Critical Evaluation and Analysis of Tesco's Annual Report

VerifiedAdded on 2022/12/09

|14

|3019

|445

AI Summary

This study critically evaluates and analyzes the annual report of Tesco, including its business model, risks faced, significant issues raised by auditors, and performance under IFRS. It also assesses the overall performance of the annual report with proper justification.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting financial analysis report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

Part 1................................................................................................................................................3

Tesco’s business model...............................................................................................................3

Risks faced by the company........................................................................................................3

Significant issues raised by the auditor and whether or not they are addressed in the CEO

report............................................................................................................................................3

Performance of the company under IFRS in aligned with its own KPIs and APMs...................3

Part 2................................................................................................................................................3

Evaluation of the performance of the annual report with proper justification............................3

PPT..............................................................................................................................................3

Conclusion.......................................................................................................................................3

References........................................................................................................................................4

Introduction......................................................................................................................................3

Part 1................................................................................................................................................3

Tesco’s business model...............................................................................................................3

Risks faced by the company........................................................................................................3

Significant issues raised by the auditor and whether or not they are addressed in the CEO

report............................................................................................................................................3

Performance of the company under IFRS in aligned with its own KPIs and APMs...................3

Part 2................................................................................................................................................3

Evaluation of the performance of the annual report with proper justification............................3

PPT..............................................................................................................................................3

Conclusion.......................................................................................................................................3

References........................................................................................................................................4

INTRODUCTION

The present study is based on the critical evaluation and analysis of the annual report of Tesco,

wherein business model of Tesco will be assessed, along with this the study will also discuss the

risks faced by the company while presenting the significant issues raised by auditors. The study

will also cover the performance of the company under IFRS in aligned with its own KPIs and

APMs, and commenting on whether the annual report of Tesco is good or not with valid

justifications.

PART 1

Tesco’s business model

The business of Tesco is organized in order of the three key pillars of Channels, Product and

Customers, and the company measures their progress with six KPIs (key performance indicators)

which are growing sales, customer recommendations, delivering profit, colleagues

recommendations, improving operating cash flow, and building trusted partnerships (Beynon-

Davies, 2018).

There is a Little Helps Plan that sets out the plans of Tesco to pursue the small actions that make

big differences, and the same is justified by the core values of Group that states ‘every little help

makes a big difference’. It is comprised of three pillars namely; people, products and places

which is supported by their commitments on business ethics, safety and data privacy (Bilińska-

Reformat and et al. 2019). Moreover, these areas are very important to Tesco’s business model,

and the planned delivery is rooted in their daily business operations. It is recognized by the

The present study is based on the critical evaluation and analysis of the annual report of Tesco,

wherein business model of Tesco will be assessed, along with this the study will also discuss the

risks faced by the company while presenting the significant issues raised by auditors. The study

will also cover the performance of the company under IFRS in aligned with its own KPIs and

APMs, and commenting on whether the annual report of Tesco is good or not with valid

justifications.

PART 1

Tesco’s business model

The business of Tesco is organized in order of the three key pillars of Channels, Product and

Customers, and the company measures their progress with six KPIs (key performance indicators)

which are growing sales, customer recommendations, delivering profit, colleagues

recommendations, improving operating cash flow, and building trusted partnerships (Beynon-

Davies, 2018).

There is a Little Helps Plan that sets out the plans of Tesco to pursue the small actions that make

big differences, and the same is justified by the core values of Group that states ‘every little help

makes a big difference’. It is comprised of three pillars namely; people, products and places

which is supported by their commitments on business ethics, safety and data privacy (Bilińska-

Reformat and et al. 2019). Moreover, these areas are very important to Tesco’s business model,

and the planned delivery is rooted in their daily business operations. It is recognized by the

company that the Little Helps Plan is associated with those principle risks; however, it is decisive

to their sustainable success of the Group (Annual report of Tesco, 2018).

The significant non-financial factors of Tesco are economic factors such as inflation and interest

rate by the bank, customer satisfaction, change in technology, and competitor’s strategy. These

factors are important to a business because it has a direct impact in the performance of the

company on an overall basis, therefore along with considering financial factors, the company is

also required to focus non-financial factors for sustainable growth and development (Gill, 2018) .

This can be justified by the fact that if these non-financial factors are overlooked and not

properly managed then this can create a negative impact on company, such as if there is increase

in interest rates or inflation, then finance costs will be increased, and purchasing power of

customer will be reduced respectively and vice-versa in situation of favourable income change.

to their sustainable success of the Group (Annual report of Tesco, 2018).

