Analyzing Financial Performance of Caltex Australia Ltd.

VerifiedAdded on 2020/05/28

|29

|2996

|73

AI Summary

This assignment requires students to perform an in-depth financial analysis comparing the performance of Caltex Australia Ltd. and Origin Energy Limited over a three-year period (2014-2016). The task involves analyzing key financial documents such as income statements, balance sheets, and cash flow statements. Students must also compute and compare various liquidity ratios including current ratio, quick ratio, and cash ratio for both companies. Additionally, the assignment demands the creation of horizontal analysis tables to identify significant trends or changes in financial metrics over the specified period. This comparative study aims to highlight differences in financial performance, operational efficiency, and strategic positioning between Caltex Australia Ltd. and Origin Energy Limited.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR BUSINESS

Executive Summary:

The current report aims to evaluate the financial statements of Caltex Australia Limited

with the help of horizontal and ratio analyses for three years ranging from 2014 to 2016. In order

to enhance the quality of analysis, Origin Energy Limited is chosen as the competitor to gain an

insight of the competitive position of Caltex Australia Limited in the Australian energy sector. It

could be stated that in terms of profitability, liquidity and rate of return, Caltex is enjoying

competitive advantage over Origin Energy in the Australian energy sector. In addition, based on

the Australian regulations, the company develops its ethical standards by conforming to a greater

degree of business risks. Thus, the investors are recommended to invest in the shares of Caltex

for maximising their overall return on investment.

Executive Summary:

The current report aims to evaluate the financial statements of Caltex Australia Limited

with the help of horizontal and ratio analyses for three years ranging from 2014 to 2016. In order

to enhance the quality of analysis, Origin Energy Limited is chosen as the competitor to gain an

insight of the competitive position of Caltex Australia Limited in the Australian energy sector. It

could be stated that in terms of profitability, liquidity and rate of return, Caltex is enjoying

competitive advantage over Origin Energy in the Australian energy sector. In addition, based on

the Australian regulations, the company develops its ethical standards by conforming to a greater

degree of business risks. Thus, the investors are recommended to invest in the shares of Caltex

for maximising their overall return on investment.

2ACCOUNTING FOR BUSINESS

Table of Contents

1. Introduction:................................................................................................................................3

2. Annual report analysis:................................................................................................................3

a. Profit and loss analysis:...........................................................................................................3

b. Balance sheet analysis:............................................................................................................5

c. Cash flow statement analysis:..................................................................................................6

3. Ratio analysis:..............................................................................................................................7

a. Profitability analysis:...............................................................................................................7

b. Efficiency analysis:..................................................................................................................9

c. Liquidity analysis:..................................................................................................................10

d. Rate of return:........................................................................................................................12

4. Corporate governance and ethical standard:..............................................................................14

a. Code of conduct:....................................................................................................................14

b. Approach of the manager to the risks:...................................................................................14

5. Conclusion:................................................................................................................................14

References and Bibliographies:.....................................................................................................16

Appendices:...................................................................................................................................18

Table of Contents

1. Introduction:................................................................................................................................3

2. Annual report analysis:................................................................................................................3

a. Profit and loss analysis:...........................................................................................................3

b. Balance sheet analysis:............................................................................................................5

c. Cash flow statement analysis:..................................................................................................6

3. Ratio analysis:..............................................................................................................................7

a. Profitability analysis:...............................................................................................................7

b. Efficiency analysis:..................................................................................................................9

c. Liquidity analysis:..................................................................................................................10

d. Rate of return:........................................................................................................................12

4. Corporate governance and ethical standard:..............................................................................14

a. Code of conduct:....................................................................................................................14

b. Approach of the manager to the risks:...................................................................................14

5. Conclusion:................................................................................................................................14

References and Bibliographies:.....................................................................................................16

Appendices:...................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR BUSINESS

1. Introduction:

The current report aims to evaluate the financial statements of Caltex Australia Limited

with the help of horizontal and ratio analyses for three years ranging from 2014 to 2016. In order

to enhance the quality of analysis, Origin Energy Limited is chosen as the competitor to gain an

insight of the competitive position of Caltex Australia Limited in the Australian energy sector.

The organisation is established in 1990 and it is headquartered at Sydney, Australia. The

organisation is involved in buying, refining, distributing and marketing of the petroleum goods in

Australia and Singapore. The main products of Caltex Australia Limited constitute of petrol,

diesel, auto gas, motor oil and lubricants along with convenience stores (Caltex 2018). Until

March 2015, Chevron was the owner of 50% shares of the organisation and the Australian

shareholders own the remaining 50%. However, after that period, Chevron sold its shares of the

organisation to the Australian shareholders.

