In-Depth Accounting Financial Analysis Report of Electricity Firms

VerifiedAdded on 2023/06/15

|9

|2014

|497

Report

AI Summary

This report provides an in-depth financial analysis of St Lucia Electricity Services and Dominica Electricity, focusing on key financial ratios such as liquidity, profitability, capital structure, and market performance. It includes a comparative analysis of these ratios, along with share and bond evaluations. The report computes current ratios, return on equity, debt ratios, and price-earnings ratios to assess the financial health and investment potential of both companies. The share evaluation calculates the market value of shares based on dividend payments and growth rates, while the bond evaluation determines the price at which bonds will trade in the market. The analysis concludes that Dominica Electricity demonstrates a higher return on equity, making it a potentially more attractive investment for shareholders.

Running head: ACCOUNTING FINANCIAL ANALYSIS REPORT

Accounting Financial Analysis Report

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Financial Analysis Report

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYSIS REPORT

Table of Contents

Part 1:.........................................................................................................................................2

Introduction:...............................................................................................................................2

Ratio Analysis............................................................................................................................2

Liquidity Ratio: Current Ratio...................................................................................................2

Profitability ratio: Return on Equity..........................................................................................3

Capital Structure Ratio: Debt Ratio:..........................................................................................3

Market Performance Ratio: Price Earnings:..............................................................................4

Part 2: Share Evaluation.............................................................................................................5

Part 3: Bond Evaluation.............................................................................................................6

Part 4: Conclusion:.....................................................................................................................6

Reference List:...........................................................................................................................8

Table of Contents

Part 1:.........................................................................................................................................2

Introduction:...............................................................................................................................2

Ratio Analysis............................................................................................................................2

Liquidity Ratio: Current Ratio...................................................................................................2

Profitability ratio: Return on Equity..........................................................................................3

Capital Structure Ratio: Debt Ratio:..........................................................................................3

Market Performance Ratio: Price Earnings:..............................................................................4

Part 2: Share Evaluation.............................................................................................................5

Part 3: Bond Evaluation.............................................................................................................6

Part 4: Conclusion:.....................................................................................................................6

Reference List:...........................................................................................................................8

2ACCOUNTING FINANCIAL ANALYSIS REPORT

Part 1:

Introduction:

The current study is based on the analysis of the ratio relating to the publicly listed

non-financial organizations that are from the same industry. An in depth analysis of the St

Lucia Electricity Services and Dominica Electricity will be performed. A comparative

analysis of the profitability ratio, liquidity ratio, capital structure ratio and market price ratio

will be performed. An interpretation of the ratio will be provided with the theoretical

concepts by comparing the same with the industry peer.

