Comprehensive Accounting and Financial Analysis Assignment - Finance

VerifiedAdded on 2023/04/19

|15

|2563

|97

Homework Assignment

AI Summary

This finance assignment delves into various aspects of accounting and financial analysis. It begins with calculations related to loan payments, comparing weekly and fortnightly payment schedules, and analyzing investment returns for different scenarios. The assignment then explores dividend policies, comparing classical and imputation taxation systems and their impact on investors. It analyzes the differences in tax methods, reduction in double taxation, and the impact on investor's investments. The assignment also includes detailed calculations of returns, standard deviations, and portfolio analysis, utilizing the Capital Asset Pricing Model (CAPM) to evaluate expected returns and risks for different assets. The analysis covers both individual asset performance and portfolio optimization, providing a comprehensive overview of financial concepts.

Running head: ACCOUNTING & FINANCIAL

Accounting & Financial

Name of the Student:

Name of the University:

Authors Note:

Accounting & Financial

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING & FINANCIAL 2

Table of Contents

Question 1:.................................................................................................................................3

Answer to a.i):............................................................................................................................3

Answer to a.ii):...........................................................................................................................3

Answer to b.i):............................................................................................................................4

Answer to b.ii):...........................................................................................................................4

Answer to b.iii):.........................................................................................................................4

Question 2:.................................................................................................................................5

Answer to i):...............................................................................................................................5

Answer to ii):..............................................................................................................................5

Question 3:.................................................................................................................................6

Answer to i):...............................................................................................................................6

Answer to ii):..............................................................................................................................7

Answer to iii):............................................................................................................................9

Question 4:...............................................................................................................................10

Answer to 1):............................................................................................................................10

Answer to 2):............................................................................................................................11

Answer to 3):............................................................................................................................11

Answer to 4):............................................................................................................................12

Answer to 5):............................................................................................................................12

Answer to 6):............................................................................................................................12

Answer to 7):............................................................................................................................13

Answer to 8):............................................................................................................................13

Answer to 9):............................................................................................................................13

Reference and Bibliography:....................................................................................................14

Table of Contents

Question 1:.................................................................................................................................3

Answer to a.i):............................................................................................................................3

Answer to a.ii):...........................................................................................................................3

Answer to b.i):............................................................................................................................4

Answer to b.ii):...........................................................................................................................4

Answer to b.iii):.........................................................................................................................4

Question 2:.................................................................................................................................5

Answer to i):...............................................................................................................................5

Answer to ii):..............................................................................................................................5

Question 3:.................................................................................................................................6

Answer to i):...............................................................................................................................6

Answer to ii):..............................................................................................................................7

Answer to iii):............................................................................................................................9

Question 4:...............................................................................................................................10

Answer to 1):............................................................................................................................10

Answer to 2):............................................................................................................................11

Answer to 3):............................................................................................................................11

Answer to 4):............................................................................................................................12

Answer to 5):............................................................................................................................12

Answer to 6):............................................................................................................................12

Answer to 7):............................................................................................................................13

Answer to 8):............................................................................................................................13

Answer to 9):............................................................................................................................13

Reference and Bibliography:....................................................................................................14

ACCOUNTING & FINANCIAL 3

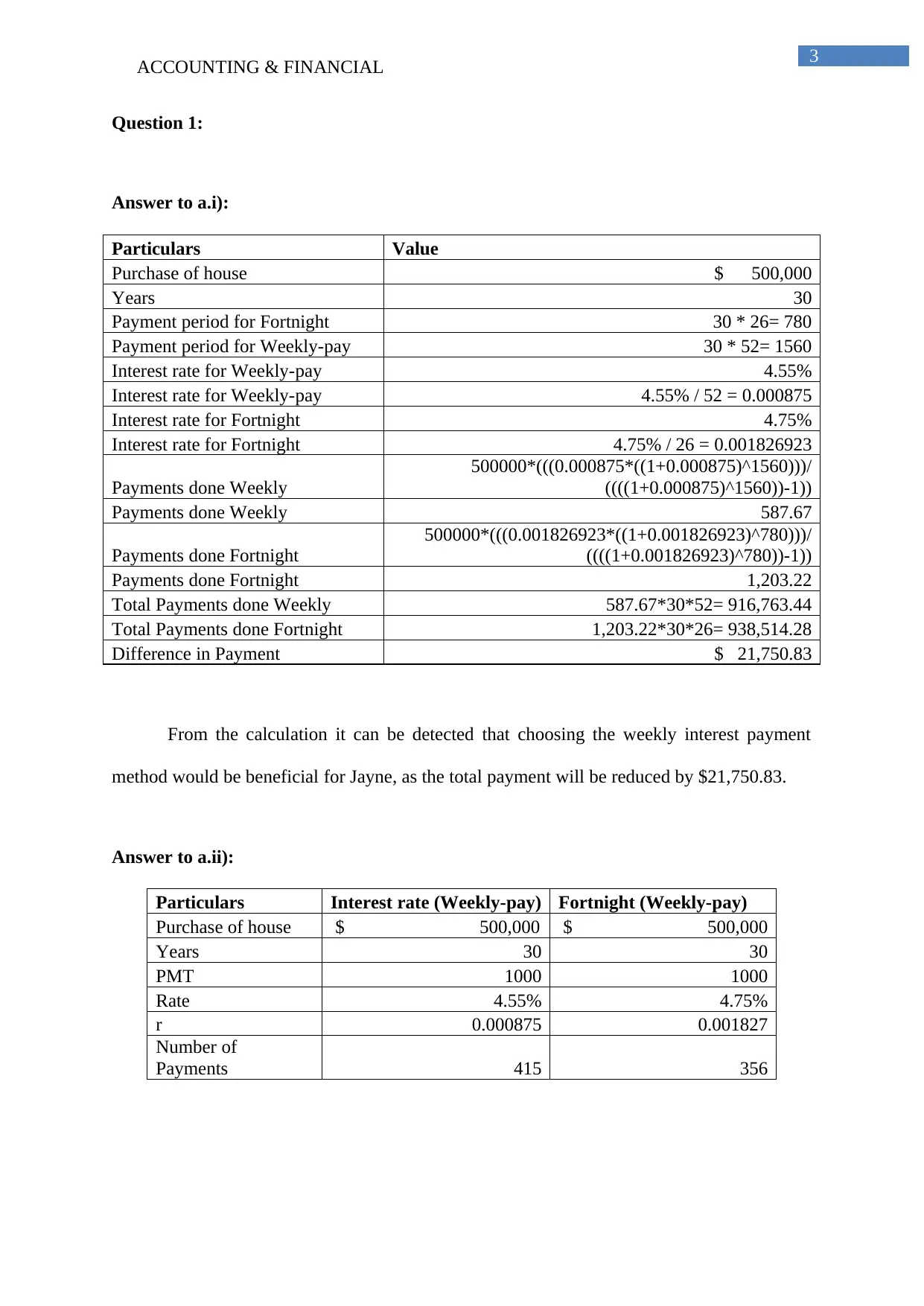

Question 1:

