Accounting for Business

Added on 2023-03-23

6 Pages1206 Words37 Views

ACCOUNTING FOR BUSINESS

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

PART A

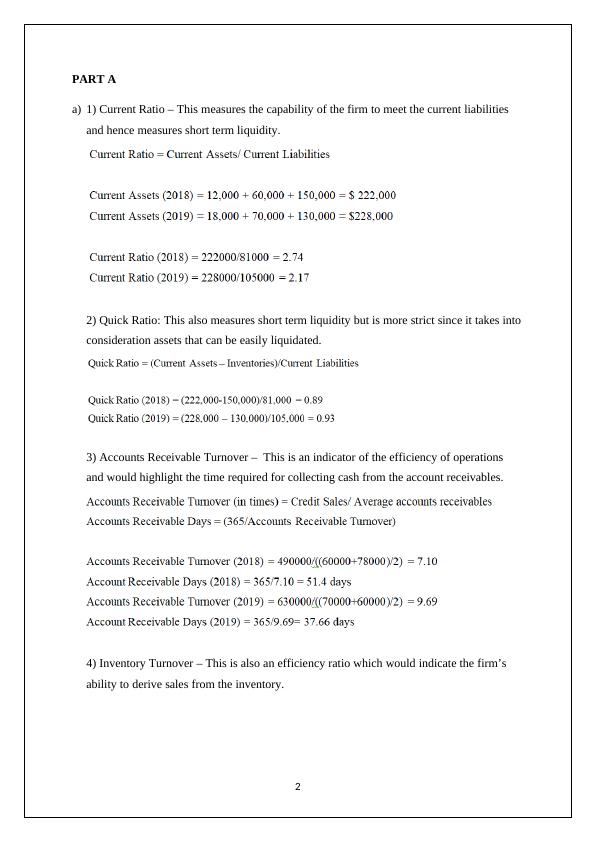

a) 1) Current Ratio – This measures the capability of the firm to meet the current liabilities

and hence measures short term liquidity.

2) Quick Ratio: This also measures short term liquidity but is more strict since it takes into

consideration assets that can be easily liquidated.

3) Accounts Receivable Turnover – This is an indicator of the efficiency of operations

and would highlight the time required for collecting cash from the account receivables.

4) Inventory Turnover – This is also an efficiency ratio which would indicate the firm’s

ability to derive sales from the inventory.

2

a) 1) Current Ratio – This measures the capability of the firm to meet the current liabilities

and hence measures short term liquidity.

2) Quick Ratio: This also measures short term liquidity but is more strict since it takes into

consideration assets that can be easily liquidated.

3) Accounts Receivable Turnover – This is an indicator of the efficiency of operations

and would highlight the time required for collecting cash from the account receivables.

4) Inventory Turnover – This is also an efficiency ratio which would indicate the firm’s

ability to derive sales from the inventory.

2

b) In the context of short term liquidity, the performance has shown a dip as the current ratio

for 2019 is lower than the value in 2018. Despite this, there is some improvement in quick

ratio in the current year which is positive. Even though the performance is lacklustre but

the current liquidity of the company is not an issue as both the ratios capturing short term

liquidity continue to remain robust (Brealey, Myers and Allen, 2014).

In context of operational efficiency, the performance of the company is significantly lower in

comparison with the industry average. The credit period as advertised by the company

amounts to only a 30 day period but the average collection period tends to exceed the 30 day

mark thereby indicating issues in recovery of cash from debtors. In the context of sales from

inventory, there has been a reduction in turnover period in 2019 which augers well for the

company. But the looming concern is that despite the improvement, it is still higher than

average of 101 days for the industry. As a result, the current cash cycle of company is higher

than peers leading to greater requirement of working capital (Damodaran, 2015).

PART B

In accordance with AASB 118, revenue is categorised as any income which arises on account

of ordinary business activities. Further, there are many revenues forms including royalties,

interest, sales, fees or dividends which may be derived by the reporting entity (AASB, 2014).

The cash flow stream indicated by the Green Apple company needs to be categorised as per

the above guideline.

3

for 2019 is lower than the value in 2018. Despite this, there is some improvement in quick

ratio in the current year which is positive. Even though the performance is lacklustre but

the current liquidity of the company is not an issue as both the ratios capturing short term

liquidity continue to remain robust (Brealey, Myers and Allen, 2014).

In context of operational efficiency, the performance of the company is significantly lower in

comparison with the industry average. The credit period as advertised by the company

amounts to only a 30 day period but the average collection period tends to exceed the 30 day

mark thereby indicating issues in recovery of cash from debtors. In the context of sales from

inventory, there has been a reduction in turnover period in 2019 which augers well for the

company. But the looming concern is that despite the improvement, it is still higher than

average of 101 days for the industry. As a result, the current cash cycle of company is higher

than peers leading to greater requirement of working capital (Damodaran, 2015).

PART B

In accordance with AASB 118, revenue is categorised as any income which arises on account

of ordinary business activities. Further, there are many revenues forms including royalties,

interest, sales, fees or dividends which may be derived by the reporting entity (AASB, 2014).

The cash flow stream indicated by the Green Apple company needs to be categorised as per

the above guideline.

3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting for Businesslg...

|7

|1323

|145

Accounting for Businesslg...

|7

|1174

|228

Accounting for Businesslg...

|7

|1245

|405

Accounting for Businesslg...

|7

|1120

|248

Accounting for Businesslg...

|6

|1184

|234

Accounting for Businesslg...

|6

|1264

|465