P

[ ( 1+ ( 2.5

12 ) % )

216

−1

( 2.5

12 ) % ]P=$ 734.11

It is given that Jennifer would contribute 30% and hence, monthly payment amount would be

30% of the periodic payment amount.

Monthly payment amount =30 %∗734.11=$ 220.23

(ii) Present value of annuity

P=$ 1000 r= ( 4

12 )% per monthn= ( 3∗12 )=36 months , Present value of annuity=$ 200,000

PV of annuity=1000+1000

[ 1−

( ( 1+ 4

12 % ) )

− ( 36−1 )

( 4

12 ) % ]=$ 33,985.60

Money remaining to Jennifer (at her 18th birthday) =200000-100000 -33985.60 = $66,014.39

It is apparent that the money remaining would remain in the bank account till 28 years age.

Amount when the age would be 28 years ¿ ( 1.04 )10∗66,014.39=$ 97,717.43

2

Now,

Periodic payment needs to be determined with the help of formula given below (Parrino &

Kidwell, 2014).

P=? r= ( 2.5

12 )%n= ( 18∗12 ) =216 months , FV of annuity=$ 200,000

200,000=P

[ ( 1+ ( 2.5

12 ) % )

216

−1

( 2.5

12 ) % ]P=$ 734.11

It is given that Jennifer would contribute 30% and hence, monthly payment amount would be

30% of the periodic payment amount.

Monthly payment amount =30 %∗734.11=$ 220.23

(ii) Present value of annuity

P=$ 1000 r= ( 4

12 )% per monthn= ( 3∗12 )=36 months , Present value of annuity=$ 200,000

PV of annuity=1000+1000

[ 1−

( ( 1+ 4

12 % ) )

− ( 36−1 )

( 4

12 ) % ]=$ 33,985.60

Money remaining to Jennifer (at her 18th birthday) =200000-100000 -33985.60 = $66,014.39

It is apparent that the money remaining would remain in the bank account till 28 years age.

Amount when the age would be 28 years ¿ ( 1.04 )10∗66,014.39=$ 97,717.43

2

(iii) Loan amount = Cost – Deposit amount

Loan amount=$ 800,000−$ 97,717.43=$ 702,282.57

Monthly Instalment = P∗R∗( 1+ R ) N

[ ( 1+ R ) N −1 ]

P=$ 702,282.57

R=( 4.5

12 )% per month

Instalment =$ 1000

N=30∗12=360 months

Now,

Monthly Repayment Instalment =

702,282.57∗( 4.5 %

12 )∗

( 1+ ( 4.5 %

12 ) )

360

[ ( 1+( 4.5 %

12 ))

360

−1 ]

