Accounting for Business: Financial Ratios and Investment Decisions

VerifiedAdded on 2023/06/14

|12

|1944

|378

Homework Assignment

AI Summary

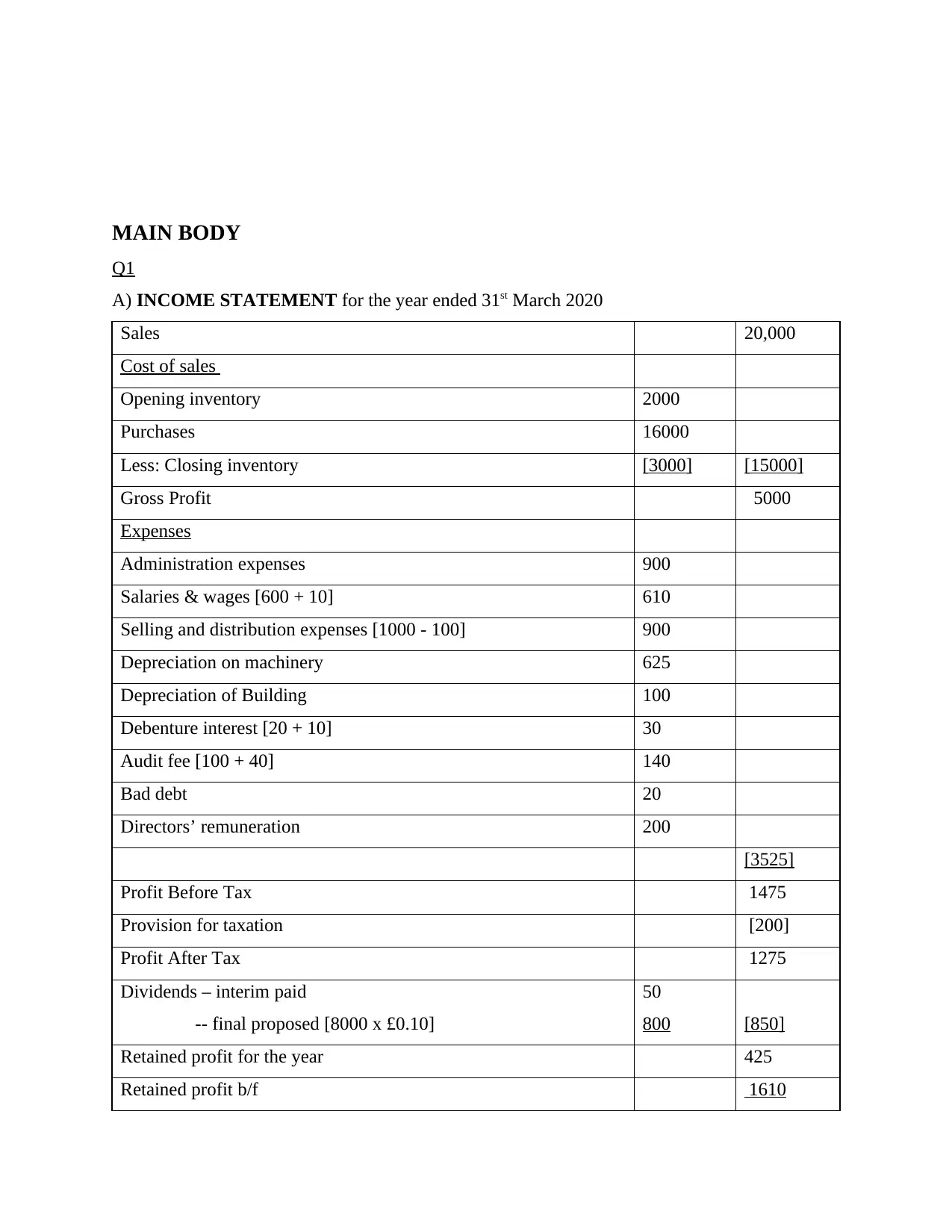

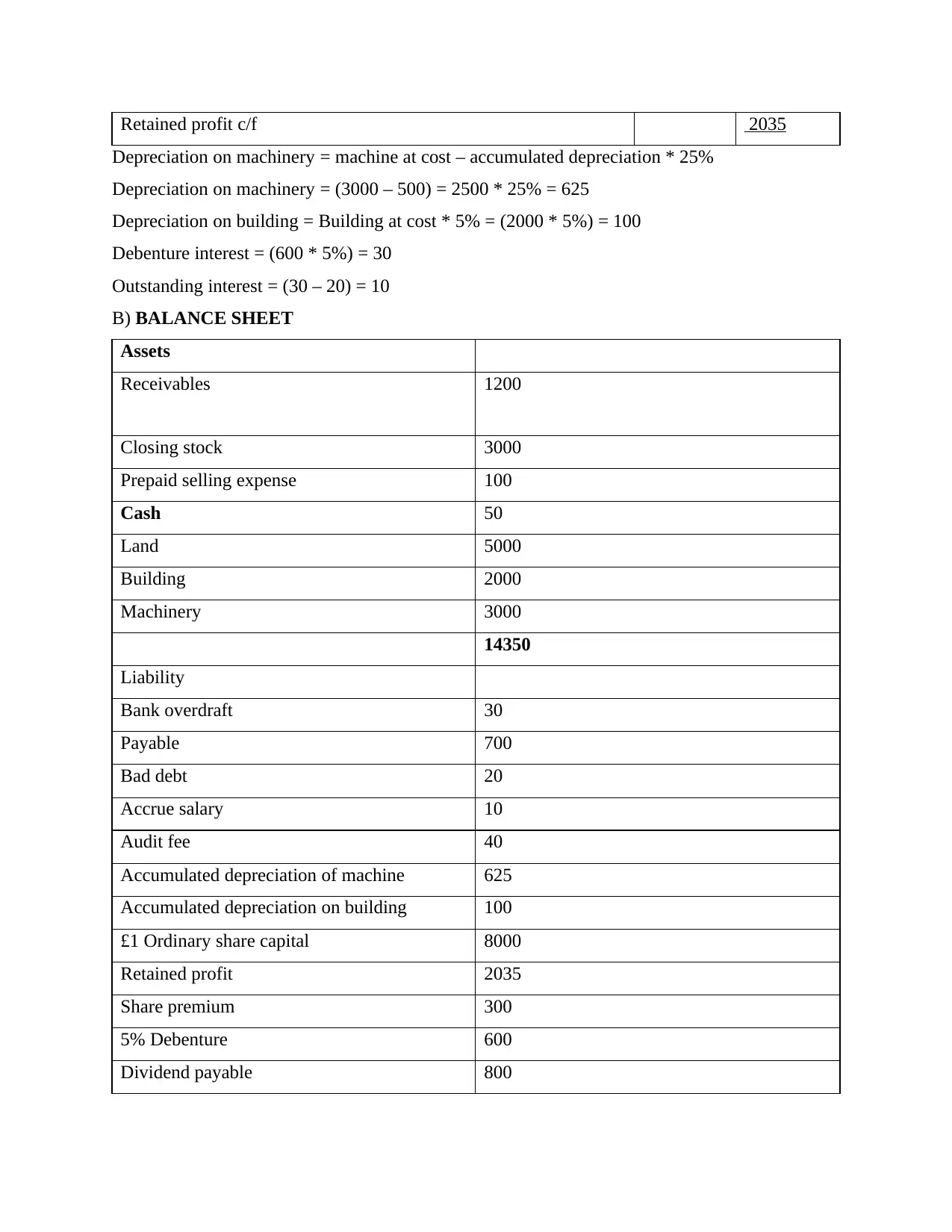

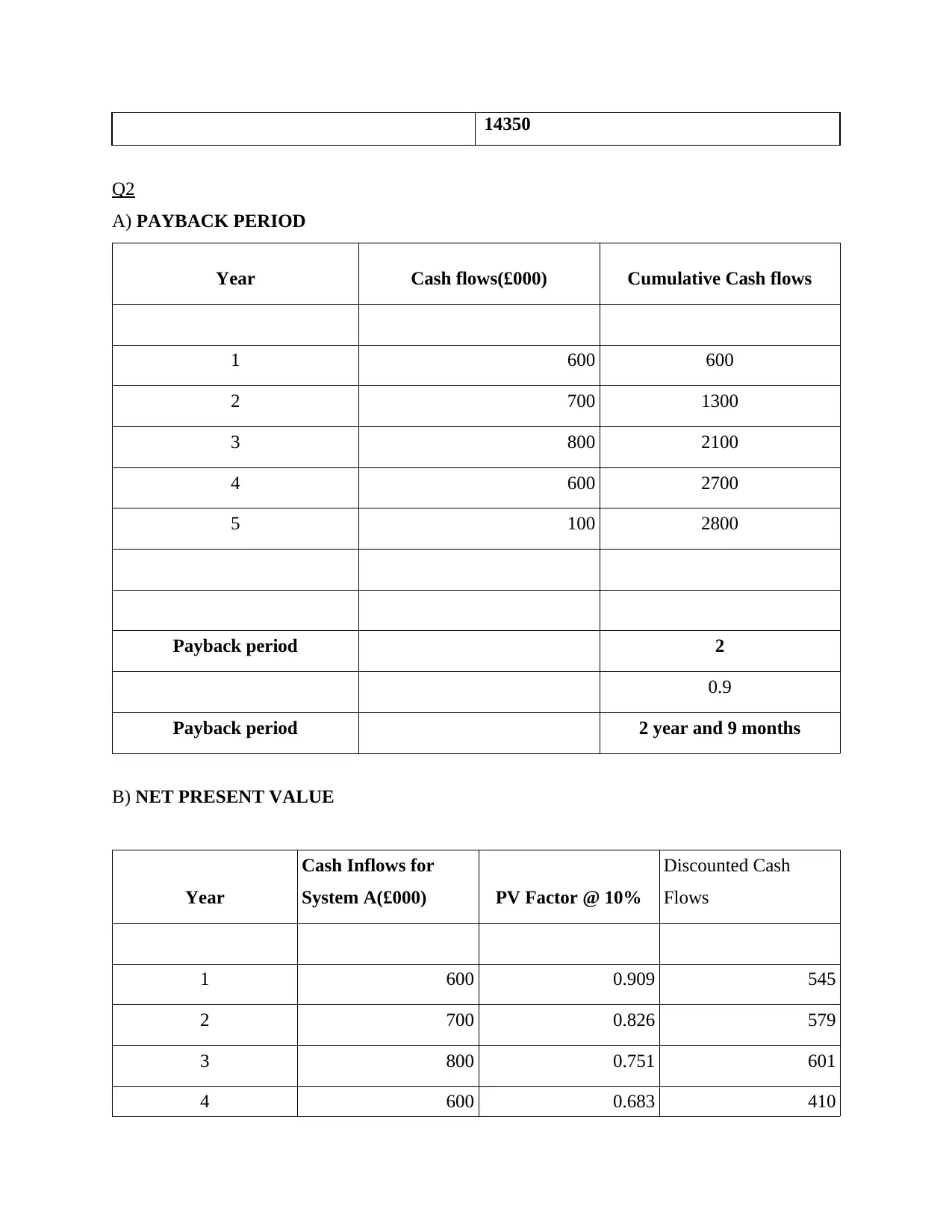

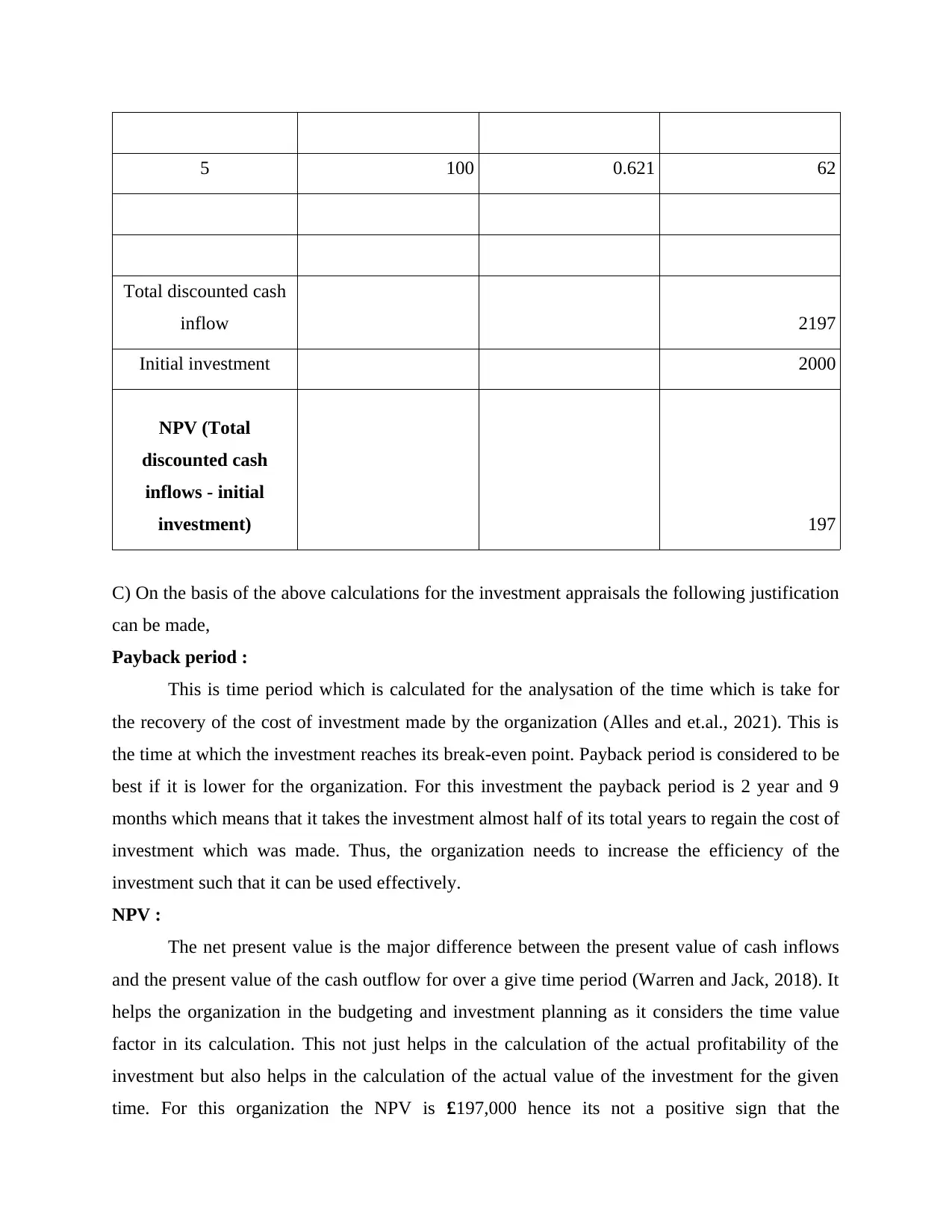

