Financial Analysis Report: NEUROFORCE and IQPOWER Project Evaluation

VerifiedAdded on 2023/03/17

|13

|2303

|72

Report

AI Summary

This report presents a financial analysis of two projects, NEUROFORCE and IQPOWER, for HITECH Ltd, employing capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and discounted payback period. The analysis evaluates the profitability of each project at different discount rates and considers the crossover rate to compare their attractiveness. The findings indicate that while NEUROFORCE has a positive NPV and IRR, it fails to meet the company's required discounted payback period. In contrast, IQPOWER satisfies all financial criteria, making it a more viable investment option. The report concludes with recommendations based on the financial analysis, emphasizing the importance of considering both quantitative and qualitative factors in making investment decisions. The report also includes a detailed comparison of the two projects, comparing their financial metrics and considering the company's preference for a shorter payback period.

Running head: ACCOUNTING FINANCIAL ANALYSIS REPORT

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Accounting financial analysis report

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYSIS REPORT

Executive summary

Main objective of the report is analysing the profitability of the project NEUROFORCE that is

considered by HITECH for taking up at present. Various methods those will be used for

analysing both the projects are internal rate of return, net present value and discounted payback

period. The report will analyse another project that is IQPOWER before taking the final decision

by the management. Further, both the projects will be compared through application of cross-

over rate.

Executive summary

Main objective of the report is analysing the profitability of the project NEUROFORCE that is

considered by HITECH for taking up at present. Various methods those will be used for

analysing both the projects are internal rate of return, net present value and discounted payback

period. The report will analyse another project that is IQPOWER before taking the final decision

by the management. Further, both the projects will be compared through application of cross-

over rate.

2ACCOUNTING FINANCIAL ANALYSIS REPORT

Table of Contents

1. Introduction..............................................................................................................................3

2. Findings....................................................................................................................................3

2.1 Quantitative.......................................................................................................................3

2.2 Qualitative.........................................................................................................................5

3. Recommendation and justification...........................................................................................6

4. Detail comparison and further recommendation......................................................................6

5. Conclusion................................................................................................................................8

Bibliography....................................................................................................................................9

Appendix........................................................................................................................................11

Table of Contents

1. Introduction..............................................................................................................................3

2. Findings....................................................................................................................................3

2.1 Quantitative.......................................................................................................................3

2.2 Qualitative.........................................................................................................................5

3. Recommendation and justification...........................................................................................6

4. Detail comparison and further recommendation......................................................................6

5. Conclusion................................................................................................................................8

Bibliography....................................................................................................................................9

Appendix........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FINANCIAL ANALYSIS REPORT

1. Introduction

HITECH Ltd is evaluating introduction of a new game product named as

NEUROFORCE. The new game can be connected with the human brain functions and is

controversial for the claim. However, the adverse impact on the human behaviour for its long

time use is still to be confirmed. Though the entity already has a analysis report regarding this

project, before investing large amount for purchase of required equipment for this project the

company wants to analyse the project in detail. Further, before taking up this project the entity

wants to analyse another project named as IQPOWER. Various methods those will be used for

analysing both the projects are internal rate of return, net present value and discounted payback

period. Further, both the projects will be compared through application of cross-over rate.

2. Findings

2.1 Quantitative

1. Introduction

HITECH Ltd is evaluating introduction of a new game product named as

NEUROFORCE. The new game can be connected with the human brain functions and is

controversial for the claim. However, the adverse impact on the human behaviour for its long

time use is still to be confirmed. Though the entity already has a analysis report regarding this

project, before investing large amount for purchase of required equipment for this project the

company wants to analyse the project in detail. Further, before taking up this project the entity

wants to analyse another project named as IQPOWER. Various methods those will be used for

analysing both the projects are internal rate of return, net present value and discounted payback

period. Further, both the projects will be compared through application of cross-over rate.