Monthly Repayment Instalment=$ 3,558.27

Question 2

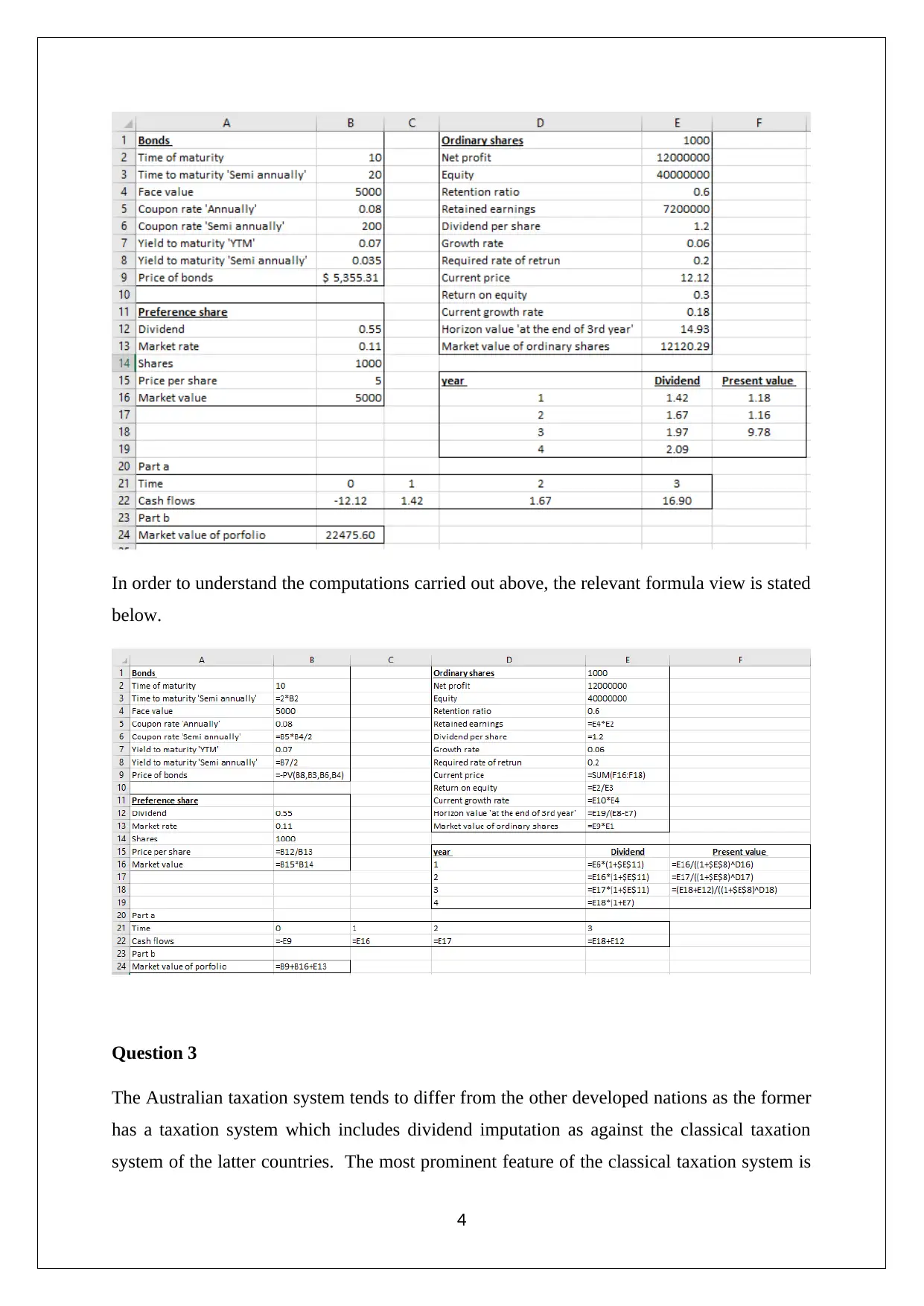

The relevant screenshot for excel computation of the cash flows from ordinary equity coupled

with market value of the various financing instruments is shown below.

3

Loan amount=$ 800,000−$ 97,717.43=$ 702,282.57

Monthly Instalment = P∗R∗( 1+ R ) N

[ ( 1+ R ) N −1 ]

P=$ 702,282.57

R=( 4.5

12 )% per month

Instalment =$ 1000

N=30∗12=360 months

Now,

Monthly Repayment Instalment =

702,282.57∗( 4.5 %

12 )∗

( 1+ ( 4.5 %

12 ) )

360

[ ( 1+( 4.5 %

12 ))

360

−1 ]

Monthly Repayment Instalment=$ 3,558.27

Question 2

The relevant screenshot for excel computation of the cash flows from ordinary equity coupled

with market value of the various financing instruments is shown below.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

In order to understand the computations carried out above, the relevant formula view is stated

below.

Question 3

The Australian taxation system tends to differ from the other developed nations as the former

has a taxation system which includes dividend imputation as against the classical taxation

system of the latter countries. The most prominent feature of the classical taxation system is

4

below.

Question 3

The Australian taxation system tends to differ from the other developed nations as the former

has a taxation system which includes dividend imputation as against the classical taxation

system of the latter countries. The most prominent feature of the classical taxation system is

4

that the profits that the businesses tend to generate are taxed twice. Firstly, the corporate

profits are charged the corporate tax which the businesses have to pay. Additionally, when

the post-tax profits are given to the shareholders as dividends, then on the shareholders

income tax is applicable as the dividend income is added into the taxable income of these

entities. In sharp contrast, the dividend imputation system prevalent in Australia tends to tax

the corporate profits only once and the complete burden in this regards is borne by the

companies. With regards to the shareholders paying tax on the dividends, it would happen

only when the marginal tax rate of the taxpayer receiving dividends is more than the

corporate tax rate i.e. 30%. This is because imputation credits are available for the franked

dividends that the company pays to the shareholders which tend to provide rebate in tax to the

extent of 30% tax (Damodaran, 2015).

This difference which has been theoretically highlighted can also be practically explained

with the aid of a numerical example. Assume that the before tax profits that the company has

generated amounts to $ 10,000 with the corporate tax rate being 30%. As a result, 30% of the

income would be deducted as corporate tax and remaining $ 7,000 is available with the

company as post tax income. Assume that the company decides to pay this entire amount as

dividends to shareholders whose average marginal tax rate is 30%. The tax levied on the

shareholders collectively would be (30/100)*7,000 = $ 2,100. Hence, the cumulative tax

burden in the traditional tax system amounts to $3,000 + $ 2,100 = $ 5,100. As a result, of the

$ 10,000 generated as pre-tax profits, 51% is taxed by the government and the remaining

49% is available for the shareholders. The situation in case of dividend imputation system

would be quite different since the underlying liability on account of tax would be

significantly lesser. On the before tax corporate profits of $ 10,000, the total amount of

corporate tax that is levied would amount to $ 3,000. Consider that 100% of the remaining

income is paid as dividends. In wake of these dividends (assuming 100% franked), the

imputation credit extended to the shareholders would amount to (7000/(1-0.3)) – 7000 = $

3,000. This amount is reflects in the taxable income for the concerned shareholders.

