Financial Statement Analysis Report of British Land - AC4410

VerifiedAdded on 2023/06/15

|11

|1849

|423

Report

AI Summary

This report presents a financial analysis of British Land, a leading UK commercial property company, utilizing ratio analysis to assess its performance. The analysis covers profitability ratios (gross profit margin, operating profit margin, return on capital employed), liquidity ratios (current ratio, quick ratio), and gearing ratios (gearing ratio, interest coverage ratio) for the years 2014-2017. The report concludes that British Land is in a stable position regarding profitability, liquidity, and solvency, but suggests improvements such as managing short-term liabilities and favoring equity over debt financing for future funding. The analysis is based on the company's financial statements and aims to provide insights into its financial health and potential areas for improvement.

Running head: ACCOUNTING FINANCIAL ANALYSIS REPORT

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYSIS REPORT

Table of Contents

1.0 Introduction.....................................................................................................................2

2.0 Ratio analysis..................................................................................................................2

2.1 Advantages of ratio analysis............................................................................................2

2.2 Limitations of ratio analysis.............................................................................................3

3.0 Profitability ratios.................................................................................................................3

3.1 Gross profit ratio..............................................................................................................4

3.2 Operating profit ratio........................................................................................................4

3.3 Return on capital employed.............................................................................................4

4.0 Liquidity ratio.......................................................................................................................4

4.1 Current ratio.....................................................................................................................5

4.2 Quick ratio........................................................................................................................5

5.0 Gearing ratio.........................................................................................................................6

5.1 Gearing ratio.....................................................................................................................6

5.2 Interest coverage ratio......................................................................................................7

6.0 Conclusion............................................................................................................................7

7.0 References............................................................................................................................8

8.0 Appendix..............................................................................................................................9

Table of Contents

1.0 Introduction.....................................................................................................................2

2.0 Ratio analysis..................................................................................................................2

2.1 Advantages of ratio analysis............................................................................................2

2.2 Limitations of ratio analysis.............................................................................................3

3.0 Profitability ratios.................................................................................................................3

3.1 Gross profit ratio..............................................................................................................4

3.2 Operating profit ratio........................................................................................................4

3.3 Return on capital employed.............................................................................................4

4.0 Liquidity ratio.......................................................................................................................4

4.1 Current ratio.....................................................................................................................5

4.2 Quick ratio........................................................................................................................5

5.0 Gearing ratio.........................................................................................................................6

5.1 Gearing ratio.....................................................................................................................6

5.2 Interest coverage ratio......................................................................................................7

6.0 Conclusion............................................................................................................................7

7.0 References............................................................................................................................8

8.0 Appendix..............................................................................................................................9

2ACCOUNTING FINANCIAL ANALYSIS REPORT

1.0 Introduction

British Land is the leading company in UK for providing commercial property related

services and it is focussed on London retail and high quality retail. The main strategy of the

company is to deliver the places that meet the requirement of the customers and it takes the

responsibility for changing the lifestyle places that are preferred by the people. The

company’s portfolio delivers attractive places for shop, work and lives. Further, the company

is focussed on the local and regional multi-let assets that are in tune with the modern lifestyle

of the consumers. It further offers well managed, well connected and attractive environment

(Britishland.com 2018).

2.0 Ratio analysis

Ratio analysis is the analysis of financial statement and is used for obtaining quick

information regarding the financial performance of the company. Ratios are segregated into

various categories like debt management ratio, market value ratio, profitability ratio, and

solvency ratio and return ratios for analysing the profitability, liquidity, efficiency and

solvency position of the company (Brigham and Ehrhardt 2013).

2.1 Advantages of ratio analysis

Various advantages of ratio analysis are as follows –

It states the company’s financial position that helps the financial institutions, banks,

creditors and potential investors to take various important decisions.

The accounting figures can be simplified, systematized and summarised through the

ratios and it helps to make the users understandable the performance in lucid form.

1.0 Introduction

British Land is the leading company in UK for providing commercial property related

services and it is focussed on London retail and high quality retail. The main strategy of the

company is to deliver the places that meet the requirement of the customers and it takes the

responsibility for changing the lifestyle places that are preferred by the people. The

company’s portfolio delivers attractive places for shop, work and lives. Further, the company

is focussed on the local and regional multi-let assets that are in tune with the modern lifestyle

of the consumers. It further offers well managed, well connected and attractive environment

(Britishland.com 2018).

2.0 Ratio analysis

Ratio analysis is the analysis of financial statement and is used for obtaining quick

information regarding the financial performance of the company. Ratios are segregated into

various categories like debt management ratio, market value ratio, profitability ratio, and

solvency ratio and return ratios for analysing the profitability, liquidity, efficiency and

solvency position of the company (Brigham and Ehrhardt 2013).

