Accounting & finance Assignment PDF

VerifiedAdded on 2021/06/14

|16

|1672

|27

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING & FINANCE

Student Name

[Pick the date]

Student Name

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

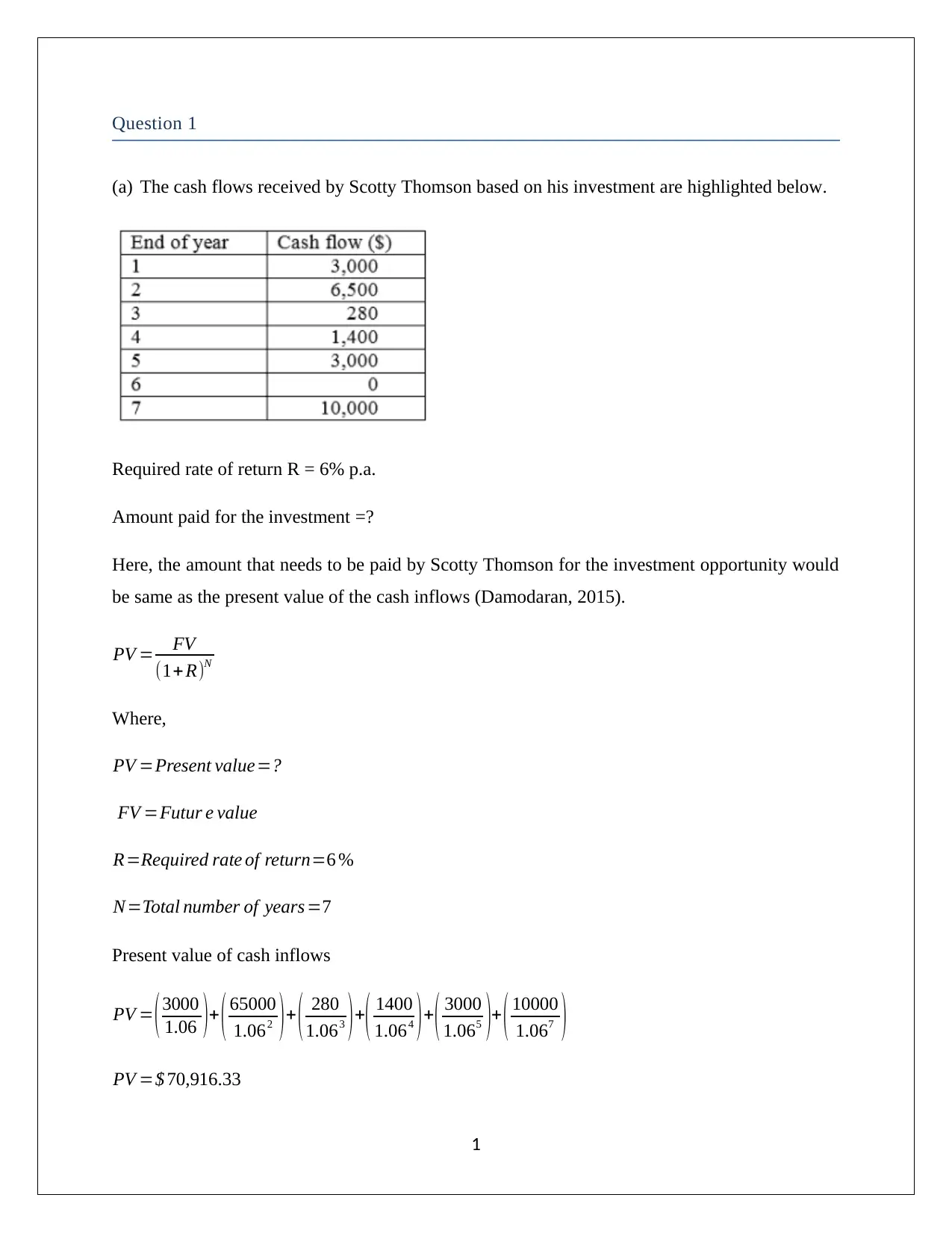

(a) The cash flows received by Scotty Thomson based on his investment are highlighted below.

Required rate of return R = 6% p.a.

Amount paid for the investment =?

Here, the amount that needs to be paid by Scotty Thomson for the investment opportunity would

be same as the present value of the cash inflows (Damodaran, 2015).

PV = FV

(1+ R)N

Where,

PV =Present value=?

FV =Futur e value

R=Required rate of return=6 %

N=Total number of years =7

Present value of cash inflows

PV = ( 3000

1.06 )+ ( 65000

1.062 ) + ( 280

1.063 ) +

( 1400

1.064 ) +

( 3000

1.065 )+ ( 10000

1.067 )

PV =$ 70,916.33

1

(a) The cash flows received by Scotty Thomson based on his investment are highlighted below.

Required rate of return R = 6% p.a.

Amount paid for the investment =?

Here, the amount that needs to be paid by Scotty Thomson for the investment opportunity would

be same as the present value of the cash inflows (Damodaran, 2015).

PV = FV

(1+ R)N

Where,

PV =Present value=?

FV =Futur e value

R=Required rate of return=6 %

N=Total number of years =7

Present value of cash inflows

PV = ( 3000

1.06 )+ ( 65000

1.062 ) + ( 280

1.063 ) +

( 1400

1.064 ) +

( 3000

1.065 )+ ( 10000

1.067 )

PV =$ 70,916.33

1

Therefore, the $70,916.33 is the amount that needs to be paid by Scotty Thomson for the

investment.

(b) Worth of new apartment in North Melbourne P=$ 1.8 million∨($ 1,800,000)

Nominal rate of loan R=5 % p . a.∨(5 /12 %) monthly=0.4167 per month

Loan offered for the time period N¿ 30 years∨ ( 30∗12 ) months=360 months

Repayment of loan = Monthly

Monthly repayment amount =?

Equal monthly instalment (Monthly repayment amount) is calculated as shown below (Arnold,

2015).