2. Findings

2.1 Quantitative

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYSIS REPORT

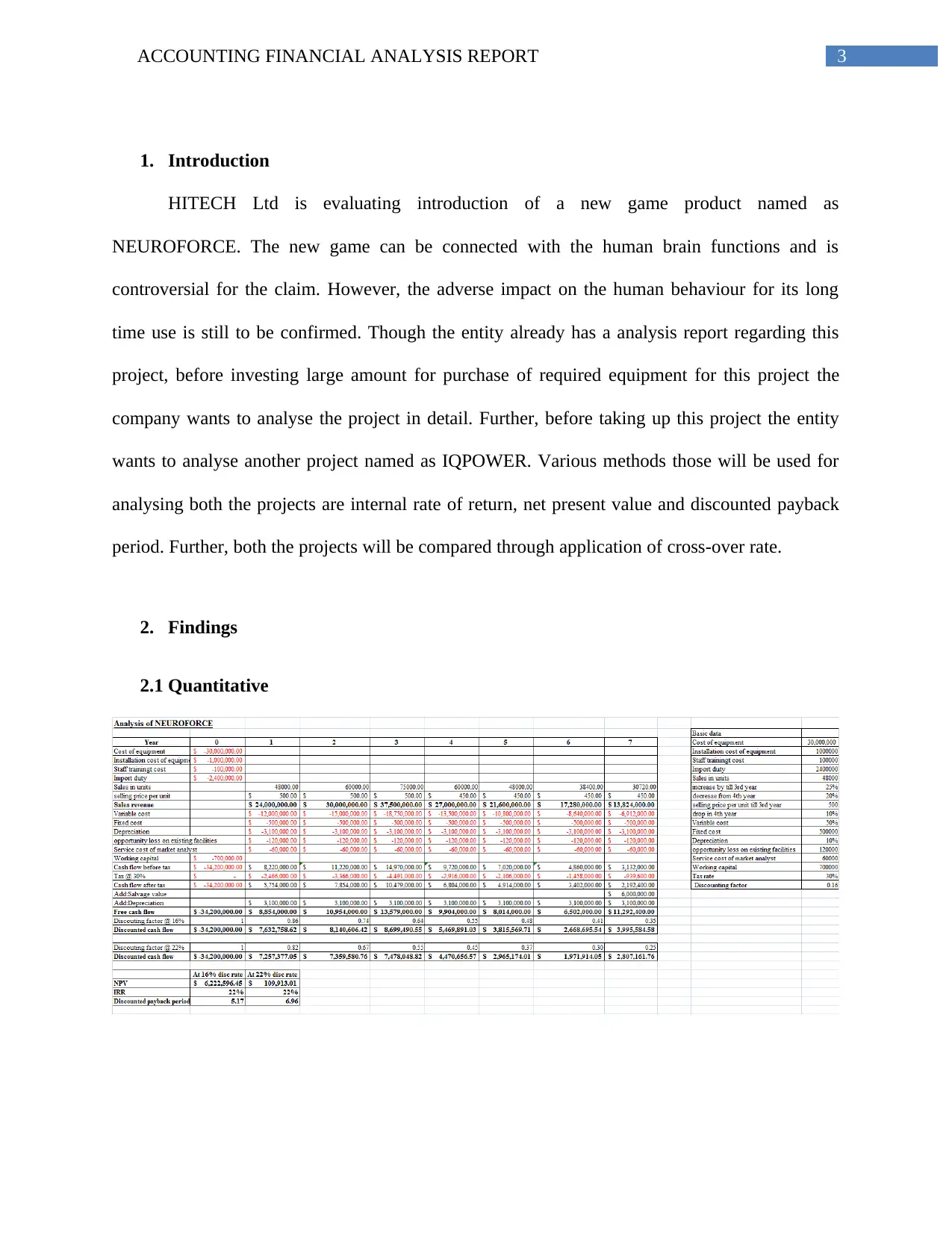

Considering the information provided for both the projects that is NEUROFORCE as

well as IQPOWER different methods those will be used for analysing them are mentioned below

–

Net present value (NPV) – NPV of the project is the expected cash from it over its useful

life after deducting the initial cash expenses required for acquiring the project. This

approach is used under capital budgeting for analysing profitability of any project or the

investment. It assists in taking decision regarding acceptability of the project. For

instance, the project with positive NPV are generally considered for up if any other

condition is not there to be considered for accepting the same. On the contrary, the

project with the negative NPV signifies that the project will not be able to generate

sufficient cash flows over its useful life for covering up the initial amount spend for

acquiring the project and hence, the same will not be considered for taking up. Taking

into consideration the NPV of NEOROFORCE, it can be identified that at the discount

rate of 16% the NPV project is $ 62,22,596.45. Hence, from the computation of NPV it

can be stated that at 16% the NPV of the project is positive. In other words, the project

will create value for the shareholders and therefore acceptable

Internal rate of return (IRR) – IRR is rate at which the NPV of entire cash flows of the

company is zero. Here in the cash flows all the negative as well as positive cash flows are

taken into consideration. IRR approach is useful for ranking the projects and selecting

one of the projects from 2 or more mutually exclusive projects. When the IRR of the

project is equal to or more than the cost of capital it is accepted. Conversely, the project

is not accepted if the IRR is less than the cost of capital of the company. From the

calculation it can be identified that the IRR of NEOROFORCE is 22%. Hence, it can be