Ratio Analysis

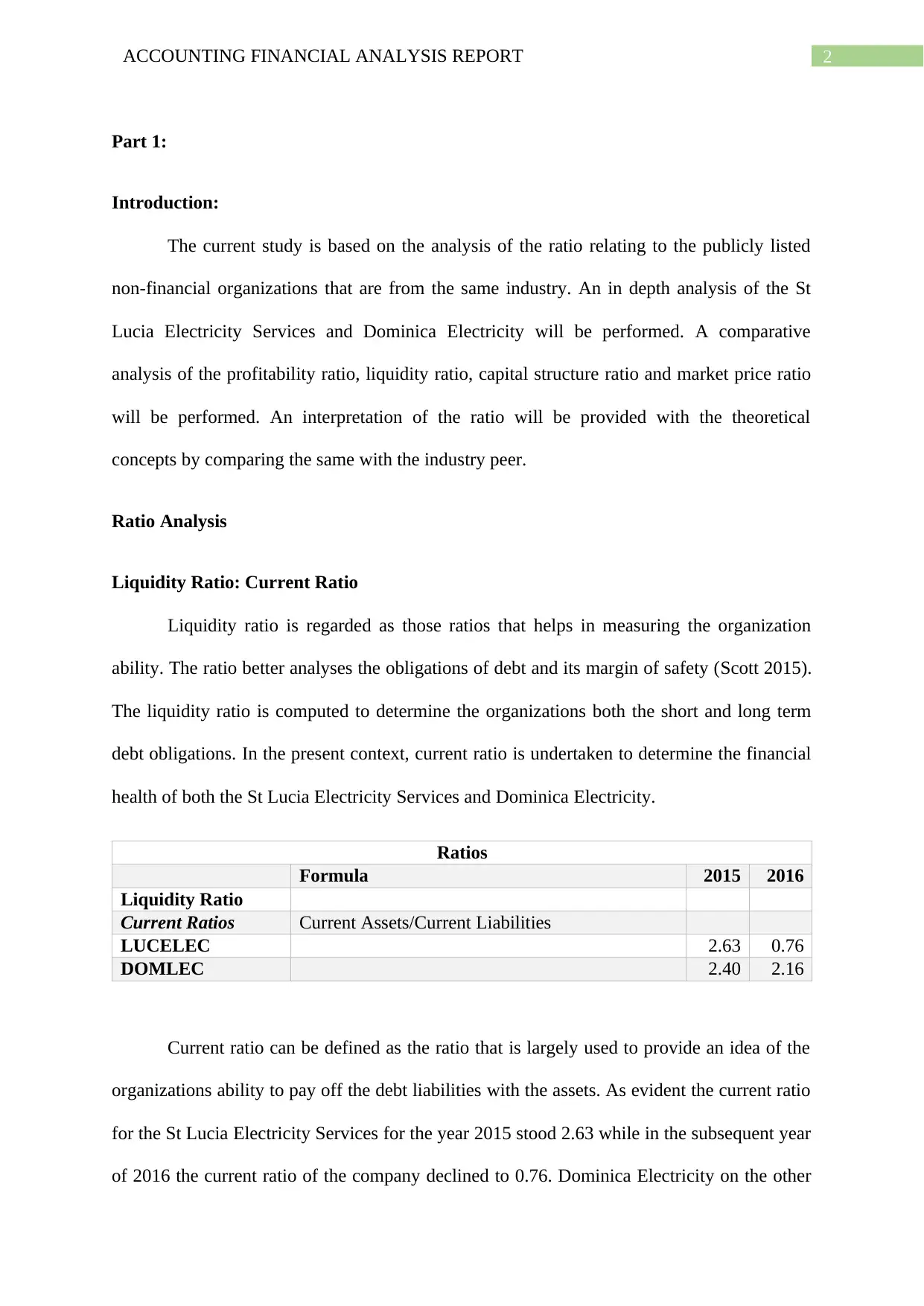

Liquidity Ratio: Current Ratio

Liquidity ratio is regarded as those ratios that helps in measuring the organization

ability. The ratio better analyses the obligations of debt and its margin of safety (Scott 2015).

The liquidity ratio is computed to determine the organizations both the short and long term

debt obligations. In the present context, current ratio is undertaken to determine the financial

health of both the St Lucia Electricity Services and Dominica Electricity.

Ratios

Formula 2015 2016

Liquidity Ratio

Current Ratios Current Assets/Current Liabilities

LUCELEC 2.63 0.76

DOMLEC 2.40 2.16

Current ratio can be defined as the ratio that is largely used to provide an idea of the

organizations ability to pay off the debt liabilities with the assets. As evident the current ratio

for the St Lucia Electricity Services for the year 2015 stood 2.63 while in the subsequent year

of 2016 the current ratio of the company declined to 0.76. Dominica Electricity on the other

Part 1:

Introduction:

The current study is based on the analysis of the ratio relating to the publicly listed

non-financial organizations that are from the same industry. An in depth analysis of the St

Lucia Electricity Services and Dominica Electricity will be performed. A comparative

analysis of the profitability ratio, liquidity ratio, capital structure ratio and market price ratio

will be performed. An interpretation of the ratio will be provided with the theoretical

concepts by comparing the same with the industry peer.

Ratio Analysis

Liquidity Ratio: Current Ratio

Liquidity ratio is regarded as those ratios that helps in measuring the organization

ability. The ratio better analyses the obligations of debt and its margin of safety (Scott 2015).

The liquidity ratio is computed to determine the organizations both the short and long term

debt obligations. In the present context, current ratio is undertaken to determine the financial

health of both the St Lucia Electricity Services and Dominica Electricity.

Ratios

Formula 2015 2016

Liquidity Ratio

Current Ratios Current Assets/Current Liabilities

LUCELEC 2.63 0.76

DOMLEC 2.40 2.16

Current ratio can be defined as the ratio that is largely used to provide an idea of the

organizations ability to pay off the debt liabilities with the assets. As evident the current ratio

for the St Lucia Electricity Services for the year 2015 stood 2.63 while in the subsequent year

of 2016 the current ratio of the company declined to 0.76. Dominica Electricity on the other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FINANCIAL ANALYSIS REPORT