EMI= P∗R∗( 1+ R ) N

( 1+ R )N −1

¿ 1,800,000∗0.004167∗( 1+0.004167 )360

( 1+0.004167 )360

¿ $ 9,662.79

Therefore, Jarrad needs to pay a monthly repayment instalment of $9,662.79.

(c) (i) Amount available for investment ¿ $ 50,000

Total number of monthly payment N=35∗12=420

Applicable interest rate R=7 %p.a.∨ ( 7

12 )%=0.5833 per month

Monthly payment P=$ 1500

2

investment.

(b) Worth of new apartment in North Melbourne P=$ 1.8 million∨($ 1,800,000)

Nominal rate of loan R=5 % p . a.∨(5 /12 %) monthly=0.4167 per month

Loan offered for the time period N¿ 30 years∨ ( 30∗12 ) months=360 months

Repayment of loan = Monthly

Monthly repayment amount =?

Equal monthly instalment (Monthly repayment amount) is calculated as shown below (Arnold,

2015).

EMI= P∗R∗( 1+ R ) N

( 1+ R )N −1

¿ 1,800,000∗0.004167∗( 1+0.004167 )360

( 1+0.004167 )360

¿ $ 9,662.79

Therefore, Jarrad needs to pay a monthly repayment instalment of $9,662.79.

(c) (i) Amount available for investment ¿ $ 50,000

Total number of monthly payment N=35∗12=420

Applicable interest rate R=7 %p.a.∨ ( 7

12 )%=0.5833 per month

Monthly payment P=$ 1500

2

The monthly payment would be in the form of annuity for 25 years. The first payment would be

at the starting of the period or from today.

Future value of annuity can be calculated by assuming that the first payment is started from

today.

FVof annuity due= ( 1+ R ) ∗P∗[ ( 1+ R ) N−1

R ]

Hence, the future value of all the consecutive monthly payments until the retirement is calculated

below.

¿ ( 1+0.005833 )∗1500∗[ ( 1+0.005833 ) 420−1

0.005833 ]=$ 2,717,341.13

Further,

The future value of total payment is determined as highlighted below.

F V =PV ( 1+ R ) N

¿ 50,000 ( 1+ 0.005833 ) 420

¿ $ 575,307.6

Hence, at the time of retirement the total amount is as computed below.

¿ $ 2,717,341.13+$ 575,307.6=$ 3,292,648.72

(ii) The aim is to find the present value of $200,000 at the interest rate of 5% per annum at the

time of retirement.

F V =PV ( 1+ R ) N

200000=PV ( 1+0.05 )25

PV =$ 59060.55

3

at the starting of the period or from today.

Future value of annuity can be calculated by assuming that the first payment is started from

today.

FVof annuity due= ( 1+ R ) ∗P∗[ ( 1+ R ) N−1

R ]

Hence, the future value of all the consecutive monthly payments until the retirement is calculated

below.

¿ ( 1+0.005833 )∗1500∗[ ( 1+0.005833 ) 420−1

0.005833 ]=$ 2,717,341.13

Further,

The future value of total payment is determined as highlighted below.

F V =PV ( 1+ R ) N

¿ 50,000 ( 1+ 0.005833 ) 420

¿ $ 575,307.6

Hence, at the time of retirement the total amount is as computed below.

¿ $ 2,717,341.13+$ 575,307.6=$ 3,292,648.72

(ii) The aim is to find the present value of $200,000 at the interest rate of 5% per annum at the

time of retirement.

F V =PV ( 1+ R ) N

200000=PV ( 1+0.05 )25

PV =$ 59060.55

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

As highlighted above, the future value at the time of retirement is $ 59060.55 .

Therefore, the amount out of which the annuity payment would be generated for the 25 years

¿ $ 3,292,648.72−$ 59060.55=$ 3,233,588.17

Assume

The annuity amount at the end of the year after the retirement would be A.

Present value of annuity PV = A [ 1−(1+ R)−N

R ]

3,233,588.1= A [ 1−(1+0.05)−25

0.05 ]

A=$ 229 , 431

Thus, the annuity amount after retirement is $229,431.

Question 2

The given information and data is shown below.

4

Therefore, the amount out of which the annuity payment would be generated for the 25 years

¿ $ 3,292,648.72−$ 59060.55=$ 3,233,588.17

Assume

The annuity amount at the end of the year after the retirement would be A.

Present value of annuity PV = A [ 1−(1+ R)−N

R ]

3,233,588.1= A [ 1−(1+0.05)−25

0.05 ]

A=$ 229 , 431

Thus, the annuity amount after retirement is $229,431.

Question 2

The given information and data is shown below.