Considering the information provided for both the projects that is NEUROFORCE as

well as IQPOWER different methods those will be used for analysing them are mentioned below

–

Net present value (NPV) – NPV of the project is the expected cash from it over its useful

life after deducting the initial cash expenses required for acquiring the project. This

approach is used under capital budgeting for analysing profitability of any project or the

investment. It assists in taking decision regarding acceptability of the project. For

instance, the project with positive NPV are generally considered for up if any other

condition is not there to be considered for accepting the same. On the contrary, the

project with the negative NPV signifies that the project will not be able to generate

sufficient cash flows over its useful life for covering up the initial amount spend for

acquiring the project and hence, the same will not be considered for taking up. Taking

into consideration the NPV of NEOROFORCE, it can be identified that at the discount

rate of 16% the NPV project is $ 62,22,596.45. Hence, from the computation of NPV it

can be stated that at 16% the NPV of the project is positive. In other words, the project

will create value for the shareholders and therefore acceptable

Internal rate of return (IRR) – IRR is rate at which the NPV of entire cash flows of the

company is zero. Here in the cash flows all the negative as well as positive cash flows are

taken into consideration. IRR approach is useful for ranking the projects and selecting

one of the projects from 2 or more mutually exclusive projects. When the IRR of the

project is equal to or more than the cost of capital it is accepted. Conversely, the project

is not accepted if the IRR is less than the cost of capital of the company. From the

calculation it can be identified that the IRR of NEOROFORCE is 22%. Hence, it can be

5ACCOUNTING FINANCIAL ANALYSIS REPORT

stated that the project is acceptable as it can generate return even after meeting all the

required expenses associated with the project and is more the cost of capital of the

company that is 16% the and therefore it is acceptable.

Discounted payback period – it calculates the period taken by the project for recovering

the initial expenses made for acquiring the project. Discounted cash flow of the project is

considered for computation of discounted payback period of the project. When the entity

does not have any particular requirement regarding the payback period that is the

company is not in a hurry to recover the initial expenses, the project is accepted if the

initial amount is recover within the useful life of the project. Considering the discounted

payback period of the project, it can be identified that at 16% discount rate the discounted

payback period for NEOROFORCE is 5.17 year. Though the project is able to recover

the initial outlay within the useful life of the project, required discounted period of the

project is 5 years and hence, the project will not be acceptable.

2.2 Qualitative

From the above calculation and analysis it can be interpreted that the project’s NPV is

positive and is amounted to $ 62,22,596.45. Positive NPV signifies that if the project is taken up

it will create value for the company and will be able to generate return for the shareholders.

Hence, from the NPV aspect the project is acceptable. If the IRR is considered it can be stated

that the IRR of the project is 22%, that exceeds the company’s cost of capital that is 16%. Hence,

the project will be able to provide positive return to the company and is therefore acceptable.

Further, if the discounted payback period is considered it can be found that the initial expenses

for acquiring the project will be recovered in 5.17 years that is less that the projects useful life of

7 years. Hence, from all the aspects the project is acceptable. However, it is mentioned in the

stated that the project is acceptable as it can generate return even after meeting all the

required expenses associated with the project and is more the cost of capital of the

company that is 16% the and therefore it is acceptable.

Discounted payback period – it calculates the period taken by the project for recovering

the initial expenses made for acquiring the project. Discounted cash flow of the project is

considered for computation of discounted payback period of the project. When the entity

does not have any particular requirement regarding the payback period that is the

company is not in a hurry to recover the initial expenses, the project is accepted if the

initial amount is recover within the useful life of the project. Considering the discounted

payback period of the project, it can be identified that at 16% discount rate the discounted

payback period for NEOROFORCE is 5.17 year. Though the project is able to recover

the initial outlay within the useful life of the project, required discounted period of the

project is 5 years and hence, the project will not be acceptable.

