Accounting and Financial Management: Long Service Leave, Employee Stock Options, and Intangible Assets

VerifiedAdded on 2023/06/04

|8

|1389

|424

AI Summary

This article covers the accounting treatment of long service leave, employee stock options, and intangible assets in Accounting and Financial Management. It includes insights into estimating expenses, journal entries, and disclosure requirements. The article cites relevant AASB standards and the conceptual framework for financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting and Financial Management

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

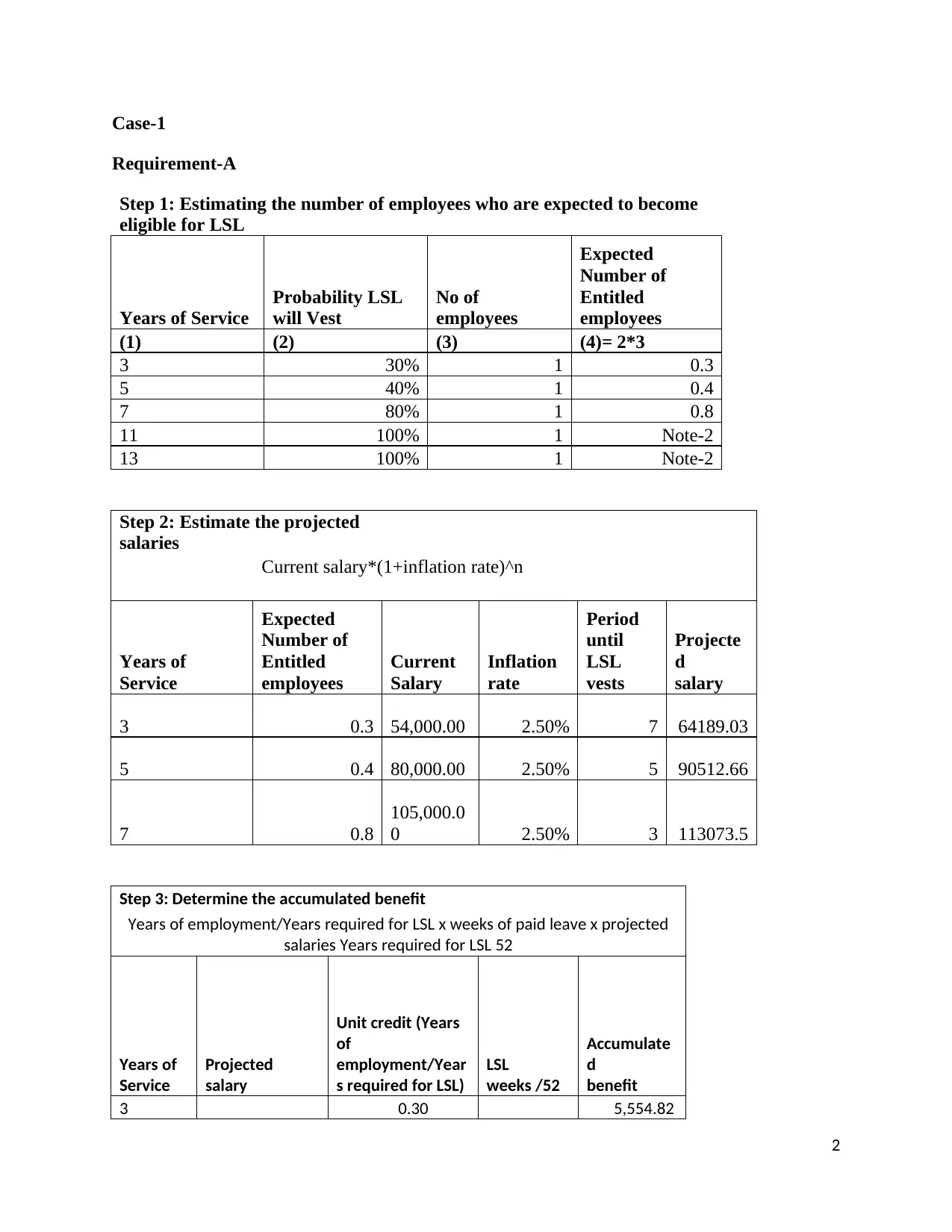

Case-1

Requirement-A

Step 1: Estimating the number of employees who are expected to become

eligible for LSL

Years of Service

Probability LSL

will Vest

No of

employees

Expected

Number of

Entitled

employees

(1) (2) (3) (4)= 2*3

3 30% 1 0.3

5 40% 1 0.4

7 80% 1 0.8

11 100% 1 Note-2

13 100% 1 Note-2

Step 2: Estimate the projected

salaries

Current salary*(1+inflation rate)^n

Years of

Service

Expected

Number of

Entitled

employees

Current

Salary

Inflation

rate

Period

until

LSL

vests

Projecte

d

salary

3 0.3 54,000.00 2.50% 7 64189.03

5 0.4 80,000.00 2.50% 5 90512.66