2.1 Advantages of ratio analysis

Various advantages of ratio analysis are as follows –

It states the company’s financial position that helps the financial institutions, banks,

creditors and potential investors to take various important decisions.

The accounting figures can be simplified, systematized and summarised through the

ratios and it helps to make the users understandable the performance in lucid form.

You're viewing a preview

Unlock full access by subscribing today!

3ACCOUNTING FINANCIAL ANALYSIS REPORT

It helps to have an idea regarding the operation of the company and further helps the

management to analyse the financial requirements and capabilities for different units

of the business.

2.2 Limitations of ratio analysis

Inspite of various advantages ratio analysis has various drawbacks. These are –

Ratios are useful when they are compared with the past performances over the long

run or against the peers in the same industry. However, the information regarding

peers or past information may not be available always.

Ratios do not take into consideration the other important factors like customer service,

product quality and morale of the employee that have huge influence on the financial

performances (Delen, Kuzey and Uyar 2013).

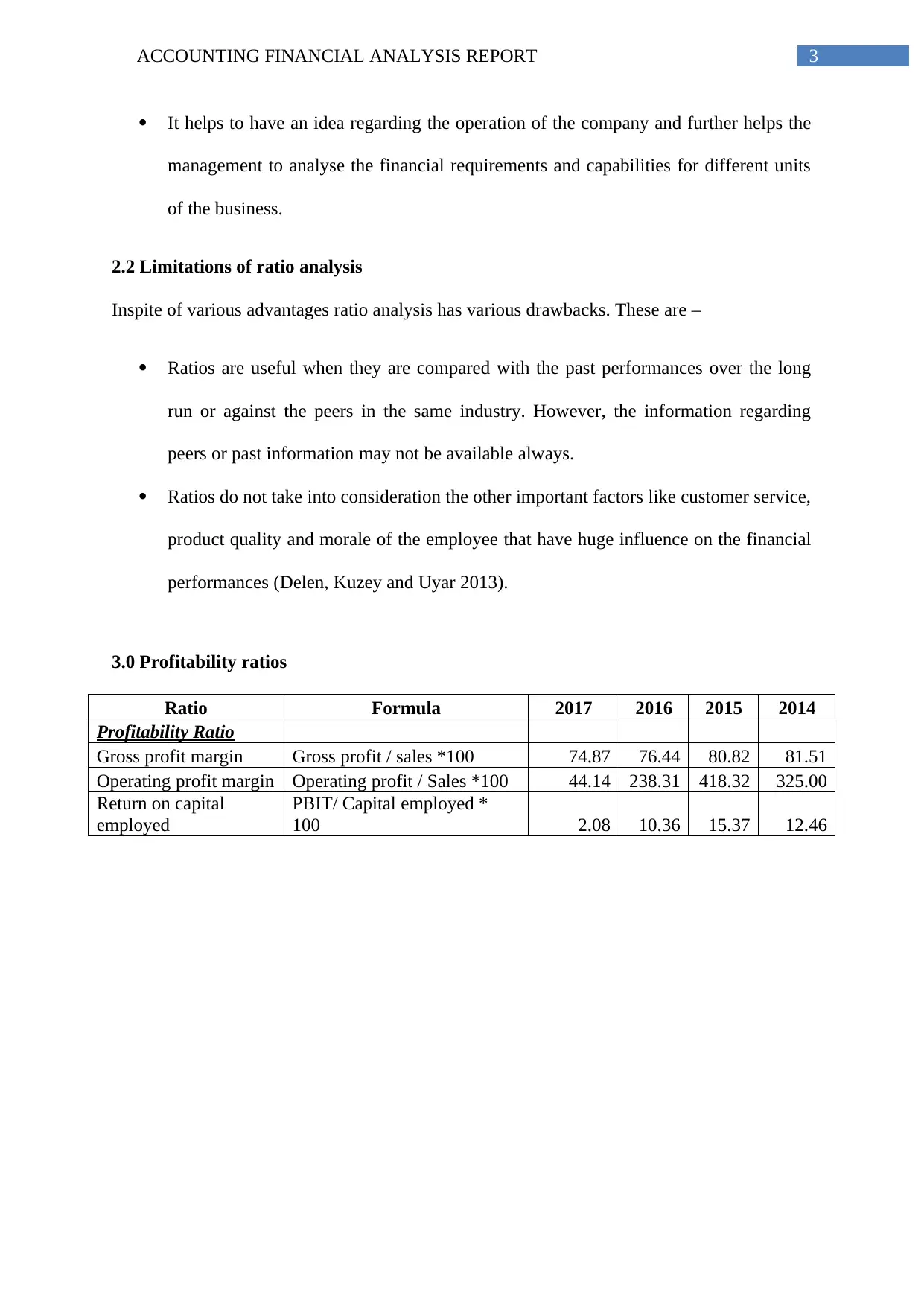

3.0 Profitability ratios

Ratio Formula 2017 2016 2015 2014

Profitability Ratio

Gross profit margin Gross profit / sales *100 74.87 76.44 80.82 81.51

Operating profit margin Operating profit / Sales *100 44.14 238.31 418.32 325.00

Return on capital

employed

PBIT/ Capital employed *

100 2.08 10.36 15.37 12.46

It helps to have an idea regarding the operation of the company and further helps the

management to analyse the financial requirements and capabilities for different units

of the business.