4

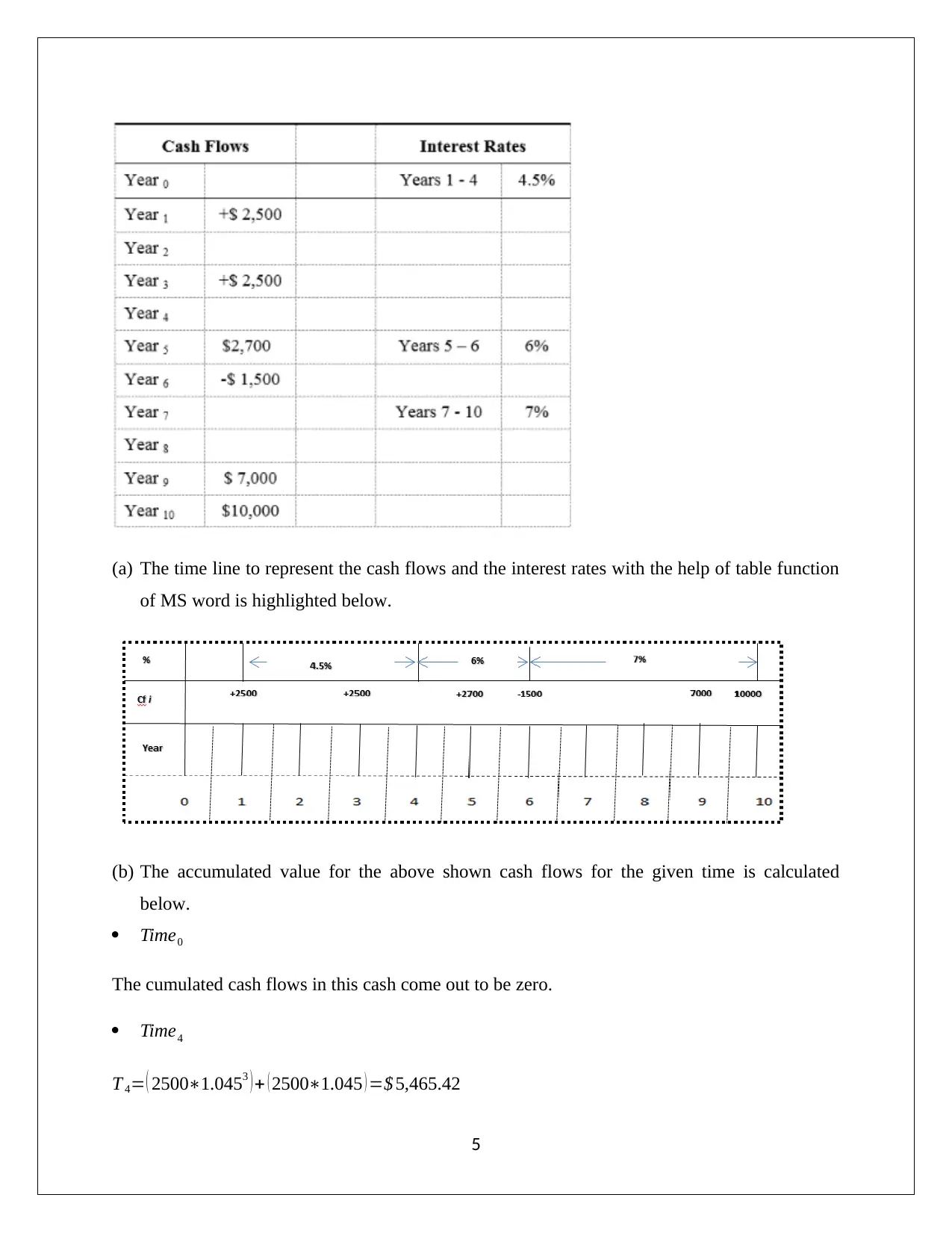

(a) The time line to represent the cash flows and the interest rates with the help of table function

of MS word is highlighted below.

(b) The accumulated value for the above shown cash flows for the given time is calculated

below.

Time0

The cumulated cash flows in this cash come out to be zero.

Time4

T 4= ( 2500∗1.0453 ) + ( 2500∗1.045 ) =$ 5,465.42

5

of MS word is highlighted below.

(b) The accumulated value for the above shown cash flows for the given time is calculated

below.

Time0

The cumulated cash flows in this cash come out to be zero.

Time4

T 4= ( 2500∗1.0453 ) + ( 2500∗1.045 ) =$ 5,465.42

5

Time10

T 10= ( 5465.42∗1.062∗1.074 ) + ( 2700∗1.06∗1.074 )− ( 1500∗1.074 ) + ( 7000∗1.07 ) +10000=$ 27,324.83

Question 3

There has been demand to reduce the Australian corporate tax for quite some time and this has

intensified in the wake of corporate tax rate in US to 21% at the beginning of the year. The

advocates of this tax cute highlight that it can serve as a key incentive in order to attract foreign

investors. They tend to highlight the lower corporate tax rate that their nations tend to offer.

However, there is one fatal flaw with this argument which needs to be highlighted (Smith, 2015).

This is with regards to the dividend imputation system as per which the dividends are not taxed

twice and instead the individual taxpayers tend to get advantage on account of the corporate

taxes paid by the company. This is a unique system in Australia based on which the payment of

dividend is a way to ensure that the corporate tax paid is deployed to earn tax credits for the

shareholders in the form of franked dividends. This system is quite different from the prevailing

system in developed world where taxation of corporate income happens twice. In these countries,

companies ought to pay tax on the corporate profits and afterwards when the company pays

dividends, then these dividends are added to the personal income of the shareholders and taxed at

personal tax rate. This leads to an effective tax rate that may be actually significant higher to that

prevailing in Australia (Smith, 2015).

Consider an example where $ 1000 is the profit made by company, hence $ 300 is the corporate

tax levied. If the remaining amount is given to shareholders as dividends and these are levied a

marginal tax of 30%, then another $ 210 would be taken as personal tax making the total tax

burden at $ 510 or 51%. In case of Australia, the total tax levied in the above case would be $

300 only. IF the corporate tax rate is decreased, then a higher amount of cash would be paid by

company but with lower franking credits. As a result, any decline in corporate tax for domestic

companies would be compensated by levying tax on the dividends which the shareholders would

obtain and hence the government revenues would not be adversely impacted. However, this is

not the case when the underlying companies have foreign ownership since the higher cash would

6

T 10= ( 5465.42∗1.062∗1.074 ) + ( 2700∗1.06∗1.074 )− ( 1500∗1.074 ) + ( 7000∗1.07 ) +10000=$ 27,324.83

Question 3

There has been demand to reduce the Australian corporate tax for quite some time and this has

intensified in the wake of corporate tax rate in US to 21% at the beginning of the year. The

advocates of this tax cute highlight that it can serve as a key incentive in order to attract foreign

investors. They tend to highlight the lower corporate tax rate that their nations tend to offer.

However, there is one fatal flaw with this argument which needs to be highlighted (Smith, 2015).

