Accounting for Business: Income Statement, Financial Position, Investment Appraisal, Financial Ratios of NS plc

VerifiedAdded on 2023/06/11

|10

|1647

|239

AI Summary

This article covers Accounting for Business including Income Statement, Financial Position, Investment Appraisal, and Financial Ratios of NS plc. It also includes non-financial factors affecting the decision and IRR and its advantages.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting for Business

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Preparing income statement for the year ended 31 December 2021.......................................3

b. Preparing statement of financial position as on 31 December 2021.......................................4

SECTION B.....................................................................................................................................5

QUESTION 2...................................................................................................................................5

a. Calculating payback period and net present value..................................................................5

b. Advising K plc for investment................................................................................................6

c. Non- financial factors affecting the decision..........................................................................7

d. IRR and its advantages............................................................................................................7

QUESTION 4...................................................................................................................................7

a. Calculating the ratios of NS plc..............................................................................................7

b. Commenting on the financial ratios of NS plc........................................................................8

REFERENCES..............................................................................................................................10

SECTION A.....................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Preparing income statement for the year ended 31 December 2021.......................................3

b. Preparing statement of financial position as on 31 December 2021.......................................4

SECTION B.....................................................................................................................................5

QUESTION 2...................................................................................................................................5

a. Calculating payback period and net present value..................................................................5

b. Advising K plc for investment................................................................................................6

c. Non- financial factors affecting the decision..........................................................................7

d. IRR and its advantages............................................................................................................7

QUESTION 4...................................................................................................................................7

a. Calculating the ratios of NS plc..............................................................................................7

b. Commenting on the financial ratios of NS plc........................................................................8

REFERENCES..............................................................................................................................10