2.2 Limitations of ratio analysis

Inspite of various advantages ratio analysis has various drawbacks. These are –

Ratios are useful when they are compared with the past performances over the long

run or against the peers in the same industry. However, the information regarding

peers or past information may not be available always.

Ratios do not take into consideration the other important factors like customer service,

product quality and morale of the employee that have huge influence on the financial

performances (Delen, Kuzey and Uyar 2013).

3.0 Profitability ratios

Ratio Formula 2017 2016 2015 2014

Profitability Ratio

Gross profit margin Gross profit / sales *100 74.87 76.44 80.82 81.51

Operating profit margin Operating profit / Sales *100 44.14 238.31 418.32 325.00

Return on capital

employed

PBIT/ Capital employed *

100 2.08 10.36 15.37 12.46

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYSIS REPORT

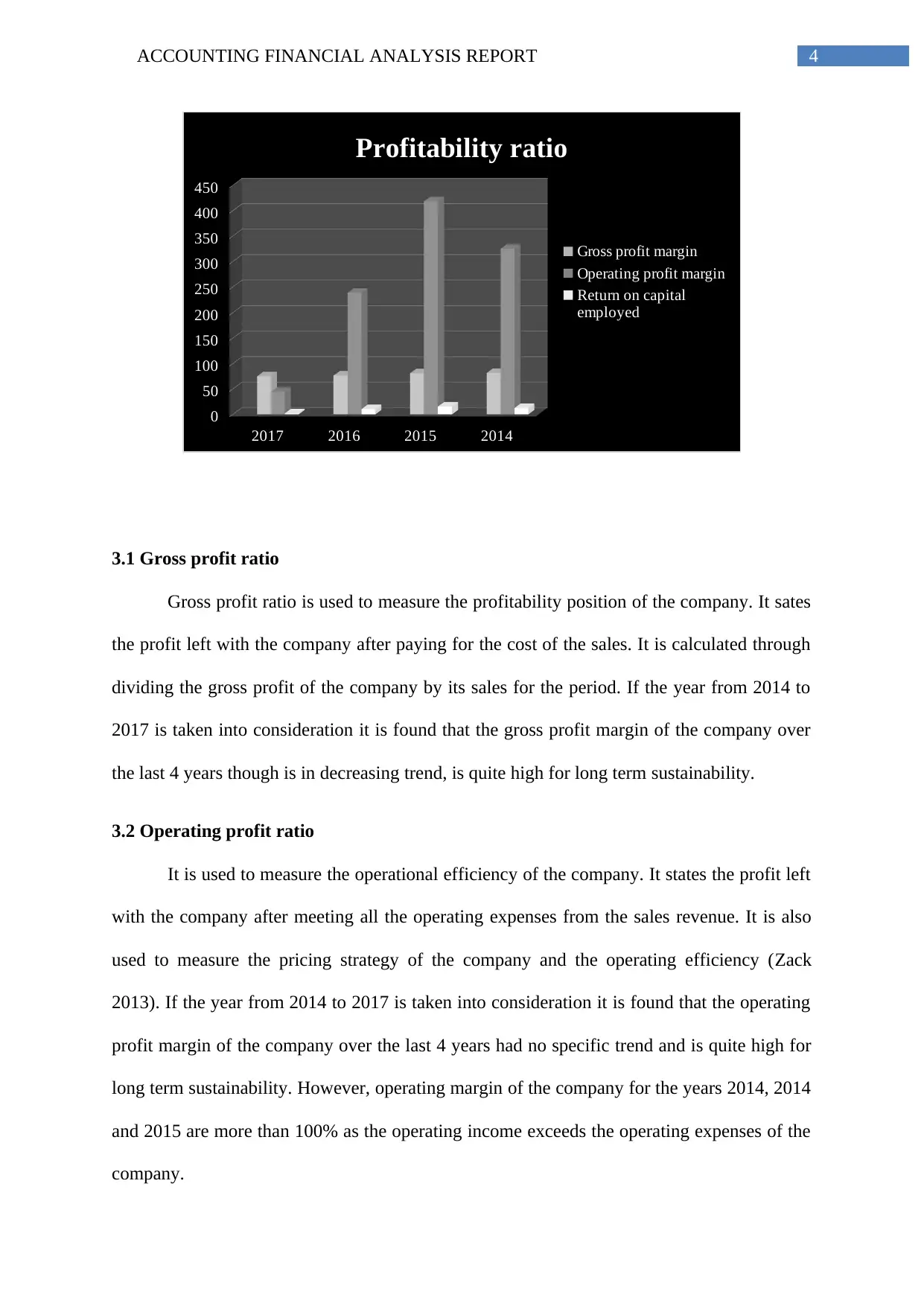

2017 2016 2015 2014

0

50

100

150

200

250

300

350

400

450

Profitability ratio

Gross profit margin

Operating profit margin

Return on capital

employed

3.1 Gross profit ratio

Gross profit ratio is used to measure the profitability position of the company. It sates

the profit left with the company after paying for the cost of the sales. It is calculated through

dividing the gross profit of the company by its sales for the period. If the year from 2014 to

2017 is taken into consideration it is found that the gross profit margin of the company over

the last 4 years though is in decreasing trend, is quite high for long term sustainability.

3.2 Operating profit ratio

It is used to measure the operational efficiency of the company. It states the profit left

with the company after meeting all the operating expenses from the sales revenue. It is also

used to measure the pricing strategy of the company and the operating efficiency (Zack

2013). If the year from 2014 to 2017 is taken into consideration it is found that the operating

profit margin of the company over the last 4 years had no specific trend and is quite high for