Therefore, on account of dividends received, the total taxable income amounts to $ 7,000 + $

3,000 = $ 10,000. Considering that the marginal tax rate of 30% applies on the shareholders,

the tax liability levied on the dividend income = 0.3*10000 = $ 3,000. However, the same

amount is already available as tax credit and thereby no tax would be payable by the

shareholder. If the marginal tax rate for the shareholder would have been higher, then to the

extent that marginal rate is higher than 30%, tax would be levied on dividends. Hence, in

5

profits are charged the corporate tax which the businesses have to pay. Additionally, when

the post-tax profits are given to the shareholders as dividends, then on the shareholders

income tax is applicable as the dividend income is added into the taxable income of these

entities. In sharp contrast, the dividend imputation system prevalent in Australia tends to tax

the corporate profits only once and the complete burden in this regards is borne by the

companies. With regards to the shareholders paying tax on the dividends, it would happen

only when the marginal tax rate of the taxpayer receiving dividends is more than the

corporate tax rate i.e. 30%. This is because imputation credits are available for the franked

dividends that the company pays to the shareholders which tend to provide rebate in tax to the

extent of 30% tax (Damodaran, 2015).

This difference which has been theoretically highlighted can also be practically explained

with the aid of a numerical example. Assume that the before tax profits that the company has

generated amounts to $ 10,000 with the corporate tax rate being 30%. As a result, 30% of the

income would be deducted as corporate tax and remaining $ 7,000 is available with the

company as post tax income. Assume that the company decides to pay this entire amount as

dividends to shareholders whose average marginal tax rate is 30%. The tax levied on the

shareholders collectively would be (30/100)*7,000 = $ 2,100. Hence, the cumulative tax

burden in the traditional tax system amounts to $3,000 + $ 2,100 = $ 5,100. As a result, of the

$ 10,000 generated as pre-tax profits, 51% is taxed by the government and the remaining

49% is available for the shareholders. The situation in case of dividend imputation system

would be quite different since the underlying liability on account of tax would be

significantly lesser. On the before tax corporate profits of $ 10,000, the total amount of

corporate tax that is levied would amount to $ 3,000. Consider that 100% of the remaining

income is paid as dividends. In wake of these dividends (assuming 100% franked), the

imputation credit extended to the shareholders would amount to (7000/(1-0.3)) – 7000 = $

3,000. This amount is reflects in the taxable income for the concerned shareholders.

Therefore, on account of dividends received, the total taxable income amounts to $ 7,000 + $

3,000 = $ 10,000. Considering that the marginal tax rate of 30% applies on the shareholders,

the tax liability levied on the dividend income = 0.3*10000 = $ 3,000. However, the same

amount is already available as tax credit and thereby no tax would be payable by the

shareholder. If the marginal tax rate for the shareholder would have been higher, then to the

extent that marginal rate is higher than 30%, tax would be levied on dividends. Hence, in

5

contrast, it is apparent that that the tax rate effectively is only 30% in imputation credit based

system as compared to 51% in the classical tax system.

In order to attract foreign businesses, there has been clamour in the recent times about

corporate tax cut. These have gained more force after the cut in taxes initiated by USA

recently and there are comparisons being made with these nations (Smith, 2015). A key factor

that is overlooked in the process is that the nations that have experienced rate cuts in the

recent times are all adherents of a classical taxation system which is not the case with

Australia. The net result is that the effective tax rate of Australia does not differ significantly

from the western peers (Montgomery, 2018). Also, tax rate cut would not help businesses as

in case of local businesses, the burden of tax would shift to the shareholders instead of

companies since imputation credits would decline. The potential beneficiaries of reduction in

corporate tax would only be foreign businesses that tend to take their profits to the host

countries. However, for such foreign businesses, the current Australian tax rates do not pose

any issue which does not make for a strong case of any tax cuts (Taylor, 2018).