2.2 Qualitative

From the above calculation and analysis it can be interpreted that the project’s NPV is

positive and is amounted to $ 62,22,596.45. Positive NPV signifies that if the project is taken up

it will create value for the company and will be able to generate return for the shareholders.

Hence, from the NPV aspect the project is acceptable. If the IRR is considered it can be stated

that the IRR of the project is 22%, that exceeds the company’s cost of capital that is 16%. Hence,

the project will be able to provide positive return to the company and is therefore acceptable.

Further, if the discounted payback period is considered it can be found that the initial expenses

for acquiring the project will be recovered in 5.17 years that is less that the projects useful life of

7 years. Hence, from all the aspects the project is acceptable. However, it is mentioned in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FINANCIAL ANALYSIS REPORT

given scenario that the required discounted payback period of the project for the company is 5

years whereas the actual discounted payback period of the project is 5.17 years which is more

than the required time. Hence, considering the payback period the project is not acceptable.

3. Recommendation and justification

Considering the above interpretation and analysis it can be stated that if the company

does not have any preference for the discounted payback period it shall be accepted as the project

is fulfilling the criteria of all the approaches used above that is NPV, IRR and discounted

payback period. However, as the company has preference for recovering the initial amount spend

for acquiring the project is 5 years, the projects shall not be accepted as the project will take

more than the preferred time that is 5.17 years for recovering the amount of initial outlay.