This is with regards to the dividend imputation system as per which the dividends are not taxed

twice and instead the individual taxpayers tend to get advantage on account of the corporate

taxes paid by the company. This is a unique system in Australia based on which the payment of

dividend is a way to ensure that the corporate tax paid is deployed to earn tax credits for the

shareholders in the form of franked dividends. This system is quite different from the prevailing

system in developed world where taxation of corporate income happens twice. In these countries,

companies ought to pay tax on the corporate profits and afterwards when the company pays

dividends, then these dividends are added to the personal income of the shareholders and taxed at

personal tax rate. This leads to an effective tax rate that may be actually significant higher to that

prevailing in Australia (Smith, 2015).

Consider an example where $ 1000 is the profit made by company, hence $ 300 is the corporate

tax levied. If the remaining amount is given to shareholders as dividends and these are levied a

marginal tax of 30%, then another $ 210 would be taken as personal tax making the total tax

burden at $ 510 or 51%. In case of Australia, the total tax levied in the above case would be $

300 only. IF the corporate tax rate is decreased, then a higher amount of cash would be paid by

company but with lower franking credits. As a result, any decline in corporate tax for domestic

companies would be compensated by levying tax on the dividends which the shareholders would

obtain and hence the government revenues would not be adversely impacted. However, this is

not the case when the underlying companies have foreign ownership since the higher cash would

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be sent to the respective country of origin with Australia not getting a share of the pie (Smith,

2015).

The above discussion clearly hints that corporate tax reduction would be useful only for foreign

companies. However, for more foreign investment to happen in Australia, it is noteworthy that

there are other factors besides tax that are considered by these investors. In primary and tertiary

sectors, Australia already has significant presence of foreign and domestic players. It is the

manufacturing sector that is lagging in Australia. But the same faces headwinds owing to limited

customer base, geographical isolation along with high cost of labour. It is unlikely that by

lowering tax rate, significant investments would happen in this regards. Besides, it needs to be

considered that the Australian taxation system also offers generous deductions which contribute

to effective tax rate in Australia being comparable or lower than the developed world

(Montgomery, 2018). Also, the current timing for corporate tax cuts may not be recommended

considering that fiscally the recent times have been challenging owing to falling mining related

exports to China and rising social security expenses (Taylor, 2018).

Owing to the discussion above, it can be concluded that the reduction in corporate tax is unlikely

to bring any significant tangible gains for the economy as the domestic companies would not be

much impacted while the foreign investments may still be limited owing to other associated

disadvantages besides tax structure. The existing foreign companies may be the prime

beneficiaries and the government may experience a shortfall in revenues which could further

worsen the already delicate fiscal position in Australia.

Question 4

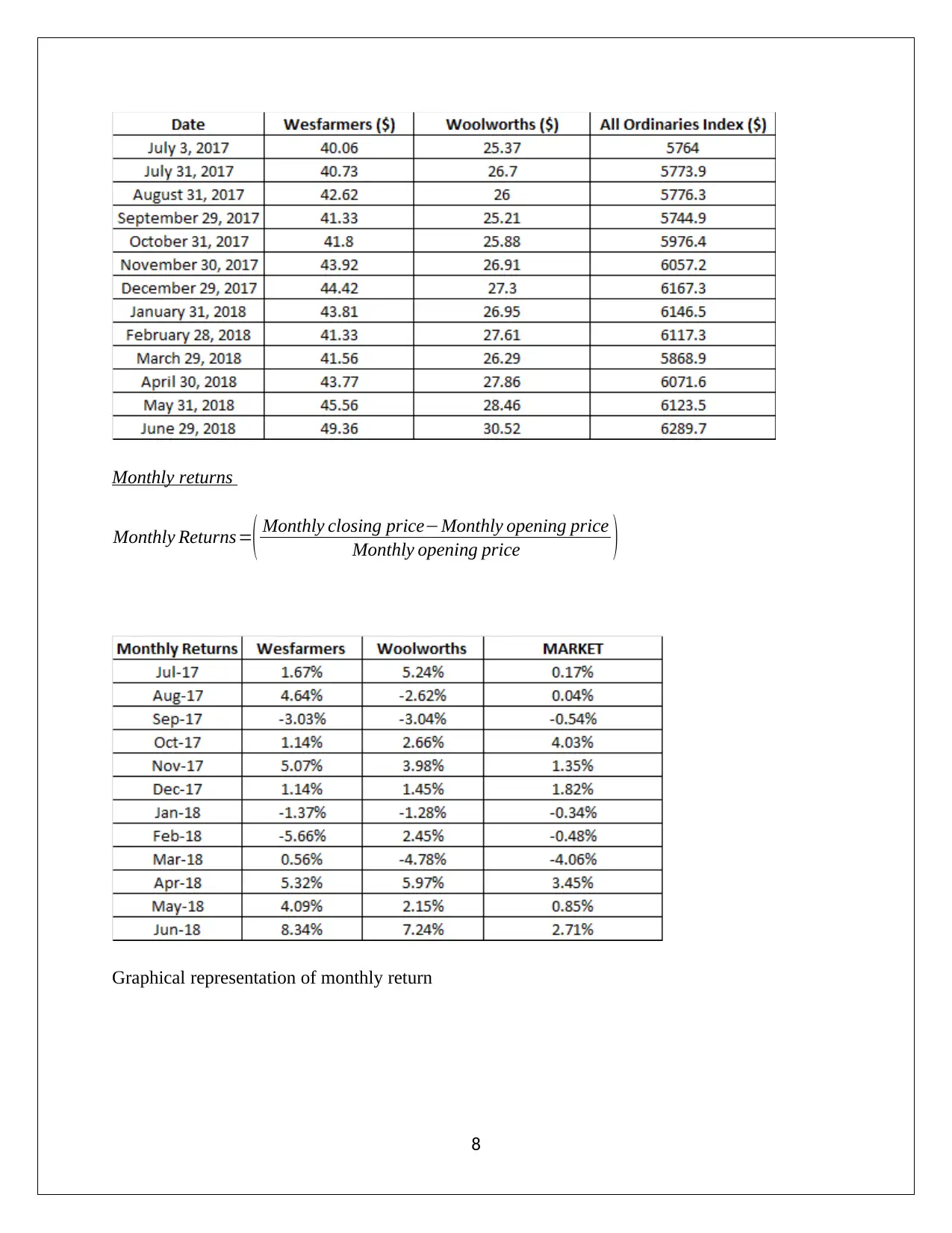

(i) Monthly holding period returns for Income year 2017/18 for Woolworths (WOW),

Wesfarmers (WES) and market (MKT) (All ordinaries index) is highlighted below.