The significant non-financial factors of Tesco are economic factors such as inflation and interest

rate by the bank, customer satisfaction, change in technology, and competitor’s strategy. These

factors are important to a business because it has a direct impact in the performance of the

company on an overall basis, therefore along with considering financial factors, the company is

also required to focus non-financial factors for sustainable growth and development (Gill, 2018) .

This can be justified by the fact that if these non-financial factors are overlooked and not

properly managed then this can create a negative impact on company, such as if there is increase

in interest rates or inflation, then finance costs will be increased, and purchasing power of

customer will be reduced respectively and vice-versa in situation of favourable income change.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

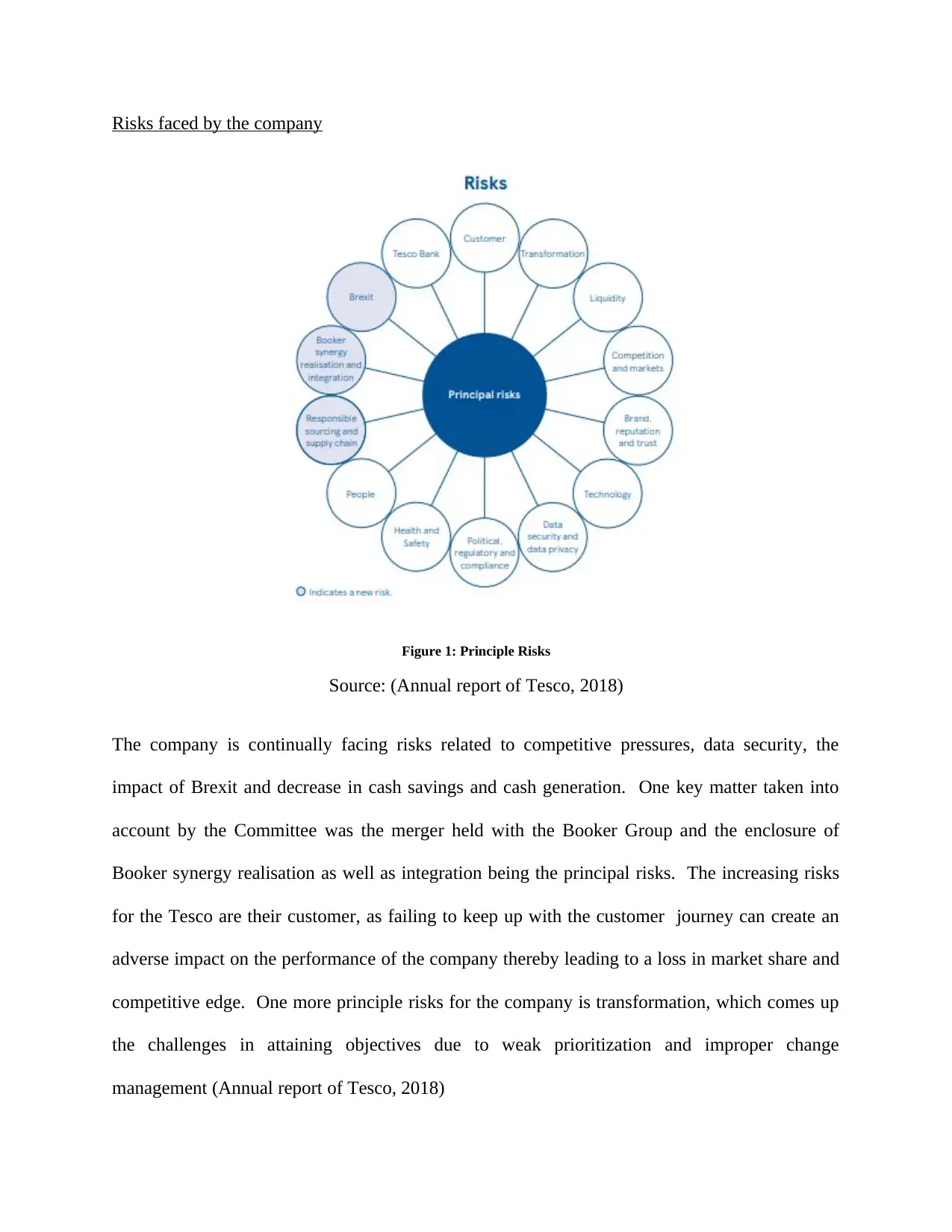

Risks faced by the company

Figure 1: Principle Risks

Source: (Annual report of Tesco, 2018)