long term sustainability. However, operating margin of the company for the years 2014, 2014

and 2015 are more than 100% as the operating income exceeds the operating expenses of the

company.

2017 2016 2015 2014

0

50

100

150

200

250

300

350

400

450

Profitability ratio

Gross profit margin

Operating profit margin

Return on capital

employed

3.1 Gross profit ratio

Gross profit ratio is used to measure the profitability position of the company. It sates

the profit left with the company after paying for the cost of the sales. It is calculated through

dividing the gross profit of the company by its sales for the period. If the year from 2014 to

2017 is taken into consideration it is found that the gross profit margin of the company over

the last 4 years though is in decreasing trend, is quite high for long term sustainability.

3.2 Operating profit ratio

It is used to measure the operational efficiency of the company. It states the profit left

with the company after meeting all the operating expenses from the sales revenue. It is also

used to measure the pricing strategy of the company and the operating efficiency (Zack

2013). If the year from 2014 to 2017 is taken into consideration it is found that the operating

profit margin of the company over the last 4 years had no specific trend and is quite high for

long term sustainability. However, operating margin of the company for the years 2014, 2014

and 2015 are more than 100% as the operating income exceeds the operating expenses of the

company.

5ACCOUNTING FINANCIAL ANALYSIS REPORT

3.3 Return on capital employed

Return on capital employed that is expressed in percentage form complements return

on equity ratio through adding the debt liabilities of the company or the borrowed capital to

the equity for reflecting the total capital employed of the company (Vogel 2014). Looking

into the calculation table it can be found that the return on capital employed of the company

though increased from 12.46 to 15.37 over the years from 2014 to 2015. However, from after

2015 till the year 2017 it is in decreasing trend.