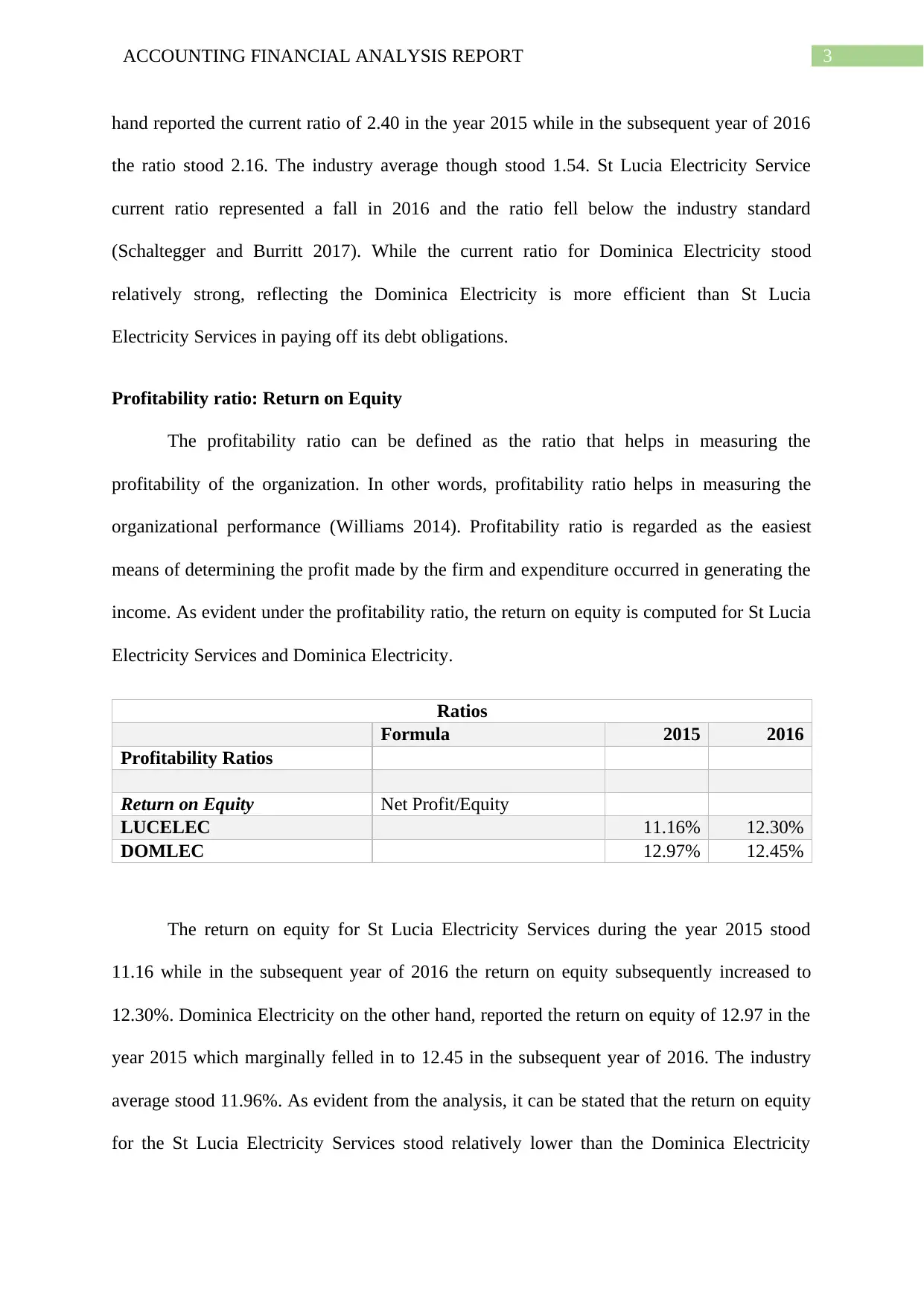

hand reported the current ratio of 2.40 in the year 2015 while in the subsequent year of 2016

the ratio stood 2.16. The industry average though stood 1.54. St Lucia Electricity Service

current ratio represented a fall in 2016 and the ratio fell below the industry standard

(Schaltegger and Burritt 2017). While the current ratio for Dominica Electricity stood

relatively strong, reflecting the Dominica Electricity is more efficient than St Lucia

Electricity Services in paying off its debt obligations.

Profitability ratio: Return on Equity

The profitability ratio can be defined as the ratio that helps in measuring the

profitability of the organization. In other words, profitability ratio helps in measuring the

organizational performance (Williams 2014). Profitability ratio is regarded as the easiest

means of determining the profit made by the firm and expenditure occurred in generating the

income. As evident under the profitability ratio, the return on equity is computed for St Lucia

Electricity Services and Dominica Electricity.

Ratios

Formula 2015 2016

Profitability Ratios

Return on Equity Net Profit/Equity

LUCELEC 11.16% 12.30%

DOMLEC 12.97% 12.45%

The return on equity for St Lucia Electricity Services during the year 2015 stood

11.16 while in the subsequent year of 2016 the return on equity subsequently increased to

12.30%. Dominica Electricity on the other hand, reported the return on equity of 12.97 in the

year 2015 which marginally felled in to 12.45 in the subsequent year of 2016. The industry

average stood 11.96%. As evident from the analysis, it can be stated that the return on equity

for the St Lucia Electricity Services stood relatively lower than the Dominica Electricity

hand reported the current ratio of 2.40 in the year 2015 while in the subsequent year of 2016

the ratio stood 2.16. The industry average though stood 1.54. St Lucia Electricity Service

current ratio represented a fall in 2016 and the ratio fell below the industry standard

(Schaltegger and Burritt 2017). While the current ratio for Dominica Electricity stood

relatively strong, reflecting the Dominica Electricity is more efficient than St Lucia

Electricity Services in paying off its debt obligations.

Profitability ratio: Return on Equity

The profitability ratio can be defined as the ratio that helps in measuring the

profitability of the organization. In other words, profitability ratio helps in measuring the

organizational performance (Williams 2014). Profitability ratio is regarded as the easiest

means of determining the profit made by the firm and expenditure occurred in generating the

income. As evident under the profitability ratio, the return on equity is computed for St Lucia

Electricity Services and Dominica Electricity.

