Accounting and Financial Analysis: Business Start-up to Statements

VerifiedAdded on 2023/06/17

|10

|1665

|241

Report

AI Summary

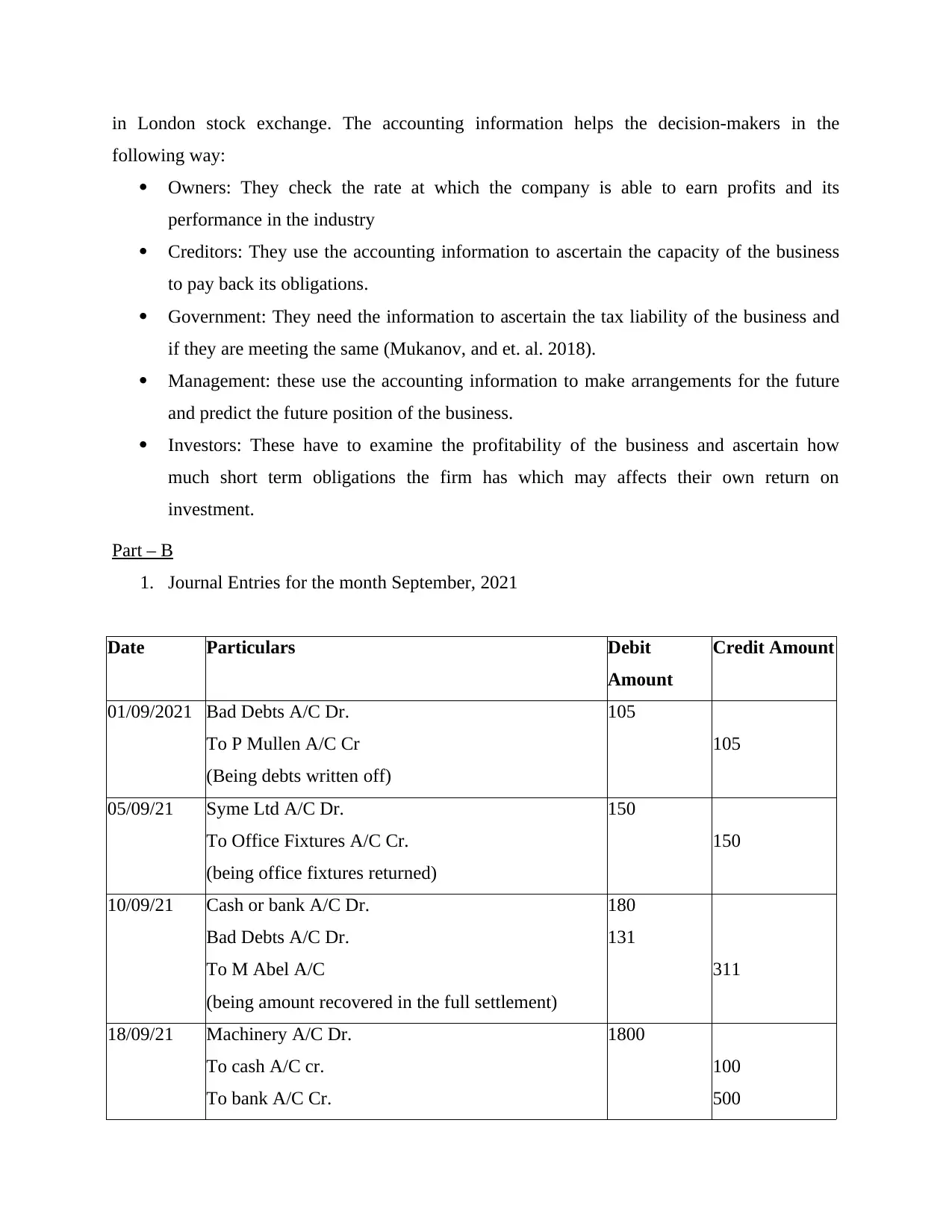

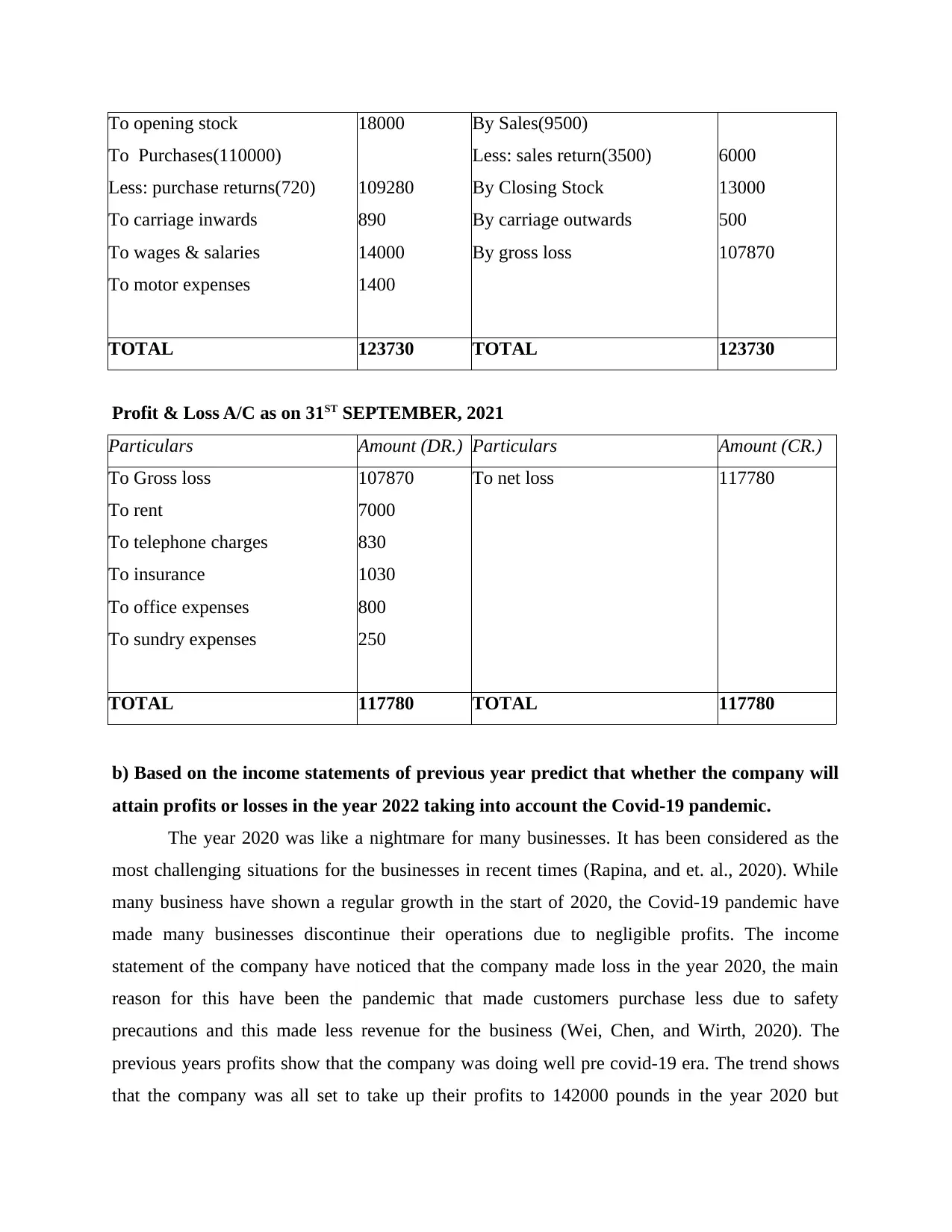

This report explores the accounting practices involved in starting a business, focusing on the steps an entrepreneur takes to establish a new venture, such as formulating a business model, building a strategy, and securing necessary equipment. It highlights the role of accounting in decision-making, using Tesco as an example to illustrate how owners, creditors, government, management, and investors utilize accounting information. The report includes practical exercises like preparing journal entries and ledger accounts for a hypothetical business scenario, culminating in the creation of an income statement. Furthermore, it analyzes the potential impact of events like the COVID-19 pandemic on a company's profitability, emphasizing the importance of adapting to changing market conditions. The report concludes by underscoring the significance of a well-formulated business strategy and accurate financial record-keeping in reflecting a company's financial health. Desklib provides additional resources, including past papers and solved assignments, for further study.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.