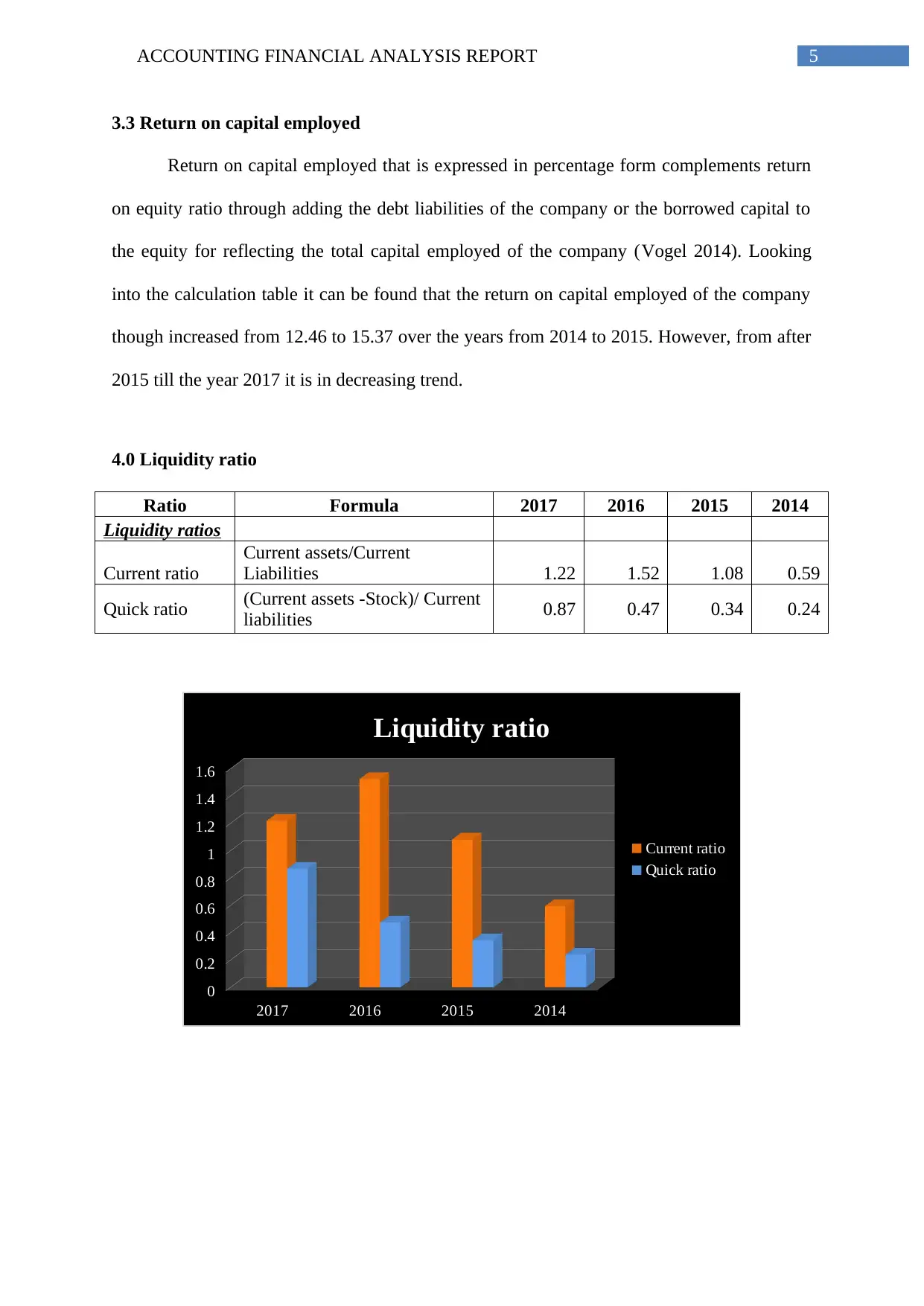

4.0 Liquidity ratio

Ratio Formula 2017 2016 2015 2014

Liquidity ratios

Current ratio

Current assets/Current

Liabilities 1.22 1.52 1.08 0.59

Quick ratio (Current assets -Stock)/ Current

liabilities 0.87 0.47 0.34 0.24

2017 2016 2015 2014

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Liquidity ratio

Current ratio

Quick ratio

3.3 Return on capital employed

Return on capital employed that is expressed in percentage form complements return

on equity ratio through adding the debt liabilities of the company or the borrowed capital to

the equity for reflecting the total capital employed of the company (Vogel 2014). Looking

into the calculation table it can be found that the return on capital employed of the company

though increased from 12.46 to 15.37 over the years from 2014 to 2015. However, from after

2015 till the year 2017 it is in decreasing trend.

4.0 Liquidity ratio

Ratio Formula 2017 2016 2015 2014

Liquidity ratios

Current ratio

Current assets/Current

Liabilities 1.22 1.52 1.08 0.59

Quick ratio (Current assets -Stock)/ Current

liabilities 0.87 0.47 0.34 0.24

2017 2016 2015 2014

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Liquidity ratio

Current ratio

Quick ratio

You're viewing a preview

Unlock full access by subscribing today!

6ACCOUNTING FINANCIAL ANALYSIS REPORT

4.1 Current ratio

It is used to analyse the company’s liquidity position. It measures the efficiency of the

company regarding payment of the short-term dues with the current assets. Current ratio is

calculated through dividing the current assets by the current liabilities of the company. It is

found that except for the year 2014 the current ratio of the company for all 3 past years is

ranged between 1.08 and 1.52 and seems to be efficient.

4.2 Quick ratio

Like the current ratio the quick ratio is also used to measure the liquidity position of

the company. The only difference between the current ratio and quick ratio is that under

quick ratio the current assets that can be converted into cash quickly are only considered

(Uechi et al. 2015). The quick ratio of the company over the last 4 years are in increasing

trend and increased from 0.24 to 0.87 over the years from 2014 to 2017.