SECTION A

QUESTION 1

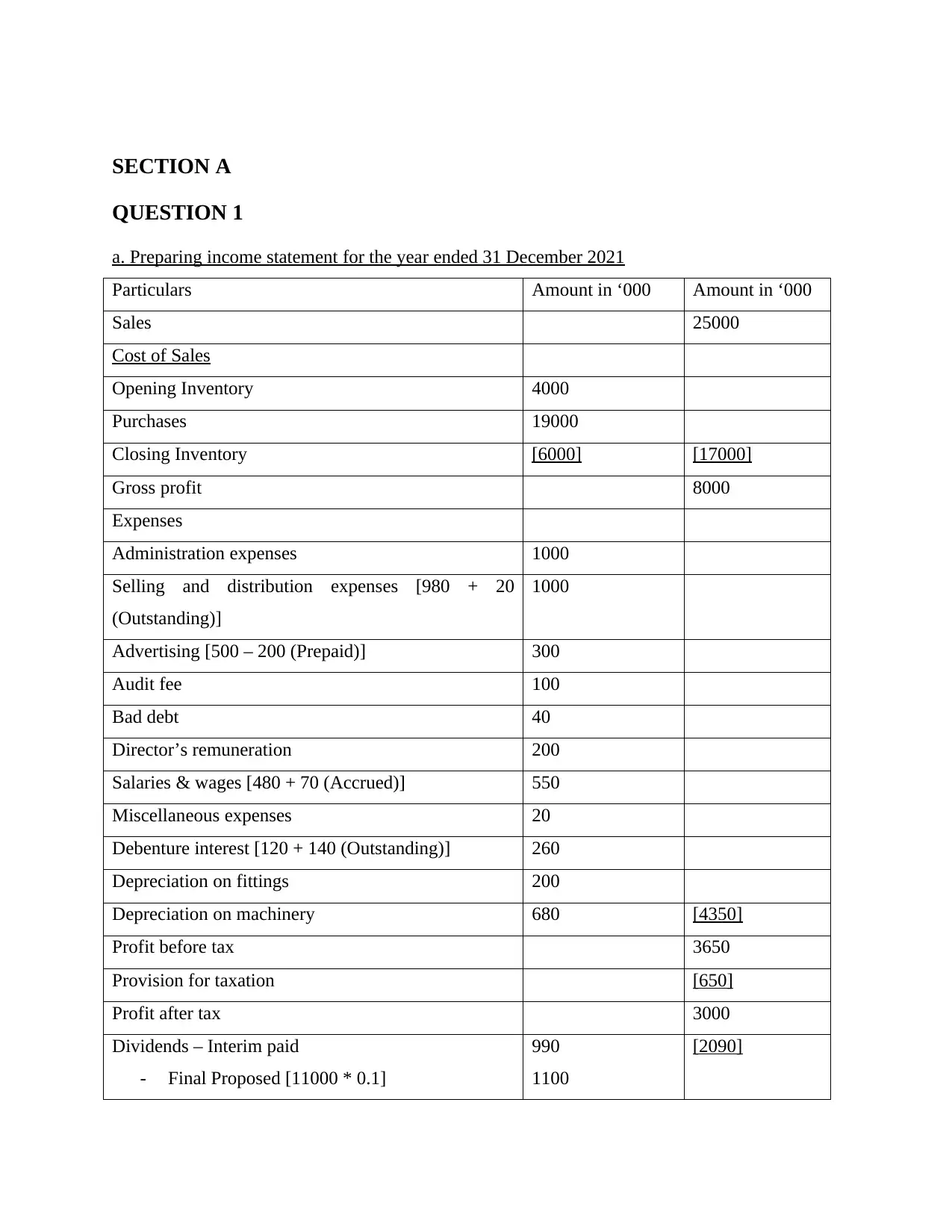

a. Preparing income statement for the year ended 31 December 2021

Particulars Amount in ‘000 Amount in ‘000

Sales 25000

Cost of Sales

Opening Inventory 4000

Purchases 19000

Closing Inventory [6000] [17000]

Gross profit 8000

Expenses

Administration expenses 1000

Selling and distribution expenses [980 + 20

(Outstanding)]

1000

Advertising [500 – 200 (Prepaid)] 300

Audit fee 100

Bad debt 40

Director’s remuneration 200

Salaries & wages [480 + 70 (Accrued)] 550

Miscellaneous expenses 20

Debenture interest [120 + 140 (Outstanding)] 260

Depreciation on fittings 200

Depreciation on machinery 680 [4350]

Profit before tax 3650

Provision for taxation [650]

Profit after tax 3000

Dividends – Interim paid

- Final Proposed [11000 * 0.1]

990

1100

[2090]

QUESTION 1

a. Preparing income statement for the year ended 31 December 2021

Particulars Amount in ‘000 Amount in ‘000

Sales 25000

Cost of Sales

Opening Inventory 4000

Purchases 19000

Closing Inventory [6000] [17000]

Gross profit 8000

Expenses

Administration expenses 1000

Selling and distribution expenses [980 + 20

(Outstanding)]

1000

Advertising [500 – 200 (Prepaid)] 300

Audit fee 100

Bad debt 40

Director’s remuneration 200

Salaries & wages [480 + 70 (Accrued)] 550

Miscellaneous expenses 20

Debenture interest [120 + 140 (Outstanding)] 260

Depreciation on fittings 200

Depreciation on machinery 680 [4350]

Profit before tax 3650

Provision for taxation [650]

Profit after tax 3000

Dividends – Interim paid

- Final Proposed [11000 * 0.1]

990

1100

[2090]

