Accounting for Business: Financial Analysis and Investment Decisions

VerifiedAdded on 2023/06/17

|12

|1463

|280

Report

AI Summary

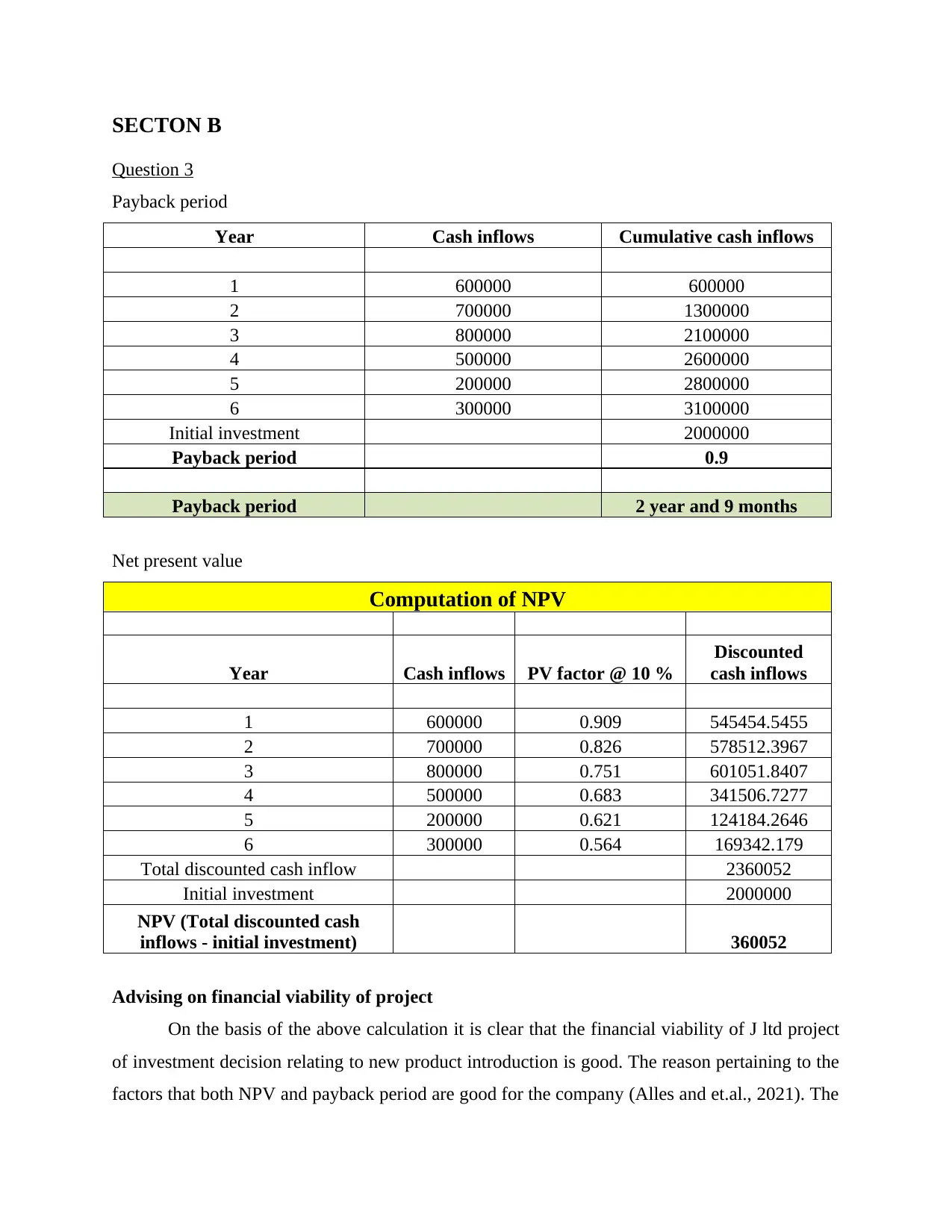

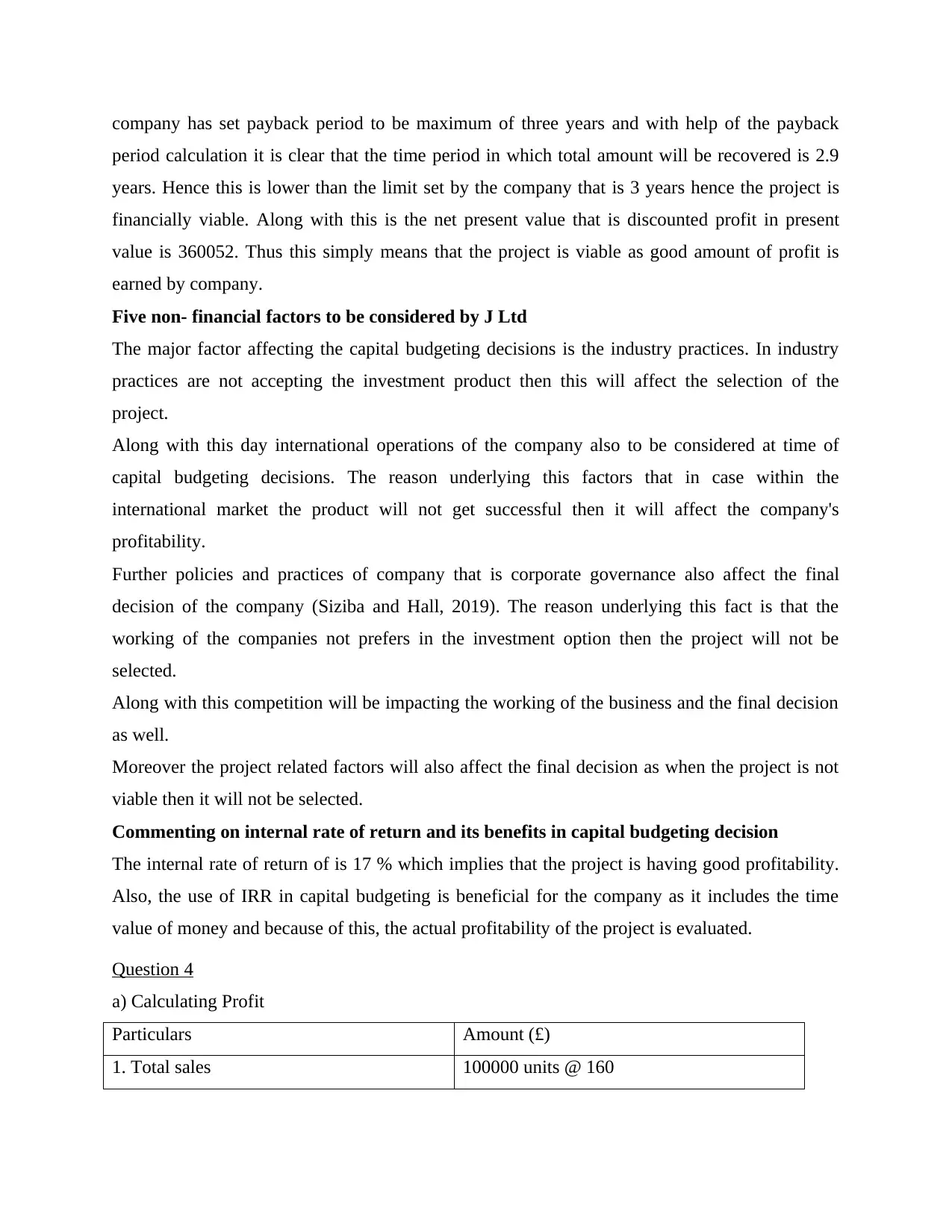