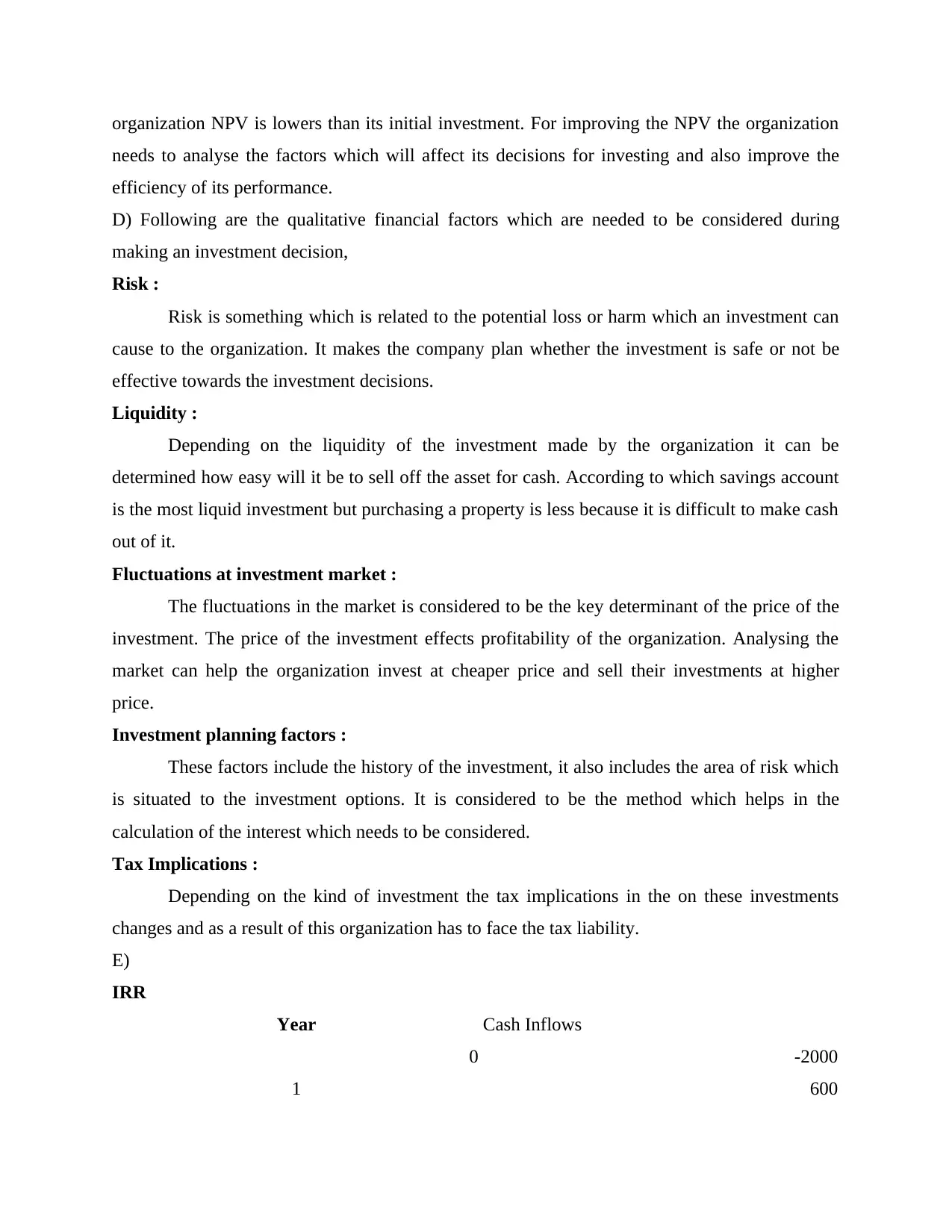

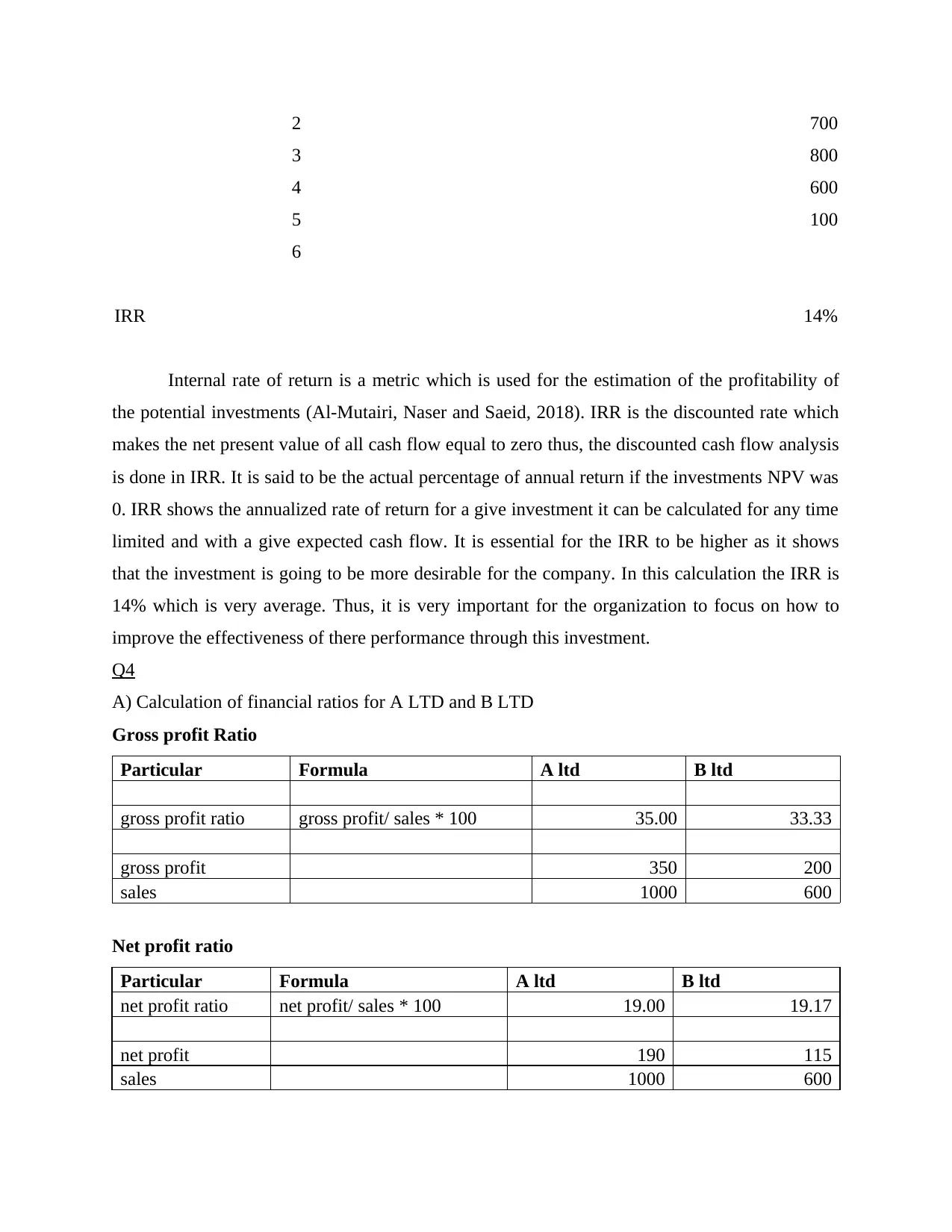

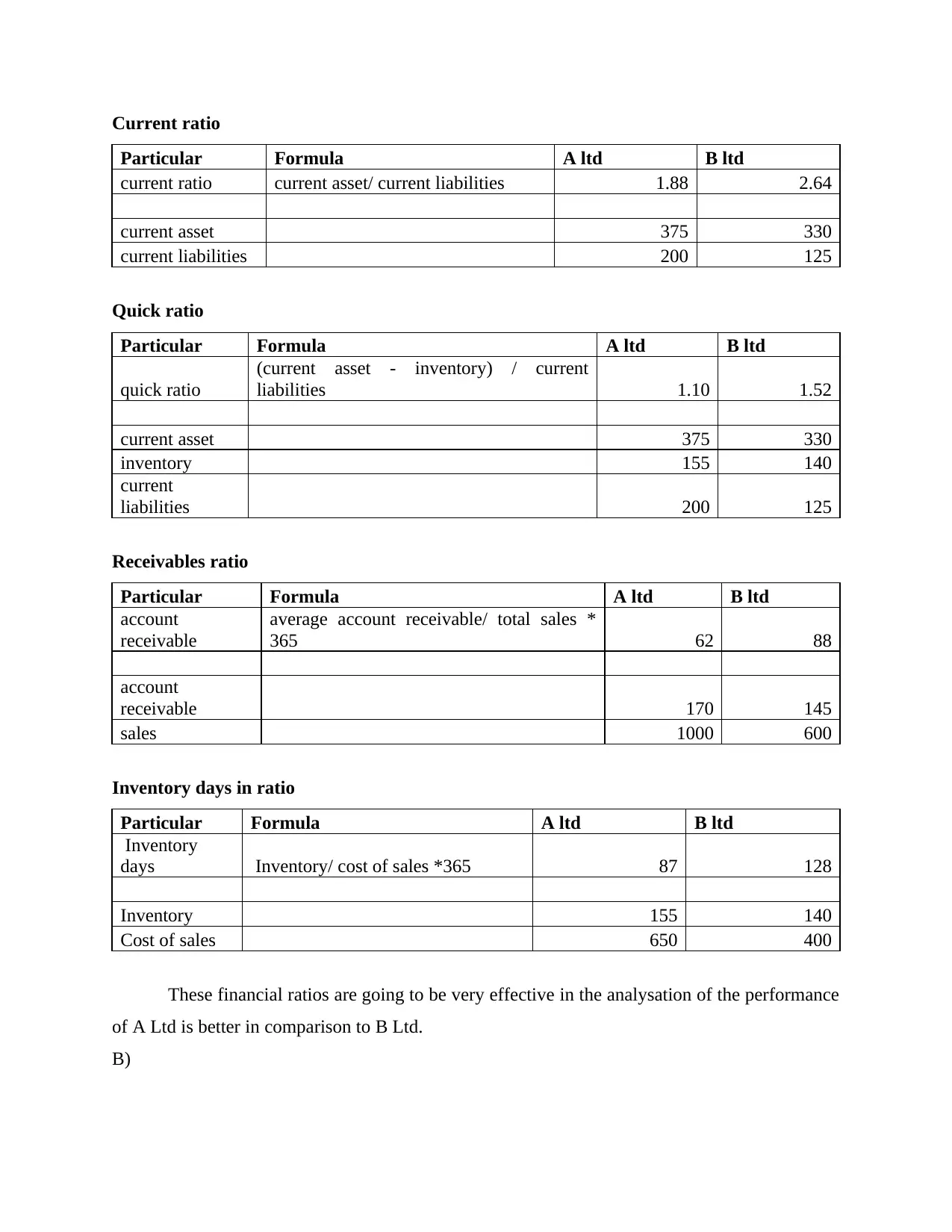

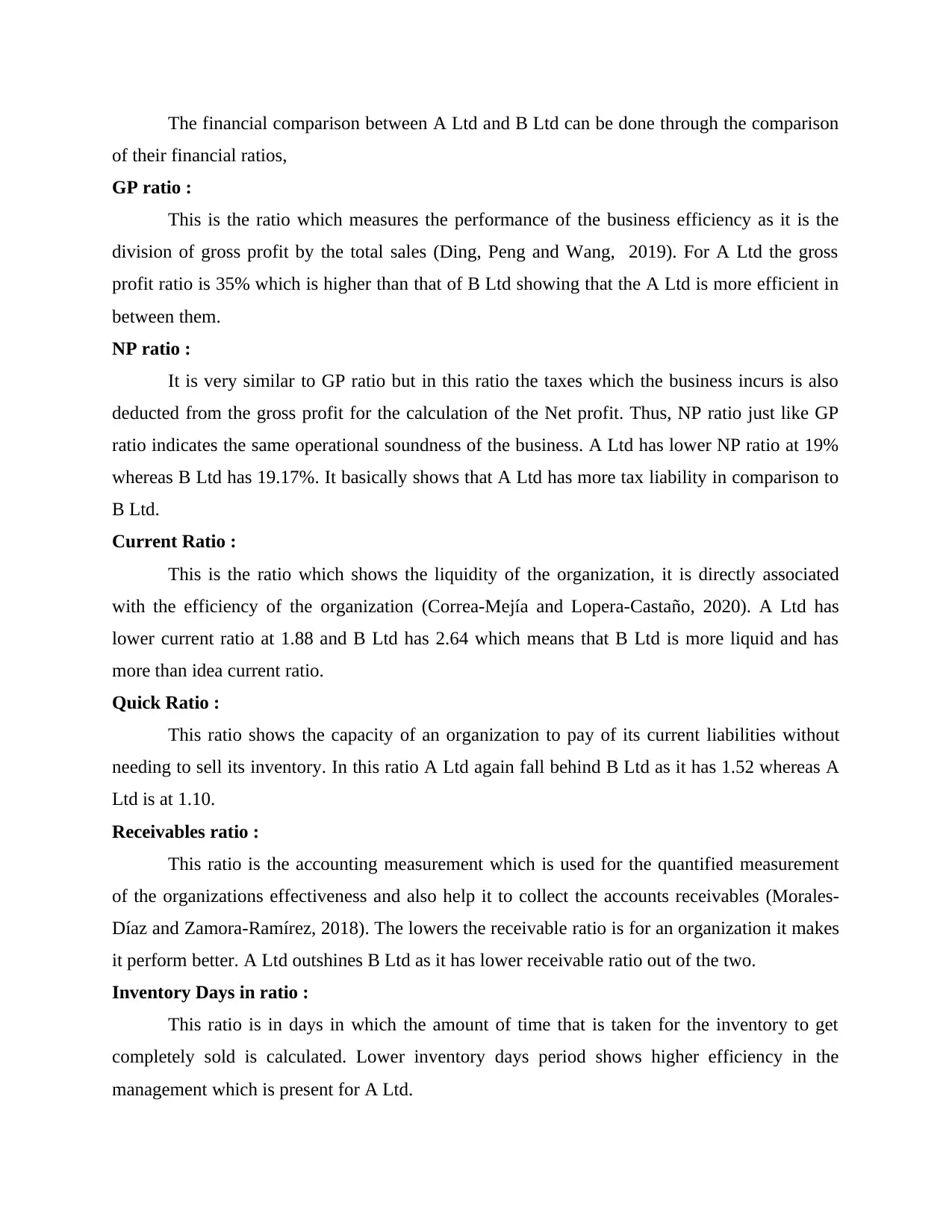

This document presents a comprehensive solution to an accounting for business exam, covering key areas such as financial statement analysis and investment appraisal. The solution includes the preparation of an income statement and balance sheet, along with calculations and interpretations of financial ratios like gross profit ratio, net profit ratio, current ratio, and quick ratio for two companies. Furthermore, the document evaluates investment opportunities using payback period, net present value (NPV), and internal rate of return (IRR) methods, discussing the qualitative factors influencing investment decisions. This resource is ideal for students seeking to understand and master fundamental concepts in accounting and finance, with Desklib providing additional study tools and solved assignments.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.