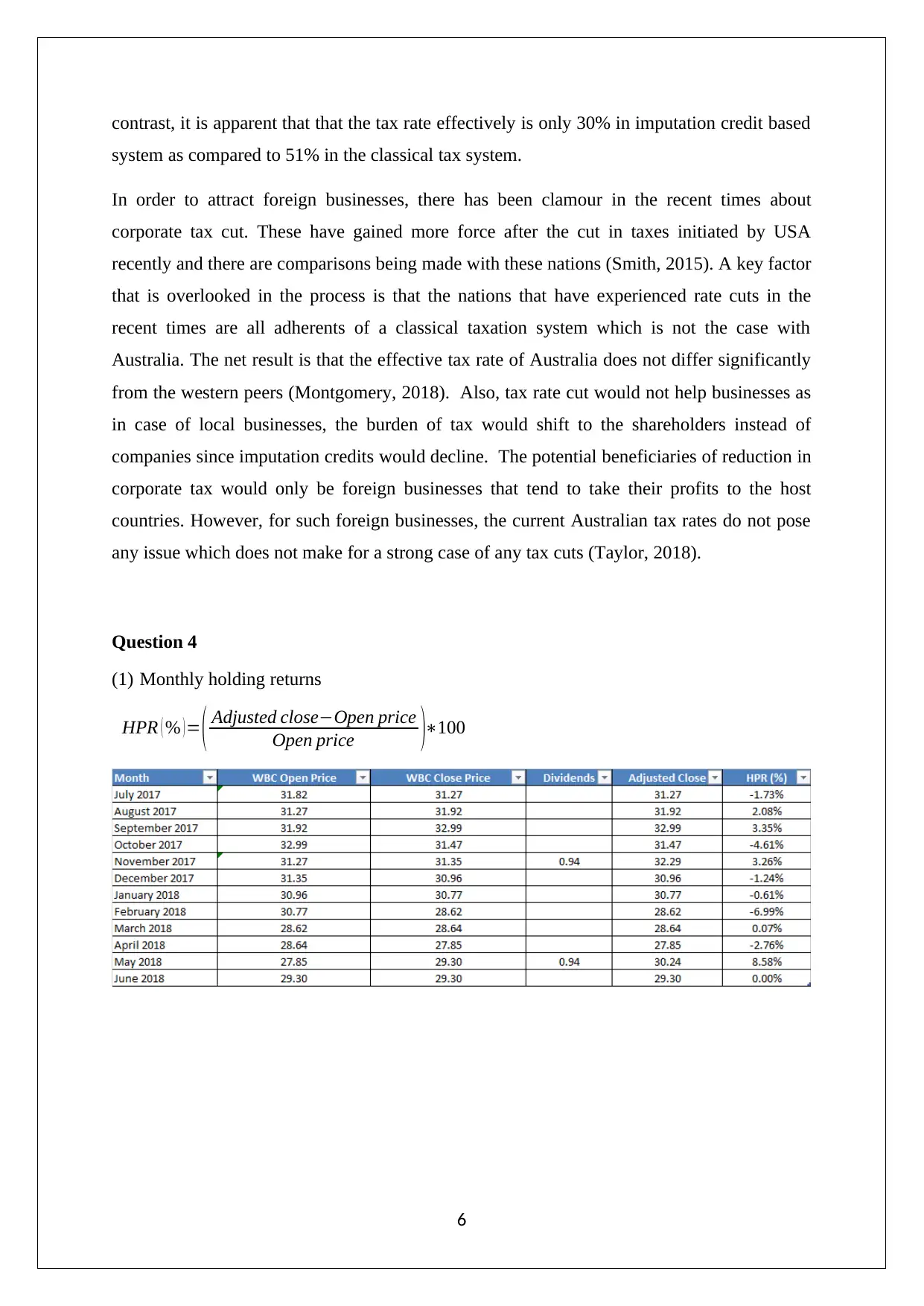

Question 4

(1) Monthly holding returns

HPR ( % ) = ( Adjusted close−Open price

Open price )∗100

6

system as compared to 51% in the classical tax system.

In order to attract foreign businesses, there has been clamour in the recent times about

corporate tax cut. These have gained more force after the cut in taxes initiated by USA

recently and there are comparisons being made with these nations (Smith, 2015). A key factor

that is overlooked in the process is that the nations that have experienced rate cuts in the

recent times are all adherents of a classical taxation system which is not the case with

Australia. The net result is that the effective tax rate of Australia does not differ significantly

from the western peers (Montgomery, 2018). Also, tax rate cut would not help businesses as

in case of local businesses, the burden of tax would shift to the shareholders instead of

companies since imputation credits would decline. The potential beneficiaries of reduction in

corporate tax would only be foreign businesses that tend to take their profits to the host

countries. However, for such foreign businesses, the current Australian tax rates do not pose

any issue which does not make for a strong case of any tax cuts (Taylor, 2018).