Answer to a.i):

Particulars Value

Purchase of house $ 500,000

Years 30

Payment period for Fortnight 30 * 26= 780

Payment period for Weekly-pay 30 * 52= 1560

Interest rate for Weekly-pay 4.55%

Interest rate for Weekly-pay 4.55% / 52 = 0.000875

Interest rate for Fortnight 4.75%

Interest rate for Fortnight 4.75% / 26 = 0.001826923

Payments done Weekly

500000*(((0.000875*((1+0.000875)^1560)))/

((((1+0.000875)^1560))-1))

Payments done Weekly 587.67

Payments done Fortnight

500000*(((0.001826923*((1+0.001826923)^780)))/

((((1+0.001826923)^780))-1))

Payments done Fortnight 1,203.22

Total Payments done Weekly 587.67*30*52= 916,763.44

Total Payments done Fortnight 1,203.22*30*26= 938,514.28

Difference in Payment $ 21,750.83

From the calculation it can be detected that choosing the weekly interest payment

method would be beneficial for Jayne, as the total payment will be reduced by $21,750.83.

Answer to a.ii):

Particulars Interest rate (Weekly-pay) Fortnight (Weekly-pay)

Purchase of house $ 500,000 $ 500,000

Years 30 30

PMT 1000 1000

Rate 4.55% 4.75%

r 0.000875 0.001827

Number of

Payments 415 356

Question 1:

Answer to a.i):

Particulars Value

Purchase of house $ 500,000

Years 30

Payment period for Fortnight 30 * 26= 780

Payment period for Weekly-pay 30 * 52= 1560

Interest rate for Weekly-pay 4.55%

Interest rate for Weekly-pay 4.55% / 52 = 0.000875

Interest rate for Fortnight 4.75%

Interest rate for Fortnight 4.75% / 26 = 0.001826923

Payments done Weekly

500000*(((0.000875*((1+0.000875)^1560)))/

((((1+0.000875)^1560))-1))

Payments done Weekly 587.67

Payments done Fortnight

500000*(((0.001826923*((1+0.001826923)^780)))/

((((1+0.001826923)^780))-1))

Payments done Fortnight 1,203.22

Total Payments done Weekly 587.67*30*52= 916,763.44

Total Payments done Fortnight 1,203.22*30*26= 938,514.28

Difference in Payment $ 21,750.83

From the calculation it can be detected that choosing the weekly interest payment

method would be beneficial for Jayne, as the total payment will be reduced by $21,750.83.

Answer to a.ii):

Particulars Interest rate (Weekly-pay) Fortnight (Weekly-pay)

Purchase of house $ 500,000 $ 500,000

Years 30 30

PMT 1000 1000

Rate 4.55% 4.75%

r 0.000875 0.001827

Number of

Payments 415 356

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING & FINANCIAL 4

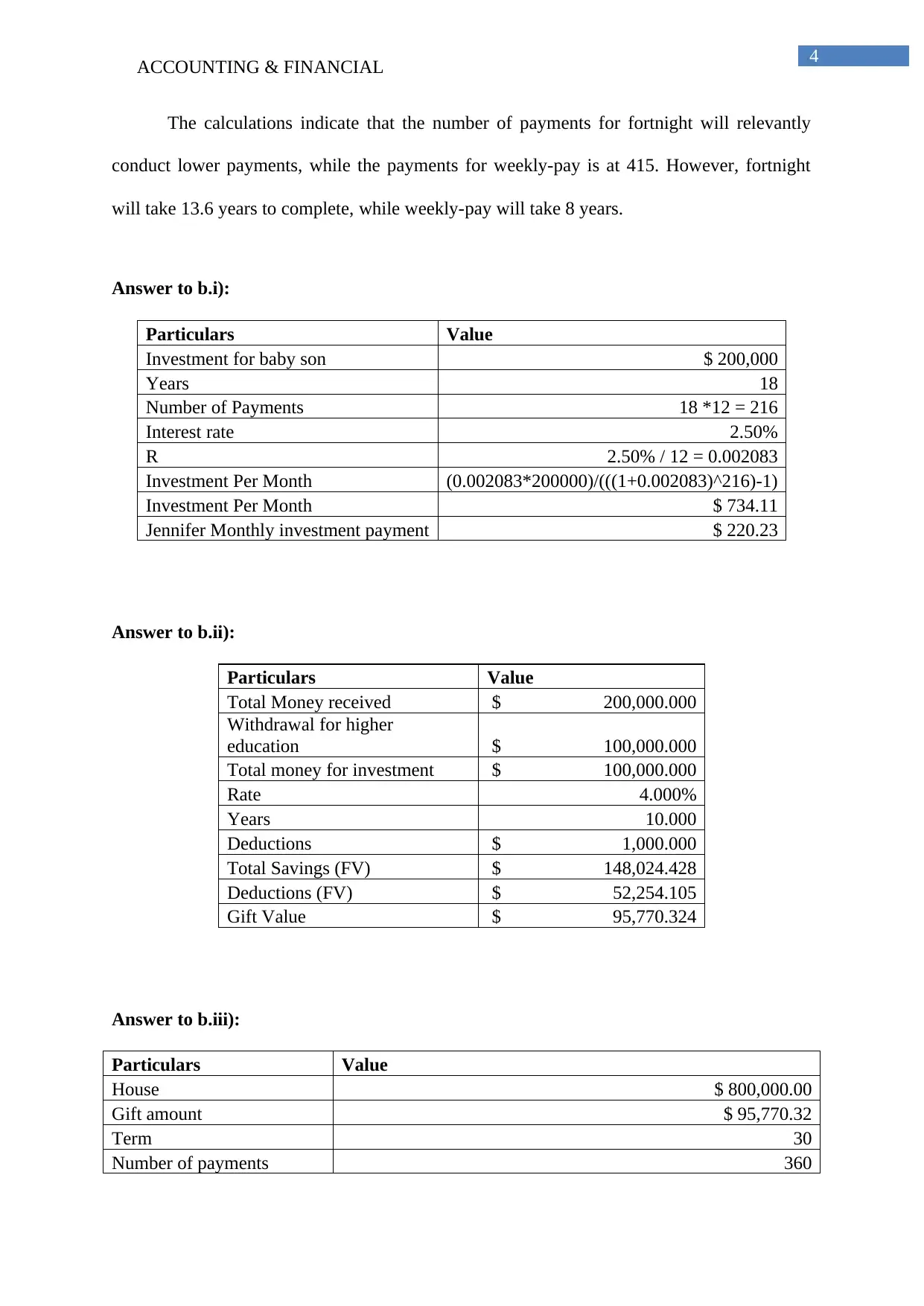

The calculations indicate that the number of payments for fortnight will relevantly

conduct lower payments, while the payments for weekly-pay is at 415. However, fortnight

will take 13.6 years to complete, while weekly-pay will take 8 years.

