Holmes Institute HC1010 Accounting for Business Assignment

VerifiedAdded on 2022/11/26

|7

|1245

|405

Homework Assignment

AI Summary

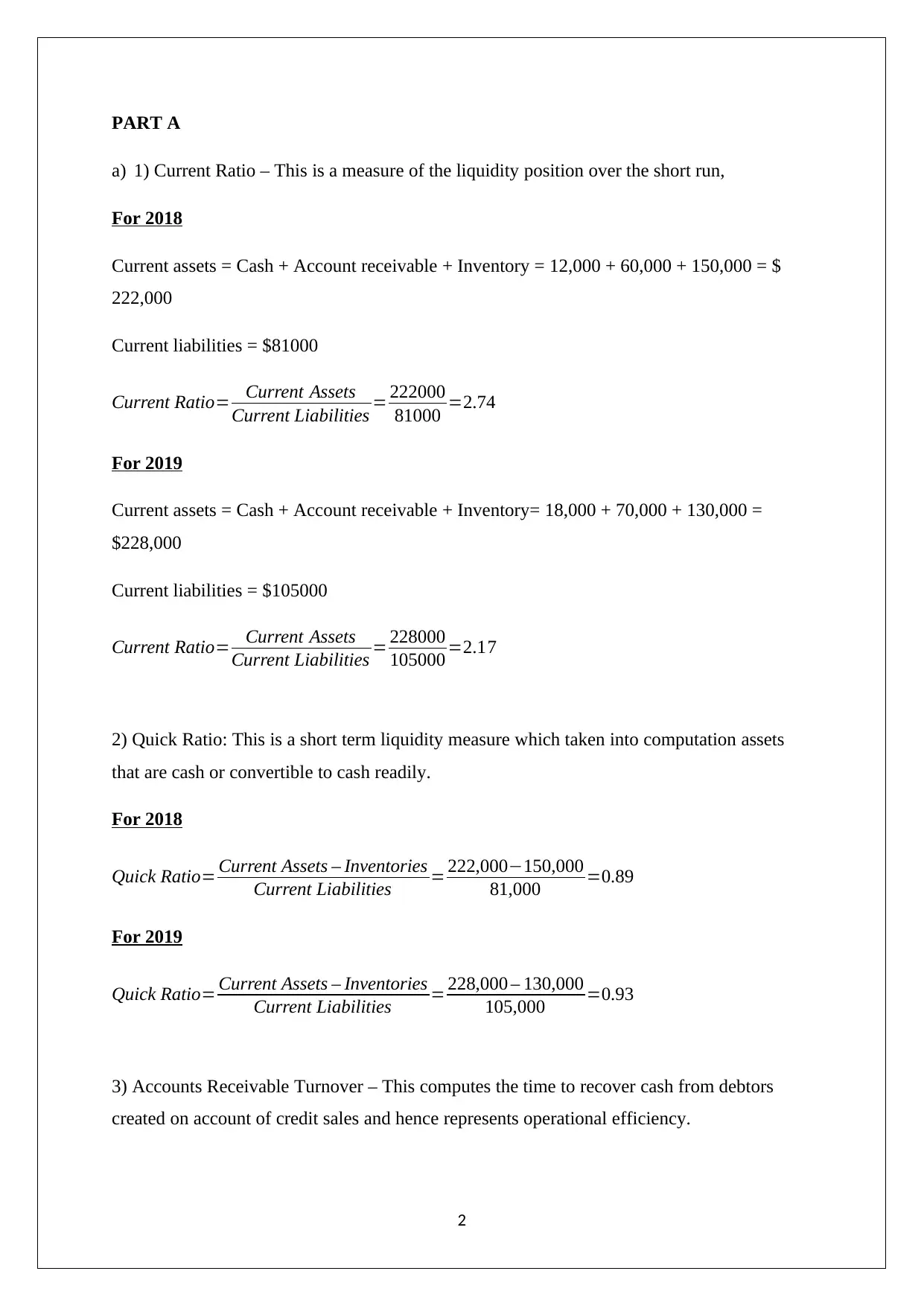

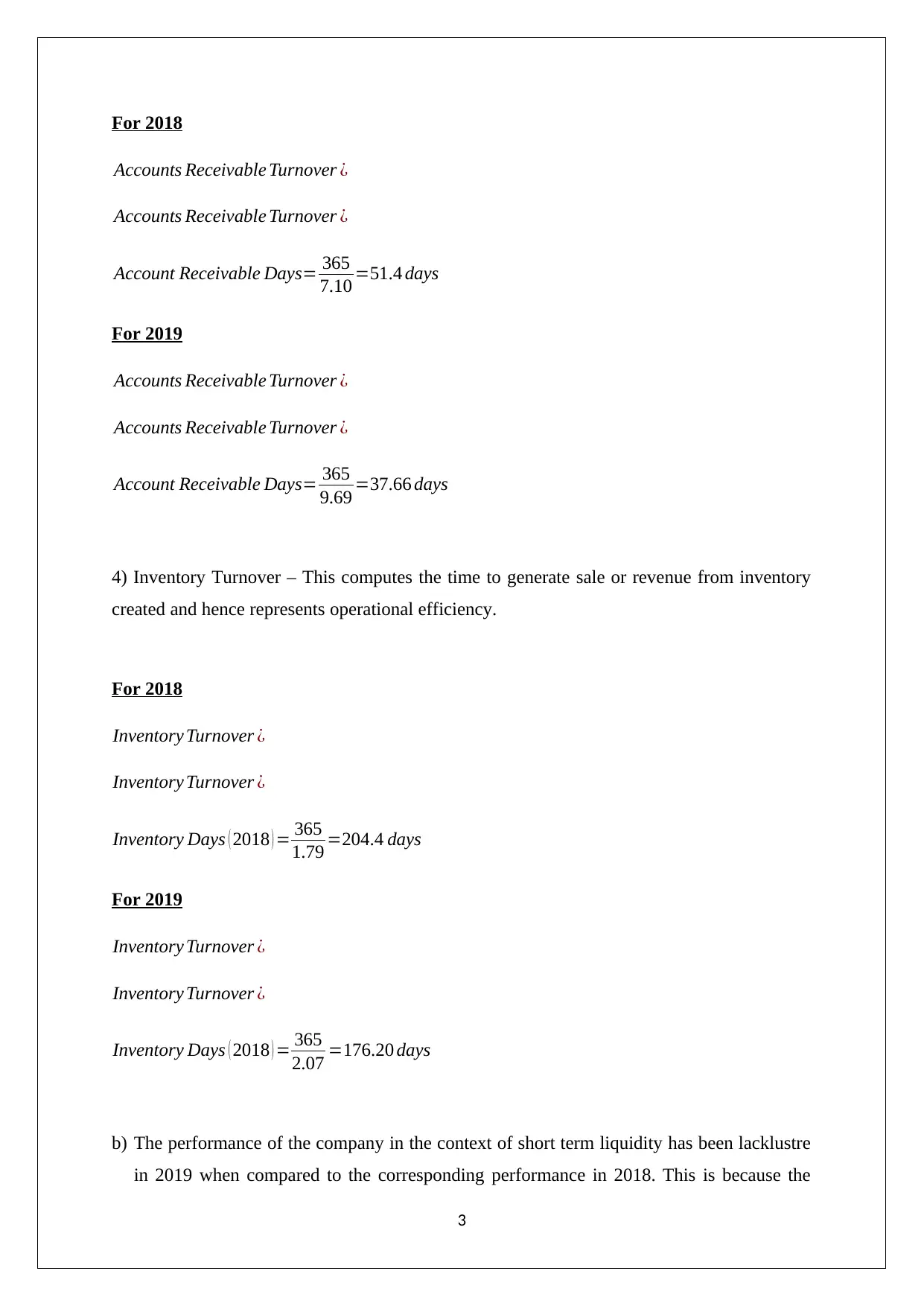

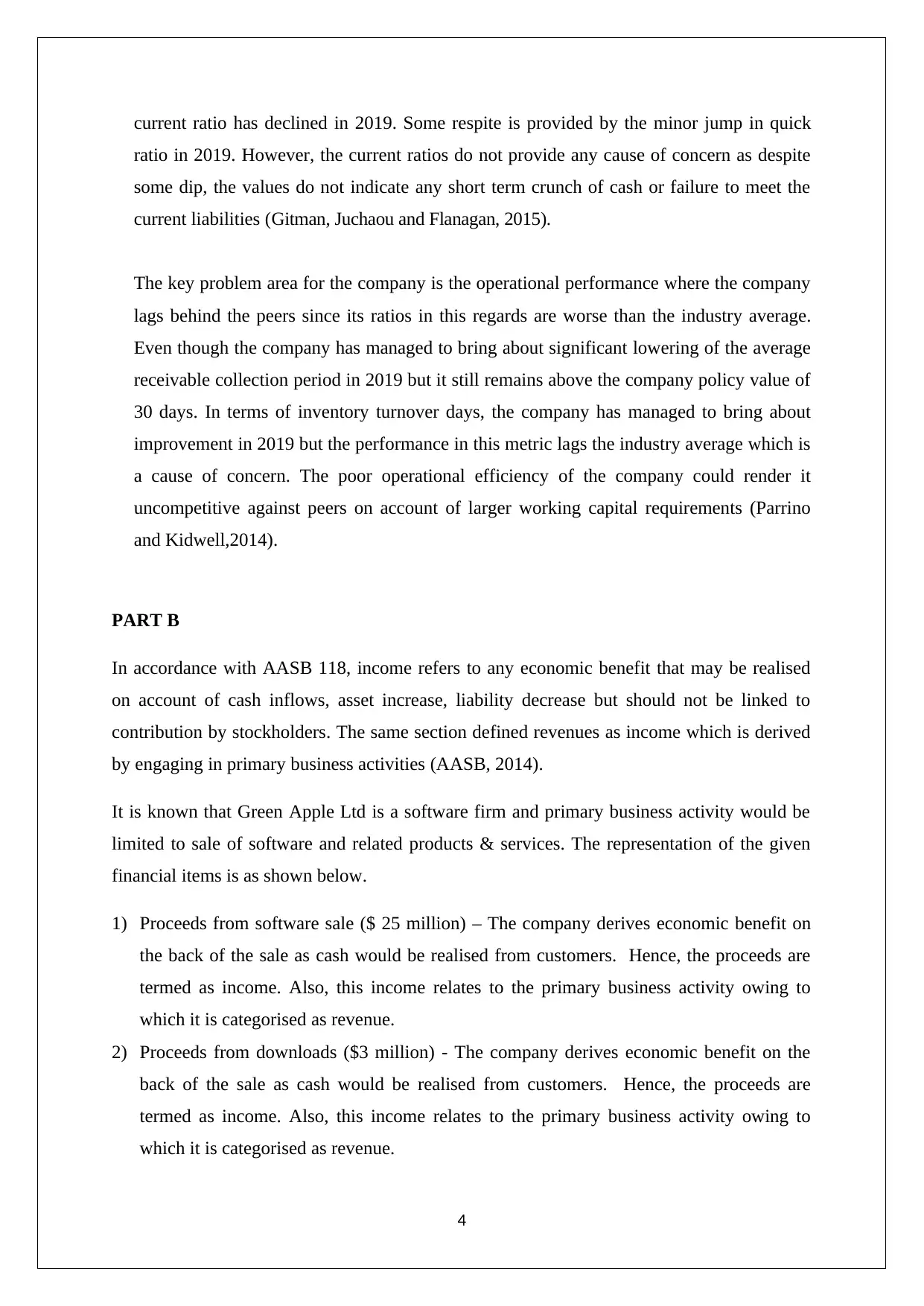

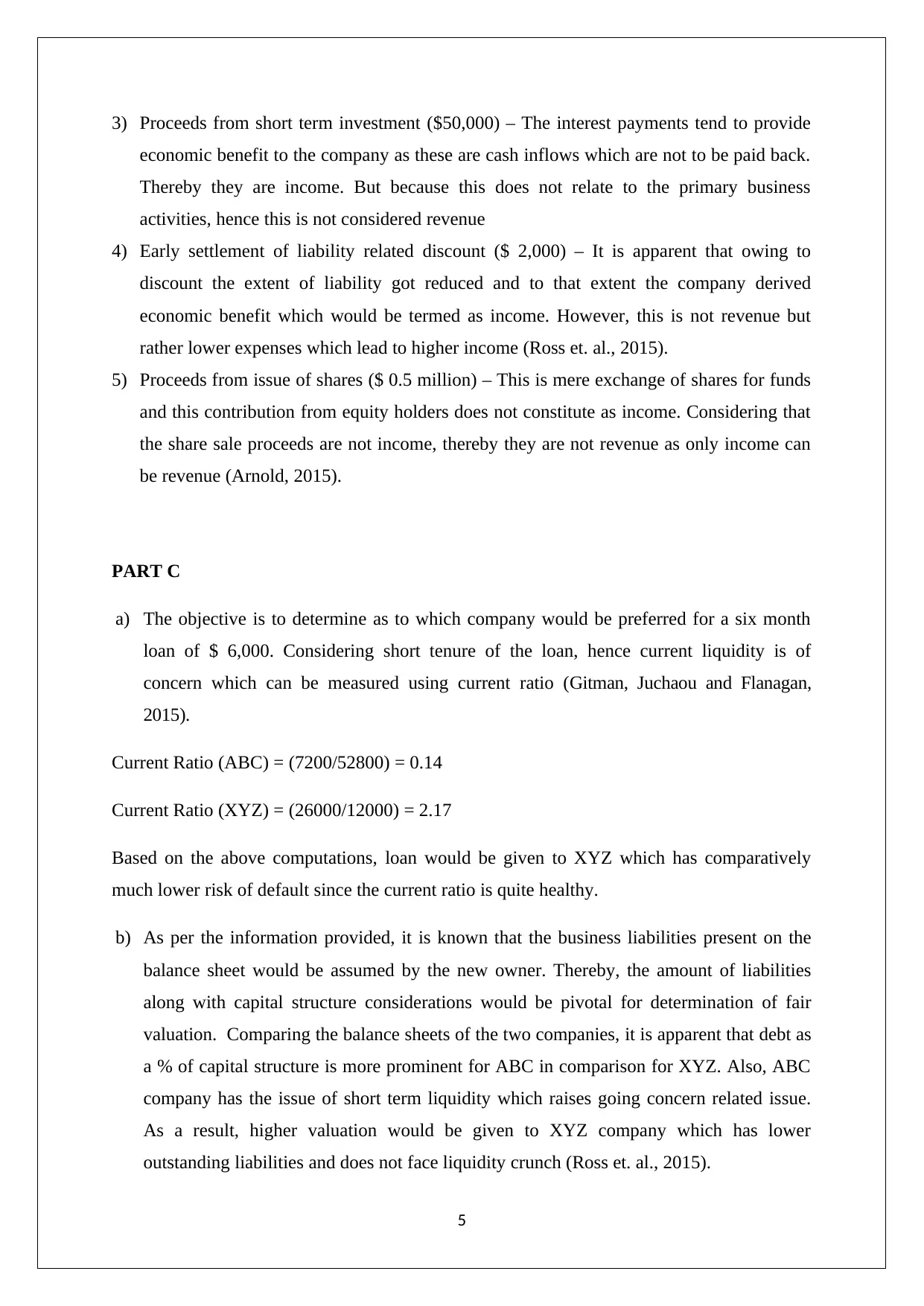

This assignment solution addresses key concepts in accounting for business, including financial statement analysis and the application of accounting standards. Part A focuses on calculating and interpreting financial ratios, such as the current ratio, quick ratio, accounts receivable turnover, and inventory turnover, to assess a company's short-term liquidity and operational efficiency. The analysis compares performance between 2018 and 2019 and benchmarks against industry averages. Part B examines the application of AASB 118, classifying various financial items like proceeds from software sales, downloads, and investments as either income or revenue. Part C uses financial ratios to determine the preferred company for a six-month loan, considering both liquidity and valuation based on debt and equity structure. The solution also discusses how changes in liability assumptions impact business valuation. The assignment references key accounting texts and standards to support its analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.