Question 4

(1) Monthly holding returns

HPR ( % ) = ( Adjusted close−Open price

Open price )∗100

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

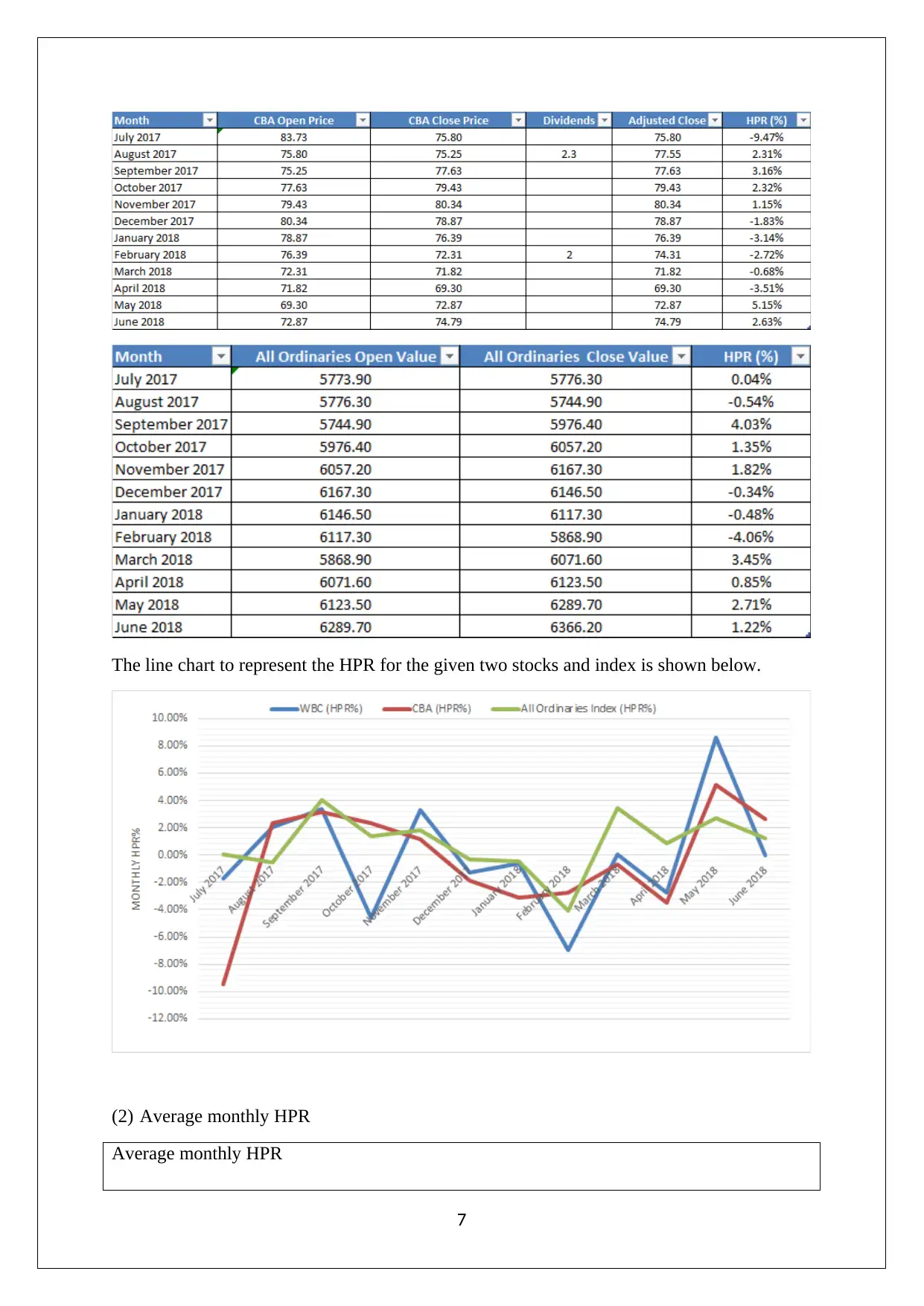

The line chart to represent the HPR for the given two stocks and index is shown below.