Answer to b.i):

Particulars Value

Investment for baby son $ 200,000

Years 18

Number of Payments 18 *12 = 216

Interest rate 2.50%

R 2.50% / 12 = 0.002083

Investment Per Month (0.002083*200000)/(((1+0.002083)^216)-1)

Investment Per Month $ 734.11

Jennifer Monthly investment payment $ 220.23

Answer to b.ii):

Particulars Value

Total Money received $ 200,000.000

Withdrawal for higher

education $ 100,000.000

Total money for investment $ 100,000.000

Rate 4.000%

Years 10.000

Deductions $ 1,000.000

Total Savings (FV) $ 148,024.428

Deductions (FV) $ 52,254.105

Gift Value $ 95,770.324

Answer to b.iii):

Particulars Value

House $ 800,000.00

Gift amount $ 95,770.32

Term 30

Number of payments 360

The calculations indicate that the number of payments for fortnight will relevantly

conduct lower payments, while the payments for weekly-pay is at 415. However, fortnight

will take 13.6 years to complete, while weekly-pay will take 8 years.

Answer to b.i):

Particulars Value

Investment for baby son $ 200,000

Years 18

Number of Payments 18 *12 = 216

Interest rate 2.50%

R 2.50% / 12 = 0.002083

Investment Per Month (0.002083*200000)/(((1+0.002083)^216)-1)

Investment Per Month $ 734.11

Jennifer Monthly investment payment $ 220.23

Answer to b.ii):

Particulars Value

Total Money received $ 200,000.000

Withdrawal for higher

education $ 100,000.000

Total money for investment $ 100,000.000

Rate 4.000%

Years 10.000

Deductions $ 1,000.000

Total Savings (FV) $ 148,024.428

Deductions (FV) $ 52,254.105

Gift Value $ 95,770.324

Answer to b.iii):

Particulars Value

House $ 800,000.00

Gift amount $ 95,770.32

Term 30

Number of payments 360

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING & FINANCIAL 5

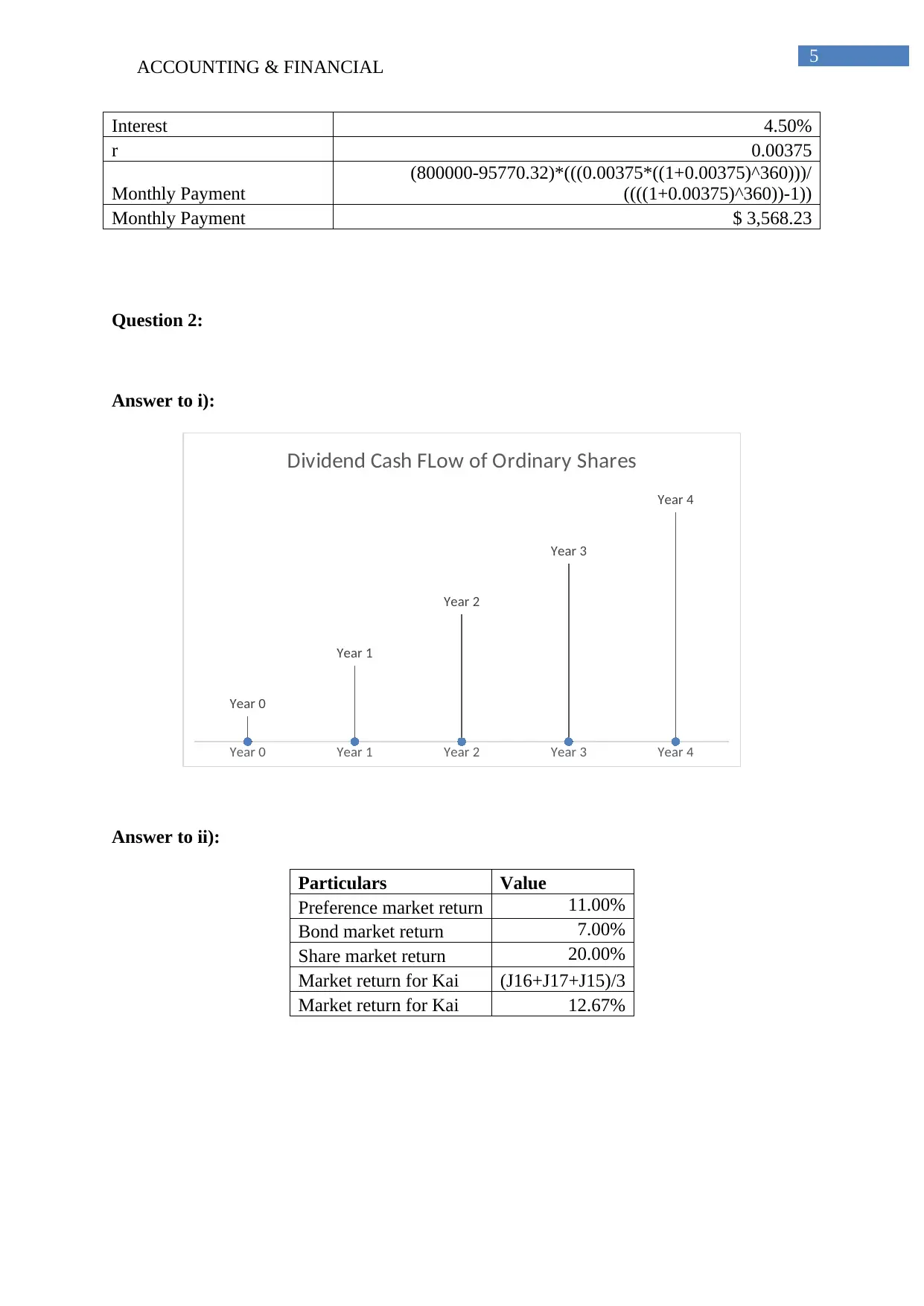

Interest 4.50%

r 0.00375

Monthly Payment

(800000-95770.32)*(((0.00375*((1+0.00375)^360)))/

((((1+0.00375)^360))-1))

Monthly Payment $ 3,568.23

Question 2:

Answer to i):

Year 0 Year 1 Year 2 Year 3 Year 4

Year 0

Year 1

Year 2

Year 3

Year 4

Dividend Cash FLow of Ordinary Shares

Answer to ii):

Particulars Value

Preference market return 11.00%

Bond market return 7.00%

Share market return 20.00%

Market return for Kai (J16+J17+J15)/3

Market return for Kai 12.67%

Interest 4.50%

r 0.00375

Monthly Payment

(800000-95770.32)*(((0.00375*((1+0.00375)^360)))/

((((1+0.00375)^360))-1))