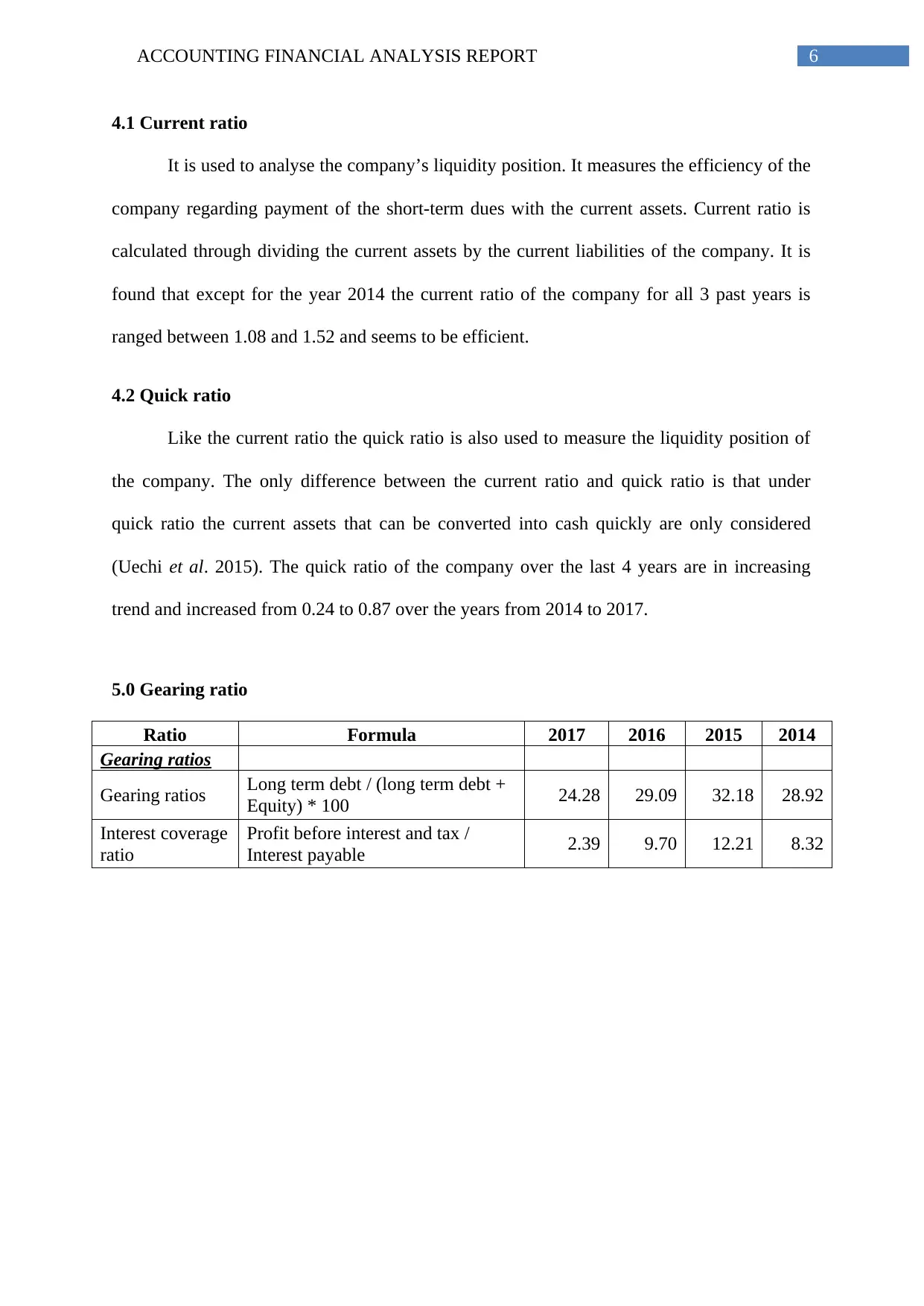

5.0 Gearing ratio

Ratio Formula 2017 2016 2015 2014

Gearing ratios

Gearing ratios Long term debt / (long term debt +

Equity) * 100 24.28 29.09 32.18 28.92

Interest coverage

ratio

Profit before interest and tax /

Interest payable 2.39 9.70 12.21 8.32

4.1 Current ratio

It is used to analyse the company’s liquidity position. It measures the efficiency of the

company regarding payment of the short-term dues with the current assets. Current ratio is

calculated through dividing the current assets by the current liabilities of the company. It is

found that except for the year 2014 the current ratio of the company for all 3 past years is

ranged between 1.08 and 1.52 and seems to be efficient.

4.2 Quick ratio

Like the current ratio the quick ratio is also used to measure the liquidity position of

the company. The only difference between the current ratio and quick ratio is that under

quick ratio the current assets that can be converted into cash quickly are only considered

(Uechi et al. 2015). The quick ratio of the company over the last 4 years are in increasing

trend and increased from 0.24 to 0.87 over the years from 2014 to 2017.