Ratios

Formula 2015 2016

Profitability Ratios

Return on Equity Net Profit/Equity

LUCELEC 11.16% 12.30%

DOMLEC 12.97% 12.45%

The return on equity for St Lucia Electricity Services during the year 2015 stood

11.16 while in the subsequent year of 2016 the return on equity subsequently increased to

12.30%. Dominica Electricity on the other hand, reported the return on equity of 12.97 in the

year 2015 which marginally felled in to 12.45 in the subsequent year of 2016. The industry

average stood 11.96%. As evident from the analysis, it can be stated that the return on equity

for the St Lucia Electricity Services stood relatively lower than the Dominica Electricity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYSIS REPORT

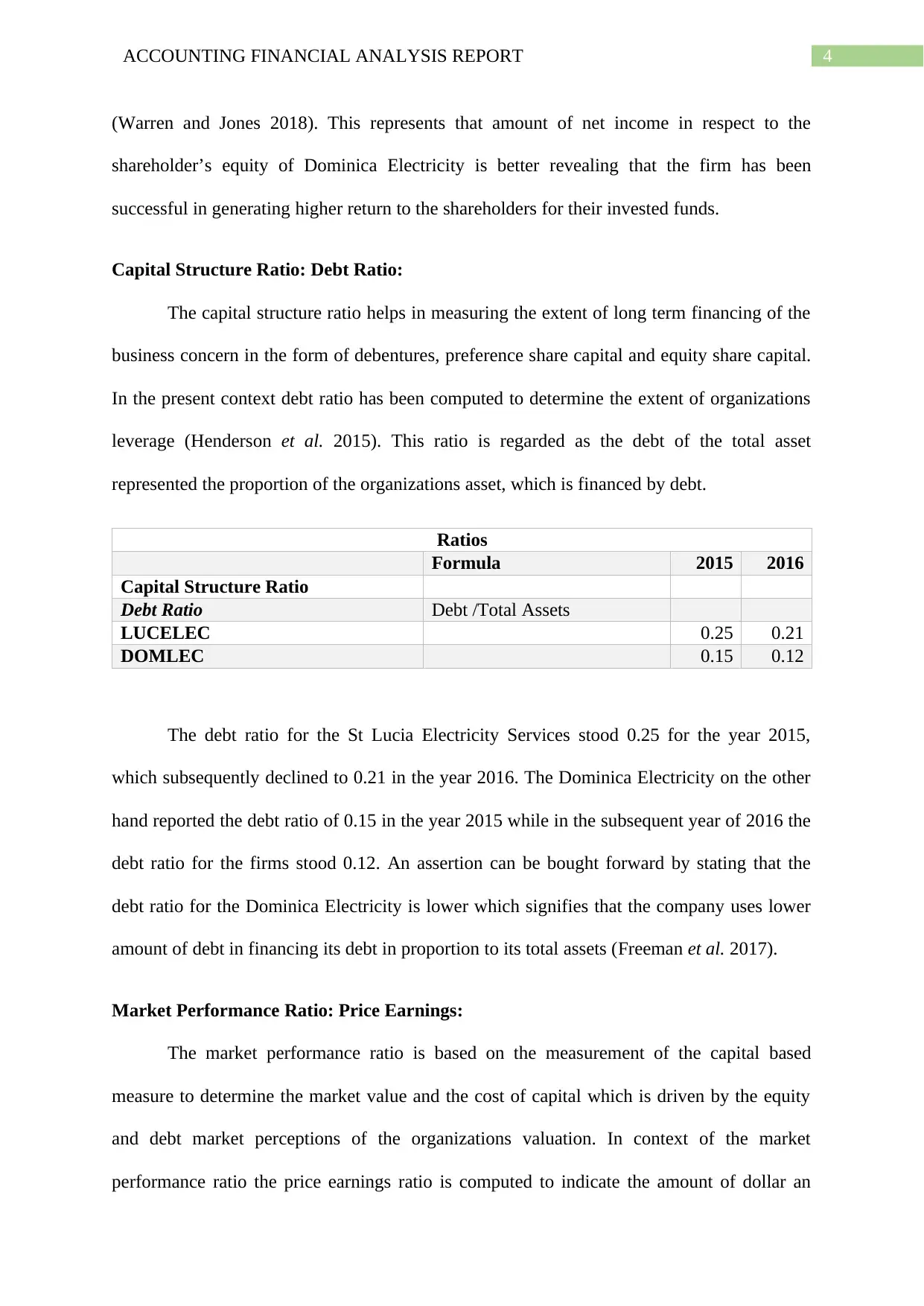

(Warren and Jones 2018). This represents that amount of net income in respect to the

shareholder’s equity of Dominica Electricity is better revealing that the firm has been

successful in generating higher return to the shareholders for their invested funds.

Capital Structure Ratio: Debt Ratio:

The capital structure ratio helps in measuring the extent of long term financing of the

business concern in the form of debentures, preference share capital and equity share capital.

In the present context debt ratio has been computed to determine the extent of organizations

leverage (Henderson et al. 2015). This ratio is regarded as the debt of the total asset

represented the proportion of the organizations asset, which is financed by debt.

Ratios

Formula 2015 2016

Capital Structure Ratio

Debt Ratio Debt /Total Assets

LUCELEC 0.25 0.21

DOMLEC 0.15 0.12

The debt ratio for the St Lucia Electricity Services stood 0.25 for the year 2015,

which subsequently declined to 0.21 in the year 2016. The Dominica Electricity on the other

hand reported the debt ratio of 0.15 in the year 2015 while in the subsequent year of 2016 the

debt ratio for the firms stood 0.12. An assertion can be bought forward by stating that the

debt ratio for the Dominica Electricity is lower which signifies that the company uses lower

amount of debt in financing its debt in proportion to its total assets (Freeman et al. 2017).