Monthly prices

7

2015).

The above discussion clearly hints that corporate tax reduction would be useful only for foreign

companies. However, for more foreign investment to happen in Australia, it is noteworthy that

there are other factors besides tax that are considered by these investors. In primary and tertiary

sectors, Australia already has significant presence of foreign and domestic players. It is the

manufacturing sector that is lagging in Australia. But the same faces headwinds owing to limited

customer base, geographical isolation along with high cost of labour. It is unlikely that by

lowering tax rate, significant investments would happen in this regards. Besides, it needs to be

considered that the Australian taxation system also offers generous deductions which contribute

to effective tax rate in Australia being comparable or lower than the developed world

(Montgomery, 2018). Also, the current timing for corporate tax cuts may not be recommended

considering that fiscally the recent times have been challenging owing to falling mining related

exports to China and rising social security expenses (Taylor, 2018).

Owing to the discussion above, it can be concluded that the reduction in corporate tax is unlikely

to bring any significant tangible gains for the economy as the domestic companies would not be

much impacted while the foreign investments may still be limited owing to other associated

disadvantages besides tax structure. The existing foreign companies may be the prime

beneficiaries and the government may experience a shortfall in revenues which could further

worsen the already delicate fiscal position in Australia.

Question 4

(i) Monthly holding period returns for Income year 2017/18 for Woolworths (WOW),

Wesfarmers (WES) and market (MKT) (All ordinaries index) is highlighted below.

Monthly prices

7

Monthly returns

Monthly Returns=( Monthly closing price−Monthly opening price

Monthly opening price )

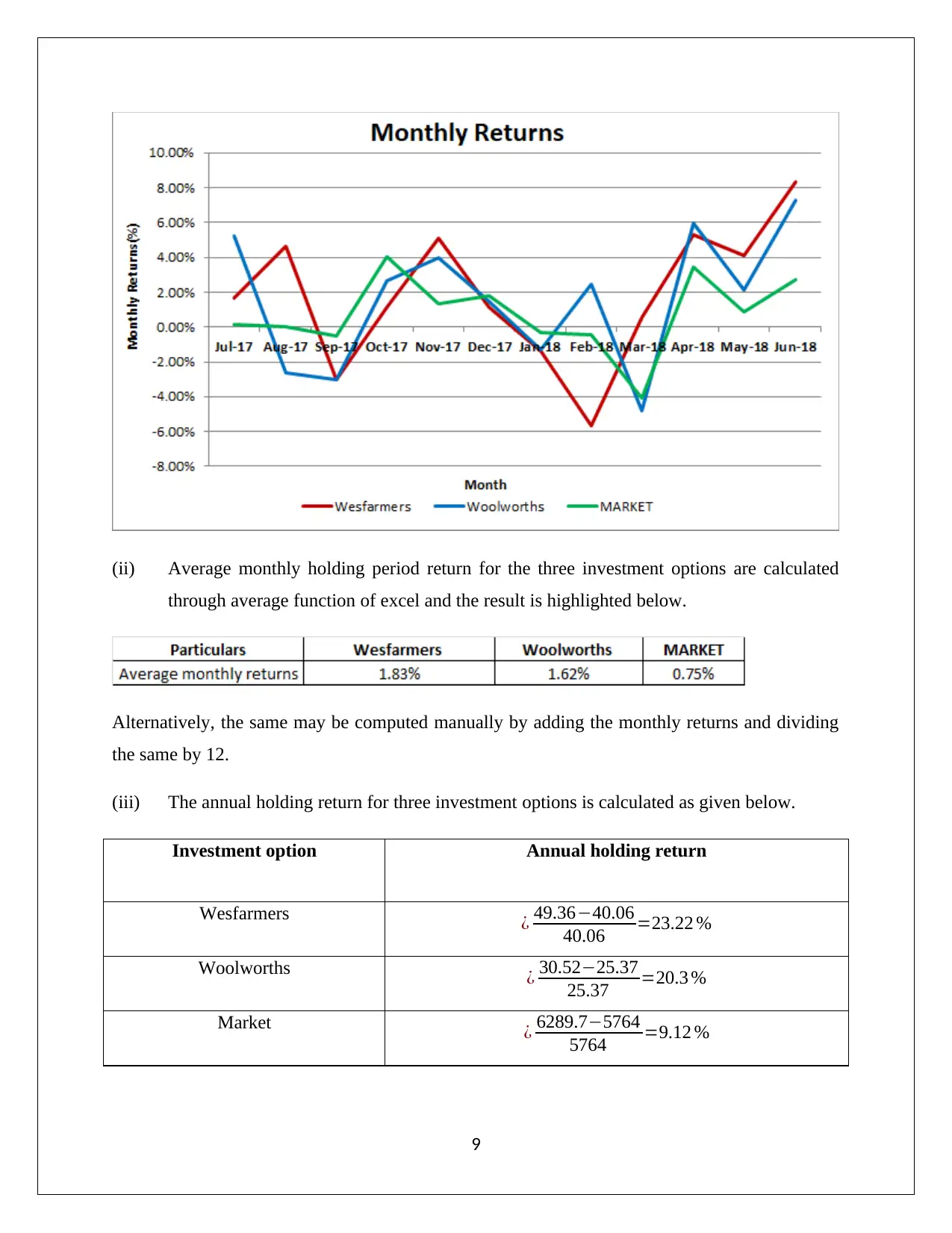

Graphical representation of monthly return

8

Monthly Returns=( Monthly closing price−Monthly opening price

Monthly opening price )

Graphical representation of monthly return

8

(ii) Average monthly holding period return for the three investment options are calculated

through average function of excel and the result is highlighted below.