5.0 Gearing ratio

Ratio Formula 2017 2016 2015 2014

Gearing ratios

Gearing ratios Long term debt / (long term debt +

Equity) * 100 24.28 29.09 32.18 28.92

Interest coverage

ratio

Profit before interest and tax /

Interest payable 2.39 9.70 12.21 8.32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYSIS REPORT

2017 2016 2015 2014

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Gearing ratio

Gearing ratios

Interest coverage ratio

5.1 Gearing ratio

It is used to measure the solvency and efficiency of the company. It states the

percentage of total assets that are generated through borrowed funds and through owner’s

fund (Jordan 2014). The gearing ratio of the company for all the past 4 years was efficient as

for all the years the ratio is lower than 50%.

5.2 Interest coverage ratio

It states the profit left with the company to pay off the payable interest. It is found that

the interest coverage ratio of the company for the last 4 years is fluctuating. However, the

company has sufficient operating profit to cover up the due interest (Palepu, Healy and Peek

2013).

6.0 Conclusion

It can be concluded from the above analysis of various ratios that the with regard to

profitability, liquidity and solvency aspect the company is in stable position. However, if the

company wants to improve its financial position and performances further, it shall make

payment for the short-term liabilities; reduce the allowed credit period to the debtors. Further

2017 2016 2015 2014

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Gearing ratio

Gearing ratios

Interest coverage ratio

5.1 Gearing ratio

It is used to measure the solvency and efficiency of the company. It states the

percentage of total assets that are generated through borrowed funds and through owner’s

fund (Jordan 2014). The gearing ratio of the company for all the past 4 years was efficient as

for all the years the ratio is lower than 50%.

5.2 Interest coverage ratio

It states the profit left with the company to pay off the payable interest. It is found that

the interest coverage ratio of the company for the last 4 years is fluctuating. However, the

company has sufficient operating profit to cover up the due interest (Palepu, Healy and Peek

2013).

6.0 Conclusion

It can be concluded from the above analysis of various ratios that the with regard to

profitability, liquidity and solvency aspect the company is in stable position. However, if the

company wants to improve its financial position and performances further, it shall make

payment for the short-term liabilities; reduce the allowed credit period to the debtors. Further

8ACCOUNTING FINANCIAL ANALYSIS REPORT

to maintain the gearing balance it shall obtain the additional fund through equity instead of

debt.

to maintain the gearing balance it shall obtain the additional fund through equity instead of

debt.

You're viewing a preview

Unlock full access by subscribing today!

9ACCOUNTING FINANCIAL ANALYSIS REPORT

7.0 References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Britishland.com., 2018. Home. [online] Available at: http://www.britishland.com/ [Accessed

5 Apr. 2018].

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Zack, G.M., 2013. Financial Statement Analysis. Financial Statement Fraud: Strategies for

Detection and Investigation, pp.209-213.

7.0 References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Britishland.com., 2018. Home. [online] Available at: http://www.britishland.com/ [Accessed

5 Apr. 2018].

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Zack, G.M., 2013. Financial Statement Analysis. Financial Statement Fraud: Strategies for

Detection and Investigation, pp.209-213.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FINANCIAL ANALYSIS REPORT