The company is continually facing risks related to competitive pressures, data security, the

impact of Brexit and decrease in cash savings and cash generation. One key matter taken into

account by the Committee was the merger held with the Booker Group and the enclosure of

Booker synergy realisation as well as integration being the principal risks. The increasing risks

for the Tesco are their customer, as failing to keep up with the customer journey can create an

adverse impact on the performance of the company thereby leading to a loss in market share and

competitive edge. One more principle risks for the company is transformation, which comes up

the challenges in attaining objectives due to weak prioritization and improper change

management (Annual report of Tesco, 2018)

Figure 1: Principle Risks

Source: (Annual report of Tesco, 2018)

The company is continually facing risks related to competitive pressures, data security, the

impact of Brexit and decrease in cash savings and cash generation. One key matter taken into

account by the Committee was the merger held with the Booker Group and the enclosure of

Booker synergy realisation as well as integration being the principal risks. The increasing risks

for the Tesco are their customer, as failing to keep up with the customer journey can create an

adverse impact on the performance of the company thereby leading to a loss in market share and

competitive edge. One more principle risks for the company is transformation, which comes up

the challenges in attaining objectives due to weak prioritization and improper change

management (Annual report of Tesco, 2018)

.

Credit risk and liquidity risk are considered as a significant risk which is dealt with the company.

Credit risk arises from cash and cash equivalent, customer deposit, financial instruments etc. On

the contrary, liquidity is related to finance operations which are relating to retained profits, debt

capital market issue, commercial paper, leases etc. (Burdorf and van Vuuren, 2018). Credit risk

comprises risk that the bank borrower or the other party does not accomplish the obligation in

accordance with agreed terms and due to the same loss can be incurred by the company. In order

to mitigate specified risk retail credit policy is framed which is managed in accordance with

appropriate credit scoring and associated rules. Further, liquidity and funding risk is assessed

through Liquidity risk management policy framework in order to assure that adequate funds are

available at the required time.

Significant issues raised by the auditor and whether or not they are addressed in the CEO report

The committee considered several significant issues while considering the views of external

auditors, these issues are provided as below and the manner by which they are addressed by the

committee:

Concern based on the viability statement and financial statement: The committee reviewed the

assessment of the management of long-term viability with the concern of foresting cash flows,

inclusive of trading sensitivity, expense plans and possible mitigating actions.

Fixed impairment as well as onerous lease provisions: This has been reviewed by the committee

while challenging the property and technological assets impairment of management and

estimation of onerous lease provisions (Kukreja and Gupta, 2016). The validity of key

estimations has been taken into account by the committee for fair value measurement and value

Credit risk and liquidity risk are considered as a significant risk which is dealt with the company.

Credit risk arises from cash and cash equivalent, customer deposit, financial instruments etc. On

the contrary, liquidity is related to finance operations which are relating to retained profits, debt

capital market issue, commercial paper, leases etc. (Burdorf and van Vuuren, 2018). Credit risk

comprises risk that the bank borrower or the other party does not accomplish the obligation in

accordance with agreed terms and due to the same loss can be incurred by the company. In order

to mitigate specified risk retail credit policy is framed which is managed in accordance with

appropriate credit scoring and associated rules. Further, liquidity and funding risk is assessed

through Liquidity risk management policy framework in order to assure that adequate funds are

available at the required time.

Significant issues raised by the auditor and whether or not they are addressed in the CEO report

The committee considered several significant issues while considering the views of external

auditors, these issues are provided as below and the manner by which they are addressed by the

committee:

Concern based on the viability statement and financial statement: The committee reviewed the

assessment of the management of long-term viability with the concern of foresting cash flows,

inclusive of trading sensitivity, expense plans and possible mitigating actions.

Fixed impairment as well as onerous lease provisions: This has been reviewed by the committee

while challenging the property and technological assets impairment of management and

estimation of onerous lease provisions (Kukreja and Gupta, 2016). The validity of key

estimations has been taken into account by the committee for fair value measurement and value

in use (Hopkin, 2018). This comprised challenging possible growth rates, using independent

third party valuations, discount rates, cash flows and consideration of uncertain impacts taking

place from Brexit.