Market Performance Ratio: Price Earnings:

The market performance ratio is based on the measurement of the capital based

measure to determine the market value and the cost of capital which is driven by the equity

and debt market perceptions of the organizations valuation. In context of the market

performance ratio the price earnings ratio is computed to indicate the amount of dollar an

(Warren and Jones 2018). This represents that amount of net income in respect to the

shareholder’s equity of Dominica Electricity is better revealing that the firm has been

successful in generating higher return to the shareholders for their invested funds.

Capital Structure Ratio: Debt Ratio:

The capital structure ratio helps in measuring the extent of long term financing of the

business concern in the form of debentures, preference share capital and equity share capital.

In the present context debt ratio has been computed to determine the extent of organizations

leverage (Henderson et al. 2015). This ratio is regarded as the debt of the total asset

represented the proportion of the organizations asset, which is financed by debt.

Ratios

Formula 2015 2016

Capital Structure Ratio

Debt Ratio Debt /Total Assets

LUCELEC 0.25 0.21

DOMLEC 0.15 0.12

The debt ratio for the St Lucia Electricity Services stood 0.25 for the year 2015,

which subsequently declined to 0.21 in the year 2016. The Dominica Electricity on the other

hand reported the debt ratio of 0.15 in the year 2015 while in the subsequent year of 2016 the

debt ratio for the firms stood 0.12. An assertion can be bought forward by stating that the

debt ratio for the Dominica Electricity is lower which signifies that the company uses lower

amount of debt in financing its debt in proportion to its total assets (Freeman et al. 2017).

Market Performance Ratio: Price Earnings:

The market performance ratio is based on the measurement of the capital based

measure to determine the market value and the cost of capital which is driven by the equity

and debt market perceptions of the organizations valuation. In context of the market

performance ratio the price earnings ratio is computed to indicate the amount of dollar an

5ACCOUNTING FINANCIAL ANALYSIS REPORT

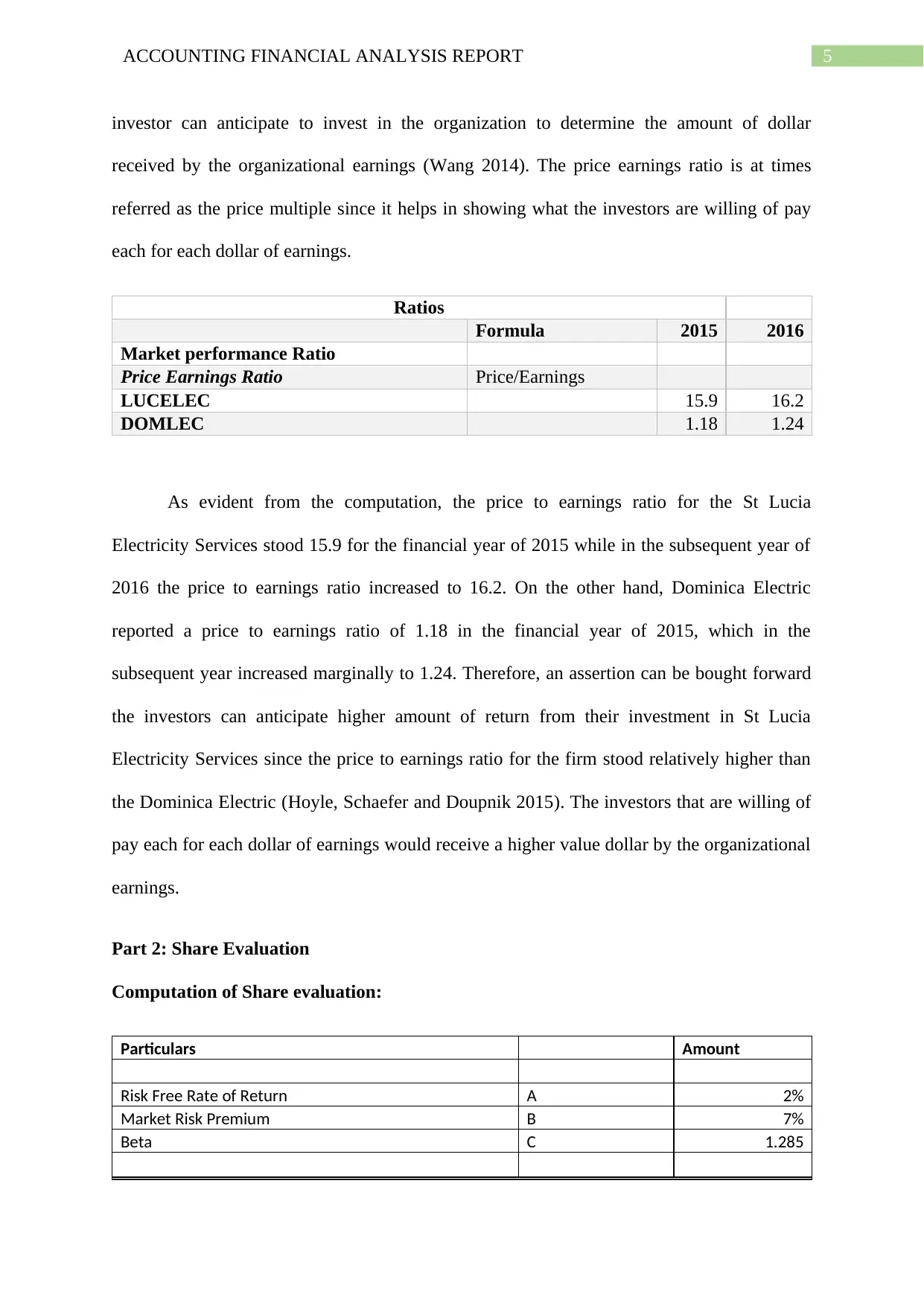

investor can anticipate to invest in the organization to determine the amount of dollar

received by the organizational earnings (Wang 2014). The price earnings ratio is at times

referred as the price multiple since it helps in showing what the investors are willing of pay

each for each dollar of earnings.