7 0.8

105,000.0

0 2.50% 3 113073.5

Step 3: Determine the accumulated benefit

Years of employment/Years required for LSL x weeks of paid leave x projected

salaries Years required for LSL 52

Years of

Service

Projected

salary

Unit credit (Years

of

employment/Year

s required for LSL)

LSL

weeks /52

Accumulate

d

benefit

3 0.30 5,554.82

2

Requirement-A

Step 1: Estimating the number of employees who are expected to become

eligible for LSL

Years of Service

Probability LSL

will Vest

No of

employees

Expected

Number of

Entitled

employees

(1) (2) (3) (4)= 2*3

3 30% 1 0.3

5 40% 1 0.4

7 80% 1 0.8

11 100% 1 Note-2

13 100% 1 Note-2

Step 2: Estimate the projected

salaries

Current salary*(1+inflation rate)^n

Years of

Service

Expected

Number of

Entitled

employees

Current

Salary

Inflation

rate

Period

until

LSL

vests

Projecte

d

salary

3 0.3 54,000.00 2.50% 7 64189.03

5 0.4 80,000.00 2.50% 5 90512.66

7 0.8

105,000.0

0 2.50% 3 113073.5

Step 3: Determine the accumulated benefit

Years of employment/Years required for LSL x weeks of paid leave x projected

salaries Years required for LSL 52

Years of

Service

Projected

salary

Unit credit (Years

of

employment/Year

s required for LSL)