Monthly Payment $ 3,568.23

Question 2:

Answer to i):

Year 0 Year 1 Year 2 Year 3 Year 4

Year 0

Year 1

Year 2

Year 3

Year 4

Dividend Cash FLow of Ordinary Shares

Answer to ii):

Particulars Value

Preference market return 11.00%

Bond market return 7.00%

Share market return 20.00%

Market return for Kai (J16+J17+J15)/3

Market return for Kai 12.67%

ACCOUNTING & FINANCIAL 6

Question 3:

Answer to i):

There is significant difference between classical taxation system and imputation

taxation system, which are used by the regulator to extract relevant taxes from companies and

individuals. With the help of classical taxation system, the regulators for conducting double

taxation on the investors that received dividend from organizations. However, the imputation

taxation system helped in minimizing the chance of double taxation that was being conducted

by regulators. The classical taxation system is still being implemented by majority of the

countries around the world, while some of the countries such as Australia and New Zealand

in using imputation taxation system to infuse growth in its financial market by luring both

international and domestic investors (Faccio & Xu, 2015).

Difference tax method: Both the classical taxation system and imputation taxation

system has a different tax method which is imposed on companies and investors.

Under the classical taxation system, the organization needs to pay the taxes before

delivering the dividend and after receiving the dividend investors need to pay taxes

according to their marginal tax rate. However, under the imputation taxation system

the organization need to pay the taxes before delivering the dividend, after which the

investors can use the tax credits to reduce the level of cash outflow and increase the

dividend payments.

Reduction in double taxation: The classical taxation system relatively motivated the

authorities to conduct double taxation and reduce the level of dividend income of the

investors. However, under the imputation taxation system the investors are able to

deduct the tax credits and reduce the level of Tax amount of the investors. Therefore,

Question 3:

Answer to i):

There is significant difference between classical taxation system and imputation

taxation system, which are used by the regulator to extract relevant taxes from companies and

individuals. With the help of classical taxation system, the regulators for conducting double

taxation on the investors that received dividend from organizations. However, the imputation

taxation system helped in minimizing the chance of double taxation that was being conducted

by regulators. The classical taxation system is still being implemented by majority of the

countries around the world, while some of the countries such as Australia and New Zealand

in using imputation taxation system to infuse growth in its financial market by luring both

international and domestic investors (Faccio & Xu, 2015).

Difference tax method: Both the classical taxation system and imputation taxation

system has a different tax method which is imposed on companies and investors.

Under the classical taxation system, the organization needs to pay the taxes before

delivering the dividend and after receiving the dividend investors need to pay taxes

according to their marginal tax rate. However, under the imputation taxation system

the organization need to pay the taxes before delivering the dividend, after which the

investors can use the tax credits to reduce the level of cash outflow and increase the

dividend payments.

Reduction in double taxation: The classical taxation system relatively motivated the

authorities to conduct double taxation and reduce the level of dividend income of the

investors. However, under the imputation taxation system the investors are able to

deduct the tax credits and reduce the level of Tax amount of the investors. Therefore,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING & FINANCIAL 7

double taxation measure is the major difference between the classical taxation system

and imputation taxation system.

Increment in investor’s investment: Under the classical taxation, system investors are

relatively charged more for the dividend as they are double taxed on their investment

returns. This mainly demotivates the investors in conducting adequate investments in

a particular market that increases the level of cost of investment. On the other hand,

imputation taxation system relatively reduces the excessive cost that is incurred by

investors in conducting investments which relatively increases the investor’s

investment in a particular financial market. Both International and Domestic investors

want imputation taxation system, as it minimizes the level of cash outflow from

investments (Nguyen, 2016).

Answer to ii):

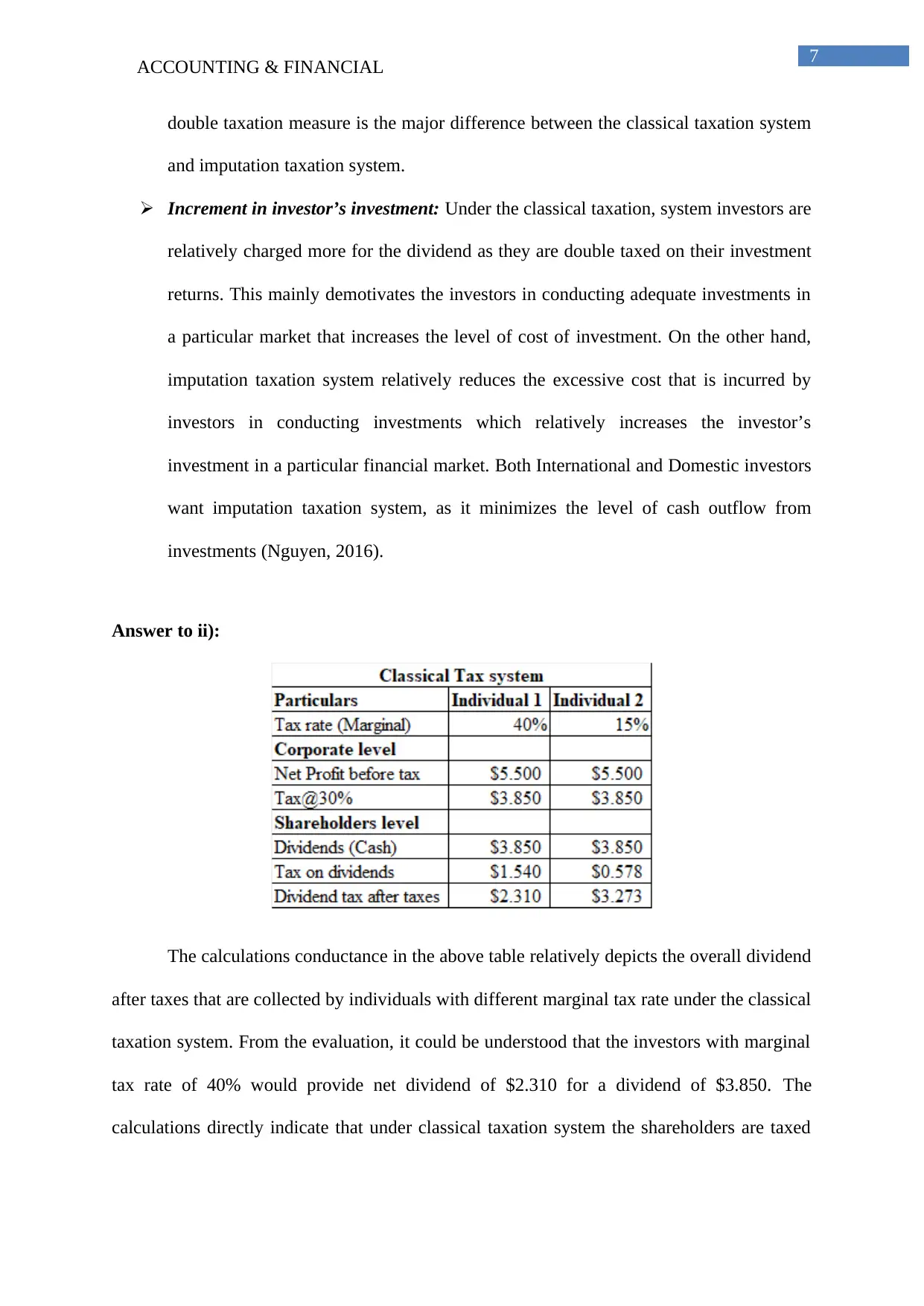

The calculations conductance in the above table relatively depicts the overall dividend