2. Annual report analysis:

a. Profit and loss analysis:

In order to analyse the profit and loss position of Caltex Australia Limited, the horizontal

analysis of its income statements has been conducted and it is compared with that of Energy

Origin Limited (Refer to Appendices, Appendix 7 and Appendix 8).

1. Introduction:

The current report aims to evaluate the financial statements of Caltex Australia Limited

with the help of horizontal and ratio analyses for three years ranging from 2014 to 2016. In order

to enhance the quality of analysis, Origin Energy Limited is chosen as the competitor to gain an

insight of the competitive position of Caltex Australia Limited in the Australian energy sector.

The organisation is established in 1990 and it is headquartered at Sydney, Australia. The

organisation is involved in buying, refining, distributing and marketing of the petroleum goods in

Australia and Singapore. The main products of Caltex Australia Limited constitute of petrol,

diesel, auto gas, motor oil and lubricants along with convenience stores (Caltex 2018). Until

March 2015, Chevron was the owner of 50% shares of the organisation and the Australian

shareholders own the remaining 50%. However, after that period, Chevron sold its shares of the

organisation to the Australian shareholders.

2. Annual report analysis:

a. Profit and loss analysis:

In order to analyse the profit and loss position of Caltex Australia Limited, the horizontal

analysis of its income statements has been conducted and it is compared with that of Energy

Origin Limited (Refer to Appendices, Appendix 7 and Appendix 8).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR BUSINESS

% change

in 2015 % change

in 2016 % change

in 2015 % change

in 2016

Caltex Australia

Limited Origin Energy

Limited

-2000.00%

-1500.00%

-1000.00%

-500.00%

0.00%

500.00%

1000.00%

1500.00%

2000.00%

2500.00%

3000.00%

Percent change in gross profit,

operating expenses and net income

Gross profit

Total operating expenses

Net income

Figure 1: Percent change in gross profit, operating expenses and net income

(Source: Caltex 2018; Originenergy.com.au 2018)

According to the above figure, it could be stated that although gross margin of the

organisation increased by 43.95% in 2015; however, the decline is considerable in 2016 by -

962.27%. This is because the cost of goods sold of the organisation has increased considerably,

while it has failed to conduct adequate sales due to falling demand in the market (Alammar and

Kohn 2016). The trend is similar in case of Origin Energy Limited; however, it has positive gross

income over the years. On the other hand, the operating expenses of Origin Energy have

increased, while Caltex has experienced operating income in the form of other operating income.

Finally, the net income of Caltex has increased considerably over the three-year period, while the

situation is just reverse in case of Origin Energy due to greater operating costs. Hence, in terms

of profitability, Caltex is enjoying competitive advantage over Origin Energy in the Australian

energy sector.

% change

in 2015 % change

in 2016 % change

in 2015 % change

in 2016

Caltex Australia

Limited Origin Energy

Limited

-2000.00%

-1500.00%

-1000.00%

-500.00%

0.00%

500.00%

1000.00%

1500.00%

2000.00%

2500.00%

3000.00%

Percent change in gross profit,

operating expenses and net income

Gross profit

Total operating expenses

Net income

Figure 1: Percent change in gross profit, operating expenses and net income

(Source: Caltex 2018; Originenergy.com.au 2018)

According to the above figure, it could be stated that although gross margin of the

organisation increased by 43.95% in 2015; however, the decline is considerable in 2016 by -

962.27%. This is because the cost of goods sold of the organisation has increased considerably,

while it has failed to conduct adequate sales due to falling demand in the market (Alammar and

Kohn 2016). The trend is similar in case of Origin Energy Limited; however, it has positive gross

income over the years. On the other hand, the operating expenses of Origin Energy have

increased, while Caltex has experienced operating income in the form of other operating income.

Finally, the net income of Caltex has increased considerably over the three-year period, while the

situation is just reverse in case of Origin Energy due to greater operating costs. Hence, in terms

of profitability, Caltex is enjoying competitive advantage over Origin Energy in the Australian

energy sector.

5ACCOUNTING FOR BUSINESS

b. Balance sheet analysis:

In order to analyse the financial position of Caltex Australia Limited, the horizontal

analysis of its balance sheet statements has been conducted and it is compared with that of

Energy Origin Limited (Refer to Appendices, Appendix 9 and Appendix 10).