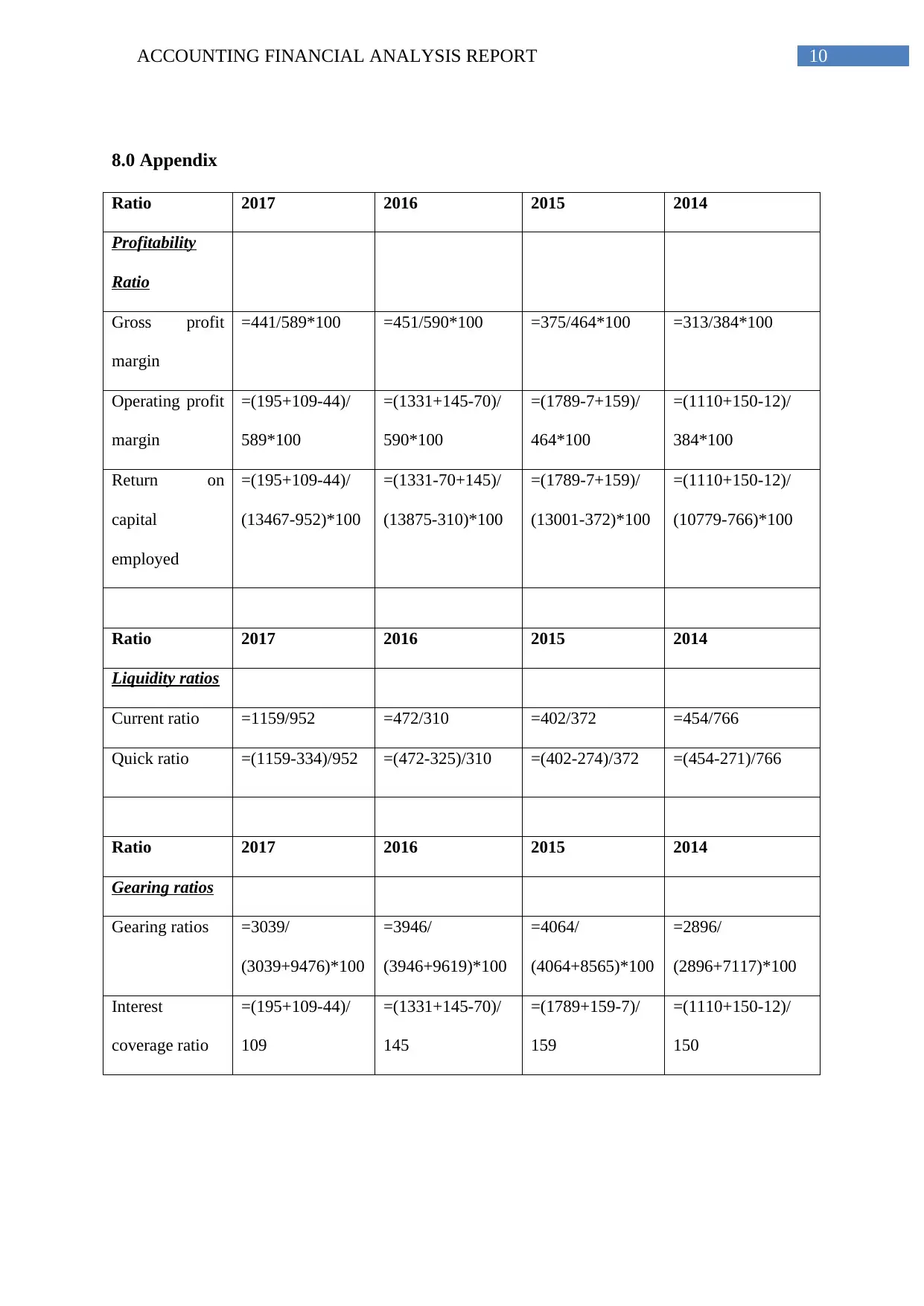

8.0 Appendix

Ratio 2017 2016 2015 2014

Profitability

Ratio

Gross profit

margin

=441/589*100 =451/590*100 =375/464*100 =313/384*100

Operating profit

margin

=(195+109-44)/

589*100

=(1331+145-70)/

590*100

=(1789-7+159)/

464*100

=(1110+150-12)/

384*100

Return on

capital

employed

=(195+109-44)/

(13467-952)*100

=(1331-70+145)/

(13875-310)*100

=(1789-7+159)/

(13001-372)*100

=(1110+150-12)/

(10779-766)*100

Ratio 2017 2016 2015 2014

Liquidity ratios

Current ratio =1159/952 =472/310 =402/372 =454/766

Quick ratio =(1159-334)/952 =(472-325)/310 =(402-274)/372 =(454-271)/766

Ratio 2017 2016 2015 2014

Gearing ratios

Gearing ratios =3039/

(3039+9476)*100

=3946/

(3946+9619)*100

=4064/

(4064+8565)*100

=2896/

(2896+7117)*100

Interest

coverage ratio

=(195+109-44)/

109

=(1331+145-70)/

145

=(1789+159-7)/

159

=(1110+150-12)/

150

8.0 Appendix

Ratio 2017 2016 2015 2014

Profitability

Ratio

Gross profit

margin

=441/589*100 =451/590*100 =375/464*100 =313/384*100

Operating profit

margin

=(195+109-44)/

589*100

=(1331+145-70)/

590*100

=(1789-7+159)/

464*100

=(1110+150-12)/

384*100

Return on

capital

employed

=(195+109-44)/

(13467-952)*100

=(1331-70+145)/

(13875-310)*100

=(1789-7+159)/

(13001-372)*100

=(1110+150-12)/

(10779-766)*100

Ratio 2017 2016 2015 2014

Liquidity ratios

Current ratio =1159/952 =472/310 =402/372 =454/766

Quick ratio =(1159-334)/952 =(472-325)/310 =(402-274)/372 =(454-271)/766

Ratio 2017 2016 2015 2014

Gearing ratios

Gearing ratios =3039/

(3039+9476)*100

=3946/

(3946+9619)*100

=4064/

(4064+8565)*100

=2896/

(2896+7117)*100

Interest

coverage ratio

=(195+109-44)/

109

=(1331+145-70)/

145

=(1789+159-7)/

159

=(1110+150-12)/

150

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.