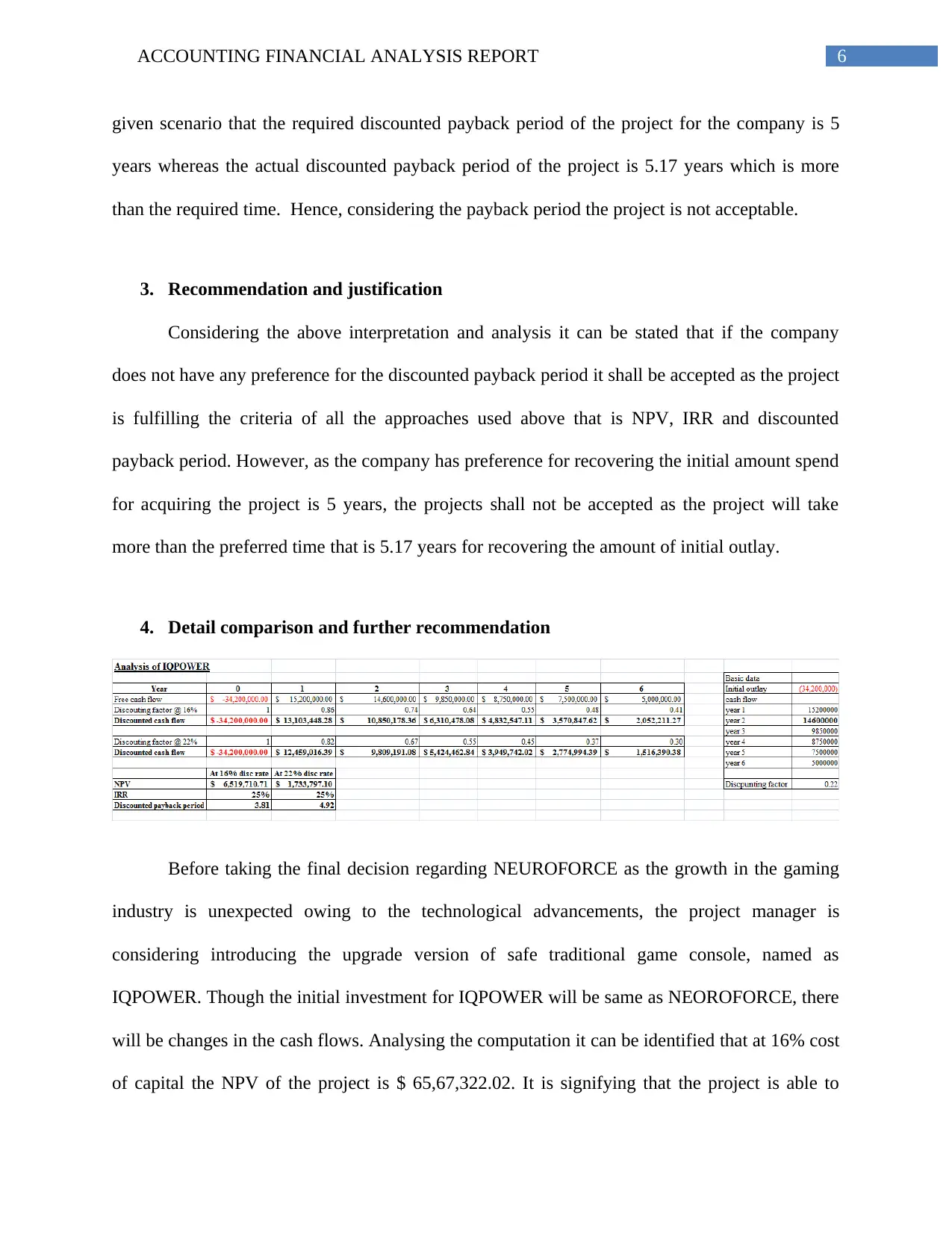

4. Detail comparison and further recommendation

Before taking the final decision regarding NEUROFORCE as the growth in the gaming

industry is unexpected owing to the technological advancements, the project manager is

considering introducing the upgrade version of safe traditional game console, named as

IQPOWER. Though the initial investment for IQPOWER will be same as NEOROFORCE, there

will be changes in the cash flows. Analysing the computation it can be identified that at 16% cost

of capital the NPV of the project is $ 65,67,322.02. It is signifying that the project is able to

given scenario that the required discounted payback period of the project for the company is 5

years whereas the actual discounted payback period of the project is 5.17 years which is more

than the required time. Hence, considering the payback period the project is not acceptable.

3. Recommendation and justification

Considering the above interpretation and analysis it can be stated that if the company

does not have any preference for the discounted payback period it shall be accepted as the project

is fulfilling the criteria of all the approaches used above that is NPV, IRR and discounted

payback period. However, as the company has preference for recovering the initial amount spend

for acquiring the project is 5 years, the projects shall not be accepted as the project will take

more than the preferred time that is 5.17 years for recovering the amount of initial outlay.

4. Detail comparison and further recommendation

Before taking the final decision regarding NEUROFORCE as the growth in the gaming

industry is unexpected owing to the technological advancements, the project manager is

considering introducing the upgrade version of safe traditional game console, named as

IQPOWER. Though the initial investment for IQPOWER will be same as NEOROFORCE, there

will be changes in the cash flows. Analysing the computation it can be identified that at 16% cost

of capital the NPV of the project is $ 65,67,322.02. It is signifying that the project is able to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYSIS REPORT

generate wealth for the shareholders of HITECH. Further, if the IRR of the project is considered

it can be stated that the IRR of the project is 25% which is more than the company’s cost of

capital. Moreover, the discounted payback period is 3.81 which is less that the company’s

required payback period of 5 years. Hence, from all the aspects the project is acceptable.

However, as the company’s WACC varies from 16% to 22%, the CF is asked to evaluate

both projects using the cost of capital as 22%. If other things remain same, at 22% the NPV of

NEUROFORCE is reduced to $ 109,913.01, IRR is same at 22% and discounted payback period

is increased to 6.96 years. Though at 22% NEOROFORCE project is still profitable, considering

its discounted payback period the project shall not be accepted. However, if the company does

not prefer to get the initial expenses of the project to be recovered by 5 years, the project can be

accepted as it is profitable. On the other hand, if the same 22% cost of capital is applied to

IQPOWER, its NPV will be reduced to $ 17,70,797.03, IRR will be same at 25% and discounted

payback period will still be lower than 5 years that is 4.91 years. Hence, from all aspects the

project is still acceptable at 22% cost of capital. Hence, it fulfils al the criteria for acceptance and

therefore shall be accepted.