LSL

weeks /52

Accumulate

d

benefit

3 0.30 5,554.82

2

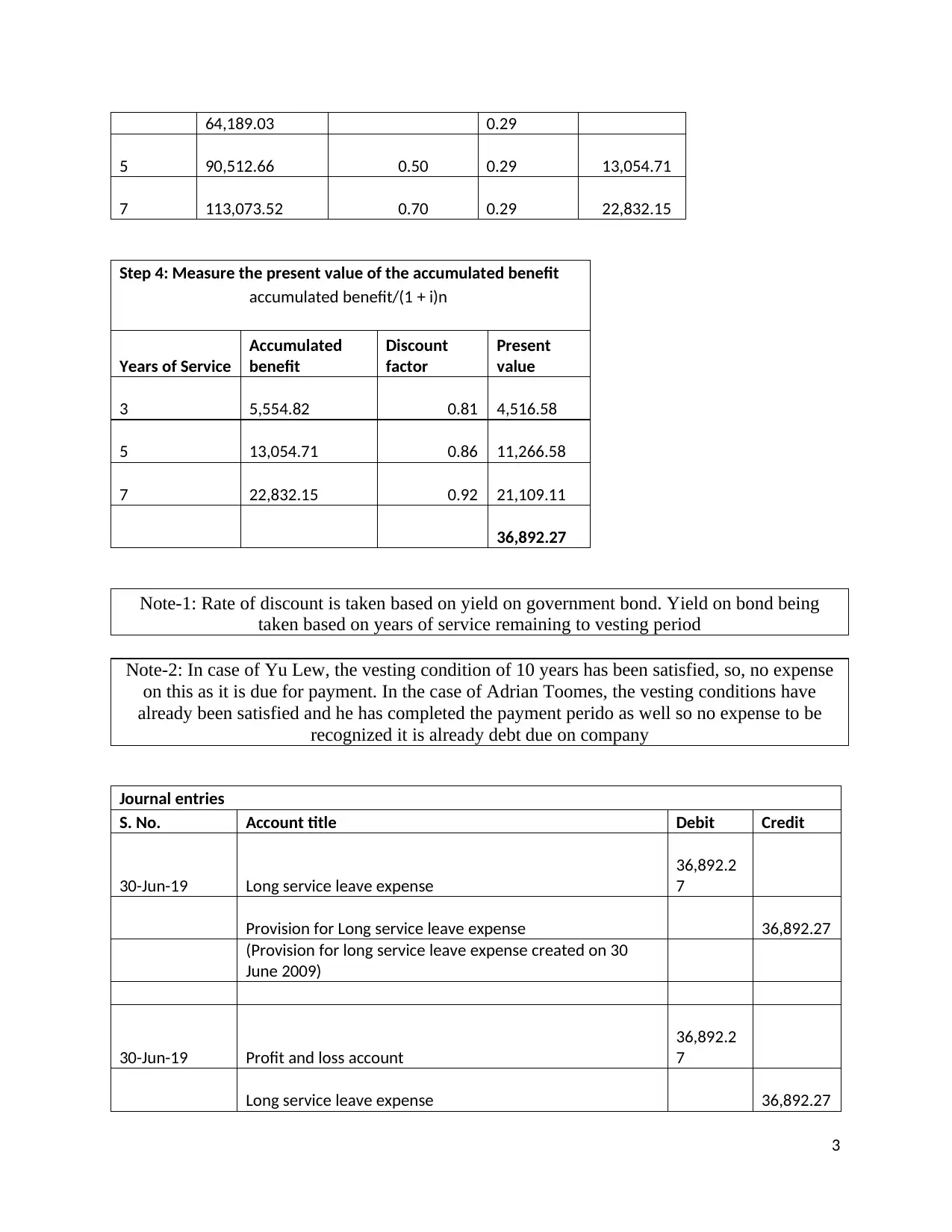

64,189.03 0.29

5 90,512.66 0.50 0.29 13,054.71

7 113,073.52 0.70 0.29 22,832.15

Step 4: Measure the present value of the accumulated benefit

accumulated benefit/(1 + i)n

Years of Service

Accumulated

benefit

Discount

factor

Present

value

3 5,554.82 0.81 4,516.58

5 13,054.71 0.86 11,266.58

7 22,832.15 0.92 21,109.11

36,892.27

Note-1: Rate of discount is taken based on yield on government bond. Yield on bond being

taken based on years of service remaining to vesting period

Note-2: In case of Yu Lew, the vesting condition of 10 years has been satisfied, so, no expense

on this as it is due for payment. In the case of Adrian Toomes, the vesting conditions have

already been satisfied and he has completed the payment perido as well so no expense to be

recognized it is already debt due on company

Journal entries

S. No. Account title Debit Credit

30-Jun-19 Long service leave expense

36,892.2

7

Provision for Long service leave expense 36,892.27

(Provision for long service leave expense created on 30

June 2009)

30-Jun-19 Profit and loss account

36,892.2

7

Long service leave expense 36,892.27

3

5 90,512.66 0.50 0.29 13,054.71

7 113,073.52 0.70 0.29 22,832.15

Step 4: Measure the present value of the accumulated benefit

accumulated benefit/(1 + i)n

Years of Service

Accumulated

benefit

Discount

factor

Present

value

3 5,554.82 0.81 4,516.58

5 13,054.71 0.86 11,266.58

7 22,832.15 0.92 21,109.11

36,892.27

Note-1: Rate of discount is taken based on yield on government bond. Yield on bond being

taken based on years of service remaining to vesting period

Note-2: In case of Yu Lew, the vesting condition of 10 years has been satisfied, so, no expense

on this as it is due for payment. In the case of Adrian Toomes, the vesting conditions have

already been satisfied and he has completed the payment perido as well so no expense to be

recognized it is already debt due on company

Journal entries

S. No. Account title Debit Credit

30-Jun-19 Long service leave expense

36,892.2

7

Provision for Long service leave expense 36,892.27

(Provision for long service leave expense created on 30

June 2009)

30-Jun-19 Profit and loss account

36,892.2

7

Long service leave expense 36,892.27

3

(Long service leave expense for 2009 charged to profit and

loss account)