(2) Average monthly HPR

Average monthly HPR

7

(2) Average monthly HPR

Average monthly HPR

7

For

WBC

For

CBA

For

Index

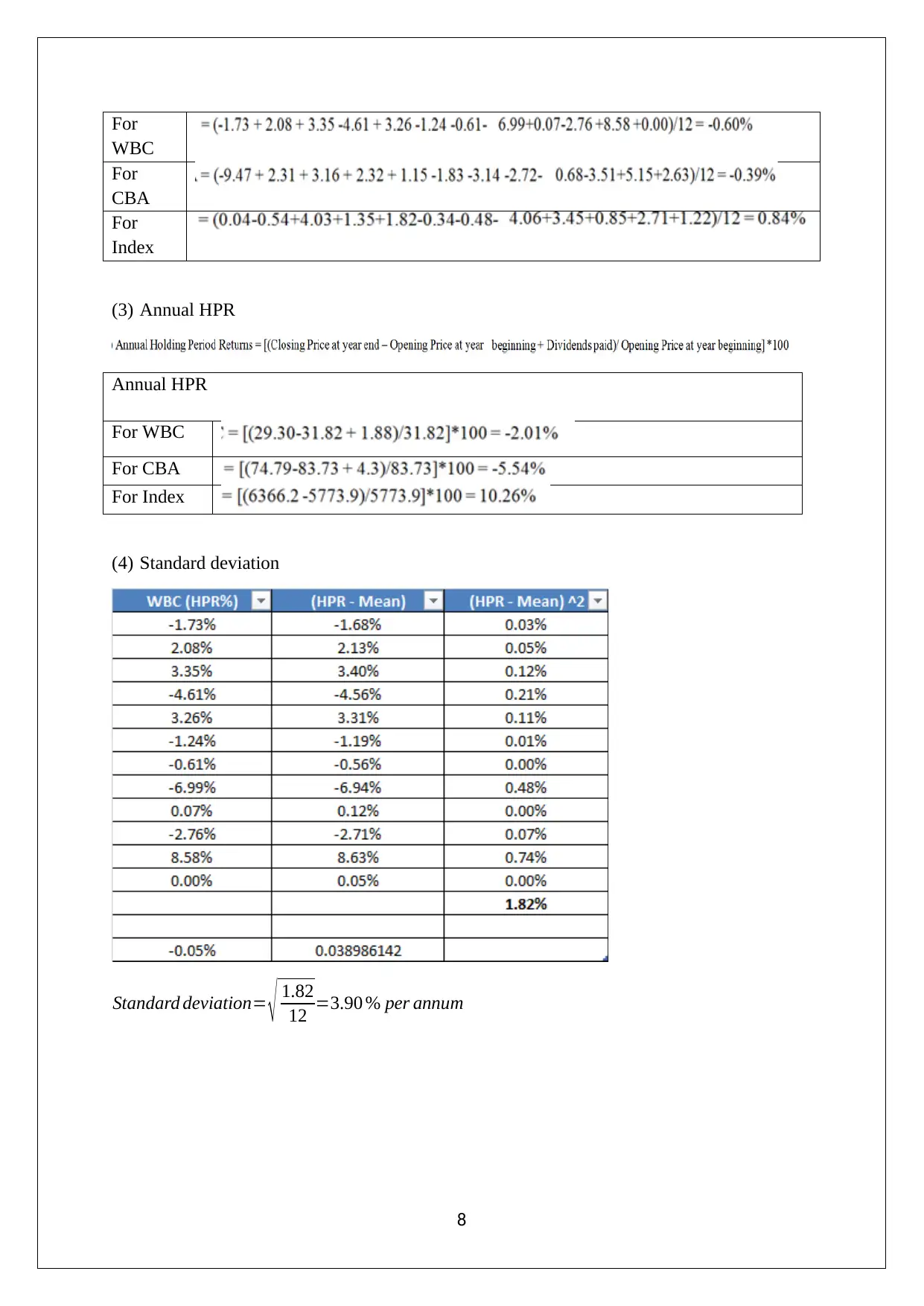

(3) Annual HPR

Annual HPR

For WBC

For CBA

For Index

(4) Standard deviation

Standard deviation= √ 1.82

12 =3.90 % per annum

8

WBC

For

CBA

For

Index

(3) Annual HPR

Annual HPR

For WBC

For CBA

For Index

(4) Standard deviation

Standard deviation= √ 1.82

12 =3.90 % per annum

8