% change

in 2015 % change

in 2016 % change

in 2015 % change

in 2016

Caltex Australia

Limited Origin Energy Limited

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

Percent change in total assets, total

liabilities and total equity

Total assets

Total liabilities

Total Stockholders' equity

Figure 2: Percent change in total assets, total liabilities and total equity

(Source: Caltex 2018; Originenergy.com.au 2018)

In accordance with the above figure, it could be stated that the total asset base of Caltex

has fallen by 0.47% in 2016; however, it has increased by 3.88% in 2016. On the other hand, the

situation is just reverse for Origin Energy, in which the total assets have increased by 7.16% in

2015; however, it has fallen to 13.39% in 2016. In case of total liabilities and total equity, the

trend is just the opposite, as the investors are interested to invest in the shares of Origin Energy

due to higher returns on investment. Hence, in terms of financial position, Origin Energy is

slightly in a better position in the Australian energy sector in contrast to Caltex Australia

Limited.

b. Balance sheet analysis:

In order to analyse the financial position of Caltex Australia Limited, the horizontal

analysis of its balance sheet statements has been conducted and it is compared with that of

Energy Origin Limited (Refer to Appendices, Appendix 9 and Appendix 10).

% change

in 2015 % change

in 2016 % change

in 2015 % change

in 2016

Caltex Australia

Limited Origin Energy Limited

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

Percent change in total assets, total

liabilities and total equity

Total assets

Total liabilities

Total Stockholders' equity

Figure 2: Percent change in total assets, total liabilities and total equity

(Source: Caltex 2018; Originenergy.com.au 2018)

In accordance with the above figure, it could be stated that the total asset base of Caltex

has fallen by 0.47% in 2016; however, it has increased by 3.88% in 2016. On the other hand, the

situation is just reverse for Origin Energy, in which the total assets have increased by 7.16% in

2015; however, it has fallen to 13.39% in 2016. In case of total liabilities and total equity, the

trend is just the opposite, as the investors are interested to invest in the shares of Origin Energy

due to higher returns on investment. Hence, in terms of financial position, Origin Energy is

slightly in a better position in the Australian energy sector in contrast to Caltex Australia

Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR BUSINESS

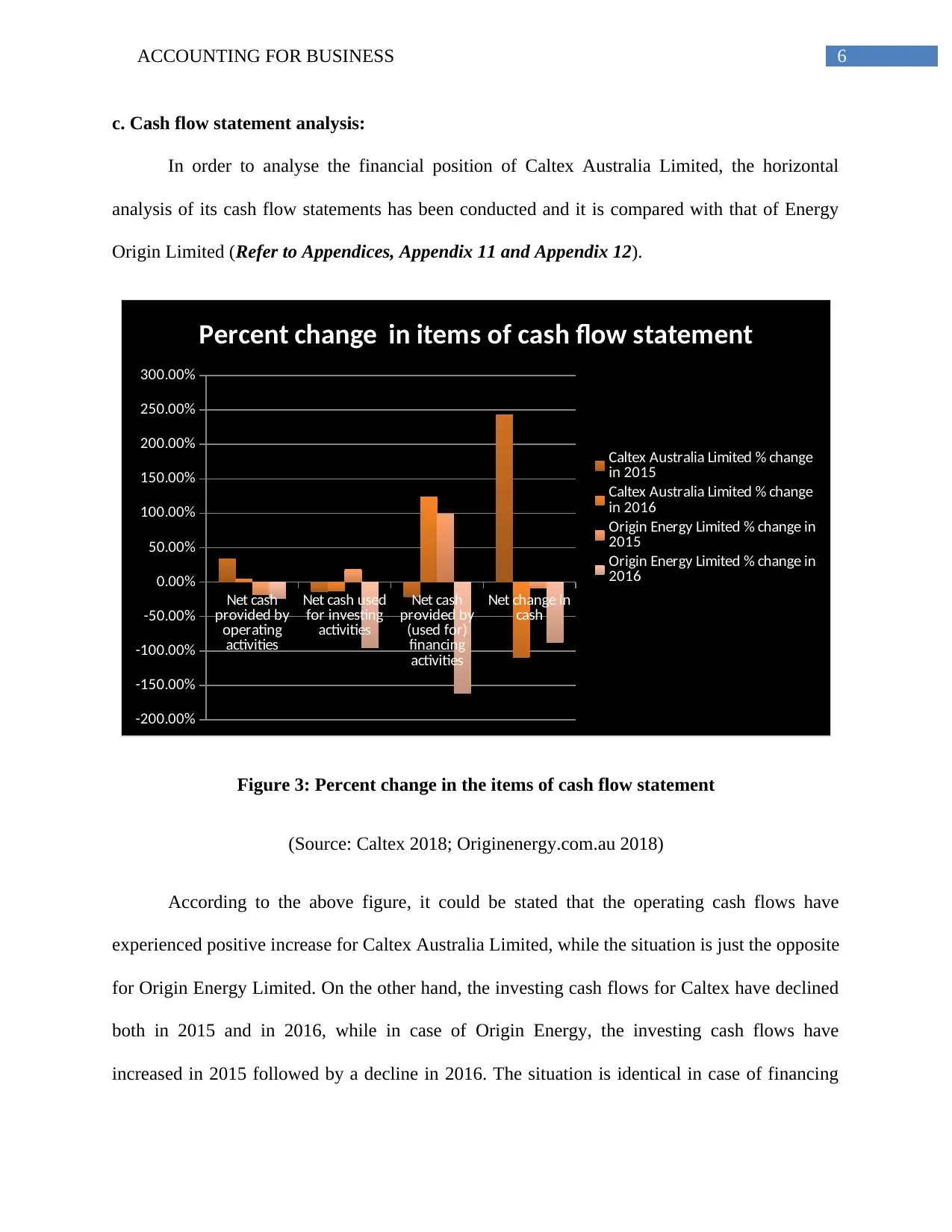

c. Cash flow statement analysis:

In order to analyse the financial position of Caltex Australia Limited, the horizontal

analysis of its cash flow statements has been conducted and it is compared with that of Energy

Origin Limited (Refer to Appendices, Appendix 11 and Appendix 12).

Net cash

provided by

operating

activities

Net cash used

for investing

activities

Net cash

provided by

(used for)

financing

activities

Net change in

cash

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Percent change in items of cash flow statement

Caltex Australia Limited % change

in 2015

Caltex Australia Limited % change

in 2016

Origin Energy Limited % change in

2015

Origin Energy Limited % change in

2016

Figure 3: Percent change in the items of cash flow statement

(Source: Caltex 2018; Originenergy.com.au 2018)

According to the above figure, it could be stated that the operating cash flows have

experienced positive increase for Caltex Australia Limited, while the situation is just the opposite

for Origin Energy Limited. On the other hand, the investing cash flows for Caltex have declined

both in 2015 and in 2016, while in case of Origin Energy, the investing cash flows have

increased in 2015 followed by a decline in 2016. The situation is identical in case of financing

c. Cash flow statement analysis:

In order to analyse the financial position of Caltex Australia Limited, the horizontal

analysis of its cash flow statements has been conducted and it is compared with that of Energy

Origin Limited (Refer to Appendices, Appendix 11 and Appendix 12).

Net cash

provided by

operating

activities

Net cash used

for investing

activities

Net cash

provided by

(used for)

financing

activities

Net change in

cash

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Percent change in items of cash flow statement

Caltex Australia Limited % change

in 2015

Caltex Australia Limited % change

in 2016

Origin Energy Limited % change in

2015

Origin Energy Limited % change in

2016

Figure 3: Percent change in the items of cash flow statement

(Source: Caltex 2018; Originenergy.com.au 2018)

According to the above figure, it could be stated that the operating cash flows have

experienced positive increase for Caltex Australia Limited, while the situation is just the opposite

for Origin Energy Limited. On the other hand, the investing cash flows for Caltex have declined

both in 2015 and in 2016, while in case of Origin Energy, the investing cash flows have

increased in 2015 followed by a decline in 2016. The situation is identical in case of financing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR BUSINESS

cash flows; however, the net cash at the end of the year 2016 has declined for both the

organisations. In this case, Caltex is in a better position, which denotes that Caltex is in a better

position in contrast to Origin Energy.

3. Ratio analysis:

a. Profitability analysis:

Particulars Details

Caltex Australia Limited Origin Energy Limited

2014 2015 2016 2014 2015 2016

Net profit A

2

0

52

2

61

0

53

0

(65

8)

(58

9)