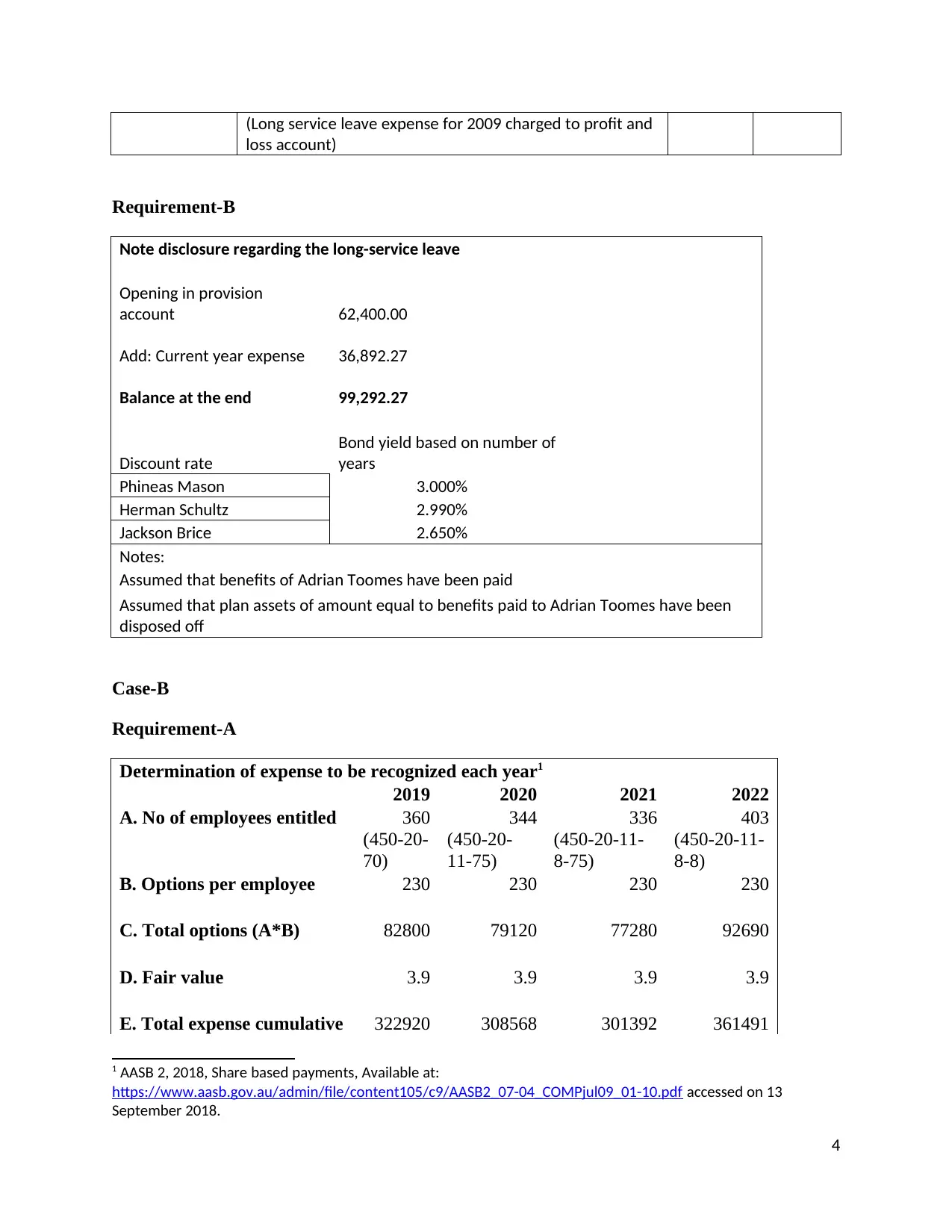

Requirement-B

Note disclosure regarding the long-service leave

Opening in provision

account 62,400.00

Add: Current year expense 36,892.27

Balance at the end 99,292.27

Discount rate

Bond yield based on number of

years

Phineas Mason 3.000%

Herman Schultz 2.990%

Jackson Brice 2.650%

Notes:

Assumed that benefits of Adrian Toomes have been paid

Assumed that plan assets of amount equal to benefits paid to Adrian Toomes have been

disposed off

Case-B

Requirement-A

Determination of expense to be recognized each year1

2019 2020 2021 2022

A. No of employees entitled 360 344 336 403

(450-20-

70)

(450-20-

11-75)

(450-20-11-

8-75)

(450-20-11-

8-8)

B. Options per employee 230 230 230 230

C. Total options (A*B) 82800 79120 77280 92690

D. Fair value 3.9 3.9 3.9 3.9

E. Total expense cumulative 322920 308568 301392 361491

1 AASB 2, 2018, Share based payments, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB2_07-04_COMPjul09_01-10.pdf accessed on 13

September 2018.