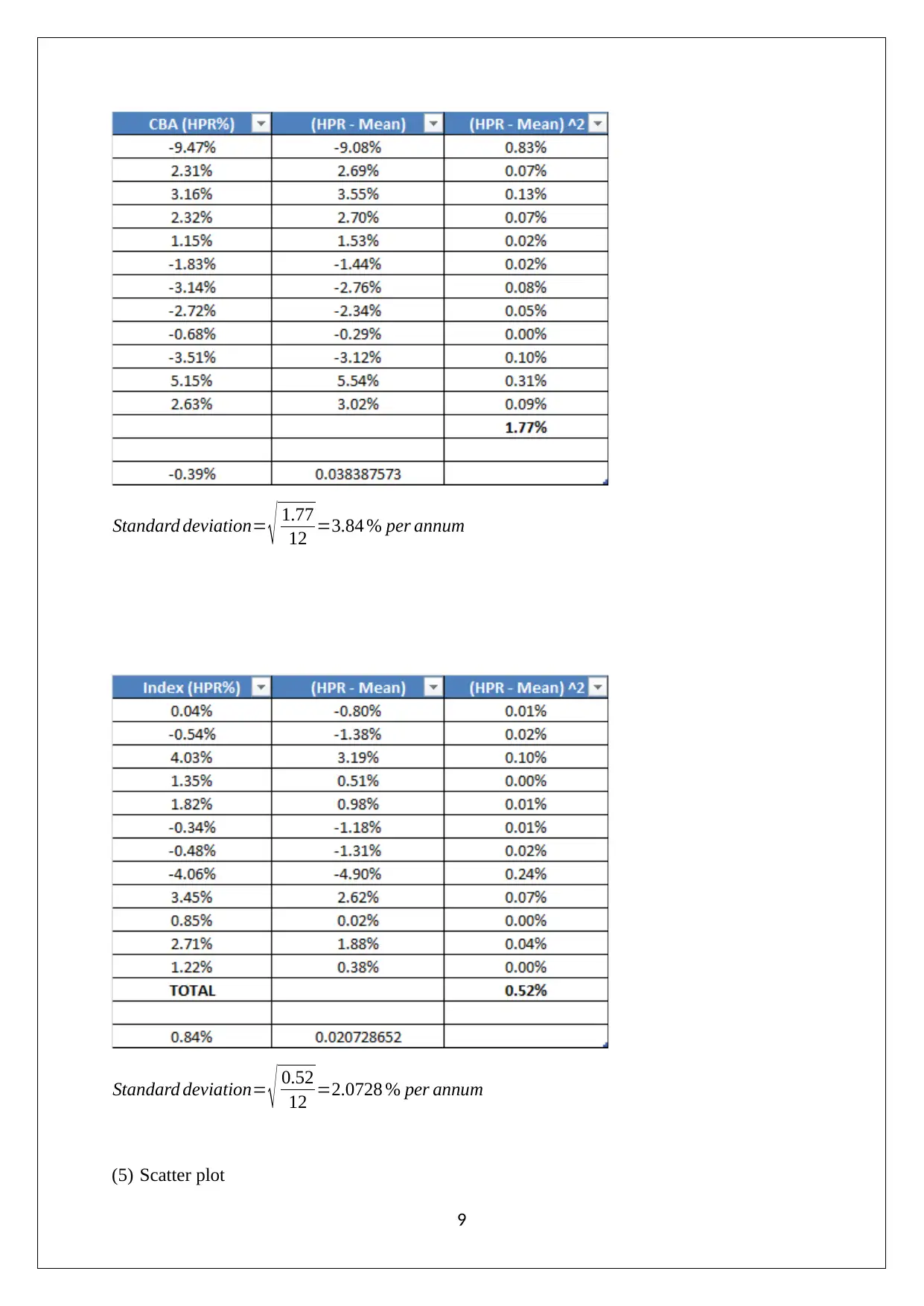

Standard deviation= √ 1.77

12 =3.84 % per annum

Standard deviation= √ 0.52

12 =2.0728 % per annum

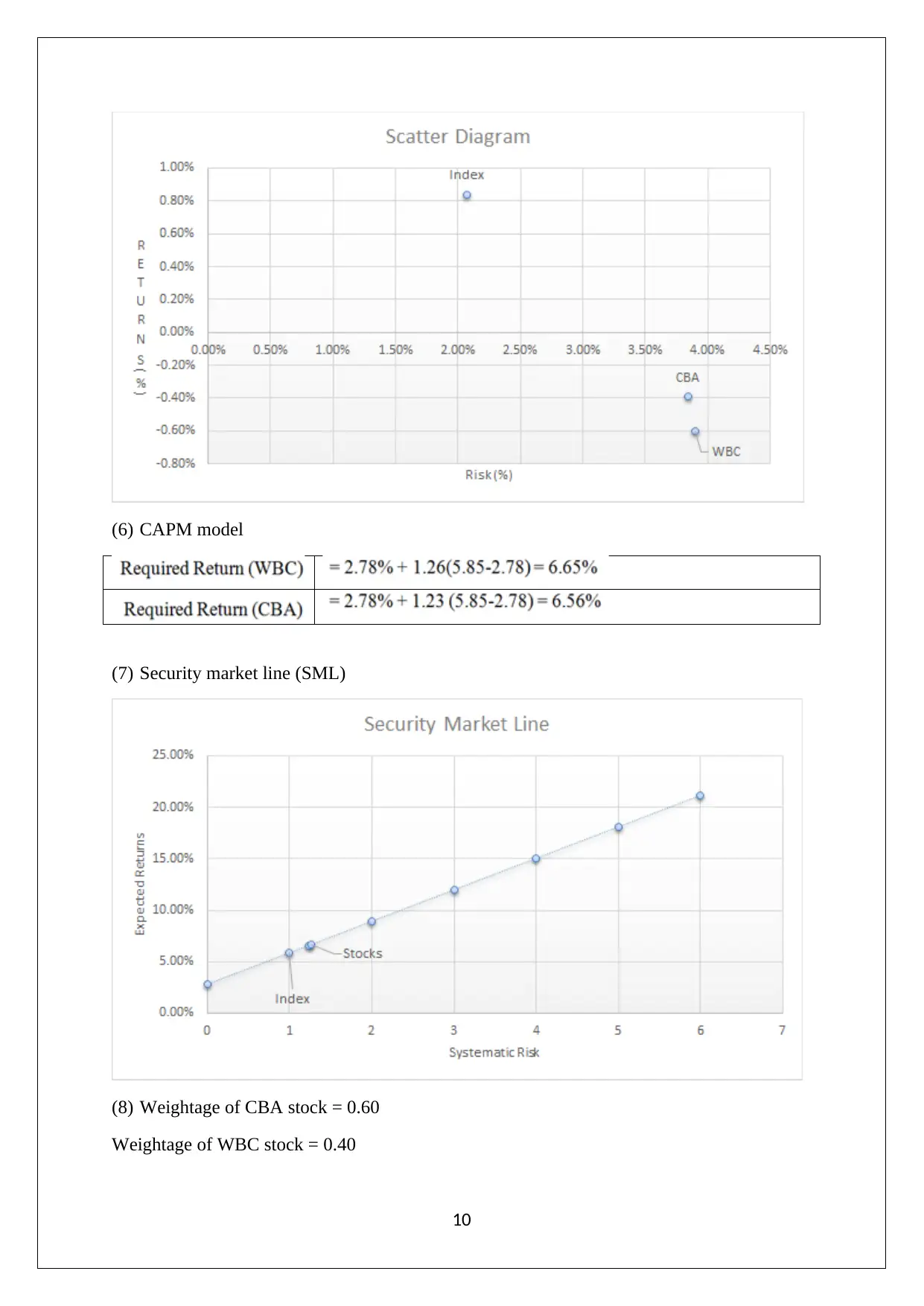

(5) Scatter plot

9

12 =3.84 % per annum

Standard deviation= √ 0.52

12 =2.0728 % per annum

(5) Scatter plot

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(6) CAPM model

(7) Security market line (SML)

(8) Weightage of CBA stock = 0.60

Weightage of WBC stock = 0.40

10

(7) Security market line (SML)

