Accounting for Business - Financial Analysis Assignment

VerifiedAdded on 2020/05/28

|7

|1590

|64

Homework Assignment

AI Summary

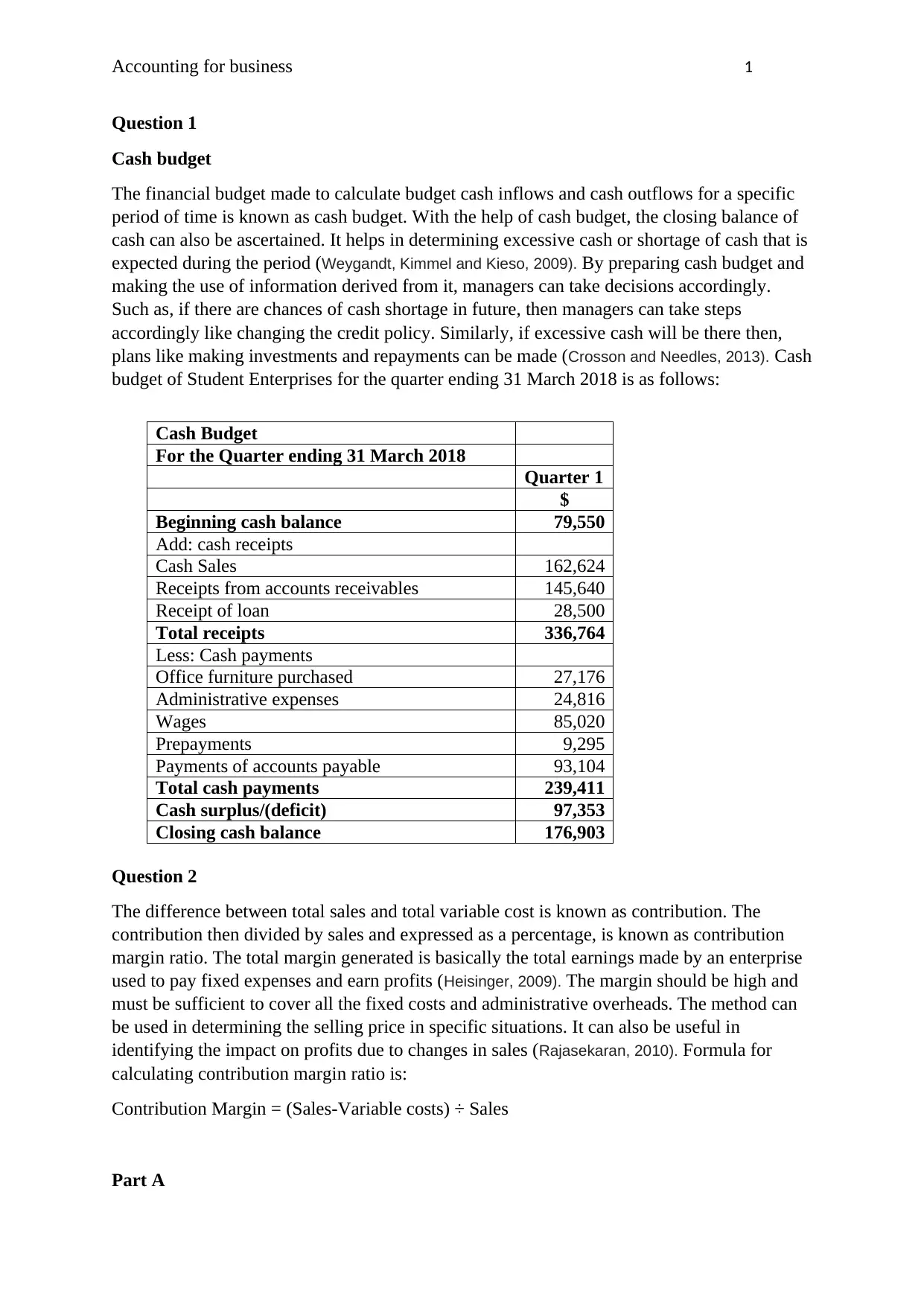

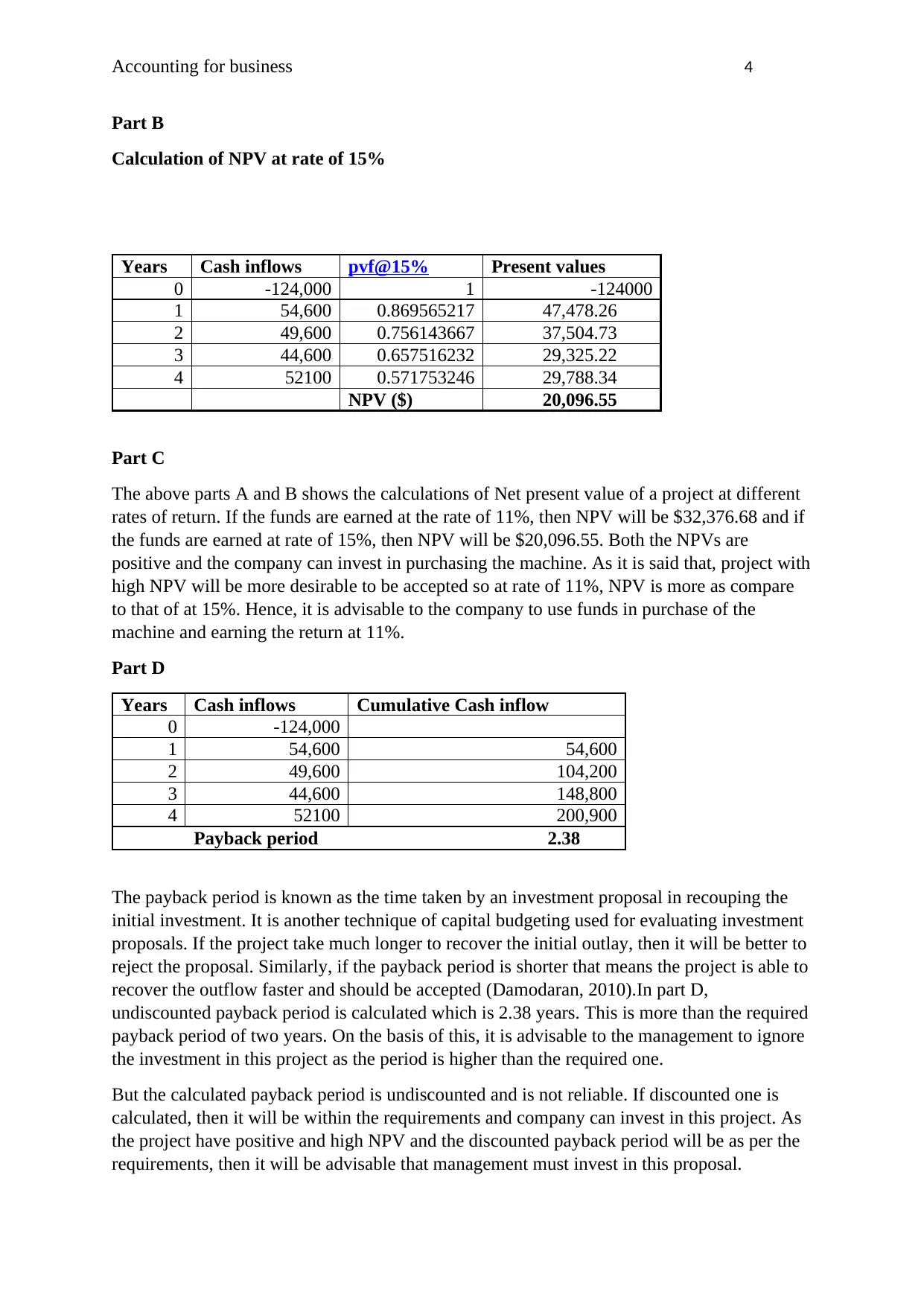

This accounting assignment solution covers several key financial concepts. Firstly, it presents a cash budget for Student Enterprises, detailing cash inflows and outflows to determine the closing cash balance. Secondly, it analyzes contribution margin ratios for printers and faxes, calculating break-even sales for the company and its product lines. Finally, the assignment explores the net present value (NPV) method, calculating NPV for a project at different rates of return (11% and 15%) and determining the payback period, providing a comprehensive overview of investment analysis techniques. The document includes references to relevant accounting literature, supporting the analysis and conclusions presented.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.