4

loss account)

Requirement-B

Note disclosure regarding the long-service leave

Opening in provision

account 62,400.00

Add: Current year expense 36,892.27

Balance at the end 99,292.27

Discount rate

Bond yield based on number of

years

Phineas Mason 3.000%

Herman Schultz 2.990%

Jackson Brice 2.650%

Notes:

Assumed that benefits of Adrian Toomes have been paid

Assumed that plan assets of amount equal to benefits paid to Adrian Toomes have been

disposed off

Case-B

Requirement-A

Determination of expense to be recognized each year1

2019 2020 2021 2022

A. No of employees entitled 360 344 336 403

(450-20-

70)

(450-20-

11-75)

(450-20-11-

8-75)

(450-20-11-

8-8)

B. Options per employee 230 230 230 230

C. Total options (A*B) 82800 79120 77280 92690

D. Fair value 3.9 3.9 3.9 3.9

E. Total expense cumulative 322920 308568 301392 361491

1 AASB 2, 2018, Share based payments, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB2_07-04_COMPjul09_01-10.pdf accessed on 13

September 2018.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(C*D)

F. Expense to be recognized 80730 150696 69966 60099

Journal entries

S. No. Account title Debit

Cred

it

30-Jun-

19 ESOP expense

8073

0

ESOP outstanding-liability

8073

0

(employee stock option expense recognized)

Profit and loss account

8073

0

ESOP expense

8073

0

(expense transferred to profit and loss account)

30-Jun-

20 ESOP expense

1506

96

ESOP outstanding-liability

1506

96

(employee stock option expense recognized)

Profit and loss account

1506

96

ESOP expense

1506

96

(expense transferred to profit and loss account)

30-Jun-

21 ESOP expense

6996

6

ESOP outstanding-liability

6996

6

(employee stock option expense recognized)

Profit and loss account

6996

6

ESOP expense

6996

6

(expense transferred to profit and loss account)

30-Jun- ESOP expense 6009

5

F. Expense to be recognized 80730 150696 69966 60099

Journal entries

S. No. Account title Debit

Cred

it

30-Jun-

19 ESOP expense

8073

0

ESOP outstanding-liability

8073

0

(employee stock option expense recognized)

Profit and loss account

8073

0

ESOP expense

8073

0

(expense transferred to profit and loss account)

30-Jun-

20 ESOP expense

1506

96

ESOP outstanding-liability

1506

96

(employee stock option expense recognized)

Profit and loss account

1506

96

ESOP expense

1506

96

(expense transferred to profit and loss account)

30-Jun-

21 ESOP expense

6996

6

ESOP outstanding-liability

6996

6

(employee stock option expense recognized)

Profit and loss account

6996

6

ESOP expense

6996

6

(expense transferred to profit and loss account)