after taxes that are collected by individuals with different marginal tax rate under the classical

taxation system. From the evaluation, it could be understood that the investors with marginal

tax rate of 40% would provide net dividend of $2.310 for a dividend of $3.850. The

calculations directly indicate that under classical taxation system the shareholders are taxed

double taxation measure is the major difference between the classical taxation system

and imputation taxation system.

Increment in investor’s investment: Under the classical taxation, system investors are

relatively charged more for the dividend as they are double taxed on their investment

returns. This mainly demotivates the investors in conducting adequate investments in

a particular market that increases the level of cost of investment. On the other hand,

imputation taxation system relatively reduces the excessive cost that is incurred by

investors in conducting investments which relatively increases the investor’s

investment in a particular financial market. Both International and Domestic investors

want imputation taxation system, as it minimizes the level of cash outflow from

investments (Nguyen, 2016).

Answer to ii):

The calculations conductance in the above table relatively depicts the overall dividend

after taxes that are collected by individuals with different marginal tax rate under the classical

taxation system. From the evaluation, it could be understood that the investors with marginal

tax rate of 40% would provide net dividend of $2.310 for a dividend of $3.850. The

calculations directly indicate that under classical taxation system the shareholders are taxed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING & FINANCIAL 8

double, which reduces the level of dividend payments of the investors., which can eventually

help in generating high level of cash inflow for the investors.

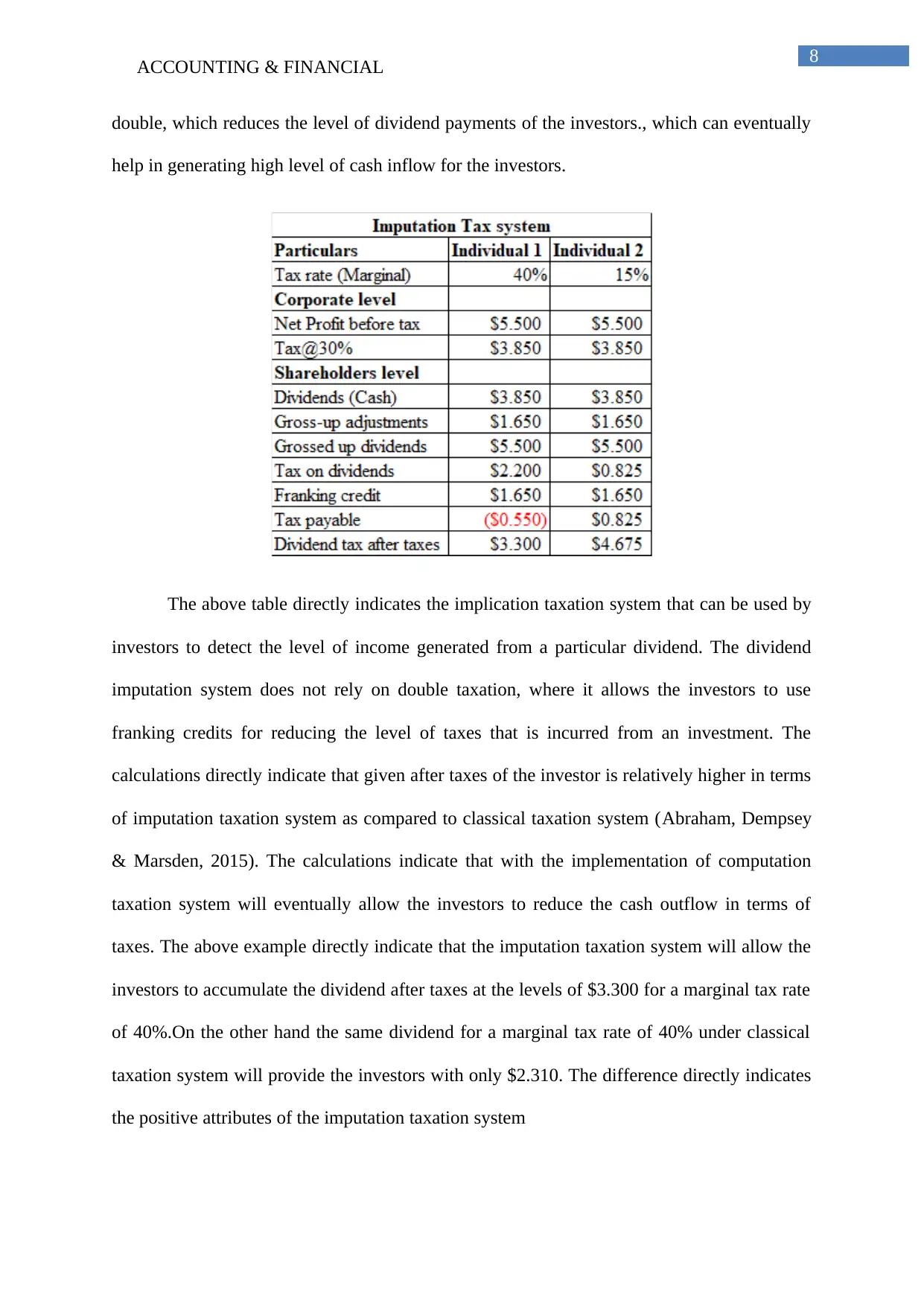

The above table directly indicates the implication taxation system that can be used by

investors to detect the level of income generated from a particular dividend. The dividend

imputation system does not rely on double taxation, where it allows the investors to use

franking credits for reducing the level of taxes that is incurred from an investment. The

calculations directly indicate that given after taxes of the investor is relatively higher in terms

of imputation taxation system as compared to classical taxation system (Abraham, Dempsey

& Marsden, 2015). The calculations indicate that with the implementation of computation

taxation system will eventually allow the investors to reduce the cash outflow in terms of

taxes. The above example directly indicate that the imputation taxation system will allow the

investors to accumulate the dividend after taxes at the levels of $3.300 for a marginal tax rate

of 40%.On the other hand the same dividend for a marginal tax rate of 40% under classical

taxation system will provide the investors with only $2.310. The difference directly indicates

the positive attributes of the imputation taxation system

double, which reduces the level of dividend payments of the investors., which can eventually

help in generating high level of cash inflow for the investors.