Goodwill impairment: The process of impairment is reviewed by the committee for testing

goodwill possible impairment and making sure that there is valid disclosure to sensitivity. This

comprised challenging the core assumptions growth rates, discount rates and principal cash flow

projections (Hay, 2015).

Other significant issues included the pensions, business combinations, exceptional items, and

contingent liabilities, disposals of property and business and new accounting standards which

were properly addressed by the committee through better compliance and code of conduct

(Annual report of Tesco, 2018).

Performance of the company under IFRS in aligned with its own KPIs and APMs

The financial statement of Group has been prepared appropriately as per the International

Financial Reporting Standards (IFRSs) to the extent applicable to the organization. Key

accounting matter comprises IFRS 9 and exceptional items as it relates to Financial Instruments.

Further, it has been stated in the director’s responsibility statement that IFRS which are adopted

by the EU and applicable on UK Accounting Standard has been compiled by the company. For

instance as IFRS 6 ‘Non-current assets held for sale and discontinuing operation’ asserts that net

results of discontinued operation required to presented separately in the group income statement

and asset and liabilities relating to same should also be stated separately under the required head.

Thus, the same method has been followed in the financial statement of Tesco (Adewuyi, 2016).

The standards which will be applicable in future have been specified with the date from which it

third party valuations, discount rates, cash flows and consideration of uncertain impacts taking

place from Brexit.

Goodwill impairment: The process of impairment is reviewed by the committee for testing

goodwill possible impairment and making sure that there is valid disclosure to sensitivity. This

comprised challenging the core assumptions growth rates, discount rates and principal cash flow

projections (Hay, 2015).

Other significant issues included the pensions, business combinations, exceptional items, and

contingent liabilities, disposals of property and business and new accounting standards which

were properly addressed by the committee through better compliance and code of conduct

(Annual report of Tesco, 2018).

Performance of the company under IFRS in aligned with its own KPIs and APMs

The financial statement of Group has been prepared appropriately as per the International

Financial Reporting Standards (IFRSs) to the extent applicable to the organization. Key

accounting matter comprises IFRS 9 and exceptional items as it relates to Financial Instruments.

Further, it has been stated in the director’s responsibility statement that IFRS which are adopted

by the EU and applicable on UK Accounting Standard has been compiled by the company. For

instance as IFRS 6 ‘Non-current assets held for sale and discontinuing operation’ asserts that net

results of discontinued operation required to presented separately in the group income statement

and asset and liabilities relating to same should also be stated separately under the required head.

Thus, the same method has been followed in the financial statement of Tesco (Adewuyi, 2016).

The standards which will be applicable in future have been specified with the date from which it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will be applicable and the manner in which it will be accounted for in the financial statement. As

in the case of IFRS 16 ‘Leases’, which will be effectively applied for 53 weeks ending of 26th

February 2020. Thus, it has been stated in the annual report that the company will adopt the

standard in a retrospective manner from the transition date 25th February 2018. Moreover,

comparatives will also be provided with restated figures.

KPI (Key performance indicators) assists an organization in ascertaining whether it is on the

right track or not. In other words, it evaluates whether the company is working towards attaining

pre-determined goal and objectives or not. APM (Alternative Performance Measures) are

adopted by the director to assess the measures which are not specified in IFRS. Thus, they should

be considered in addition to available provisions and not be substituted or superseded to existing

provisions. KPI and APM (Alternative Performance Measures) are different as APM provide

additional information relating to underlying trends, performance and position of the company

(Morales-Díaz and Zamora-Ramírez, 2018). The analysis comprises the nature of item and the

impact of the same on the specified performance. Even reversal of prior exceptional items is

analysed on the basis of the same criteria. APM is applied regarding net debt, diluted earnings

per share, etc. and on the contrary, the key performance indicators of the company are products,

customers, channels through which it operates and investments (Sovbetov, 2015) .

PART 2

Evaluation of the performance of the annual report with proper justification

In the annual report, all the achievements made by the company are highlighted in an appropriate

manner which assists in developing trust in stakeholder regarding the organization. But for

making an appropriate and complete report all the dealing, accomplishment applied strategies,

in the case of IFRS 16 ‘Leases’, which will be effectively applied for 53 weeks ending of 26th

February 2020. Thus, it has been stated in the annual report that the company will adopt the

standard in a retrospective manner from the transition date 25th February 2018. Moreover,

comparatives will also be provided with restated figures.