Ratios

Formula 2015 2016

Market performance Ratio

Price Earnings Ratio Price/Earnings

LUCELEC 15.9 16.2

DOMLEC 1.18 1.24

As evident from the computation, the price to earnings ratio for the St Lucia

Electricity Services stood 15.9 for the financial year of 2015 while in the subsequent year of

2016 the price to earnings ratio increased to 16.2. On the other hand, Dominica Electric

reported a price to earnings ratio of 1.18 in the financial year of 2015, which in the

subsequent year increased marginally to 1.24. Therefore, an assertion can be bought forward

the investors can anticipate higher amount of return from their investment in St Lucia

Electricity Services since the price to earnings ratio for the firm stood relatively higher than

the Dominica Electric (Hoyle, Schaefer and Doupnik 2015). The investors that are willing of

pay each for each dollar of earnings would receive a higher value dollar by the organizational

earnings.

Part 2: Share Evaluation

Computation of Share evaluation:

Particulars Amount

Risk Free Rate of Return A 2%

Market Risk Premium B 7%

Beta C 1.285

investor can anticipate to invest in the organization to determine the amount of dollar

received by the organizational earnings (Wang 2014). The price earnings ratio is at times

referred as the price multiple since it helps in showing what the investors are willing of pay

each for each dollar of earnings.

Ratios

Formula 2015 2016

Market performance Ratio

Price Earnings Ratio Price/Earnings

LUCELEC 15.9 16.2

DOMLEC 1.18 1.24

As evident from the computation, the price to earnings ratio for the St Lucia

Electricity Services stood 15.9 for the financial year of 2015 while in the subsequent year of

2016 the price to earnings ratio increased to 16.2. On the other hand, Dominica Electric

reported a price to earnings ratio of 1.18 in the financial year of 2015, which in the

subsequent year increased marginally to 1.24. Therefore, an assertion can be bought forward

the investors can anticipate higher amount of return from their investment in St Lucia

Electricity Services since the price to earnings ratio for the firm stood relatively higher than

the Dominica Electric (Hoyle, Schaefer and Doupnik 2015). The investors that are willing of

pay each for each dollar of earnings would receive a higher value dollar by the organizational

earnings.

Part 2: Share Evaluation

Computation of Share evaluation:

Particulars Amount

Risk Free Rate of Return A 2%

Market Risk Premium B 7%

Beta C 1.285

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FINANCIAL ANALYSIS REPORT

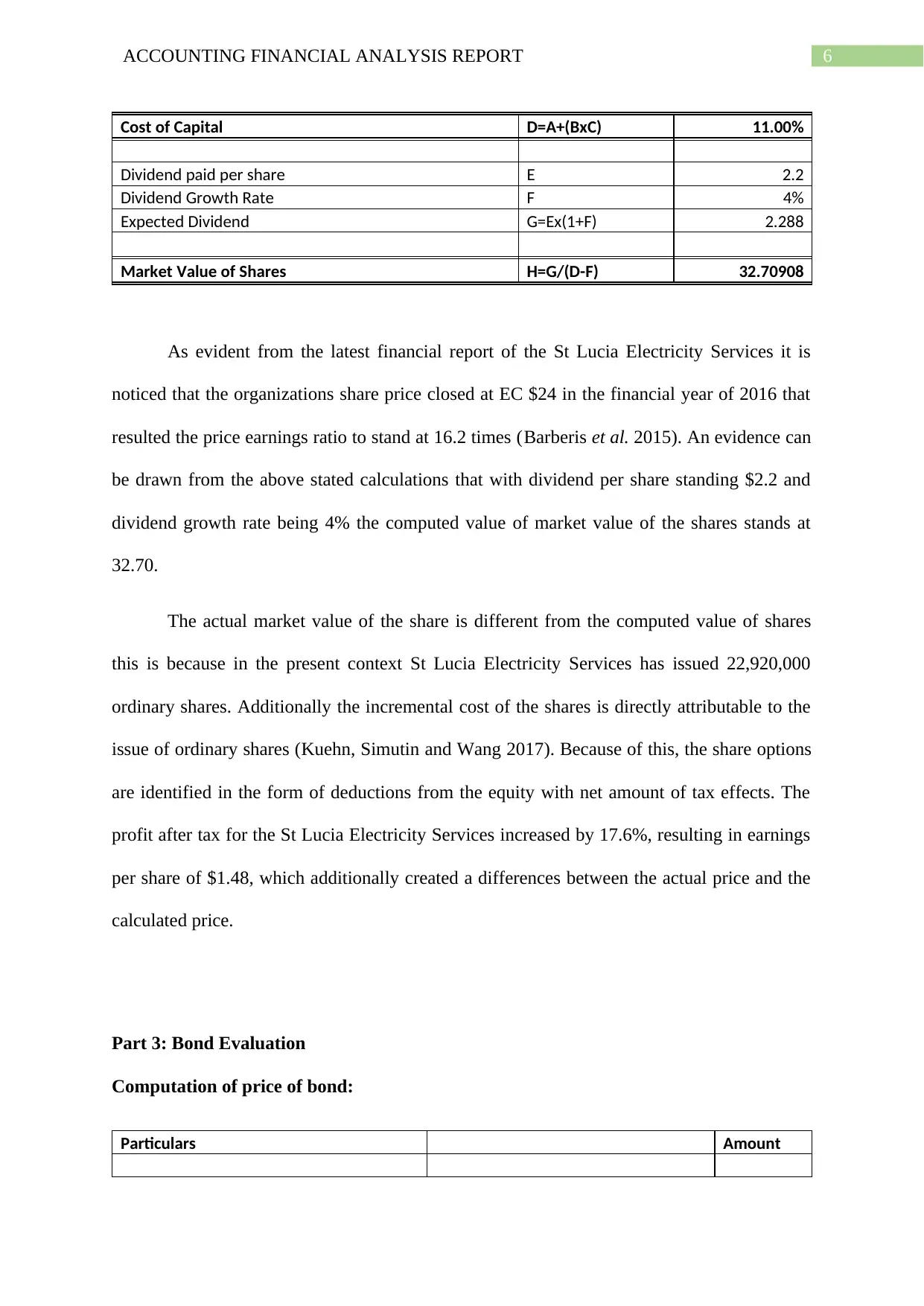

Cost of Capital D=A+(BxC) 11.00%

Dividend paid per share E 2.2

Dividend Growth Rate F 4%

Expected Dividend G=Ex(1+F) 2.288

Market Value of Shares H=G/(D-F) 32.70908

As evident from the latest financial report of the St Lucia Electricity Services it is

noticed that the organizations share price closed at EC $24 in the financial year of 2016 that

resulted the price earnings ratio to stand at 16.2 times (Barberis et al. 2015). An evidence can

be drawn from the above stated calculations that with dividend per share standing $2.2 and

dividend growth rate being 4% the computed value of market value of the shares stands at

32.70.

The actual market value of the share is different from the computed value of shares

this is because in the present context St Lucia Electricity Services has issued 22,920,000

ordinary shares. Additionally the incremental cost of the shares is directly attributable to the

issue of ordinary shares (Kuehn, Simutin and Wang 2017). Because of this, the share options

are identified in the form of deductions from the equity with net amount of tax effects. The

profit after tax for the St Lucia Electricity Services increased by 17.6%, resulting in earnings

per share of $1.48, which additionally created a differences between the actual price and the

calculated price.

Part 3: Bond Evaluation

Computation of price of bond:

Particulars Amount

Cost of Capital D=A+(BxC) 11.00%

Dividend paid per share E 2.2

Dividend Growth Rate F 4%

Expected Dividend G=Ex(1+F) 2.288

Market Value of Shares H=G/(D-F) 32.70908

As evident from the latest financial report of the St Lucia Electricity Services it is

noticed that the organizations share price closed at EC $24 in the financial year of 2016 that

resulted the price earnings ratio to stand at 16.2 times (Barberis et al. 2015). An evidence can

be drawn from the above stated calculations that with dividend per share standing $2.2 and

dividend growth rate being 4% the computed value of market value of the shares stands at

32.70.

The actual market value of the share is different from the computed value of shares

this is because in the present context St Lucia Electricity Services has issued 22,920,000

ordinary shares. Additionally the incremental cost of the shares is directly attributable to the

issue of ordinary shares (Kuehn, Simutin and Wang 2017). Because of this, the share options

are identified in the form of deductions from the equity with net amount of tax effects. The

profit after tax for the St Lucia Electricity Services increased by 17.6%, resulting in earnings

per share of $1.48, which additionally created a differences between the actual price and the

calculated price.

Part 3: Bond Evaluation

Computation of price of bond:

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYSIS REPORT

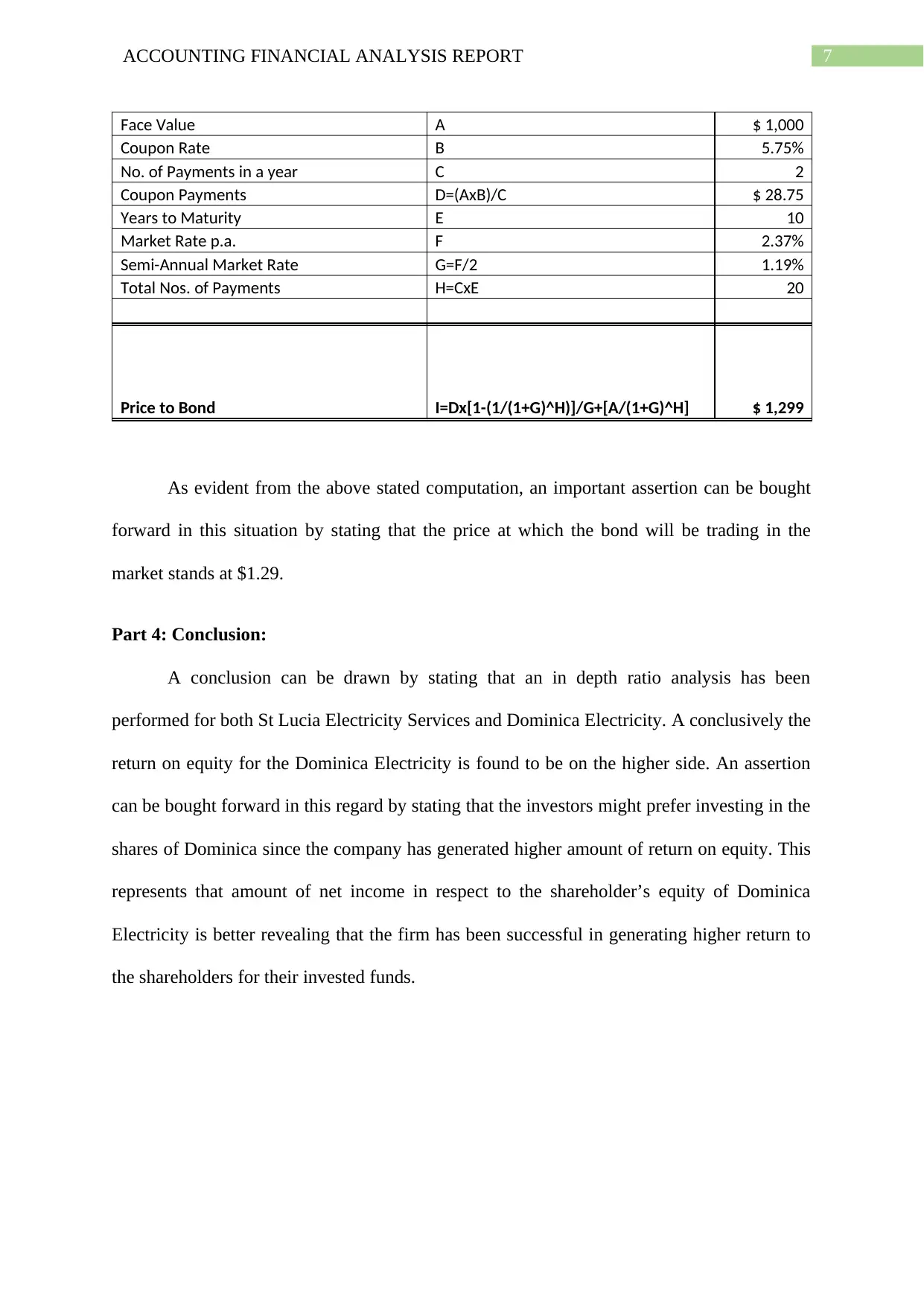

Face Value A $ 1,000

Coupon Rate B 5.75%

No. of Payments in a year C 2

Coupon Payments D=(AxB)/C $ 28.75

Years to Maturity E 10

Market Rate p.a. F 2.37%

Semi-Annual Market Rate G=F/2 1.19%

Total Nos. of Payments H=CxE 20

Price to Bond I=Dx[1-(1/(1+G)^H)]/G+[A/(1+G)^H] $ 1,299

As evident from the above stated computation, an important assertion can be bought

forward in this situation by stating that the price at which the bond will be trading in the

market stands at $1.29.

Part 4: Conclusion:

A conclusion can be drawn by stating that an in depth ratio analysis has been

performed for both St Lucia Electricity Services and Dominica Electricity. A conclusively the

return on equity for the Dominica Electricity is found to be on the higher side. An assertion

can be bought forward in this regard by stating that the investors might prefer investing in the

shares of Dominica since the company has generated higher amount of return on equity. This

represents that amount of net income in respect to the shareholder’s equity of Dominica

Electricity is better revealing that the firm has been successful in generating higher return to

the shareholders for their invested funds.

Face Value A $ 1,000

Coupon Rate B 5.75%

No. of Payments in a year C 2

Coupon Payments D=(AxB)/C $ 28.75

Years to Maturity E 10

Market Rate p.a. F 2.37%

Semi-Annual Market Rate G=F/2 1.19%

Total Nos. of Payments H=CxE 20

Price to Bond I=Dx[1-(1/(1+G)^H)]/G+[A/(1+G)^H] $ 1,299

As evident from the above stated computation, an important assertion can be bought

forward in this situation by stating that the price at which the bond will be trading in the

market stands at $1.29.

Part 4: Conclusion:

A conclusion can be drawn by stating that an in depth ratio analysis has been

performed for both St Lucia Electricity Services and Dominica Electricity. A conclusively the

return on equity for the Dominica Electricity is found to be on the higher side. An assertion

can be bought forward in this regard by stating that the investors might prefer investing in the

shares of Dominica since the company has generated higher amount of return on equity. This

represents that amount of net income in respect to the shareholder’s equity of Dominica

Electricity is better revealing that the firm has been successful in generating higher return to

the shareholders for their invested funds.

8ACCOUNTING FINANCIAL ANALYSIS REPORT

Reference List:

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Freeman, R.J., Shoulders, C.D., McSwain, D.N. and Scott, R.B., 2017. Governmental and

nonprofit accounting. Pearson.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Reference List:

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Freeman, R.J., Shoulders, C.D., McSwain, D.N. and Scott, R.B., 2017. Governmental and

nonprofit accounting. Pearson.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9