The above table directly indicates the implication taxation system that can be used by

investors to detect the level of income generated from a particular dividend. The dividend

imputation system does not rely on double taxation, where it allows the investors to use

franking credits for reducing the level of taxes that is incurred from an investment. The

calculations directly indicate that given after taxes of the investor is relatively higher in terms

of imputation taxation system as compared to classical taxation system (Abraham, Dempsey

& Marsden, 2015). The calculations indicate that with the implementation of computation

taxation system will eventually allow the investors to reduce the cash outflow in terms of

taxes. The above example directly indicate that the imputation taxation system will allow the

investors to accumulate the dividend after taxes at the levels of $3.300 for a marginal tax rate

of 40%.On the other hand the same dividend for a marginal tax rate of 40% under classical

taxation system will provide the investors with only $2.310. The difference directly indicates

the positive attributes of the imputation taxation system

ACCOUNTING & FINANCIAL 9

Answer to iii):

The imputation taxation system has relevant impact on both the domestic and

international investors, as it increases the level of Income for the investors. Imputation

system has a relevant impact on the decision-making capability of the investors as it allows

them to generate high level of income ignorance of double taxation method. Countries such

as New Zealand and Australia are relatively using imputation taxation system to lure in more

investors and increase investment from both domestic and international investors. Decision

making capability of the investors are relatively impact by the imputation taxation system, as

investors tend to reduce the level of cost incurred from investment by ignoring the countries

using classical taxation system. This measure relatively helps the investors to increase the

level of income from investment while reducing the tax cash outflow. This measure but

relatively increase the level of investment from both International and domestic investors, as

we can earn higher returns from investment. Furthermore, alterations in dividend policy of

the company would also have impact on the investors decision-making capabilities, as

investors will raise the level of investment in an organization, due to the low level of cost

incurred from investment (Nguyen, 2016).

Answer to iii):

The imputation taxation system has relevant impact on both the domestic and

international investors, as it increases the level of Income for the investors. Imputation

system has a relevant impact on the decision-making capability of the investors as it allows

them to generate high level of income ignorance of double taxation method. Countries such

as New Zealand and Australia are relatively using imputation taxation system to lure in more

investors and increase investment from both domestic and international investors. Decision

making capability of the investors are relatively impact by the imputation taxation system, as

investors tend to reduce the level of cost incurred from investment by ignoring the countries

using classical taxation system. This measure relatively helps the investors to increase the

level of income from investment while reducing the tax cash outflow. This measure but

relatively increase the level of investment from both International and domestic investors, as

we can earn higher returns from investment. Furthermore, alterations in dividend policy of

the company would also have impact on the investors decision-making capabilities, as

investors will raise the level of investment in an organization, due to the low level of cost

incurred from investment (Nguyen, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING & FINANCIAL 10

Question 4:

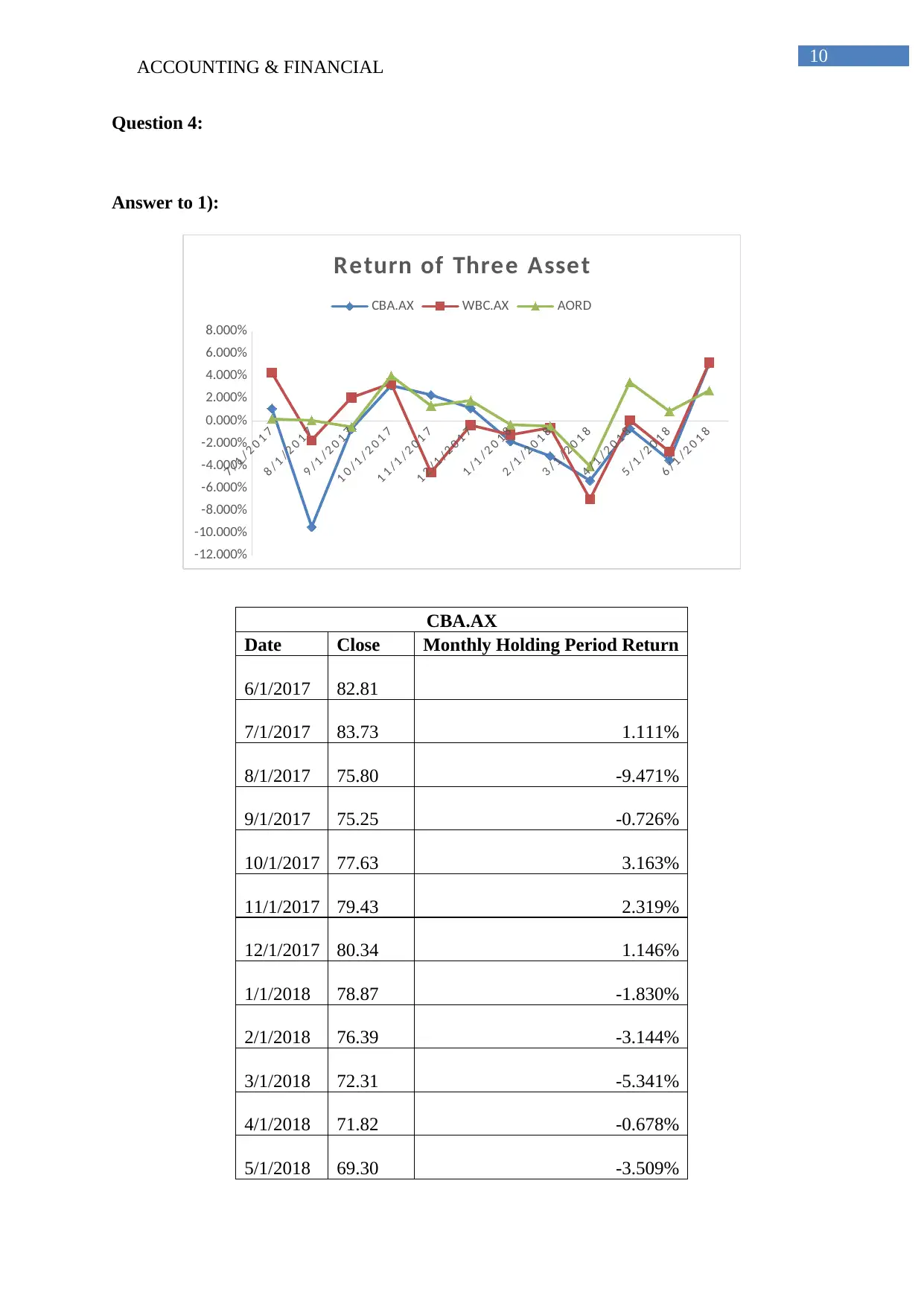

Answer to 1):