Alternatively, the same may be computed manually by adding the monthly returns and dividing

the same by 12.

(iii) The annual holding return for three investment options is calculated as given below.

Investment option Annual holding return

Wesfarmers ¿ 49.36−40.06

40.06 =23.22 %

Woolworths ¿ 30.52−25.37

25.37 =20.3 %

Market ¿ 6289.7−5764

5764 =9.12 %

9

through average function of excel and the result is highlighted below.

Alternatively, the same may be computed manually by adding the monthly returns and dividing

the same by 12.

(iii) The annual holding return for three investment options is calculated as given below.

Investment option Annual holding return

Wesfarmers ¿ 49.36−40.06

40.06 =23.22 %

Woolworths ¿ 30.52−25.37

25.37 =20.3 %

Market ¿ 6289.7−5764

5764 =9.12 %

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

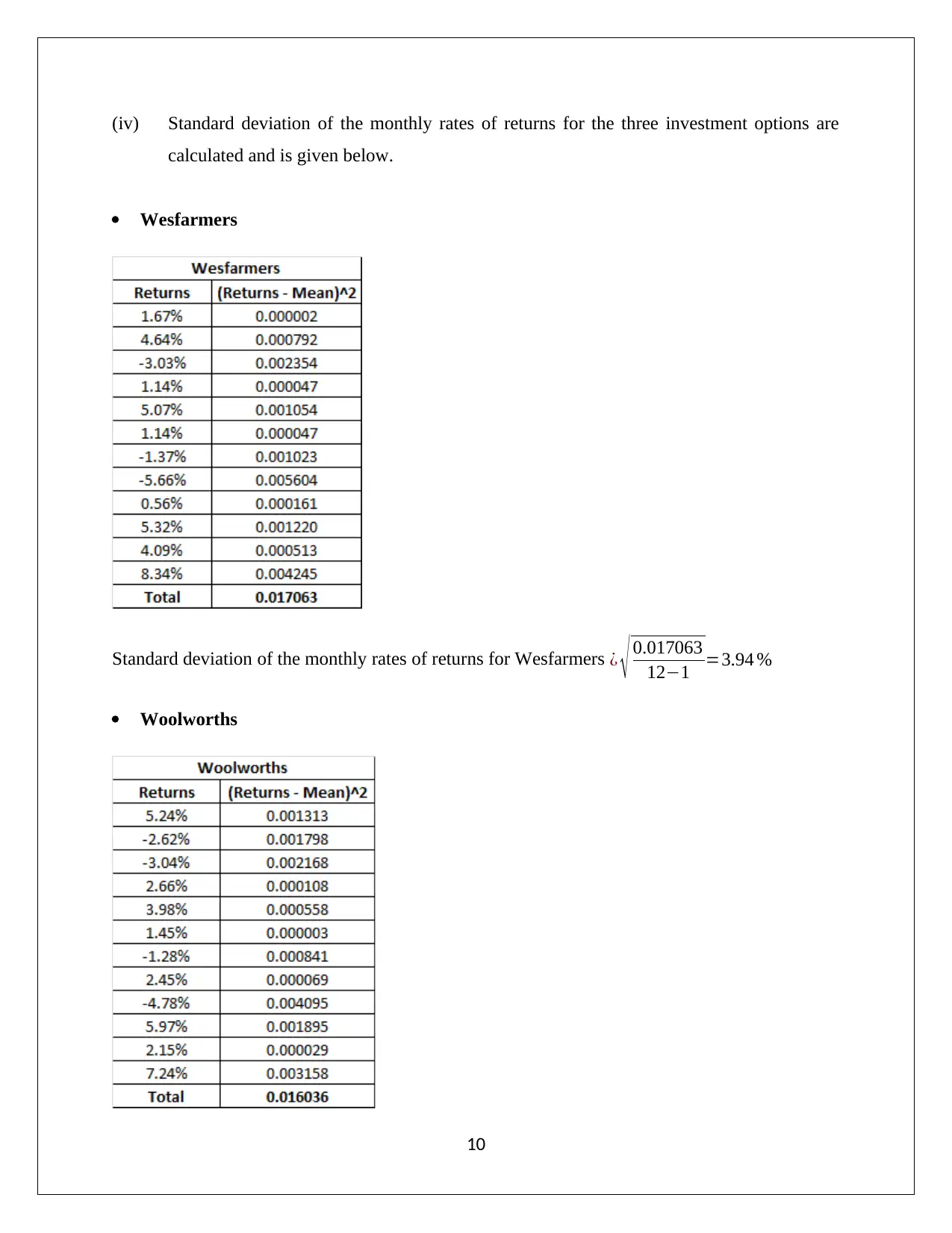

(iv) Standard deviation of the monthly rates of returns for the three investment options are

calculated and is given below.

Wesfarmers

Standard deviation of the monthly rates of returns for Wesfarmers ¿ √ 0.017063

12−1 =3.94 %

Woolworths

10

calculated and is given below.