(8) Weightage of CBA stock = 0.60

Weightage of WBC stock = 0.40

10

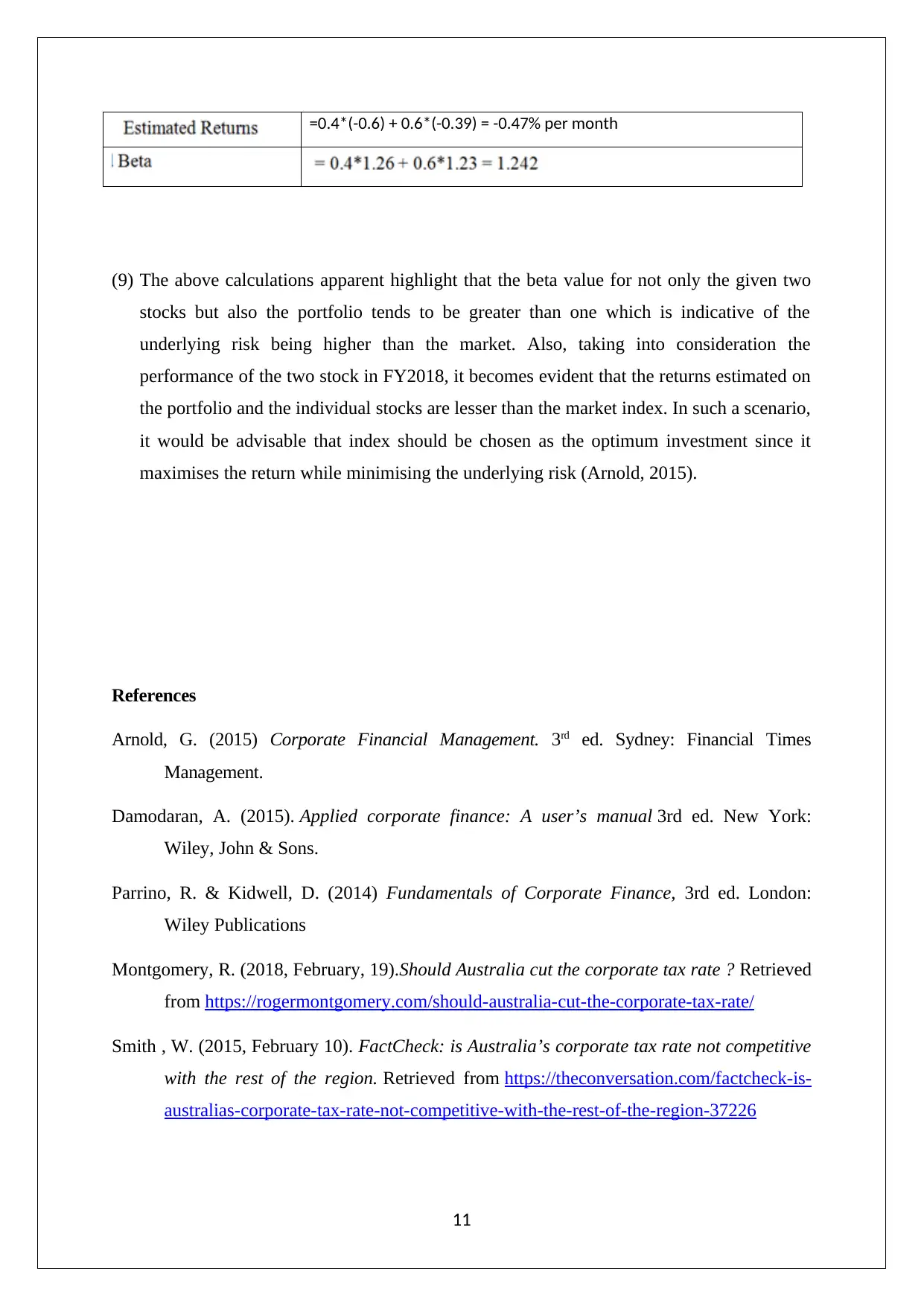

=0.4*(-0.6) + 0.6*(-0.39) = -0.47% per month

(9) The above calculations apparent highlight that the beta value for not only the given two

stocks but also the portfolio tends to be greater than one which is indicative of the

underlying risk being higher than the market. Also, taking into consideration the

performance of the two stock in FY2018, it becomes evident that the returns estimated on

the portfolio and the individual stocks are lesser than the market index. In such a scenario,

it would be advisable that index should be chosen as the optimum investment since it

maximises the return while minimising the underlying risk (Arnold, 2015).

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

11

(9) The above calculations apparent highlight that the beta value for not only the given two

stocks but also the portfolio tends to be greater than one which is indicative of the

underlying risk being higher than the market. Also, taking into consideration the

performance of the two stock in FY2018, it becomes evident that the returns estimated on

the portfolio and the individual stocks are lesser than the market index. In such a scenario,

it would be advisable that index should be chosen as the optimum investment since it

maximises the return while minimising the underlying risk (Arnold, 2015).

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

11

Taylor, D. (2018, March 29). Corporate tax cuts: What are the key issues in the

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

12

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

12

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.