Retained profit for the year 910

Brought forward retained profit 2360

Retained profit carried forward 3270

Working notes

1. Debenture interest to

be paid for year

2. Outstanding debenture

2600 * 10% = 260

Debenture to be paid-

debenture paid= 260- 120=

140

Depreciation of fitting @ 10

%

2000 * 10 % = 200

Depreciation on Machinery on

WDV

= Cost – accumulated

depreciation

4000- 600= 3400

Depreciation= 3400 * 20 % =

680

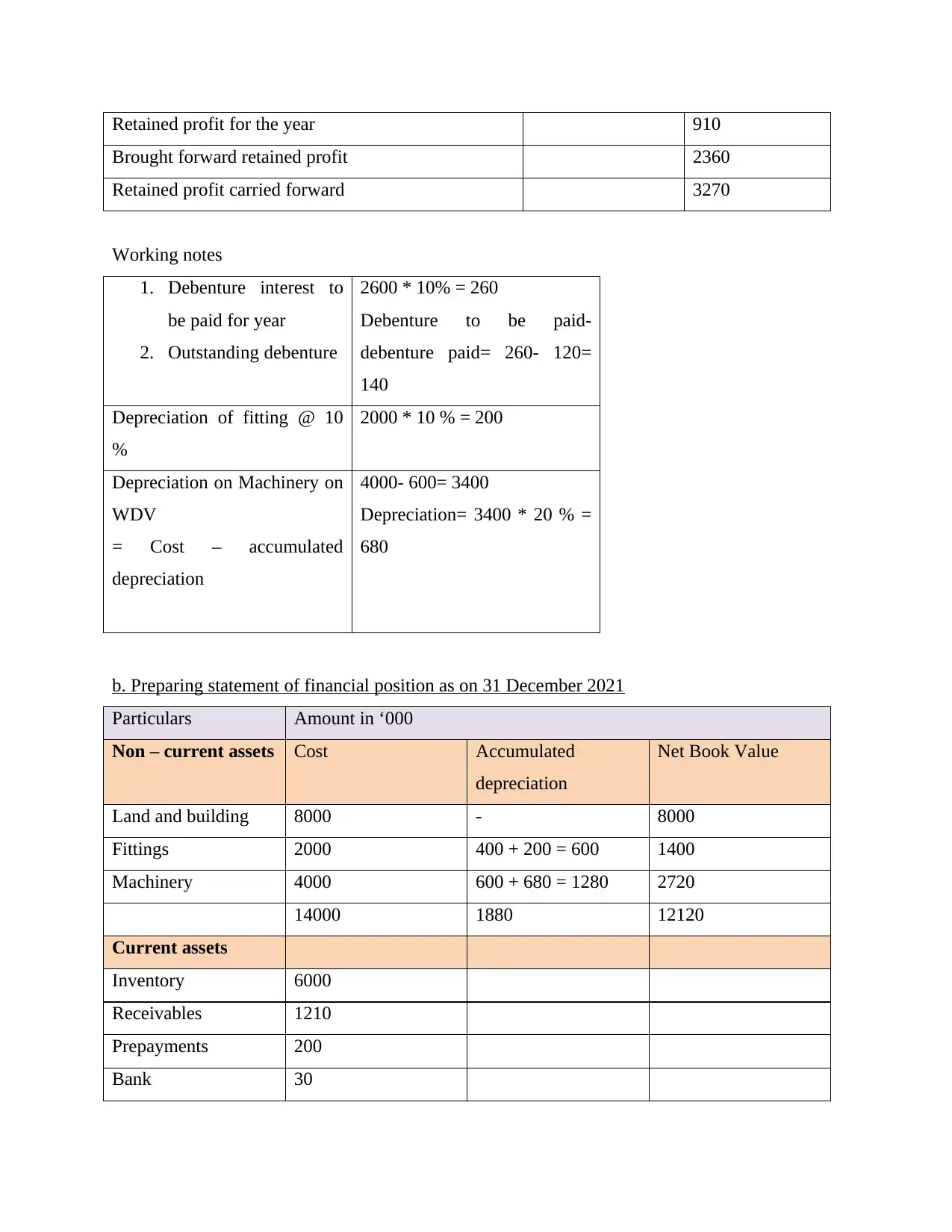

b. Preparing statement of financial position as on 31 December 2021

Particulars Amount in ‘000

Non – current assets Cost Accumulated

depreciation

Net Book Value

Land and building 8000 - 8000

Fittings 2000 400 + 200 = 600 1400

Machinery 4000 600 + 680 = 1280 2720

14000 1880 12120

Current assets

Inventory 6000

Receivables 1210

Prepayments 200

Bank 30

Brought forward retained profit 2360

Retained profit carried forward 3270

Working notes

1. Debenture interest to

be paid for year

2. Outstanding debenture

2600 * 10% = 260

Debenture to be paid-

debenture paid= 260- 120=

140

Depreciation of fitting @ 10

%

2000 * 10 % = 200

Depreciation on Machinery on

WDV

= Cost – accumulated

depreciation

4000- 600= 3400

Depreciation= 3400 * 20 % =

680