Wesfarmers

Standard deviation of the monthly rates of returns for Wesfarmers ¿ √ 0.017063

12−1 =3.94 %

Woolworths

10

Standard deviation of the monthly rates of returns for Woolworths ¿ √ 0.016063

12−1 =3.82%

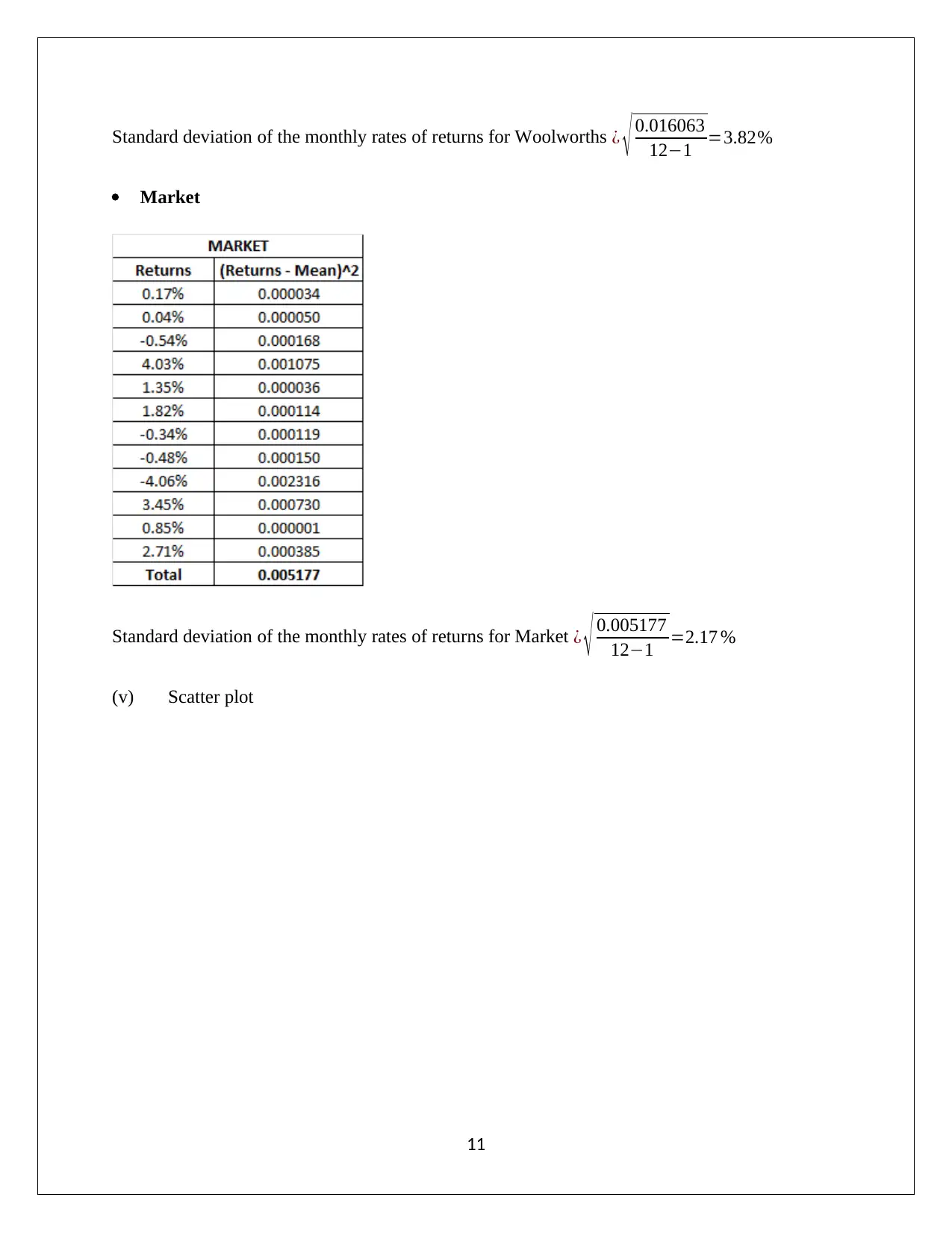

Market

Standard deviation of the monthly rates of returns for Market ¿ √ 0.005177

12−1 =2.17 %

(v) Scatter plot

11

12−1 =3.82%

Market

Standard deviation of the monthly rates of returns for Market ¿ √ 0.005177

12−1 =2.17 %

(v) Scatter plot

11

(vi) Capital Asset Pricing Model (CAPM) model to find the expected returns for Woolworths

and Wesfarmers is calculated below (Parrino & Kidwell, 2014).

Expected Returns=Risk Free Rate +(β∗Market Risk Premium)

Expected Returns

Woolworths (WOW) ¿ 2+( 0.77∗(5.75−2))=4.89 % p . a .

Wesfarmers (WES) ¿ 2+( 0.81∗(5.75−2))=5.04 % p . a .

(vii) Security market line

12

and Wesfarmers is calculated below (Parrino & Kidwell, 2014).

Expected Returns=Risk Free Rate +(β∗Market Risk Premium)

Expected Returns

Woolworths (WOW) ¿ 2+( 0.77∗(5.75−2))=4.89 % p . a .

Wesfarmers (WES) ¿ 2+( 0.81∗(5.75−2))=5.04 % p . a .

(vii) Security market line

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be said that market is overvalued while, Woolworths and Wesfarmers are undervalued

which is apparent from the above shown security market line. This is because, the two stocks are

located above the SML while the market is located just below the SML (Arnold, 2015).

(viii) Estmiated return and beta of the portfolio

Woolworths = 30%

Wesfarmers = 70%

Beta of portfolio= ( 30 %∗βWoolworths ) + ( 70 %∗βWesfarmers )

Beta of portfolio= ( 30 %∗0.77 )+ ( 70 %∗0.81 )=0.80

Further,

Return of portfolio ¿ ( 30 %∗RWoolworths ) + ( 70 %∗RWesfarmers )

Return of portfolio ¿ ( 30 %∗1.62 ) + ( 70 %∗1.83 ) =1.76 % per month

13

which is apparent from the above shown security market line. This is because, the two stocks are

located above the SML while the market is located just below the SML (Arnold, 2015).