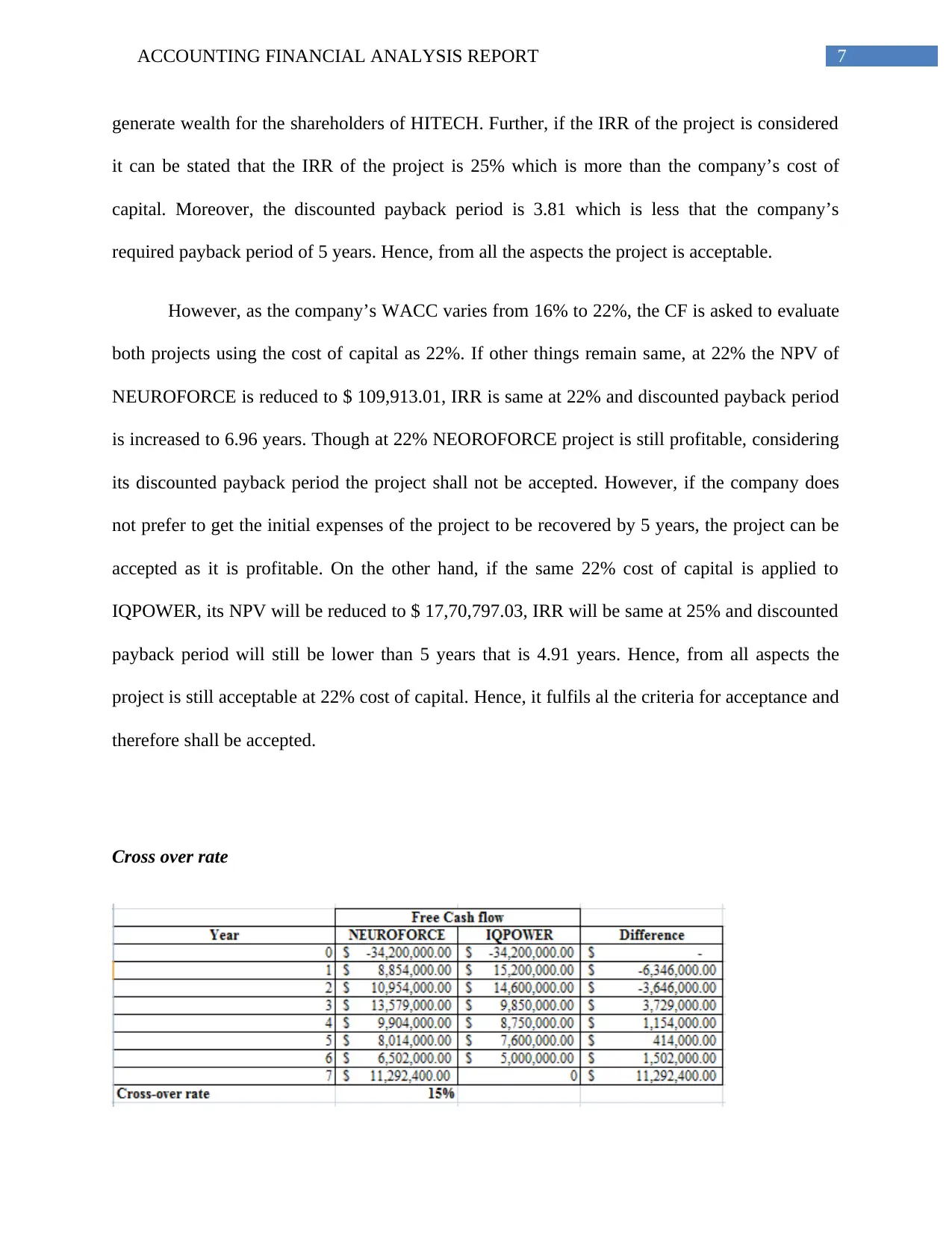

Cross over rate

generate wealth for the shareholders of HITECH. Further, if the IRR of the project is considered

it can be stated that the IRR of the project is 25% which is more than the company’s cost of

capital. Moreover, the discounted payback period is 3.81 which is less that the company’s

required payback period of 5 years. Hence, from all the aspects the project is acceptable.

However, as the company’s WACC varies from 16% to 22%, the CF is asked to evaluate

both projects using the cost of capital as 22%. If other things remain same, at 22% the NPV of

NEUROFORCE is reduced to $ 109,913.01, IRR is same at 22% and discounted payback period

is increased to 6.96 years. Though at 22% NEOROFORCE project is still profitable, considering

its discounted payback period the project shall not be accepted. However, if the company does

not prefer to get the initial expenses of the project to be recovered by 5 years, the project can be

accepted as it is profitable. On the other hand, if the same 22% cost of capital is applied to

IQPOWER, its NPV will be reduced to $ 17,70,797.03, IRR will be same at 25% and discounted

payback period will still be lower than 5 years that is 4.91 years. Hence, from all aspects the

project is still acceptable at 22% cost of capital. Hence, it fulfils al the criteria for acceptance and

therefore shall be accepted.