b. Preparing statement of financial position as on 31 December 2021

Particulars Amount in ‘000

Non – current assets Cost Accumulated

depreciation

Net Book Value

Land and building 8000 - 8000

Fittings 2000 400 + 200 = 600 1400

Machinery 4000 600 + 680 = 1280 2720

14000 1880 12120

Current assets

Inventory 6000

Receivables 1210

Prepayments 200

Bank 30

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

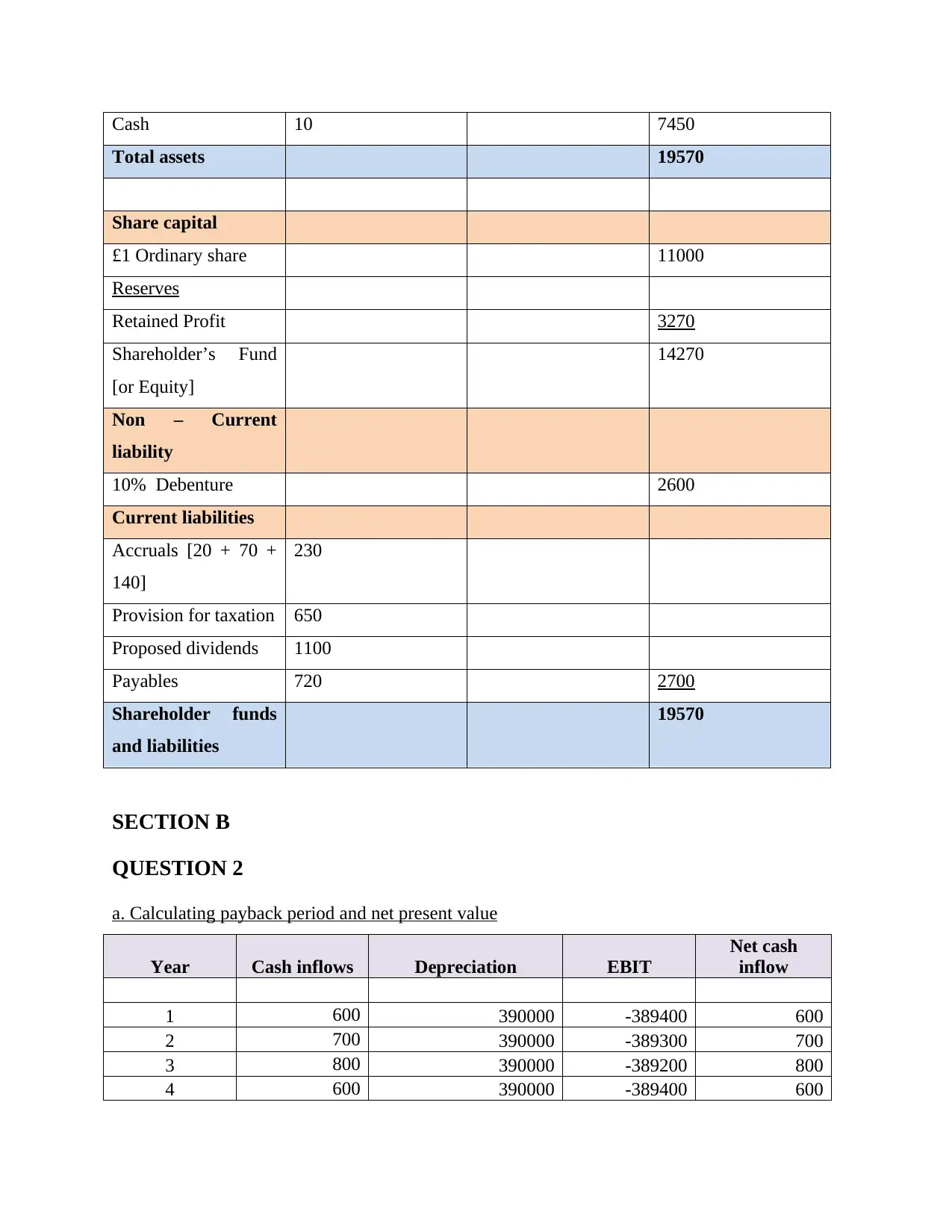

Cash 10 7450

Total assets 19570

Share capital

£1 Ordinary share 11000

Reserves

Retained Profit 3270

Shareholder’s Fund

[or Equity]

14270

Non – Current

liability

10% Debenture 2600

Current liabilities

Accruals [20 + 70 +

140]

230

Provision for taxation 650

Proposed dividends 1100

Payables 720 2700

Shareholder funds

and liabilities

19570

SECTION B

QUESTION 2

a. Calculating payback period and net present value

Year Cash inflows Depreciation EBIT

Net cash

inflow

1 600 390000 -389400 600

2 700 390000 -389300 700

3 800 390000 -389200 800

4 600 390000 -389400 600

Total assets 19570

Share capital

£1 Ordinary share 11000

Reserves

Retained Profit 3270

Shareholder’s Fund

[or Equity]

14270

Non – Current

liability

10% Debenture 2600

Current liabilities

Accruals [20 + 70 +

140]