(viii) Estmiated return and beta of the portfolio

Woolworths = 30%

Wesfarmers = 70%

Beta of portfolio= ( 30 %∗βWoolworths ) + ( 70 %∗βWesfarmers )

Beta of portfolio= ( 30 %∗0.77 )+ ( 70 %∗0.81 )=0.80

Further,

Return of portfolio ¿ ( 30 %∗RWoolworths ) + ( 70 %∗RWesfarmers )

Return of portfolio ¿ ( 30 %∗1.62 ) + ( 70 %∗1.83 ) =1.76 % per month

13

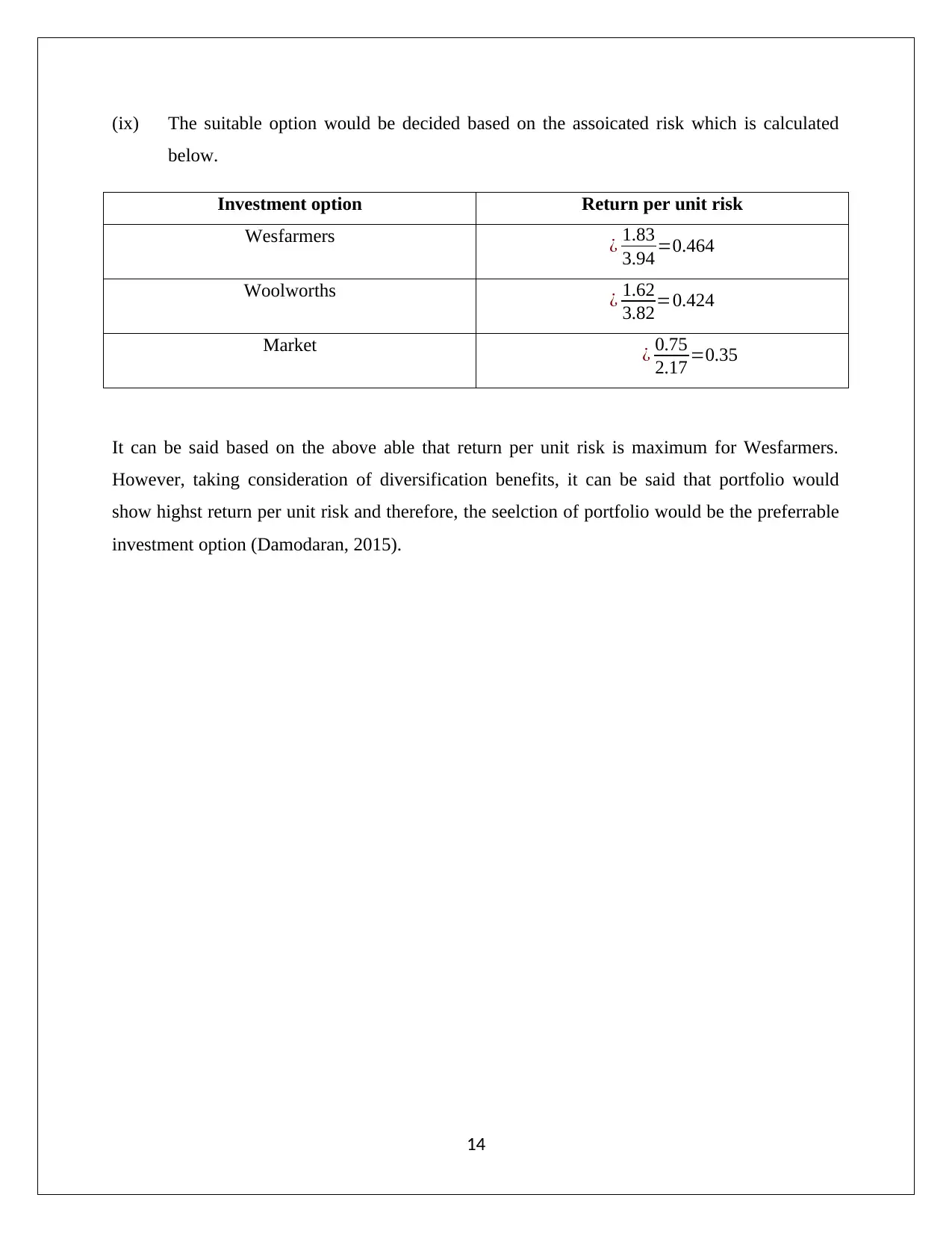

(ix) The suitable option would be decided based on the assoicated risk which is calculated

below.

Investment option Return per unit risk

Wesfarmers ¿ 1.83

3.94 =0.464

Woolworths ¿ 1.62

3.82=0.424

Market ¿ 0.75

2.17 =0.35

It can be said based on the above able that return per unit risk is maximum for Wesfarmers.

However, taking consideration of diversification benefits, it can be said that portfolio would

show highst return per unit risk and therefore, the seelction of portfolio would be the preferrable

investment option (Damodaran, 2015).

14

below.

Investment option Return per unit risk

Wesfarmers ¿ 1.83

3.94 =0.464

Woolworths ¿ 1.62

3.82=0.424

Market ¿ 0.75

2.17 =0.35

It can be said based on the above able that return per unit risk is maximum for Wesfarmers.

However, taking consideration of diversification benefits, it can be said that portfolio would

show highst return per unit risk and therefore, the seelction of portfolio would be the preferrable

investment option (Damodaran, 2015).

14

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley,

John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

Taylor, D. (2018, March 29). Corporate tax cuts: What are the key issues in the

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

15

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley,

John & Sons.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Montgomery, R. (2018, February, 19).Should Australia cut the corporate tax rate ? Retrieved

from https://rogermontgomery.com/should-australia-cut-the-corporate-tax-rate/

Smith , W. (2015, February 10). FactCheck: is Australia’s corporate tax rate not competitive

with the rest of the region. Retrieved from https://theconversation.com/factcheck-is-

australias-corporate-tax-rate-not-competitive-with-the-rest-of-the-region-37226

Taylor, D. (2018, March 29). Corporate tax cuts: What are the key issues in the

debate? Retrieved from http://www.abc.net.au/news/2018-03-29/corporate-tax-cuts-

explained/9600004

15

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.