Opening total

assets B

6,02

1

5,12

9

5,10

5

29,58

6

31,13

9

33,36

7

Closing total

assets C

5,12

9

5,10

5

5,30

3

31,13

9

33,36

7

28,89

8

Average total

assets

D=(B+C)/

2

5,57

5

5,11

7

5,20

4

30,36

3

32,25

3

31,13

3

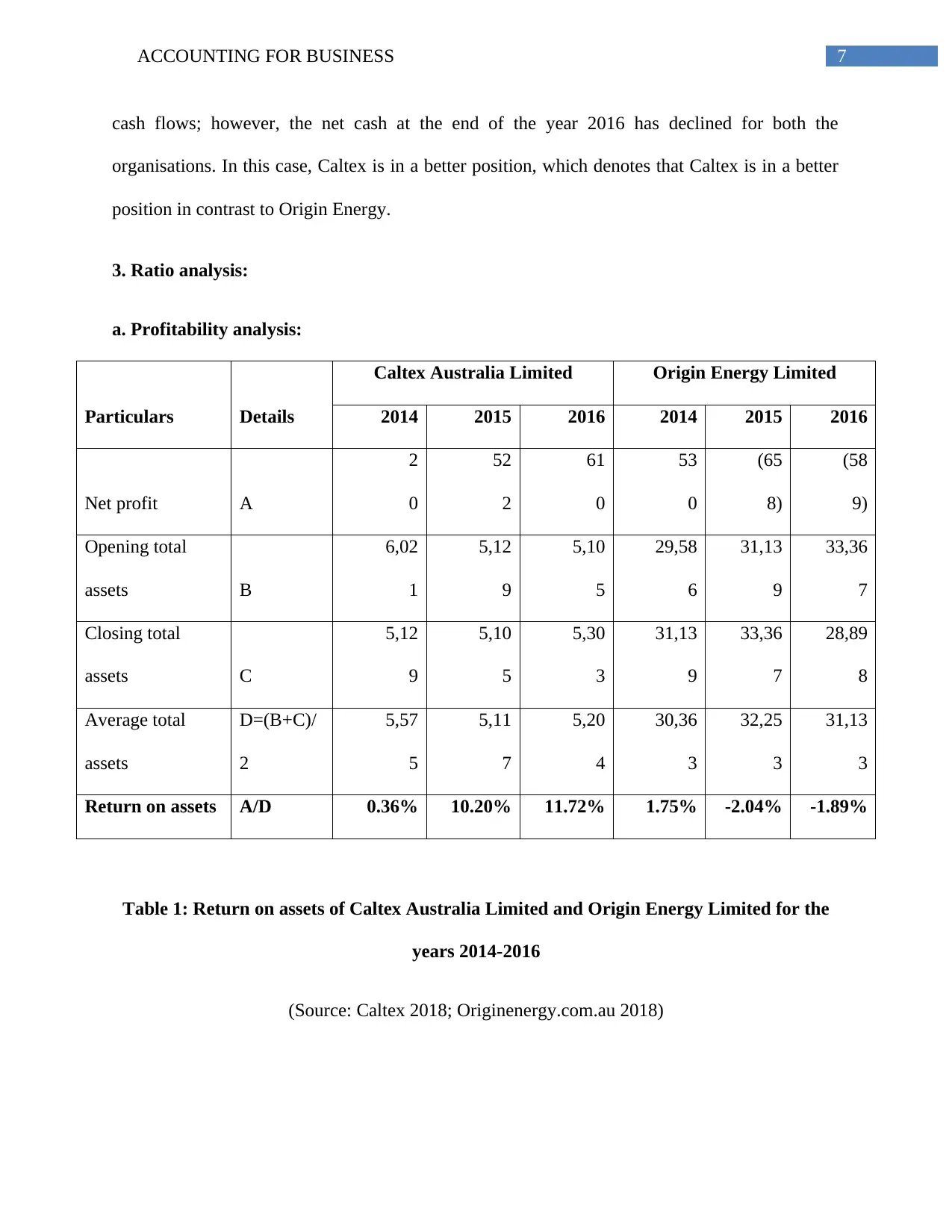

Return on assets A/D 0.36% 10.20% 11.72% 1.75% -2.04% -1.89%

Table 1: Return on assets of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

cash flows; however, the net cash at the end of the year 2016 has declined for both the

organisations. In this case, Caltex is in a better position, which denotes that Caltex is in a better

position in contrast to Origin Energy.

3. Ratio analysis:

a. Profitability analysis:

Particulars Details

Caltex Australia Limited Origin Energy Limited

2014 2015 2016 2014 2015 2016

Net profit A

2

0

52

2

61

0

53

0

(65

8)

(58

9)

Opening total

assets B

6,02

1

5,12

9

5,10

5

29,58

6

31,13

9

33,36

7

Closing total

assets C

5,12

9

5,10

5

5,30

3

31,13

9

33,36

7

28,89

8

Average total

assets

D=(B+C)/

2

5,57

5

5,11

7

5,20

4

30,36

3

32,25

3

31,13

3

Return on assets A/D 0.36% 10.20% 11.72% 1.75% -2.04% -1.89%

Table 1: Return on assets of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

8ACCOUNTING FOR BUSINESS

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

0.36%

10.20% 11.72%

1.75% -2.04% -1.89%

Return on assets

Figure 4: Return on assets of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

The above figure clearly denotes that the return on assets for Caltex Australia Limited has

increased from 0.36% in 2014 to 10.20% in 2015 and it has increased further to 11.72% in 2016.