230

Provision for taxation 650

Proposed dividends 1100

Payables 720 2700

Shareholder funds

and liabilities

19570

SECTION B

QUESTION 2

a. Calculating payback period and net present value

Year Cash inflows Depreciation EBIT

Net cash

inflow

1 600 390000 -389400 600

2 700 390000 -389300 700

3 800 390000 -389200 800

4 600 390000 -389400 600

5 100 390000 -389900 100

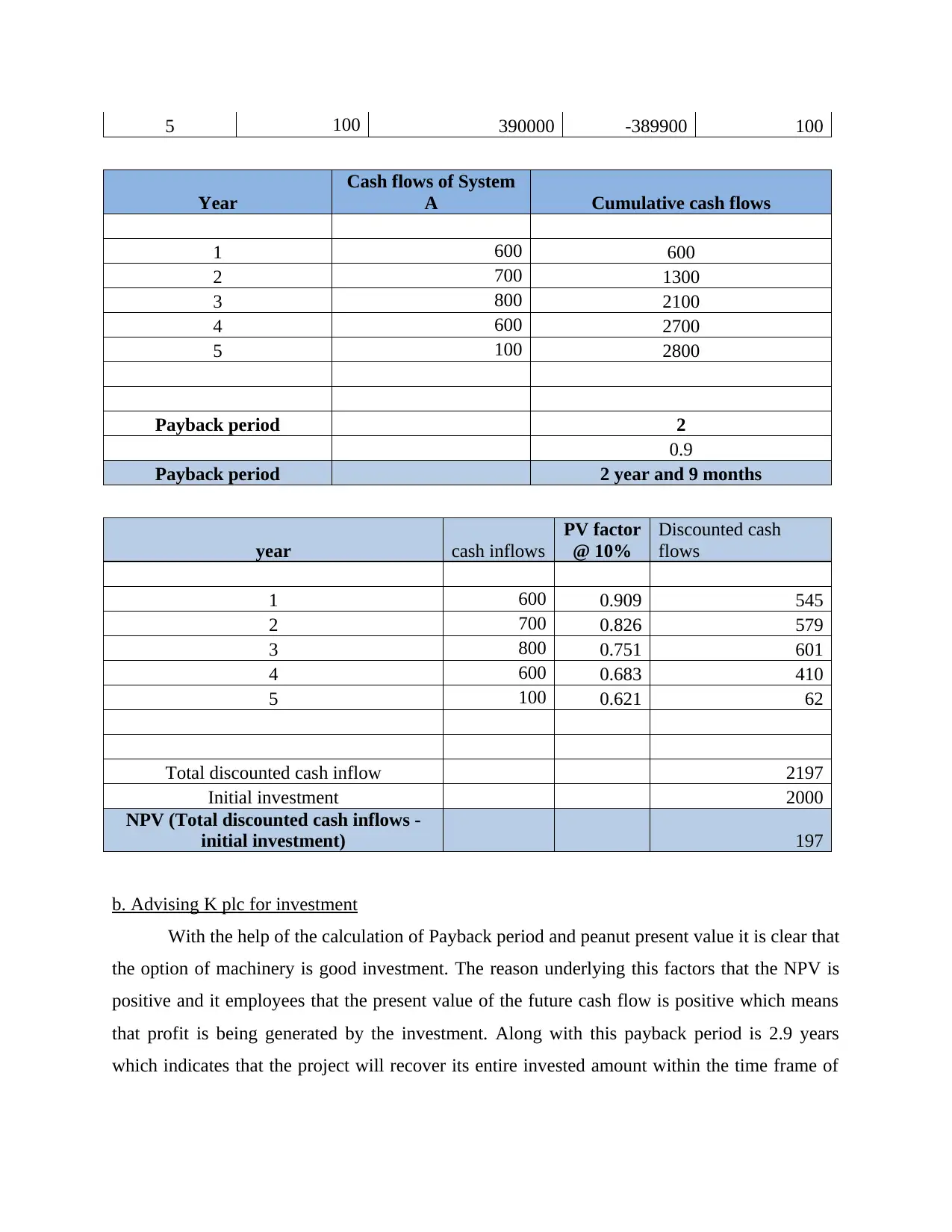

Year

Cash flows of System

A Cumulative cash flows

1 600 600

2 700 1300

3 800 2100

4 600 2700

5 100 2800

Payback period 2

0.9

Payback period 2 year and 9 months

year cash inflows

PV factor

@ 10%

Discounted cash

flows

1 600 0.909 545

2 700 0.826 579

3 800 0.751 601

4 600 0.683 410

5 100 0.621 62

Total discounted cash inflow 2197

Initial investment 2000

NPV (Total discounted cash inflows -

initial investment) 197

b. Advising K plc for investment

With the help of the calculation of Payback period and peanut present value it is clear that

the option of machinery is good investment. The reason underlying this factors that the NPV is

positive and it employees that the present value of the future cash flow is positive which means

that profit is being generated by the investment. Along with this payback period is 2.9 years

which indicates that the project will recover its entire invested amount within the time frame of