30-Jun- ESOP expense 6009

5

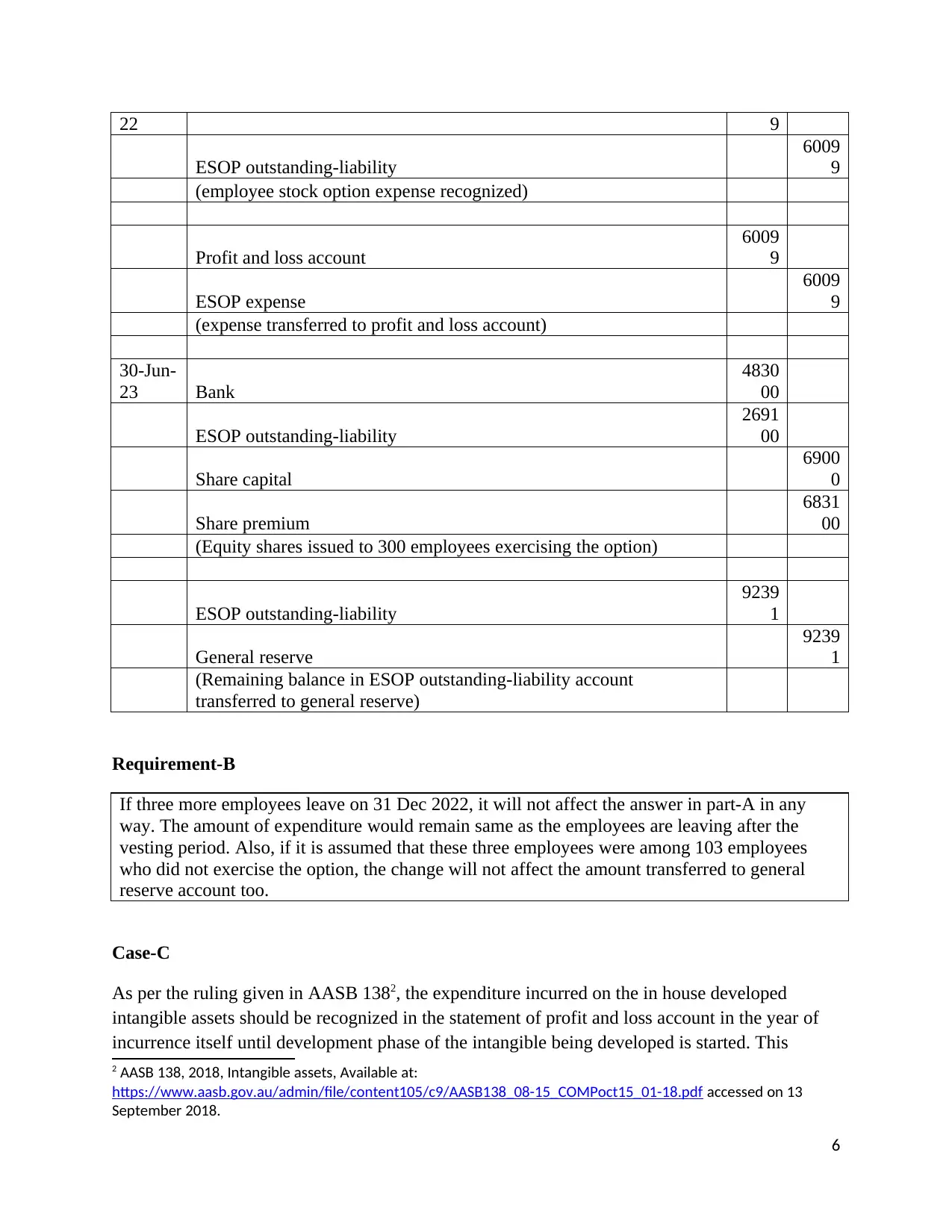

22 9

ESOP outstanding-liability

6009

9

(employee stock option expense recognized)

Profit and loss account

6009

9

ESOP expense

6009

9

(expense transferred to profit and loss account)

30-Jun-

23 Bank

4830

00

ESOP outstanding-liability

2691

00

Share capital

6900

0

Share premium

6831

00

(Equity shares issued to 300 employees exercising the option)

ESOP outstanding-liability

9239

1

General reserve

9239

1

(Remaining balance in ESOP outstanding-liability account

transferred to general reserve)

Requirement-B

If three more employees leave on 31 Dec 2022, it will not affect the answer in part-A in any

way. The amount of expenditure would remain same as the employees are leaving after the

vesting period. Also, if it is assumed that these three employees were among 103 employees

who did not exercise the option, the change will not affect the amount transferred to general

reserve account too.

Case-C

As per the ruling given in AASB 1382, the expenditure incurred on the in house developed

intangible assets should be recognized in the statement of profit and loss account in the year of

incurrence itself until development phase of the intangible being developed is started. This

2 AASB 138, 2018, Intangible assets, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf accessed on 13

September 2018.

6

ESOP outstanding-liability

6009

9

(employee stock option expense recognized)

Profit and loss account

6009

9

ESOP expense

6009

9

(expense transferred to profit and loss account)

30-Jun-

23 Bank

4830

00

ESOP outstanding-liability

2691

00

Share capital

6900

0

Share premium

6831

00

(Equity shares issued to 300 employees exercising the option)

ESOP outstanding-liability

9239

1

General reserve

9239

1

(Remaining balance in ESOP outstanding-liability account

transferred to general reserve)

Requirement-B

If three more employees leave on 31 Dec 2022, it will not affect the answer in part-A in any

way. The amount of expenditure would remain same as the employees are leaving after the

vesting period. Also, if it is assumed that these three employees were among 103 employees

who did not exercise the option, the change will not affect the amount transferred to general

reserve account too.