On the other hand, the ratio for Origin Energy Limited has declined from 1.75% in 2014 to -

2.04% in 2015; however, it has slightly increased to -1.89% in 2016. As commented by

Alstadsæter et al. (2016), the return on assets denotes the overall return that an organisation

earns by deploying its asset base. In this case, the ratio is greater for Caltex Australia Limited,

which signifies that it has deployed its assets for leasing resulting in greater returns. Thus, it

could be stated that Caltex is enjoying competitive supremacy over Origin Energy in the energy

sector of Australia in terms of profitability.

b. Efficiency analysis:

Particulars Details Caltex Australia Limited Origin Energy Limited

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

0.36%

10.20% 11.72%

1.75% -2.04% -1.89%

Return on assets

Figure 4: Return on assets of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

The above figure clearly denotes that the return on assets for Caltex Australia Limited has

increased from 0.36% in 2014 to 10.20% in 2015 and it has increased further to 11.72% in 2016.

On the other hand, the ratio for Origin Energy Limited has declined from 1.75% in 2014 to -

2.04% in 2015; however, it has slightly increased to -1.89% in 2016. As commented by

Alstadsæter et al. (2016), the return on assets denotes the overall return that an organisation

earns by deploying its asset base. In this case, the ratio is greater for Caltex Australia Limited,

which signifies that it has deployed its assets for leasing resulting in greater returns. Thus, it

could be stated that Caltex is enjoying competitive supremacy over Origin Energy in the energy

sector of Australia in terms of profitability.

b. Efficiency analysis:

Particulars Details Caltex Australia Limited Origin Energy Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR BUSINESS