Year

Cash flows of System

A Cumulative cash flows

1 600 600

2 700 1300

3 800 2100

4 600 2700

5 100 2800

Payback period 2

0.9

Payback period 2 year and 9 months

year cash inflows

PV factor

@ 10%

Discounted cash

flows

1 600 0.909 545

2 700 0.826 579

3 800 0.751 601

4 600 0.683 410

5 100 0.621 62

Total discounted cash inflow 2197

Initial investment 2000

NPV (Total discounted cash inflows -

initial investment) 197

b. Advising K plc for investment

With the help of the calculation of Payback period and peanut present value it is clear that

the option of machinery is good investment. The reason underlying this factors that the NPV is

positive and it employees that the present value of the future cash flow is positive which means

that profit is being generated by the investment. Along with this payback period is 2.9 years

which indicates that the project will recover its entire invested amount within the time frame of

less than 3 years. This is advisable to the company that they must invest within the project as the

payback period required by the companies also 3 years.

c. Non- financial factors affecting the decision

The non financial factors which need to be considered at time of taking investment appraisal

decision includes the following-

The first thing to be considered is to match the industry standard and the practices which

other companies are following (Hazen and Magni, 2021). This is necessary because in case

this will not be considered then it will be impacting the working efficiency.

Along with this another non financial factors to be considered is complaint with the future

legislations and current laws.

In addition to this another non financial factor to be considered for taking investment

decision is the political and other changes being taken place within the environment.

Moreover in addition to this another thing to be considered is the product quality and the

services which will be provided to the consumers need to be good and effective.

Along with this the technology and others related aspects need to be considered while taking

decision relating to the investment appraisal.

d. IRR and its advantages

The internal rate of return is a tool used within the financial analysis while estimating the

profitability which or potential investment can generate. Any investment is being done in order

to improve the profitability of the business and in case the investment option is not profitable

than it will be affecting the work in efficiency. Hence IRR helps company in estimating the

profitability of the investment and the present value of the future cash flow.

Advantages of IRR

One of the most common benefits of using internal rate of return is that it includes the

time value of money within the calculation. Hence this includes the present value of the

future cash flow is equivalent to the required capital investment.

In addition to this another benefit is that be use of IRR is very easy to be calculated.

Along with this another benefit of using the IRR is that it assists in ranking the project on

the basis of the profitability which they generate (Al-Mutairi, Naser and Saeid, 2018).

payback period required by the companies also 3 years.

c. Non- financial factors affecting the decision

The non financial factors which need to be considered at time of taking investment appraisal

decision includes the following-

The first thing to be considered is to match the industry standard and the practices which

other companies are following (Hazen and Magni, 2021). This is necessary because in case

this will not be considered then it will be impacting the working efficiency.

Along with this another non financial factors to be considered is complaint with the future

legislations and current laws.

In addition to this another non financial factor to be considered for taking investment

decision is the political and other changes being taken place within the environment.

Moreover in addition to this another thing to be considered is the product quality and the

services which will be provided to the consumers need to be good and effective.

Along with this the technology and others related aspects need to be considered while taking

decision relating to the investment appraisal.

d. IRR and its advantages

The internal rate of return is a tool used within the financial analysis while estimating the

profitability which or potential investment can generate. Any investment is being done in order

to improve the profitability of the business and in case the investment option is not profitable

than it will be affecting the work in efficiency. Hence IRR helps company in estimating the

profitability of the investment and the present value of the future cash flow.

Advantages of IRR

One of the most common benefits of using internal rate of return is that it includes the

time value of money within the calculation. Hence this includes the present value of the

future cash flow is equivalent to the required capital investment.

In addition to this another benefit is that be use of IRR is very easy to be calculated.