Cross over rate

8ACCOUNTING FINANCIAL ANALYSIS REPORT

Cross over rate is cost of capital where the NPV of both the projects care same. In other

words, at cross over rate NPV of one project intersects with NPV of another project. This

approach is useful to know at which rate both the project are equally good. It suggests that when

the company’s cost of capital crosses the crossover rate the comparative attractiveness for both

projects are altered. It can be observed from the computation carried out in excel that the

crossover rate for the projects mentioned above is 15%. Hence, at more than 15% of cost of

capital both projects attractiveness will be altered.

5. Conclusion

It is concluded on the basis of above interpretation and analysis of both the projects that

though NEUROFORCE is providing positive NPV at 16% as well as 22% and IRR is more than

the cost of capital, as it is not fulfilling the company’s criteria for required discounted payback

period of 5 years, the project is not acceptable. Conversely, IQPOWER is providing positive

NPV at 16% as well as 22% and IRR is more than the cost of capital and is fulfilling the

company’s criteria for required discounted payback period of 5 years it is acceptable at both 16%

as well as 22%. However, as the NPV is more at 16% and discounted payback period is less at

16% as compared to 22%, if given choice, the project shall be accepted at 16%.

Cross over rate is cost of capital where the NPV of both the projects care same. In other

words, at cross over rate NPV of one project intersects with NPV of another project. This

approach is useful to know at which rate both the project are equally good. It suggests that when

the company’s cost of capital crosses the crossover rate the comparative attractiveness for both

projects are altered. It can be observed from the computation carried out in excel that the

crossover rate for the projects mentioned above is 15%. Hence, at more than 15% of cost of

capital both projects attractiveness will be altered.

5. Conclusion

It is concluded on the basis of above interpretation and analysis of both the projects that

though NEUROFORCE is providing positive NPV at 16% as well as 22% and IRR is more than

the cost of capital, as it is not fulfilling the company’s criteria for required discounted payback

period of 5 years, the project is not acceptable. Conversely, IQPOWER is providing positive

NPV at 16% as well as 22% and IRR is more than the cost of capital and is fulfilling the

company’s criteria for required discounted payback period of 5 years it is acceptable at both 16%

as well as 22%. However, as the NPV is more at 16% and discounted payback period is less at

16% as compared to 22%, if given choice, the project shall be accepted at 16%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FINANCIAL ANALYSIS REPORT

Bibliography

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Corporate Finance Institute., 2019. Crossover Rate - Formula, Examples, and Guide to Discount

Rate, NPV. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/valuation/crossover-rate/ [Accessed 7

May 2019].

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Dhavale, D. G., and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89, 324-336.

Fleten, S. E., Linnerud, K., Molnár, P., and Nygaard, M. T., 2016. Green electricity investment

timing in practice: Real options or net present value?. Energy, 116, 498-506.

Gaudard, L., 2015. Pumped-storage project: A short to long term investment analysis including

climate change. Renewable and Sustainable Energy Reviews, 49, 91-99.

Götze, U., Northcott, D., and Schuster, P., 2015. Discounted Cash Flow Methods. In Investment

Appraisal (pp. 47-83). Springer, Berlin, Heidelberg.

Qiu, Y., Wang, Y. D., and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), 2218-2233.

Bibliography

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Corporate Finance Institute., 2019. Crossover Rate - Formula, Examples, and Guide to Discount

Rate, NPV. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/valuation/crossover-rate/ [Accessed 7

May 2019].

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Dhavale, D. G., and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89, 324-336.

Fleten, S. E., Linnerud, K., Molnár, P., and Nygaard, M. T., 2016. Green electricity investment

timing in practice: Real options or net present value?. Energy, 116, 498-506.

Gaudard, L., 2015. Pumped-storage project: A short to long term investment analysis including

climate change. Renewable and Sustainable Energy Reviews, 49, 91-99.

Götze, U., Northcott, D., and Schuster, P., 2015. Discounted Cash Flow Methods. In Investment

Appraisal (pp. 47-83). Springer, Berlin, Heidelberg.

Qiu, Y., Wang, Y. D., and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), 2218-2233.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FINANCIAL ANALYSIS REPORT

Santandrea, M., Sironi, A., Grassi, L., and Giorgino, M., 2017. Concentration risk and internal

rate of return: Evidence from the infrastructure equity market. International Journal of Project

Management, 35(3), 241-251.

Shu, S. B., Zeithammer, R., and Payne, J. W., 2016. Consumer preferences for annuity attributes:

Beyond net present value. Journal of Marketing Research, 53(2), 240-262.