2014 2015 2016 2014 2015 2016

Cost of goods

sold A

22,73

0

18,03

8

31,88

0

10,81

1

8,40

6

8,96

4

Opening

inventory B

2,02

8

1,11

8

97

0

23

1

28

7

23

9

Closing

inventory C

1,11

8

97

0

1,08

1

28

7

23

9

24

8

Average

inventory

D=(B+C)/

2

1,57

3

1,04

4

1,02

6

25

9

26

3

243.5

0

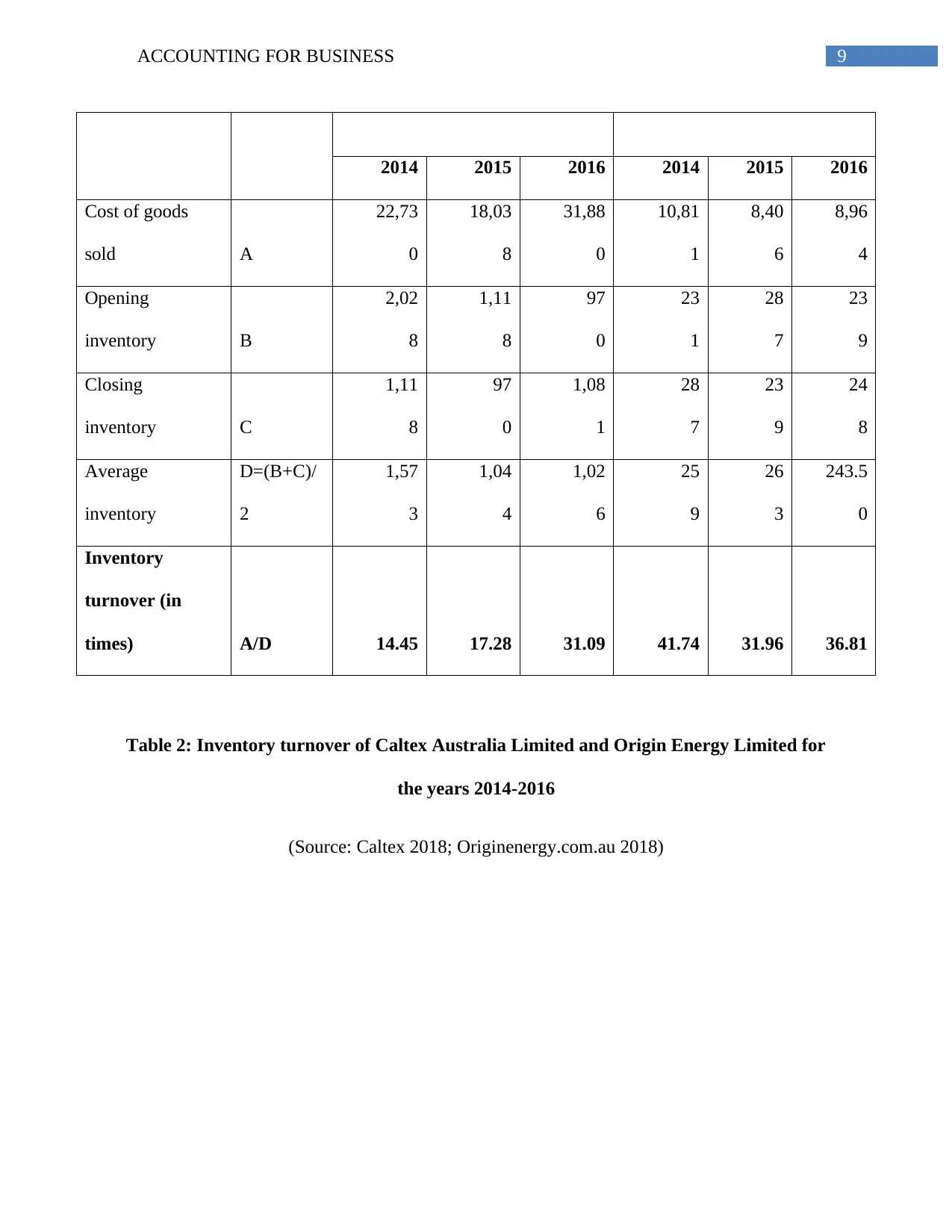

Inventory

turnover (in

times) A/D 14.45 17.28 31.09 41.74 31.96 36.81

Table 2: Inventory turnover of Caltex Australia Limited and Origin Energy Limited for

the years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

2014 2015 2016 2014 2015 2016

Cost of goods

sold A

22,73

0

18,03

8

31,88

0

10,81

1

8,40

6

8,96

4

Opening

inventory B

2,02

8

1,11

8

97

0

23

1

28

7

23

9

Closing

inventory C

1,11

8

97

0

1,08

1

28

7

23

9

24

8

Average

inventory

D=(B+C)/

2

1,57

3

1,04

4

1,02

6

25

9

26

3

243.5

0

Inventory

turnover (in

times) A/D 14.45 17.28 31.09 41.74 31.96 36.81

Table 2: Inventory turnover of Caltex Australia Limited and Origin Energy Limited for

the years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR BUSINESS

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

14.45 17.28

31.09

41.74

31.96 36.81

Inventory turnover (in times)

Figure 5: Inventory turnover of Caltex Australia Limited and Origin Energy Limited for

the years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

In accordance with the above table, the inventory turnover of Caltex has increased from

14.45 times in 2014 to 17.28 times in 2015 and the trend is inherent further to 31.09 times in

2016. On the other hand, the inventory turnover for Origin Energy has fallen from 41.74 times

in 2014 to 31.96 in 2015; however, it has increased to 36.81 times in 2016. In the words of

Bodie, Kane and Marcus (2014), inventory turnover denotes the number of times a product is

manufactured and sold in the market. In this case, although there is decline in the ratio for Origin

Energy, it is still higher compared to Caltex. Thus, in terms of efficiency position, Origin Energy

is enjoying competitive supremacy over Caltex in the market.