Along with this another benefit of using the IRR is that it assists in ranking the project on

the basis of the profitability which they generate (Al-Mutairi, Naser and Saeid, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4

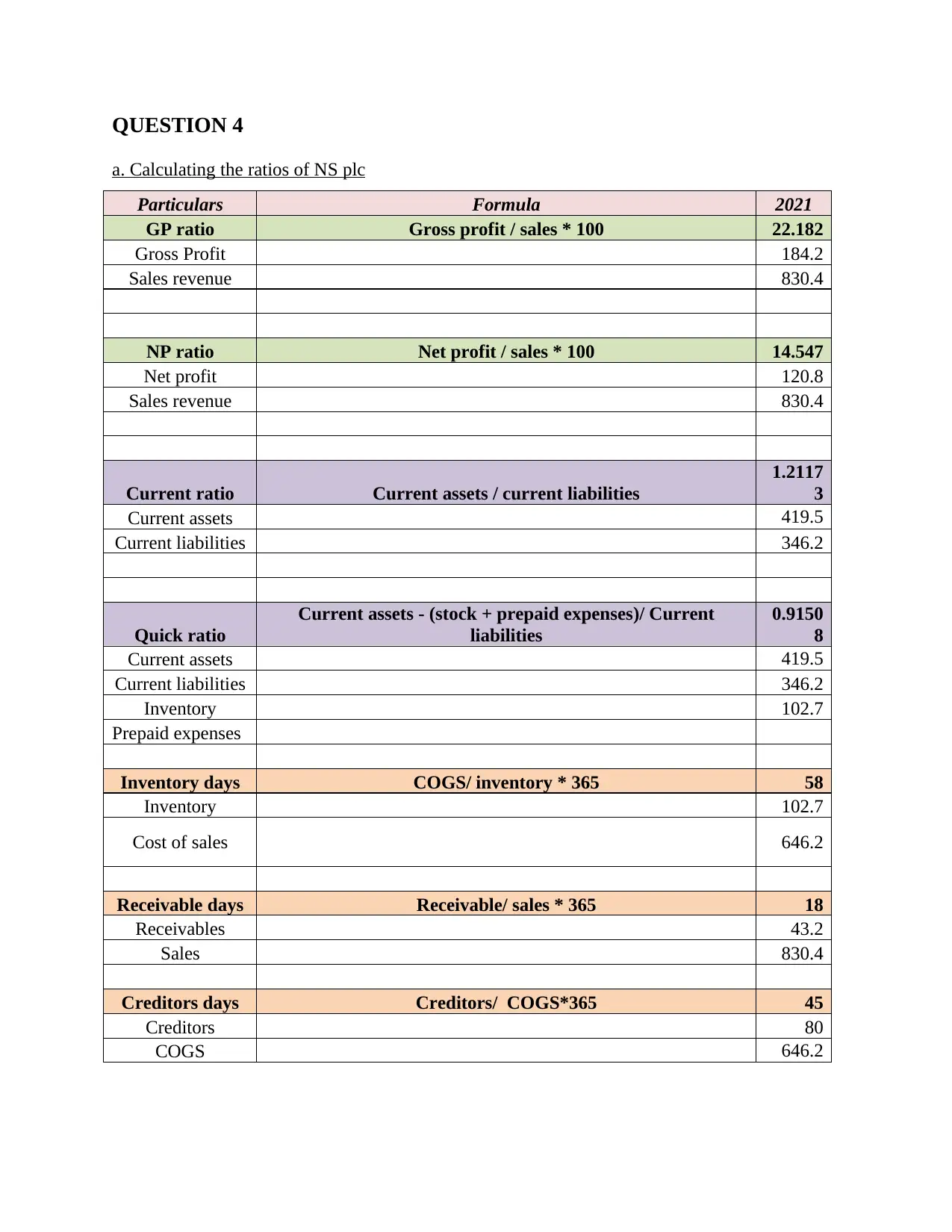

a. Calculating the ratios of NS plc

Particulars Formula 2021

GP ratio Gross profit / sales * 100 22.182

Gross Profit 184.2

Sales revenue 830.4

NP ratio Net profit / sales * 100 14.547

Net profit 120.8

Sales revenue 830.4

Current ratio Current assets / current liabilities

1.2117

3

Current assets 419.5

Current liabilities 346.2

Quick ratio

Current assets - (stock + prepaid expenses)/ Current

liabilities

0.9150

8

Current assets 419.5

Current liabilities 346.2

Inventory 102.7

Prepaid expenses

Inventory days COGS/ inventory * 365 58

Inventory 102.7

Cost of sales 646.2

Receivable days Receivable/ sales * 365 18

Receivables 43.2

Sales 830.4

Creditors days Creditors/ COGS*365 45

Creditors 80

COGS 646.2

a. Calculating the ratios of NS plc

Particulars Formula 2021

GP ratio Gross profit / sales * 100 22.182

Gross Profit 184.2

Sales revenue 830.4

NP ratio Net profit / sales * 100 14.547

Net profit 120.8

Sales revenue 830.4

Current ratio Current assets / current liabilities

1.2117

3

Current assets 419.5

Current liabilities 346.2

Quick ratio

Current assets - (stock + prepaid expenses)/ Current

liabilities

0.9150

8

Current assets 419.5

Current liabilities 346.2

Inventory 102.7

Prepaid expenses

Inventory days COGS/ inventory * 365 58

Inventory 102.7

Cost of sales 646.2

Receivable days Receivable/ sales * 365 18

Receivables 43.2

Sales 830.4

Creditors days Creditors/ COGS*365 45

Creditors 80

COGS 646.2

b. Commenting on the financial ratios of NS plc

With the help of the profitability ratio it is clear that the gross profit ratio of the company

is 22% where as the industry average is 35%. This simply implies that working of the company

is not good in comparison to the industry average and NS PLC need to improve its working.

Along with this with the help of the net profit ratio it is clear that companies having 14% where

as the industry average is having 16%. It employees that there is light difference within the net

profit ratio of both the companies.

For the with help of the liquidity ratio that is the current ratio it is 1.2 times where as the

industry average is 2.2 times. Hence, it implies that the performance of the company is not good

in terms of liquidity (Zavadskas and et.al., 2018). With respect to the quick ratio it is somewhat

near to the industry average that as the companies having 0.91 times where as industry average is

0.96 times.

Further with help of the efficiency ratio it is clear that the industry average is good as

compared to the companies’ calculation. This is particularly because of the reason that them the

inventory days of NS plc is 58 days where as the industry average is 50 days. On the other hand