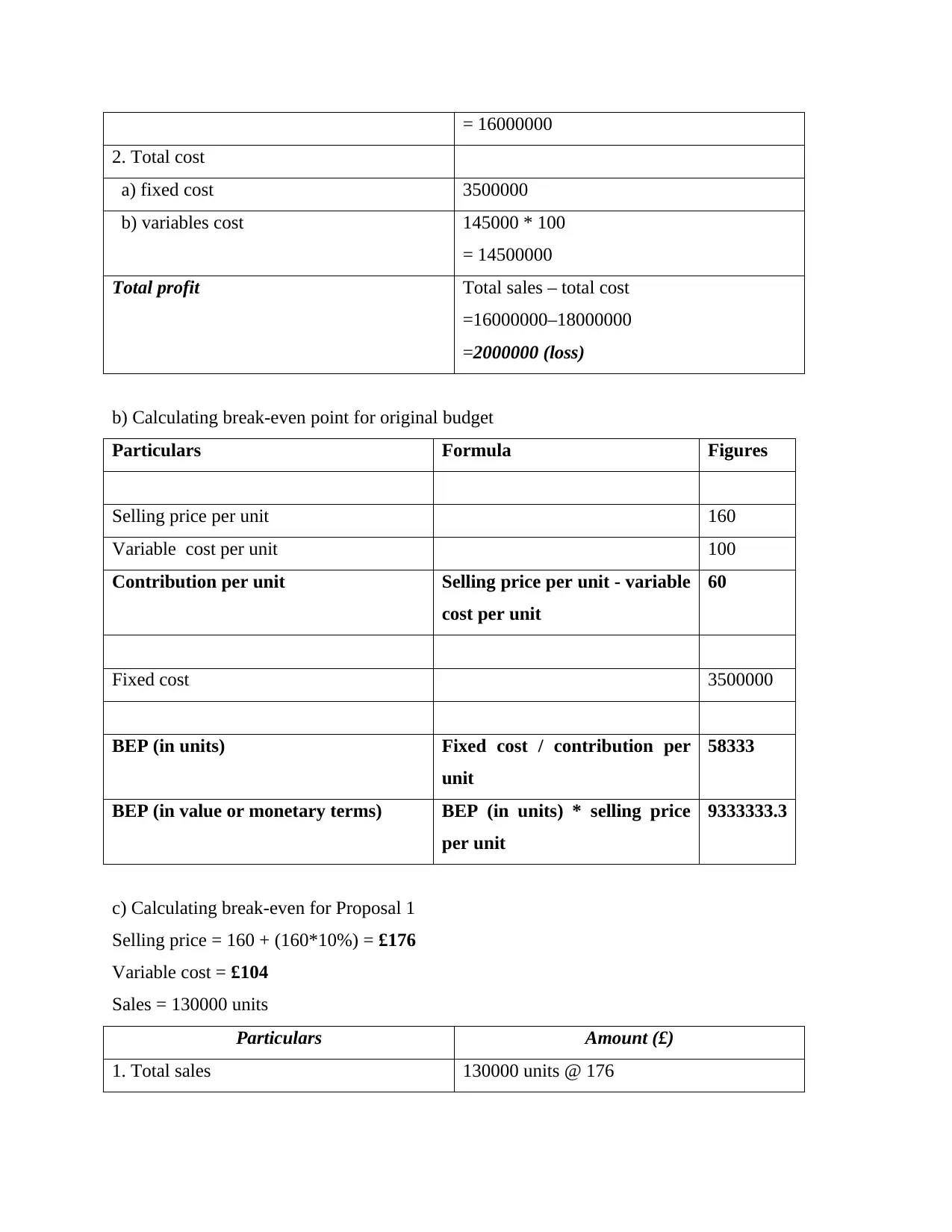

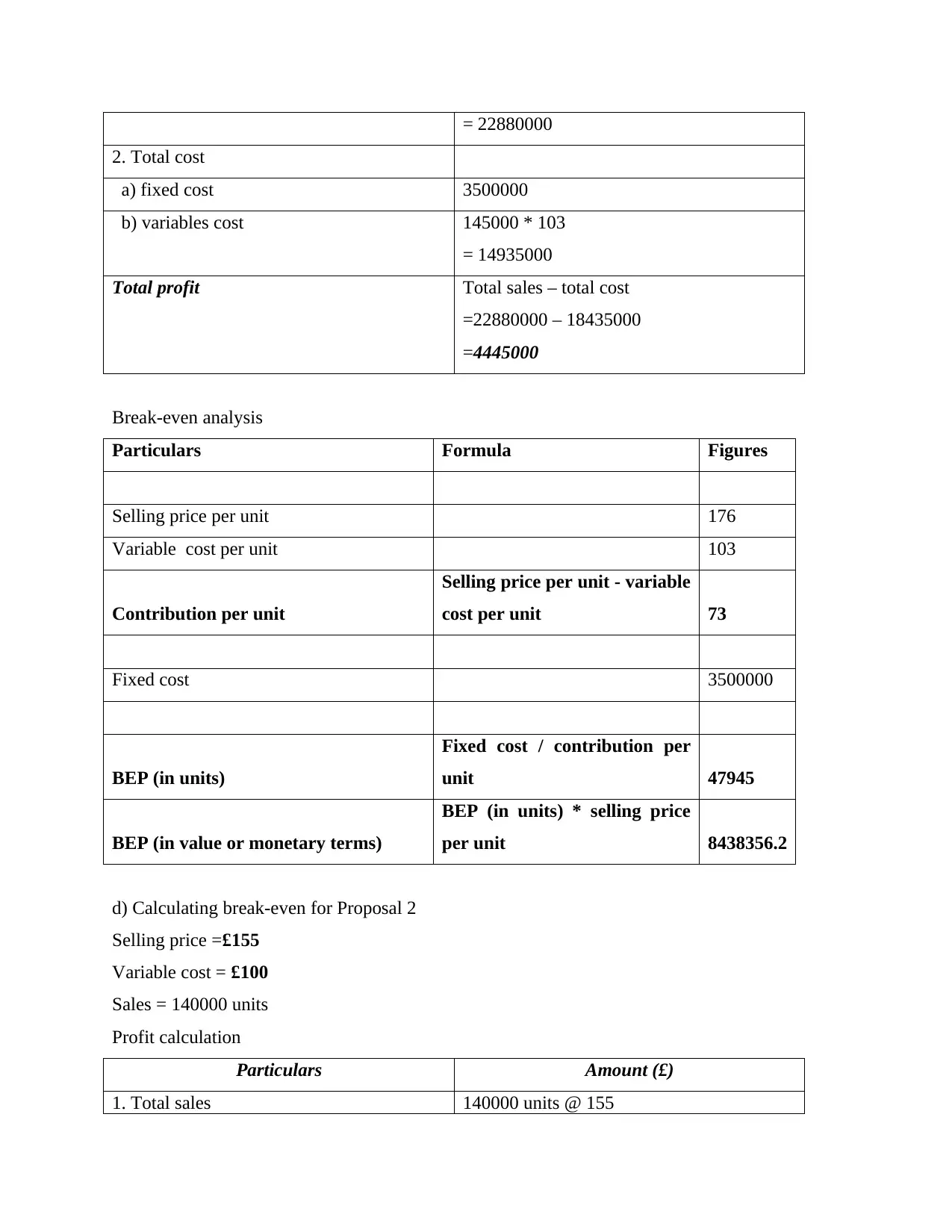

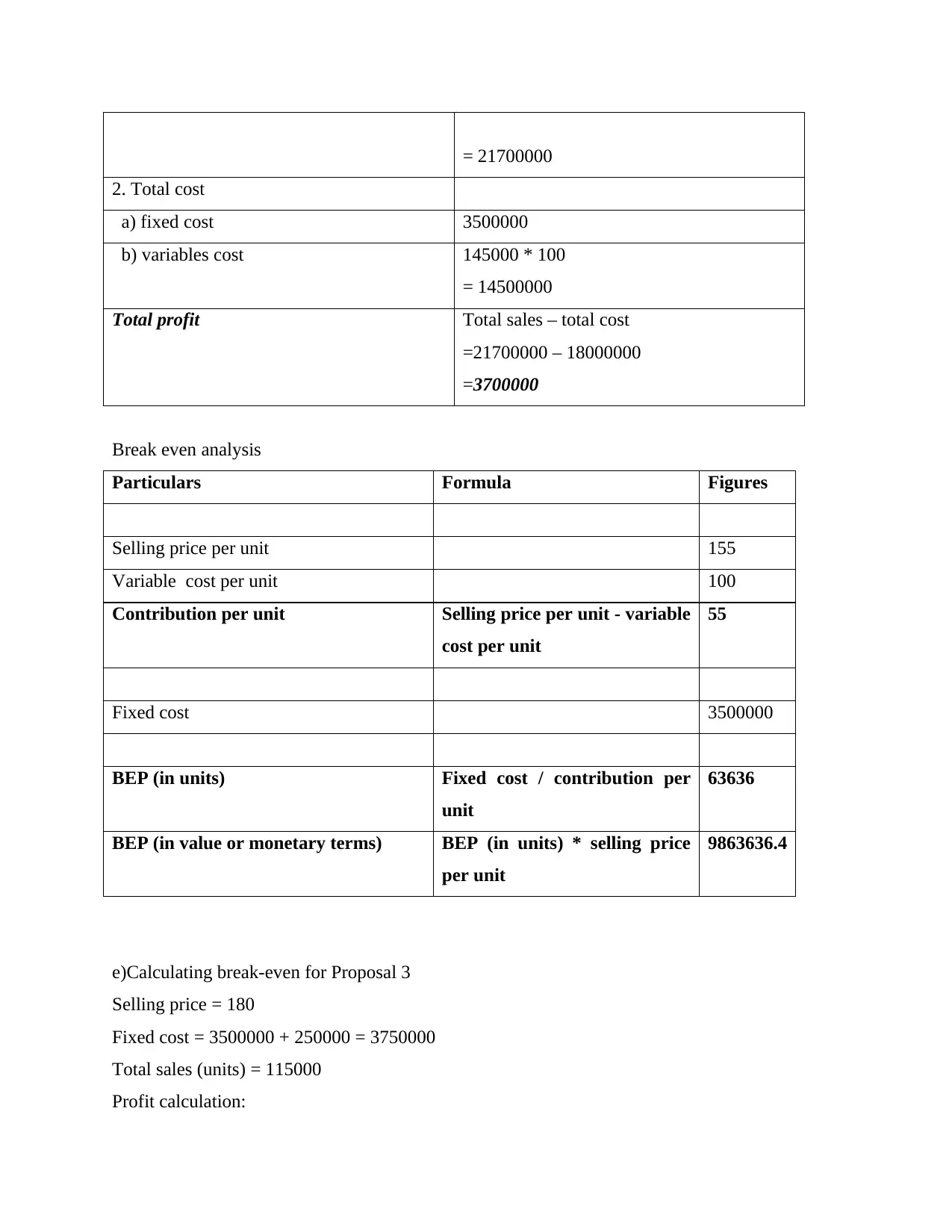

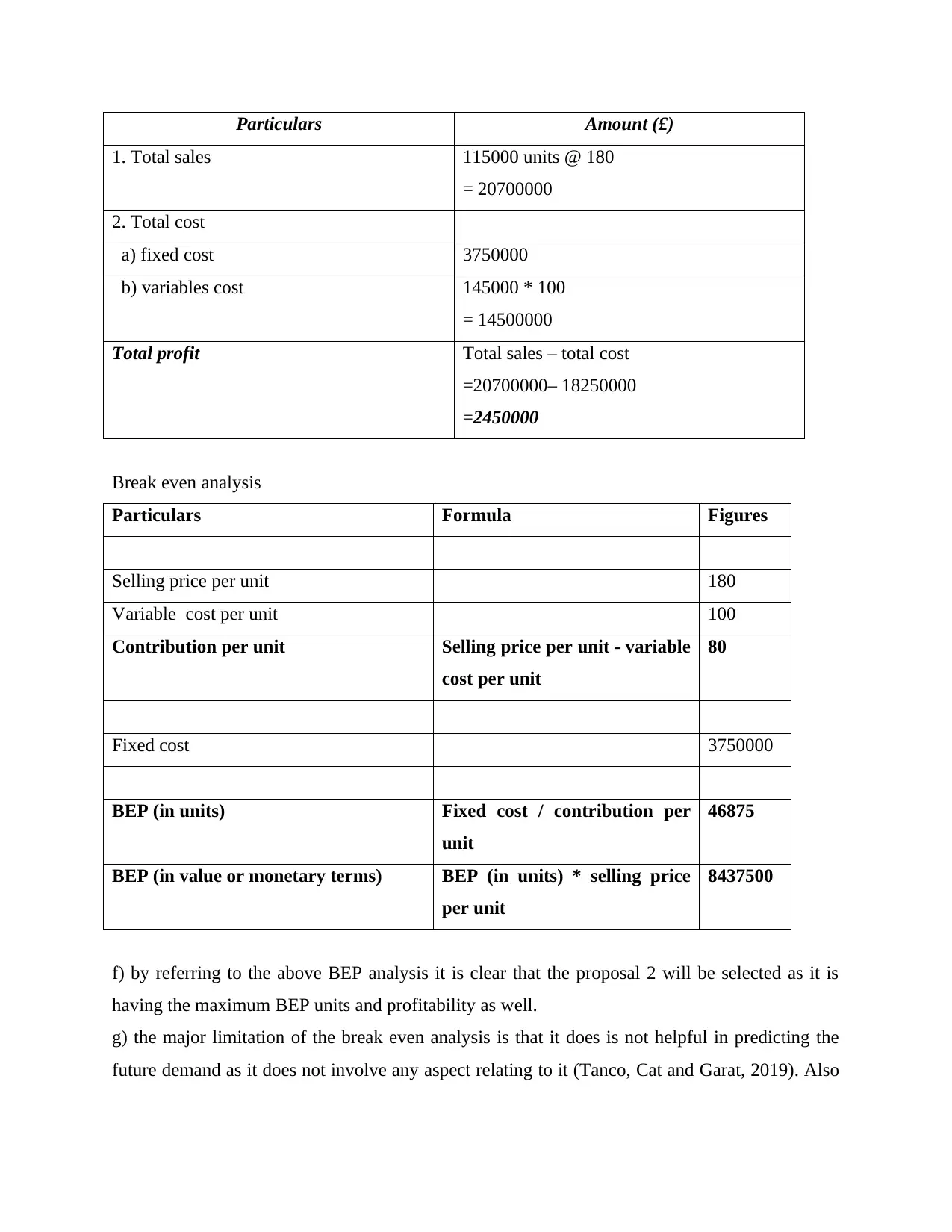

This accounting report provides a detailed analysis of financial statements, investment appraisal techniques, and break-even analysis. It begins with the preparation of an income statement and statement of financial position based on provided data. The report then evaluates a project's financial viability using payback period and net present value (NPV) calculations, advising on the project's feasibility based on these metrics. It also discusses non-financial factors that should be considered in investment decisions and comments on the internal rate of return (IRR). Furthermore, the report calculates break-even points under different scenarios, evaluating the profitability and BEP units for various proposals, and discusses the limitations of break-even analysis. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.