Santandrea, M., Sironi, A., Grassi, L., and Giorgino, M., 2017. Concentration risk and internal

rate of return: Evidence from the infrastructure equity market. International Journal of Project

Management, 35(3), 241-251.

Shu, S. B., Zeithammer, R., and Payne, J. W., 2016. Consumer preferences for annuity attributes:

Beyond net present value. Journal of Marketing Research, 53(2), 240-262.

11ACCOUNTING FINANCIAL ANALYSIS REPORT

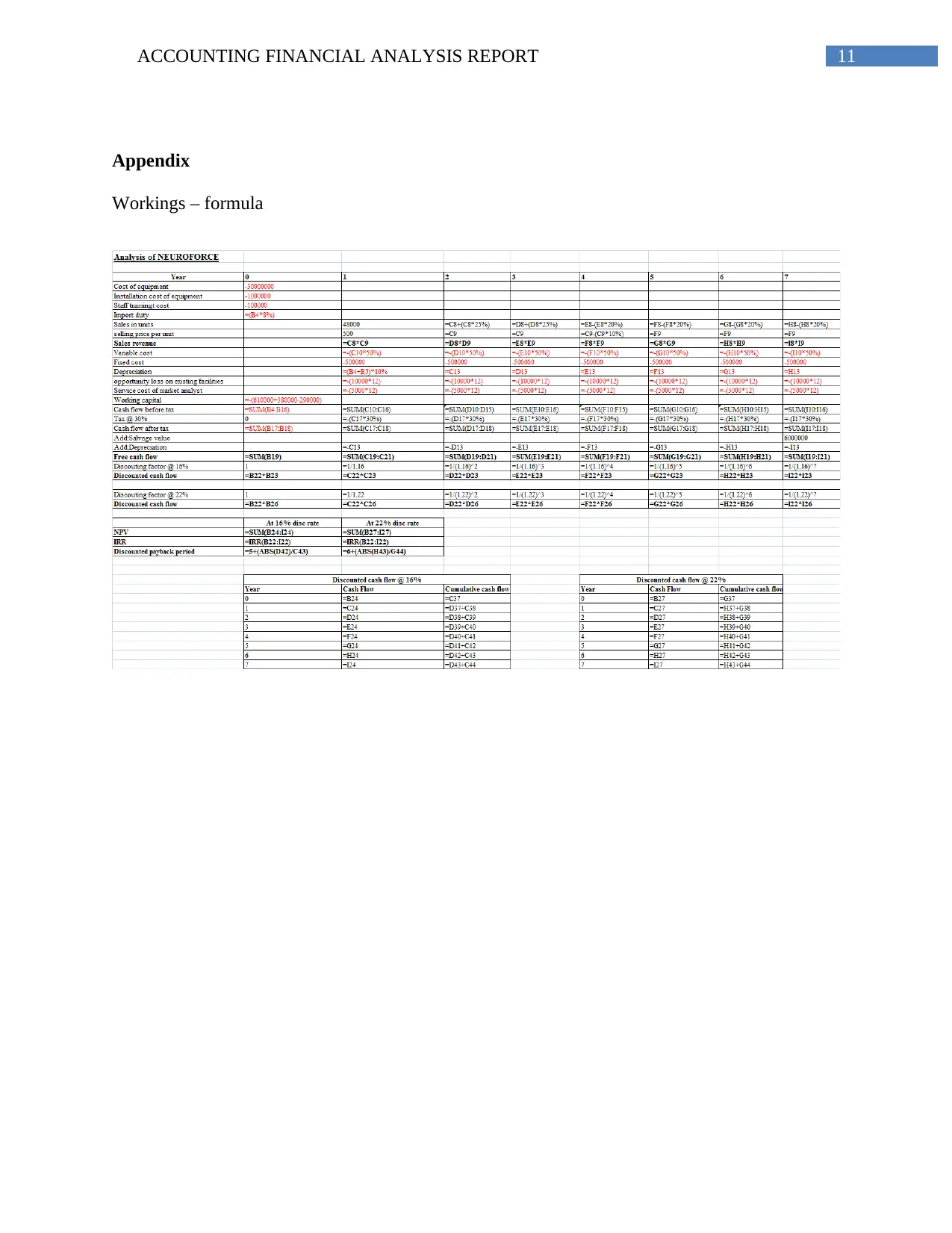

Appendix

Workings – formula

Appendix

Workings – formula

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.