Case-C

As per the ruling given in AASB 1382, the expenditure incurred on the in house developed

intangible assets should be recognized in the statement of profit and loss account in the year of

incurrence itself until development phase of the intangible being developed is started. This

2 AASB 138, 2018, Intangible assets, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf accessed on 13

September 2018.

6

means that the expenditure after starting the development phase activities of the intangible being

developed can be capitalized. However, this is also subject to certain conditions.

Based on the above ruling, the accounting treatment of the expenditure incurred on development

of a motion- sensing system by StarK Ltd is given below:

Expenses to be charged to profit and loss account (Research phase)

All expenses incurred during the research phase would be charged to the statement of profit and

loss account. The project started on 01 August 2017. The research phase of this project continued

till May 2018 until company developed a prototype of the motion-sensing system. The

expenditure incurred till May 2018 would be charged to profit and loss of the current year i.e.

2017-18. Thus, salary paid in September 2017 of 319000, cost of basic model production of

215000 incurred in November 2017, a $103000 incurred in January 2018 and another $93000

incurred in January 2018 would be charged to the profit and loss account. Further, a sum of

$230000 incurred in April 2018 for incorporating new design would also be charged to the profit

and loss account. So, a total of $960,000 would be charged to profit and loss account in 2017-18.

Expenses to be capitalized (Development phase)

The expenses incurred in the development phase can be capitalized to meeting the asset

recognition criteria as set out in the framework. The framework states that an item can be

recognized as asset in books if future economic benefits are expected to flow from its use in

future years3. In May 2018, Stark Ltd had developed a prototype of the system which shows that

the system would be successfully available to the company for future economic benefits. Thus,

expenses of $112,000, $38,000, and $40,000 resulting in total of 190,000 to be capitalized as

intangible assets and these expenses would be amortized on yearly basis.

3 Conceptual framework, 2018, Conceptual Framework for Financial Reporting, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf accessed on 13 September 2018.

7

developed can be capitalized. However, this is also subject to certain conditions.

Based on the above ruling, the accounting treatment of the expenditure incurred on development

of a motion- sensing system by StarK Ltd is given below:

Expenses to be charged to profit and loss account (Research phase)

All expenses incurred during the research phase would be charged to the statement of profit and

loss account. The project started on 01 August 2017. The research phase of this project continued

till May 2018 until company developed a prototype of the motion-sensing system. The

expenditure incurred till May 2018 would be charged to profit and loss of the current year i.e.

2017-18. Thus, salary paid in September 2017 of 319000, cost of basic model production of

215000 incurred in November 2017, a $103000 incurred in January 2018 and another $93000

incurred in January 2018 would be charged to the profit and loss account. Further, a sum of

$230000 incurred in April 2018 for incorporating new design would also be charged to the profit

and loss account. So, a total of $960,000 would be charged to profit and loss account in 2017-18.

Expenses to be capitalized (Development phase)

The expenses incurred in the development phase can be capitalized to meeting the asset

recognition criteria as set out in the framework. The framework states that an item can be

recognized as asset in books if future economic benefits are expected to flow from its use in

future years3. In May 2018, Stark Ltd had developed a prototype of the system which shows that

the system would be successfully available to the company for future economic benefits. Thus,

expenses of $112,000, $38,000, and $40,000 resulting in total of 190,000 to be capitalized as

intangible assets and these expenses would be amortized on yearly basis.

3 Conceptual framework, 2018, Conceptual Framework for Financial Reporting, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf accessed on 13 September 2018.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

AASB 119, 2018, Employee benefits, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11_COMPjun14_07-14.pdf

accessed on 13 September 2018.

AASB 138, 2018, Intangible assets, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

accessed on 13 September 2018.

AASB 2, 2018, Share based payments, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB2_07-04_COMPjul09_01-10.pdf

accessed on 13 September 2018.

Conceptual framework, 2018, Conceptual Framework for Financial Reporting, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf accessed on 13

September 2018.

8

AASB 119, 2018, Employee benefits, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11_COMPjun14_07-14.pdf

accessed on 13 September 2018.

AASB 138, 2018, Intangible assets, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

accessed on 13 September 2018.

AASB 2, 2018, Share based payments, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB2_07-04_COMPjul09_01-10.pdf

accessed on 13 September 2018.

Conceptual framework, 2018, Conceptual Framework for Financial Reporting, Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf accessed on 13

September 2018.

8

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.