KPI (Key performance indicators) assists an organization in ascertaining whether it is on the

right track or not. In other words, it evaluates whether the company is working towards attaining

pre-determined goal and objectives or not. APM (Alternative Performance Measures) are

adopted by the director to assess the measures which are not specified in IFRS. Thus, they should

be considered in addition to available provisions and not be substituted or superseded to existing

provisions. KPI and APM (Alternative Performance Measures) are different as APM provide

additional information relating to underlying trends, performance and position of the company

(Morales-Díaz and Zamora-Ramírez, 2018). The analysis comprises the nature of item and the

impact of the same on the specified performance. Even reversal of prior exceptional items is

analysed on the basis of the same criteria. APM is applied regarding net debt, diluted earnings

per share, etc. and on the contrary, the key performance indicators of the company are products,

customers, channels through which it operates and investments (Sovbetov, 2015) .

PART 2

Evaluation of the performance of the annual report with proper justification

In the annual report, all the achievements made by the company are highlighted in an appropriate

manner which assists in developing trust in stakeholder regarding the organization. But for

making an appropriate and complete report all the dealing, accomplishment applied strategies,

their impacts, profit margins; turnover and other important aspects should be covered briefly.

Thus, as per the analysis of Tesco Annual Report, it can be said that is a proper and complete

report in which all the aspects are covered that nailed the annual report. Tesco is well known for

its better serving every day which was clearly explained in the report (Ismail, 2017). The report

collectively highlights performance measures regarding corporate governance, associates, and

workers and connected authorities with it. The manner in which they make a substantial growth

every year and efforts which they made is described in the report. Further specification relating

to efforts made by the company to serve their customers and society as well as details relating to

the manner in which they deal with opportunities comes in front of them while promoting the

products is provided in an appropriate manner (Bourne, Bourne and Ferguson, 2017).

Company strategies, key ideas, financial review, principal risk and uncertainties that the

company is bearing, reasons behind the losses, solutions, backup plans, feedbacks are enclosed

in the present report. Furthermore associated corporate government, executive committee,

government framework, connection with stakeholders, engagement of shareholders and all the

other committees those are connected and working with the organization is clearly defined with

their roles and responsibilities (Zentes, Morschett and Schramm-Klein, 2017). In addition, the

progress of the business is measured by the six key performance indicators, and it has been

specified that the company is organised around the three pillars that are customers, channels and

products. Thus, these important aspects are completely covered in the report which demonstrates

that business is working according to the planned strategies and procedure and which is the

biggest reason behind its achievements.

Documentation regarding the activities and performance of the company and major steps towards

the enhancement of the technical aspect and a detailed analysis relating to director and

Thus, as per the analysis of Tesco Annual Report, it can be said that is a proper and complete

report in which all the aspects are covered that nailed the annual report. Tesco is well known for

its better serving every day which was clearly explained in the report (Ismail, 2017). The report

collectively highlights performance measures regarding corporate governance, associates, and

workers and connected authorities with it. The manner in which they make a substantial growth

every year and efforts which they made is described in the report. Further specification relating

to efforts made by the company to serve their customers and society as well as details relating to

the manner in which they deal with opportunities comes in front of them while promoting the

products is provided in an appropriate manner (Bourne, Bourne and Ferguson, 2017).

Company strategies, key ideas, financial review, principal risk and uncertainties that the

company is bearing, reasons behind the losses, solutions, backup plans, feedbacks are enclosed

in the present report. Furthermore associated corporate government, executive committee,

government framework, connection with stakeholders, engagement of shareholders and all the

other committees those are connected and working with the organization is clearly defined with

their roles and responsibilities (Zentes, Morschett and Schramm-Klein, 2017). In addition, the

progress of the business is measured by the six key performance indicators, and it has been

specified that the company is organised around the three pillars that are customers, channels and

products. Thus, these important aspects are completely covered in the report which demonstrates

that business is working according to the planned strategies and procedure and which is the

biggest reason behind its achievements.

Documentation regarding the activities and performance of the company and major steps towards

the enhancement of the technical aspect and a detailed analysis relating to director and

executives has been provided as Remuneration Report of Directors, Statement of Directors’

responsibilities. Thus, the detail provides stakeholders with information relating to the

responsibilities and roles of senior executives so that even they can know the responsibilities of

senior management (Tesco PLC, 2017).