7 / 1 / 2 0 1 7

8 / 1 / 2 0 1 7

9 / 1 / 2 0 1 7

1 0 / 1 / 2 0 1 7

1 1 / 1 / 2 0 1 7

1 2 / 1 / 2 0 1 7

1 / 1 / 2 0 1 8

2 / 1 / 2 0 1 8

3 / 1 / 2 0 1 8

4 / 1 / 2 0 1 8

5 / 1 / 2 0 1 8

6 / 1 / 2 0 1 8

-12.000%

-10.000%

-8.000%

-6.000%

-4.000%

-2.000%

0.000%

2.000%

4.000%

6.000%

8.000%

Return of Three Asset

CBA.AX WBC.AX AORD

CBA.AX

Date Close Monthly Holding Period Return

6/1/2017 82.81

7/1/2017 83.73 1.111%

8/1/2017 75.80 -9.471%

9/1/2017 75.25 -0.726%

10/1/2017 77.63 3.163%

11/1/2017 79.43 2.319%

12/1/2017 80.34 1.146%

1/1/2018 78.87 -1.830%

2/1/2018 76.39 -3.144%

3/1/2018 72.31 -5.341%

4/1/2018 71.82 -0.678%

5/1/2018 69.30 -3.509%

Question 4:

Answer to 1):

7 / 1 / 2 0 1 7

8 / 1 / 2 0 1 7

9 / 1 / 2 0 1 7

1 0 / 1 / 2 0 1 7

1 1 / 1 / 2 0 1 7

1 2 / 1 / 2 0 1 7

1 / 1 / 2 0 1 8

2 / 1 / 2 0 1 8

3 / 1 / 2 0 1 8

4 / 1 / 2 0 1 8

5 / 1 / 2 0 1 8

6 / 1 / 2 0 1 8

-12.000%

-10.000%

-8.000%

-6.000%

-4.000%

-2.000%

0.000%

2.000%

4.000%

6.000%

8.000%

Return of Three Asset

CBA.AX WBC.AX AORD

CBA.AX

Date Close Monthly Holding Period Return

6/1/2017 82.81

7/1/2017 83.73 1.111%

8/1/2017 75.80 -9.471%

9/1/2017 75.25 -0.726%

10/1/2017 77.63 3.163%

11/1/2017 79.43 2.319%

12/1/2017 80.34 1.146%

1/1/2018 78.87 -1.830%

2/1/2018 76.39 -3.144%

3/1/2018 72.31 -5.341%

4/1/2018 71.82 -0.678%

5/1/2018 69.30 -3.509%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING & FINANCIAL 11