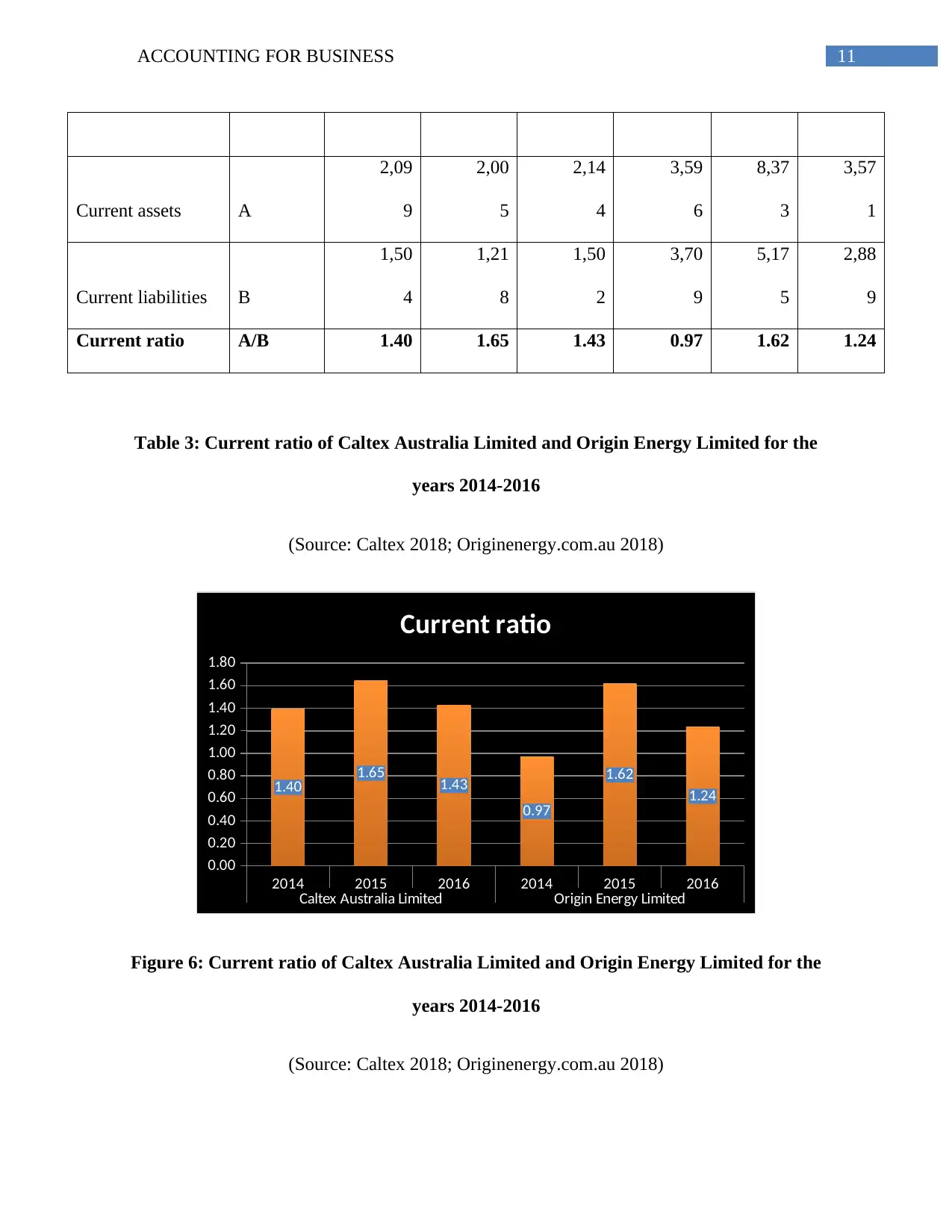

c. Liquidity analysis:

Particulars Details

Caltex Australia Limited Origin Energy Limited

2014 2015 2016 2014 2015 2016

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

14.45 17.28

31.09

41.74

31.96 36.81

Inventory turnover (in times)

Figure 5: Inventory turnover of Caltex Australia Limited and Origin Energy Limited for

the years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

In accordance with the above table, the inventory turnover of Caltex has increased from

14.45 times in 2014 to 17.28 times in 2015 and the trend is inherent further to 31.09 times in

2016. On the other hand, the inventory turnover for Origin Energy has fallen from 41.74 times

in 2014 to 31.96 in 2015; however, it has increased to 36.81 times in 2016. In the words of

Bodie, Kane and Marcus (2014), inventory turnover denotes the number of times a product is

manufactured and sold in the market. In this case, although there is decline in the ratio for Origin

Energy, it is still higher compared to Caltex. Thus, in terms of efficiency position, Origin Energy

is enjoying competitive supremacy over Caltex in the market.

c. Liquidity analysis:

Particulars Details

Caltex Australia Limited Origin Energy Limited

2014 2015 2016 2014 2015 2016

11ACCOUNTING FOR BUSINESS

Current assets A

2,09

9

2,00

5

2,14

4

3,59

6

8,37

3

3,57

1

Current liabilities B

1,50

4

1,21

8

1,50

2

3,70

9

5,17

5

2,88

9

Current ratio A/B 1.40 1.65 1.43 0.97 1.62 1.24

Table 3: Current ratio of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.40 1.65 1.43

0.97

1.62

1.24

Current ratio

Figure 6: Current ratio of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

Current assets A

2,09

9

2,00

5

2,14

4

3,59

6

8,37

3

3,57

1

Current liabilities B

1,50

4

1,21

8

1,50

2

3,70

9

5,17

5

2,88

9

Current ratio A/B 1.40 1.65 1.43 0.97 1.62 1.24

Table 3: Current ratio of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

2014 2015 2016 2014 2015 2016

Caltex Australia Limited Origin Energy Limited

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.40 1.65 1.43

0.97

1.62

1.24

Current ratio

Figure 6: Current ratio of Caltex Australia Limited and Origin Energy Limited for the

years 2014-2016

(Source: Caltex 2018; Originenergy.com.au 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.