The present report is reader-friendly and easy, and understandable language is used by the

management so that everyone gets the concept involved with it. The presentation in the report is

well organised and which seems to be very purposeful. The report is result oriented which

highlights all the necessary facts that make it complete. An honest description is provided by the

in the report which makes it straightforward and attractive. Moreover in the report difference is

clearly made between the controllable and uncontrollable factors which can be further taken into

consideration separately and details have also been provided relating to actions that have been

taken by the authority to control then further (Zentes, Morschett and Schramm-Klein, 2017).

Appropriate remarks are mentioned in the report which helps in saving valuable time of the

organization and make sure about the prompt attention. Thus, the annual report of Tesco can be

considered as a good report as the whole report is provided in easy language due to which same

can be understood and assessed by stakeholders (Clark, Feiner and Viehs, 2015.). Further,

adequate comparison chart and diagram are provided in order to make it interactive to readers of

the report.

CONCLUSION

Annual report of the company illustrates its position; therefore it should be attractive and

straightforward. Thus, it is necessary that the report must disclose all related facts relating to the

business operation of the organization. After assessing the above study, it can be concluded that

responsibilities. Thus, the detail provides stakeholders with information relating to the

responsibilities and roles of senior executives so that even they can know the responsibilities of

senior management (Tesco PLC, 2017).

The present report is reader-friendly and easy, and understandable language is used by the

management so that everyone gets the concept involved with it. The presentation in the report is

well organised and which seems to be very purposeful. The report is result oriented which

highlights all the necessary facts that make it complete. An honest description is provided by the

in the report which makes it straightforward and attractive. Moreover in the report difference is

clearly made between the controllable and uncontrollable factors which can be further taken into

consideration separately and details have also been provided relating to actions that have been

taken by the authority to control then further (Zentes, Morschett and Schramm-Klein, 2017).

Appropriate remarks are mentioned in the report which helps in saving valuable time of the

organization and make sure about the prompt attention. Thus, the annual report of Tesco can be

considered as a good report as the whole report is provided in easy language due to which same

can be understood and assessed by stakeholders (Clark, Feiner and Viehs, 2015.). Further,

adequate comparison chart and diagram are provided in order to make it interactive to readers of

the report.

CONCLUSION

Annual report of the company illustrates its position; therefore it should be attractive and

straightforward. Thus, it is necessary that the report must disclose all related facts relating to the

business operation of the organization. After assessing the above study, it can be concluded that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

while generating the report the thing that should be kept in mind is that it should be clearly

understood and free from the duplication and errors. However, by analysing the current report of

Tesco, it is clear that the report is result oriented and specifies every important relating to the

operation of the business in an adequate manner. However, management required to emphasize

on certain areas such as the detail of more than one year should be provided for comparison so

that trend regarding the specific subject can be ascertained by the stakeholder. Overall, each

information has been provided in an appropriate and detail manner, due to which the reader of

the report could analyse the actual position of the company.

understood and free from the duplication and errors. However, by analysing the current report of

Tesco, it is clear that the report is result oriented and specifies every important relating to the

operation of the business in an adequate manner. However, management required to emphasize

on certain areas such as the detail of more than one year should be provided for comparison so

that trend regarding the specific subject can be ascertained by the stakeholder. Overall, each

information has been provided in an appropriate and detail manner, due to which the reader of

the report could analyse the actual position of the company.

REFERENCES

Books and Journals

Beynon-Davies, P., 2018. Characterizing Business Models for Digital Business Through

Patterns. International Journal of Electronic Commerce, 22(1), pp.98-124.

Bilińska-Reformat, K., Kucharska, B., Twardzik, M. and Dolega, L., 2019. Sustainable

development concept and creation of innovative business models by retail chains. International

Journal of Retail & Distribution Management, 47(1), pp.2-18.

Gill, N.S., 2018. Relationship between diversity on the board of directors’ and firm financial

performance. Doctoral dissertation. 1(1). pp.15-20.

Hopkin, P., 2018. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers, UK.

Burdorf, T. and van Vuuren, G., 2018. An evaluation and comparison of Value at Risk and

Expected Shortfall. Innovations, 15(4), pp.17-34.

Kukreja, G. and Gupta, S., 2016. Tesco Accounting Misstatements: Myopic Ideologies

Overshadowing Larger Organisational Interests. SDMIMD Journal of Management, 7(1), pp.9-

18.

Hay, D., 2015. The frontiers of auditing research. Meditari Accountancy Research, 23(2),

pp.158-174.