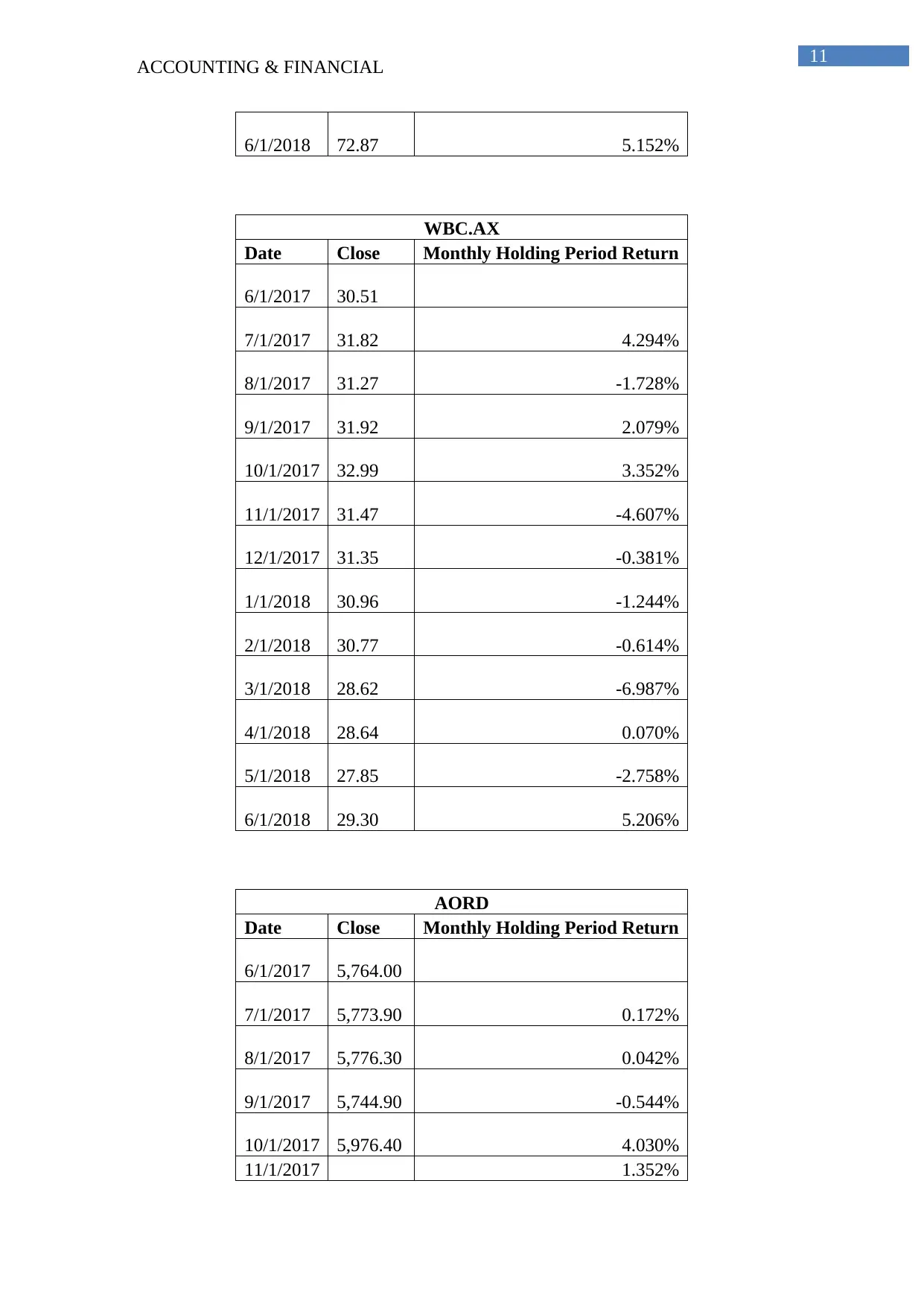

6/1/2018 72.87 5.152%

WBC.AX

Date Close Monthly Holding Period Return

6/1/2017 30.51

7/1/2017 31.82 4.294%

8/1/2017 31.27 -1.728%

9/1/2017 31.92 2.079%

10/1/2017 32.99 3.352%

11/1/2017 31.47 -4.607%

12/1/2017 31.35 -0.381%

1/1/2018 30.96 -1.244%

2/1/2018 30.77 -0.614%

3/1/2018 28.62 -6.987%

4/1/2018 28.64 0.070%

5/1/2018 27.85 -2.758%

6/1/2018 29.30 5.206%

AORD

Date Close Monthly Holding Period Return

6/1/2017 5,764.00

7/1/2017 5,773.90 0.172%

8/1/2017 5,776.30 0.042%

9/1/2017 5,744.90 -0.544%

10/1/2017 5,976.40 4.030%

11/1/2017 1.352%

6/1/2018 72.87 5.152%

WBC.AX

Date Close Monthly Holding Period Return

6/1/2017 30.51

7/1/2017 31.82 4.294%

8/1/2017 31.27 -1.728%

9/1/2017 31.92 2.079%

10/1/2017 32.99 3.352%

11/1/2017 31.47 -4.607%

12/1/2017 31.35 -0.381%

1/1/2018 30.96 -1.244%

2/1/2018 30.77 -0.614%

3/1/2018 28.62 -6.987%

4/1/2018 28.64 0.070%

5/1/2018 27.85 -2.758%

6/1/2018 29.30 5.206%

AORD

Date Close Monthly Holding Period Return

6/1/2017 5,764.00

7/1/2017 5,773.90 0.172%

8/1/2017 5,776.30 0.042%

9/1/2017 5,744.90 -0.544%

10/1/2017 5,976.40 4.030%

11/1/2017 1.352%

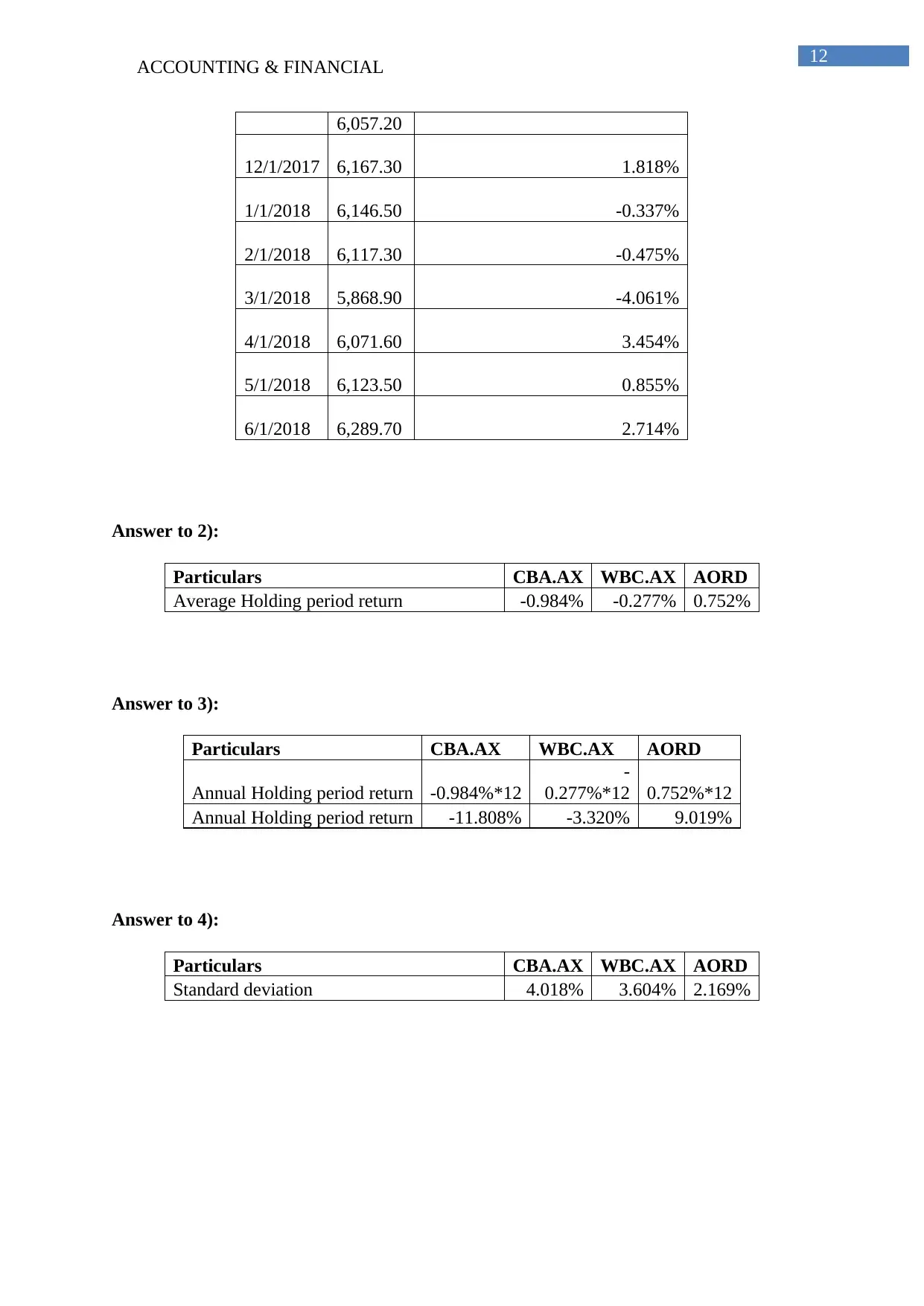

ACCOUNTING & FINANCIAL 12

6,057.20

12/1/2017 6,167.30 1.818%

1/1/2018 6,146.50 -0.337%

2/1/2018 6,117.30 -0.475%

3/1/2018 5,868.90 -4.061%

4/1/2018 6,071.60 3.454%

5/1/2018 6,123.50 0.855%

6/1/2018 6,289.70 2.714%

Answer to 2):

Particulars CBA.AX WBC.AX AORD

Average Holding period return -0.984% -0.277% 0.752%

Answer to 3):

Particulars CBA.AX WBC.AX AORD

Annual Holding period return -0.984%*12

-

0.277%*12 0.752%*12

Annual Holding period return -11.808% -3.320% 9.019%

Answer to 4):

Particulars CBA.AX WBC.AX AORD

Standard deviation 4.018% 3.604% 2.169%

6,057.20

12/1/2017 6,167.30 1.818%

1/1/2018 6,146.50 -0.337%

2/1/2018 6,117.30 -0.475%

3/1/2018 5,868.90 -4.061%

4/1/2018 6,071.60 3.454%

5/1/2018 6,123.50 0.855%

6/1/2018 6,289.70 2.714%

Answer to 2):

Particulars CBA.AX WBC.AX AORD

Average Holding period return -0.984% -0.277% 0.752%

Answer to 3):

Particulars CBA.AX WBC.AX AORD

Annual Holding period return -0.984%*12

-

0.277%*12 0.752%*12

Annual Holding period return -11.808% -3.320% 9.019%

Answer to 4):

Particulars CBA.AX WBC.AX AORD

Standard deviation 4.018% 3.604% 2.169%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.