the receivable 18 for the company and 30 for the industry average. In addition to these credited

days is 45 days for companies and 30 days for the industry average. With the overall analysis it

is clear that the efficiency ratio and all the other ratios are good for the industry average and not

for the company. Hence it is advisable to company that they must improve the performance of

them in better an effective manner.

With the help of the profitability ratio it is clear that the gross profit ratio of the company

is 22% where as the industry average is 35%. This simply implies that working of the company

is not good in comparison to the industry average and NS PLC need to improve its working.

Along with this with the help of the net profit ratio it is clear that companies having 14% where

as the industry average is having 16%. It employees that there is light difference within the net

profit ratio of both the companies.

For the with help of the liquidity ratio that is the current ratio it is 1.2 times where as the

industry average is 2.2 times. Hence, it implies that the performance of the company is not good

in terms of liquidity (Zavadskas and et.al., 2018). With respect to the quick ratio it is somewhat

near to the industry average that as the companies having 0.91 times where as industry average is

0.96 times.

Further with help of the efficiency ratio it is clear that the industry average is good as

compared to the companies’ calculation. This is particularly because of the reason that them the

inventory days of NS plc is 58 days where as the industry average is 50 days. On the other hand

the receivable 18 for the company and 30 for the industry average. In addition to these credited

days is 45 days for companies and 30 days for the industry average. With the overall analysis it

is clear that the efficiency ratio and all the other ratios are good for the industry average and not

for the company. Hence it is advisable to company that they must improve the performance of

them in better an effective manner.

REFERENCES

Books and Journals

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics &

Finance. 6(1). p.1468232.

Hazen, G. and Magni, C. A., 2021. Average internal rate of return for risky projects. The

Engineering Economist. 66(2). pp.90-120.

Zavadskas, E. K. and et.al., 2018. A novel multicriteria approach–rough step-wise weight

assessment ratio analysis method (R-SWARA) and its application in logistics. Studies in

Informatics and Control. 27(1). pp.97-106.

Books and Journals

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics &

Finance. 6(1). p.1468232.

Hazen, G. and Magni, C. A., 2021. Average internal rate of return for risky projects. The

Engineering Economist. 66(2). pp.90-120.

Zavadskas, E. K. and et.al., 2018. A novel multicriteria approach–rough step-wise weight

assessment ratio analysis method (R-SWARA) and its application in logistics. Studies in

Informatics and Control. 27(1). pp.97-106.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.