Adewuyi, A.W., 2016. Ratio Analysis of Tesco Plc Financial Performance between 2010 and

2014 in Comparison to Both Sainsbury and Morrisons. Open Journal of Accounting, 5(03), p.45.

Books and Journals

Beynon-Davies, P., 2018. Characterizing Business Models for Digital Business Through

Patterns. International Journal of Electronic Commerce, 22(1), pp.98-124.

Bilińska-Reformat, K., Kucharska, B., Twardzik, M. and Dolega, L., 2019. Sustainable

development concept and creation of innovative business models by retail chains. International

Journal of Retail & Distribution Management, 47(1), pp.2-18.

Gill, N.S., 2018. Relationship between diversity on the board of directors’ and firm financial

performance. Doctoral dissertation. 1(1). pp.15-20.

Hopkin, P., 2018. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers, UK.

Burdorf, T. and van Vuuren, G., 2018. An evaluation and comparison of Value at Risk and

Expected Shortfall. Innovations, 15(4), pp.17-34.

Kukreja, G. and Gupta, S., 2016. Tesco Accounting Misstatements: Myopic Ideologies

Overshadowing Larger Organisational Interests. SDMIMD Journal of Management, 7(1), pp.9-

18.

Hay, D., 2015. The frontiers of auditing research. Meditari Accountancy Research, 23(2),

pp.158-174.

Adewuyi, A.W., 2016. Ratio Analysis of Tesco Plc Financial Performance between 2010 and

2014 in Comparison to Both Sainsbury and Morrisons. Open Journal of Accounting, 5(03), p.45.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Sovbetov, Y., 2015. How IFRS Affects Value Relevance and Key Financial Indicators?

Evidence from the UK. International Review of Accounting, Banking and Finance, 7(1), pp.73-

96.

Ismail, I.N., 2017. The Roles of Corporate Governance and its Influences on Risk and

Performance: Tesco Plc. 1(1), pp.23-36

Zentes, J., Morschett, D. and Schramm-Klein, H., 2017. Monitoring Operational and Financial

Performance. Strategic Retail Management (pp. 441-461). Springer Gabler, Wiesbaden.

Clark, G.L., Feiner, A. and Viehs, M., 2015. From the stockholder to the stakeholder: How

sustainability can drive financial outperformance. Routledge. 1(1).

Zentes, J., Morschett, D. and Schramm-Klein, H., 2017. Monitoring Operational and Financial

Performance. Strategic Retail Management (pp. 441-461). Springer Gabler, Wiesbaden.

Bourne, M., Bourne, P. and Ferguson, D., 2017. Strategic business performance for

sustainability. In Cranfield on Corporate Sustainability (pp. 80-104). Routledge, UK.

Online

Tesco PLC, 2017. Annual Report 2017 (Online). Available from <

https://www.tescoplc.com/investors/reports-results-and-presentations/annual-report-2017/>.

[Accessed on 30 April 2019].

a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Sovbetov, Y., 2015. How IFRS Affects Value Relevance and Key Financial Indicators?

Evidence from the UK. International Review of Accounting, Banking and Finance, 7(1), pp.73-

96.

Ismail, I.N., 2017. The Roles of Corporate Governance and its Influences on Risk and

Performance: Tesco Plc. 1(1), pp.23-36

Zentes, J., Morschett, D. and Schramm-Klein, H., 2017. Monitoring Operational and Financial

Performance. Strategic Retail Management (pp. 441-461). Springer Gabler, Wiesbaden.

Clark, G.L., Feiner, A. and Viehs, M., 2015. From the stockholder to the stakeholder: How

sustainability can drive financial outperformance. Routledge. 1(1).

Zentes, J., Morschett, D. and Schramm-Klein, H., 2017. Monitoring Operational and Financial

Performance. Strategic Retail Management (pp. 441-461). Springer Gabler, Wiesbaden.

Bourne, M., Bourne, P. and Ferguson, D., 2017. Strategic business performance for

sustainability. In Cranfield on Corporate Sustainability (pp. 80-104). Routledge, UK.

Online

Tesco PLC, 2017. Annual Report 2017 (Online). Available from <

https://www.tescoplc.com/investors/reports-results-and-presentations/annual-report-2017/>.

[Accessed on 30 April 2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Annual report of Tesco, 2018. Serving shoppers a little better every day. Available from <

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf>. [Accessed on 29 April 2019].

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf>. [Accessed on 29 April 2019].

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.